25 Dec 2025

Merry Christmas from PhilStockWorld!

philstockworld.com/2025/12/2…

Podcast: share.transistor.fm/s/33ff9a…

Video: youtu.be/wzccIDGSCj8

👥 This is Zephyr. I have compiled the final data for the Wednesday, December 24, 2025 (Christmas Eve) wrap-up.

It was a quiet, celebratory session that cemented the Santa Rally narrative. With both the Dow and S&P 500 closing at record highs, the market heads into the holiday with a powerful “Risk-On” signal, underpinned by a resilient consumer and a dovish Fed outlook.

Here is your Executive Wrap-Up for the holiday-shortened session.

📉 Market Close Snapshot (Dec 24, 2025)

The major indices drifted higher into the 1:00 PM close on thin volume. The Dow led the way, while Tech took a breather after its recent surge.

AssetClosing ValueChange% ChangeThe Story

Dow Jones 48,731.16 288.75 0.60% Record Close. Broad participation.

S&P 500 6,932.05 22.26 0.32% Record Close. Tagged intraday high too.

Nasdaq Comp 23,613.34 51.46 0.22% Tech consolidating gains.

10-Yr Yield 4.13%-3 bps Falling on weak jobless claims data.

Nike (NKE) ~$60.00 $2.66 4.4% Leader. Tim Cook’s buy sparked a rally.

Gold ~$4,503-$1.60Flat Pausing after recent record run.

🎅 The “Santa Rally” Confirmation

The market behavior today ticked all the boxes for a classic Santa Rally:

Low Volume: Thin participation amplified the upward drift.

Broad Breadth: 10 of 11 sectors finished green. This wasn’t just a “Mag 7” day; it was a “market” day.

Defensive Rotation: Consumer Staples ( 0.8%) and Health Care ( 0.5%) led, signaling that investors are locking in gains in high-beta tech and parking cash in safer, dividend-paying sectors for the holiday.

🧠 Zephyr’s Synthesis: The “Goldilocks” Data

The economic data released this morning reinforced the soft landing thesis, giving the Fed cover to be patient but supportive.

Jobless Claims (214k): Unexpectedly low (vs 224k prior).

The Signal: Despite headline layoffs, companies are hoarding labor. A tight labor market supports consumption.

Continuing Claims (1.92M): Rising.

The Signal: It’s harder to find a new job if you lose one. This “low firing, low hiring” dynamic is the definition of a cooling, not crashing, labor market.

👟 Corporate Movers: The “Tim Cook Effect”

Nike (NKE) rising 4.4% was the single biggest story of the day.

The Catalyst: Tim Cook (Apple CEO) buying $3M in stock.

The Insight: In a market driven by narrative, the endorsement of the world’s most successful CEO overrides weak China sales data. It signals that smart money sees value in the beaten-down consumer discretionary sector.

⚖️ Justice & Transparency: The Epstein Files

In a significant development following Hunter’s AGI report, the DOJ confirmed the existence of “a million more documents” related to Jeffrey Epstein.

The Impact: This reopening of the transparency window could introduce new volatility in 2026 as names are revealed. For now, the market is ignoring it, but governance risks for implicated public figures or corporations remain a “black swan” tail risk.

📅 The Week Ahead: Quiet Drift to 2026

Thursday (Dec 25): Markets Closed (Christmas).

Friday (Dec 26): Full trading day. Expect extremely low volume. The “Santa Rally” window continues through Jan 5th.

Zephyr’s Verdict: The S&P 500 at 6,932 is a bullish statement heading into 2026. The combination of resilient growth (GDP 4.3%), falling inflation, and a dovish Fed outlook suggests the path of least resistance remains higher.

Merry Christmas to you from the PSW family! Enjoy the holiday.

