To jako policajt mimo službu může být čurák, primitiv a rasista? Může si i zahajlovat? Kontrola osob ve velitelských podtech je ve veřejném zájmu.

1

3

48

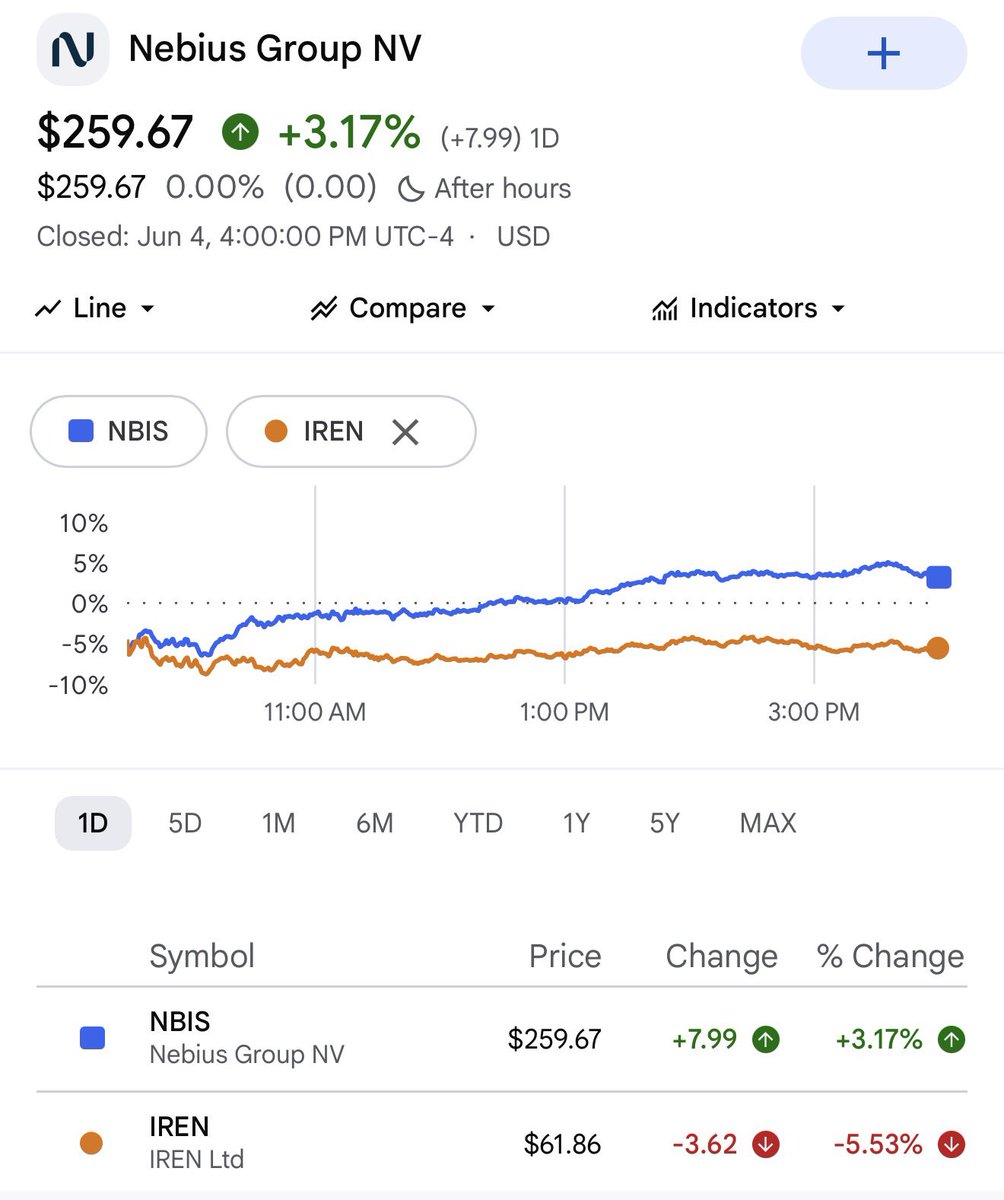

🚨 $IREN is down today, so cue the "Power Monger" cope on the timeline.

Expect to hear:

"We have GWs of power!"

"You can't just build grid access!"

"Most undervalued Neocloud out there!"

Iris Energy is operating less like a cloud play and more like a dilution machine. Look at their shopping spree:

🛒 Rackforce/PodTech

🛒 Mirantis

🛒 Nostrum

🛒 Awaken

The playbook is painfully obvious:

1. Flood X with ads

2. Pay influencers to pump the pivot

3. Tap the ATM, dilute shareholders to oblivion, buy another business.

Meanwhile, early investors are out here pumping their bags.

$NBIS and $CRWV are the only AI Infra plays that matter. No wonder $NVDA invested in both.

