Jun 10

📚 CallforReading - Closed Special Issue: Volatility Modeling in Financial Market

#OpenAccess with over 79,000 views

🔗 Read the full special issue: brnw.ch/21x3epn

#VolatilityModeling #FinancialEconometrics #MarketVolatility

#GARCH #RiskManagement #FinancialMarkets

7

May 3

📘 GARCH Quant Insights|Bayesian GARCH Paper Review

Day 3 · Efficient MCMC Sampling Innovation

📚 Paper Information

• Title: A Markov-Chain Sampling Algorithm for GARCH Models

• Author: Teruo Nakatsuma (1998)

• Journal: Studies in Nonlinear Dynamics & Econometrics

✨ Core Highlight

Dramatically improved the computational efficiency of Bayesian GARCH estimation.

🔬 Method Innovation

• Introduced data augmentation and block-wise parameter updating, achieving over 50% faster convergence

• Simplified the posterior distribution for significantly better chain mixing

• Remains a core algorithm used in modern Bayesian tools such as PyMC and Stan

💡 Practical Value

Has become the efficiency benchmark for large-scale volatility estimation and Bayesian inference in GARCH models.

#BayesianGARCH #MCMC #GARCH #ComputationalEfficiency #VolatilityModeling

4

55

May 2

📘 GARCH Quant Insights|Bayesian GARCH Paper Review

Day 1 · Founding Paradigm of Bayesian GARCH

📚 Paper Information

• Title: Bayesian Inference on GARCH Models using the Gibbs Sampler

• Authors: Bauwens & Lubrano (1998)

• Journal: Econometrics Journal

✨ Core Highlight

This is the foundational milestone of Bayesian GARCH.

It solved the critical challenge of high-dimensional posterior estimation using Gibbs Sampling.

🔬 Method Innovation

• Built the complete Bayesian GARCH framework: Prior → Conditional Posterior → MCMC → Convergence Check

• Demonstrated that Bayesian estimation significantly outperforms classical Maximum Likelihood under small samples and extreme volatility regimes

• Established the universal algorithmic foundation for all subsequent Bayesian GARCH extensions

💡 Practical Value

Completely redefined the volatility modeling paradigm and remains the global benchmark for both academia and industry.

#BayesianGARCH #GARCH #MCMC #VolatilityModeling

3

4

98

May 1

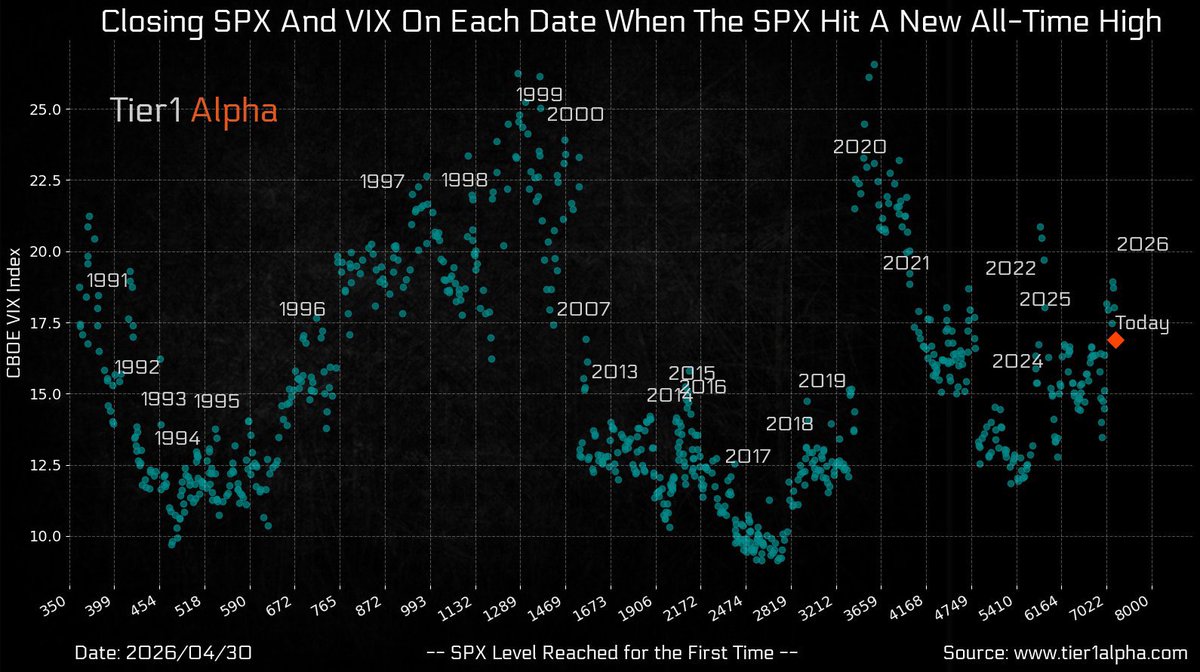

📘 GARCH Quant Insights|VIX at S&P 500 All-Time Highs: Today's Signal 🌪️📊

This scatter plot shows the **closing VIX level** on every date the S&P 500 ($SPX) reached a new all-time high — from the early 1990s through today (April 30, 2026).

