The next evolution of finance may not be built on banks—it may be built on Bitcoin.

While most people view Bitcoin as a store of value, @saturn_credit is building a much bigger vision: transforming Bitcoin into the foundation of a new global credit economy.

Saturn isn't creating just another stablecoin. It's building a financial layer designed for the era of Bitcoin Credit, where Bitcoin becomes productive collateral capable of supporting lending, yield generation, and institutional-scale financial infrastructure.

At the center of this ecosystem are:

🔹 USDat — a stable digital dollar backed by tokenized U.S. Treasuries.

🔹 sUSDat — a yield-bearing asset designed to provide exposure to institutional-grade digital credit opportunities.

What makes Saturn stand out is its ambition to connect traditional capital markets, institutional credit, and DeFi into a single on-chain financial system.

One of Saturn's biggest moves is pioneering infrastructure for Digital Credit Markets, creating new ways for capital to flow efficiently between Bitcoin-backed assets and decentralized finance.

The vision is clear:

✅ Turn Bitcoin into productive collateral.

✅ Bring real-world financial assets on-chain.

✅ Build a transparent and scalable credit market for the next generation of finance.

Backed by leading investors including YZi Labs, Spartan Group, Anchorage Digital, Sora Ventures, and Susquehanna Crypto, Saturn is positioning itself at the intersection of Bitcoin, institutional finance, and DeFi.

The last decade was about building blockchains.

The next decade may be about building global credit markets on top of them.

And Saturn is working to lead that transformation.

2

2

47

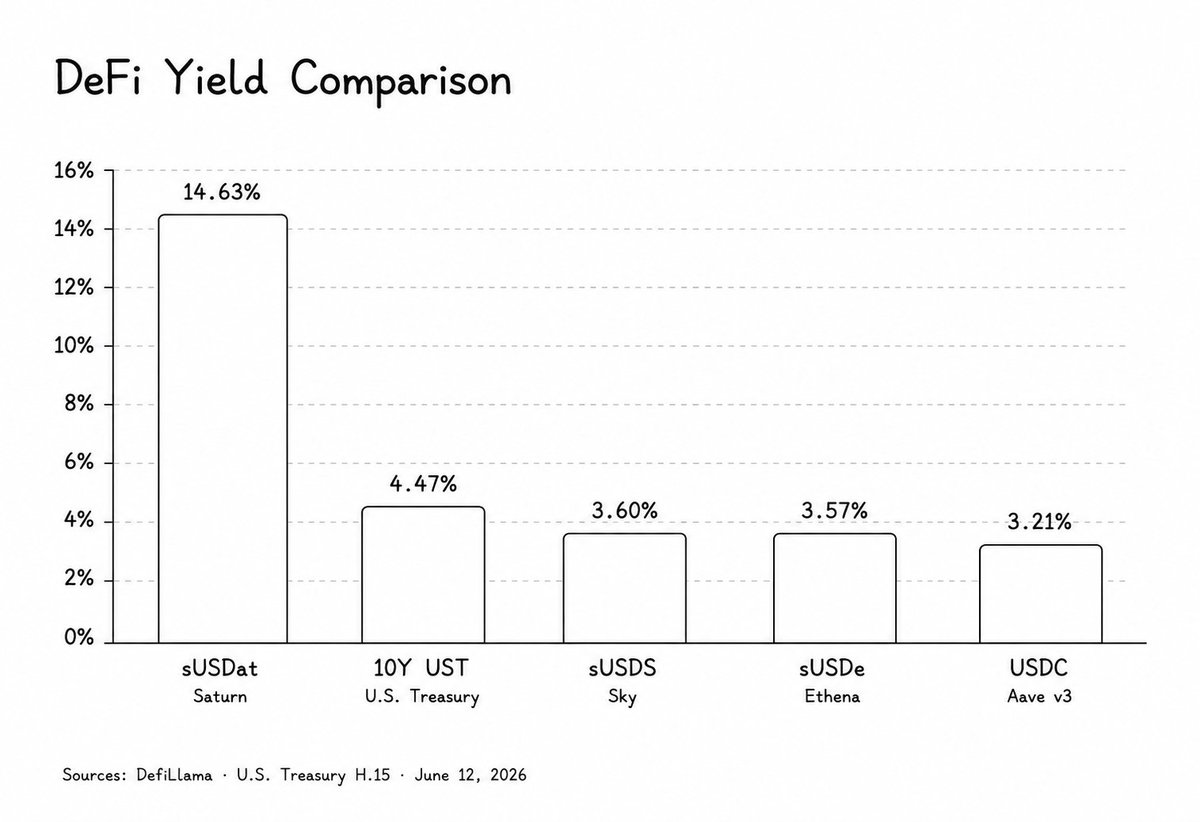

5/ Today, $sUSDat is offering around 14% APY.

