🚧 We’re Hiring Across Gujarat & Mumbai! 🚧

PSP Projects Limited is looking for experienced professionals to join its growing team for ongoing building construction projects.

📌 Openings in:

Hashtags

#Hiring #ConstructionJobs #PSPProjects #BuildToLast #NowHiring

18

3

4

88

5,804

May 5

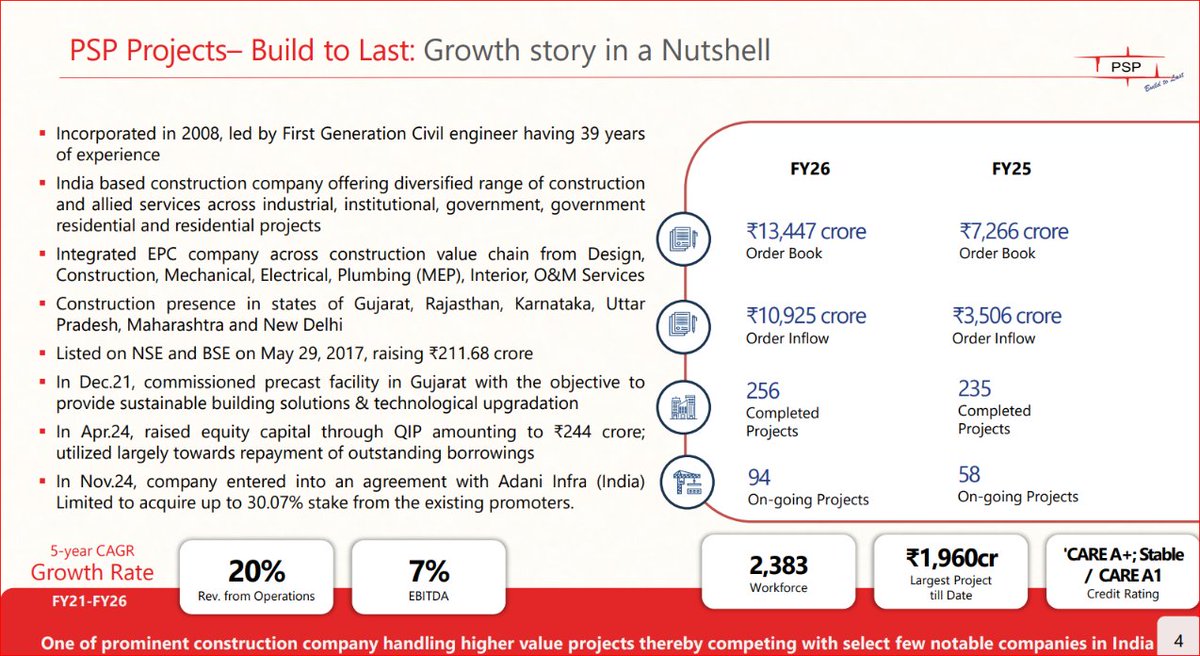

PSP Projects Ltd Concall Summary for Q4FY26

CORE HIGHLIGHT

- Record execution momentum with highest-ever quarterly revenue and strong order book visibility driven by large-scale projects

MANAGEMENT COMMENTARY

- FY26 described as a year of execution, scale, and strategic transformation

- Strong Q4 performance with record revenue driven by execution strength

- High confidence in scaling business with 20–25% growth aspiration till FY30

- Margin moderation attributed to one-off ECL provision and project mix changes

- Focus areas: execution excellence, large project delivery, order book visibility

FUTURE OUTLOOK & GUIDANCE

- FY27 revenue guidance: ₹4,500 Cr

- EBITDA margin expected to improve to 7–8% (vs 6% in FY26)

- Long-term target: ₹19,000 Cr revenue by FY30

- Expected order inflow: ₹5,000–₹6,000 Cr

- Strong pipeline from large infra/government projects

INDUSTRY & MACRO TRENDS

- Indian EPC/construction sector outlook remains structurally strong

- Government spending driving growth in infra, healthcare, education

- Revival in private capex (manufacturing, logistics, data centers)

- Shift toward organized players and pre-cast/modular construction

COMPETITIVE POSITIONING

- Strong differentiation via pre-cast construction technology

- Proven execution track record (e.g., G 18 in 148 days)

- Positioning toward large, complex, landmark projects

- Ability to deliver faster timelines vs peers

RISKS & CONCERNS

- ₹29 Cr ECL provision impacted FY26 profitability

- Trade receivables elevated at ₹928 Cr (working capital pressure)

- Project execution delays in early stages (land clearance, piling issues)

- High dependence on timely billing and collections

GROWTH DRIVERS & STRATEGY

ORDER BOOK STRENGTH

- Strong visibility with large project pipeline

- Adani Group contributes ~67% of order book

PRE-CAST EXPANSION

- Facility capacity: 3 million sq. ft.

