🤣🤣🤣🤣 IIT Supernumerary DEIMAXxing

its like toppers should be ashamed of themselves for having the privilege.

How JEE gave only a trickle of visibility into toppers..hiding the rest like lil wmps..

Jun 5

JEE ranks to be banned from IIT CVs? But wait!

There is a valid reason ...

The All IITs Placement Committee is discussing a major policy change for the 2026–27 session: a total ban on sharing JEE Advanced ranks with campus recruiters.

The Goal: Protect students from historically marginalized communities (SC/ST/OBC) from rank-based discrimination during hiring.

The Problem: Certain international and quant firms currently restrict interviews exclusively to the top 100 or 1,000 rankers.

The Argument: students and placement cells believe hiring should be based on college achievements, not an entrance exam score from years ago.

A final approval is pending, but it could completely reshape the upcoming placement season.

What's your take? A fair move for equality, or unfair to top rankers? Drop your thoughts below! 👇

Reported by: sheena.sachdeva on instagram

👉 READ Full story here: buff.ly/r5mErVJ

#iitplacements #education #delhi #india #trending

8

9

35

5,264

All the people freaking out about the Nvidia structure Michael Burry has just highlighted presumably have no issue with China using economically similar structures for years?

To recap, Burry points out Nvidia/Xai are using an SPV for off-balance-sheet holding of GPUs/debt, with Nvidia providing sales plus equity, Apollo-sourced debt, and ultimate risk passed to retail via Athene annuities.

The irony is the structure shares notable parallels with Chinese financing practices for capital-intensive projects (infrastructure, real estate, industry). These often rely on opacity, leverage, and implicit risk-shifting to households/savers, which can be viewed as a form of financial repression when savers/retirees effectively subsidize growth with limited upside and hidden downside.

Core Similarities:

1. Off-Balance-Sheet SPVs to Hide Leverage and Debt:

In the xAI/Nvidia case, Valor (the SPV) allows massive GPU acquisition and deployment without full ownership or debt appearing on xAI’s or Nvidia’s main books. Nvidia sells $5.4 bn in chips while investing $1.9 bn; and the $3.5 bn debt stays “off.”

In the China case: Local Government Financing Vehicles (LGFVs) are classic SPVs set up by local governments to borrow for infrastructure, property, and industrial projects post-2008 stimulus (and earlier). These are nominally corporate entities but carry implicit government backing. LGFV debt is largely off official government balance sheets (estimated at some 40-50% of GDP in recent years), enabling rapid capital-intensive investment without breaching borrowing limits or transparency rules.

Many LGFVs fund low-return or non-cash-flowing assets and rely on refinancing/subsidies.

In the BRI case: China has used SPVs, joint ventures, and state-owned enterprise (SOE) structures for Belt and Road Initiative projects. Debts often sit with non-sovereign entities (SOEs, SPVs, private partners) rather than central government books creating ~$385 bn in “hidden debts” across recipient countries. This obscures total leverage while allowing host governments to pursue big projects. Implicit guarantees blur lines, similar to how Valor ties back to the principals.

2. Funding via Intermediaries and Retail/Household “Bag Holders”

Apollo debt packaged into Athene annuities shifts risk to American retirees via leveraged, opaque Level 3 assets (no clear market prices).

Retirees provide stable, long-term funding but bear credit/liquidity risks indirectly.

In China’s case: Wealth Management Products (WMPs) and trust products have historically raised trillions from households/retail investors seeking yields above repressed deposit rates. Banks often sell these (implicitly guaranteed) and channel the funds to LGFVs, real estate, or infrastructure via layered structures.

Historically this kept risks off bank balance sheets while households funded capital-intensive growth.

In both cases, ordinary savers (via annuities/WMPs/bank deposits) provide cheap, patient capital for high-risk, high-scale projects. Upside goes to tech/SOEs/project sponsors; downside risk is socialized or hidden until stress emerges (e.g., LGFV rollovers, annuity underperformance).

