Jun 13

这 8 个美股 GitHub 项目,很适合和 Codex 一起用

从行情数据、SEC 财报、策略回测到 AI 量化研究,基本覆盖了一套美股投研工作流

把它们封装成 Skills 后,Codex 就不只是帮你写分析,而是能参与完整研究流程

1. OpenBB

金融数据平台,覆盖股票、ETF、宏观、基本面、期权等场景

适合让 Codex 输入 ticker 后,自动拉数据、整理指标、生成公司研究摘要

github.com/OpenBB-finance/Op…

2. yfinance

美股数据分析入门工具,可以获取行情、历史价格、分红、拆股和部分财务数据

适合让 Codex 自动写脚本、画走势图、算最大回撤、对比多只股票表现

github.com/ranaroussi/yfinan…

3. edgartools

用于读取和分析 SEC EDGAR 文件,包括 10-K、10-Q、8-K、Form 4、13F 等

适合让 Codex 直接读公司披露原文,而不是只看二手新闻

github.com/dgunning/edgartoo…

4. sec-edgar-downloader

适合批量下载 SEC 文件

比如下载公司过去几年的 10-K、10-Q、8-K,再让 Codex 提取风险因素、管理层讨论和收入结构变化

github.com/jadchaar/sec-edga…

5. vectorbt

策略回测工具,适合测试不同参数、不同股票、不同周期

比如均线突破、RSI 反转、突破新高后持有 N 天,都可以让 Codex 写成回测脚本

github.com/polakowo/vectorbt

6. QuantStats

回测绩效分析工具,可以生成夏普、最大回撤、波动率、胜率、月度收益等指标

适合接在 vectorbt 后面,让 Codex 输出完整策略体检报告

github.com/ranaroussi/quants…

7. Microsoft Qlib

微软开源的 AI 量化研究平台,覆盖数据、模型、训练、回测等流程

适合让 Codex 帮你拆框架、改模型、跑实验、复现量化论文思路

github.com/microsoft/qlib

8. FinRL

金融强化学习开源项目,适合研究自动交易、组合配置和强化学习策略

适合让 Codex 帮你理解交易环境、修改 reward function、调整策略逻辑

github.com/AI4Finance-Founda…

Codex 做美股最有价值的地方,不是临时问它“这只股票怎么看”

而是把数据源、财报源、回测框架和 AI 量化项目,封装成自己的研究 workflow

普通人用 Codex 写 prompt

高手用 Codex 搭 workflow

非投资建议,只是 AI 投研工具流分享

52

35

148

11,154

May 26

El stack cuantitativo que tomó años a las instituciones construir está sentado en GitHub ahora mismo

5 repositorios. gratis. de código abierto. más útil que cualquier curso

1. freqtrade/freqtrade github.com/freqtrade/freq…

50k estrellas. bot de cripto con un módulo de ML integrado llamado freqai que entrena modelos en datos en vivo, reoptimiza automáticamente, soporta 30 exchanges. integración con Telegram de fábrica. la comunidad ha estado probándolo en batalla desde 2018 y solo la pestaña de issues vale la pena leerla

2. hummingbot/hummingbot github.com/hummingbot/hum…

19k estrellas. motor de market making y arbitraje cross-exchange. maneja colocación de bid/ask, ajuste de spreads e hedging de inventario en 50 CEX y DEX simultáneamente. usado por proveedores de liquidez reales en producción. los docs de arquitectura explican cosas que ningún curso te dirá

3. AI4Finance-Foundation/FinRL github.com/AI4Finance-Fou…

12k estrellas. aprendizaje por refuerzo aplicado al trading. agentes entrenados con PPO, DQN, DDPG en entornos de mercado reales. el repo incluye pipelines de datos de cripto vía API de Binance y CCXT. no es un juguete; investigadores publican papers usando esta base de código

4. nautechsystems/nautilus_trader github.com/nautechsystems…

9k estrellas. Python en la superficie, Rust por debajo. el motor de backtesting es idéntico byte por byte al motor de trading en vivo: lo que pruebas es lo que despliegas. construido para estrategias sensibles a la latencia donde los milisegundos importan