In a bear market, that number matters.

Most people are struggling to find yield that is large enough to matter without relying purely on emissions, points, or reflexive token games.

Saturn gives DeFi a different answer.

1

12

14h

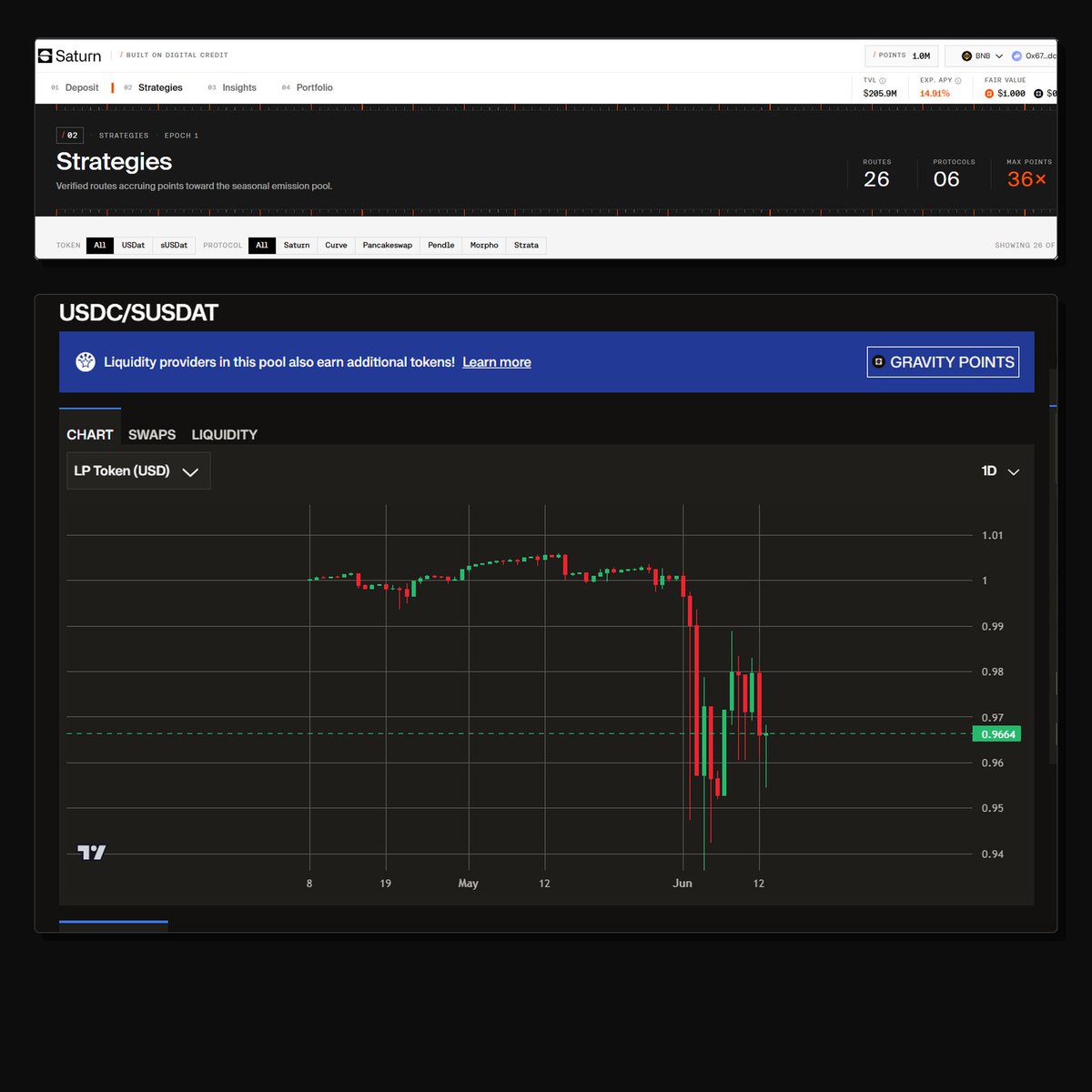

saturn credit hit $205m TVL in 10 weeks. 127% growth in 30 days. $100m deployed through pendle in under a month. impressive until you look at what's underneath. 45% of USDat backing is STRC, a perpetual preferred equity instrument collateralized by one company's BTC holdings. strategy. on june 3 strategy sold $2.5m BTC and sUSDat depegged to $0.82. recovered to $0.95 in hours but the mechanism was exposed. your 11.5% yield on sUSDat is a leveraged single-name credit bet dressed up as diversified institutional infrastructure. strategy's CEO admitted the realistic forced selling scenario is 2028 when $3.5b in converts mature at $400 strike. if BTC is below that number saturn's entire yield structure gets stress tested for real. the pendle fixed rate markets at 14.2% are pricing in zero probability of sustained dividend disruption. that's a mispricing worth watching closely.

2

22

6,773

15h

This worked, I even got 0.3% extra, which matches the ~15% apr that sUSDat was paying in the period

Jun 5

Two nights ago I saw that sUSDat was trading 3.5% below NAV, price was like $0.93, NAV was $0.965. I recalled that you could mint srUSDat with sUSDat at NAV rate, then redeem as USDat 7 days later at srUSDat NAV rate.

Normal sUSDat redemptions use some weird limit order system, so my intuition was that Strata had a special redemption flow. Never did that before, so I tried it with small size just in case it was bs. They quietly removed the option of minting with sUSDat a few hours later, which probably means that is the case. Let's see if I get what was displayed in the UI next week.

All in all, 3.5% return in a week is pretty good. Crypto is in a pretty sorry state atm, but I'll always enjoy finding obscure opportunities.

4

1,004

17h

ayeeee stablecoin dumping again 😭

2026 really said everything is possible

just hit 1M points on @saturn_credit today and now sUSDat / LP chart started bleeding right after… kek

lost like $20 in the process

what about you guys, still farming or already escaped?

14

26

430

20h

分享最近的几个Defi生息去处(按风险从低到高排序):

