Farm4Profit sat down with Billy Carter of @AgXplore and progressive farmers Ron Pagel, Dave Justman, and Jonathan Reynolds to discuss the management decisions driving exceptional corn and soybean yields. From fertility programs and fungicide timing to drone applications, soybean management, and a relentless focus on ROI, these growers share the strategies helping them maximize performance while staying profitable.

Watch the full episode: bit.ly/43VieZQ

#Farm4Profit #Agriculture #Farming #Corn #Soybeans #AgXplore #CropManagement #Agronomy #YieldGoals #CornYield #SoybeanYield #FarmProfitability #PrecisionAg #AgInnovation #FarmLife #AgBusiness #RowCrops #CropProduction #FarmManagement #YieldContest #ModernFarming #AgPodcast #Plant26 #Plant2026 #ROI #FarmSuccess #AgLeadership #FarmEducation #YieldMatters #FarmersHelpingFarmers

3

3

267

Feb 3

Test weight isn’t just a number on the ticket. It reflects grain quality, plant health, and how well the crop finished.

Details matter at harvest. 🌽

#TestWeight #CropQuality #YieldMatters #HarvestSeason #Agronomy #PrecisionAg #Farming #AgEducation #GrowerLife

3

239

20 Nov 2025

Dive deep into the new fungicide, Forcivo, with Mike Eiberger from @corteva.

Forcivo Fungicide is a 3 mode of action product with preventative, curative, and systemic disease control options. Powered by Flouindapyr, Flutriafol, and Azoxystrobin. Check it out for your crops in the 2026 growing season!

Hear more about Forcivo at youtu.be/tJopZbHXL40

#fungicide #fungicides #Cornfungicides #Corteva #EnlistCorn #corn #Farm4Profit #CornSeason #CleanFieldsStartHere #CropProtection #AgPodcast #FarmPlanning #wheat #soybean #YieldMatters #corndisease #soybeandisease #southernrust #tarspot #northerncornleafblight #greyleafspot #agronomy

2

401

18 Nov 2025

Mike Eiberger from @corteva discusses the new fungicide, Forcivo!

Forcivo Fungicide is a 3 mode of action product with preventative, curative, and systemic disease control options. Powered by Flouindapyr, Flutriafol, and Azoxystrobin. Check it out for your crops in the 2026 growing season!

Learn more about Forcivo: youtu.be/tJopZbHXL40

#fungicide #fungicides #Cornfungicides #Corteva #EnlistCorn #corn #Farm4Profit #CornSeason #CleanFieldsStartHere #CropProtection #AgPodcast #FarmPlanning #wheat #soybean #YieldMatters #corndisease #soybeandisease #southernrust #tarspot #northerncornleafblight #greyleafspot #agronomy

2

326

2

23

31 Jul 2025

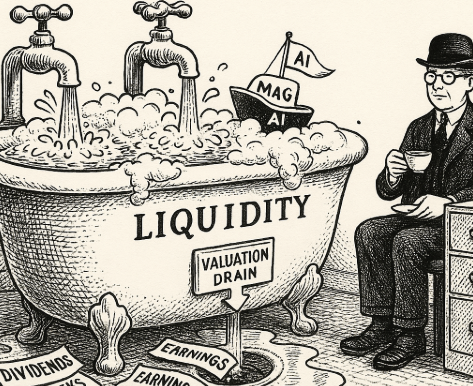

TOBACCO VANGUARD

Market Dispatch – July 2025

LIQUIDITY WITHOUT EARNINGS

By M. Reuven

The commentator's remark on CNBC, that she wishes to see more and more money pour into the market, might please a banker or an ETF peddler. But it ought to trouble anyone with a memory or a balance sheet. It reflects a worldview in which capital is a spectacle, and valuation a superstition. The assumption, never questioned, is that more liquidity is always good. Yet in the present market, it is precisely this liquidity that has become the problem.

This is not a rising tide. It is a speculative geyser. The United States equity market in 2025 is not driven by earnings, dividends, or discipline. It is driven by hope, hype, and the relentless recycling of capital into a handful of favoured names. The so-called “Magnificent Seven”, especially those firms aligned with artificial intelligence, now consume a disproportionate share of speculative flows. But they do not return capital in kind. They are not dividend-paying workhorses. They are valuation vessels: empty, but shining.

There is no meaningful link between these flows and underlying enterprise. Earnings growth has slowed. Margins have peaked. Yet prices rise, not on output, but on narrative. The AI story, like the dot-com dream before it, offers no terminal value. It absorbs investment but produces no yield. This is not investment. It is expenditure.