9

835

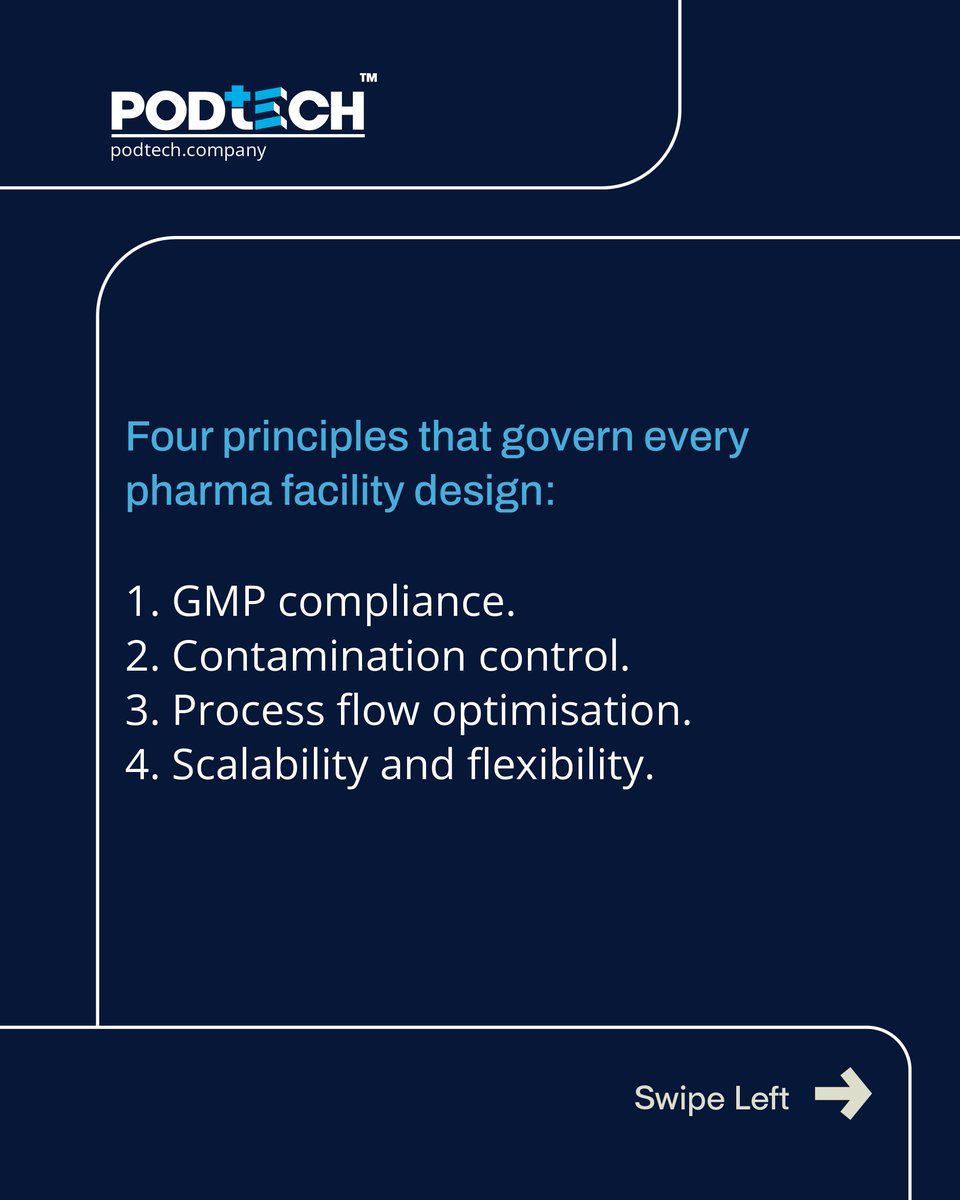

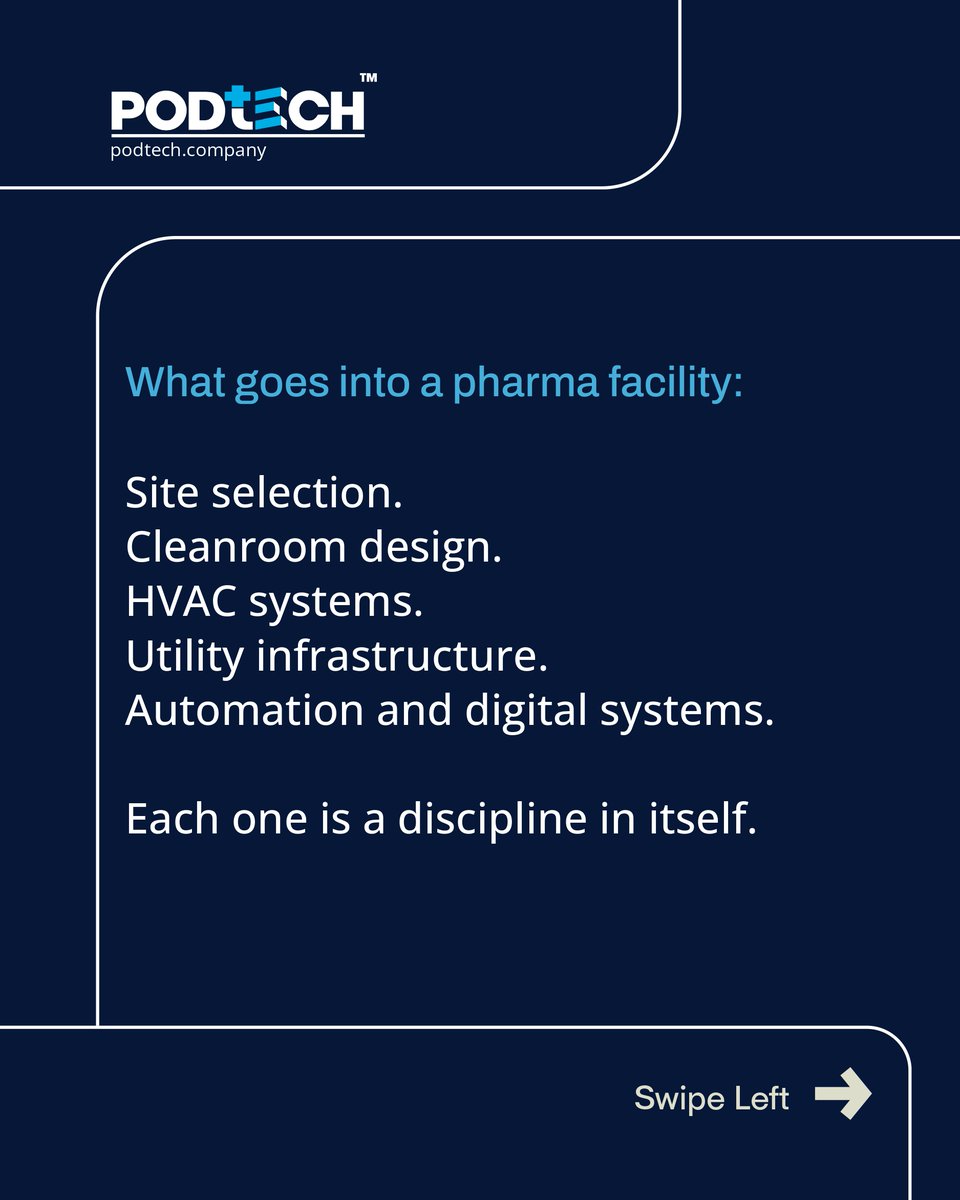

Cleanrooms are the heart. HVAC is the lungs. Utilities are the bloodstream. Automation is the nervous system.

A pharmaceutical facility is a living system. Every component depends on every other. Design them in isolation and you spend years managing the gaps.

Our guide covers how to design them as one integrated whole.

With PodTech™, it is possible.

1

10

May 26

To all celebrating, Eid Mubarak! 🌙

Wishing you and your families a day full of blessings, togetherness, and gratitude. تقبل الله منا ومنكم

As we pause to celebrate, we are reminded of what matters most: Community, Compassion, and Connection. From PodTech Data Center, have a beautiful Eid.

#EidAlAdha #EidMubarak #PodTechDataCenter

1

1

16

🎙️ It's happening RIGHT NOW.

Our CEO @IkeOrizu is on stage at #TheProductFrontier — talking UX, tech & the future of podcast platforms.

Alongside:

→ @MehulFotedar, VP Product of @Podimo

→ Ellie Rubenstein, Head of Pocket Casts of @automattic

Hosted by the legendary @StuartMiles, founder of @PocketLint 🎧

#PodcastShowLondon #PodTech #Jamit

4

13

337

May 19

Drugs save lives but they’re scarce. Speed decides who gets them in time.

That’s exactly why PodTech exists. We believe that the future of healthcare won’t just be built on medicine. It will be built on infrastructure capable of scaling it.

But modern industry runs on something equally critical:

Data.

As the industry becomes more connected, digital, and compute-intensive, infrastructure no longer stops at the factory floor. It extends into data centers.

That’s what made Prasa such a natural fit for us.

For decades, Prasa has been building high-performance data centre infrastructure engineered for uptime, scalability, cooling efficiency, and operational continuity — the backbone modern industries increasingly depend on. So, the synergy was obvious.

And that’s why we’re excited to announce our investment in Prasa Infocom & Power Solutions Pvt. Ltd.