- Additional capex of ₹15–20 Cr planned for scaling

GEOGRAPHIC EXPANSION

- Expanding beyond Gujarat into:

- Uttar Pradesh

- Rajasthan

- Maharashtra

- Karnataka

- Delhi

EXECUTION FOCUS

- Shift toward mega-scale infrastructure & high-rise projects

- Increased capability for complex engineering execution

PRODUCT MIX & PORTFOLIO

- Order book mix:

- Institutional: 67%

- Government: 25%

- Balance: Industrial & residential

- Increasing focus on large-scale landmark projects

- Examples include high-rise developments and airport infrastructure

FINANCIAL PERFORMANCE

FY26

- Revenue: ₹3,149 Cr (↑ 25% YoY)

- PAT: ₹55 Cr (↓ 2% YoY due to ECL provision)

- EBITDA Margin: 6% (vs 7.7% YoY)

BALANCE SHEET

- Long-term debt: ₹43 Cr

- Short-term debt: ₹274 Cr

- Target: Debt-free in FY27

WORKING CAPITAL

- Receivable days: 90–100 days

- Target: 60–70 days

MOAT CHARACTERISTICS

- Strong execution capability in large EPC projects

- Pre-cast tech-led speed advantage

- Large repeat business from marquee clients

- Growing presence in high-value projects

KEY INSIGHT

- Margin pressure is temporary (one-off mix impact) while execution scale remains structurally strong

OUTLOOK

- Strong revenue growth visibility backed by order book

- Margin recovery expected in FY27

- Working capital discipline will be key monitorable

- Continued shift toward large, complex projects

CONCLUSION

- PSP Projects delivered strong FY26 topline growth with record execution and order book expansion, though profitability was impacted by a ₹29 Cr one-off provision.

- The company is transitioning toward mega-project execution, supported by its pre-cast technology advantage and strong client relationships (notably Adani Group).

- With ₹4,500 Cr revenue guidance and margin recovery to 7–8%, FY27 is expected to mark an improvement phase.

- Key monitorables remain receivables, client concentration, and execution pace, but long-term growth visibility remains robust given sector tailwinds and order inflow pipeline.

#PSPprojects

1

4

160

💥 Q4FY26 — Strong Results List

Earnings momentum broad-based 👀

Names to keep on radar 👇

#AdaniPorts #BajajFinance #CholaFinance #AUbank #CEAT

#Equitas #ESAF #GRSE #Granules #HFCL #Ideaforge

#Indegene #Kajaria #KirloskarPnu #MAS #MotilalOswal

#NavinFluorine #NipponLife #PhoenixMills #Piramal

#PSPProjects #RRKabel #Railtel #Schaeffler

#Skipper #SterliteTech #SupremeInd #TMB

#UltraTech #Vedanta #Waaree #Websol

Results driving the trend ⚡

Stay focused 💣

#StockMarket #Results

8

353

As growth trajectory improves from four negative to flat quarters...charts can give momentum ....#pspprojects dont miss the run ..