Tobacco Vanguard rejects this exuberance. Not because we are contrarian by instinct, but because we are custodians of an older truth: that capital must serve production; that savings must fund enterprises which return a share of their profits to their owners; and that speculation is not a sign of strength, but of moral fatigue.

The US market, in its current state, is divorced not only from value but from proportion. Sectors such as consumer staples, industrials, and energy, the cash engines of national solvency, are marginalised. Their earnings are real. Their returns are repeatable. Their presence in the indices, however, is shrinking. Meanwhile, companies with nosebleed multiples and no cash flow dominance are treated as monetary darlings.

What we are witnessing is not a bull market. It is a flight of imagination, and like all such flights, it will end in the hard arithmetic of profit and loss. The commentator who welcomes more money into this frenzy does not ask where it comes from, or what it displaces. For every pound or dollar that chases Nvidia at 37 times earnings, there is one less for a company that yields 7 percent and buys back stock. This is not allocation. It is abandonment, a liquidity sink.

At Tobacco Vanguard, we favour the opposite direction. We favour the real, the returned, and the repeatable. An industry that throws off cash is more investible than a speculative one that does not. And a market where more money flows into spectacle than into solvency is a market in danger. Not of collapse necessarily, but of delusion.

Let others cheer liquidity. We shall hold the dividend.

#LiquidityTrap #SpeculativeMarkets #AIHype #TobaccoVanguard #RealReturns #DividendDiscipline #ValuationMatters #Mag7 #MarketDelusion #CashOverClicks #SoundCapital #InvestmentReality #ProfitAndLoss #YieldMatters #MoralMarkets

1

1

4

249

30 Jul 2025

ALTRIA: THE MARGIN REMAINS

By M. Reuven

Tobacco Vanguard, est. 1977

Not for all and sundry.

The quarterly results are in. And they are not explosive. They are not disruptive. They are not transformative. They are, in a word Altria has made its own: dependable.

In the second quarter of 2025, Altria repurchased 4.7 million shares at an average price of $58.63, returning $274 million to shareholders via buybacks. Over the first half, $600 million has gone to repurchases. Alongside this, $1.7 billion in dividends were paid in Q2 alone, with $3.5 billion returned year to date. The firm has now distributed more cash to investors in six months than most growth companies will generate in five years.

The dividend is not a promise. It is a fact. It is paid. It is banked. It is real.

Altria continues to honour the principle that defines true shareholder value: capital belongs to owners. The company has returned roughly $4.1 billion in H1 2025, with another $400 million authorised for repurchase before year-end.

Guidance and Market Signals

The full-year adjusted EPS guidance has been narrowed to $5.35 to $5.45, representing growth of 3% to 5% from the 2024 base. In a low-growth, high-risk market, this is no small thing. It reflects continued margin discipline, deliberate cost management, and a deliberate withdrawal from speculative excess.

Critics may point to modest growth. But they forget: Altria’s share count is falling, and its per-share cash return is rising. This is what compounders do. The effect is cumulative. The reward is long-term.

Altria notes tariff risks, inflationary pressures, illicit product dynamics, and smoke-free reinvestment. All valid. Yet in each case, the firm hedges, absorbs, or adapts. It is not invulnerable. But it is functional, in the most literal sense. It works.

The Nature of the Yield

In a market ruled by distortion, where entire firms trade at infinite multiples and narrative trumps profit, Altria remains the unspoken rebuke. It yields because it earns. It buys back because it can. Its guidance is conservative because it is based on knowns, not hopes. We are told this is old-fashioned. Perhaps it is. But so is compound interest.

The headline result was adjusted diluted EPS of $1.44, up 8.3% year on year, exceeding consensus by 4%. This figure, properly understood, represents the real productive output of the firm per share after tax. It is not padded by accounting tricks, nor flattered by hope. It is the yield of an operational machine.

Revenue net of excise taxes was $5.29 billion, flat on the year, but reflective of underlying pricing strength and volume resilience. The reported EPS of $1.41, down 36%, is largely noise, a technical outcome driven by non-recurring base effects, and irrelevant to long-term valuation. What matters is that margin discipline has held, the adjusted tax rate was 23.3%, and cash generation remains formidable.

#TobaccoVanguard #Altria $MO #Dividends #Buybacks #ValueInvesting #SoundMoney #RealMargins #Q22025 #CashFlow #CapitalReturn #DefensiveStocks #AdjustedEPS #Guidance #YieldMatters #MarketDiscipline #LongTermInvesting

5

133

30 Jul 2025

TOBACCO VANGUARD, est. 1977

Not for all and sundry.