We’re proud to welcome Jay Burse, Promoter and Chief Vision Officer at Prasa and Prakash Burse , Founder of Prasa, whose long-term vision, execution-first mindset, and decades of commitment to building mission-critical infrastructure eventually led us to this juncture.

A special thank you to Anand Bathiya of Bathiya Legal and everyone behind the scenes whose persistence and attention to detail helped bring this partnership together.

2

2

28

May 14

@kerdoscapital with an outstanding, detailed thread on $IREN — one of the clearest explanations I’ve seen of why their capital structure and financing playbook is so powerful.

Back in 2020 during the IREN–PodTech merger, I had a front-row seat to Dan Roberts’ rare skill: using first-principles thinking and a deep understanding of human nature to align incentives perfectly.

He applies that same approach to every deal — from individuals all the way up to Nvidia and Mirantis.

The flywheel just keeps spinning faster and faster.

May 14

$IREN

I want to clear something up about IREN's financing position because I don't think enough people understand how well structured this actually is.

IREN has already deployed ~$2.9B of the $5.8B $MSFT GPU buildout — roughly half — with the remaining Dell tranches scheduled to ship in H2 2026. Per the original 8-K: "GPUs and ancillary products and services, scheduled to be delivered in several tranches from March 2026, for an aggregate purchase price of approximately $5.8 billion payable in installments within 30 days of each tranche shipping." The remaining ~$2.9B will almost certainly come from the $3.6B Goldman Sachs & JPMorgan delayed-draw facility at <6% — secured by the GPUs and Microsoft's own contracted cash flows. Their financing, combined with Microsoft's $1.94B prepayment, covers roughly 95% of GPU-related capex. The balance sheet cash barely needs to be touched.

The $NVDA deal ($3.4B over 5 years) will likely follow the exact same playbook — GPU-backed financing plus a potential NVIDIA prepayment mirroring what Microsoft did. And NVIDIA isn't just a customer here. They hold investment rights to purchase up to 30M IREN shares at $70 — a potential $2.1B investment — with those rights vesting per 100K GPUs deployed through 2031. They don't get the equity until they deliver. That's the kind of alignment you want to see.

Now let's talk about the cash pile because this is where it gets interesting. Audited cash as of March 31 was $2.213B. Unaudited preliminary cash as of April 30 grew to $2.6B — IREN's own words from the Q3 business update. Then on May 11 they priced an upsized $2.6B convertible at 1.00% coupon with a $400M overallotment option. If fully exercised, after estimated underwriting fees, net proceeds would likely be ~$2.925B — potentially putting total cash at roughly $5.5B.

And the ATM tells the same story. The original $1B ATM? Completely exhausted. Replaced in March 2026 with a $6B facility. Just over $1B has already been drawn from the new facility to date. The stock components of Mirantis (~$562M) and Nostrum (~$63M) will likely be sourced from ATM-registered shares — meaning zero additional cash drain. If so, after existing draws and both acquisitions close, the ATM would still have approximately ~$4.4B in remaining capacity.

I've said it before — dilution is accretive if used right. The combined actual cash outflow from both acquisitions is only ~$107M. That barely registers against a potential $5.5B cash position.

So ask yourself — why is a company whose current buildouts are essentially self-financing sitting on $5.5B in cash and ~$4.6B in ATM capacity? I don't think management is hoarding capital for fun. You don't load up like this unless something bigger is coming. Another hyperscaler, a sovereign AI deal, a transformational acquisition — I don't know what it is but the setup is clear. IREN is loading the chamber.

5

105

9,435

May 8

Not trying to argue with you here, but the company is also a company which John Gross joined and took his whole team to, a company that started with PodTech from the beginning, a company which Mirantis joined. They wouldn’t all hop on a sinking ship

2

254

So true. Even had a back-and-forth with Brian Fry(Rackforce/Podtech founder, $IREN acquired them and boasted we were always a Data Center company 😂) to figure out the competence.

135

Apr 28

Multiple companies I co-founded since 2001 have designed, built, and operated the most efficient and advanced data centers of their time. $IREN merged with our company PodTech in 2021, folding in all our early work and innovation. $IREN took this to a whole new level and even hired John Gross. They exponentially leveraged our combined expertise, making them the closest you can get to pulling data centers out of their ______s. 🤣

15

881

Apr 22

Very balanced Daniel. One piece I would add is I think Irens data centre construction capacity is underrated by Nebius fans. I’m not saying it’s better or worse than Nebius , but going back to their inception Iren inherited a 20 year DNA in data centre construction expertise by acquiring PodTech

@brianfry01 is best qualified to talk to this point. Would love to hear more about Nebius from you

305

Apr 21

Greg is amazing at business development. It was Greg @g_duerksen (PodTech) and Paul Gordon ($IREN Director in 2019) who connected the two companies. The rest is history, as they say.

