May 30

#SME #Techera #TecheraEngineering

Techera Engineering H2 FY26 Concall Highlights

👉 FY27 & Future Outlook:

▫️ FY26 was positioned as a year of capacity and capability building despite the significant revenue impact from the lost Turkish Aerospace contract.

💠Management views it as a temporary geopolitical setback and remains focused on sustainable long-term value creation

💠 Guidance: 30-40% YoY revenue growth expected for FY27 with PAT margins targeted above 10%.

💠Mr. Nimesh although looking unaware at times during the call; expressed optimism, noting that FY27 should mark a return to a upward trajectory, with the team’s enhanced skill levels supporting higher output with only ~20% manpower increase)

💠Full-year revenue is expected to comfortably cross previous levels (targeting 75-80 Cr ), with H1/H2 improvements from new order execution and diversification.

👉 Notable Points:

▫️ Turkish Contract Impact:

💠Signed 110 Cr (5-year) deal for commercial components (~20 Cr annual).

💠Eight months of development, fixtures/jigs, and machine orders completed before communications ceased post-Operation Sindoor (May 2025 geopolitical event with Turkey-Pakistan angle).

💠Despite repeated follow-ups and even MOD outreach, it was written off, causing a major revenue shortfall vs. 40% growth expectations.

💠Management noted efforts to route indirectly but prioritized consolidation and profitability preservation.

💠Lessons: Diversify aggressively; they successfully offset partially through quick pivots to other customers.

▫️ Financial & Operational Notes:

💠Promoter stake sales (Dec/Mar) were for personal debt resolution — no plans for further dilution or primary raises that erode stakes

💠Emphasis on building investor confidence via execution.

💠Interest default was a short-term working capital timing mismatch (paid May after March due date), regularized promptly.

💠Expensive 15% NCD targeted for closure by September; average borrowing cost ~8-8.5%.

💠Significant capex (~100-125 Cr range referenced) already deployed — no major additional capex needed for at least 1-1.5 years; focus on monetizing existing assets.

💠Inventory/receivables rose due to new project ramp-up post-Turkish realization (Q4 was stronger; collections on track within 90-day cycle).

▫️ Revenue was ~70-75% aerospace/defense with new clients added.

💠Management addressed investor concerns on guidance realism, margin fluctuations (not seen as structural), and positioning for defense indigenization and HAL/IAF scale

👉 Order Book / Projects and Future Pipeline:

▫️ Current Order Book: ~46-47 Cr in hand, with ~40 Cr executable in FY27 (remaining 7-8 Cr spread over 1-2 years).

💠This is described as meaningfully higher than at the start of FY26.

▫️ Key Executing / Secured Projects:

💠Private aircraft OEM tooling set: Order received, design completed, manufacturing underway — full delivery targeted by September 2026.

💠Significant milestone as the company will be the sole provider of a complete aerospace tooling set for the aircraft, with involvement from National Aeronautical Laboratories.

💠HAL Insourcing: Already assembling sub-assemblies in HAL’s plant for over six months.

💠Tenders submitted for additional projects (expected decision within 60 days), enabling 20-30% more manpower utilization.

▫️Includes full HTT-40 aircraft assembly and vertical fin components (outsourced model).

💠Initial work under Techera brand; potential shift of larger components to Nashik subsidiary later based on HAL’s strategic decision for scale.

▫️IAF: Certified as authorized vendor for ground support equipment (GSE) across multiple platforms (e.g., Rafale, Tejas, and others).

💠This opens a major indigenization opportunity. RFQs received; first orders and 5-year supply licenses anticipated in 2-3 months.

▫️ Pipeline & Outlook:

💠170-180 Cr worth of RFQs/quotations already submitted and under discussion.

💠Expect 30-40 Cr additional orders in the next 4-5 months.

💠New customer acquisition (now 10-15 active aerospace/defense clients) and pilot projects are building momentum.

💠Revenue mix: 70-75% from aerospace & defense. Within aerospace, FY26 was tooling-heavy; FY27 shift expected toward MRO (potentially 1), followed by tooling and GSE.

💠International funnels and non-India customers also being developed.

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

2

5

22

5,274

Apr 22

India’s aerospace ecosystem is shifting from

support role → global manufacturing MRO hub

This is a long-duration, compounding opportunity

hidden inside a highly regulated ecosystem.

