17h

Resistant maltodextrin is included in the 2004/5 Nutrient Profiling Model as it is classified as fibre because of its characteristics. So why is digestible maltodextrin omitted from both 2004/5 and 2018 NPMs - when it ought to be classified as 'sugar'?

1

61

Jun 13

All teams must revise sec models. Ai gives asymmetric advantage to black hats. Supply chain attacks just started and bring avalanches. We already know the weakest points, github and npms, but nothing is excluded really.

178

It's almost hysterical in a not funny way how many people who use Arch Linux are freaking out about compromised npms on the AUR. I'm not saying "you can't use Arch" but the stereotype is Arch users go the extra mile to "do it right" you can use scan tools AND check the code diffs

1

2

28

Jun 9

i really dont trust any 3rd party repo

they are constantly being hacked, and if that happens, their js would have full control of my user’s dashboard

we install zero sdks/npms here except the really needed ones (frameworks mainly)

1

111

It's National #VolunteersWeek could you become an NPMS volunteer like Alexandre? There are plenty of available squares waiting for new volunteers to monitor them! Head to our website to look for a square local to you. ow.ly/Sne850Z6xHc

3

3

109

Yeah, that and the fact that LLMs npm and npx all day every day, when npm and npx are getting pwned 24/7 with high severity and fast moving hacks, including hacked dependencies of such npms in the thousands.

2

206

Socket is great. I definitely recommend pinning your npms though, it's getting wild out there:

I do not alias npm/npx. They are blocked for Codex for supply chain security reasons.

Local dependency fetch/install goes through Socket-wrapped pnpm:

socket-pnpm install --frozen-lockfile

Adding packages also goes through Socket-wrapped pnpm:

socket-pnpm add --save-exact <package>

Existing local scripts run with pnpm:

pnpm run <script>

Verify the protected setup:

codex-protected-settings-verify

5

804

May 21

Yeah I don't think people celebrating this have had to deal with npms wall of 2FA lately

3

245

🙌Hands up if you spotted Alan Sumnall from @plantlife.loveplants & @AdamHenson on BBC Countryfile yesterday talking about the NPMS & praising the efforts of the survey volunteers nationwide! There are 5 NPMS plots on Adam's Farm, surveyed by long term volunteer Chris Millet.

1

1

8

202

Shouting CONGRATULATIONS to our NPMS Green Power team. They received FIRST place in the intermediate 2026 Stock Race. We are so proud of their hard work and accomplishments. 🏎️🥇🏁 @suptking @JMCSSInnovation @ChontelBri30557

3

11

162

May 16

Love the caring that your NPMS family shows to the scholars, faculty, and staff!😍

3

21

May 15

The transparency is awesome. I think there are lessons for the entire industry here, and not just those shipping npms.

2

878

May 13

$SMR ---- $SMR delivers reliable, carbon‑free power solutions for AI data centers, industrial operations, and electric grids, and is currently the only U.S. SMR player with an NRC‑approved design.

ENTRA1 Energy, its exclusive global strategic partner, is advancing PPA negotiations with TVA targeting America’s largest‑ever nuclear deployment of up to 6 GW of NuScale SMR capacity.

For Romania’s RoPower project, shareholders have approved the next phase to deploy six NuScale Power Modules (NPMs) at a former coal‑fired plant site.

Framatome, its supply‑chain partner, is expanding across the U.S. and Europe to speed up fuel delivery, with NPM components now in production.

Additional Catalysts: Partnerships with Ebara Elliott Energy to explore petrochemical plant applications; nuclear renaissance policy tailwinds fueled by surging AI power demand; and NRC design approval strengthening its competitive edge.

Overall Drivers: AI data center power shortages combined with favorable nuclear‑energy policies focused on carbon neutrality and supply‑chain security. NuScale is the commercialization leader in the SMR space despite being in a pre‑revenue stage.