5. ranaroussi/quantstats github.com/ranaroussi/qua…

7k estrellas. biblioteca de analítica de performance. Sharpe, Sortino, Calmar, max drawdown, mapas de calor de retornos mensuales, Monte Carlo: una sola llamada de función genera una hoja de lágrimas completa. la herramienta estándar para evaluar si una estrategia es real o solo suerte

no necesitas un curso para entender cómo funciona el trading sistemático

necesitas leer código escrito por gente que realmente lo hace

8

3

20

736

these 5 repos solve what courses charge 2k for

freqtrade alone covers 80 percent of what gets sold as algotrading. freqai retrains models on live data out of the box

quantstats tells you if your strategy is real or just got lucky on the backtest

nautilus gives you a backtester byte for byte identical to live execution. what you test is what you deploy

hummingbot runs market making across 50 plus venues

finrl ships rl agents trained with ppo and dqn on real market data

people pay thousands to learn what is sitting open source

you do not need a course, you need to read code written by people who actually trade

polymarket.com/?r=vorty279

The quant stack that took institutions years to build is sitting on github right now

5 repositories. free. open source. more useful than any course

1. freqtrade/freqtrade github.com/freqtrade/freqtra…

50k stars. crypto bot with a built-in ml module called freqai trains models on live data, reoptimizes automatically, supports 30 exchanges. telegram integration out of the box. the community has been battle-testing this since 2018 and the issues tab alone is worth reading

2. hummingbot/hummingbot github.com/hummingbot/hummin…

19k stars. market making and cross-exchange arbitrage engine. manages bid/ask placement, spread adjustment, and inventory hedging across 50 cex and dex simultaneously. used by actual liquidity providers in production. the architecture docs explain things no course will tell you

3. AI4Finance-Foundation/FinRL github.com/AI4Finance-Founda…

12k stars. reinforcement learning applied to trading. agents trained with PPO, DQN, DDPG on real market environments. the repo includes crypto data pipelines via binance api and ccxt. not a toy researchers publish papers using this codebase

4. nautechsystems/nautilus_trader github.com/nautechsystems/na…

9k stars. python on the surface, rust underneath. the backtesting engine is byte-for-byte identical to the live trading engine what you test is what you deploy. built for latency-sensitive strategies where milliseconds matter

5. ranaroussi/quantstats github.com/ranaroussi/quants…

7k stars. performance analytics library. sharpe, sortino, calmar, max drawdown, monthly return heatmaps, monte carlo one function call generates a full tearsheet. the standard tool for evaluating whether a strategy is real or just lucky

you don't need a course to understand how systematic trading works

you need to read code written by people who actually do it

11

1

39

1,427

The quant stack that took institutions years to build is sitting on github right now

5 repositories. free. open source. more useful than any course

1. freqtrade/freqtrade github.com/freqtrade/freqtra…

50k stars. crypto bot with a built-in ml module called freqai trains models on live data, reoptimizes automatically, supports 30 exchanges. telegram integration out of the box. the community has been battle-testing this since 2018 and the issues tab alone is worth reading

2. hummingbot/hummingbot github.com/hummingbot/hummin…

19k stars. market making and cross-exchange arbitrage engine. manages bid/ask placement, spread adjustment, and inventory hedging across 50 cex and dex simultaneously. used by actual liquidity providers in production. the architecture docs explain things no course will tell you

3. AI4Finance-Foundation/FinRL github.com/AI4Finance-Founda…

12k stars. reinforcement learning applied to trading. agents trained with PPO, DQN, DDPG on real market environments. the repo includes crypto data pipelines via binance api and ccxt. not a toy researchers publish papers using this codebase

4. nautechsystems/nautilus_trader github.com/nautechsystems/na…

9k stars. python on the surface, rust underneath. the backtesting engine is byte-for-byte identical to the live trading engine what you test is what you deploy. built for latency-sensitive strategies where milliseconds matter