🐢🐢🐢🙏

24

3,134

COMPANY TOADY #Q4FY26 RESULT STATUS ☑️🔈

1.𝙎𝙊𝙇𝙄𝘿 𝙍𝙀𝙎𝙐𝙇𝙏 𝙎𝙏𝘼𝙏𝙐𝙎📊

🟢#IDEAFORGE

🟢#CGCL

🟢#HFCL

🟢#RAILTEL

🟢#RRKABEL

🟢#KAJARIA

🟢#EQUITAS

2.𝙂𝙊𝙊𝘿 𝙍𝙀𝙎𝙐𝙇𝙏 𝙎𝙏𝘼𝙏𝙐𝙎

🔹#SILVERTUC

🔹#LAURUSLAB

🔹#ASTERDM

🔹#PSPPROJECTS

🔹#ESAFSFB

🔹#ACUTAAS

2

740

COMPANY TOADY #Q4FY26 RESULT STATUS TILL 9:00PM ☑️🔈

1.𝙎𝙊𝙇𝙄𝘿 𝙍𝙀𝙎𝙐𝙇𝙏 𝙎𝙏𝘼𝙏𝙐𝙎📊

🟢#IDEAFORGE

🟢#CGCL

🟢#HFCL

🟢#RAILTEL

🟢#RRKABEL

🟢#KAJARIA

🟢#EQUITAS

2.𝙂𝙊𝙊𝘿 𝙍𝙀𝙎𝙐𝙇𝙏 𝙎𝙏𝘼𝙏𝙐𝙎 📊

🔹#SILVERTUC

🔹#LAURUSLAB

🔹#ASTERDM

🔹#PSPPROJECTS

🔹#ESAFSFB

🔹#ACUTAAS

4.𝘿𝙀𝘾𝙀𝙉𝙏/ 𝘼𝙑𝙀𝙍𝘼𝙂𝙀 𝙍𝙀𝙎𝙐𝙇𝙏/𝙁𝙇𝘼𝙏/ 𝙈𝙐𝙏𝙀𝘿 𝙎𝙏𝘼𝙏𝙐𝙎 📊

🔷#GODREJAGRO

🔷#SONACOMS

🔷#INDIAMART

COMPANY TOADY #Q4FY26 RESULT STATUS TILL 9:15 PM ☑️🔈(29- APRIL-2026 )

1.𝙎𝙊𝙇𝙄𝘿 𝙍𝙀𝙎𝙐𝙇𝙏 𝙎𝙏𝘼𝙏𝙐𝙎📊

🟢#IIFLFIN

🟢#ADOR

🟢#STERLITETECH

🟢#GRANULES

🟢#VEDANTA

2.𝙂𝙊𝙊𝘿 𝙍𝙀𝙎𝙐𝙇𝙏 𝙎𝙏𝘼𝙏𝙐𝙎 📊

🔹#SCHAEFLER

🔹#FEDERALBNK

🔹#GRANULES

🔹#BAJFINANCE

🔹#NAVINFLUOR

4.𝘿𝙀𝘾𝙀𝙉𝙏/ 𝘼𝙑𝙀𝙍𝘼𝙂𝙀 𝙍𝙀𝙎𝙐𝙇𝙏/𝙁𝙇𝘼𝙏/ 𝙈𝙐𝙏𝙀𝘿 𝙎𝙏𝘼𝙏𝙐𝙎 📊

🔷#SYNGENE

🔷#HEG

🔷#MOTILALOFS

🔷#FORCEMOT

🔷#ADANIPOWER

🔷#INDIANB

🔷#BANSALWIRE

🔷#IOB

WEAK NUMBER💔

♦️#SUMMITSEC

7

12

68

18,459

Apr 30

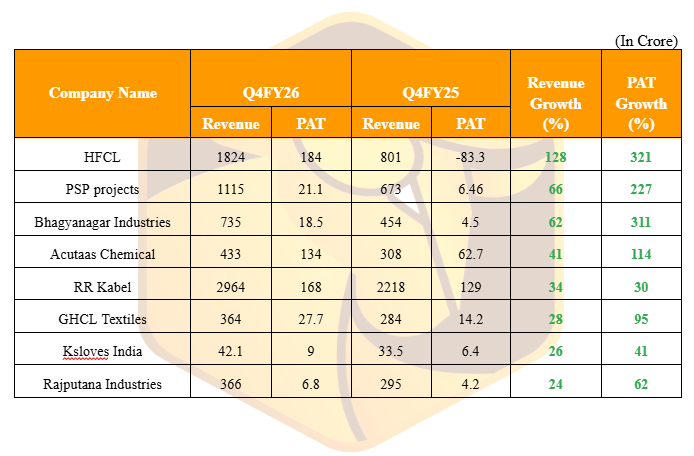

#Q4FY26 Good Results!

List of companies that have reported a growth of 20% or more in Revenue & PAT as on 30-04-2026.

