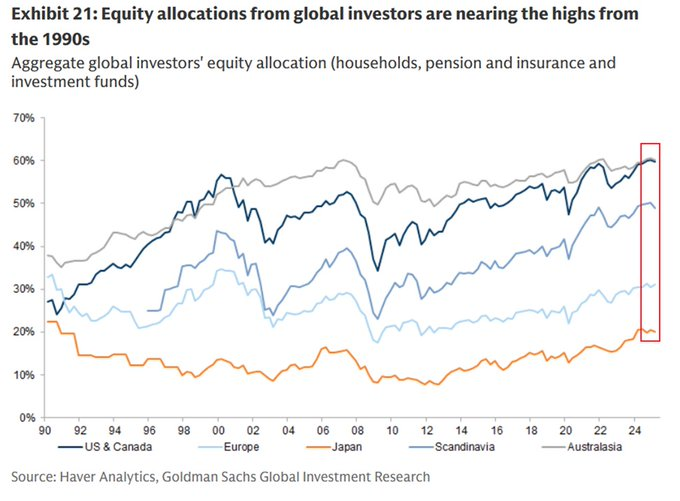

🚨 北美家庭“全仓”股票,危险信号?

📊 美国家庭、养老金和投资基金——股票配置占金融资产的比例已接近 60%,超越2000年、2007年和2021年熊市前的峰值。

🌍 横向对比:

• 斯堪的纳维亚:约 50%

• 欧洲其他地区:约 31%

• 日本:仅 20% ——不到北美的一半

⚠️ 没有哪个地区像北美这样把如此大比例的财富押在股票上。当60%的资产都在股市里,一次20%的回调就不只是伤害投资组合了——它会打击消费信心、抑制支出,甚至引发经济衰退。

#NorthAmerica #EquityAllocation #MarketRisk #WealthEffect #AssetAllocation

1

21

5,070

Jun 13

I feel like a #trillionaire; waiters in Europe don’t get many tips, but #Elon has me feeling good about the future of humanity

#wealtheffect #YoPorElon

6

Jun 9

💰 LE CONSOMMATEUR AMÉRICAIN N’EST PAS FAUCHÉ : Il est devenu aristocratique open.substack.com/pub/blogal…

NOUVELLE NOTE SUBSTACK PREMIUM

💰 Le consommateur américain n'est pas fauché.

Il est devenu aristocratique.

Pendant que les médias parlent d'inflation, de dettes et de ralentissement économique...

6 000 milliards de dollars de richesse supplémentaire ont été créés depuis le début de l'année.

Près d'un Américain sur 11 est désormais millionnaire.

Les 1 % les plus riches possèdent davantage que l'ensemble de la classe moyenne.

Et les ventes de luxe explosent :

⚡ Rolex

⚡ Hermès

⚡ Coach

⚡ Bulgari

⚡ Croisières

⚡ Voyages premium

Le vrai changement est ailleurs.

Nous ne vivons plus dans une économie du revenu.

Nous vivons dans une économie du patrimoine.

La question n'est plus :

« Combien gagnez-vous ? »

La question est devenue :

« Que possédez-vous ? »

Actions.

Immobilier.

Private equity.

IA.

Le capital travaille désormais plus vite que le travail.

🔥 Derrière l'euphorie boursière se dessine une nouvelle Amérique :

Une Amérique patrimoniale.

Une Amérique salariale.

Et l'écart entre les deux se creuse chaque jour davantage.

💰⚡🏛️

« Le grand récit du XXIe siècle n'est peut-être pas la lutte entre le capital et le travail.

C'est la lutte entre ceux qui possèdent des actifs... et ceux qui n'en possèdent pas. »

#AI #WealthEffect #WallStreet #Capitalism #Millionaires #TS2F #Markets #BlogALupus

3

2

85

Letting StockMarket crash will've neg. WealthEffect n hurt dis. consumption & in turn investment/GDP growth.LettingINR crash is better: Will boost exports.Costlier imports'll economise their use. Reversing TigerGlobal ruling & cutting LTCG'll bring in FPIs & check LRS outflows

2

107

Apr 29

Visa reported yesterday.

Consumer spending: strong.

No signs of slowdown.

The consumer is resilient.

That is the headline.

───────────────

Here is what the headline misses.

The top 10% of US households

account for approximately 50%

of all consumer spending.

These households own equities.

They own real estate.

They receive bonuses.

When the S&P is at all-time highs —

they spend more.

Visa is not measuring

the health of the American consumer.

