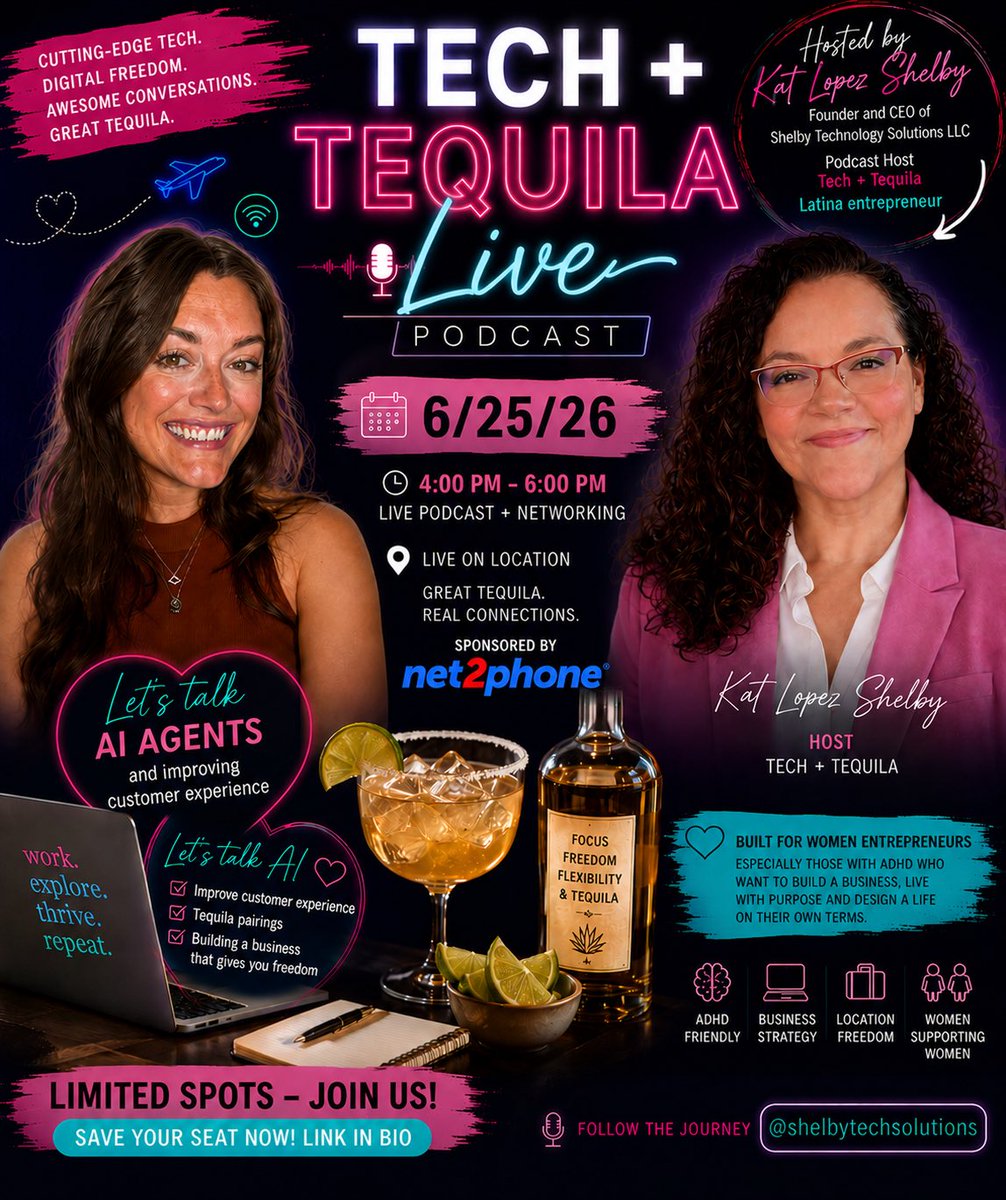

What if your next employee never slept, never missed a lead, and helped create an incredible customer experience 24/7?

That’s exactly why business owners are talking about AI Agents.

Join us for a special LIVE edition of 🎙️ Tech Tequila as we explore how AI Agents are helping businesses automate conversations, improve customer experience, and create more freedom for entrepreneurs.

✨ Let’s Talk AI Agents

✨ Improving Customer Experience

✨ Tequila Pairings 🍹

✨ Building a Business That Gives You Freedom

I’m excited to be joined by special guest Maddie Webster as we share real-world AI strategies that businesses can start implementing today.