China excels at this for growth: Post-GFC LGFV boom and BRI enabled massive fixed-asset investment.

But recipient countries (and ultimately their taxpayers) often face hidden liabilities; Chinese lenders (policy banks/SOEs) manage such risks via restructuring or resource-backed deals, but domestic Chinese savers indirectly backstop via the broader model.

In that context it’s difficult for Western countries to maintain an upper hand on capital intensive investments without resorting to similar tactics.

The only difference is that while China’s model is state-orchestrated for national development goals, the xAI/Nvidia structure is market-driven financial engineering in a competitive AI race, more akin to Enron-era or pre-2008 project finance.

8

24

100

15,372

From the files of Mr. Smarty Pants: Rick Dees was fired as a disc jockey at WMPS for merely mentioning his record “Disco Duck” on-air.

2

916

The Rt Hon Speaker immediately started his duty by advising the two Gorgeous Hon WMPs and former Ministers to keep it up with smartness always @HonMutasingwa @JudithNabakoob1 Mwashemera mazima abazukuru ba jajja

2

924

May 20

China Off-Balance-Sheet Debt Exceeds GDP of Most Nations | Antonio Graceffo, The Gateway Pundit

For decades, there have been claims that China had the fastest-growing economy, and that it would eventually overtake the U.S. as the world’s largest economy. However, the fastest-growing economies are always developing economies because mature economies do not have as much room to grow.

In other words, a country with a per-capita GDP of $80 per month, as China had in the year 2000, has far more room for rapid expansion than a country like the United States, where the figure now stands at around $7,000 per month.

There is also the concept of low-hanging fruit. When a country has no highways or rail infrastructure, building highways and railways causes GDP to skyrocket. But once all major cities are connected, building additional highways and rail lines has only a marginal impact on economic growth.

A case in point is China’s famous high-speed rail system. Once highways and conventional railways already existed in China, converting to high-speed rail represented a massive economic investment and a large accumulation of debt, while the resulting increase in GDP was relatively minimal. For one thing, high-speed rail cannot be used to carry freight.

While China is still building high-speed rail lines, linking small communities with other small communities, the world is moving toward a remote-work model, making the movement of people a smaller contributor to GDP. Moving freight, however, remains critically important. Despite having a population less than one-quarter the size of China’s, the United States operates approximately 220,000 kilometers of total rail, about 33 percent more than China’s 162,000 kilometers, the vast majority of which is dedicated to freight.

Along with this development boom in China came debt. Because of the centrally planned economy, the central government was able to order local governments to invest and develop by creating debt. That debt was financed largely through real-estate sales, as the Chinese government controls actual land ownership rather than simple lease arrangements, which is what individual “homeowners” in China actually possess.

In order to keep this debt from detracting from the appearance of investment and economic performance, large portions of the debt were kept off the balance sheet.

In accounting, off-balance-sheet debt, sometimes called incognito leverage, describes an asset, debt, or financing activity that does not appear on an entity’s balance sheet. The structure involves using legal arrangements to borrow money, acquire assets, or take on obligations that do not appear on the balance sheet. Common instruments include operating leases, special purpose entities (SPEs), and joint ventures.

In China’s case, the instrument is the Local Government Financing Vehicle, or LGFV, a government-created special purpose entity that borrows on behalf of local governments while keeping the resulting debt off official government balance sheets.

The LGFV structure is rooted in a 1994 budget law that banned local governments from issuing bonds or running deficits. To work around this, local governments created special-purpose entities to borrow from banks and capital markets, primarily to fund infrastructure. Because LGFV debt does not count toward official government debt ceilings, no definitive official statistics exist on total liabilities.

