Jun 13

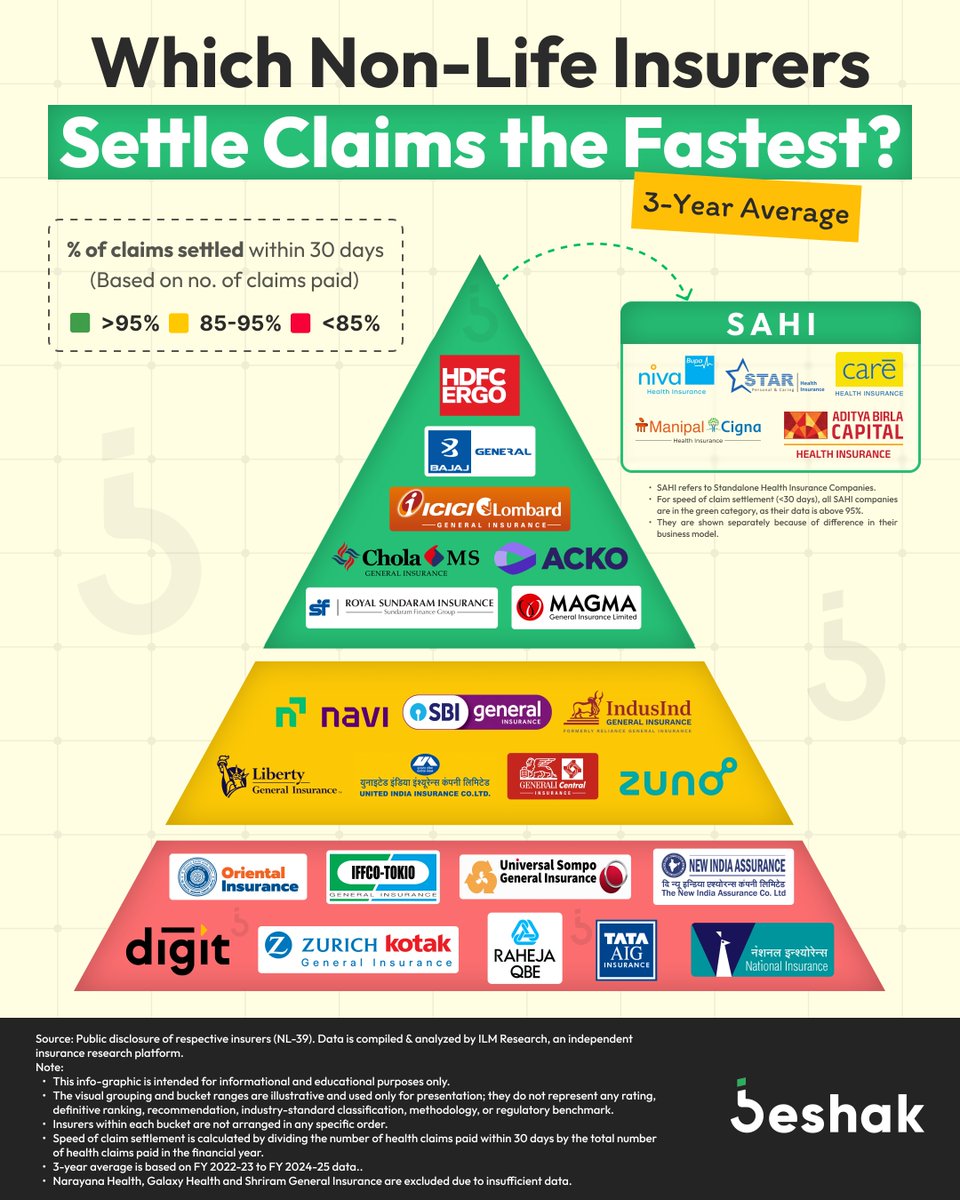

Which non-life insurers actually settle health insurance claims the fastest, consistently over 3 years?

We analysed the average of the last 3 financial years’ data to find out how many valid claims non-life insurers settle within 30 days.

Why does speed matter? Because a claim that takes months doesn't help during a medical emergency. The faster your insurer pays, the sooner you can move forward.

Here's a quick context:

👉 The highlighted names, Aditya Birla Health, Care Health, Manipal Cigna, Niva Bupa, and Star Health, are SAHI companies. These companies specialise exclusively in health insurance products.