Apr 20

1

1

47

4,836

Apr 21

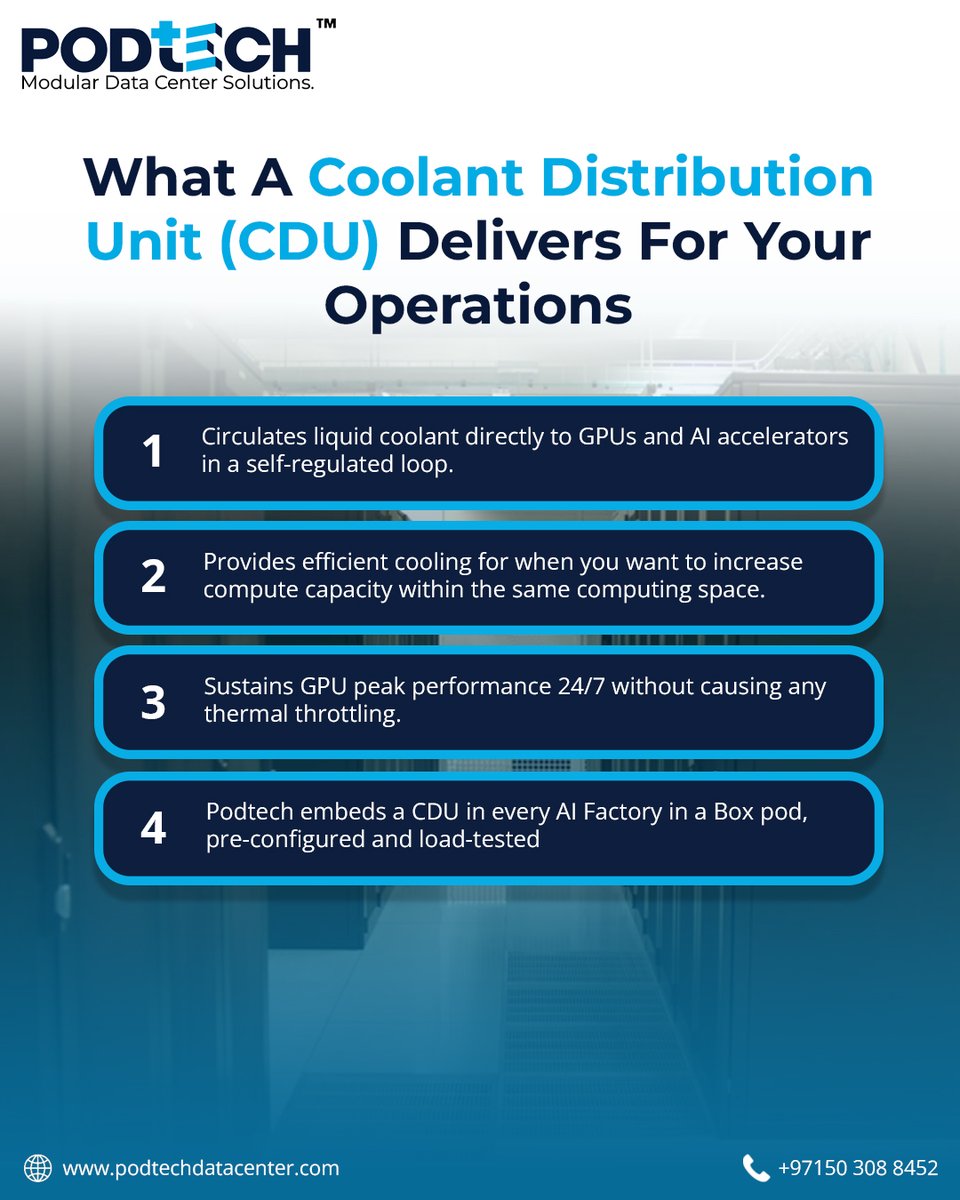

Your GPUs are only as powerful as the systems cooling them.

Most infrastructure decisions focus on compute. But as AI rack densities climb past 80 kW, the Coolant Distribution Unit (CDU) has become the silent differentiator.

A CDU actively regulates coolant flow to every GPU and AI accelerator in real time, ensuring sustained peak performance 24/7.

At Podtech, our AI Factory in a Box solution has the flexibility to integrate CDUs to assist AI workloads. These units are pre-configured, load-tested, and have thermal sustenance.

Learn more about it here: podtechdatacenter.com/what-i…

#DataCenter #ModularDataCenter #LiquidCooling #PodTechDataCenter #DataCenterCooling

2

3

22

Apr 20

💯 correct. @brianfry01 and I were leading the push towards compute from PodTech and into Iris Energy, now IREN.

From the start, we designed the very first data centers to handle various workloads. From custom, adjustable racks to building PSU's.

Future proof by design.

3

4

146

104,894

Apr 20

As it relates to $IREN, your facts and conclusions are off, Daniel.