Visa is measuring

the wealth effect

of the top income decile.

───────────────

Now look at the other side

of the same economy.

Domino's Pizza — Q1 2026.

US same-store sales: 0.9%.

Consensus expected: 2.72%.

Stock: -8% on the day.

Full-year guidance: cut.

CEO Russell Weiner on the earnings call:

Consumer sentiment in March

reached "COVID-level lows."

Delivery sales: -0.3%.

Lower-income consumers

pulling back on discretionary spending.

A pizza delivery order

is a $15-20 decision.

When that gets cut —

the consumer is not resilient.

The consumer is rationing.

───────────────

Dollar General —

one of America's largest

discount retail chains,

with 20,000 stores serving

predominantly rural and low-income communities.

Core customer: households earning

$30,000 to $45,000 annually.

CEO Todd Vasos:

"The majority of our customers

state they feel worse off financially

than they were six months ago."

More customers are using credit cards

for basic household needs.

Not for discretionary purchases.

For groceries and essentials.

Dollar General's outlook for 2026:

subdued. Growth slowing.

Same-store sales guidance: cut.

───────────────

The Federal Reserve Bank of Boston

documented this split precisely.

Since 2022, real spending growth

has been driven almost entirely

by high-income consumers.

Low-income consumers:

substantially higher credit card debt

than in 2019 —

while their inflation-adjusted spending

has barely moved.

───────────────

Two earnings reports.

Two different Americas.

Visa: top 10% spending freely.

Markets at all-time highs.

Wealth effect intact.

Domino's: consumer at COVID-level lows.

Dollar General: customers buying

essentials on credit cards.

───────────────

This is not a new pattern.

In 2007:

Visa reported strong consumer spending

through Q3 and into Q4.

The numbers looked fine.

Meanwhile:

subprime was already cracking.

Lower-income households

were already under pressure.

The lag between

"Visa says consumer is strong"

and "consumer is broken"

is measured in quarters.

Not months.

───────────────

The leading indicators

are not in the Visa report.

They are in:

WARN notices at their highest since 2009.

Quits rate at multi-year lows.

Michigan Sentiment at its lowest

since records began in 1978.

ADP 12-month average

at 2008 recession levels.

These are the Domino's consumer.

The Dollar General consumer.

The consumer that Visa doesn't see.

───────────────

Strong Visa numbers

in a late-cycle environment

are not a green light.

They are a yellow light

with a very short amber phase.

The pattern is consistent

across every cycle:

Top-income spending strong.

Bottom-income spending cracking.

Aggregate numbers: fine.

Until the labor market

catches up with the leading indicators.

Then everything reprices

at the same time.

@TheBigCycleGame

Not financial advice. DYOR.