#Hfcl

#Pspprojects

#Bhagyanagarindustries

1

5

30

3,136

Apr 30

Good #Q4FY26-30/4/26 post 2pm till 5pm

RR Kabel

#RRKabel

Solid Q4FY26

Highest ever revenue, EBITDA, PBT and PAT in comps history

Rev at 2964cr vs 2217cr, Q3 at 2535cr

EBITDA at 261cr⏫35% with OPM at 9% almost

PBT at 223cr vs 172cr, Q3 at 176cr

PAT at 168cr vs 129cr, Q3 at 118cr

Good QoQ and YoY uptick across all parameters

OCF at 295cr vs 494cr

Kajaria Ceramics

#Kajaria

Solid margin expansion QoQ and YoY

PBT and PAT more than 2x YoY

Decent revenue uptick after flat qtrs

Rev at 1373cr vs 1222cr, Q3 at 1168cr

EBITDA ⏫90% at 265cr

PBT at 228cr vs 101cr, Q3 at 165cr

PAT at 157cr vs 74cr, Q3 at 86cr

OCF at 664cr vs 501cr

Equitas SFB

#Equitas

#EquitasSFB

Solid Q4FY26

Good uptick QoQ and YoY across all parameters

Rev at 2100cr vs 1869cr, Q3 at 1981cr

PPOP at 402cr vs 311cr, Q3 at 307cr

PBT at 278cr vs 53cr, Q3 at 114cr

PAT at 212ce vs 42cr, Q3 at 90cr

Solid set overall

Asset quality good

GNPA and NNPA down QoQ and YoY

NNPA at 0.72% vs 0.98%, Q3 at 0.72%

RoA shoots up to 0.35% vs 0.16% QoQ, prev Q4 was 0.08%

ESAF Small Finance Bank

#EsafSFB

Getting better, gradually

Rev at 1196cr vs 1036cr, Q3 at 1163cr

PPOP at 241cr vs 90cr Q3 at 252cr

Lower provisions YoY

PBT at 27cr vs -240cr, Q2 at 9cr

PAT at 24cr vs -184cr, Q3 at 7cr

Sharp reduction in GNPA and NNPA QoQ and YoY

NNPA at 1.77% vs 2.99%, Q2 at 2.73%

Laurus Labs

#Laurus

Good Q4FY26

Good margin expansion,but topline below estimates

Rev at 1811cr vs 1720cr, Q3 at 1778cr

PBT at 361cr vs 272cr, Q3 at 327cr

PAT at 282cr vs 182cr, Q3 at 252cr

OCF at 1623cr vs 602cr

Aster DM Healthcare

#AsterDM

Solid Q4FY26

Rev at 1182cr vs 1000cr, Q3 at 1185cr

Good margin expansion QoQ and YoY

PBT at 163cr vs 91cr, Q3 at 103cr

PAT at 153cr vs 85cr, Q3 at 59cr

OCF at 655cr vs 425cr

PSP Projects

#PSPProjects

#PSP

Solid revenue growth,margins yet to catch up

Rev at 1115cr vs 672cr, Q3 at 813cr

PBT at 27cr vs 9cr Q3 at 24cr

PAT at 21cr vs 7cr, Q3 at 18cr

OCF at 322cr vs 53cr

GHCL Textiles

#GHCLTextiles

Rev at 363cr vs 283cr, Q3 at 349cr

Other income higher at 10cr vs 1.4cr

PBT at 35cr vs 19cr, Q3 at 18cr

PAT at 28cr vs 14cr, Q3 at 13cr

OCF at 4cr vs 162cr

Sonal BLW Precision Forgings

#SonaComstar

#SonaCOMS

#SonaBLW

Good set, rich valuations

Solid orderbook

Rev at 1177cr vs 770cr, Q3 at 1127cr

PBT at 269cr vs 204cr, Q3 at 244cr

PAT at 207cr vs 152cr, Q3 at 154cr

OCF at 614cr vs 733cr

Bajaj Finserv

#BajFinserve

Rev at 38508cr vs 36434cr, Q3 at 39507cr

PBT at 6917cr vs 5993cr, Q3 at 6304cr

Biopol Chemicals

#Biopol

Rev at 49cr vs 33cr, H1 at 32cr

PBT at 8cr vs 4cr, H1 at 4cr

PAT at 6cr vs 3cr, H1 at 3cr

OCF at -13cr vs -2cr

Receivables at 28cr vs 17cr

Inventory at 20cr vs 12cr

Decent:

#AdaniEnt

Rev⏫20%, EBITDA ⏫3%

Airports rev⏫21%, EBITDA ⏫75%

New Industries ⏫41%, EBITDA ⏫6%

#AdaniPorts

Rev at 10737cr vs 8488cr, Q3 at 9704cr

PBT at 3761cr vs 3556cr, Q3 at 3756cr

OCF at 20356cr

#Eveready

Rev at 327cr vs 299cr, Q3 at 367cr

PBT at 16cr vs 12cr, Q3 at 22cr

6

30

367

42,661

Apr 30

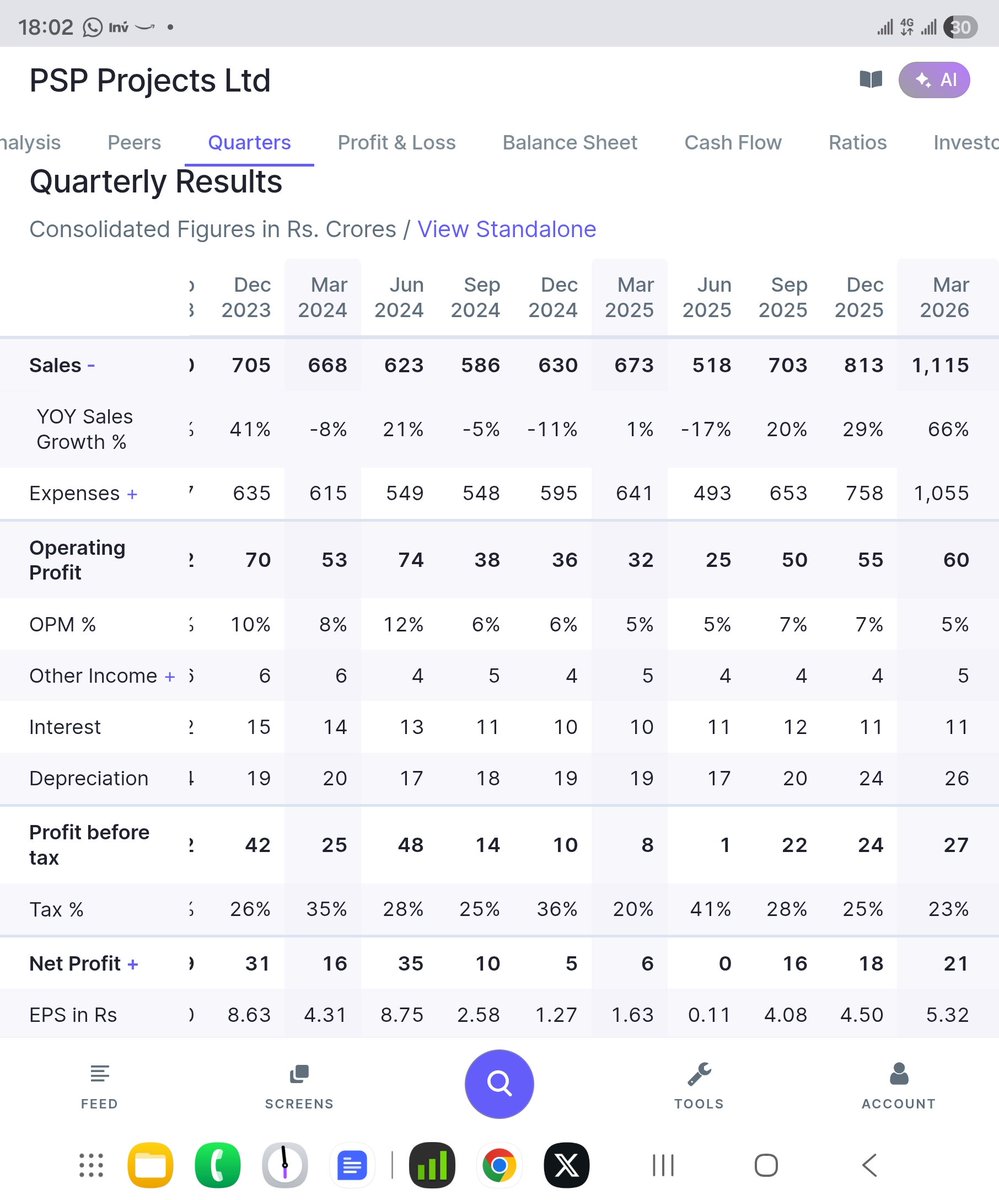

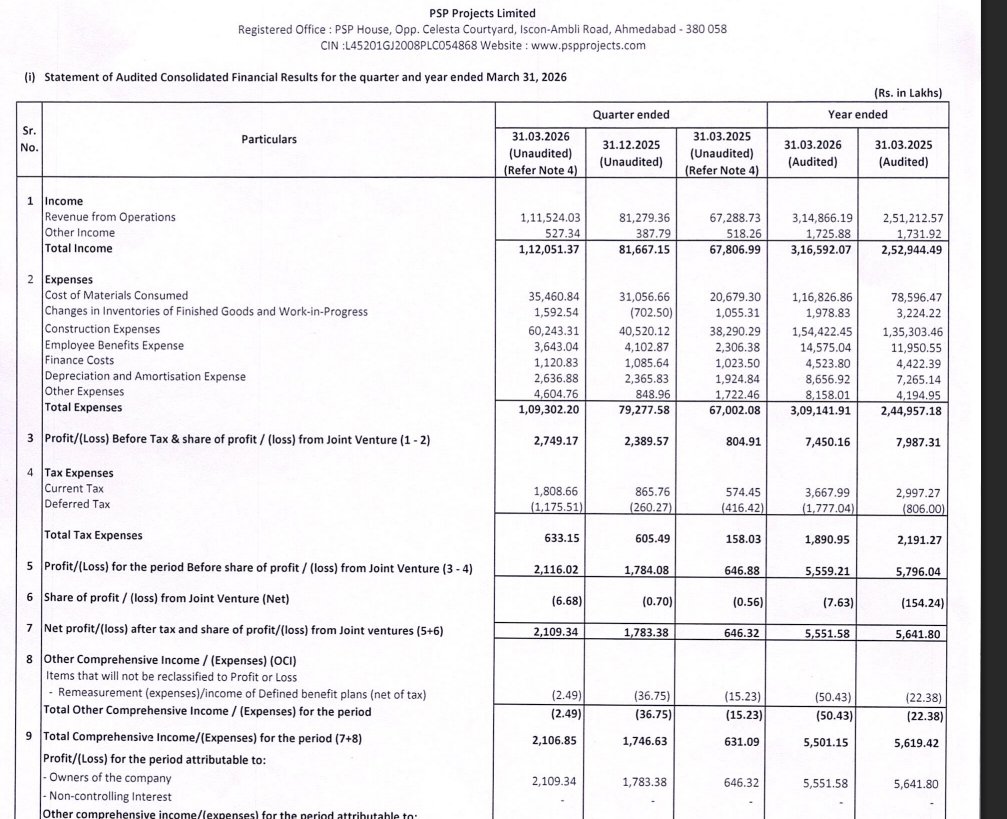

PSP Projects Limited Q4FY26 Results:-

#Q4Results #Q4FY26 #Stockmarket #Nifty #PSPProjects

Revenue 1115.24 Cr vs 672.89 Cr

( 65.74% YoY┃ 37.21% QoQ)

EBITDA 59.80 Cr vs 32.35 Cr

( 84.84% YoY ┃ 9.65% QoQ)

EBITDA Margin 5.36% vs 4.81% YoY & 6.71% QoQ

PBT 27.49 Cr vs 8.05 Cr

( 241.55% YoY┃ 15.05% QoQ)

PAT 21.09 Cr vs 6.46 Cr

( 226.36% YoY┃ 18.28% QoQ)

2

16

1,440

Mar 26

#MarketsWithMC | यहां एक ऐसे स्टॉक की डिटेल्स दी जा रही है जो अपने रिकॉर्ड हाई से तीन ही महीने में 38% टूट चुका है। हालांकि अब रिकवरी का दौर वापस आ गया और मौजूदा लेवल से यह 61% ऊपर चढ़ सकता है। क्या आपके पोर्टफोलियो में है शेयर?