$IREN did in fact start developing "AI data centers" as early as 2021, when breaking ground in Prince George & Mackenzie (Canada).

Technically, you could even go as far back as 2019, when you take into account the company's first site 'Canal Flats', partially developed by PodTech, a data center company $IREN merged with in early 2020.

You are conflating a few things...

Yes, $IREN's first batch of H100 GPUs, did not get installed until February 2024, but the underlying data center infrastructure already existed many years prior.

While that infrastructure was initially purposed to mine $BTC, it was always over-specced for that singular purpose (much more expensive & durable than traditional mining data centers).

Since day 1, management positioned itself as a disruptive data center company.

Mining $BTC was merely the easiest path forward to monetize its powered-land portfolio quickly & scale its data center footprint at rapid speeds. As such, the facilities were always designed to be modular and multi-purpose.

That design philosophy allowed $IREN to "re-purpose" its 50 MW Prince George data centers for its AI cloud operations by simply taking out $BTC mining ASICs and replacing them with GPU racks.

Sure, to run cloud operations $IREN had to add back-up generators and other redundancy-purposed infrastructure at its sites, but that's merely a question of costs, not "development expertise".

The core data center footprint has been developed in-house many years ago, not in "mid 2024" as you claim.

It's also misleading to measure $IREN's build speed by anchoring to the start of its cloud operations and extrapolating from there.

These are 2 completely different KPIs...

Once Childress was fully ramped, $IREN proofed it could build 50 MW (gross) of air-cooled data center infrastructure in a timeframe of just 1 month. Then, if you account for the extra time needed to install back-up generators (for cloud) installing the GPU racks, you land at roughly 2-3 months.

That lands you at a build speed of ~17 MW / months.

Admittedly, that's the speed for air-cooled deployments, not liquid cooled, which would take significantly longer to develop. But that's beside the point.

You used an inherently flawed method to calculate "build speed" and paint a negative picture of $IREN relative to $NBIS.

I don't think you did that on purpose, but you still got to be careful making these kinds of blunt statements. It's an easy way to loose credibility fast.

What you calculated is still a valid KPI, but its not the same as "build speed".

You effectively calculated how quickly $IREN scaled its existing cloud operations over the past years, relative to $NBIS. And yes, $IREN comes up short in that comparison.

But why is that? As I demonstrated, $IREN is clearly not lacking in development speed, so why did they scale rather slowly?

If you had been following the company for a whale, you'd know by now that $IREN is incredibly meticulous about timing hardware cycles.

Management is executing the exact same playbook during its $BTC mining times...

While most competitors over-commit to hardware that will soon be overshadowed by newer tech, $IREN scales slowly until it has the capacity to go 'all-in' at the start of a new hardware cycle.

This strategy allowed $IREN to quickly emerge from merely a 'top 10' miner (by monthly $BTC output), to the number 1 operator in the space within a timeframe of just ~1 year.

$IREN is following that exact same playbook today, but with AI hardware instead of mining ASICs.

Instead of over-committing on H100/H200s, years after that GPU generation came out, $IREN took it slow, and focused instead on building out 100s of MW of data center infrastructure (both liquid & air-cooled) at its Childress (TX) campus.

Today, the company is in a position in which it can casually purchase 50k units of new Blackwells (as it did last month), and become one of the fastest growing clouds in the sector.

Likewise, we can observe the same pattern at $IREN's next flagship site: Sweetwater 1 (1.4 GW).

Many investor seem to grow inpatient that management still hasn't signed large-scale deals for that new site yet, but $IREN is obviously just following the exact same strategy...

This time with the Rubin GPU generation, which won't be produced at scale until H1 2027.

There are several other reasons, that I haven't covered here, that make up $IREN's cycling strategy (such as financing, negotiating leverage, etc.), but the point remains.

You can't make an apples to oranges comparison and label is as "facts".

It's clear to me that your post is surface-level analayis at best... good for engagement, but not the type of content that will age very well.

That said, based on your commentary, it seems like you have genuine interest in getting deeper into the $IREN rabbit hole.