5. ranaroussi/quantstats github.com/ranaroussi/quants…

7k stars. performance analytics library. sharpe, sortino, calmar, max drawdown, monthly return heatmaps, monte carlo one function call generates a full tearsheet. the standard tool for evaluating whether a strategy is real or just lucky

you don't need a course to understand how systematic trading works

you need to read code written by people who actually do it

22

40

243

57,615

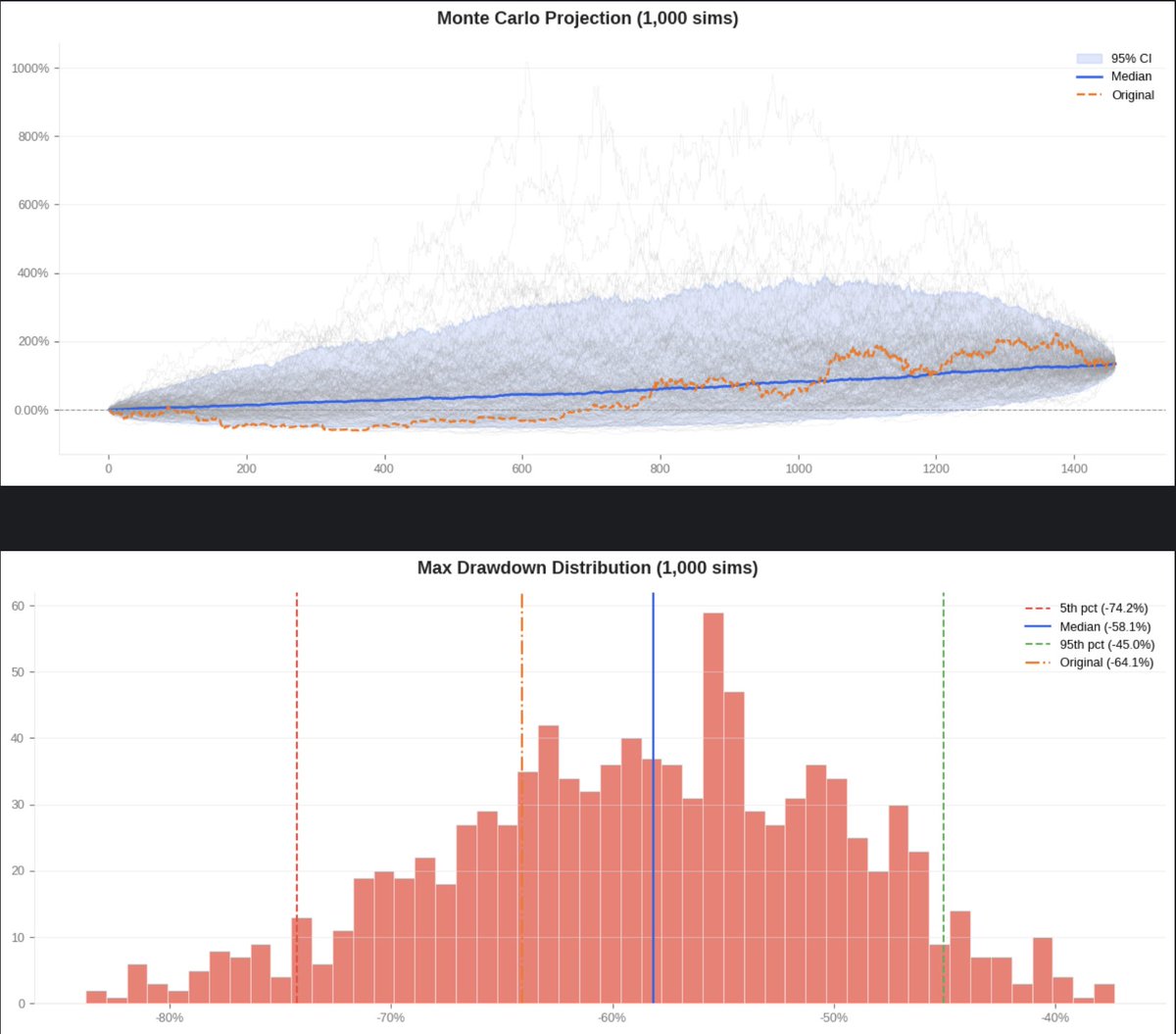

リスク分析しっかりしたい方向けに、quantstatsに倣いkatsustatsもmonte carlo simulationに対応しました

以下のようにmonte_carlo=Trueを渡すだけで使えます

katsustats.reports.html(

returns,

monte_carlo=True,

)