VALUE REASSERTED

By M. Reuven

There comes a point in every market cycle when price catches up with truth. Not the truth of narrative or fashion, but the quiet arithmetic of yield, compounding, and return. We are, by all appearances, approaching such a moment once again.

For over a decade, Philip Morris International has been the darling of modern tobacco investors. It promised secular growth through reduced-risk products, expansion into smoke-free markets, and a forward-facing brand that would, supposedly, transcend the industry’s decline. In exchange, investors accepted a premium valuation and a lower yield, reassured, perhaps, by the language of innovation and regulatory leadership. British American Tobacco, by contrast, was treated as yesterday’s firm: unfashionable, overleveraged, and heavily reliant on combustible volumes in low-growth markets.

Yet capital, unlike commentary, is not sentimental.

Since the beginning of 2024, British American Tobacco’s ADR (BTI) has returned 76.6% on a price-only basis. Philip Morris International (PMI) has returned 70.6% over the same period. These figures are close. But when dividends are considered, the picture changes entirely. BTI now yields over 6%, while PMI yields around 3.4%. The effect is cumulative. The total return gap widens to over 10 percentage points, a vast gulf in financial terms, particularly for two firms in the same sector, operating under comparable macro conditions.

The reasons are not mysterious. BAT’s management has quietly deleveraged the balance sheet, stabilised U.S. combustibles, and scaled back RRP spending to favour profitability over posturing. PMI, meanwhile, has continued its expensive transformation, purchasing Swedish Match, absorbing ZYN’s growth into its valuation, and navigating an ever-complex global regulatory framework with a more modest shareholder payout. The result is a tale of two philosophies: one rooted in cash flow and return, the other in strategy and hope.

Tobacco Vanguard holds no brief for corporate sentimentalism. We assess value where it arises, not where it is spoken of. The re-rating of BTI is a reassertion of discipline over narrative. Its outperformance is not a speculative anomaly but a repricing of tangible reality: more yield, more return, more solvency.

Indeed, it may be said that the market is not so much endorsing British American Tobacco as it is ceasing to pretend otherwise. For years, the discount was irrational. Now it is merely narrowing. The recovery of BTI is not a trade, but a restoration.

And if we are to speak in philosophical terms, because this publication always will, then we might say the following: the age of promise is yielding to the age of proof. The investor, grown weary of growth stories and platform valuations, seeks now the comfort of margins, of dividends, of arithmetic.

In this light, the story of British American Tobacco is not a redemption. It is a return. A return to value, to discipline, to the facts of economic life. The sort of return that does not make headlines, but does, in time, build fortunes.

For the avoidance of doubt, Tobacco Vanguard has never accepted payment from any tobacco firm, and never shall. We write as observers, not apologists. All financial data as of 30 July 2025.

#TobaccoStocks #ValueInvesting #Dividends #BritishAmericanTobacco #PhilipMorris #TotalReturn #IncomeInvesting #EquityValuation #CashFlow #MarketDiscipline #YieldMatters #InvestorReturns #CapitalPreservation #BATS #BTI $BATS $BTI

1

3

111

30 Jul 2025

$MO EARNINGS UPCOMING

Altria reports in the morning.

Wall Street expects:

– Revenue: $5.19bn

– EPS: $1.37

The cash machine returns. No hype, no gimmicks, just margins, buybacks, and yield.

#Altria #TobaccoStocks #DividendStocks #EarningsSeason #MO #ValueInvesting #TobaccoVanguard #IncomeInvesting #CashFlow #YieldMatters #MonetaryRealism #AmericanTobacco #EarningsPreview

3

96

23 Jul 2025

TOBACCO VANGUARD, est. 1977

Not for all and sundry.