Early stage. Underfollowed. High barriers.

India is becoming one of the fastest-growing aviation markets globally. Fleet size is expected to more than double over the next decade.

Large orders from IndiGo, Air India, and Akasa Air are not just airline news; they are a multi-year revenue pipeline for maintenance, repairs & components.

At the same time, defence policy is undergoing a structural shift.

Import restrictions “Make in India” push are redirecting billions of dollars from global OEMs to domestic suppliers.

This is not cyclical. It’s policy-driven.

Add to that:

GST on MRO cut from 18% → 5%

100% FDI allowed

Easier infra access at airports

The intent is clear: build India into a global MRO aerospace hub, and the economics are compelling:

India offers

1. Skilled engineering talent

2. At significantly lower cost than global hubs

Making it globally competitive in labour-intensive aerospace work

The numbers reflect this shift:

MRO market: ~$1.7B → $4–7B over the next decade

Aerospace & defence: ~$26B → $48B by 2032

Growing faster than global averages.

But this is NOT a commodity industry.

Entry barriers are massive:

1. Certifications (DGCA, FAA, EASA, CEMILAC) take years

2. Switching costs are high (downtime = huge losses)

3. Requires heavy infra (hangars, tooling, testing systems)

---> Once a company enters the ecosystem, it tends to stay embedded

And this is where it gets interesting

India now has a set of emerging, highly specialized listed players across this value chain:

India Aerospace Value Chain (Listed Small Caps)

Precision Manufacturing & Components

Aequs Limited → integrated aerospace ecosystem (SEZ-led model)

Unimech Aerospace & Manufacturing Limited → high-precision tooling & assemblies

MTAR Technologies Limited → precision manufacturing for aerospace & defence

Electronics, Avionics & Subsystems

Rossell Techsys Limited → deep relationship with Boeing

DCX Systems Limited → harnesses & electronic subsystems

Paras Defence and Space Technologies Limited → optics, space & defence electronics

Astra Microwave Products Limited → radar & RF systems

Apollo Micro Systems Limited → embedded avionics systems

Sigma Advanced Systems Limited → electronic warfare & avionics

Tooling, Integration & Engineering Systems

TechEra Engineering (India) Limited → precision tooling MRO equipment

CFF Fluid Control Limited → fluid systems for aerospace/defence

MRO, Systems & Infrastructure

Sika Interplant Systems Limited → defence MRO system upgrades

Taneja Aerospace & Aviation Limited → owns rare private airfield infra

Specialized Inputs & Critical Components

Premier Explosives Limited → propellants & aerospace chemicals

High Energy Batteries (India) Limited → aerospace & defence batteries

India’s aerospace opportunity is not a single-company story; it’s a full-stack ecosystem spanning tooling, electronics, MRO, and precision manufacturing

#Aequs #RossellTechsys #UnimechAerospace #SikaInterplant #TanejaAerospace #DCXSystems #TechEraEngineering #MTARTechnologies #ParasDefence #AstraMicrowave #ApolloMicroSystems

#SigmaAdvancedSystems #CFFFluidControl #PremierExplosives #Aerospace

#Defence

#MRO #HighEnergyBatteries. .

1

10

1,088

Apr 13

Techera Engineering was exhibiting in Aero Defence Expo in New Delhi last week.

I took the opportunity to visit the Expo, and decided to share my views based on in-person experience and discussions with Techera's Management.

#Techera #TecheraEngineering

3

25

4,135

Apr 13

#Orders Snapshot – Apr 13, 2026

✅ #TecheraEngineering – ₹1.60 Cr

Defence order for fuselage assembly jig work

🕒 Duration: By Oct 7, 2026

✅ #EnviroInfra – ₹972.19 Cr

LoEs for 2 EPC sewage projects in Maharashtra

🕒 Duration: 24 months

✅ #GHVInfra – ₹1,250 Cr

EPC contract for Jalna–Nanded expressway connectors

🕒 Duration: 30 months

🔔 Real-time stock alerts on WhatsApp → finq.in

2

19

1,209

Mar 22

#MarketsWithMC | आशीष कचोलिया ने दो नए स्टॉक्स को अपने पोर्टफोलियो में जगह दी है तो दो में होल्डिंग हल्की की है और दो में होल्डिंग बढ़ाई है। चेक करें इन सभी स्टॉक्स की लिस्ट और लेटेस्ट होल्डिंग

hindi.moneycontrol.com/news/…

#AshishKacholia #Stockstowatch #TechEraEngineering #moneycontrol

2

216

Mar 19

#TecheraEngineering – Order Update

✅ ₹9.76 Cr

Design & manufacturing order (domestic client)