#Visa #Dominos #DollarGeneral

#ConsumerSpending #MacroAnalysis

#EndCycle #LCIF #Contrarian

#LaborMarket #BusinessCycle

#DotcomFractal #FinalPhase

#WealthEffect #Recession

19

429

Apr 3

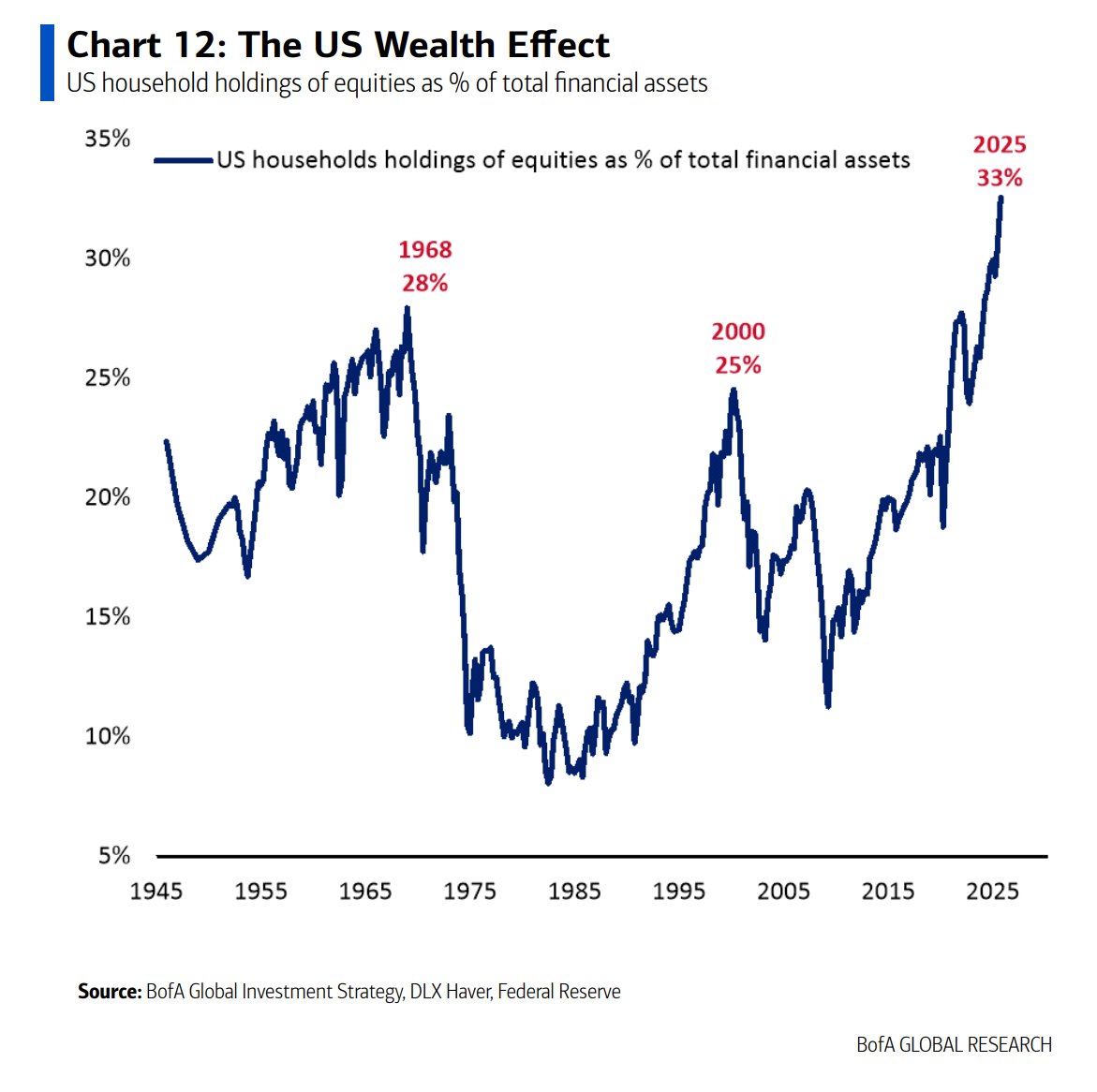

25.63%.

This is not just a percentage.

It’s evidence of power being redistributed.

U.S. households now hold a record 25.63% of their total net worth in stocks, surpassing the Dot-Com bubble peak.

But this time, the capital isn’t betting on .com domain names.

It’s pouring into compute, energy, and data. The real infrastructure of AI.

The old system is judging the new era with old metrics.

This is exactly why frameworks matter more than raw data.

Those who see it clearly are already positioned on the right side of acceleration.

Those still screaming “bubble” might still be living in 2000.

Infrastructure always wins.

What’s your framework for this?

#AI #Bitcoin #PowerStructures #MarketFramework #WealthEffect

2

1

32

455

Feb 24

ABD Borsası “Batamayacak Kadar Büyük” Hale mi Geldi? 📊

ABD’de hanehalkı finansal varlıklarının yaklaşık 3’ü artık hisse senetlerinde tutuluyor. Bu, tarihî bir zirve. 📈

Bu durum, ekonominin giderek daha fazla borsa performansına bağımlı hale geldiğini gösteriyor. Olası bir sert düşüş ise yalnızca Wall Street’i değil, tüketimi ve büyümeyi de doğrudan etkileyebilir.

Borsa artık sadece bir yatırım alanı değil, ekonomik istikrarın temel unsurlarından biri haline geliyor.

#Borsa #ABD #SP500 #Nasdaq #Ekonomi #Finans #Yatırım #WealthEffect #Piyasalar

2

234

Feb 12

Why $META Keeps Printing While Others Hesitate

Most traders lose on $META before the market opens, not because they’re wrong, but because they’re late.

That’s the real cost: opportunity cost.

When AI-driven earnings momentum shows up in stocks like $META, capital rotates instantly. Institutions don’t wait for confirmation, they position early.

Triggers (What Moves It)

• AI monetization ad efficiency

• Consistent earnings in a shaky macro

• Gold at ATHs = risk hedging, not tech rejection

• Weekend macro headlines → Monday gaps

Traditional brokers close on weekends. Narratives don’t.