👉 The remaining insurers are general insurers, covering motor, fire, and other lines beyond health.

But speed alone doesn't tell the full story. To truly judge an insurer, you need to look beyond one metric.

That’s where a deeper comparison helps.

Use Beshak’s Health Insurance Decoder, with data analysis powered by ILM Research, to compare health insurance plans across multiple important parameters before you decide.

#healthinsurance #claimsettlement #nonlifeinsurance #SAHI #insuranceindia #awareness #beshak

5

7

24

3,067

🚨 Bangladesh has adopted a Zero Commission Model for non-life insurance sales.

Could this reshape the future of insurance distribution—and could India be next?

#Insurance #Bangladesh #ZeroCommission #NonLifeInsurance #InsuranceNews #Finance #BusinessNews

12

Jun 11

DUI-related claim disputes surged 67% last year, overtaking lack of due care as the leading motor-insurance complaint.

Read more: moonstone.co.za/dui-exclusio…

#2025annualreport #allrisks #claims #commercialinsurance #complaints #homeownersinsurance #householdcontentsinsurance #motorvehicleinsurance #NationalFinancialOmbudScheme #NFO #nonlifeinsurance #NonlifeInsuranceDivision #policyexclusion

9

Every journey deserves confidence.

Drive ahead knowing your vehicle is backed by NECO Motor Insurance.

☎️01-4542263

🌐neco.com.np

MAKE A VISIBLE DIFFERENCE!!

#policies #aviation #motorinsurance #insurance #notice #financialloss #necoinsurance #nonlifeinsurance

11

Jun 8

Can an insurance theft claim succeed without direct evidence of theft? A recent NFO ruling suggests it can.

Read more: moonstone.co.za/nfos-only-no…

#finalruling #goodsintransit #householdcontents #insurance #insuredperil #NationalFinancialOmbudScheme #NFO #nonlifeinsurance #NonlifeInsuranceDivision #shortterminsurance #theft

8

Are you well-equipped to bounce back in case of unpleasant surprises?

Don’t let life’s uncertainties derail your progress. Get cover against risks such as motor accidents, fire damage, theft and other property losses. These protect you against financial burden when things don’t go as planned.

Stay prepared for life’s setbacks.

Visit uia.co.ug/non-life-companies for the list of Licensed Non-Life Insurers to get started.

#NonLifeInsurance #GeneralInsurance #GetInsured

2

15

231

As you put in the effort every day, you can’t always predict what tomorrow brings, but you can make sure that what you’ve earned, is protected.

Work smart by ensuring that your business & assets are insured, so that repair or replacement costs don’t erase your wins. Contact a licensed Non-Life Insurer today.