hindi.moneycontrol.com/news/…

#stockmarketnews #sharemarketindia #PSPProjects #moneycontrol

3

160

Jan 30

Good #Q3FY26-30/1/2026 till 3pm

Welspun Corp

#WelCorp

#WelspunCorp

Good Q3FY26

Highest ever revenue, EBITDA, PBT and PAT in comps history

Rev at 4532cr vs 3613cr, Q2 at 4373cr

PBT at 502ce vs 305cr, Q2 at 492cr

One off gains of last year Q3 at 438cr

Adj PAT at 456cr vs 245cr

Solid QoQ and YoY uptick across all parameters

PSP Projects

#PSPProjects

#PSPProj

Rev at 813cr vs 630cr, Q2 at 703cr

EBITDA at 55cr vs 34cr

PBT at 24cr vs 10cr Q2 at 22cr

PAT at 18cr vs 5cr Q2 at 16cr

Aegis Logistics

#AegisLog

Flattish revenue growth, good margin expansion

Rev at 1725cr vs 1706cr, Q2 at 2294cr

Other income at 81cr vs 60cr, Q2 at 96cr

EBITDA ⏫28% at 297cr vs 233cr

OPM at 17% vs 14%

PBT at 300cr vs 204cr, Q2 at 310cr

PAT at 233cr vs 160cr⏫42%, Q2 at 244cr

Bhagyanagar India

#Bhagyanagar

Good Q3FY26

Highest ever EBITDA, PBT and PAT in comps history

Rev at 577cr vs 394cr, Q2 at 580cr

PBT at 17.7cr vs 5cr, Q2 at 15cr

PAT at 12.8cr vs 4cr, Q2 at 11.2cr

Arvind Ltd

#Arvind

Rev at 2372cr vs 2089cr, flat QoQ

Decent margin expansion

PBT at 172cr vs 146cr, Q2 at 149cr

One off expenses at 24cr related to labour code changes

#Strides

Strides Pharma Sciences

One time other income of 106cr lead to 200cr PAT

EBITDA ⏫12%, Rev ⏫3%

Better margins

Adj PBT at 148cr vs 115 r, Q2 at 145cr

Asahi India Glass

#AsahiGlass

Rev at 1255cr vs 1124cr, Q2 at 1151cr

PBT at 145cr vs 109cr, Q2 at 71cr

Nila Spaces

#NilaSpaces

Solid Q3FY26

Rev at 52cr vs 33cr, Q2 at 42 r

PBT at 12cr vs 5cr, Q2 at 7.7cr

Good QoQ and YoY uptick across all parameters

PAT at 8cr vs 4cr, Q2 at 5cr

Hester Biosciences

#Hester

Rev at 77cr vs 63cr, Q2 at 71cr

PBT at 12cr vs 5cr, Q2 at 5cr

Adjusted for higher other income of prev 2 qtrs

PGHH

#PGHH

Rev flattish at 1260cr

PBT at 402cr vs 354cr, Q2 at 282cr

PAT at 301cr vs 268cr, Q2 at 210cr

Ponni Sugar Erode

#PonniErode

Rev at 151cr vs 115cr, Q2 at 117cr

PBT at 10cr vs 3cr, Q2 at 16cr

Sicagen

#Sicagen

Rev at 264cr vs 210cr, Q2 at 226cr

PBT at 7cr vs 3cr, Q2 at 6cr

PAT flattish due to one off items

RattanIndia Power

#RattanPower

Rev flat at 727cr vs 733cr

PBT at 54cr vs 4cr, Q2 had a loss of 31cr

Decent:

#SaintGobain

5

13

212

25,693

Q3RESULTS update -

#MOIL Net Profit down 17% At ₹53cr YoY

#StridesPhatm NET PROFIT ₹202cr up 140% YoY

#PSPProjects NET PROFIT ₹18cr Cr up

253% YoY

#ARVIND Net Profit up 5% At ₹97cr YoY

#AegisLogistics Net Profit up 42% At ₹177cr YoY

3

2

156

Jan 30

#3QWithCNBCTV18 | #PSPProjects announces its Q3 results

▶️Net Profit At ₹17.8 Cr Vs ₹5 Cr (YoY)

▶️Revenue Up 29% At ₹812.8 Cr Vs ₹630.2 Cr (YoY)

▶️EBITDA Up 54.2% At ₹54.6 Cr Vs ₹35.4 Cr (YoY)

▶️Margin At 6.7% Vs 5.6% (YoY)

4

17

3,581

Jan 30

PSP Projects Ltd Q3 FY26 Results:-

Revenue 812.79 Cr vs 630.21 Cr

( 28.97% YoY┃ 15.64% QoQ)

PAT 17.83 Cr vs 5.05 Cr

( 252.93% YoY┃ 10.32% QoQ)