github.com/katsu1110/katsust…

2

22

2,244

こんにちは、日本爆損防止委員会です

愛用していたquantstatsがモダンな環境で動かなくなってしまったので、katsustatsというライブラリを作りました

polarsベースで高速、かつ昔から欲しかった曜日別分析等も含めてます

katsustats⇩

github.com/katsu1110/katsust…

紹介記事⇩

note.com/bakuson_dameyo/n/n4…

1

12

101

7,073

Mar 25

Quantstats

k-dm.work/finance/main/010-q…

例えばこんないいライブラリがあって

import quantstats as qs

この1行でexcel関数のように株式市場を分析できる関数が山盛り使えて(事例は添付サイト参照)、

import yfinance as yfでYahooファイナンスから株価情報を機械的にドサッと集められるので後はむふふ

1

3

167

Mar 17

My 9 favorite GitHub repos (after 13 years of starring them):

• optopsy

• ArcticDB

• quantstats

• zipline-reloaded

• awesome-quant

• OpenBBTerminal

• python-cheatsheet

• alphalens-reloaded

• PythonDataScienceHandbook

1

1

5

1,319

Mar 17

quantstats

Portfolio profiling, in-depth analytics and risk metrics.

github.com/ranaroussi/quants…

1

2

613

Mar 9

퀀트 자동매매 시스템, 아키텍처부터 제대로 짜야 실전에서 안 터진다

백테스트에서 연 수익률 300%가 나와도 실전에서 계좌를 날리는 이유가 뭘까.

시스템 아키텍처, 리스크 관리, 슬리피지 처리, 장애 대응 - 이 "지루한" 부분을 무시했기 때문이다.

업계 표준은 이벤트 기반 아키텍처(EDA)다.

시장 데이터 수신 → 시그널 생성 → 리스크 검증 → 주문 실행이 이벤트 버스로 느슨하게 연결된다.

덕분에 백테스트와 라이브 트레이딩을 동일한 코드로 돌릴 수 있다.

팩터 전략도 마찬가지다.

모멘텀(12-1개월)과 밸류(PBR) 팩터를 결합하면 상관관계가 낮아져 리스크 분산 효과가 생긴다.

단, 반드시 피해야 할 함정이 있다.

① 생존 편향 - 현재 상장 종목만 쓰면 수익률 과대추정

② 미래 정보 참조 - 리밸런싱 시점에 미래 데이터가 살짝 들어가는 것만으로도 결과 왜곡

③ 거래비용·슬리피지 무시 - 백테스트 수익률이 실전에서 반토막 나는 주범

④ 모멘텀 크래시 - 시장 급반전 시 모멘텀 전략 급락, 밸류 팩터로 헤지 필요

실용 스택: pykrx(한국 주식 데이터) VectorBT(Rust 코어, 초당 500만 행 처리) QuantStats(성과 리포트)

피지컬 AI 관점에서 보면, 2026년은 로봇·자율주행 섹터가 소프트웨어 AI에서 하드웨어 AI로 투자 트렌드가 이동하는 전환점이다.

한국도 기술·규제·시장 세 축이 동시에 맞물리기 시작했다.

자동매매 전략을 짤 때 이 섹터 로테이션까지 반영하면 알파를 더 뽑아낼 수 있다.

데이터로 의사결정하는 것이 퀀트의 본질.

감이 아니라 코드로 검증한 전략만 살아남는다.

🐶🐾💕

@miwoooo

1

2

52

Feb 27

Backtesting Before LLMs vs Backtesting in the Agentic Era

Backtesting Before LLMs

Write data fetching code

Debug indicator libraries

Build signal generation logic

Wire up portfolio simulation

Add realistic brokerage fees

Fetch benchmark data separately

Build comparison tables from scratch

Create Plotly charts manually

Optimize parameters with nested loops

Generate QuantStats tearsheets

Then repeat everything when you change one idea

Easily 2 to 3 days of coding for a single strategy comparison.

