a les cuento, una vez trabajé como dos semanas en teleperformance, me arrepiento? sí, alguien me iba a regalar esos 4000 pesos de mi liquidación y mi semana de jale? no, así q a chingarle cabrones

1

24

We’re Hiring: Customer Operations Experts

Are you fluent in Hausa, Yoruba, Igbo, Fulfulde, Kanuri, Tiv, or Nigerian Pidgin? Do you have a passion for delivering exceptional customer experiences and want to build a global career?

Join Teleperformance as a Customer

2

68

Jun 14

Cada que escucho "Xfinity" me da un dolor en el pecho gracias teleperformance por el estrés postraumático

1

82

Still Teleperformance $TEP.PA

20 Dec 2025

Just published a contrarian take on so-called “AI losers” that I think are mispriced.

The mistake: assuming AI deletes demand, rather than reshaping workflows.

In enterprise settings, AI usually:

• automates the easy path

• creates complexity (edge cases, QA, compliance)

• shifts value to whoever owns the workflow

That distinction matters for investors.

Several incumbents are priced as if AI would erase their revenue.

A more likely outcome:

• demand shifts

• unit economics change

• incumbents sell AI back into their installed base

That’s the setup.

The piece looks at three names across the stack:

• Teleperformance — scaled CX operations

• Text S.A. — customer communication & orchestration

• RWS — language, content, and IP workflows

Different businesses. Same market overreaction.

Why these work as a basket:

• AI panic already priced in

• expectations are low

• outcomes don’t need to be heroic for re-ratings

Two of them also pay solid dividends.

This isn’t risk-free:

• pricing pressure

• execution risk

• slower-than-expected pivots

But when stocks price in unlikely catastrophes, “normal” outcomes can surprise.

Full piece here:

open.substack.com/pub/hydrar…

Thoughtful pushback welcome. Happy to debate.

211

Jun 13

La dotación de los árbitros en este Mundial parece que la hubiera hecho Teleperformance.

44

Jun 13

😂😂Jipe moyo kabisa. Wakenya waliohitimu chuo huenda Middle East as professionals: nurses, engineers. Aya ni F4 na class 8. Ripoti hapa ya BPO. Teleperformance and CCI employ over 5k in Kenya today. CCM lies to you that Eng ni ukoloni mtapitwa na Ug soon. uchumi360.com/uchumi/workfor…

1

63

Jun 13

Reminder against self hate: the competition of TCS, Infosys and Tech Mahindra is Teleperformance, Genpact and Accenture. TCS and Infosys didn’t make foundation models. Neither did their competition. They’re services firms, not tech and in fact the best ones out there.

1

1

14

1,218

Jun 13

Si ya eres mayor de edad podrías probar en Teleperformance, ganas decente aunque a veces los horarios con una mrd

Part time o full y se puede ahorrar con tranquilidad, así han hecho conocidos míos

Lo otro sería las comisiones pero necesitas buena llegada y saberle al inglés

76

Jun 13

La CAF devrait faire comme les opérateurs telecoms, c’est à dire délocaliser leurs centres d’appels au Maroc et à Madagascar avec Teleperformance et Intelcia (qui ne sont naturellement pas comptés comme étant employés en France) 😎