#GetInsured #NonLifeInsurance

2

6

172

Apr 9

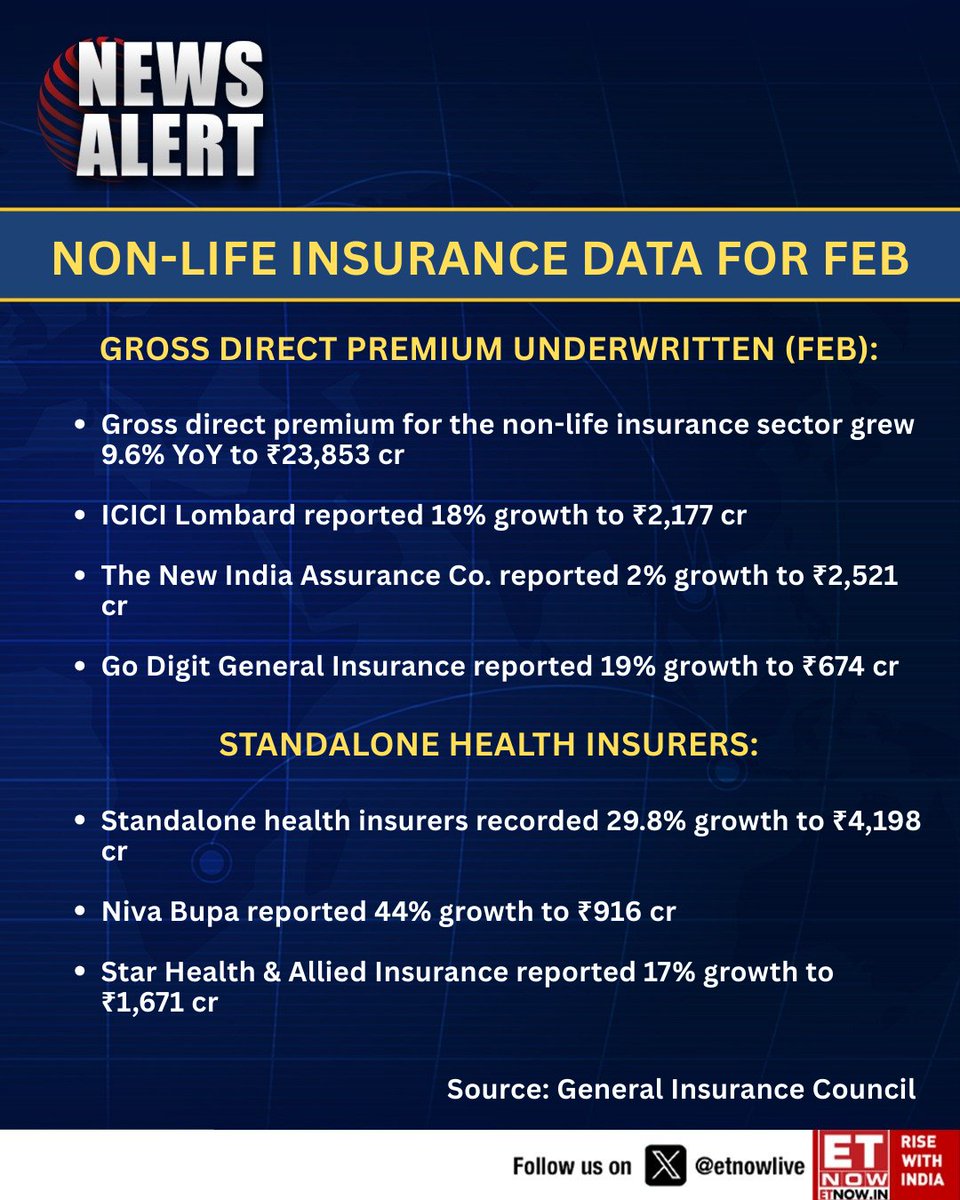

#WATCH | The non-life insurance industry delivered a solid FY26, with premiums rising nearly 10% to ₹3.25 lakh crore, led by strong growth in standalone health insurers

@anuragshah_ joins with the highlights

#InsuranceSector #NonLifeInsurance #HealthInsurance #IndiaMarkets #FY26 #Financials

2

1,015

Hard work pays off, but only when it’s protected, otherwise, all that effort could go to waste.

From business equipment to personal valuables, the right cover ensures that if your business faces a setback or your assets are damaged, your finances remain secure.

Contact a Licensed Non-Life Insurer today to protect your hard work.

#NonLifeInsurance #GetInsured

2

18

365

Access here: bit.ly/4bwmy6B

Proposed changes in how the #HongKongInsuranceAuthority (HKIA) evaluates #nonlife #insurers’ required capital levels around natural #catastrophes & man-made risks,...

#insurance #nonlifeinsurance #AsiaPacific #HongKong #AMBestCommentary

2

181

Building a business takes grit, long nights, bold decisions and a vision that refuses to quit. The last thing you need is uncertainty undoing all that effort.

You may not always know what’s coming your way, but you can choose to be prepared. With Insurance, you get to safeguard your hard work, so when challenges arise, your operations remain steady and your progress stays intact.

Contact a Licensed Non-Life Insurer to get started.

#GetInsured #NonLifeInsurance

4

18

274

Mar 9

#NewsAlert | Non-life insurance premiums rise 9.6% YoY in February; standalone health insurers lead growth with nearly 30% jump

#InsuranceSector #NonLifeInsurance #HealthInsurance #ICICILombard #NivaBupa

1

2

821

Feb 24

MASTERCLASS: How to do Fundamental analysis of Health / General / P&C insurers? #ICICILombard #StarHealth #CareHealth #GoDigit #NivaBupa

Putting Buffett wisdom in action — in simple lang

Combined Ratio FY23 FY24 FY25

New India Assurance 117.2% 120.9% 119.1%

GoDigit 107.4% 108.7% 108.6%

ICICI Lombard 104.5% 103.3% 102.8%

Star Health 95.3% 96.7% 101.1%

Niva Bupa 97.1% 98.8% 101.2%

The 𝗰𝗼𝗺𝗯𝗶𝗻𝗲𝗱 𝗿𝗮𝘁𝗶𝗼 𝗖𝗼𝗥 for general insurers is a simple way to measure how profitable an insurer is from its core business i.e., underwriting policies

CoR = claim payouts expenses an insurance company has, divided by the premiums it earns — expressed as %

CoR < 100% — Insurer is making a profit from underwriting

CoR = 100% — Break even

CoR > 100% — Underwriting losses (claims expenses > premiums)

So does that mean Star and Niva Bupa are the only profitable insurers and multiline insurers are incurring losses? No!