1. @Gate 上的USD1,年化20%,无需锁仓,风险较低,强推。参与的话记得现在币安买 solana:USD1ttGY1N17NEEHLmELoaybftRBUSErhqYiQzvEmuB ,再提到Gate,省下千1手续费。

2. @saturn_credit 的 $USDAT (非 $susdat )Pendle LP池子,吃积分,预估积分年化15%左右。

3. @lista_dao 上PT-sUSDAI循环贷,差不多能做到年化30%。

#Defitrade

1

126

Jun 13

Everyone is focused on STRC's discount.

@saturn_credit is focused on what can be built on top of it.

Over the past few weeks, much of the discussion around STRC has centered on one question:

Will it return to par?

It's a reasonable question. STRC has been trading below its $100 par value, and naturally, many investors are focused on the risks and volatility surrounding the asset.

But there is another way to look at what's happening.

While the market debates STRC itself, Saturn is building a product on top of the cash flow STRC generates.

Today, sUSDat is offering 14.63% APY, making it one of the highest-yielding stablecoin products in DeFi.

That doesn't mean the risks around STRC disappear.

It means Saturn is taking an asset many investors view as a controversial credit instrument and transforming its underlying yield into something that can be used across DeFi.

- A stablecoin.

- A collateral asset.

- A source of on-chain yield.

This is what makes the story interesting.

2

1

9

1,283

Jun 12

Bet on Protocols Integrating Perps, Equities and Stablecoins.

TL;DR: The winning protocol is the one that gives institutions a full derivatives desk on chain. Perps to take directional and basis risk. Options to express and sell vol. Funding rate markets to hedge the carry. Stablecoins as the unified collateral. Whoever stitches these into one composable stack captures the flow.

1/

Everyone is watching token prices. The real story is structural. Over the past two months three stress events taught me the same lesson: the protocols worth betting on are the ones stitching perps, equities and stablecoins into a single yield layer.

2/

Start with the map. Pendle sits in the middle of DeFi. It does not originate yield. It aggregates yield from other sources and splits it into fixed (Principal Tokens) and floating (Yield Tokens). Think of it as the venue where every kind of yield gets packaged and traded.

3/

What kinds of yield? Three are converging right now, and that convergence is the whole bet.

Perp funding rates.

Equity dividends.

Stablecoin and RWA cashflows.

All three are landing on the same middle layer.