8

2,626

In-field training. 12th June Ranscombe Farm Reserve, Kent: Intro to NPMS & survey methods. Learn about NPMS recording & how to get started. We will walk cover practicalities of plot set up & recording while enjoying this important plant area. More info ow.ly/pCax50YXwHx

2

53

May 12

fuck NPMs I can write my own software without the bloat and Niko you know I am a fan of pure functions not bullshit abstracted classes --> control makes me happy

2

11

May 7

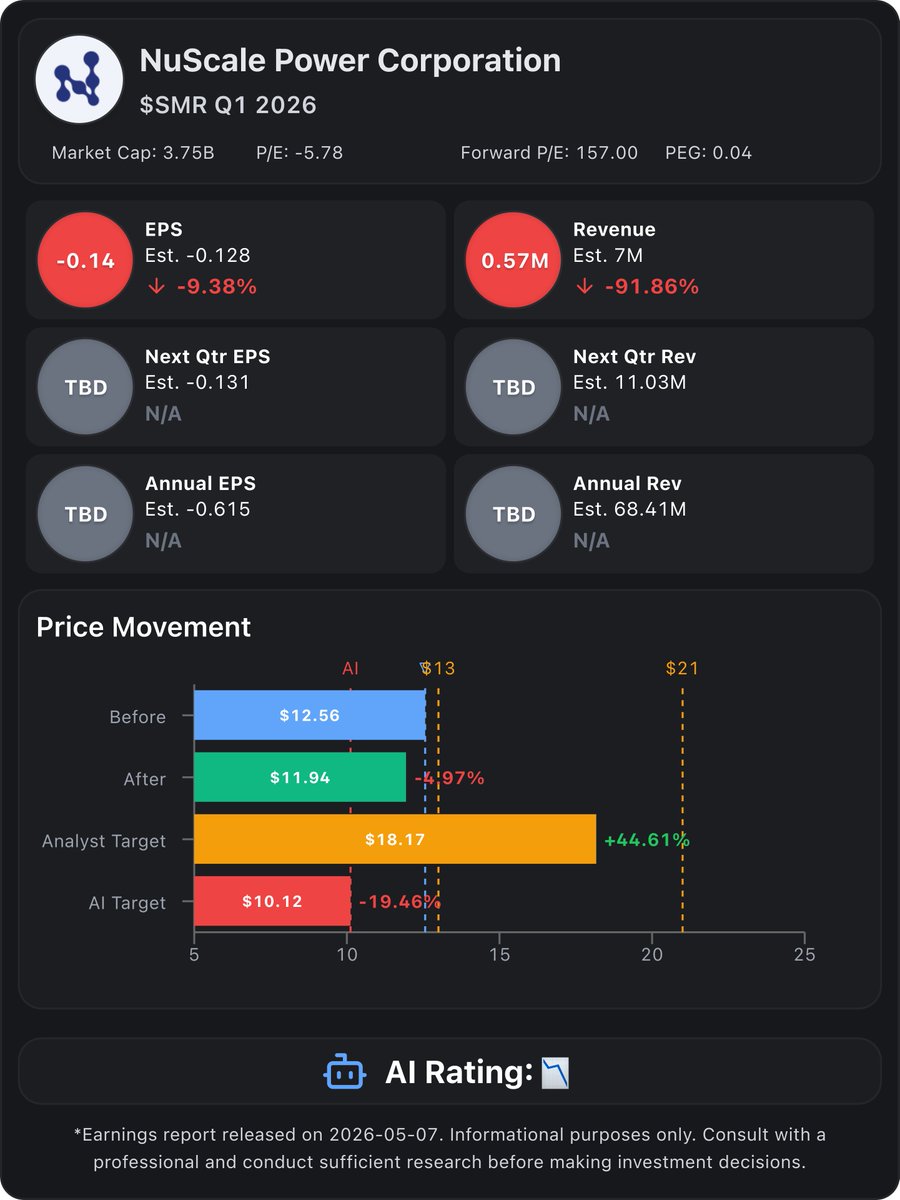

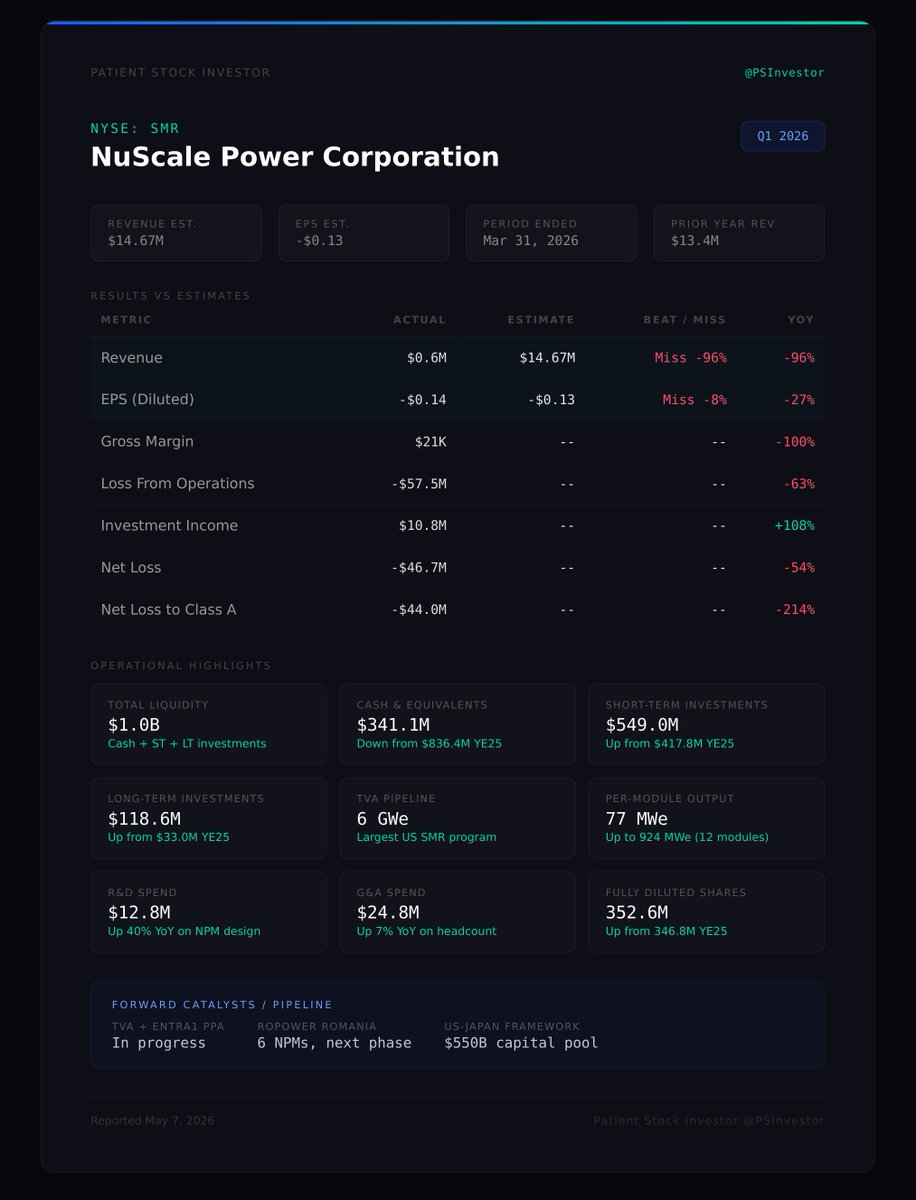

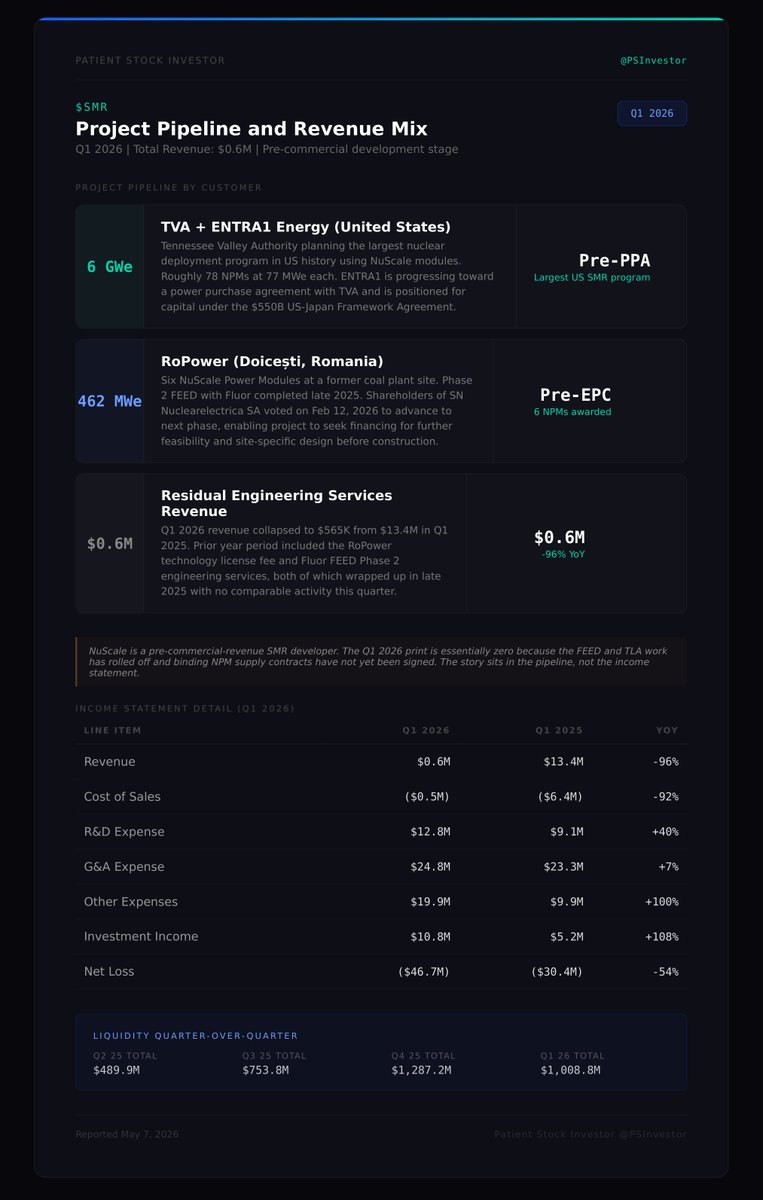

$SMR Q1 2026 earnings: A Billion-Dollar Fortress Awaiting a Spark

NuScale has successfully fortified its balance sheet, boasting $1.0 billion in liquidity, but its income statement is essentially bare. Q1 2026 revenue