1

4

973

Jun 12

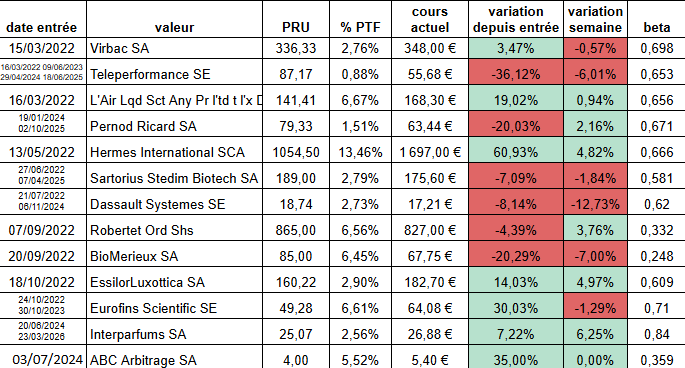

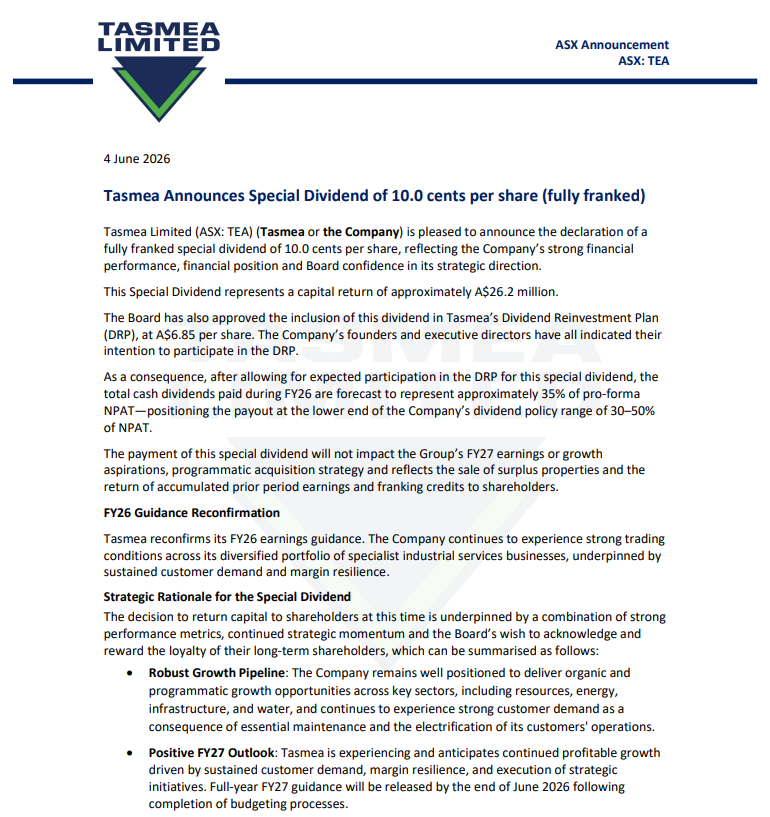

Ya he cobrado más dividendos en lo que llevamos de 2026 que en todo 2025.

Gracias principalmente a #Teleperformance, #NovoNordisk y, sobre todo, #Tasmea.

Lo interesante de $TEA es que el dividendo especial de junio no llega porque el negocio esté maduro o sin oportunidades.

1

1

161

The CareerSource Broward Veteran Job Fair is bringing serious opportunities to Broward! 🌴 Great positions are available across top employers, with salaries ranging from $16/hour to $207,000/year!

Whether you're looking to launch your career or level up, there's something here for you. These employers are ready to hire 💼

This is just a snapshot, more companies are still being added. Register today and don't miss your chance to connect!

Tuesday, June 16, 2026

10 a.m. to Noon (first 30 mins exclusive to veterans!)

South Career Center | 7550 Davie Road Extension, Hollywood, FL

Register at: bit.ly/veteranjobfair1

Reminder: All job seekers are welcome to attend

Shoutout to some of our attending companies listed below:

Boeing

Broward Health

City of Hollywood

Goodwill

Pembroke Pines Police Department

Seminole Classic Casino

Teleperformance

1

1

75

Jun 12

TELEPERFORMANCE ( $TEP ) saw its net short position held by CITADEL ADVISORS LLC grow to 1.71% on 10 June 2026, up 0.11 percentage points from 1.60%, reports datagouv

64

Jun 12

Cartera actualizada

Frequentis

Clínica Baviera

Jensen-group

Kri-kri

Verbio

Reach Subsea

IEG

Phoenix Spree

Metlen energy

GPW

Aurubis

Itafos

Befesa

De Nora

Tasmea

Hortico

Ferronordic

Centiel

Viafin

Lindbergh

Soma gold

Ramsdens holdings

Grupa Recykl

Teleperformance

Derichebourg

1

194

Jun 12

Sus nagarros, teleperformance, goeasy entre otras no dicen eso

1

43