Apr 22

“The ideal business is one that earns very high returns on capital and can keep using lots of capital at those high returns. That becomes a compounding machine. If you can put $100 million into a business that earns 20% on capital, ideally it would be able to earn 20% on $120 million the following year, $144 million the following year, and so on. You could keep redeploying capital at these same returns over time.

But there are very, very, very few businesses like that. We look for them, but they don't exist."

- Warren Buffett, 2003 Meeting

open.substack.com/pub/cannib…

$TOI.V $TOITF $CSU.TO $CNSWF $LMN.V $LMNXF

1

2

575

Apr 21

My name is Sandro. I run Cannibal Stocks.

You know my style. I buy hated companies in hated industries. Alpha Metallurgical Resources at 1.3 billion in free cash flow on a 2 billion market cap. Transocean at about 25 cents on the dollar of replacement value. Ugly cheap. So cheap that even if I am wrong about everything else the price saves me.

So when I tell you I just bought a stock at 123 times earnings you should probably check if someone hacked my account. 🙂

Full Write up: open.substack.com/pub/cannib…

$TOI.V $TOITF $CSU.TO $CNSWF $LMN.V $LMNXF

1

6

648

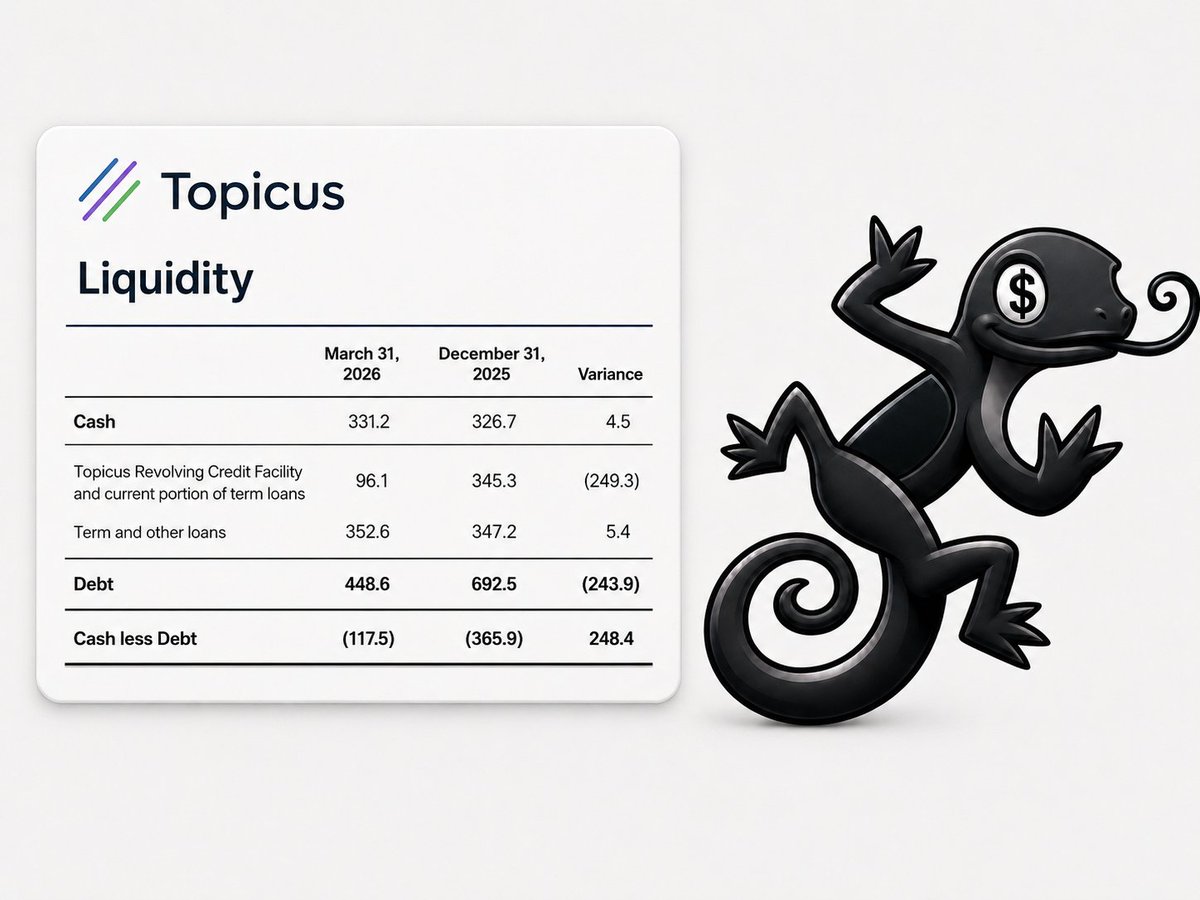

Apr 13

Constellation fell 50 percent. From 5,300 dollars to 2,300. Billions in market value gone. Other software names fell 70 percent or more.