collapsed to near-zero as the RoPower Phase 2 engineering work wrapped up in late 2025. With no new major service contracts immediately replacing it, idle engineering personnel drove a sharp acceleration in internal operating expenses. NuScale remains the only SMR provider with NRC design approval, giving it a massive technological moat. However, the entire investment thesis now hinges on its exclusive partner, ENTRA1, executing a binding Power Purchase Agreement (PPA) with the Tennessee Valley Authority (TVA). Until that 'black box' partnership delivers a signed contract, the company is in an expensive holding pattern.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐔𝐧𝐫𝐢𝐯𝐚𝐥𝐞𝐝 𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲 𝐑𝐮𝐧𝐰𝐚𝐲 — With $1.0 billion in cash, short-term, and long-term investments, NuScale has effectively removed existential financial risk for the near future. They can comfortably fund operations while awaiting utility and hyperscaler deployment timelines.

• 𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐚𝐧𝐝 𝐒𝐮𝐩𝐩𝐥𝐲 𝐂𝐡𝐚𝐢𝐧 𝐌𝐨𝐚𝐭 — NuScale remains the only SMR technology provider with U. S. NRC approval. An expanded Framatome fuel partnership and ongoing module production at Doosan validate that this is not a 'paper reactor'—it is ready for commercial scaling.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐎𝐩𝐚𝐪𝐮𝐞 𝐏𝐚𝐫𝐭𝐧𝐞𝐫𝐬𝐡𝐢𝐩 𝐌𝐨𝐝𝐞𝐥 — NuScale relies entirely on ENTRA1 for financing and project development. Management's historical refusal to provide transparency into ENTRA1's financials or specific gating factors for the TVA deal creates significant execution risk.