I hope my feedback is of some help in that regard. 🤝

25

36

435

88,385

Apr 11

Read more: podtechdatacenter.com/data-c…

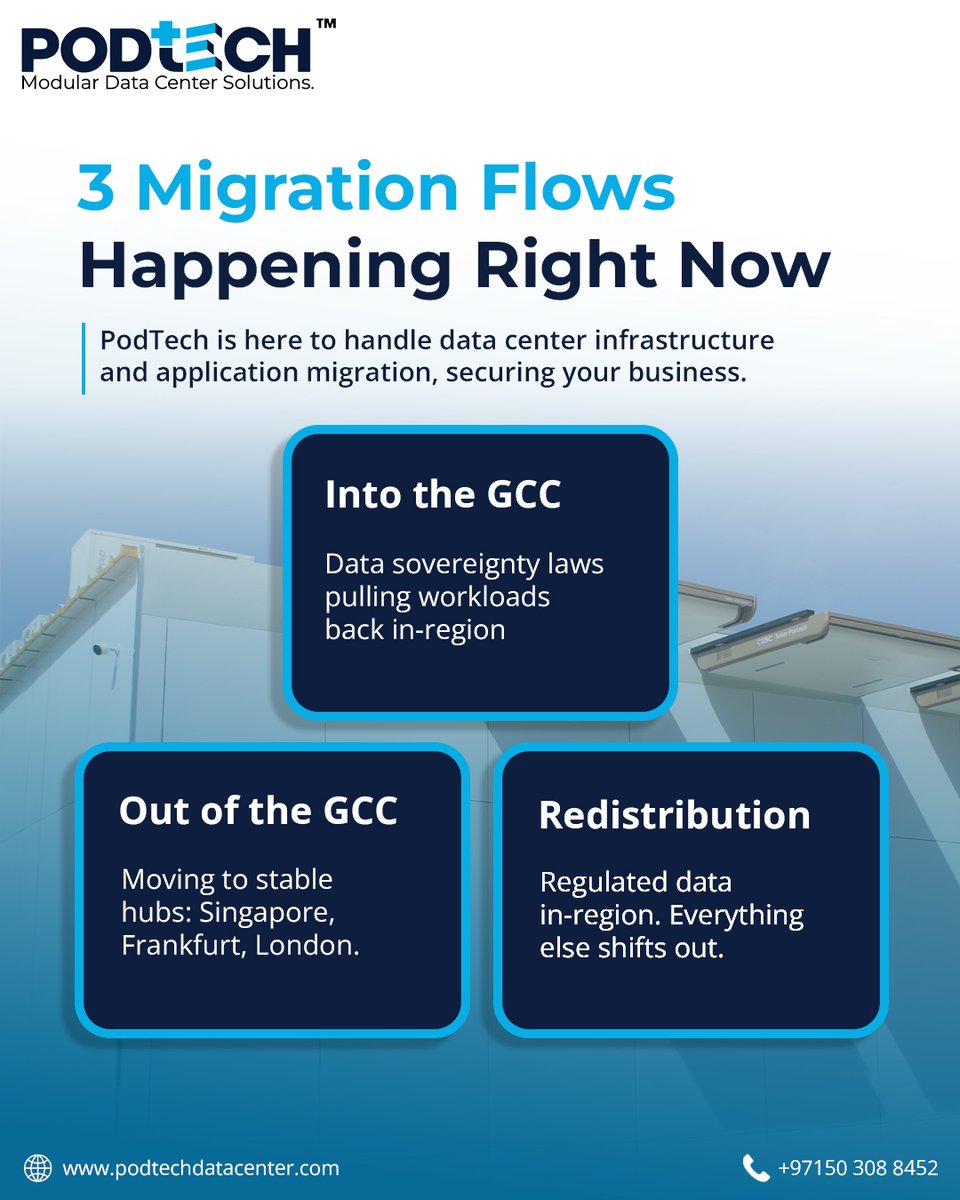

Sovereignty laws. Cyberattacks. Geopolitical pressure.

These three forces are driving one of the largest data center migration waves the GCC has ever seen, and organizations are responding in three distinct ways.

Move workloads in-region to meet sovereignty mandates. Move select data out to stable hubs like Singapore, Frankfurt, and London, or redistribute, keeping regulated data local and shifting everything else.

The ones moving intentionally are building resilient, compliant infrastructure on their terms.

PodTech is handling data center infrastructure and application migration to incorporate resilience to your business.

Which of these three flows describes your organization's current position?

#DataCenterMigration #DataCenter #ITInfrastructure #PodTech #ModularDataCenter

2

2

11

Happy Holidays from @InvestNorthwise!

We just published our $IREN analysis on the Canal Flats site.

Check out the full report in the comments ⤵️

Although many underestimate the significance of the IREN Canadian sites due to the much larger and newer site developments across Texas and Oklahoma, these sites still pack a serious punch and will be some of the first to fully transition into AI GPU leasing and cloud offerings.

These sites, in our view, should be looked at as a driver in cash flows as IREN continues to buildout the rest of the portfolio, as well as proof of concept that they can successfully manage this transition with much larger stakes.

The opportunity for IREN is evident at this point, but it will come down to execution and the ability to continue to pivot to an increasingly competitive buildout and financing environment.

IREN must build a long term moat that can help distinguish itself as eventually capacity begins to close the gap with the current supply shortage.

IREN has an immense amount of bargaining power today with many names in the Mag 7 but may not forever as a bare metal provider.

Proving that specialized colocation works long term, or building out software to accompany its land and power moat will be key to unlocking secondary demand outside of names like MSFT.