Because much of this debt is off the balance sheet, it is difficult to estimate accurately, and different methods produce different totals. The IMF estimates LGFV debt at $9.04 trillion as of the end of 2024. Other approaches produce significantly higher figures. A compilation of interest-bearing liabilities across roughly 4,000 LGFVs places the total at $12.10 trillion, while broader market estimates place the range between $8.35 trillion and $11.13 trillion. Overall, estimates suggest that China’s LGFV debt load has grown from approximately $1.2 trillion in 2014 to between $9 trillion and $14 trillion in 2024, representing roughly 50 to 80 percent of China’s GDP.

Only four countries, the United States, China itself, Germany, and Japan, have total GDPs exceeding $4 trillion. At the IMF’s conservative estimate, LGFV debt alone exceeds the GDP of every other nation on earth. China’s foreign-exchange reserves, the largest in the world, stood at approximately $3.2 trillion at the end of 2024, meaning estimated LGFV debt is larger than the foreign-exchange reserves of any country on earth and roughly three to four times larger than China’s own reserves.

The IMF has warned that even a 5 percent LGFV default rate would be equivalent to a 75 percent increase in the banking system’s non-performing loans. Debt not backed by earnings sufficient to cover interest payments already amounts to 37 percent of GDP.

Additionally, China is throwing good money after bad. Proof that massive state investment now has minimal impact on GDP is that only 3 percent of LGFVs post a return on equity of 4 percent or higher, while approximately 10 percent record net losses. Aggregate net profit for 2024 totaled $76.5 billion, yet government subsidies exceeded $139.1 billion, meaning that absent subsidies, nearly half would be loss-making.

Following the collapse of land-sale revenues after 2022, the primary source of financing for LGFVs, many vehicles lost cash flow and have relied on bank forbearance, debt refinancing, and repayment-deadline extensions. In November 2024, Beijing announced a 12 trillion yuan package to address hidden debt, the largest policy intervention directed at local-government liabilities.

However, Fitch Ratings estimated that the restructured portion covered only approximately 25 percent of the hidden debt load. Beijing’s own executive director to the IMF placed total LGFV debt at 44 trillion yuan, roughly three times the figure cited at the time of the restructuring announcement.

China has accumulated a second category of debt that exists outside formal accounting ledgers. Shadow banking refers to credit intermediation conducted outside the regulated banking system, primarily through non-bank entities and bank off-balance-sheet vehicles that circumvent the capital, liquidity, and lending restrictions imposed on commercial banks.

A key characteristic distinguishing China’s shadow-banking system from the Western model is that Chinese commercial banks themselves dominate the system, routing credit through structures that keep liabilities off their books while retaining effective control.

The primary instruments include wealth-management products, trust loans, entrusted loans, bankers’ acceptances, and informal lending. Wealth-management products are issued by banks, trusts, and securities firms and offer returns above standard deposit rates. They are sold as savings products that do not appear on the issuing institution’s balance sheet. Depositors’ funds are packaged into WMPs and deployed into property developers, LGFVs, or other restricted borrowers while the bank’s balance sheet shows nothing.

Trust companies, separately regulated firms with broad latitude to lend to restricted industries, including real estate and LGFVs, serve as conduits through which state banks on-lend to borrowers they cannot officially finance. Entrusted loans are made by one non-bank party to another borrower using a bank as a servicing agent, a structure necessitated by Chinese legislation prohibiting direct lending between companies.

Bankers’ acceptances are certificates issued by banks promising future payment, allowing financing to occur without a formal loan appearing on either party’s books. Informal lending consists of loans between private entities with no payment agents, operating entirely outside the banking system and unreported to regulators.

These mechanisms expanded after the 2008 global financial crisis as fiscal stimulus and tight formal credit controls pushed borrowers toward unregulated channels. Credit through shadow channels grew at an annualized rate of 34 percent from 2010 to 2013, with the sector reaching an estimated 60 trillion RMB before regulatory interventions reduced it by 16 trillion RMB by the end of 2019. Broad shadow banking assets rose to RMB 53.3 trillion in 2024, equivalent to approximately $7.3 trillion. China’s banking regulator previously estimated shadow banking at 84.8 trillion yuan ($12.9 trillion) in 2019, equivalent to 86 percent of GDP.