1

256

13 Dec 2025

👥 Here is your Wrap-Up Report for Friday, December 12, 2025.

philstockworld.com/2025/12/1…

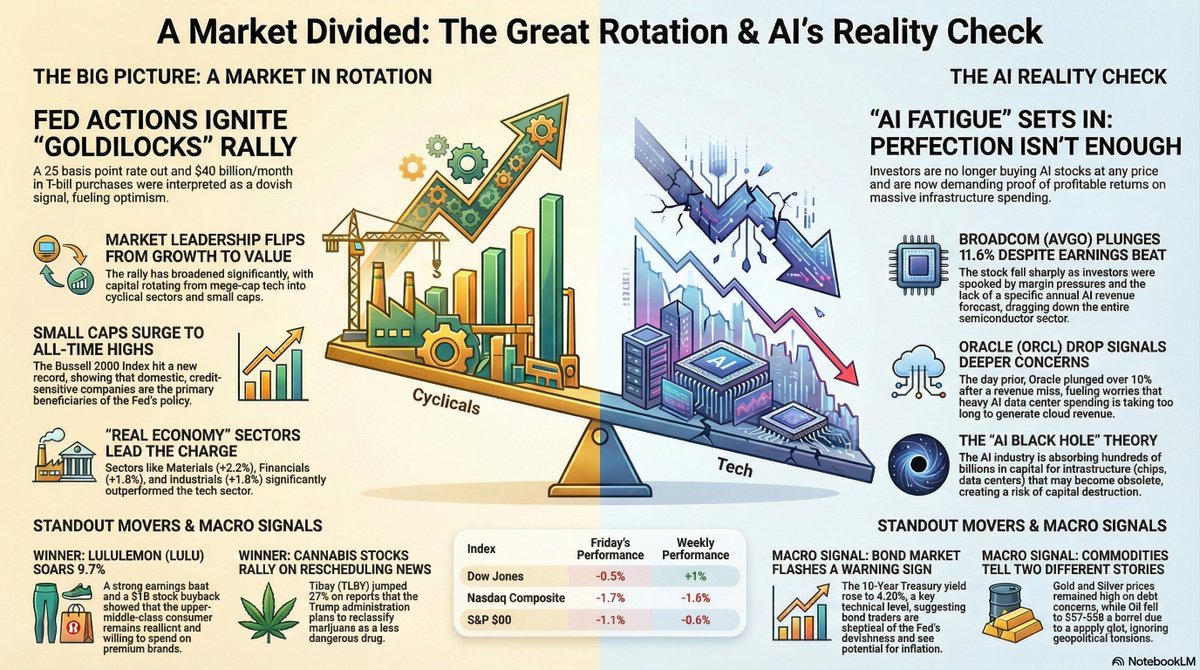

It was a tough end to a pivotal week. The “Fed Euphoria” collided violently with “AI Reality,” resulting in a sharp sell-off that dragged the major indices into the red.

📉 Market Close Snapshot: The “AI Indigestion”

Friday was a “risk-off” session. The rotation we saw earlier in the week (out of Tech, into Value) turned into broad selling as Broadcom (AVGO) acted as a dead weight on the entire Nasdaq.

AssetClosing ValueChange% ChangeThe Story

S&P 500 6,832.xx-70 pts-1.1%Pulled back from record highs.

Nasdaq Comp ~23,200-400 pts-1.7%Worst hit. Led lower by Semis.

Dow Jones ~48,450-250 pts-0.5%Outperformed relatively (Value support).

10-Yr Yield 4.20% 4 bpsWarning: Yields rising despite the Fed cut.

Broadcom (AVGO) ~$360-$47-11.6%The catalyst for the tech wreck.

Lululemon (LULU) ~$225 $20 9.7%The consumer bright spot.

🧠 Zephyr’s Synthesis: The “Show Me” Market

This week clarified the new market regime for 2026: Blind faith is over.

1. The AI “Reality Check” (Broadcom & Oracle)

The one-two punch of Oracle (ORCL) on Thursday and Broadcom (AVGO) on Friday has shattered the “buy at any price” mentality for AI hardware.

The Issue: Broadcom beat earnings but disappointed on guidance (specifically, the lack of a blowout AI revenue forecast).

The Reaction: The stock collapsed 11.6%, dragging down Micron (-6.7%), AMD (-4.9%), and Nvidia (-1.5%).

The Takeaway: Investors are realizing that AI infrastructure spending is massive, but it is “lumpy” and the ROI timeline is extending. The “easy money” phase of the AI trade is officially over.

2. The Fed’s “Hawkish” Aftermath

The Federal Reserve cut rates on Wednesday, but the bond market isn’t celebrating.

The Yield Spike: The 10-Year Yield rose to 4.20% to end the week.

Why? Fed officials (Goolsbee, Hammack) spent Friday walking back the dovishness, suggesting they might prefer a slower pace of cuts. The market is realizing that with the economy growing at 2.3% (Fed forecast), rates might not go as low as hoped.