General insurers have another source of income — Interest Income on Float

𝗪𝗵𝗮𝘁 𝗶𝘀 𝗙𝗹𝗼𝗮𝘁?

Insurers collect premiums upfront, but often don’t have to pay a lot of claims until later — sometimes years later. During that time, they invest the remaining premium money (called "float") to earn interest income

Buffet calls 𝗳𝗹𝗼𝗮𝘁 the money, insurers hold, but don't own

The longer an insurer is able to hold float, the more interest income it makes.

Btw, how do you get a sense of the float holding period?

Insurers with total float size overtime >> premium collection in a year — have high float retention

New India Assurance, Go Digit and ICICI L — float size 2x premiums

Star Health, Niva Bupa — 1x

Multiline insurers seem to be retaining float for longer. Why do you think?

if 𝗖𝗼𝗥 > 𝟭𝟬𝟬% (i.e small losses in core business), insurer can still be overall very profitable if they have accumulated a lot of float overtime — thru good holding periods

e.g ICICI Lombard

if 𝗖𝗼𝗥 >> 𝟭𝟬𝟬% then the UW loss is significant and it eats into the interest income

e.g New India Assu., GoDigit

A low 𝗖𝗼𝗥 <= 𝟭𝟬𝟬% is always desired

e.g Star and Niva Bupa

but you have to be careful

Low CoR 𝘮𝘢𝘺 𝘣𝘦 because of low claim payouts much at the dismay of customers. If customers are not happy, they will stop renewing and hence float accumulation will slow down overtime

Summary

CoR <=100% overtime is always desired, but low does not always equate to good. So double click to ensure it isn't a lemon 🍋

CoR slightly >100% overtime is fine so long as the insurers has accumulated sizable float relative to premiums

CoR >> 100% and float is not significant relative to premiums — you have a🍋

——————————————————

Want to understand #WarrenBuffett method of evaluating a general insurer in detail? Watch this linked video:

youtu.be/XhK7HakNwxY?si=sLZ_…

I simplify #businessanalysis / #businessmodels. Reach out to me for guidance on #equityresearch #valuation #financialstatementanalysis

#investandrise #emergingmarkets #generalinsurance #nonlifeinsurance #healthinsurance