When sentiment shifts before Monday, I prefer to be positioned, risk defined, not chasing a gap.

Public Action

Early positioning clean execution = edge.

That’s how I trade event-driven stocks like $META.

Access stock futures like $META here:

bitget.com/promotion/futures…

Be honest, are you positioning early, or reacting after the gap?

#META #Stocks #AITrades #Macro #WealthEffect #Bitget

1

3

60

Feb 10

“ไพบูลย์” มั่นใจรัฐบาลใหม่ทุบสถิติเสถียรภาพ ชี้เป้า SET 1,500 จุด หากดัน TISA สำเร็จ

.

นายไพบูลย์ นลินทรางกูร CEO บล.ทิสโก้ ประเมินทิศทางตลาดทุนไทยหลังทราบผลการเลือกตั้งปี 2569 โดยชี้ว่าชัยชนะถล่มทลายของพรรคแกนนำจัดตั้งรัฐบาลคือ "จุดเปลี่ยน" สำคัญที่ทำให้นักลงทุนกลับมาเชื่อมั่นในเสถียรภาพทางการเมืองรอบ 20 ปี

.

ส่งผลให้ดัชนี SET กลับมายืนเหนือ 1,400 จุดได้ทันที และมีโอกาสแตะ 1,500 จุด หากรัฐบาลใหม่ภายใต้การนำของนายอนุทิน ชาญวีรกูล เร่งแก้ปัญหาโครงสร้างเศรษฐกิจและผลักดันนโยบายตลาดทุนอย่างเป็นรูปธรรม

.

ข้อเสนอสำคัญที่ตลาดจับตามองคือการเดินหน้า "โครงการ TISA" เพื่อดึงเม็ดเงินออมเข้าสู่ตลาดหุ้นไทยแบบถาวร ซึ่งนายไพบูลย์เน้นย้ำถึง 5 เงื่อนไขสำคัญที่จะช่วยสร้าง "Wealth Effect" หรือผลกระทบจากความมั่งคั่ง

.

โดยหากมูลค่าตลาดหุ้นไทยเพิ่มขึ้นเพียง 10% จะสามารถปลุกเม็ดเงินหมุนเวียนในระบบได้ถึง 60,000 ล้านบาท และดัน GDP ให้โตเพิ่มได้ถึง 1% โดยไม่ต้องใช้งบประมาณรัฐ ท่านที่สนใจสามารถอ่านรายละเอียดเงื่อนไข TISA ทั้ง 5 ข้อ และบทวิเคราะห์เจาะลึกอุตสาหกรรมเป้าหมายที่จะได้รับอานิสงส์จากนโยบายเศรษฐกิจชุดใหม่

.

#หุ้นไทย

#เลือกตั้ง2569

#TISA

#SETIndex

#เศรษฐกิจไทย

#WealthEffect

#ลงทุนหุ้น

#ข่าวเศรษฐกิจ

#โพสต์ทูเดย์

1

1

418

Feb 8

🚨 India's Golden Legacy: Households Hoard More Than Top Central Banks Combined

India's affinity for gold runs deep, woven into culture, traditions, and economic strategy. The viral infographic spotlights how Indian households hold an staggering 34,600 tonnes of gold—surpassing the combined reserves of the world's top 10 central banks, which total around 24,413 tonnes based on latest data.

But is this accurate? Let's dive into the numbers. 🪙

First, verifying central bank holdings as of late 2025: The U.S. leads with 8,133 tonnes, followed by Germany (3,350t), Italy (2,452t), France (2,437t), Russia (2,330t), China (2,304t), Switzerland (1,040t), Japan (846t), India itself (880t), and Turkey (641t).

Summing these: approximately 24,413 tonnes—yes, Indian private holdings eclipse this by over 10,000 tonnes.

On the household side, recent estimates from Morgan Stanley peg Indian families' gold at 34,600 tonnes, up from older figures around 25,000t due to sustained demand and price appreciation.

This represents about 11% of global above-ground gold stocks, primarily in jewelry form for weddings, festivals like Diwali, and as intergenerational wealth.

Per capita, with India's 1.4 billion population, that's roughly 24.7 grams per person—modest individually but colossal collectively.

Economically, this hoard is a powerhouse. At today's gold spot price of ~$4,969 per troy ounce, those 34,600 tonnes equate to over $5.5 trillion in value—exceeding India's nominal GDP of around $4.2 trillion and rivaling the market cap of all NSE-listed companies.