Key observations:

- Early 1990s: VIX often 15–20 at new highs

- Late 1990s bubble: VIX spiked above 25

- Post-2010 era: Generally lower VIX at highs (10–15 range in many cases)

- 2020–2022: Elevated volatility even at peaks

- **Today (red diamond)**: SPX ~8000 new high with VIX ≈17

This places current volatility **neither extremely low nor crisis-level**, but noticeably higher than many previous bull-market peaks in the last decade.

Implication for quant risk models:

Even at record highs, the market is pricing in meaningful uncertainty — a reminder that volatility regimes can persist longer than price trends.

#SPX #VIX #MarketVolatility #AllTimeHighs #QuantInsights #VolatilityModeling

5

39

May 1

📘 GARCH Quant Insights|Bayesian GARCH Paper Review

Day 1 · Founding Paradigm of Bayesian GARCH

📚 Paper Information

• Title: Bayesian Inference on GARCH Models using the Gibbs Sampler

• Authors: Bauwens & Lubrano (1998)

• Journal: Econometrics Journal

✨ Core Highlight

This is the foundational milestone of Bayesian GARCH.

It solved the critical challenge of high-dimensional posterior estimation using Gibbs Sampling.

🔬 Method Innovation

• Built the complete Bayesian GARCH framework: Prior → Conditional Posterior → MCMC → Convergence Check

• Demonstrated that Bayesian estimation significantly outperforms classical Maximum Likelihood under small samples and extreme volatility regimes

• Established the universal algorithmic foundation for all subsequent Bayesian GARCH extensions

💡 Practical Value

Completely redefined the volatility modeling paradigm and remains the global benchmark for both academia and industry.

#BayesianGARCH #GARCH #MCMC #Econometrics #VolatilityModeling #QuantitativeResearch

4

47

May 1

📘 GARCH Quant|Volatility is the True Source of Excess Returns 🌪️📊

I. Returns Come from Volatility, Not Price 📈

Most investors obsess over price direction.

Top academic quant research has proven the opposite:

RETURN PREDICTABILITY IS EXTREMELY LOW, but VOLATILITY PREDICTABILITY IS EXTREMELY STRONG.

Volatility clustering, persistence, and asymmetry are the most reliable laws in financial markets.

II. The Three Core Features of Volatility 🔬

1️⃣ Volatility Clustering

Big moves tend to be followed by more big moves. Calm periods tend to stay calm.

GARCH models were built exactly on this pattern — they remain the cornerstone of time-series risk control.

2️⃣ Leverage Effect (Asymmetry)

Bad news triggers far greater volatility than good news.

EGARCH, APARCH and other asymmetric models capture this “fear amplification” in bear markets with precision.

3️⃣ Long Memory

Once volatility trends form, they can persist for months or even years.

GARCH-MIDAS elegantly blends high-frequency volatility with low-frequency macro data.

III. Why Volatility Strategies Deliver Long-Term Alpha 🧠

1️⃣ Risk-Pricing Bias

Markets systematically overprice tail risk.

Implied volatility stays persistently higher than realized volatility — creating a reliable premium for volatility-selling and risk-premium arbitrage strategies.

2️⃣ Mean-Reverting Nature

Extremely low volatility eventually expands. Extremely high volatility eventually contracts.

Target-volatility strategies and volatility timing thrive on this powerful reversion.

3️⃣ Low Correlation with Traditional Assets

Volatility strategies show near-zero correlation with stocks and bonds — making them essential diversifiers for institutions.

Volatility funds and hedge funds treat them as core portfolio building blocks.

IV. GARCH in Practice 💡

Cross-sectional factors drive direction & returns

GARCH volatility models drive position sizing & risk control

High-volatility regime → Reduce factor exposure & hedge tail risk

Low-volatility regime → Amplify factor exposure & boost return elasticity

This is the institutional mantra:

“LOOK AT FACTORS FOR RETURNS, LOOK AT VOLATILITY FOR SURVIVAL.”