1

2

156

Feb 9

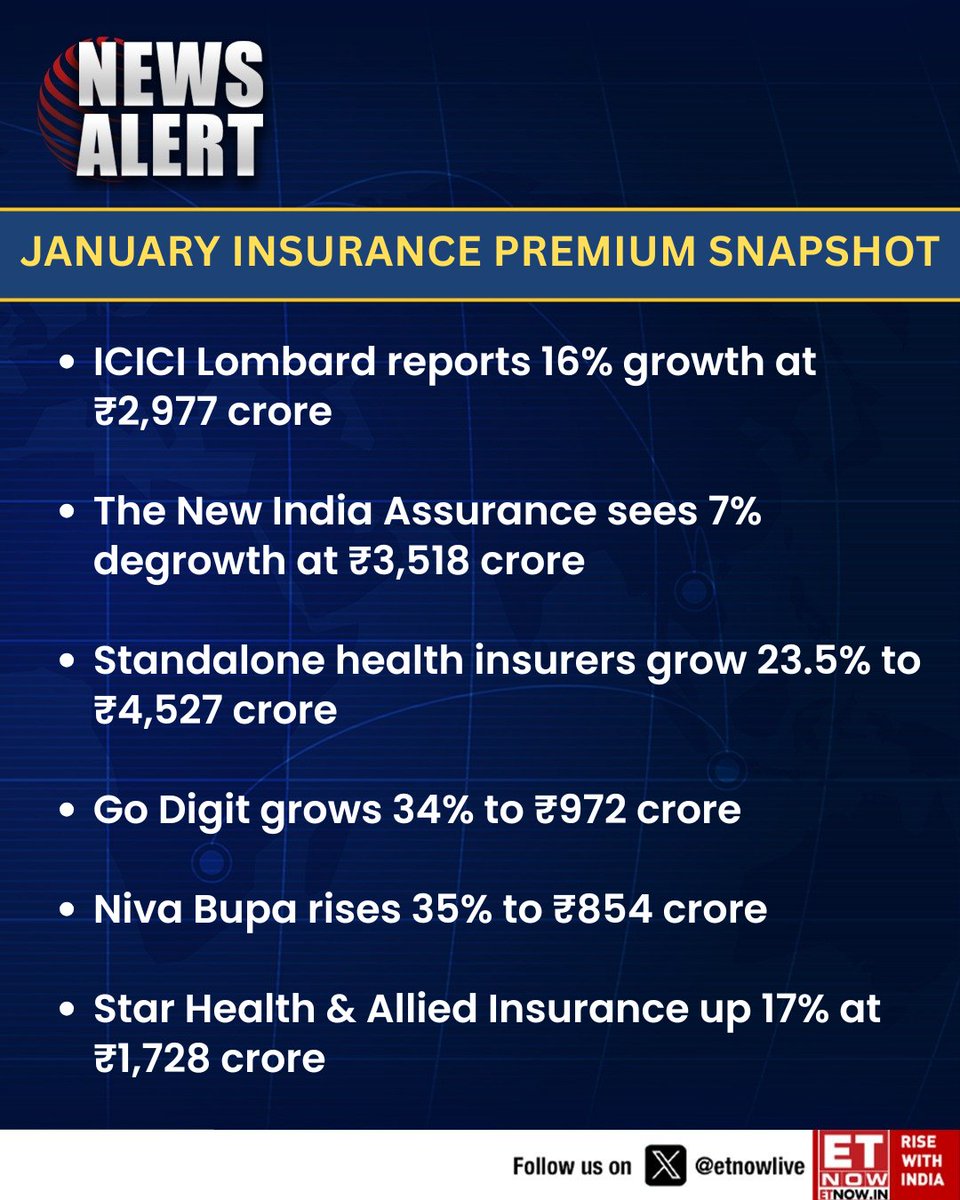

#NewsAlert | January insurance premiums highlight strong growth for standalone health insurers, while ICICI Lombard gains and New India Assurance sees degrowth

#Insurance #NonLifeInsurance #HealthInsurance #ICICILombard

3

2

1,051

#NewYearResolutions

The new year is a time for new goals and fresh beginnings.

As you lay the foundation for the big goals, make sure you also have a safety net in place for the unforeseen, so that you are able keep going, no matter what.

Contact a Non-Life Insurer today to get started.

#NonLifeInsurance #MondayMotivation

2

7

15

336

18 Dec 2025

The festive season is for fun, family and unforgettable moments, just don’t forget your protection.

With Non-Life Insurance, you can insure your assets, your travels and your everyday risks while you focus on making holiday memories.

Contact a Non-Life Insurer today to get started.

#NonLifeInsurance

4

13

181

9 Dec 2025

The holidays are coming and calling for more family time, road trips, gifts and good food. But nothing ruins the fun like unexpected risks.

Protect your home, your car and the things you value with General Insurance and enjoy the season knowing you’re covered from all angles.

Contact a licensed Non-Life insurer today.

#NonLifeInsurance #GeneralInsurance

6

12

347

8 Dec 2025

गाडी मात्र होइन, तपाईंको यात्राको निश्चिन्तता पनि

नेको मोटर इन्स्योरेन्स, भरोसाको साथमा।

☎️01-4542263

🌐neco.com.np

MAKE A VISIBLE DIFFERENCE!!

#policies #aviation #motorinsurance #insurance #notice #financialloss #necoinsurance #nonlifeinsurance #policy #insurance

2

2

327

27 Nov 2025

जहाँ गए पनि, नेको सँग यात्रा सुनिश्चित बनाउनुहोस्।

𝐍𝐄𝐂𝐎 𝐓𝐑𝐀𝐕𝐄𝐋 𝐈𝐍𝐒𝐔𝐑𝐀𝐍𝐂𝐄

__________________________________________

☎01-4542263

🌐neco.com.np

MAKE A VISIBLE DIFFERENCE!!

#policies #insurance #coverage #necoinsurance #nonlifeinsurance #policy

1

1

2

261