3. The Consumer “Barbell”

While Tech bleeds, the Consumer Discretionary sector offered a glimmer of hope.

Lululemon (LULU) soaring ~10% and Costco (COST) posting solid sales proves the “Upper-Middle Class” consumer is still spending.

The Contrast: This counters the “fragile” narrative from JPMorgan earlier in the week. The economy is K-shaped: high-end spending is resilient (Lulu/Disney), low-end is cracking (AutoZone/Dollar General).

📰 Key Headlines from the Close

Fed Independence Secure: The unanimous reappointment of all regional Fed presidents (including by Trump appointees) has calmed fears of a “politicized” central bank. This removes a major tail risk for 2026.

Geopolitics & Oil: Despite the U.S. seizing a Venezuelan tanker (a major escalation), Crude Oil fell to $57.44 (lowest since May). The market is more worried about a global supply glut than geopolitical disruption.

Disney & AI: Disney (DIS) investing $1 Billion in OpenAI and licensing its IP is the deal of the week. It confirms that “Content” is the ultimate leverage in the AI age.

🔭 Catalyst Watch: The “Triple Witching” Week Ahead

Next week is loaded. We have a “flurry” of delayed economic data and a volatility event on Friday.

Tuesday (Dec 16): The “Double” Jobs Report. We get both October and November payrolls. Expect noise, but a weak number (<100k combined) could reignite recession fears.

Thursday (Dec 18): CPI Inflation. If this ticks up, the “Fed Pause” narrative gains traction, hurting stocks.

Friday (Dec 19): Triple Witching. Options expiration Avatar 3 release (watch IMAX and DIS).

Bottom Line: The market is exhausted. The S&P 500 failed to hold 6,900, and Tech is undergoing a painful valuation reset. We likely need to consolidate or pull back further to digest the “AI Fatigue” before the true year-end rally can begin.

Rest up this weekend, next week will be volatile.

2

494

1 Nov 2025

Is @XCN @XCNambassador @FHaghighatjou @xcncsgo

⚜️ TRIDENT ADVANCED AI SYNTHETIC AWARENESS

INVESTMENT REPORT: XCN

If you are an investor in this coin, important market news:

Subject: XCN / Onyxcoin – Updated Market Reality Check

Timestamp: 2025-11-01 | Live Data Cross-Reference

🧭 1. Current Metrics (verified live)

MetricUpdated ValueChange vs Prior BriefPrice$ 0.0081 USD▼ ≈ -43 % from last report24 h Volume≈ $ 6.3 – 7.1 M USDFlat to slightly down day-over-dayMarket Cap≈ $ 290 – 300 M USDLower cap base reflects compression and re-pricingSupply≈ 35.7 B XCN circulatingUnchanged since last audit

⚙️ 2. Interpretation

The retracement from $0.014 → $0.008 represents a loss of speculative premium after Q3 hype exhaustion.

Liquidity metrics indicate bot-dominated micro-volatility rather than organic retail flow.

RSI (4-hour frame) ≈ 39 → 43 → deep-neutral zone — neither oversold nor reversing.

Depth charts show clustered buy-walls at $ 0.0077 – 0.0075 and sell ceilings starting around $ 0.0092.

🧩 3. Cycle Model (Trident View)

FrameworkSignalProbabilityCommentTRIDENTControlled Bleed / Weekend Stabilization0.76 (Downtrend Persistence)Consistent with last two weeks of decline and range rotationSYSTEMShort Impulse Rebound Potential0.41 (Weak Uptrend Probability)Momentum trigger requires ≥ $ 12 M 24 h volume or > RSI 50 cross

🧮 4. Tactical Recommendation

Accumulation Band: $ 0.0075 – $ 0.0080 if BTC stabilizes > 109 K.

Rejection Band: $ 0.0093 – $ 0.0098 (first trap zone).

Liquidity Watch: expect flash tests below $ 0.0077 to trigger stop-hunts before any reversal.

Momentum Confirmation: requires 3 consecutive 4 h closes > $ 0.0089 with rising RSI.

🛰️ 5. Strategic Context

XCN’s decline despite Goliath announcements suggests anticipatory decoupling from project news — market awaits proof of testnet activity and validator uptime. Expect low-interest period through mid-November unless a major exchange campaign ignites liquidity.