✨ Core Conclusion

Price determines profit or loss.

VOLATILITY DETERMINES SURVIVAL.

Only by stably forecasting volatility can you achieve true long-term compounding.

#VolatilityModeling #GARCH #RealizedVolatility #AcademicTrading #InstitutionalQuant #RiskParity

4

40

12 Nov 2025

Moving ML from notebook to production? Our new guide walks you through the complete pipeline—data ingestion, feature engineering with PCA, XGBoost integration, and distributed training across time-partitioned data.

medium.com/@DolphinDB_Inc/fr…

Learn more about us 👉 dolphindb.com

#DolphinDB #MachineLearning #DataEngineering #FeatureEngineering #RealTimeAnalytics #VolatilityModeling

5

50

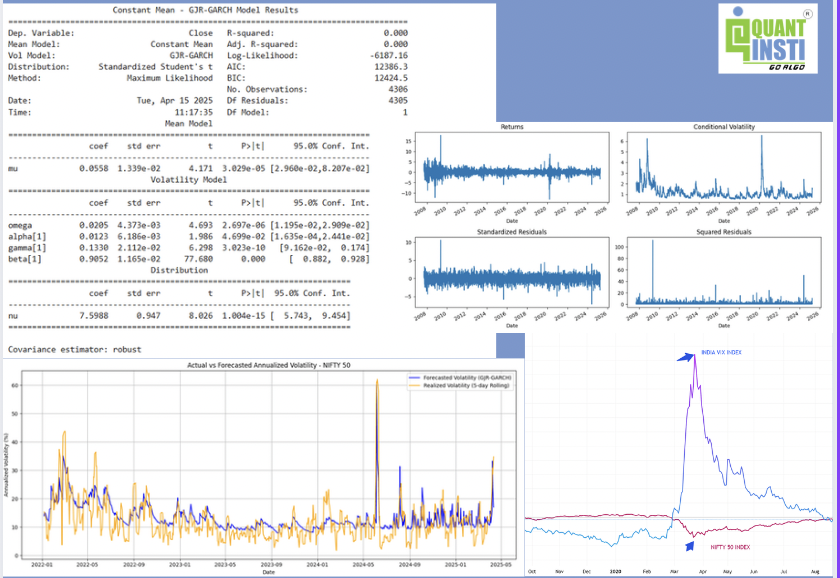

15 May 2025

🌪️Why do markets stay quiet for weeks... then explode?

Because volatility isn’t random.

It clusters, spikes, and reacts more to bad news than good.

📉 Enter: GJR-GARCH — a smarter volatility model.

Unlike standard GARCH, it captures asymmetric shocks:

🔻 Losses cause more panic (and volatility) than gains.

🧠 It models fear, not just fluctuations.

In our latest blog, we:

✅ Compare GARCH vs GJR-GARCH

✅ Forecast NIFTY 50 volatility using Python

✅ Use Student’s t-distribution for fat tails

✅ Diagnose model fit & residuals

✅ Make rolling 1-day forecasts

✅ Achieve a 0.74 correlation with realized volatility

📈 During COVID and mid-2024 market shocks, GJR-GARCH nailed the volatility spikes.

🔧 Tools used:

1. Python (arch package)

2. Daily returns

3. Statistical testing

Why it matters:

✅Better risk management.

✅Sharper hedges.

✅Smarter exposure.

👉 Read the full blog: blog.quantinsti.com/garch-gj…

💬 Curious how this compares to LSTM or ML-based forecasts? Let’s discuss 👇

#QuantFinance #GARCH #VolatilityModeling #PythonForFinance #AlgoTrading #TimeSeriesAnalysis #RiskManagement #NIFTY50

5

319

Now accepting submissions for Special Issue "Financial Crisis and Datamining" until 30 April 2020 mdpi.com/journal/jrfm/specia… #FinancialCrisis; #BigData; #MachineLearning; #VolatilityModeling; #MarketSentiment

12 Jun 2019

CALL FOR PAPERS: Special issue "Financial Crisis and Datamining" @JRFM_MDPI . We welcome papers on #FinancialCrisis #BigData #MachineLearning #VolatilityModeling #MarketSentiment More info: bit.ly/2wLXsfL Please RT

5

6

12 Jun 2019

CALL FOR PAPERS: Special issue "Financial Crisis and Datamining" @JRFM_MDPI . We welcome papers on #FinancialCrisis #BigData #MachineLearning #VolatilityModeling #MarketSentiment More info: bit.ly/2wLXsfL Please RT

3

3