🕒 Duration: 12 months

4

360

Jan 25

Many Stocks look juicy. My watch list & PF includes:-

#QualityPower @ 590

#TirupatiForge @ 33

#SammanCapital @ 138

#Pacedigitek @ 168

#RainIndustries @ 138

#NaclIndustries @ 158

#ABSMarines @ 175

#TecheraEngineering @ 186

#Himatsingka @ 98

Not saying they can't fall more. But 👀

1

4

2,217

11 Nov 2025

#SME #Techera #TecheraEngineering

Techera Engineering H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️Re-iterated a minimum growth guidance of 30-40% for FY26, with optimism for FY27

💠Revenue ramp-up is expected in H2 (typically 30% in H1 and 70% in H2), driven by capital goods purchasing from December onwards in automation

💠Current capacity supports peak revenue potential ~120cr

▫️Gross margins for H1 FY26 stood at 71-72%, expected to be maintained for the full year

💠EBITDA margins are currently at 18-20%, projected to improve to 22-23% in H2 due to operating leverage, stabilized employee costs (no further acceleration for 12-18 months), and reduced employee expenses as a percentage of revenue

💠Other operating expenditures are expected to remain stable at 25-27%

💠Blended EBITDA margins at ~22% plus/minus over the next couple of years

💠Employee headcount (currently 200 ) is sufficient for 70-100cr of revenue without major additions

💠Depreciation impact to rise in H2 as new machinery fully operational

👉Order book / projects and pipeline:

▫️Current order book : ~40cr

💠Split across multiple sectors (insourcing, flying parts manufacturing, tooling, and ground support equipment)

💠Timelines vary: 2 months for some orders, up to 2-4 years for flying parts

💠One additional ~15cr order (for flying parts manufacturing, valid till 2030) is on hold due to geopolitical issues but remains optimistic.

💠~84% of H1 revenue from defense/aerospace, expected to reduce to ~60% in FY26 with automation growth

▫️Entry into space/satellite: Tooling supply to Skyroot Aerospace (announced recently; promoters from ISRO); groundwork for ISRO/DRDO equipment.

▫️Automation: Projects with Godrej (across divisions like aerospace/security) and Safran (testing equipment for Singapore export, delivery in ~15 days); entering AI/camera-based systems

▫️Flying Parts: Shift to long-term contracts (5-10 years commercial, 2-4 years defense); initial focus on structural components, progressing to titanium/special alloys

▫️Other: Remanufacturing for C-295; ground support equipment and MRO

▫️NADCAP certification targeted in ~12 months for Airbus/Boeing qualification (need substitute machines, chemical processes development); delaying engagement until fully ready

▫️Pipeline: ~120-130cr quoted

💠With 50-60% from PSUs (defense/aerospace) and rest from automation/commercial/private

💠Historical win rate: 40-50% (up to 90% in some cases post-RFQ)

💠Potential US opportunities via Techera USA Inc. (discussions with Pratt & Whitney, GE)

c

💠Planning ahead for defense ramp-ups (e.g., SJ-100 in 2 years); potential fundraising/expansion in 6-8 months based on order mix. Supplier development via project to build ecosystem

👉 Others :

▫️No dilution due to delayed delivery from HAL for Tejas Project

▫️Strategy: Emphasis on high-value contracts in defense aviation and industrial automation

💠Groundwork from FY25 capex (plant/machinery for defense/aerospace) validating strategy despite short-term higher finance costs

💠Bifurcation of H1 revenue: Primarily tooling design/manufacturing, followed by MRO, ground support, and emerging flying parts (expected to rise to 2nd/3rd place in 2 years)

💠Long term vision to move from project-based (low repeat) to sticky flying parts for stable monthly revenue. Diversified segments (no single dominance; tooling critical and growing). Open to tech tie-ups if fast-converting (avoid crowded areas like drones)