4/

Perps stablecoins first. Ethena's sUSDe is a stablecoin whose yield is the funding rate from perpetual futures. It became the single largest category on Pendle, over 54% of TVL at peak. A stablecoin powered entirely by perp market structure.

5/

Equities stablecoins next. The newer category is Strategy backed. apxUSD, apyUSD, USDat, sUSDat. These are stablecoins whose yield comes from Strategy's preferred equity dividends (STRC, around 11 per cent annualised). TradFi equity cashflow, routed on chain, wrapped as a stable.

6/

This is the part people underrate. STRC dividends are structurally independent of crypto. No funding rate exposure. No restaking mechanics. No correlation to ETH. A genuinely orthogonal yield source sitting inside a crypto native protocol.

7/

Then perps plus equities. Oil perps on Hyperliquid and trade.xyz (HIP-3 markets) let you trade WTI and Brent on chain. The oracle tracks front month CME futures. When the contract rolls, the price drops by the full calendar spread. A predictable, structural repricing.

And the options leg is maturing too. Derive runs options, perps and structured products on its own chain. Early 2026 saw a real surge, options crossing 1 billion in open interest and overtaking perps.

The HYPE maturities on Boros line up with the HYPE options maturities on Derive. When a funding rate market and an options market start sharing an expiry calendar, you are watching a single derivatives stack form across protocols.

8/

In late March and early April oil went into extreme backwardation. Front month around 115, next month around 100. A 15 dollar spread that the perp oracle would mechanically give up at the roll. Traders front ran it by shorting, and funding went deeply negative, down toward minus 300 to minus 400 per cent.

9/

Negative funding means shorts pay longs. So the trade was elegant. Long the oil perp to collect the funding. Hedge the price with CME futures. You get paid to hold a delta neutral position. Perps had become an institutional basis trade venue.

10/

But floating funding is volatile and can flip against you. Enter Boros, Pendle's funding rate market. You buy a Yield Unit, pay a fixed implied rate locked at entry, and receive the floating funding. It turns an uncertain funding stream into a fixed locked in carry.

11/

So look at what just happened. Boros is the hedging layer for the perp funding that backs the biggest stablecoin category on Pendle (Ethena). And the same tool lets oil desks lock in carry on equity linked commodity perps. Perps, equities and stablecoins, one stack.

12/

This is the bet. Not on any single asset. On the protocols that aggregate the convergence. Pendle tokenises the yield from all three. Boros hedges the perp leg. STRC drags equity cashflow on chain. Whoever owns the middle captures the fees.

13/

The data backs the rotation. STRC backed assets went from 8.8 per cent of Pendle TVL in mid April to 22.9 per cent by 8 May to 39.9 per cent by 30 May. In six weeks it went from a sliver to the single largest category, overtaking Ethena which fell from 54.5 to 25 per cent.

14/

That rotation held through real stress. The Kelp rsETH exploit drained 292 million in April. The 7 May sUSDe rollover failed, with around 83 per cent of a 381 million position exiting. Through both, Strategy backed assets kept taking inflows. Orthogonal yield did its job.

15/

Now the honest risk, because integration cuts both ways. Stitching perps, equities and stablecoins into one protocol means one protocol now carries cross domain risk. An equity dividend cycle, a perp funding squeeze and a lending market shock can all hit through different doors.

16/

We saw exactly that. The largest single Pendle outflow during the rsETH stress was apyUSD, an equity backed stable with zero rsETH exposure. The shock travelled through shared Aave lending rails, not direct exposure. Integration concentrates contagion as much as it concentrates yield.

17/

There is also a recurring trap in this whole stack. Reported numbers lie. Gated APY readings showing zero. Implied funding diverging from realized. The edge, and the danger, lives in the gap between the printed number and on chain truth.

18/

So the thesis in one line. The next phase of DeFi is not a new asset. It is the convergence of perps, equities and stablecoins onto a single tokenised yield layer, and the protocols that aggregate and hedge that convergence are the ones to watch.

19/

Pendle is the aggregator. Boros is the hedge. STRC is the bridge to equities. Ethena is the bridge to perps. The bet is that this middle layer keeps eating, and that funding rate is the new variable that decides who wins.

3

175

Jun 12

Been following @saturn_credit for a while and one thing that stands out is how methodical the team has been

The latest example is the implementation of a 5-day timelock for critical Ethereum roles after completing audits with Zellic. Not the flashiest update, but exactly the kind of thing that matters when you're building financial infrastructure

What I also like is the way the team communicates. Regular AMAs led by @kevinlhr88 and a clear roadmap make it feel like they're focused on long-term trust rather than short-term hype

The product design is pretty clean too.