Thirty years of compounding. And half of it erased in months.

Now here is where most people stop thinking. The stock is down. The founder is gone. AI is coming. Sell everything.

But stop for a second... $csu.to $toi.v $toitf $lmgif

cannibalstocks.substack.com/…

4

466

Apr 11

Chris Mayer of 100 Baggers book fame rarely does podcasts. Pretty sure this one with @DrewCohenMoney is his first in several months and for 2026.

$DUOL investors might not like hearing that he suggested it could be the next Peloton!

$CSU $CSU.TO $CNSWF Constellation Software stock, he seemed to remain just as bullish on it in the post Mark Leonard era. Expecting FCF to "at least" 2x over next 5 years.

Though he did say he found the "daughters" Lumine Group $LMN $LMN.V $LMGIF and Topicus $TOI $TOI.V $TOITF more attractive right now from current valuation and future growth perspectives.

Was a bit surprised to hear he sold Dino Polska $DNOPY $DNOPF $DNP.WA. His cited reason of not liking the fact the founder and largest shareholder doesn't talk to anyone, that's certainly not a new thing, so using as reason to sell now didn't make much sense to me.

I'm thinking poor stock performance subconsciously made him look for things he didn't like. To be clear we are all guilty of this, so I'm not picking on him. I do it too.

I say this because if you look at metrics, what we've seen is a valuation compression - attachments from @gurufocus @GurufocusC. Dino's growth has been not just fine, but phenomenal.

As someone who, as previously documented, went through probably 100k shares of $ODFL the past couple years, I was really hoping to hear why he sold Old Dominion but didn't hear that one brought up. I'm not selling!

He did sell out of Evolution AB $EVO $EVVTY $EVGGF and similar to Dino Polska, I didn't find the reason super compelling. Yes he cited capital allocation choice and finally, they're doing buybacks vs. dividends now but still, this is another stock where so much of it is sentiment driven I believe.

I've always said the reason to not own Evolution is more to do with ethics, as it's not exactly making the world a better place. Then again, same can be said about so many industries, including social media (does more harm than good IMO).

I highly recommend you listen to the full episode here: youtu.be/pidvgNGFkew

Thanks to Drew for posting it a little earlier so I could listen to it at the gym Wednesday. Almost 90 mins so perfect for that.