• 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐕𝐨𝐢𝐝 & 𝐒𝐮𝐫𝐠𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧 — With revenue dropping 96% YoY to just $0.565M and operating loss widening to $57.5M, NuScale is burning substantial capital. Until a firm equipment order is signed, investors are financing an idle engineering workforce.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The asset-light, partner-led model is theoretically brilliant, and $1 billion in liquidity is a phenomenal achievement. But an SMR company trading at a premium valuation needs to show commercial execution, not just balance sheet padding. The clock is ticking on the TVA PPA.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 𝐭𝐨 𝐙𝐞𝐫𝐨 [NEW]

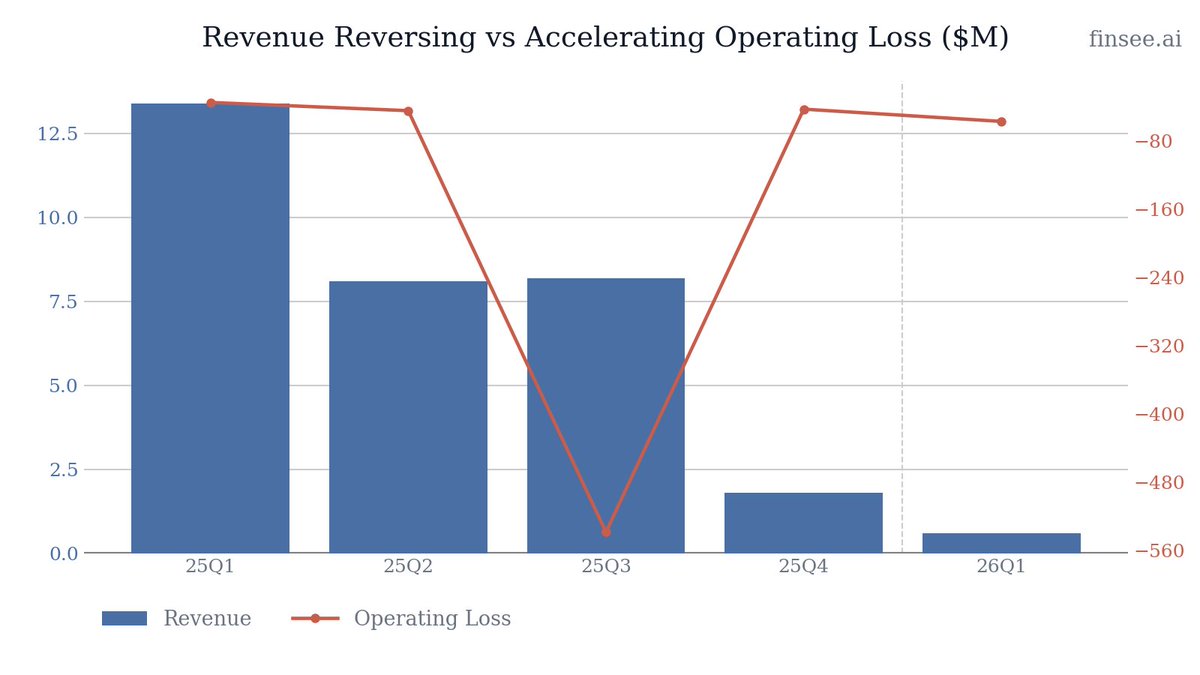

Revenue decelerated violently and practically reversed, dropping $12.8 million YoY to just $565,000. This was entirely expected internally, as Fluor's FEED Phase 2 engineering services for the RoPower project concluded in late 2025. However, it exposes the reality that NuScale lacks a diversified, recurring revenue stream bridging the gap between early engineering studies and actual SMR module delivery.

🔴 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐎𝐯𝐞𝐫𝐡𝐞𝐚𝐝 𝐟𝐫𝐨𝐦 𝐔𝐧𝐝𝐞𝐫𝐮𝐭𝐢𝐥𝐢𝐳𝐞𝐝 𝐄𝐧𝐠𝐢𝐧𝐞𝐞𝐫𝐬 [NEW]

With fewer commercial projects to bill against, overhead expenses are accelerating. 'Other expenses' surged by $10.0 million YoY to $19.9 million. Management explicitly attributed this to engineers and project personnel no longer being allocated to cost of sales, as well as higher compensation costs to support 'supply chain readiness.' This represents a structural cash burn drag until ENTRA1 secures a firm order.