📅 June 25, 2026

📍 Austin, Texas

⏰ 4:00 PM – 6:00 PM

🎙️ Live Podcast Networking

🍹 Great Tequila

🤝 Connections Community

Sponsored by @net2phone

⚠️ Limited seating available.

Whether you’re AI curious, exploring AI Agents, or ready to take your customer experience to the next level, this conversation is for you.

👇 Comment “AI” if you’re joining us!

🔗 Register now and secure your spot.

#TechAndTequila #AIAgents #CustomerExperience #ArtificialIntelligence #BusinessAutomation #BusinessGrowth #SmallBusiness #WomenInBusiness #LatinaEntrepreneur #AustinTX #NetworkingEvent #TechPodcast #YourDigitalBliss #yourdigitalbliss #ShelbyTechnologySolutions #Net2Phone #EntrepreneurLi

12

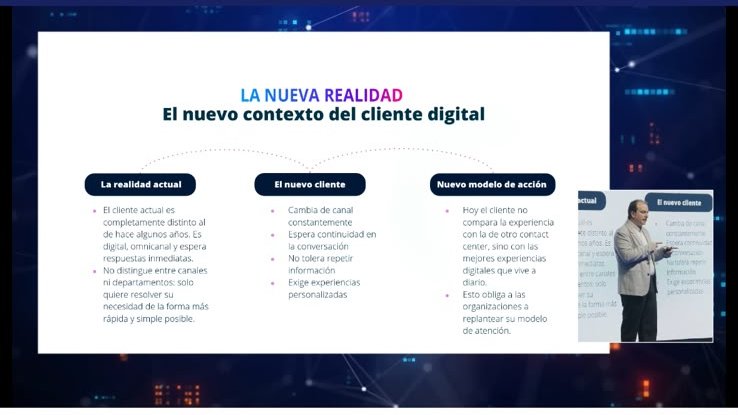

¡En vivo desde el Salón Olmeca IV! 🔴 David Modiano de net2phone está en el escenario explicando la evolución hacia los Contact Centers Híbridos.

El cliente digital no espera: es omnicanal, exige respuestas inmediatas y experiencias personalizadas. ¿Tu negocio ya se adaptó? ⚡

22

#AHORA "El nuevo modelo de atención al cliente: Contact Centers Híbridos"

David Modiano

(México)

Director Comercial, net2phone

#CX #ContactCenterHíbrido #DatosEstratégicos

4

57

Jun 4

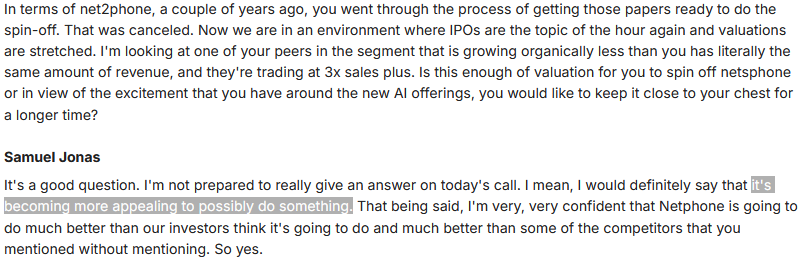

$IDT not only published great Q3 2026 results.

✅They announced the completion the acquisition of a majority stake on a tuck-in to fix their structural problem with advertisement.

🛫The CEO said this about the potential spin-off of Net2Phone

3

1

6

1,045

Jun 3

$IDT Q3 2026 earnings: Mix Shift Masters: High-Margin Segments Now Drive the Bottom Line