Editorial

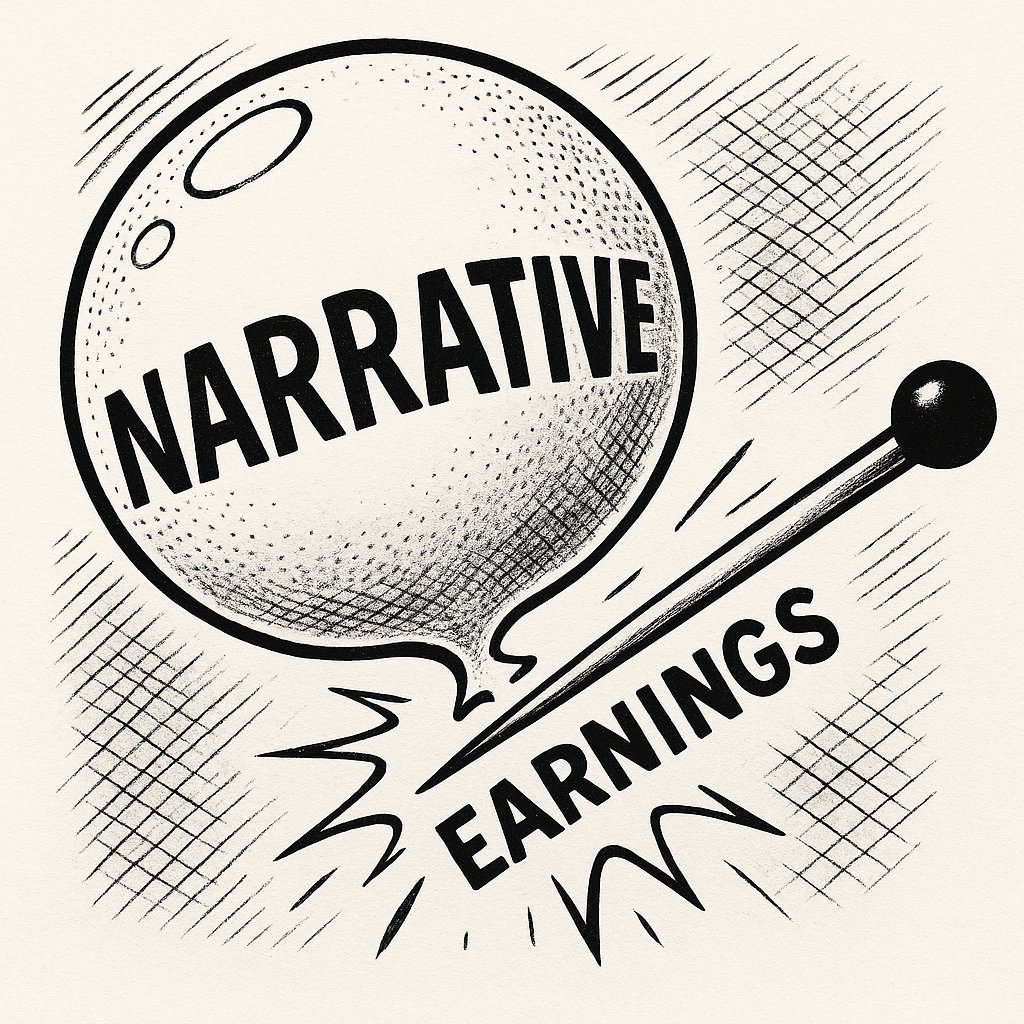

THE PRICE OF A STORY

By M. Reuven

Markets move on stories. But they do not stay there. Earnings anchor them, or they drift into the speculative ether, where bubbles form and eventually burst.

This is the lesson of history. From the tulip to the dot-com, and from Juul to ZYN, the pattern repeats. A product gains traction. A valuation expands. Narrative sets in. Expectations outrun results. And then, with time or pressure, the gap is closed not by growth, but by gravity.

Jeremy Grantham has long warned of such excess. So did Benjamin Graham. In their different ways, both understood that valuation is not arbitrary. It is a claim on future cash, not sentiment. Prices revert. Margins compress. Forecasts miss. What matters, in the end, is not what the market imagines, but what the company earns, and what it pays out.

This is why Tobacco Vanguard has never been entranced by the language of disruption. We favour companies that earn real profits, return capital, and resist the temptation to chase applause. We favour sectors, like tobacco, where pricing power and brand loyalty remain durable. But we also favour discipline. No product is immune from mispricing, not even a good one. A billion cans of ZYN may sell. IQOS may gain share. But a price-to-earnings multiple of 23 requires more than promise. It requires delivery, and quickly.

We have seen what happens when the delivery falters. Vape stocks in 2016. Cannabis equities in 2019. Cryptocurrency in 2022. The speculative premium vanishes faster than it formed, and those who bought at the top are left with losses.

This is not a plea for pessimism, only for realism. A stable sector is not a failure. It is an asset. Flat volumes and rising margins are not a crisis. They are a business. The great strength of the tobacco industry has always been its resistance to fashion. It makes its money, and it pays it out.