Shadow banking and LGFV debt are distinct pools that fund different borrowers through different mechanisms. LGFVs finance government infrastructure through special-purpose entities; shadow banking finances property developers, small businesses, and consumers through non-bank channels. However, local governments have used both simultaneously, and LGFVs themselves borrow through shadow banking channels, meaning the two systems are interconnected. A stress event in one transmits directly into the other.

Stacking the figures, the IMF estimates LGFV’s hidden debt at approximately $9 trillion, while broader market estimates place it between $9 trillion and $14 trillion. Shadow-banking assets stand at approximately $7.3 trillion, and official local-government bonds total roughly $7.5 trillion. The conservative combined total is approximately $24 trillion, while the high-end estimate approaches $29 trillion, against China’s official GDP of roughly $18 trillion.

China’s total non-financial debt, government, corporate, and household combined, reached 302.3 percent of GDP in 2025, according to the National Institution for Finance and Development, and 312 percent as of 2024, according to the IMF’s Article IV Consultation, up from 245 percent in 2019. By comparison, total U.S. public and private debt stood at approximately 265 percent of GDP in 2024.

thegatewaypundit.com/2026/05…

10

15

59

3,689

Apr 14

This has really not addressed the primary issue raised in the initial quote which is: "it is illegal to market FFMP as milk in EU''. One of the reasons is because it is considered deception as the term ''milk'' is legally reserved for the "normal mammary secretion" obtained from animal milkings, without adding or removing anything from it.

The issue it think @wearegst is trying to point out is that FFMP is considered to be NUTRITIONALLY ''inferior'' to real milk, hence the ''ban'', This is because they have "extracted" the natural animal fat and "added" a non-dairy plant fat. So the protein content is significantly less per 100g, compared to milk or Whole Milk Powder (WMP).

Also, natural milk fat contains specific vitamins (A, D, E, and K) and fatty acids that are easily absorbed by the body. While FFMP is often "fortified" with these vitamins, the synthetic versions added to FFMP aren't always processed by the body as efficiently as the natural versions found in dairy fat.

The EU views FFMP as a "functional substitute" designed for cost-cutting, not for nutrition. It was created for industrial use (like in bakeries or chocolate making) where the taste and fat content matter more than the dairy nutrients. Also, vegetable fat is much cheaper than dairy fat.

If the constraints were just limited cold-chain infrastructure, transportation and sub-optimized storage systems, WMP, which is real milk with the water removed could have been a better substitute. This keeps the original animal fats, while also somewhat avoiding the constraints itemized.

In Nigeria, FFMP are sold under names like "Milk Product" or "Filled Milk," whereas in Europe, it would have to be clearly labeled as a "Fat Filled Powder" and kept far away from the dairy aisle.

So, I think the primary reason our regulators look away is because they probably know that the majority won't be able to afford the real milk or WMPs. The least they could do is ensure these companies label them appropriately as "Fat Filled Powder" because FFMPs in the nutritional sense of it are not MILK!

3

6

417

Mar 29

2

4

7

196

Feb 13

Political control? On Wednesday a certain MP that puts airports in Pakistan and banning Israeli football fans high on his priority list, called other MPs ‘rubbish’. The same MP clearly tried to influence WMPs decision

3

69

Real estate was never just “25–30% of GDP.”

That statistic undersells the reality. Housing in China functioned as the base layer of the entire financial operating system:

• Land sales = ~40% of local government revenue

• Property = ~70% of household wealth

• Developers = primary credit transmission channel

• Shadow banks = stuffed with property-linked WMPs

• Banks = using land as synthetic sovereign collateral

Housing wasn’t an asset class. It was China’s monetary substrate.

The CCP didn’t just overbuild cities. They monetized belief. They turned land into fiscal policy, apartments into pensions, and pre-sales into a national Ponzi-style liquidity engine.

Growth wasn’t driven by productivity — it was driven by balance sheet expansion anchored to a single assumption: prices never fall.