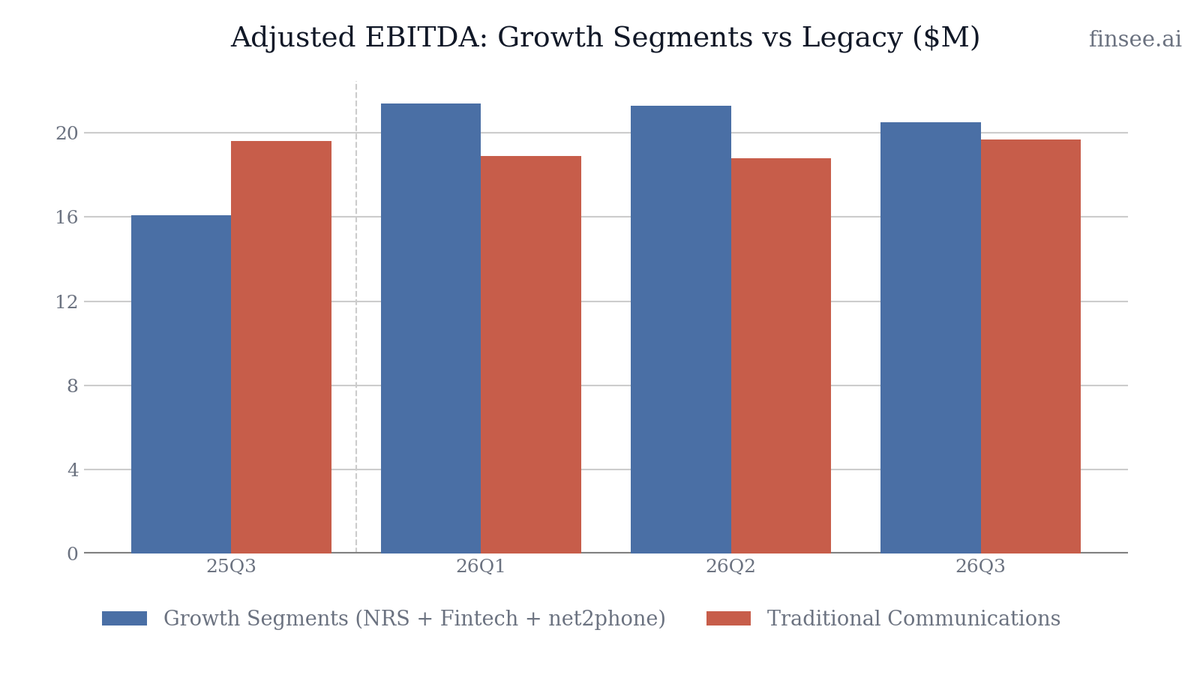

IDT delivered a textbook example of business transformation in Q3. While consolidated revenue grew a modest 5% YoY, gross profit jumped 9% and Adjusted EBITDA expanded 13% as the company's revenue mix continues shifting toward its three high-growth, high-margin engines (NRS, Fintech, and net2phone). For the first time, these three segments combined to consistently generate more Adjusted EBITDA than the legacy Traditional Communications business. This operational leverage gave management the confidence to raise FY26 Adjusted EBITDA guidance to $150-$152 million.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐫𝐠𝐢𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐢𝐬 𝐒𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 — Gross margin expanded 170 bps YoY to 38.8%. This is not a one-time benefit but a permanent structural improvement as higher-margin software and fintech revenues replace lower-margin telecom revenues.

• 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 — Net2phone operating income grew 76% on just 11% revenue growth, proving that past investments in product architecture (CCaaS, AI) are now scaling rapidly without requiring proportional SG&A increases.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐍𝐑𝐒 𝐀𝐝𝐯𝐞𝐫𝐭𝐢𝐬𝐢𝐧𝐠 𝐕𝐨𝐥𝐚𝐭𝐢𝐥𝐢𝐭𝐲 — Advertising & Data revenue at NRS fell 3% YoY and 37% sequentially from Q2. As IDT scales this segment, its exposure to broader digital ad market fluctuations creates quarterly lumpiness.

• 𝐓𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬 — The legacy business saw gross margins compress 130 bps to 19.4%, shrinking gross profit by 7% YoY. This cash cow is stable for now, but margin decay requires monitoring.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. Management is executing flawlessly on its transition strategy. Top-line numbers mask the underlying earnings power of the NRS and Fintech platforms, which are generating heavy cash and justifying an upward revision to full-year guidance.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐍𝐑𝐒 𝐏𝐫𝐞𝐦𝐢𝐮𝐦 𝐒𝐞𝐫𝐯𝐢𝐜𝐞𝐬 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠

NRS recurring revenue grew 22% YoY, led by a 31% surge in Merchant Services and a 17% increase in SaaS Fees. This pushed monthly average recurring revenue per terminal up 10% YoY to $307. The company's strategy to move beyond basic POS hardware into integrated payment processing and software is succeeding, increasing both stickiness and unit economics.