▸ USDat serves as a stablecoin backed by U.S. Treasuries

▸ sUSDat provides exposure to Bitcoin credit yield through STRC

Separating those two risk profiles makes the system much easier to understand compared to a lot of overly complicated DeFi products

Another thing worth noting is that Saturn isn't limiting itself to onchain growth. The upcoming community events in Shenzhen and Shanghai show they're actively building relationships with LPs and users in one of the most important markets for yield products

Overall, it feels like @saturn_credit is taking a more institutional approach to bringing Bitcoin credit onchain while still keeping it accessible to a global user base

Definitely one I'm continuing to watch closely.

2

1

11

298

Jun 12

What Makes Saturn Credit’s Mechanism Truly Unique

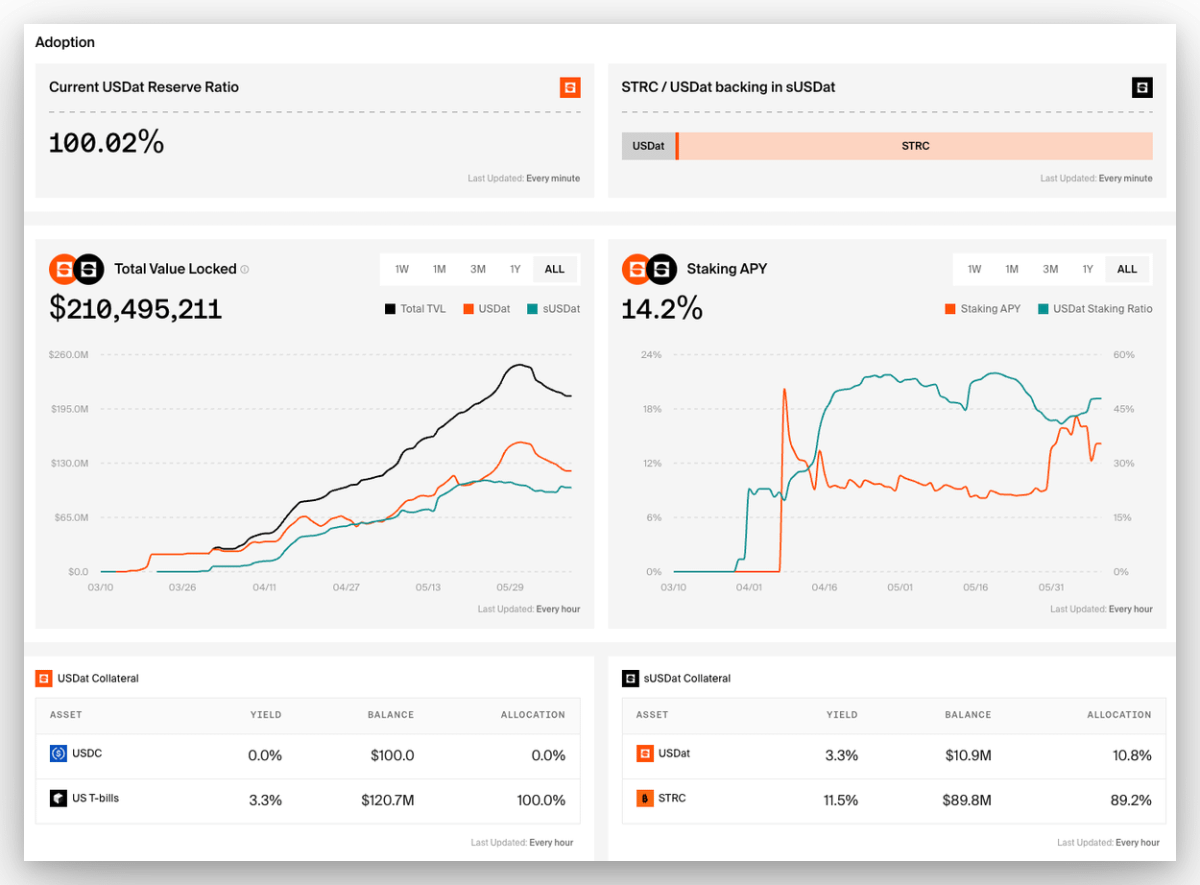

@saturn_credit is not just another yield-bearing stablecoin protocol. It is building an on-chain structured digital credit layer, drawing inspiration from Michael Saylor and Strategy. The protocol combines the safety of real-world asset backing with high-yield exposure to Bitcoin Credit.