▫️Challenges: Working capital strains in H1 due to advance requirements (~40-50% of order value for ~40cr orders, e.g., SLB project); no payment delays from PSUs (prompt payers)

💠Sufficient capitalization for FY26 growth; minor challenges non-critical

💠Subsidiary acquired 24 months ago for coaxial motors/tech synergy but exited at profitable price due to slower progress vs. expectations (Not into focus anymore)

3

18

3,975

16 Oct 2025

TECHERA ENGINEERING (INDIA) PARTNERS IN INAUGURATION OF HAL'S NEW LCA MK1A & HTT-40 FACILITIES

🇮🇳 Played key MSME partner role in India’s indigenous defence manufacturing at HAL’s Nashik production unit inauguration.

✈️ HAL’s new plant boosts Light Combat Aircraft (LCA) MK1A & HTT-40 production capacity, strengthening national security & defence sector growth.

🔧 Techera’s precision engineering supports advanced aerospace manufacturing and ‘Make in India’ initiatives.

#TecheraEngineering

283

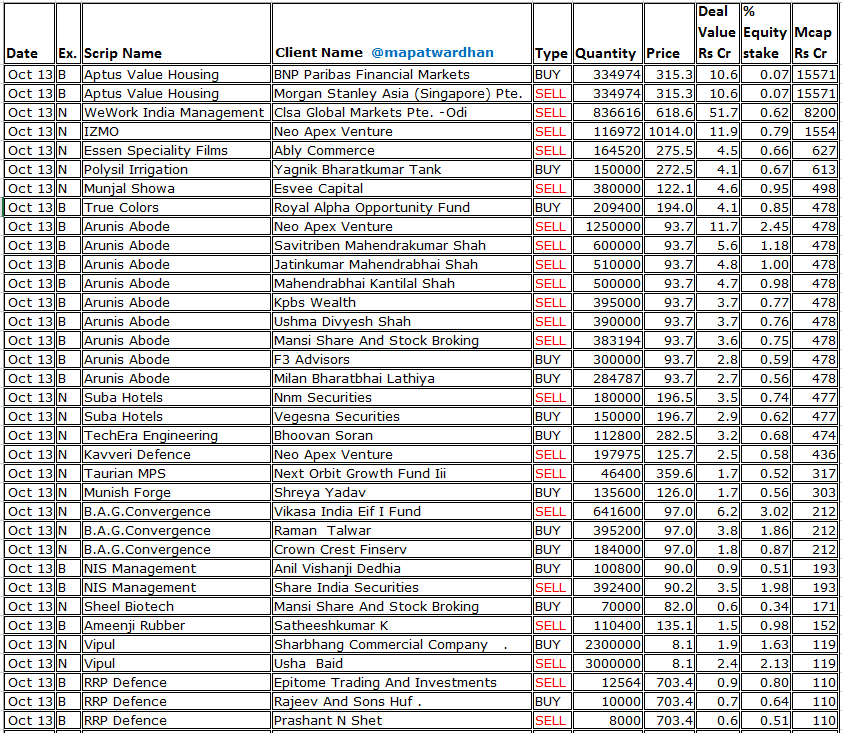

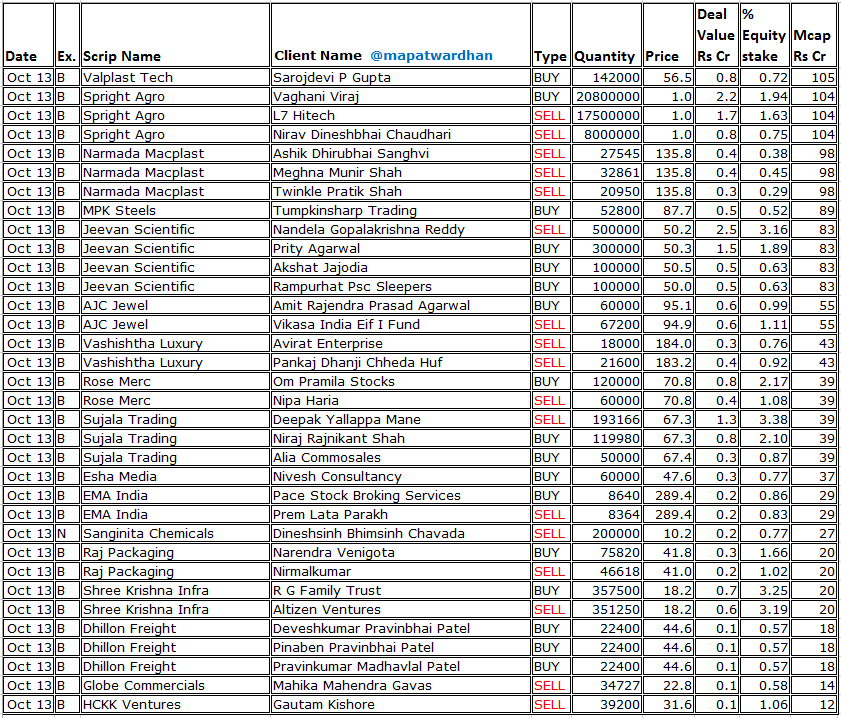

13 Oct 2025

*Today's bulk / block deals*

#AptusValue #WeWork #IZMO #EssenSpeciality #PolysilIrrigation #MunjalShowa #ArunisAbode #TrudeColors #SubaHotels #TechEraEngineering #KavveriDefence #TaurianMPS #BagDigital #NISManagement #SheelBiotech #AmeenjiRubber #Vipul #RRPDefence #Valplast