#Q3Results #Q3FY26 #Stockmarket #Nifty #PSPProjects

2

3

760

Jan 12

#PSPProjects wins ₹61-crore arbitration award from Bhiwandi Nizampur #MunicipalCorporation

@jpullokaran

cnbctv18.com/market/stocks/p…

2

10

5,691

Jan 12

#PSPProjects wins ₹61-crore arbitration award from #BhiwandiNizampur Municipal Corporation

@jpullokaran

buff.ly/7LBIFdf

1

1

1,172

23 Dec 2025

1

2

555

8 Dec 2025

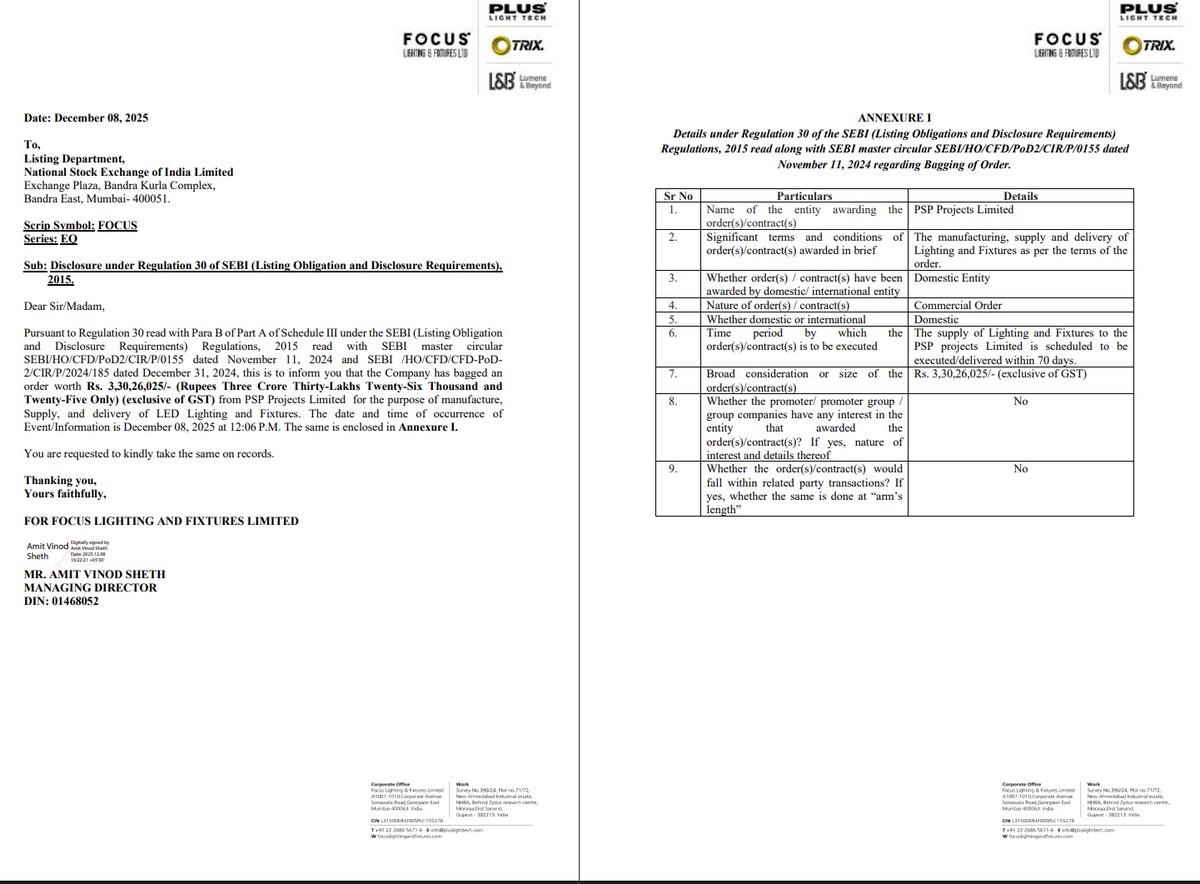

#FocusLighting&FixturesLimited

Focus Lighting & Fixtures Limited has secured an order worth ₹3.30 Cr (exclusive of GST) from PSP Projects Limited for the manufacture, supply, and delivery of LED lighting and fixtures. The order is scheduled to be executed within 70 days.

#Focus

#PSPProjects

#LightingSolutions

#OrderWin

3

6

1,399