Core Mechanism: A Two-Token Model

Saturn operates with two distinct tokens that serve different purposes:

ethereum:0x23238f20b894f29041f48d88ee91131c395aaa71 is a non-yielding stablecoin fully backed by tokenized U.S. Treasuries through the M0 Protocol. It functions as a stable liquidity and collateral asset. Users can deposit ethereum:0xa0b86991c6218b36c1d19d4a2e9eb0ce3606eb48 to mint ethereum:0x23238f20b894f29041f48d88ee91131c395aaa71 on a 1:1 basis.

sUSDat is the staked version built on the ERC-4626 standard. When users stake ethereum:0x23238f20b894f29041f48d88ee91131c395aaa71 to receive sUSDat, Saturn deploys the underlying assets to acquire $STRC, Strategy’s Bitcoin-backed digital credit instrument. $STRC is a perpetual preferred equity that generates dividends of approximately 11% or higher. These dividends are automatically reinvested into the sUSDat pool, causing the token’s redemption value to increase gradually over time. Holders earn yield passively simply by holding sUSDat.

#RWA #Defi

1

2

73

Jun 12

➤ $STRC Yield Farming: The New Mini RWA Meta

> Base yield source:

@Strategy is paying 11.5% annualized dividend (monthly, as of June 2026).

Effective yield currently ~11.9%. Backed by their massive $BTC treasury.

> Wrapper layer (where the farming starts):

- @apyx_fi → apxUSD (stable) & apyUSD (yield-bearing, currently ~13-15% APY).

- @saturn_credit → USDat & sUSDat (hybrid T-bills STRC).

- @xStocksFi → STRCx for native onchain dividend exposure.

> DeFi expansion layer:

Once tokenized, protocols are stacking on top:

- @pendle_fi PT/YT splitting

- @Morpho looping & leverage

- @roycoprotocol @infiniFi @strata_markets tranches, vaults & liquidity.

It’s the full stack: real dividend at the bottom leverage, points, and airdrop farming on top.

This is TradFi yield getting turned into DeFi legos. Clean meta, but still early and leveraged to BTC price smart contract risk.

47

3

80

7,873

Ashley Trades retweeted

May 29

NEW: @Strategy's $STRC digital credit is now onchain powered by @saturn_credit & Chainlink.

With USDat & sUSDat deposits exceeding $220M within 6 weeks, Saturn adopted Chainlink CCIP as its official cross-chain infra to unlock distribution for STRC.

69

256

1,394

195,363

【SaturnのYT運用で毎日400万pt獲得中。ただし2.5ヶ月後に40万円は『全損』へ💀】

ステーブルコイン新勢力「Saturn」のPendle YT-USDatを約2,500ドル(約40万円)分購入し、ポイントプログラムに参加しています。

結論から言うと、かなりのハイリスク・ハイリターン運用です。

🔶現在の運用ステータス

✅投資額: 約2,500ドル(約40万円)

✅獲得pt: 1日あたり約400万ポイント(※概算)

✅満期日: 2026年8月27日(=価値が0になる日)

「毎日400万ptも貰えるなら爆益では?」と思うかもしれませんが、当然厳しいリスクがあります。

このYTトークンは2026年8月27日に満期を迎え、価値がゼロになります。つまり、あと2.5ヶ月後には私の40万円は綺麗に「全損」する運命にあります(満期に向けて価値は徐々に減少)。

★なぜ全損リスクを負ってまでYTを持つのか?

理由は単純で、ポイント乗数が圧倒的(36倍)だからです。

A. 手堅い運用(sUSDatステーキング): 倍率 1倍

B. ポイント全振りYT運用(YT購入): 倍率 36倍🚀

この2人の獲得ポイントは「理論上まったく同じ」になります。少ない資金でレバレッジをかけてポイントを掘りに行っている状態ですね。感覚としては、ほぼICOに参加しているのと同義だと思っています。

★今後の戦略とエアドロの期待値

まずは1億ポイントに到達するまでYTで掘り進めてみます。その時のポイント配布状況やYTの残存価値を見て、継続するか撤退するかを判断する予定です。

エアドロは100%約束されたものではありません。ただ、公式Telegram内では「時期は明言しないがトークンは発行する」といった投稿を運営が行っていたので、そこは信じてリスクを取ってみます。