1

19

3,186

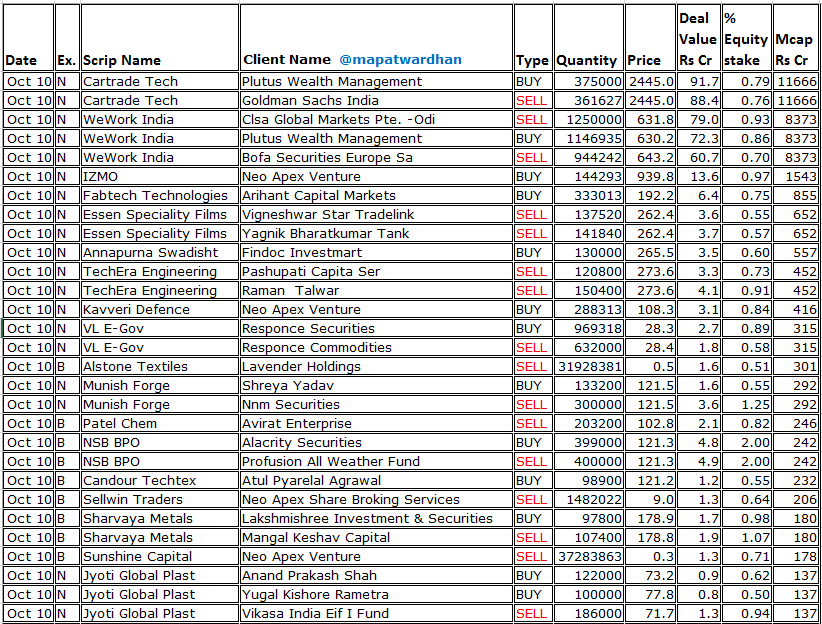

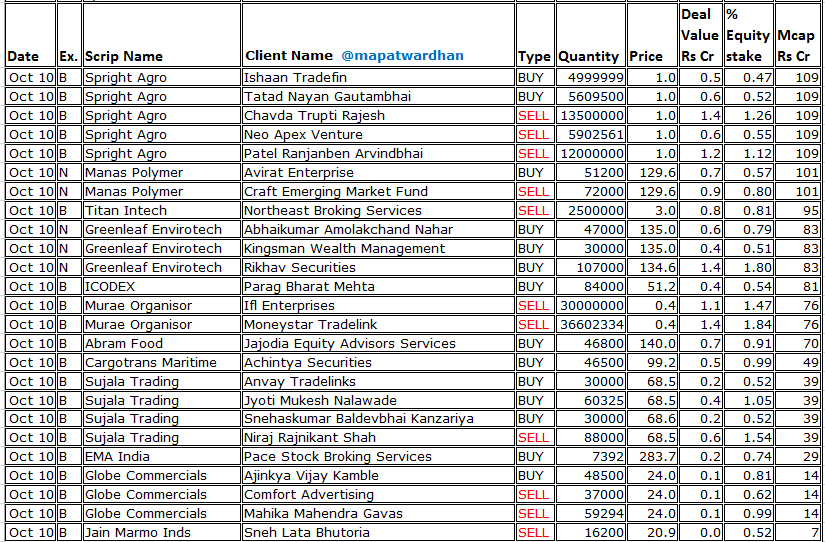

10 Oct 2025

*Today's bulk / block deals*

#CarTrade #WeWorkIndia #IZMO #Fabtech #EssenSpeciality #AnnapurnaSwadisht #TechEraEngineering #KavveriDefence #VLEEGov #AlstoneTextiles #MunishForge #PatelChem #NSBBPO #Candourtechtex #SellwinTraders #SharvayaMetals #JyotiGlobalTrust #SunshineCapital

2

1

24

2,615

10 Oct 2025

TechEra Engineering Update: Ashish Kacholia adds to stake!

✅ Purchase Details: Bought 2 lakh shares via open market.

✅ Investor Insight: Signals confidence in the company’s growth potential.

#TechEraEngineering #AshishKacholia #StockMarket #InvestorUpdates #ShareMarket #BuyAlert #OpenMarket

2

308

5 Oct 2025

#TecheraEngineering ✈️

🔹Bagged ₹4.66 Cr PSU order for MRO ground-support equipment

🔹Execution timeline: 60 days

(for real-time WhatsApp alerts finq.in)

2

409

29 Sep 2025

TECHERA ENGINEERING: LARGE TRADE NSE

Maharashtra Defence & Aerospace Venture Fund sold 🔴 11.29 lakh shares (6.83%) @ ₹243.85/share

Bengal Finance & Investment Pvt Ltd (Ashish Kacholia) bought 🟢 4.22 lakh shares (2.55%) @ ₹243.85/share

Surya Vanshi Commotrade Pvt Ltd bought 🟢 4.49 lakh shares (2.72%) @ ₹243.85/share

#TecheraEngineering #Stocks #BlockDeal

1

373

28 Sep 2025

5. Strategic Approvals

Listed on Turkish Aerospace vendor list (May’25)

– Only 3 Indian cos approved: CIM Tools, Tata Adv Systems, Techera.

Certifications = real moat (time & money intensive, not easily replicable).

6.Strong Hands

Ashish Kacholia’s Bengal Finance arm invested @ avg ₹244.

Shareholding concentrated: ~80–82% with promoters, DIIs, FIIs & HNIs.

Holders reduced from 1,237 → 814 (Mar’25).

Maharashtra Defence fund sold ~12.3L shares, but HNIs like Ashish Kacholia, Laroia Mona & Sarabpreet Kaur bought ~10.5L shares.