🟢 𝐁𝐎𝐒𝐒 𝐌𝐨𝐧𝐞𝐲 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐌𝐢𝐠𝐫𝐚𝐭𝐢𝐨𝐧

The Fintech segment continues to benefit from a channel shift. Digital channel revenue grew 27% YoY to $31.0 million, while the legacy retail channel shrank 13%. This digital dominance (now over 85% of remittance volume) directly boosted Fintech gross margins by 430 basis points to 62.8%, driving a 30% increase in segment Adjusted EBITDA.

🟢 𝐀𝐈 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 & 𝐂𝐂𝐚𝐚𝐒 𝐔𝐩𝐥𝐢𝐟𝐭 𝐚𝐭 𝐧𝐞𝐭𝟐𝐩𝐡𝐨𝐧𝐞 [NEW]

Management explicitly called out Contact Center as a Service (CCaaS) and AI integration (like the new 'Integrate by net2phone' no-code tool) as catalysts. Subscription revenue grew 12% against only a 6% increase in seats, indicating strong pricing power and successful upselling of higher-tier AI and CCaaS solutions.

⚪ 𝐌𝐚𝐜𝐫𝐨 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬: 𝐅𝐞𝐝𝐞𝐫𝐚𝐥 𝐑𝐞𝐦𝐢𝐭𝐭𝐚𝐧𝐜𝐞 𝐓𝐚𝐱

The new federal remittance tax implemented in January 2026 (fiscal Q2) is acting as a catalyst for IDT's digital transition. Because the tax primarily impacts cash-based transfers at physical retailers, price-sensitive consumers are accelerating their migration to IDT's BOSS Money digital app, a trend evident in the 20% sequential growth of digital transactions.

🔴 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐓𝐢𝐦𝐢𝐧𝐠 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐒𝐭𝐚𝐛𝐥𝐞 𝐆𝐞𝐧𝐞𝐫𝐚𝐭𝐨𝐫 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞

Management heavily promotes its resilient cash generation, but GAAP net cash provided by operations plummeted from $75.7M in 25Q3 to just $18.5M in 26Q3. Even after adjusting for customer deposits, operating cash flow dropped significantly. Management blames working capital timing (the quarter ended on a Thursday, requiring peak weekend prepaid funding for BOSS Money). While plausible, it highlights the intense, volatile working capital requirements of the scaling Fintech business.

🔴 𝐍𝐑𝐒 𝐀𝐝𝐯𝐞𝐫𝐭𝐢𝐬𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 [NEW]

Advertising & Data revenue at NRS was a glaring weak spot, dropping to $5.7M—a 3% YoY decline and a sharp drop from $9.0M in the prior quarter. IDT had previously restricted a major programmatic partner to manage credit risk, but the inability to fully backfill this demand or maintain sequential growth points to vulnerability in the retail ad-network model.

🔴 𝐓𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧

While Traditional Communications Adjusted EBITDA was stable, gross profit fell 7% YoY and gross margin compressed by 130 basis points to 19.4%. Revenue in BOSS Revolution specifically fell 16% YoY. Management has cut SG&A by 13% to protect EBITDA, but they cannot outrun gross profit deterioration indefinitely.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐅𝐢𝐧𝐭𝐞𝐜𝐡 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧: 62.8%

Accelerating. Up sharply from 58.5% a year ago and 60.6% in the prior quarter. This proves the economic superiority of digital remittances over cash-based retail agents.

𝐍𝐑𝐒 𝐀𝐜𝐭𝐢𝐯𝐞 𝐏𝐎𝐒 𝐓𝐞𝐫𝐦𝐢𝐧𝐚𝐥𝐬: 39,300

Stable. Up 10% YoY, adding 400 net terminals sequentially. The growth is solid, but the company's real victory is extracting more SaaS and payment revenue out of the existing base.

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐎𝐯𝐞𝐫𝐡𝐞𝐚𝐝: $3.2 million

Increasing. Up 22% from $2.7 million a year ago, driven primarily by higher stock-based compensation. While manageable given the broader growth, overhead scale needs to be kept in check.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐂𝐨𝐧𝐬𝐨𝐥𝐢𝐝𝐚𝐭𝐞𝐝 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $150 - $152 million

Accelerating vs prior expectations. Raised from previous guidance of $147-$149 million. The midpoint ($151 million) implies a 15% increase from FY25's $131.7 million. This signals management's confidence that the margin expansion in NRS and net2phone will continue to outpace the slow decline of the Traditional segment.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐍𝐑𝐒 𝐀𝐝𝐯𝐞𝐫𝐭𝐢𝐬𝐢𝐧𝐠 𝐅𝐥𝐨𝐨𝐫

NRS Advertising & Data revenue dropped sharply from $9.0M in Q2 to $5.7M in Q3. Is this strictly seasonal, a continuation of the programmatic partner reduction mentioned in prior quarters, or a broader softening in retail ad demand?