There is a window of opportunity for a few years where land, power, and GPU access is enough. This is the time for IREN to execute flawlessly, while building out a real long term moat beyond 2029-2030.

The IREN Canal Flats facility in British Columbia’s Columbia Valley started as a legacy Tembec sawmill that later operated under Canfor before closing in the early 2010s.

In 2020 IREN acquired the 10-acre brownfield site through a deal with PodTech and the Columbia Lake Technology Centre group turning it into the company’s first operational high-performance computing campus.

The 30-megawatt site runs entirely on hydroelectric power from the BC Hydro grid supporting roughly 1.6 exahashes per second of Bitcoin mining capacity while now transitioning toward AI workloads.

Its cool Kootenay climate enables efficient passive air cooling and the existing industrial grid connection from the old mill provided the perfect foundation for IREN’s vertically integrated ownership model of land power infrastructure and data center architecture.

Canal Flats served as the prototype that shaped every larger campus that followed including the 80-megawatt Mackenzie site the 50-megawatt Prince George site and the hyperscale developments in Texas.

The facility also includes formal revenue-sharing agreements that direct about two percent of operating profits to four Ktunaxa Nation communities the ʔakisq̓nuk First Nation ʔaq̓am St. Mary’s Indian Band Yaq̓it ʔa·knuqⱡi’it First Nation and Tobacco Plains Indian Band.

3

2

42

9,393

Don’t know fishy companies.

Go through the entire post lol. They have 0 early mover advantage. Connected with Brian Fry(Rackforce/PodTech merged with $IREN to apparently build Data Centers) to get the correct information.

91

Why $IREN will probably fail as a NeoCloud 🚨

The pivot from Bitcoin mining to AI sounds great on paper, but looking under the hood reveals a massive disconnect between management's narrative and their actual technical capabilities. Let's break it down👇

1. Management has ZERO foundational AI talent

Look at the leadership driving this $11B pivot:

• Co-CEO Dan Roberts: Finance/Infrastructure background.

• Co-CEO Will Roberts: Resources/Commodities background.

• Mike Alfred (Board): Bitcoin investor/Grifter on X.

But the biggest red flag? CTO Denis Skrinnikoff. His 15 years of background is strictly traditional networking and standard Colocation. Worse, his own LinkedIn lists his CTO role at Iris Energy as "Permanent Part-time".

A part-time CTO is leading a $9.7B AI rollout? 🚩

2. The "RackForce" Myth & Lack of Transparency

Management claims they were an AI Data Center company from day one, using Bitcoin just to bootstrap. Bulls point to their absorption of RackForce/PodTech as proof of their AI capabilities.

We dug into this - In our recent back-and-forth with RackForce founder Brian Fry, he admitted their "AI" experience was running 25kW racks in 2012 for "other purposes".🤔

Running traditional HPC over a decade ago is fundamentally different from managing modern 100kW AI GPU clusters.

3. Identity Crisis: Colocation vs. NeoCloud

Dan Roberts wants IREN to be a NeoCloud because it commands $7M-$10M in ARR per MW, compared to standard Colocation at $2M-$3M per MW.

They know how to run power-dense Colocation, but are attempting a full-stack NeoCloud pivot with zero experience.

4. The Microsoft Deal Defense

Bulls scream: "Why would $MSFT trust them if they couldn't deliver?"

Reminder: Microsoft's due diligence isn't bulletproof. They heavily backed Builder.ai at a $1.5B valuation, which recently went bankrupt after its "AI" was revealed to be just 700 engineers in India manually writing code.😂

Microsoft has a habit of throwing capital at the wall to test the waters and secure capacity. A contract is not a definitive stamp of flawless execution capability. Furthermore, IREN hasn't announced a single major deal since that Microsoft contract months ago.

5. Abysmal Performance & Topology Mismatch (The Technical Reality)

Because they lack foundational AI merits, it translates to the metal. IREN lacks(currently Underperforming) the top-tier @SemiAnalysis_ ClusterMAX ratings (like Platinum $CRWV and Gold $NBIS) that true AI-native juggernauts achieve.

Bitcoin mining has high fault tolerance; if a miner goes down, you just lose a fraction of your hash rate. AI training clusters require synchronized, flawless uptime and incredibly complex backend networking (InfiniBand/RoCEv2). IREN's DNA is entirely in the former.

***This is not to shame anyone. These are seasoned individuals who have built a great crypto-mining and infrastructure business.

But traditional colocation and Bitcoin mining skills simply do not seamlessly translate into an AI Data Center juggernaut.

Bottom line: We have seen all we need to be a permabear on IREN. We aren't going to touch this to buy it, or even to short it.

This company might eventually do very well as a pure power/data center landlord, but as a top-tier NeoCloud? Not a chance.📉

#ai #DataCenters

49

7

101

73,519