7.Sector tailwinds

India’s defense & aerospace demand surging (planes, airports, MRO).

Techera well placed with approvals capability new capacity.

8. Valuation view

At ~₹400cr mcap, Techera could see both earnings growth (revenue margin expansion) PE rerating.

Peer check: Unimech ₹250cr sales @ ₹6500cr mcap.

👉 Even conservative FY26 numbers (₹80cr rev, ₹11cr PAT) → 37x PE.

Any big order/result could change the growth trajectory fast.

Definitely Worth studying and try to look beyond the current PE.

#TecheraEngineering #SME

1

4

597

17 Jul 2025

Interesting shape made by #TecheraEngineering cmp 208.95

*It designs, manufactures and supplies precise tooling and components for the aerospace and defense industries.

4

712

28 May 2025

#SME #TECHERA #TECHERAENGINEERING #TECHERAENGG

Techera Engineering India FY25 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️ No specific revenue figures were disclosed but expects to maintain 30-40% CAGR growth, driven by a doubled order book and new capacity from the five-axis machine (Aug'25)

▫️Sustainable EBITDA range 17-25% for FY26

▫️Marketing efforts (e.g., Paris Airshow) and export growth (targeting 15-20% of revenue) are expected to contribute significantly

▫️Commitment to transparency with investors, considering quarterly business updates following board discussions

👉Current projects and pipeline:

▫️Order book for FY25 has doubled, possible 70:30 aerospace / defence and automation / precision split. Specific numbers were not disclosed to protect competitive advantage

▫️The company is running three shifts, indicating high capacity utilization

▫️Projects range from small tooling (3-6 months execution) to large, multi-year contracts (up to 5-6 years)