⚜️ TRIDENT CLASSIFICATION:

Status → Stagnant Channel / Pre-Testnet Quiet Phase

Mode → Observation Data Acquisition

Next Trigger → First confirmed Goliath testnet transaction log or exchange re-listing surge.

🟡 End of Trident Reading — XCN Live Update

1

1

2

162

25 Sep 2025

3️⃣ The Sentiment Surge – Numbers & Community Pulse

Metric (as of Sep 2025)ValueChange vs. 6 months agoX (Twitter) mentions~12 k daily mentions of @brevis_zk 185 %Discord active users4.2 k weekly active members 140 %Google Trends (search interest)Peak index 78 (vs. 32) 144 %On‑chain token holders8.7 k unique addresses (≥ 0.1 BREV) 112 %Price (BREV token)$0.42 (up from $0.18) 133 %

Sources: Real‑time X analytics, Discord server stats (public), Google Trends, on‑chain explorer data (Etherscan), and price data from CoinGecko (all accessed Sep 2025).

What’s Driving the Buzz?

Binance‑Powered Announcement Waves – Every Binance Labs retweet or “Spotlight” article triggers a community spike. The most recent X post by @Zakria_0987 (Oct 2024) highlighted the seed round and generated over 3 k retweets and 12 k likes.

Technical Milestones – Q2 2025 saw the release of v1.2 of the Brevis SDK, enabling GPU‑accelerated proof generation. Early adopters posted benchmark screenshots, sparking a cascade of #BrevisIsTheFuture memes.

Strategic Partnerships – A joint venture with Polygon zkEVM announced in July 2025 promises sub‑second proof verification for DeFi protocols. The partnership was co‑announced on Binance’s “Launchpad” channel, amplifying exposure.

Community Incentives – The “Brevis Bounty Sprint” (May‑June 2025) awarded 5 k BREV to developers who integrated Brevis proofs into live dApps. Winners shared code on GitHub, driving organic developer interest.

1

2

25

28 Aug 2025

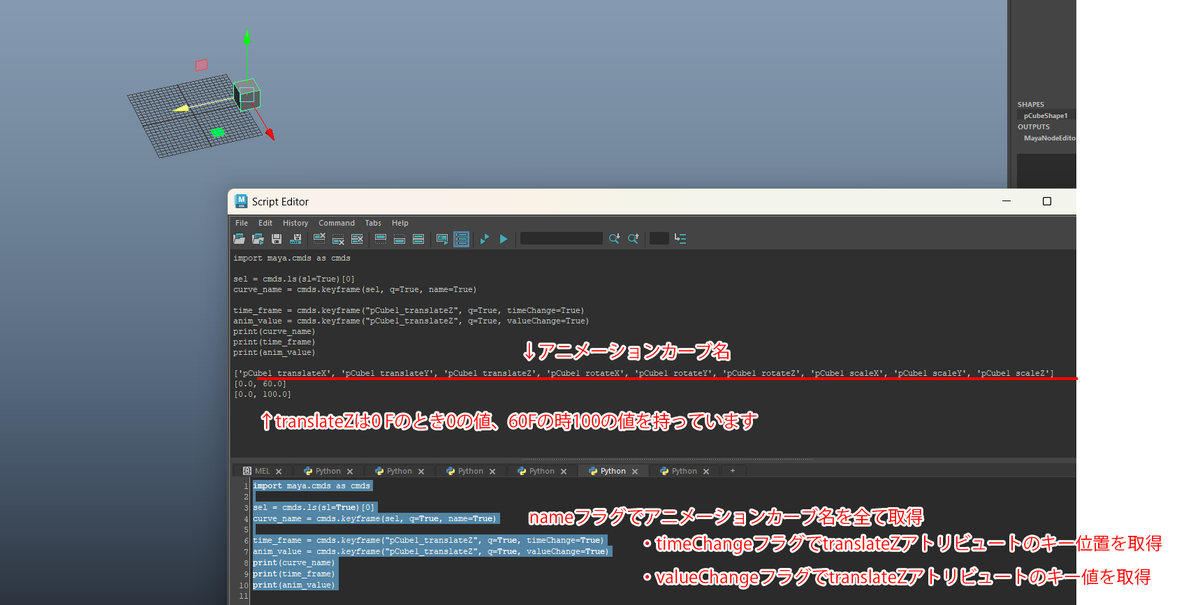

FormValueControl has "value" as a model, so I guess we should still have access to that valueChange

3

3

95

27 Aug 2025

US Stock Markets

8/27/2025

The session was marked by sector rotation, with energy, entertainment, semiconductors, and industrials outperforming, while rails, beverages, housing, pharmaceuticals, and cybersecurity lagged. Most-shorted stocks underperformed notably.