That assumption is now broken.

And when collateral breaks, everything reprices:

Not just assets — trust, risk, and time.

Look at the signals:

• New home sales still down ~30–40% from peak

• Developer defaults > $300B in liabilities

• Youth unemployment structurally double-digit

• Household savings rising while credit demand collapses

• Stimulus failing because velocity is dead

This is the key:

China doesn’t have a demand problem. It has a belief problem.

Liquidity no longer converts into activity because the psychological loop has inverted. People don’t borrow because they expect growth — they hoard because they expect decay.

That’s the real regime shift.

In financial systems, growth is reflexive:

Optimism → leverage → prices → confidence → more leverage.

China has flipped the sign:

Pessimism → deleveraging → falling prices → distrust → capital paralysis.

Once that loop turns negative, no amount of stimulus works, because stimulus only operates through confidence — and confidence is gone.

The state is now trapped in a trilemma:

• Too big to bail everything

• Too fragile to allow liquidation

• Too centralized to allow creative destruction

So it chooses the only remaining path: managed stagnation.

Not collapse. Not recovery. A slow, silent erosion of returns, innovation, and trust.

This is what Japan looked like in 1990 — except China is:

• More leveraged

• More opaque

• More demographically constrained

• More politically rigid

Which means the end state is worse.

The crisis already happened.

What we’re watching now is just the accounting phase of a broken growth model.

China didn’t lose money.

It lost belief in its own future.

And in macro, belief is the only asset that actually compounds.

1

5

516

Jan 27

Matters will only improve when WMPs shift their focus from nonsense, like imaging and lab-values, to the things that matter, like mindfulness and providing a warm and supportive doctor-patient relationship.

2

96

This isn't the first time that the Chinese central government has reined in an episode of stock market exuberance that it helped to cause in the first place.

It's arguably just a partial retread of an episode that took place only a little over a decade ago.

We are quick to forget that in 2015, one of Xi Jinping's biggest tests during his first term in office was a meltdown in the Chinese stock market.

What's important to note is that both the initial rally and the subsequent crash both occurred at the prompting of Chinese officials, still lacking experience in the subtleties of the market's animal spirits.

Xi has been a committed supporter of capital markets - and the stock market in particular, ever since assuming office, contrary to the murmurs of those who accuse him of being the second coming of Mao.

Only a few years after Xi became president, Chinese authorities encouraged domestic retail investors to enter the stock market.

The motives then were the same as the motives for it now.

Beijing wanted to provide greater funding to tech companies, as well as for the wealth effects of democratized share investment to spur growth in Chinese consumption.

Back then, Beijing also hoped that a healthier stock market would help state-owned enterprises to deal with their debt burdens by means of equity issues.

Chinese retail investors took the hint from Beijing and poured into the stock market.

They didn't need any encouragement, because their investment options were limited by China's restrictive financial environment to bank deposits, wealth management products and property.

Yields on bank deposits were artificially suppressed, while WMPs and the overheating real estate market looked like risky bets.

The immediate result was a sharp boom in the Chinese stock market, driven by retail investors following the lead of policymakers.

The Shanghai Composite Index surged from just north of 2,000 at the start of June 2015, to peak of 5,168 a year subsequently.

Shanghai had become the world's second-largest stock market in terms of market capitalisation.

The final outcome, however, was a stock market bubble that diverged wildly from underlying fundamentals.

Analysts warned that speculative trading had led to shares hitting "price-to-dream" ratios.

Market leverage also reached unprecedented levels, as margin-driven speculation surged.

Alarmed Chinese regulators resorted to hasty action, which triggered a stock market crash.

They put pressure on margin lending, which led to a sudden panic and mass withdrawals from mutual funds.

Mutual funds were forced to engage in fire sales of both good and speculative shares.

The result was a 30% fall in the Shanghai Composite Index.

Chinese regulators then needed to reverse course again to support the market.

The eventually managed to calm the panic and restore order, using overt measures off limits in other economies.