▫️Pipeline:

💠Participate in programs like the Tata-Airbus H125 helicopter assembly and Safran’s engine manufacturing for Tejas/MiG-2

💠Global expansion through the Paris Airshow aims to secure new contracts, particularly in MRO and tooling

💠Potential exploration into nuclear energy turbine components, though not currently in active discussion

💠Lead conversion takes 6 months to 1 year due to the slow-moving nature of the industry

👉 Others :

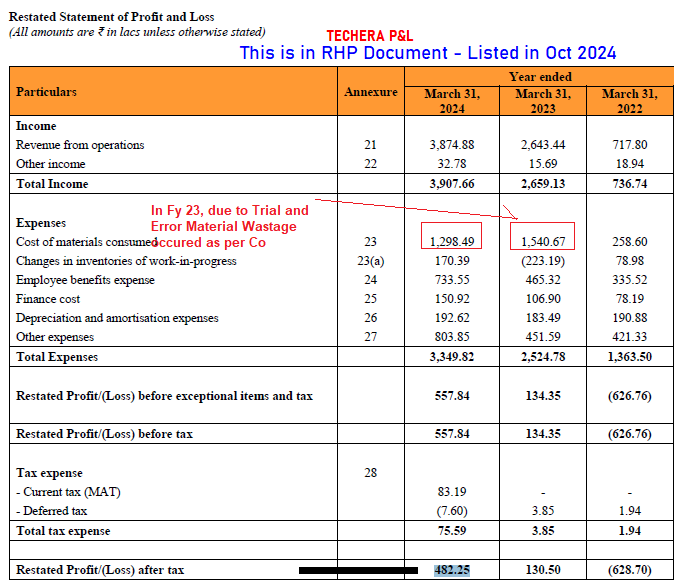

▫️ Regarding PAT for FY24 as in RHP was 4.82cr, while the results released today show a PAT of 2.82cr ;

Management clarified that the discrepancy is due to the difference between restated and notated financials. A detailed explanation was provided in a cover letter on Stock Exchange

▫️But the above cover letter is still not available on NSE Website

▫️Clean rooms are being established for critical aerospace components, ensuring compliance

▫️The Techera Design Center supports end-to-end engineering, including digitization of 1970s/80s design data, to modernize legacy systems

▫️Investment in a 6m x 3m x 1.2m five-axis machine (imported, unique in India for its size) to manufacture large components (e.g., PSLV shells), enhancing competitive positioning

▫️2.7cr excess expenditure from IPO proceeds was for infrastructure upgrades (e.g., IT hardware, compliance for confidential aerospace data)

1

11

2,522

28 May 2025

#TECHERA ENGINEERING RESULTS. H2, FY25 ANNUAL RESULTS. 186was at 64p/e. Now 91x👎🤣

The positive is that from loss has gone into profits and hopefully should report better numbers in future. But for a tool maker, valuation seem out of place

H2 Vs.H1 FY25

REV: 32 Vs 17.7Cr 👍

PAT: 4.33 Vs (-1.16) Cr 👍 👍This is good

FY25 Vs FY24

REV: 50 Vs 39Cr

PAT: 3.36 Vs 2.82Cr How this reduced to 2.82?!🤣 (Interesting! FY24 PAT was 4.82CR reported previously including in RHP and IPO was price based on 4.82Cr PAT!!!)