It's a natural hedge: gold has surged 73% year-over-year, delivering a "wealth effect" that boosts consumer spending and buffers against inflation or rupee volatility.

Why so much? Beyond culture, gold's tax advantages (no capital gains on inherited jewelry), distrust of banks in rural areas, and its role as "stridhan" (women's property) drive accumulation. India imports ~800-1,000 tonnes annually, making it the second-largest consumer after China.

Meanwhile, the RBI has ramped up its own reserves by ~75 tonnes since 2024, now at 880t or 14% of forex reserves, signaling strategic diversification amid global uncertainties.

This decentralized "people's reserve" underscores India's unique economic resilience—where family vaults outshine Fort Knox. In a volatile world, it's a glittering testament to timeless wisdom.

Behold the shine: India's households aren't just saving gold; they're safeguarding a nation's enduring prosperity. 💰

#GoldReserves #IndiaEconomy #WealthEffect #PreciousMetals

2

314

Jan 21

Nifty Realty back to Square 1 !

Down 46% from its highs

Massive correction

Earlier, share market profits flowed straight into real estate 🏠💰

Now, with markets sliding to new lows almost every day, that surplus cash has dried up.

No easy market money = less fresh capital chasing realty.

#NiftyRealty #RealEstate #StockMarket #MarketCorrection #WealthEffect #IndianMarkets #EquityToRealty #DalalStreet

2

169

Jan 17

Gold-driven wealth boost for Indian households ✨

Indian households saw a massive ₹117 lakh crore ($1.3 trillion) wealth surge in CY2025, driven by rising gold prices.

This creates a strong spending buffer, with retail loans against gold already rising sharply, says HDFC Mutual Fund Yearbook 2026.

Gold once again emerges as both wealth creator & liquidity enabler.

#Gold #IndianHouseholds #WealthEffect #Consumption #Macro #India2025

1

3

268

Jan 14

India’s estimated gold holdings (~35,000 tonnes) is worth ~$5.2 Trillion at current prices

roughly equal to the entire Indian stock market cap (~$5.3Trillion)!

#WealthEffect

29

39

691

61,327

A friend has ₹1.1 Cr allocated in ONE stock , that’s currently the global market’s darling.

The idea of a 10-bagger alone can hijack your emotions.

Excitement. Fear. Hope. Bias , all at once.

My only advice to him ?

Practice EQUANIMITY 🎯

Because the real risk isn’t volatility , it’s losing objectivity.

“The market doesn’t reward emotions, it rewards discipline.”

P.S: He Comes from a Middle class background.

#AI #Journaling #AE #WealthEffect

1

9

1,128

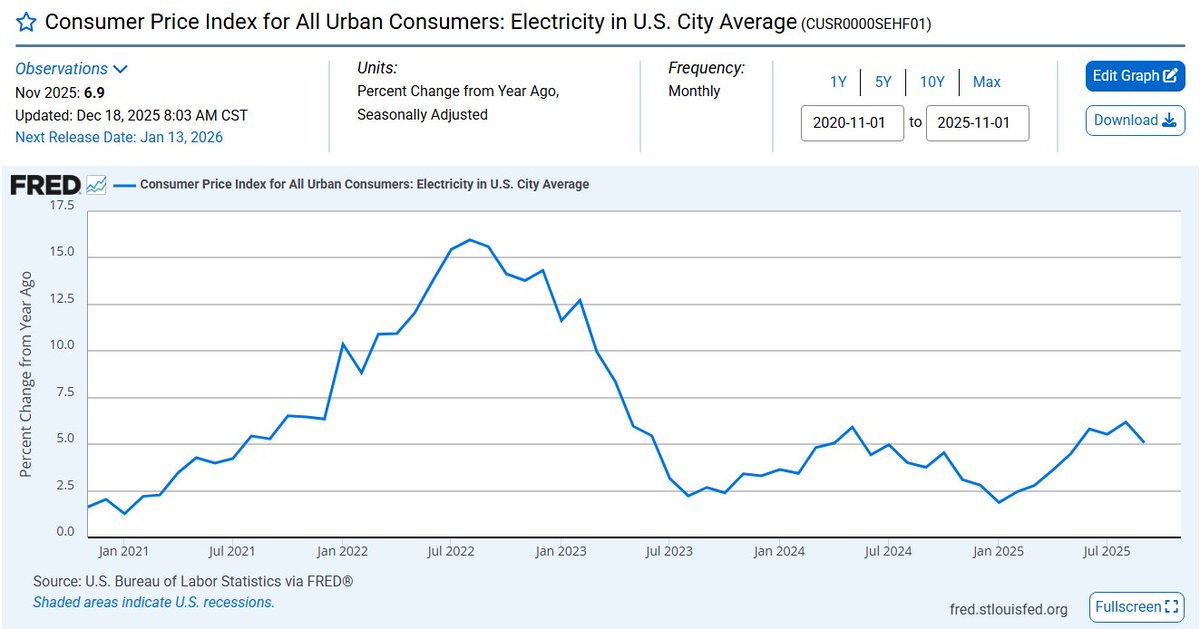

25 Dec 2025

Electricity CPI 6.9% YoY (Nov). One of three headwinds consumers face in 2026.