Backtesting in the Agentic Era

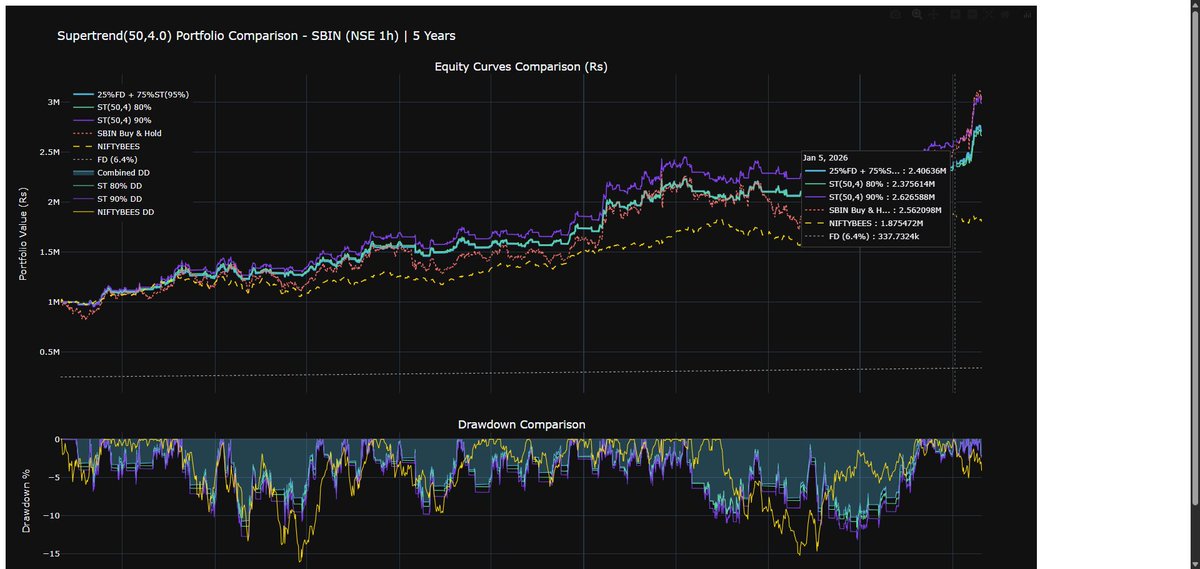

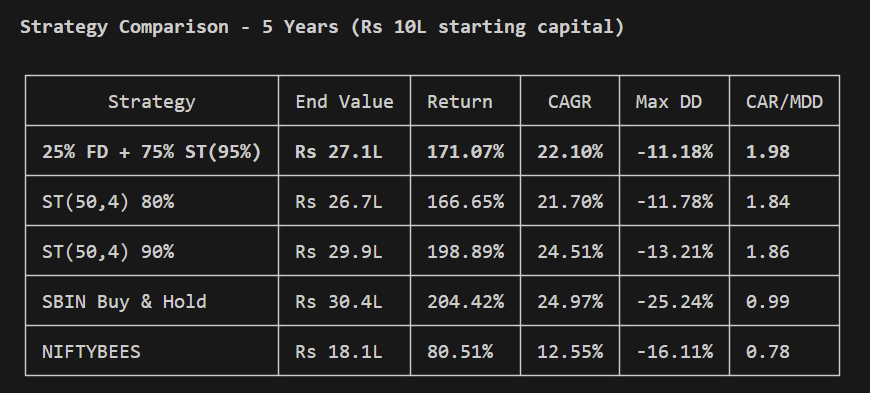

"I want 25% in FD and 75% in Supertrend. Compare it with Buy & Hold and NIFTYBEES."

That is the prompt.

Parameter optimization, equity curves, drawdown charts, comparison tables, tearsheets. All generated in a conversation.

The hardest part of quant trading was never the ideas. It was the engineering overhead that killed most ideas before they could even be tested.

Tools like Claude Code VectorBT skills are removing that barrier entirely.

The future of quant trading is faster iteration, lower friction, and more ideas tested, not just better models.

#ClaudeCode #VectorBT #Backtesting #Python

2

3

79

5,791

Feb 27

VectorBT Skills Updated:

Updated Support for Indian, US Markets, Crypto and Costing too Market Specific.

Also added Quantstats Tearsheets support.

Now use /setup to run the complete setup environment.

that will solve the painful effort of setting up the environment for backtesting.