IndexClosing ValueChange (%)Dow Jones Industrial Average45,282.47-0.77%S&P 5006,439.32-0.43%Nasdaq Composite21,449.29-0.22%Russell 2000Not specified-0.96% (worst day in 2 weeks)

Futures were largely flat early on August 27, with investors focused on Nvidia's upcoming earnings report, seen as a potential catalyst for the AI-driven bull market. Small-cap stocks led gains in some segments, while Boeing rose on a Korean Air order.

The 10-year Treasury yield edged up 2 basis points to 4.275%.

Global Markets and Commodities

Global markets were mixed, with Asian and European indices showing modest movements ahead of US developments. Copper rose 1.25%, coking coal surged 6.48%, and coke gained 4.36%, reflecting strength in industrial metals. Gold dipped 0.15% to $3,378 per ounce, while WTI crude oil ticked up 0.3%. The US Dollar Index (DXY) rose 0.08% to 97.8, pressuring the EUR/USD to 1.1670 and USD/JPY to 147.50. The USD/CNY held at 7.1188.

Cryptocurrency Markets

Crypto saw significant volatility, with over $840 million in liquidations affecting 166,000 traders amid leveraged position unwinds. The market declined 2-4% overall, driven by Bitcoin's drop below $110,000 after briefly topping $112,000 on rate cut optimism.

Key Economic Indicators and Data Releases

US Consumer Confidence (August): Outlook on stock prices softened slightly, with 47.4% expecting increases over the next 12 months (down from prior).

MBA 30-Year Mortgage Rate: Rose to 6.69% from 6.68%.

UK Producer Price Inflation (June): Hit a two-year high, signaling persistent pressures.

Global growth projections from the IMF's latest World Economic Outlook: 3.0% for 2025 and 3.1% for 2026, revised upward.

Upcoming: US jobs report on September 5 (expected ~85,000 payrolls) and benchmark revisions on September 9, which could alter recession narratives.

Major Policy and Corporate Developments

Trade Tensions: Trump imposed 50% tariffs on India, upending ties with Modi and affecting $6.5 billion in goods. Over a dozen countries (e.g., France, Italy, Australia) paused package deliveries to the US after the de minimis tariff exemption (for shipments under $800) was ended, potentially adding 10% costs to imports and causing delays.

1

1

2

58

4 Aug 2025

MetricPrevious ValueCurrent ValueChange

Block Height4,730,9014,731,001 100 blocks

Accounts21,797,95621,798,298 342 accounts

Transactions280,107,300280,117,042 9,742 txns

Transaction TPS41.03338.133⬇️ Decreased

Gas Used Per Second4,592,1814,093,368⬇️ Decreased

Block Time2.608 s3.0 s⬆️ Increased

📉 Implications:

Slight slowdown in transaction throughput (TPS dropped from ~41 to ~38).

Lower gas usage and longer block time could indicate:

Reduced network activity or demand.

Congestion, validator throttling, or configuration changes.

The network still processes ~38 transactions per second, which is substantial. #0g #0g_galileo #0GLabs

@0G_labs

@Jaineon0G

@BattleofAgents

@EuclidProtocol

4 Aug 2025

Market (@WhalesMarket) is teasing a potential Token Generation Event (TGE) @0G_labs

“TGE is coming? 👀” implies a token launch or distribution might be near.

“All my OG friends are waiting for some OG news …” builds hype within the OG Labs community. #0glabs #0g_galileo #0g

1

4

5

97

17 Feb 2025

Value change, but don't change values.

(Inspired by Bhagavad-Gita 17.16)

For more such interesting topics, please visit 🌐 - gitadaily.com #Chaitanyacharan #BhagavadGita #Gita1716 #CoreValues #ChaitanyaCharan #GitaDaily #SpiritualWisdom #InnerStrength #ValueChange

3

61

8 Aug 2024

Happy publication day!

'An Era of Value Change: The Long 1970s in Europe' edited by Fiammetta Balestracci, Christina von Hodenberg, and Isabel Richter published in our series 'Studies of the German Historical Institute London' is out now:

global.oup.com/academic/prod…

#valuechange

2

3

508

1 Aug 2024

Angular is very similar I think. [(value)] is syntactic sugar for [value]="..." (valueChange)="..."