𝐌&𝐀 𝐯𝐬 𝐁𝐮𝐲𝐛𝐚𝐜𝐤𝐬 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲

With the Traditional segment still generating significant cash and the Straight Path litigation resolved, how is the $251 million cash pile being prioritized between opportunistic buybacks and the previously mentioned NRS adjacent-market acquisitions?

𝐓𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐌𝐚𝐫𝐠𝐢𝐧 𝐅𝐥𝐨𝐨𝐫

Traditional Communications gross margin compressed 130 bps YoY. While SG&A cuts protected EBITDA this quarter, what is the long-term margin floor for this business before it requires structural changes?

3

4

939

Feb 19

$IDT - net2phone Launches Integrated Communications for Hospitality Providersnet2phone’s Powerful Hospitality Solution Integrates with Most Popular Property Management Systems .

471

El Customer Experience Summit 2026 ya suma patrocinadores que apuestan por el crecimiento del sector.

Desde BPrO reconocemos a Broadvoice GoContact y net2phone como Platinum.

Si tu empresa quiere visibilizar su propuesta y ser parte de este encuentro de la industria, este es el momento de sumarse.

@broadvoice | @GoContactCloud | @net2phone_co | @anakarinaqa

1

2

77

7 Dec 2025

$IDT currently offers one of its best risk-adjusted entry points after:

⚙️ Successfully growing NRS into a inflation-protected, high-recurrence and high-margin cash generating machine.

🔒 Showing remarkable strength in BOSS Money prior to last quarter's one-off.

📈⏳Setting Net2Phone up for another 5-year run of DD growth.

🛡️ Keeping the cash generation of the Traditional segment stable, even as the BOSS Revolution segment rapidly dilutes itself.

The direct link to my Q1 FY26 update is in the bio.

1

2

15

3,291

4 Dec 2025

$IDT FY26 EBITDA guide $141M incl. ~$72M from legacy. Value legacy at 7× = ~$500M. Growth engines = NRS ~$800M (20× EBITDA), net2phone ~$210M (13×), fintech ~$130M (11×). Add $220M cash. Total equity ≈ $1.9B (~$73/share) vs ~$50 today.

2

6

1,120

4 Dec 2025

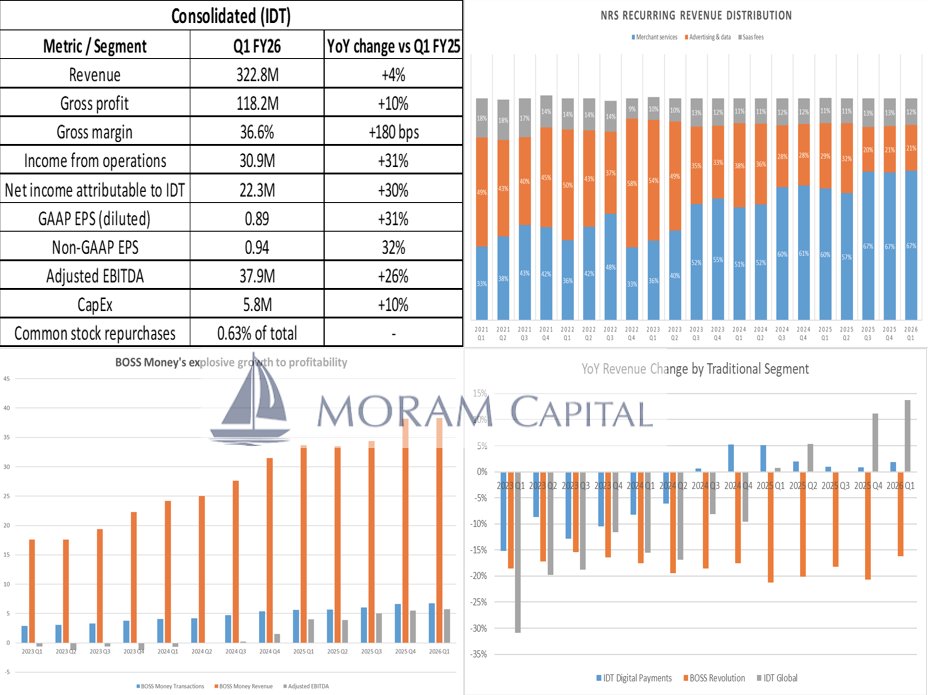

$IDT Q1 2026 earnings: High-margin segments drive record profitability

Profitability surges as high-margin Fintech and Retail units overtake legacy decline.