Feb 25

Install your backtesting skills simply using the command

npx skills add marketcalls/vectorbt-backtesting-skills

Ensure openalgo is running connected with your broker.

and start making a conversation and build a trading strategy that is in your mind for quite some time.

1

2

30

3,351

It was actually very fast with Claude Code - I mean, just a few hours (I linked my own CSV database). Claude Code converted my strategy into the framework on the first attempt. It used QuantStats for the stats, and I had it modify the output for my needs. I was surprised by how smooth it was. But I haven’t automated the trading itself - just the backtest on historical data.

4

675

Feb 10

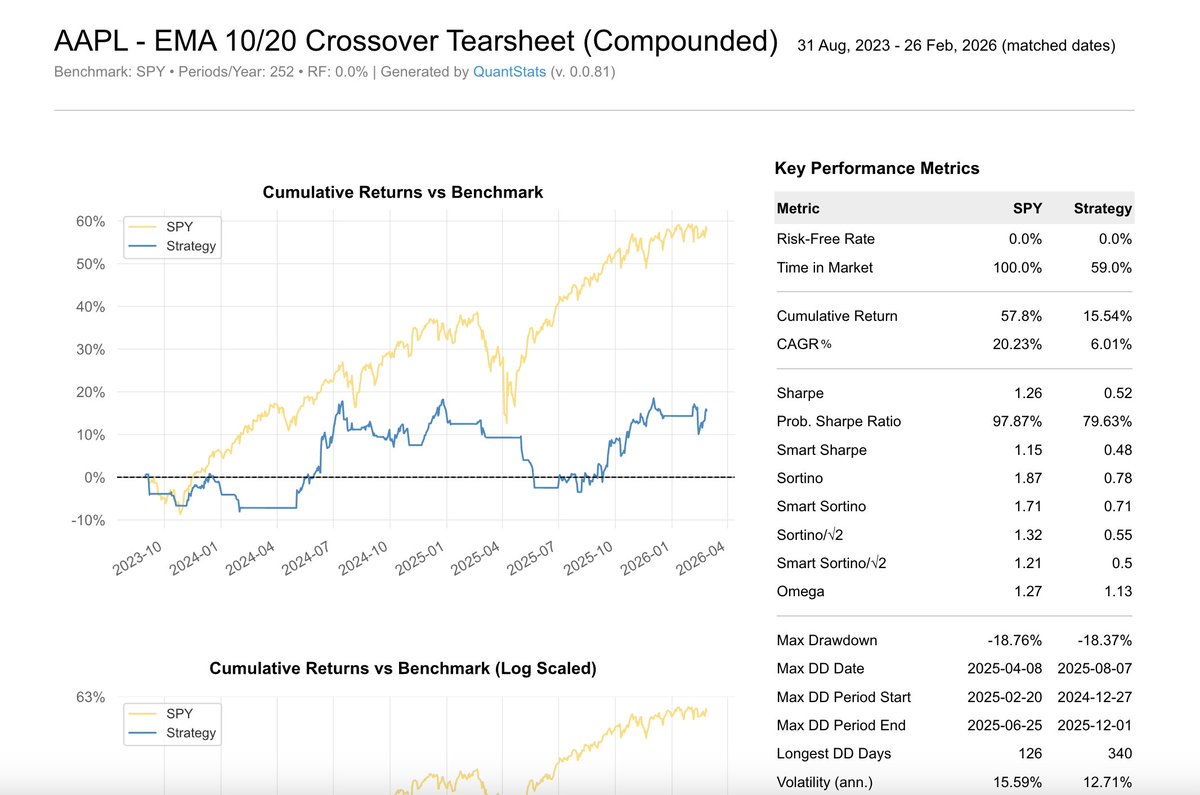

We'll use QuantStats to generate performance and risk statistics.

Use the strategy returns and the rolling futures strategy as the benchmark.

Let's see how well it did!