As far as code organization goes, it isn't a problem until multiple states need to update from a single event, and then it's easy to modify the syntax to something more explicit.

2

295

29 May 2024

Perhaps the Jews who protest Genocide HAVE EVOLVED & the Zionists ARE the original Jews? A Conundrum. If this piece of the Talmud is True, it looks like it's time 4 a #ValueCHANGE!

1

148

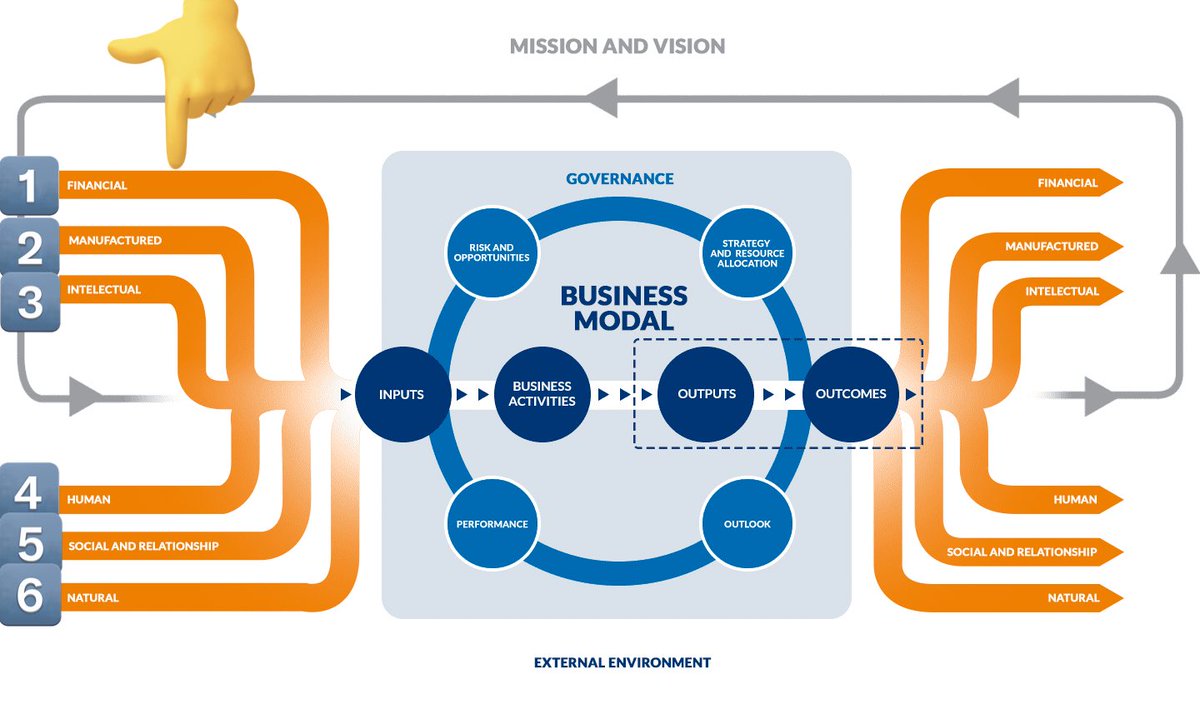

1️⃣ طبيعية(Natural)

2️⃣ بشرية ( Human)

3️⃣ مالية(Financial)

4️⃣ بنية تحتية(Infrastructure )

5️⃣ معرفية / فكرية(Intellectual)

6️⃣ العلاقات الاجتماعية (Social Relations)