🟢 𝐓𝐡𝐞 𝐓𝐕𝐀 𝟔 𝐆𝐢𝐠𝐚𝐰𝐚𝐭𝐭 𝐂𝐚𝐭𝐚𝐥𝐲𝐬𝐭

The entire growth story hinges on the exclusive strategic partner, ENTRA1 Energy, successfully navigating the Tennessee Valley Authority (TVA) through a 6-gigawatt deployment program. If executed, this would be the largest nuclear deployment in U. S. history (equivalent to ~72 NuScale modules). The lack of explicit timeline updates in this quarter's release indicates complex, ongoing negotiations behind closed doors.

⚪ 𝐑𝐨𝐏𝐨𝐰𝐞𝐫 𝐏𝐫𝐨𝐣𝐞𝐜𝐭 𝐈𝐧𝐜𝐡𝐞𝐬 𝐅𝐨𝐫𝐰𝐚𝐫𝐝 [NEW]

International momentum remains stable. SN Nuclearelectrica SA shareholders approved proceeding with the next phase of the RoPower project at a former coal site in Doicești, Romania. This 6-module plant acts as a critical international proof-of-concept, though the timeline to Final Investment Decision (FID) has historically been pushed back.

🟢 𝐒𝐞𝐜𝐮𝐫𝐢𝐧𝐠 𝐭𝐡𝐞 𝐅𝐮𝐞𝐥 𝐒𝐮𝐩𝐩𝐥𝐲 𝐂𝐡𝐚𝐢𝐧 [NEW]

NuScale expanded its global supply chain partnership with Framatome across the U. S. and Europe to support accelerated fuel delivery. Unlike competitors relying on High-Assay Low-Enriched Uranium (HALEU)—which suffers from geopolitical supply constraints—NuScale's use of standard enriched uranium allows it to leverage established giants like Framatome, significantly de-risking commercial deployment.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐓𝐨𝐭𝐚𝐥 𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲: $1.0 billion

Stable and formidable. Driven by a massive $475M ATM raise in late 2025 and rising investment income ($10.8M in Q1 2026, up $5.6M YoY). NuScale is sitting on $341.1M in cash, $549.0M in short-term investments, and $118.6M in long-term investments. This balance sheet essentially inoculates the company against near-term macro shocks or standard FOAK (First-Of-A-Kind) delays.

𝐑&𝐃 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬: $12.8 million

Accelerating. Up $3.7M YoY. With the May 2025 SDA approval completed, regulatory costs fell by $1.9M. However, this was more than offset by a $5.7M increase in activities advancing the technological readiness and design maturity of NPM components for actual commercial manufacturing.

𝐆&𝐀 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬: $24.8 million

Stable. Up slightly by $1.6M YoY. Increased headcount compensation and organizational costs were offset by a $1.1M drop in legal and accounting fees, as the company has normalized its operations post-transition to a large accelerated filer.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐚𝐥 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞: None provided

Management continues to deliberately withhold traditional quantitative revenue or earnings guidance, reflecting the binary and lumpy nature of nuclear power plant contracts.

𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐢𝐚𝐥 𝐃𝐞𝐥𝐢𝐯𝐞𝐫𝐲 𝐓𝐚𝐫𝐠𝐞𝐭𝐬: TVA (Up to 6 GW) & RoPower (6 NPMs)

Operational guidance remains focused on advancing the planning phase for TVA and moving into the pre-EPC phase for RoPower. Investors are entirely blind to when these milestones will translate into actual cash inflows.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐄𝐧𝐠𝐢𝐧𝐞𝐞𝐫 𝐔𝐭𝐢𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐚𝐧𝐝 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧

With the RoPower FEED Phase 2 work concluded, 'Other Expenses' surged due to unallocated engineers. What is the normalized quarterly cash burn we should expect going forward until a major firm order is signed?

𝐓𝐕𝐀 𝐏𝐏𝐀 𝐆𝐚𝐭𝐢𝐧𝐠 𝐅𝐚𝐜𝐭𝐨𝐫𝐬

Acknowledging the NDAs surrounding ENTRA1, what are the technical or regulatory gating factors holding back a firm, binding Power Purchase Agreement with the TVA?