10

7

124

16,113

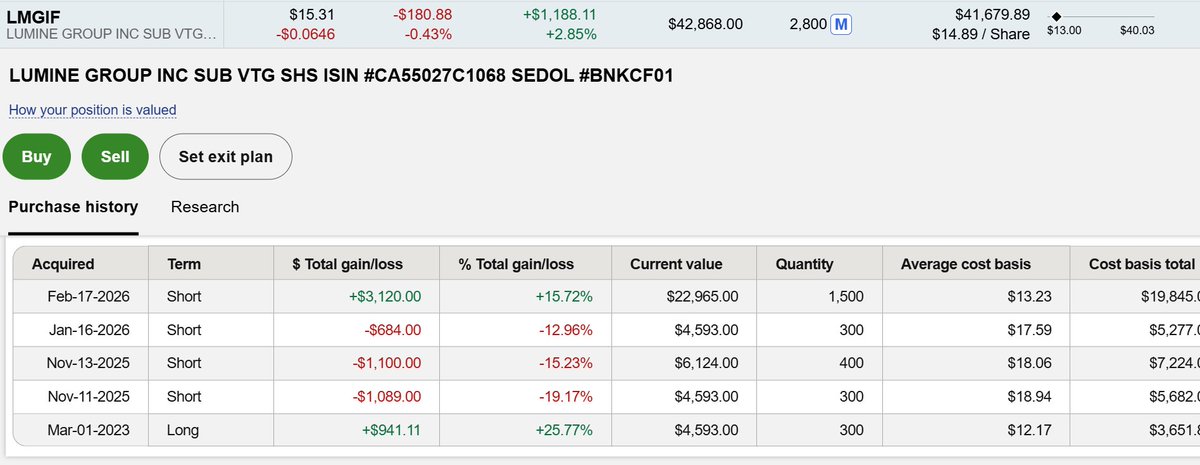

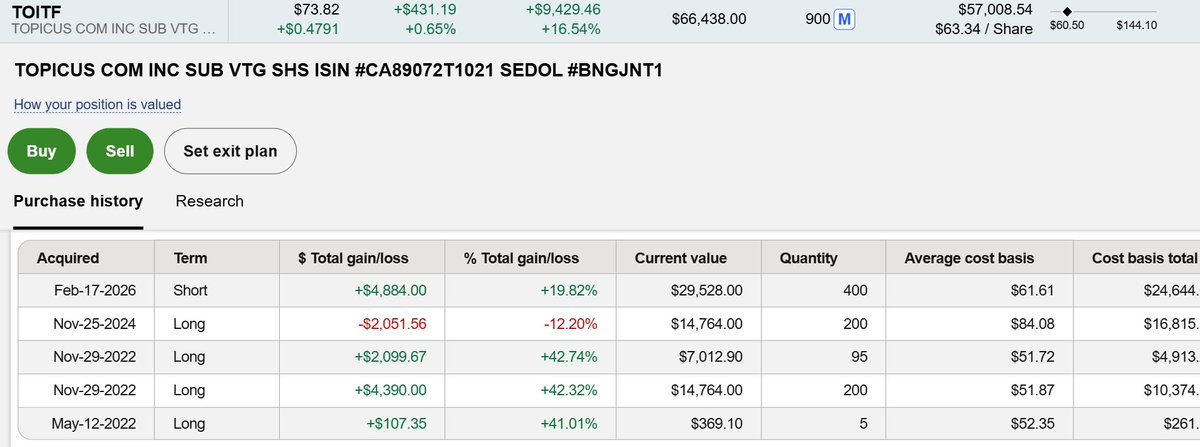

Mark Leonard mothership and his children...

Nice to see Constellation Software $CSU $CSU.TO $CNSWF up 20% off its low last month. I will keep my 100 newest shares in the $1,600-$1,700s and sell the 100 highest cost after further recovery.

Lumine Group $LMN.V $LMGIF, fortunately my final buy was the biggest, which offsets my unrealized losses from my November 2025 adds.

Similar for Topicus $TOI $TOI.V $TOITF stock. I always try to save the biggest buy for the most hopeless feeling day.

Has anyone heard any updates on Mark? Like I said, I think he's dying. Just being realistic. A founder like him would not flee in such a way, with zero communication during/after and zero transition period, unless it were a very grim prognosis.