# TECHERAENGINEERING #RESULTS2025

5

1

25

8,915

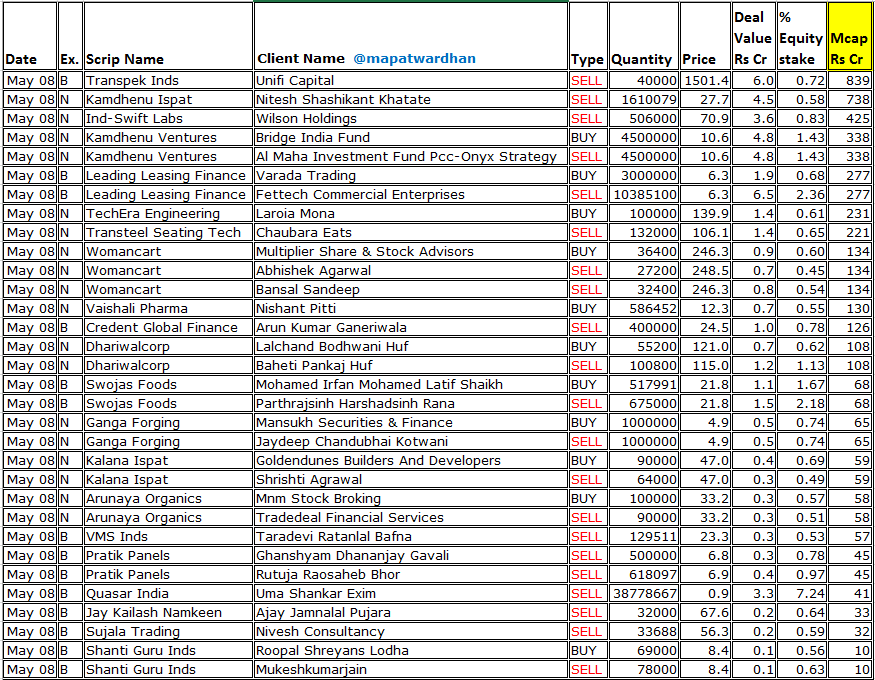

8 May 2025

*Today's bulk / block deals*

#Transpek #Kamdhenu #IndSwiftLab #LeadingLeasing #TechEraEngineering #TransteelSeating #Womancart #VaishaliPharma #CGFL #DhariwalCorp #SwojasFoods #GangaForging #KalanaIspat #ArunayaOrganics #VMSInds #PratikPanels #QuasarIndia #JayKailashNamkeen

16

2,585

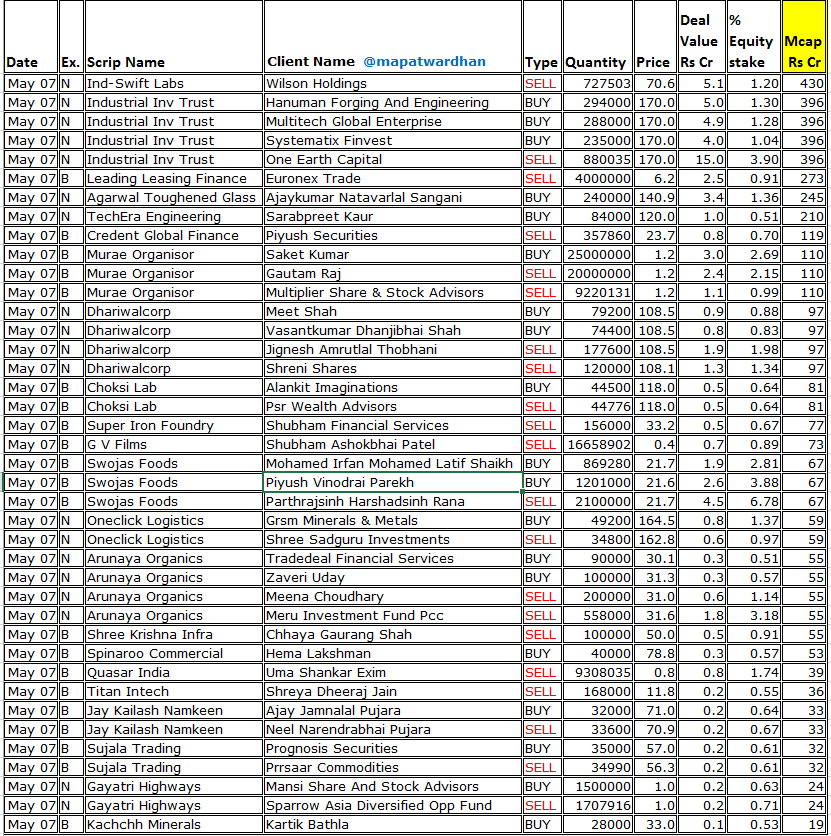

7 May 2025

*Today's bulk / block deals*

#IndSwiftLabs #IITL #LeadingLeasing #AgarwalToughenedGlass #TechEraEngineering #CGFL #MuraeOrganisor #Dharwalcorp #ChoksiLab #SuperIronFoundry #GVFilms #OneClickLogistics #ArunayaOrganics #ShreeKrishnaInfra #SpinarooCommercial #QuasarIndia

1

1

14

1,674