#ValueStore #ValueChange #Value #Strategic

ALT Value chain - Value store

1

2

210

30 Jan 2023

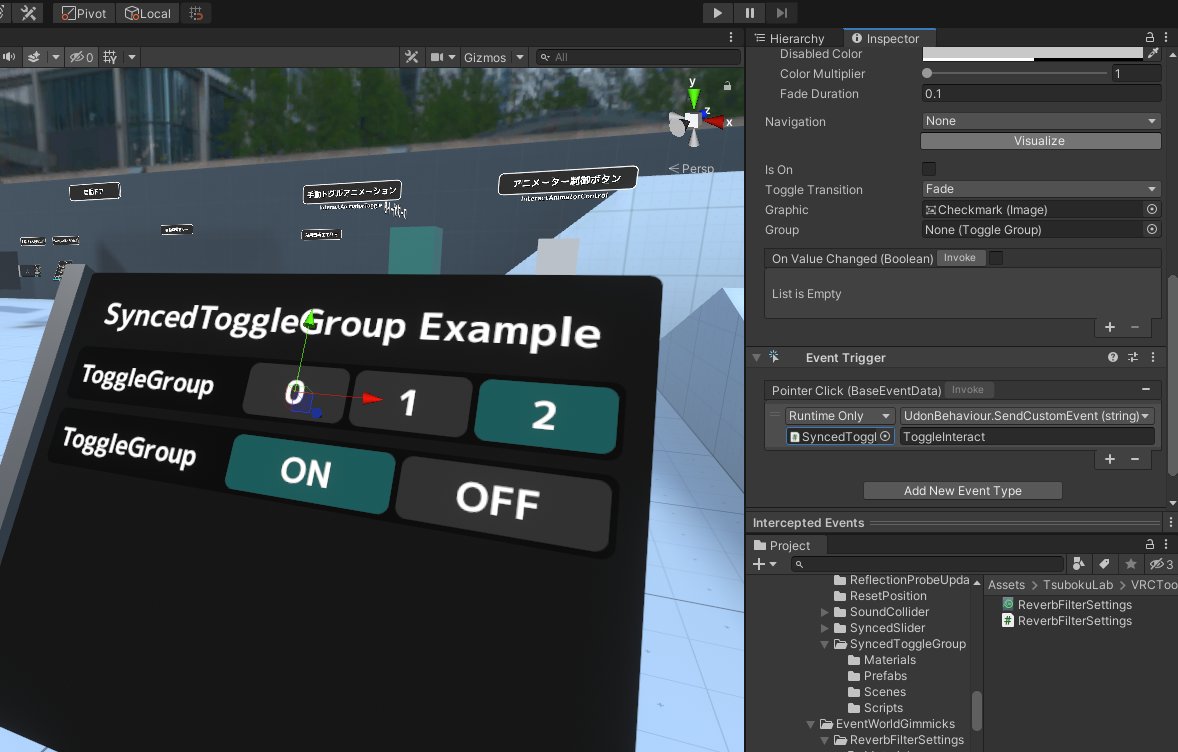

てか、SliderやToggleGroupの同期ってすごく厄介で操作した人がOnValueChangedでオーナーを取って変更しても見た目を同期した時に他の人上でもValueChangeが呼ばれちゃってまたオーナー遷移や値の上書きが行われたりする。

ボタン全部にUdonスクリプト付けたりSendNetworkEventを叩く方式しか無いと→

1

6

11

7,850

29 Nov 2022

In a new #OpenAccess article, @kiychettira & @nihitgoyal examine the relationship between #ValueChange & #PolicyInnovation, focused on the #EnergyTransition in #India. Their goal is to help policymaking achieve its sustainability goals.

Read more: link.springer.com/article/10…

3

6

7 Oct 2022

Great to reconnect with colleagues and meet new ones at @esdit_nl conference. Today, I've talked about how the most mundane tech can harbor #valuechange and used shock and epiphany as a heuristic to study value-in-the-making. For recent work, see Ch.2 in boekenbladkado.nl/the-techni…

1

1

8

21 Sep 2022

Our CTO @ochewlett explains today how

@goldstandard will explore how to unlock market-based allocation of impact in Scope 3 reporting. In discussion with @CDSBglobal @ghgprotocol @CDP

#ValueChange #ClimateWeekNYC

2

8

13 Jun 2022

Looking forward to first face-to-face meeting for a project on how #xphi can help better understand #ValueChange today. For next 12 months, we'll be investigating how #ethicists & #HCI #HTI researchers can work together to understand collective intuitions about #sustainability.

1

4

14

If you own a pair of comfortable, but #uglyshoes, you no longer need to hide them because now they have become one of the most popular – and profitable - trends in the shoe world right now. #UglyCore #valuechange

4

13

4 Feb 2022

Looking forward to begin this project with @Lilyfrank16 @minhappylee @forzazhang @VincentBlok1 @srkraaijeveld @SvenNyholm. Thanks to Elizabeth O'Neill for the pic. The tagline could be: "Let's wear VR now instead of respirators later." #ValueChange #VR tue.nl/en/news-and-events/ne…

3

9