4

38

6,543

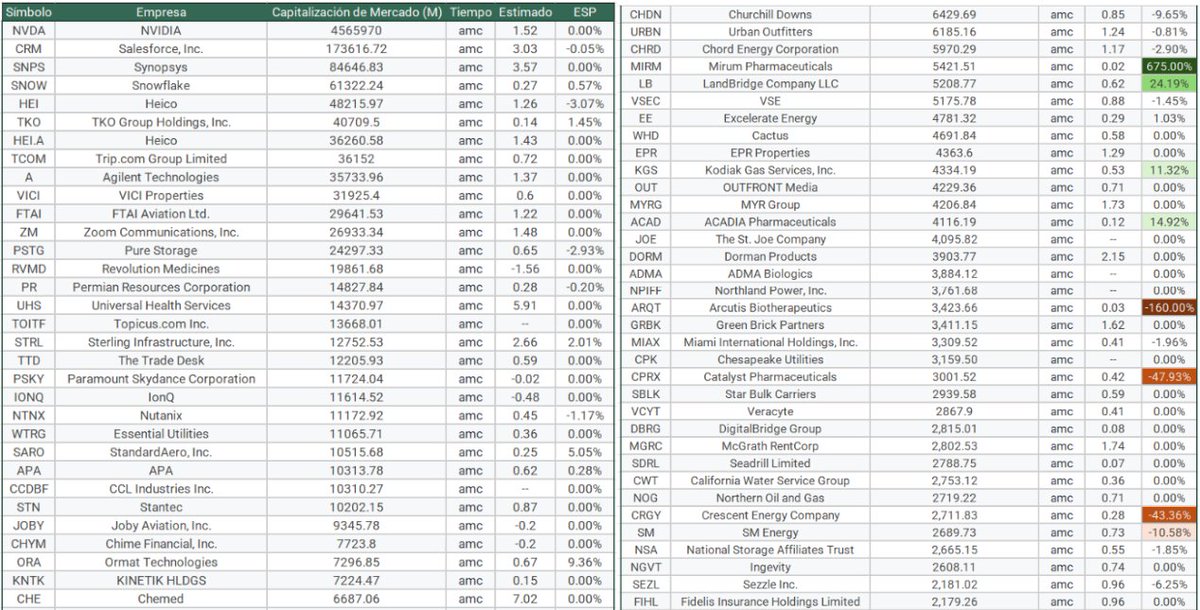

Feb 25

Presentación de resultados MIÉRCOLES después de cierre de mercado👇

$NVDA $CRM $SNPS $SNOW $HEI $TKO $HEI.A $TCOM $A $VICI $FTAI $ZM $PSTG $RVMD $PR $UHS $TOITF $STRL $TTD $PSKY $IONQ $NTNX $WTRG $SARO $APA $ARQT $CPRX $NOG

¡Decirnos en comentarios si estáis interesados en alguna empresa y os pasamos un análisis detallado por privado! 💡

#Earnings #OptionsTrading #ESP

4

465

Feb 20

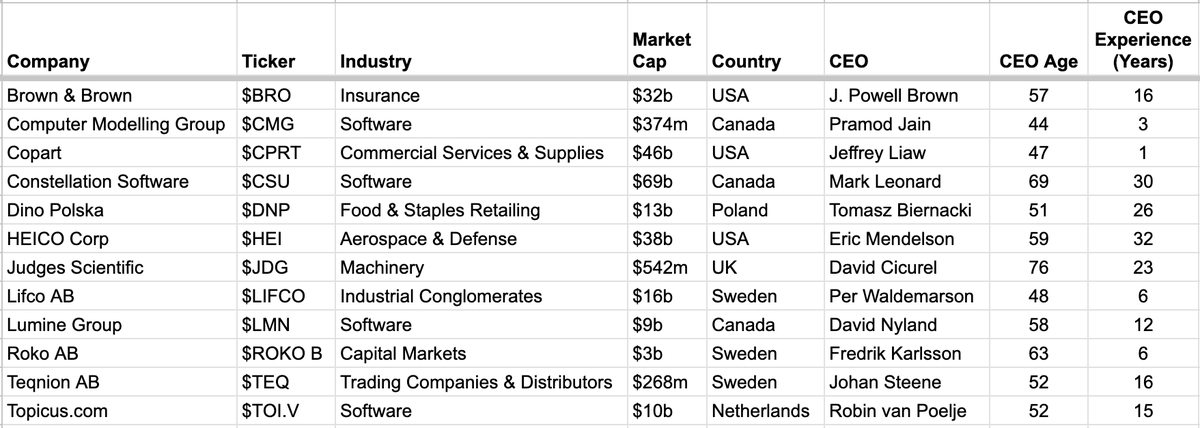

Before talking about Copart $CPRT earnings, let's talk about Chris Mayer of 100 Baggers book fame.

Latest public data for portfolio - Woodlock Family Capital - was revealed on a Swedish podcast in July of last year. It's the attached list of 12 stocks:

1. $BRO

2. $CMG.TO / $CMDXF

3. $CPRT

4. $CSU / $CSU.TO / $CNSWF

5. $DNP.WA / $DNOPY / $DNOPF

6. $HEI / $HEIA

7. $JDG.L

8. $LIFCO / $LFCBY / $LFABF

9. $LMN.V / $LMGIF

10. $ROKO.AB / $ROKOF

11. $TEQ.ST

12. $TOI / $TOI.V / $TOITF

Almost all of these stocks have had substantial declines within the past several months.

If equal weighted, I wouldn't be surprised if it's up to a 40-50% decline from their highs of 2025. I mean, we can even assume $CSU is a heavy weighting and that one is more than a 50% plunge since last year's high.

Tried getting Grok to calculate exact return with assumption of equal weighting as of 7-15-2025, but it got lazy on the foreign stocks and refused.