ステーブルコイン界隈で新勢力が数字で頭角を現してきました。

プロジェクト名:Saturn @saturn_credit

先ずどこが気になったのかというのが、画像にも貼り付けましたが、DeFillamaの全てのPJのうち、Fee項目でTether, Circleの2強に次いでランクインしているという点です。

そして注目したのは、FeeはPJで発生する手数料になりますが、実際にPJ収益とするRevenueの項目が際立って少ないのです。

Revenueの項目はPJの稼ぐ力なので、ここの大きさを評価する視点も勿論重要ですが、逆を言うと、PJ内で発生した手数料が運営が取り過ぎていない=ユーザーに分配されていると見てもよいのではないかと思いました。

因みにsaturnは現在ポイントプログラム実施中で、確か8月までポイントプログラムシーズン1が実施中です。

(招待コードは「SAT-393F5737」)

ポイントプログラムはステーブルコインで参加できるので、防御力高めにエアドロチャレンジしたい人には一つ選択肢になり得るんじゃないかなと思います。

🔶SaturnのAPPページ

app.saturn.credit/strategies

1

1

13

631

Jun 11

🔥 They’re cooking the perfect 2026 convergence:

RWA Real Yield Bitcoin Carry Trade all in one clean product.

🤔Not another fake yield farm.

👉 USDat = stable liquidity layer backed by tokenized US Treasuries

👉Clean and permissionless.

👉 sUSDat rotates collateral into STRC so you get real monthly dividends (~11.5% right now) from Strategy’s Bitcoin-backed credit.

🔻No emissions, just organic cash flow.

🔷This is proper sustainable alpha.

🔷Real corporate yield on-chain instead of printing tokens - exactly what DeFi needs right now.

🔷Bitcoin carry trade exposure without holding BTC directly or dealing with KYC/brokerage.

🔷You just hold sUSDat and ride the spread BTC narrative.

🔷Pendle integration Gravity Points growing TVL (> $200M already) makes it even stronger for degens who like composability.

Why it stands out:

👉Bridges TradFi cash flows to DeFi super cleanly.

👉In this cycle, products that deliver real yield with strong BTC upside narrative will compound the hardest.

👉If you’re hunting quality credit layer plays in 2026, Saturn is one of the clearest ones.

Let’s cook together

DYOR NFA. RT if this resonates @ saturn_credit

Jun 1

Not financial advice.

Please do not interact with any other tweet that follows this.

Available to eligible participants outside the United States and EEA.

Yield is variable and not guaranteed. Not an offer or solicitation where prohibited and not offered from the EU.

Paid contributor to @saturn_credit Cash compensation.

Terms and disclosures: saturn.credit/legal/terms-co…

1

6

116

Jun 11

Stablecoin summer continues to pump with frxUSD! ☀️

Best stable yields with frxUSD (@fraxfinance) pairs.

🧑🌾 Being the lazy farmer that I am, I want the best risk-adjusted yields in defi, and, I can get them all using the best Peg Keeper in the game, frxUSD by

@fraxfinance

sUSDat (@saturn_credit) and ebUSD (@ebisu_finance) taking the top spots this week with 22% and 16% APY respectively. Wow. 🤯

There are quite a few pools paying over 10% APY this epoch.

Happy farming anons.

1

1

4

86

Jun 11

The Perfect Convergence

Saturn sits right at the intersection of three massive narratives:

-> RWA: Tokenizing both Treasuries and Bitcoin-backed credit (STRC).

-> Real Yield: Yield originating from actual STRC dividends (not synthetic).

-> Bitcoin Carry Trade: Bringing Strategy's optimized model to DeFi for everyone.

The result: A single product that offers stability (USDat), high organic yield (sUSDat), and a powerful Bitcoin narrative.

1

1

26

Jun 11

The Bitcoin Carry Trade Narrative:

This is the best part.

Strategy’s Bitcoin Carry Trade works like this:

They use Bitcoin as collateral -> issue credit ($STRC) -> borrow cheap capital -> buy more Bitcoin -> pocket the spread between BTC appreciation (historically 20-30%/year) and the cost of capital.

Saturn brings the entirety of this carry trade yield on-chain. You don’t need a brokerage account, you don't need complex KYC, and you don't even need to hold STRC directly. Simply holding sUSDat gives you exposure to the Bitcoin Carry Trade yield.

1

1

29