The other two? Subscribe to my Daily Insight blog post on X. Yes, I am a bit Scroogy on this Christmas Day...

#Markets #Economy #ConsumerSpending #Macro #2026Outlook #WealthEffect #Inflation

4

13

3,865

18 Dec 2025

2️⃣ The Wealth Effect: Markets Don’t Reflect Growth - They Create It!!

👉One of the most underappreciated forces in India’s future growth is the Wealth Effect.

👉When asset values rise, people don’t just feel richer - they spend more, even if income hasn’t changed. This extra spending feeds directly into GDP growth.

👉In India, this effect is likely stronger than in developed markets due to high marginal propensity to consume.

🔹Rising market cap boosts discretionary spending

🔹Consumption lifts corporate revenues and profits

🔹Higher profits feed back into equity valuations

🔹The loop repeats - faster, stronger each cycle

👉Even a modest wealth effect can add 0.4-0.5% to annual GDP growth, before accounting for multiplier effects.

👉This is why equity markets matter more than sentiment suggests. They are not passive mirrors - they are active accelerators of economic expansion.

👉As more Indians participate via demat accounts, SIPs, and pensions, this loop becomes deeper and more stable.

👉In simple terms: Rising markets → higher spending → higher profits → stronger markets

👉That’s the engine behind India’s MTD thesis.

#WealthEffect #Financialization #EquityCulture #IndiaConsumption #Macro @SandhyaKuntnur @AlphaWithRaunak @BaluGorade @RCee_RC

1

2

66

21 Nov 2025

#MCPro | Know the impact of ‘The Wealth Effect’, while spending. Larissa Fernand’s column highlights how to spend wisely @LarissaFernand ⬇🔗

moneycontrol.com/news/busine…

#PersonalFinance #Wealth #Spending #WealthEffect

2

7

2,343

13 Nov 2025

The economy isn’t slowing… it’s splitting.

Luxury stores packed, credit cards maxed, and two Americas heading in opposite directions.

My new video breaks down the real K-shaped recovery everyone is missing.

Watch here:

youtu.be/SzZsoNs1ec4

#economy #wealtheffect #kshape #WallStreet

1

3

62

13 Nov 2025

Advisors, the old saying “The stock market is NOT the economy” is losing its punch. New research from Oxford Economics and JPMorgan shows the Wealth Effect is now SUPERCHARGED:

- Every $1 gain in stock wealth now triggers 5¢ in new consumer spending

(up from <2¢ in 2010)

- Every $1 gain in home equity adds another 4¢ from 3¢)

That’s real GDP juice—70% of the economy is consumer spending, remember.

Translation:

When client portfolios hit new highs, Main Street feels it faster than ever.

When markets correct, the slowdown hits Main Street harder too.

The punchline?

The Fed and Congress now have an even bigger incentive to keep risk assets elevated. Call it the unspoken “Wall Street Put.”

Bottom line for your clients:

Staying invested isn’t just about building wealth anymore—it’s literally propping up the spending power of the entire country.

#WealthEffect #RetirementPlanning #MarketInsights #TuckerAdvisors

ALT Powerful lightning illuminates a dark ocean scene under dramatic storm clouds.

5

34

8 Nov 2025

Met a friend who now works in a semiconductor company.

He began his career in 2005 earning ₹6,500/month , a typical middle-class story back then.

Fast forward to today , his CTC just touched ₹1 crore per annum 💥

What a journey. Couldn’t be happier for him 🙌

The consumption boom in India 🇮🇳 is getting real , this entire cohort is on the rise, thanks to Startups & GCCs fueling prosperity.

Now the big question : What will they buy next?

What can you do : Buy the companies shares, they’ll buy the product from! 😄📈

I am BULLISH on #CONSUMPTION ✅

#GCC #WealthEffect #MiddleClass #AE

1

14

3,566