Noticeably absent is $ODFL. As previously discussed, I went through tens of thousands of shares last year so I know the price action exactly. I'm holding 1k shares at $126 from November and now it's around $200. Who knows exactly where Chris sold but he probably missed at least a 25% gain. Selling out anytime in most of 2025 was a mistake, even if you did want out.

On the bright side, about the only winner here is $HEI Heico. However, no way that can offset the fact that many/most of these names have been chopped in half.

What's the lesson here?

Investing isn't about being academically correct. This is the same reason Michael Burry's returns blow, even if he is right [eventually] on many of his bets.

Because timing is just as, if not more important, than being right or wrong.

You don't have to agree with the market, but I do think it's a mistake to totally avoid exposure to numerous sectors and themes simply because you don't agree with them for whatever reason (overhyped, overvalued, etc.).

Even if the market is wrong, your "correct" prediction may not come true for many years. Perhaps hundreds of percent later.

Or it may not come true at all, as America has uncanny success at papering over one bubble with another to keep the pyramid scheme going.

So many sector cycles are 5-15 years. You can invest in great long term multi-decade winners (which beat the S&P long term) but experience sideways chop for several years if their sector is out of favor, as their valuations go wildly in both directions. Even if underlying fundamentals are growing that entire time.

So they may underperform for 5 years, then outperform the next 5 as an example.

In fact, a lot of big names today like $MA, $SPGI, $AMZN, $INTU, $MELI etc. may fit that bill. Their 3 or 5-year charts may be disasters but overlay with fundamentals for true story.

With the exception of couple of Chris Mayer's holdings I've discussed disliking before, overall I love his stocks. However, I hate how correlated they are.

Now you may look at the industries they are in and the foreign exposure and argue, how can that be correlated?

Well, it's very uncorrelated to the S&P. That's how.

- Not much large cap, no mega cap.

- No trending themes like AI.

- No US winners, with foreign focus on Europe and Canada only.

Yes, I know why he loves Sweden and also why he chose most of these. This fund would likely outperform US in bear market or AI-bust scenario, so I'm not saying the story is finished by any means.

However, if you don't want gut-wrenching 40-50% drawdowns, you have to own some stuff correlating with S&P.

Same reason why a portfolio of all X stocks is so painful right now, while S&P is near ATH.

At any given time, the market is a rolling bubble of overvalued themes contrasted with undervalued themes.

When you own the whole market, you own both over and undervalued, which is why it's smoother ride.

The problem is, everything except for $HEI here is within an underperforming theme right now. That's why it's so painful, for now.

I think his portfolio will recover and do great long term, but personally, I would not want all or a high percentage of my net worth in holdings like this.

I like having diverse exposure to my favorite stocks in each industry, because I know each will get their turn at being in and out of favor.

Some spice is nice too, because then you don't get FOMO when say, you see $RKLB or $X (SpaceX) going to the moon. I own both of those as you may know, even though they are egregiously overvalued.

Rather than sell on overvaluation, I prefer to just *hold* unless the business thesis has materially and permanently changed (or seems to have). If not, I'll just hold through the boom-bust-boom.

As far as Copart $CPRT earnings, not going to say anything until after I listen to earnings call and evaluate.

23

14

178

25,887

Jan 18

6

1

76

19,971

Jan 16

Simplicity and expertise are two key reasons I believe businesses and other organizations will continue largely to rely on software from $CSU and $TOI.V rather than build their own.

It is simpler for businesses to purchase software than build and manage it internally. Even if AI makes it easier than it is currently to build software, purchasing it will still be the simplest option. Furthermore, security patches and long-term maintenance will still be headaches for internally built software even with the help of AI.

$CSU and $TOI.V have expertise that other businesses lack. They focus solely on vertical market software (VMS). A business that builds its own software will lack the depth of expertise and experience in building and managing VMS. The result would be software that lacks feature parity as compared to software offered by Constellation and Topicus.

Cloud computing is one example of how businesses value simplicity and expertise. Many businesses could host their own servers and do everything internally, but many choose to use cloud service providers instead for simplicity and the expertise that they provide. Many businesses use outside accounting agencies and law firms for similar reasons even though both functions could be performed internally.

This is not financial advice. This is just my opinion.

I am long $CNSWF and $TOITF.

1

9

1,361

10 Dec 2025

And another acquisition for Topicus. $TOITF.🎯

This time in Romania, first time. 🔥

Typical acquisition when it comes to crucial software. 👍🏻

1

1

24

5,425