They called upon government institutions to buy up shares and hold on to them, as well as used state-owned media to boost the mood of the market.

Short-selling was restricted, while limits on margin trading were loosened.

Xi no doubt hopes that the top brass at China's financial regulators have sharpened their chops since then, and will be able to corral the stock market without too much commotion in 2026.

This is of critical importance for China right now, given Xi still has hopes of using a thriving capital market to:

a) Boost funding for tech companies in the hope of achieving scientific and technological independence, and

b) Boost consumption via the wealth effects created by rising share prices.

Jan 26

1/2

Bloomberg: "Record outflows from exchange-traded funds held by Central Huijin sent the clearest signal yet that Beijing is no longer simply propping up the market, but actively reining in the rally — a sharp break from past rescue playbooks."

bloomberg.com/news/articles/…

1

3

29

3,776

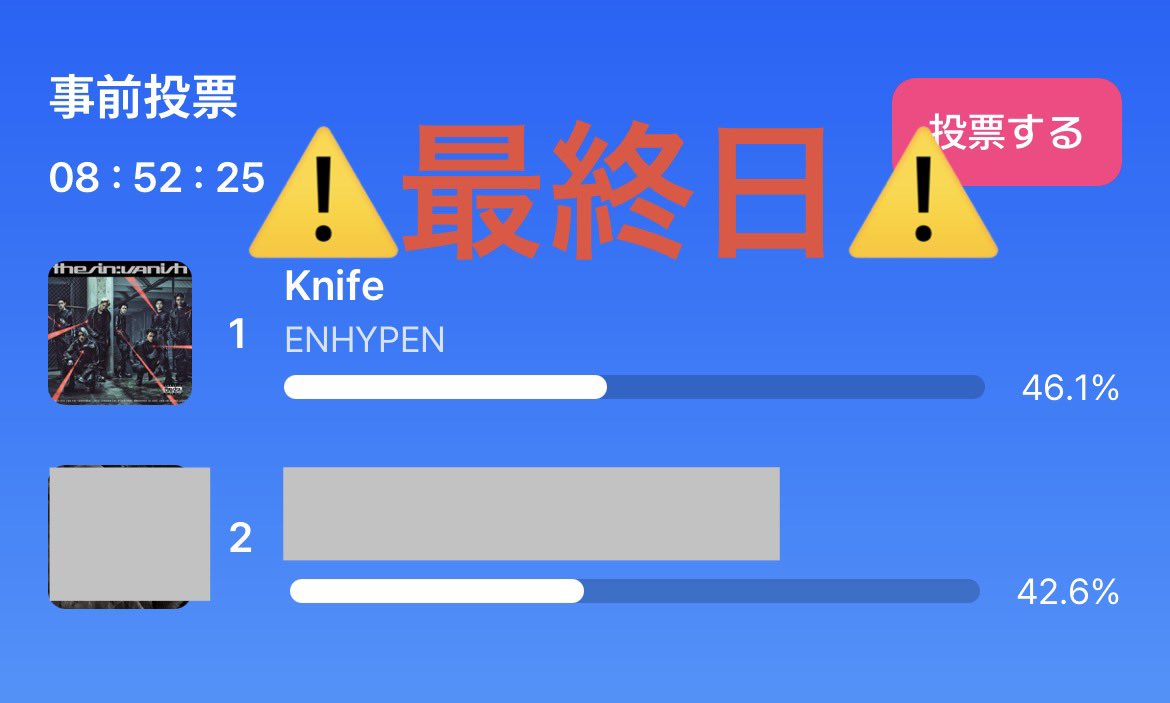

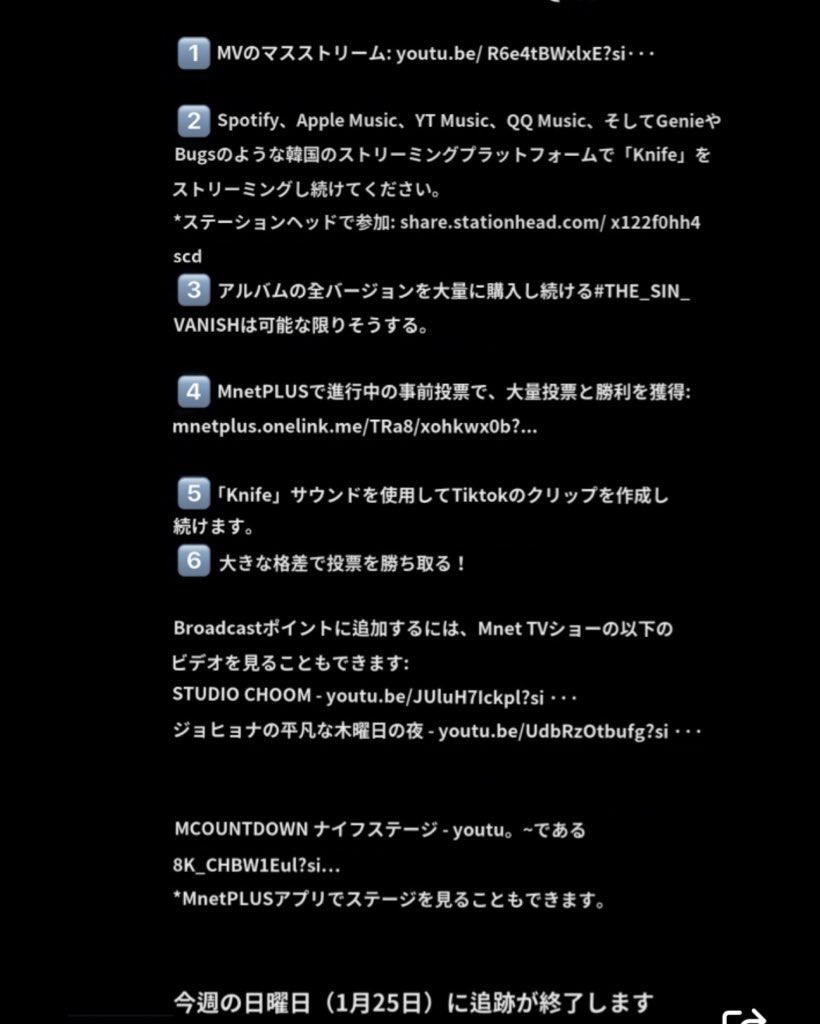

Jan 26

1/26(月)