𝐅𝐫𝐚𝐦𝐚𝐭𝐨𝐦𝐞 𝐏𝐚𝐫𝐭𝐧𝐞𝐫𝐬𝐡𝐢𝐩 𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐚𝐥𝐬

Regarding the expanded Framatome fuel delivery partnership, does this require any upfront capital commitments or milestone payments from NuScale, similar to the ENTRA1 structure?

1

4

1,575

May 7

💡 NuScale Power Corporation $SMR Q1 2026決算 2026-05-07

💰 今四半期業績

- 🔴 EPS:$-0.14 (予想$-0.128)

- 🔴 売上高:$0.57M (予想$7M)

📊 重要指標

- 🟢 流動性・資本資源:$1.0B (現金・現金同等物・短期/長期投資合計)

- 🔴 粗利益:$0.02M (前年同期: $7.0M, YoY-99.7%)

- 🔴 営業損失:-$57.52M (前年同期: -$35.33M, YoY悪化62.8%)

- ⚫️ 研究開発費:$12.81M (前年同期: $9.13M, YoY 40.3%)

- 🟢 投資収益:$10.84M (前年同期: $5.21M, YoY 107.9%)

- 🔴 営業キャッシュフロー:-$314.68M (前年同期: -$22.79M)

- 🔴 Fluor Corp インサイダー売却:4月に約39.9M株を$11.17-$12.07で売却 (約$460M相当)

📍決算内容の注目ポイント

- ENTRA1 EnergyがTennessee Valley Authority (TVA)と協力し、最大6GWのNuScale SMR容量を含む米国史上最大規模の原子力発電導入プログラムの計画を推進中

- SN Nuclearelectrica SAの株主がRomaniaのDoicesti旧石炭火力発電所跡地に6基のNuScale Power Modules (NPMs)を展開するRoPowerプロジェクトの次フェーズ進行を承認

- NuScaleとFramatomeが米国・欧州にわたるグローバルサプライチェーンパートナーシップを拡大し、燃料供給の加速を支援

- 四半期末時点で$1Bの流動性を維持し、プロジェクト開発・展開に向けた強固な資金基盤を確保

- 親会社Fluor Corpが4月に大規模なインサイダー売却(約39.9M株、約$460M相当)を実施

🤵♂️CEO (John Hopkins) コメント

「信頼性が高くカーボンフリーな電力への需要はかつてないほど高まっており、NuScaleはU.S. Nuclear Regulatory Commission (NRC)の設計承認を取得した唯一のSMR技術プロバイダーであり、確立されたサプライチェーンと商用利用のために現在製造中のNPMコンポーネントを有しています。第1四半期を$1Bの流動性で終え、Framatomeとのサプライチェーンパートナーシップを拡大し、TVAプログラムの継続的な進展を確認しました。この重要な局面が求めるインフラを構築しています。」

🔍 主要ファンダメンタルズ指標

- 時価総額: 3.75B

- PER: -5.78

- Forward PER: 157.00

- PEG: 0.04

🎯市場評価

- 株価 (発表前): 📉$12.565 (-7.06%)

- 株価 (発表後): 📉$11.94 (-4.97%)

- 決算前アナリスト目標株価: $18.17 ($21 ~ $13) D

- 決算総合サプライズ率 (AI推定): 😫-31.25%

- 決算後目標株価 (AI推定): $10.12

🤖 決算まとめるくん(AI)コメント

「NuScale Power Corporationの2026年度Q1決算は、売上高・EPSともにアナリスト予想を大幅に下回る厳しい結果となりました。

売上高は$0.57Mと前年同期の$13.38Mから95.8%減少しており、これは2025年Q1に計上されたRoPowerプロジェクト向けテクノロジーライセンス契約(TLA)収入およびFluorのFEED Phase 2エンジニアリングサービス収入が2025年末に完了し、2026年Q1には同等の商業活動がなかったことが主因です。EPSも-$0.14と予想の-$0.128を下回りました。