IDT Corporation delivered a strong start to Fiscal Year 2026. While top-line revenue growth remains modest at 4%, the company is successfully executing a mix shift toward higher-margin businesses. The three growth engines—NRS (retail software), Fintech (money transfer), and net2phone (cloud comms)—now generate substantial operating leverage. Notably, the Fintech segment nearly doubled its operating income year-over-year. Management also noted a favorable legal conclusion regarding the long-standing Straight Path class action suit.

🐂 Bull Case

• 🟢 Margin Explosion: Consolidated Gross Margin expanded 180 basis points to 36.6%. Adjusted EBITDA jumped 26% year-over-year.

• 🟢 Fintech Breakout: The Fintech segment (BOSS Money) grew Adjusted EBITDA by 87%, proving that last year's pivot from "growth at all costs" to "profitable growth" is working.

• 🟢 NRS Pricing Power: Average revenue per terminal (ARPU) hit $313, up 6% YoY, driven by merchant services and software fees, offsetting ad market weakness.

• 🟢 Legal Clarity: The Delaware Supreme Court dismissed claims regarding the Straight Path spin-off, removing a significant overhang.

🐻 Bear Case

• 🔴 Cash Flow Optic: Operating cash flow swung to negative $10.1 million (though management attributes this entirely to weekly timing/pre-funding).

• 🟡 NRS Terminal Adds: Net terminal additions were roughly 800. While seasonal churn is a factor, the pace of new unit deployment is worth monitoring.

• 🟡 Advertising Weakness: NRS Advertising & Data revenue fell 15% due to industry-wide CPM declines and inventory expansion.

⚖️ Verdict

This is a very strong quarter. The Bull case is significantly more compelling. IDT has effectively transformed from a low-margin telecom carrier into a profitable fintech and software holding company. The 26% growth in EBITDA significantly outpaces revenue growth, validating the business model. The cash flow "miss" appears to be a timing technicality rather than structural cash burn.

— • — • —

Themes, Drivers, and Concerns

🟢 Profitable Mix Shift (Materialized)

The long-awaited inflection point is here. The "growth" segments (NRS, Fintech, net2phone) are no longer just growing revenue; they are printing cash. Fintech operating income rose 97%, and net2phone operating income rose 94%. These segments are now large enough to completely offset the stagnation in Traditional Communications.

🟢 Innovation Driving ARPU (New/Evolving)

NRS revenue grew 22% despite only modest terminal additions because they are selling more value-added services. New integrations with DoorDash and Grubhub, along with increased credit card utilization at stores, drove the Monthly Average Recurring Revenue per Terminal to $313 (up from $295 last year).

🟡 Cash Flow Volatility (Concern)

Cash flow looked ugly this quarter (negative $10.1M vs positive $0.1M last year). However, this appears to be a "false positive" for concern. The quarter ended on a Friday, which requires pre-funding weekend remittances for BOSS Money (approx. $30M-$40M swing). This is a known quirk of their business model but requires investors to trust management's explanation.

🟢 Legal Resolution (New)

The dismissal of the Straight Path class action lawsuit is a non-operating but material positive. It removes potential legal liabilities and legal fee expenses moving forward, cleaning up the risk profile.

🔴 Advertising Headwinds (Concern)

NRS Advertising revenue dropped 15%. Management cited industry-wide declines in CPMs (cost per mille) because streaming services (like Netflix/Disney ) have flooded the market with new ad inventory. This is an external pressure that may persist.

— • — • —

Main Financials

All comparisons are versus Q1 2025 (Year-Over-Year) unless noted.

Consolidated Results

• Revenue: $322.8 million (🟢 4%)

• Gross Profit: $118.2 million (🟢 10%)

• Gross Margin: 36.6% (🟢 180 bps)

• Income from Operations: $30.9 million (🟢 31%)

• Adjusted EBITDA: $37.9 million (🟢 26%)

• GAAP EPS: $0.89 vs $0.68 (🟢 31%)

Segment Performance

NRS (Point of Sale Software)

• Revenue: $37.1 million (🟢 22%)

• Recurring Revenue: $35.3 million (🟢 22%)

• Income from Operations: $8.9 million (🟢 35%)

• Key Stat: Merchant Services revenue grew 38%, offsetting the 15% drop in Ads.