1

1

581

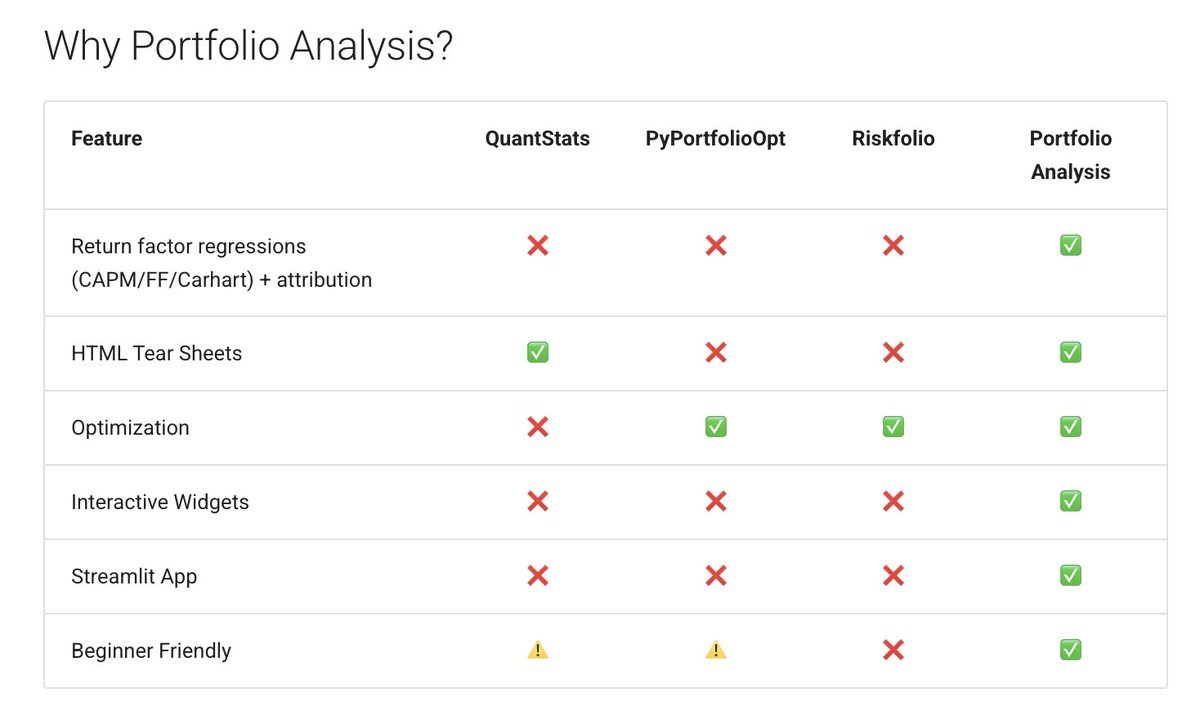

Huge respect for QuantStats, PyPortfolioOpt, and Riskfolio, all excellent packages. I built Portfolio Analysis to help fill a few gaps: factor regressions attribution (CAPM/FF/Carhart), interactive widgets, a Streamlit app, and a more beginner-friendly workflow.

Sharing the comparison chart 👇

What would you like to see next?

Source: engineerinvestor.github.io/P…

2

2

276

Hey Ran, how are you doing?

The Solana community has really come together to support the funding/sponsorship you mentioned needing for keeping yfinance and quantstats going on!

Quick explainer for context: Bags.app (bags.fm) is a super popular mobile-first Solana-native platform/app where anyone can easily launch, trade, discover, and earn from memecoins/tokens.

It's like a creator-focused launchpad that lets people create tokens in seconds, trade them with friends, find trending ones, and — crucially — automatically route transaction fees/royalties back to the original creators (even artists or non-crypto folks).

Creators are earning huge passive income from these fees — some tokens on Bags have pushed millions in total creator earnings already (e.g., $21M distributed platform-wide, with individual launches hitting big numbers via "Income Assignment" features).

And we choose to help you! Check DM's and Patreon when you can!

bags.fm/8fYEKoWFf2ySykDK2mA5…

1

2

15

1,160

Jan 13

Fyi: I (and @claudeai) just shipped QuantStats v0.0.78 🚀

Modernized for 2026 (Python 3.10 , pandas 2.x, numpy 2.x), 12 bug fixes from community feedback, and a new Monte Carlo simulation module to stress-test your strategies.

50 metrics. Beautiful tearsheets. One pip install.

🔗 github.com/ranaroussi/quants…

1

1

4

819