営業損失は-$57.52Mと前年同期の-$35.33Mから62.8%悪化しており、R&D費用の増加(NPMコンポーネントの技術成熟度向上に伴う$5.7Mの追加コスト)やサプライチェーン準備・将来の商業プロジェクト支援のための人員増強に起因するその他費用の$10.0M増が圧迫要因です。一方、投資収益は$10.84Mと前年同期比で倍増しており、$1Bの強固な流動性ポジションが寄与しています。

注目すべきは、営業キャッシュフローが-$314.68Mと急激に悪化した点です。これは主に買掛金・未払費用の$264.2M減少によるもので、一時的な運転資本変動と考えられますが、キャッシュバーン率の高さは懸念材料です。

ファンダメンタルズ面では、Altman Z-Scoreが5.83と財務破綻リスクは低いものの、Piotroskiスコアは0と収益性・効率性指標が極めて低水準です。P/S比率118.97倍という高いバリュエーションは、将来の商業化への期待を大きく織り込んでいます。

親会社Fluor Corpによる4月の大規模株式売却(約$460M相当)は、市場のセンチメントに対する重大なネガティブシグナルです。TVAプログラムやRoPowerプロジェクトの進展は中長期的な成長ドライバーですが、実際の収益貢献までには相当の時間を要する見通しであり、短期的には収益の谷間が続くことが予想されます。 評価は📉ポヨ」

🏢 NuScale Power Corporation 概要

- セクター: 公益事業

- 特徴: NRC承認済みの小型モジュール炉(SMR)技術を開発・提供する唯一の企業。77MWeの出力を持つNuScale Power Moduleを基盤に、最大924MWeまでスケーラブルな原子力発電ソリューションを展開

🤘情報提供

Stock Slayer : stock-slayer.com/?s=U01SLTIw…

4

4

57

12,197

May 7

$SMR NuScale Power Q1 2026 earnings are out.

This is a pipeline-and-liquidity story, not an income statement story. Revenue is essentially zero because the prior FEED and license work rolled off and the next wave of binding contracts has not yet been signed. The franchise lives in the regulatory moat, the NRC-approved design, and the partnerships behind the next 6 GW of US capacity.

Key catalysts from the report:

- TVA and ENTRA1 Energy continue planning the largest nuclear power deployment program in US history, up to 6 gigawatts of NuScale $SMR capacity

- Shareholders of SN Nuclearelectrica SA approved advancing the RoPower project in Doicești, Romania, with 6 NPMs at a former coal plant site

- $SMR and Framatome expanded their global supply chain partnership across the US and Europe to support accelerated fuel delivery

- ENTRA1 is positioned to receive investment capital from the $550 billion US-Japan Framework Agreement to fund baseload power infrastructure

John Hopkins, $SMR President and Chief Executive Officer:

'The demand for reliable, carbon-free power has never been greater, and NuScale is the only SMR technology provider with a U.S. Nuclear Regulatory Commission approved design, an established supply chain and NPM components currently in production for commercial use to meet this essential need.'

John Hopkins, $SMR President and Chief Executive Officer:

'We ended the first quarter with $1 billion in liquidity, expanded our supply chain partnership with Framatome and saw continued progress on the TVA program. We are building the infrastructure that this pivotal moment requires.'

Revenue mix is concentrated in development-stage activity. The TVA-ENTRA1 program is the headline future contract, RoPower is the live international deployment, and residual engineering services are winding down as Phase 2 FEED with Fluor wraps. Component manufacturing for commercial use has begun across the supplier ecosystem with Doosan, Framatome, Honeywell, IHI, Curtiss-Wright, and others.

Inflection point: $SMR is transitioning from a study-and-license revenue model to a module-supply model, where the next leg of revenue depends on TVA pre-PPA progress and RoPower pre-EPC financing closing within the next several quarters.

My take is that this is the kind of quarter where the screen looks ugly but the underlying setup keeps improving. A billion in liquidity buys patience, and patience is the whole game when you are years ahead on regulatory and supply chain.

6

1,662

Mr. Nasser Bourita, Minister of Foreign Affairs & African Cooperation, & Ms @AminaBouayach, Chairperson of the Network of African #NPMs against #torture signed an agreement establishing the HQ of the Network in Morocco

reaffirming a shared commitment to promoting HR across Africa

3

10

2,504