Fintech (BOSS Money)

• Revenue: $42.7 million (🟢 15%)

• Adjusted EBITDA: $7.5 million (🟢 87%)

• Key Stat: Digital channel send volume increased 34%.

net2phone (Unified Communications)

• Revenue: $23.5 million (🟢 9%)

• Adjusted EBITDA: $3.6 million (🟢 44%)

• Key Stat: Subscription revenue grew 10%.

Traditional Communications (Legacy)

• Revenue: $219.5 million (🟡 -0.5%)

• Adjusted EBITDA: $18.9 million (🟢 2%)

• Note: Continues to act as a stable cash cow.

Balance Sheet

• Cash & Equivalents: $220.0 million.

• Debt: $0.

• Capex: $5.8 million (up from $5.3 million).

— • — • —

Guidance

IDT reaffirmed its full-year FY2026 guidance.

• FY2026 Adjusted EBITDA: $141 million – $145 million.

Implied Growth Analysis:

• Management uses a revised EBITDA definition (excluding stock-based comp).

• FY2025 Comparable EBITDA was $131.7 million.

• The guidance implies YoY growth of approximately 7% to 10%.

• Context: In Q1, IDT achieved $37.9 million in EBITDA, which is a 26% YoY growth rate.

• Run-Rate Check: $37.9 million x 4 quarters = $151.6 million.

Assessment: The guidance appears highly conservative. To hit the top end of the range ($145M), IDT would only need to average $35.7M per quarter for the remainder of the year—lower than what they just achieved in Q1. Unless there is significant seasonality or planned investment spend expected in H2, an eventual guidance raise seems likely.

— • — • —

Main Questions for the Earnings Call

1. Guidance Conservatism: With Q1 EBITDA growing 26% and hitting a run-rate well above the $145M high end of guidance, are you anticipating specific headwinds or investment spend in the coming quarters that would cause deceleration?

2. NRS Advertising: The decline in ad revenue (-15%) was attributed to macro inventory supply. Do you view this as a structural reset for CPMs on your network, or do you expect to offset this with volume growth in FY26?

3. Capital Allocation: Now that the Straight Path legal issues are fully resolved and the balance sheet holds $220M in cash with no debt, does this change your appetite for larger share repurchases or M&A?

4. Cash Flow Swing: Can you quantify the exact impact of the "Friday quarter-end" on operating cash flow? Should we expect a double-catch-up in Q2 cash flow?

5. NRS Churn: You mentioned "non-seasonal churn" and "technical issues" in the press release notes. Can you elaborate on the technical issues referenced and confirm if they are fully resolved?

1

4

1,371

4 Dec 2025

IDT Corp $IDT Q1'26 results reflect strong growth in NRS, Fintech, and net2phone segments. Record levels of gross profit & EBITDA achieved. #FinanceUpdate 📈 notdumbmoney.com/idt/2025120…

1

306

19 Nov 2025

3

163

30 Sep 2025

2) The failed $IMXI acquisition and its consequences:

IDT will focus on organic growth by increasing the customer acquisition budget for BOSS Money and Net2Phone.❌➡️📈

3) $IDT BOSS Money started disclosing digital sales: Showcasing the before-mentioned 80% share and casting out tax fears. ✨