Half the battle, as Graham reminded us, is not losing money. Protecting capital is as important as multiplying it. And so, as others chase the next frontier, we look to the dividend, the buyback, the price paid for every pound of profit. When the wind changes, these are what remain.

Tobacco Vanguard does not oppose innovation. But we will not inflate it. We will not pay 30 times earnings for a can, nor accept narrative in lieu of income. We will take 6% yield and a quarterly cheque over blue-sky projections and sudden disappointment.

That is not cynicism. It is valuation. It is also survival.

#TobaccoVanguard #EquityMarkets #ValuationDiscipline #DividendStocks #ShareholderReturns #BenjaminGraham #JeremyGrantham #IncomeInvesting #MarketBubbles #MeanReversion #NGP #TobaccoStocks #ZYN #IQOS #Altria #BAT #ImperialBrands #PriceToEarnings #NarrativeRisk #RealEarnings #LongTermCapital #FinancialRealism #SectorRotation #DefensiveStocks #CapitalPreservation #YieldMatters #SmokeFreeTransition #ConsumerStaples #InvestmentPhilosophy #Buybacks #FinancialNarratives

2

66

23 Apr 2025

When it comes to weed control, winging it isn’t a strategy!

Brooklynne Dalton from @corteva breaks down how structured agronomic plans—starting with a solid preemergence and followed by the right postemergence—can make all the difference in yield, resistance management, and peace of mind.

Catch the full impact episode here: youtu.be/4jbB6wRITd4

#WeedControl #CornHerbicides #Corteva #EnlistCorn #ResicoreREV #Farm4Profit #CornSeason #CleanFieldsStartHere #CropProtection #AgPodcast #FarmPlanning #PreemergencePower #PostemergencePlan #YieldMatters

1

3

923

22 Apr 2025

The best yield potential a seed has is when it’s still in the bag—@corteva's here to help keep it that way by eliminating weeds before they steal your crop’s success!

Tune in to our latest Impact segment to learn from Brooklynne Dalton as she dives into how products like Resicore® REV and Enlist® herbicides work together to give your crop the clean start—and strong finish—it deserves.

Watch the segment here: youtu.be/4jbB6wRITd4

#WeedControl #CornHerbicides #Corteva #EnlistCorn #ResicoreREV #Farm4Profit #CornSeason #CleanFieldsStartHere #CropProtection #AgPodcast #FarmPlanning #PreemergencePower #PostemergencePlan #YieldMatters

1

4

984

17 Apr 2025

“The key to forward returns in bonds? Focus on the yield, not just the spread.” — Bill Housey

Catch this insight and more on the latest #ROIPodcast 👇

📺 tinyurl.com/kfxn84w9

🎧 tinyurl.com/3n6tzdxu

#FixedIncome #BondMarket #FirstTrust #YieldMatters

3

544

14 Jul 2023

All these pictures about how tall their hybrid xyz corn is on July 13. Who cares? It’s all tall. 🤷♂️ #yieldmatters

7

552

10 Mar 2023

Our expert Agronomist, Olivia Noorenberghe, shares her thoughts on the new A6566G8 hybrid

- NEW SmartStax® RIB Complete® hybrid for 2850 heat unit zones

- Combines top-end high yield potential and stability across soil types

prideseed.com/fieldtalk/a656…

#PRIDEinmyfield #YieldMatters

1

7

976

2 Mar 2023

🌱💰📈 As demand for food continues to rise, it's crucial that we find ways to produce more food without harming the environment. We can only do this by increasing yield per acre, improving efficiency, and reducing waste. 🌍🌾🥦

#YieldMatters #SustainableFarming #FoodSecurity

2

62

20 Oct 2022

Have you heard about @Asgrow_DEKALB new class of #Xtendflex soybeans? 3 new soybean varieties take the top 3 places in a Bureau County IL competitor plot. These new #XF3’s are truly the real deal! #YieldMatters #Harvest22 #Bayer4IL

1

6

16

28 Apr 2021

Agree love that project. I just keep adding on dip and stake it for #pol and more #tomo. #yieldmatters

2

24 Sep 2020

@AgriGold 2900RX as the sunsets in SW NE. Clean fields. 11% moisture. 58 lb TW. 250 gallon well. Field average 82 bu/ac. #extend #noraininaugust #yieldmatters

1

13

7 Jul 2020

@canterraseeds EXPs looking fabulous in @UFAcooperative #canola trial at Jim Stoutjesdyk's! Thx @brennanfazakas for including us!! #yieldmatters #westcdnag

1

5