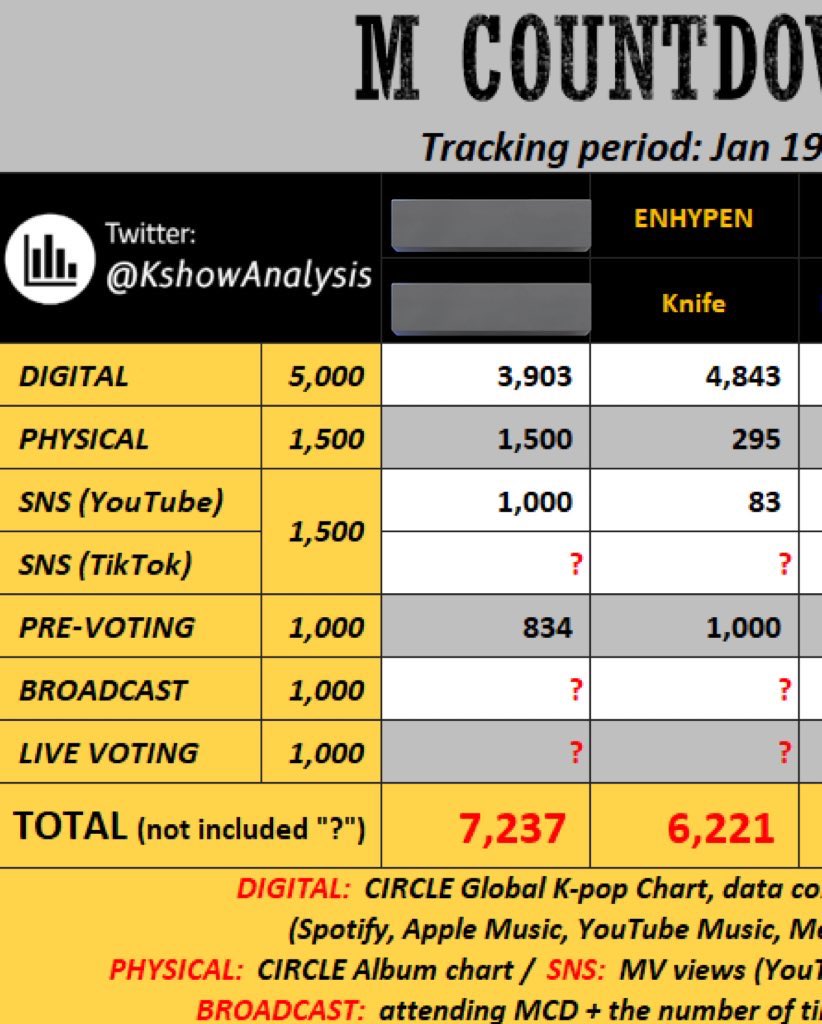

☑️Mnet Plus エムカ

事前投票•WMPS投票最終日🚨

☑️Fancast ミューバン

事前投票(無制限) 〜1/28(水)11時まで

☑️Muniverse

毎日1垢10票 〜1/29(木)11時まで

集票

✔︎UPICK D Awards

✔︎Higherなど各アプリ

✔︎DUCKAD

🎧推しリク

🎧MV再生•Spotify•ステへ等

#ENHYPEN

10

31

1,019

Jan 25

1/25(日)

Mカ•ショーチャン•ミューバン集計最終日

🔥Mnet Plus

事前投票・WMPS 🗳️

1端末5票 〜1/26(月)まで毎日

🔥MV再生•Spotify•ステヘ等

大差で勝つ必要あり!推しに1位を‼︎

✔︎Muniverse投票🗳️

✔︎対象アプリ集票

✔︎推しリク•🦆

ENGENE 一致団結してFighting🔥

#ENHYPEN

16

30

4,426

Jan 24

1/24(土)

投票

☑️Mnet Plus

🔥事前投票 1/26(月)まで3日間

⚫︎WMPS投票 1/26(月)まで4日間

☑️Mubeat

1位候補で Live投票

15:20頃〜放送中に1垢150

☑️Muniverse

毎日1垢10票

17:00〜1/29(木)11時まで

集票

Fancast

IDOLCHAMP

UPICK

🎧推しリク

🎧DUCKAD

🎧MV再生•Spotify•ステヘ等

#ENHYPEN

Jan 24

M COUNTDOWN

#ENHYPEN に1位を贈れる可能性あり!

✅2週目集計期間は明日1/25(日)まで

MV再生

Spotify等

音盤購入

TikTok

✅Mnet Plusで投票🗳️

毎日1端末5票

✔︎事前投票スタート🔥

※本日〜1/26(月)23:59までの3日間

✔︎WEEKLY MCD PICK STAGE投票

※1/23〜1/26(月)23:59までの4日間

Fighting🔥

13

20

1,696

Also bei meinem Nachbarn, war am Vormittag der Installeur Notdienst da, um die 2 WmPs zu enteisen. Die Wetterseite ist ungünstig für die Dinger, meinte der Monteur. Nicht ideal.

1

4

570

Jan 18

You assume China is in a financial position to take over US trade. They are not. They are burning ~$1T/yr keeping their banks alive by extending and pretending. WMPs and LGFV’s are upside down. Propdev’s failing. It’s so bad the CCP isn’t allowing RMB to be exchanged for gold.

2

1

20

2,519