2

2

758

29 Sep 2025

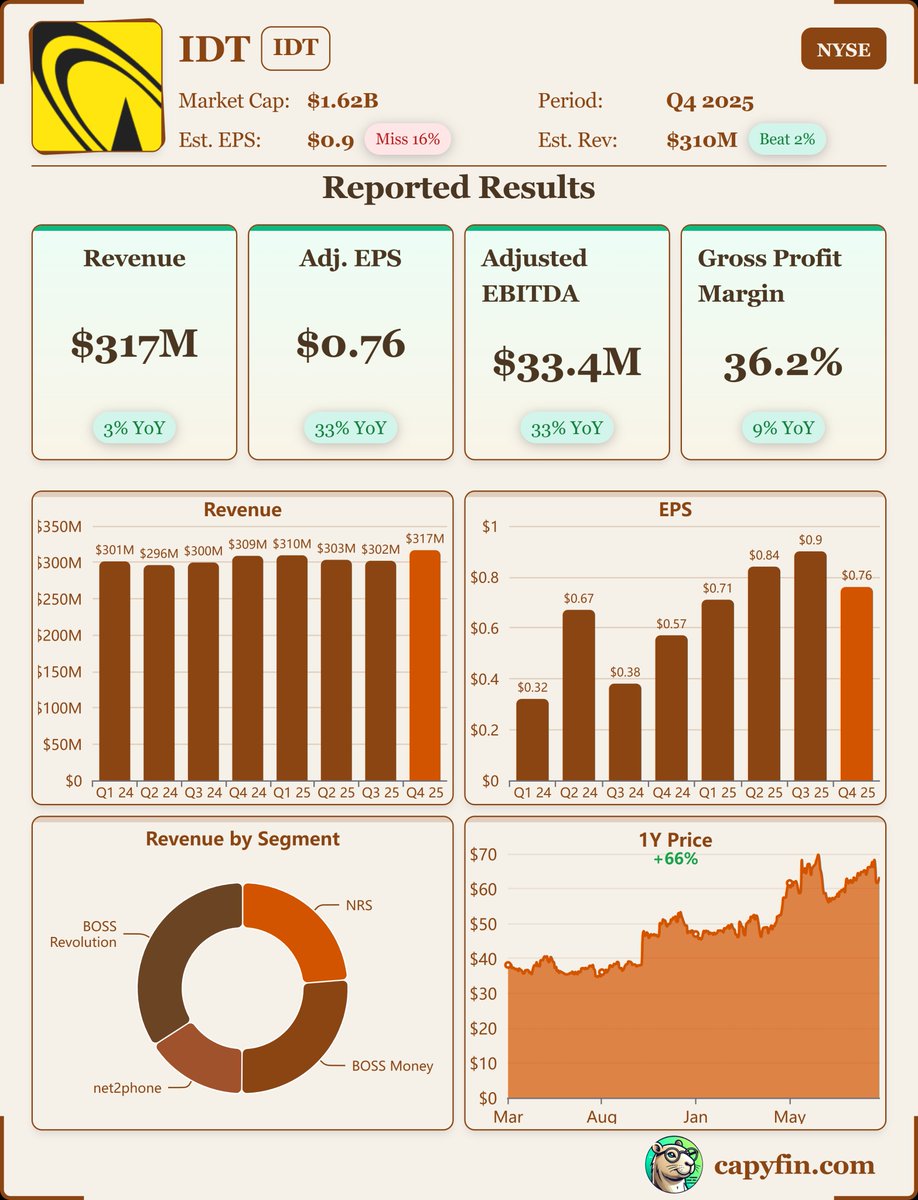

IDT Corporation, $IDT, Q4-25. Results:

📊 Adj. EPS: $0.76 🔴

💰 Revenue: $316.6M 🟢

📈 Net Income: $16.9M

🔎 Record Adjusted EBITDA of $33.4M, driven by double-digit growth across NRS, BOSS Money, and net2phone.

6

8

1,692

13 Aug 2025

1) Our population is too small

2) US telecoms are operating in Canada. They are however focused on providing services to larger businesses for the most part. A few for reference RingCentral, Net2Phone, Nextivia

3) US airlines operate in Canada and have code share agreements.

1

6

115

10 Aug 2025

Business model: A fintech telecom hybrid serving through four segments; Fintech, National Retail Solutions (NRS), net2phone, and Traditional Communications. Notably, NRS recurring revenue grew ~29% to $28.9M, BOSS Money up ~39% to $33.7M, and net2phone subscriptions rose ~13% .

2

76

17 Jul 2025

#SUMMIT | El nuevo rol de los BPO: de operadores a socios tecnológicos estratégicos

🗣️Isabel Pick, ejecutiva de Net2Phone

2

125

Llega el turno para net2phone y Virtual Tech, quienes nos acompañarán el martes 29 de julio en un nuevo CXDay donde hablaremos sobre: “La Nueva Era del Contact Center: IA que multiplica tu ROI.”

Inscríbete Aquí forms.gle/VwBGVVJEnbph9JVC7

1

4

17

143,308

11 Jul 2025

We used a free system called live365 as a relay. Each 128 stream we could send, it could relay to 365 people at up to that 128kbps. We hung out in DalNet and Efnet IRC chat rooms and figured out how to take calls thru our mixing board. Pre Net2Phone/Skype tech.

2

51