God First. Intel is cool

Joined May 2026

- Tweets 211

- Following 47

- Followers 667

- Likes 220

59 Photos and videos

20h

It is still AI or nothing. Only money tells the truth.

A little bit of background, a Z‑score tells you how extreme the flow is compared to before.

In other words, > 2 = people keep buying

> 3 = people buy like there's no tomorrow, and vice versa

The US is still the biggest winner. We're gonna win so much you may even get tired of winning.

So, the emerging markets are just TSMC and Samsung and SK Hynix.

Funds are dumping financials consumer goods to make room for tech.

It’s productivity vs. rate‑sensitivity.

Sell banks and consumer names (rate peak soft consumption). Buy AI.

Clear rotation signal.

3

5

24

1,543

Jun 13

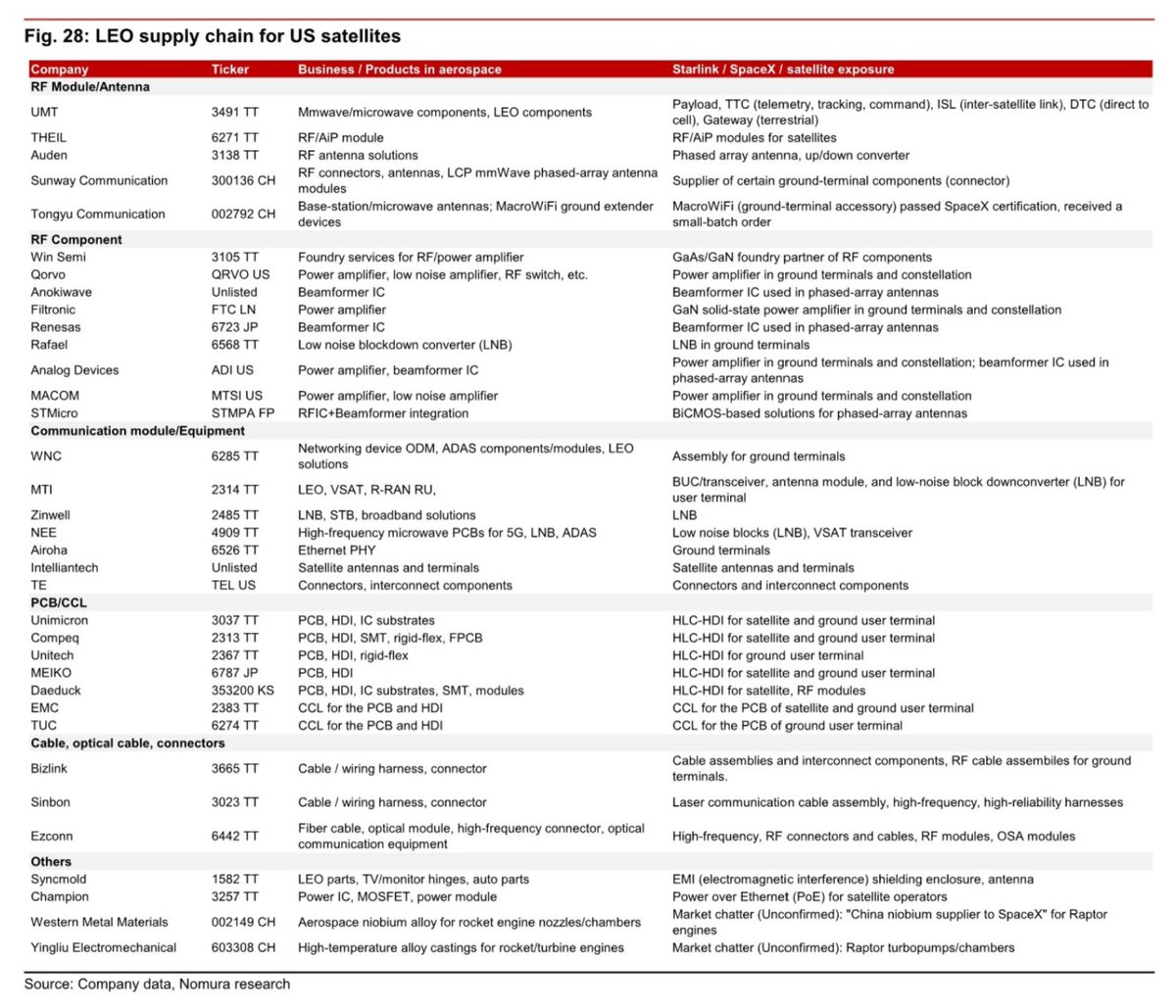

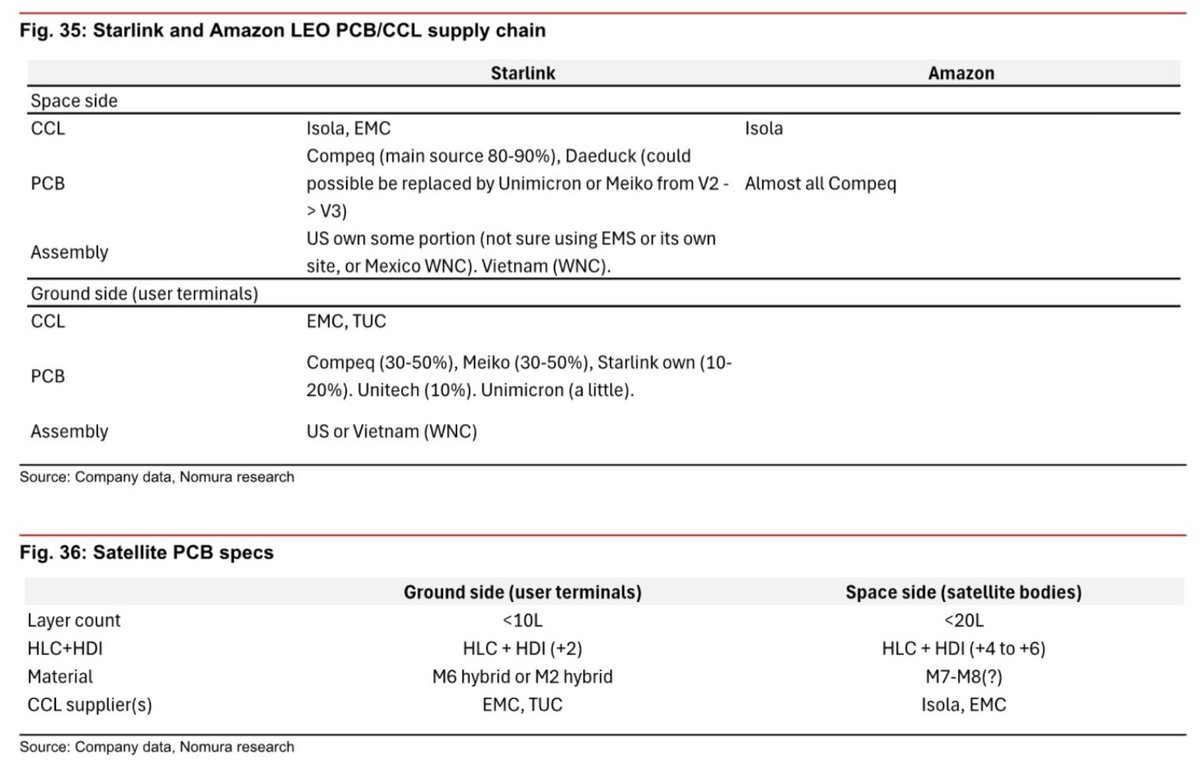

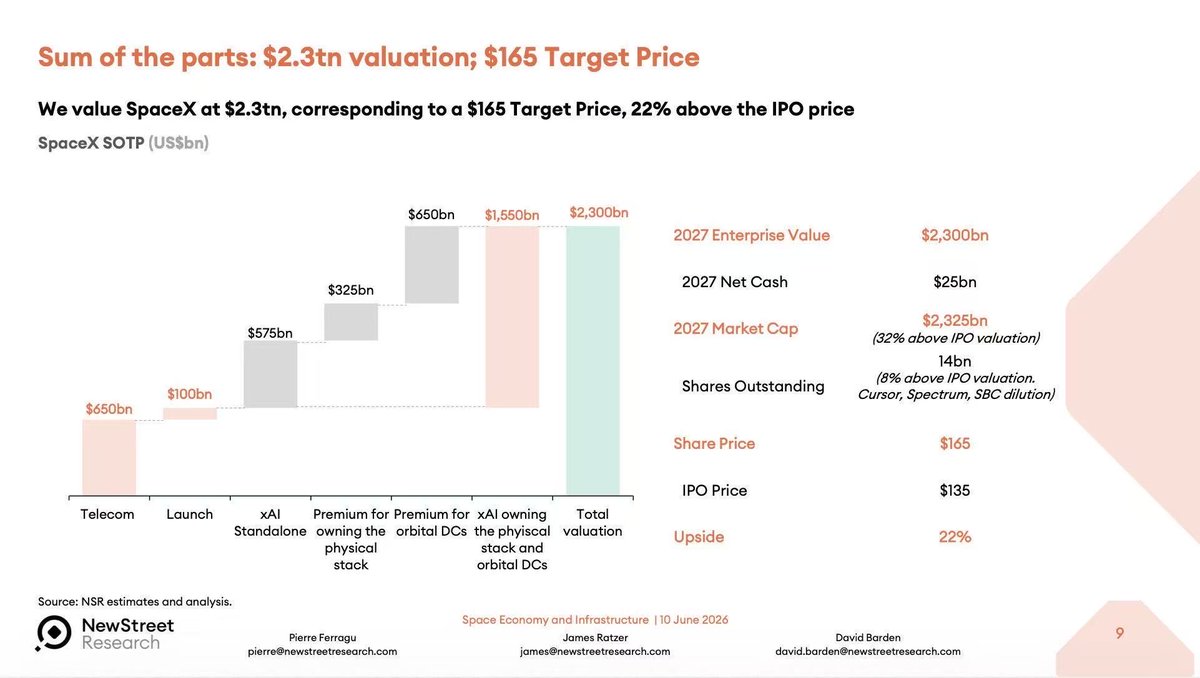

Hot take: SpaceX may be more valuable than most people realize.

Not a rocket scientist, but why people think $SPCX is overvalued?

To my best understandings after reading, AI isn't just consuming GPUs. It's absorbing high-end PCB, CCL, connectors, power components and manufacturing capacity across the electronics supply chain.

AI demand rises → electronics supply tightens → satellite production slows → launch demand gets pushed out.

SpaceX wins because it’s vertically integrated.

While much of the industry depends on fragmented suppliers, SpaceX controls large parts of its own stack.

AI infrastructure and space infrastructure are becoming more interconnected than most investors realize.

And Elon Musk controls both of them

BTW, if you are looking for high end PCB, you should take a look at Compeq.

But again, I think Starlink alone already make SpaceX much more valuable than just a 2 trillion market cap.

2

4

7

658

Jun 12

$SPCX can justify the valuation because they are the monopoly in the making

No company has them all

1. Reusable rockets launch

2. Starlink, I think just the Starlink alone can justify the valuation already

Basically Starlink is basically AWS in space

One battle after another, Starlink is proven to be very important!

3. Space logistics

1

4

2,834

Jun 12

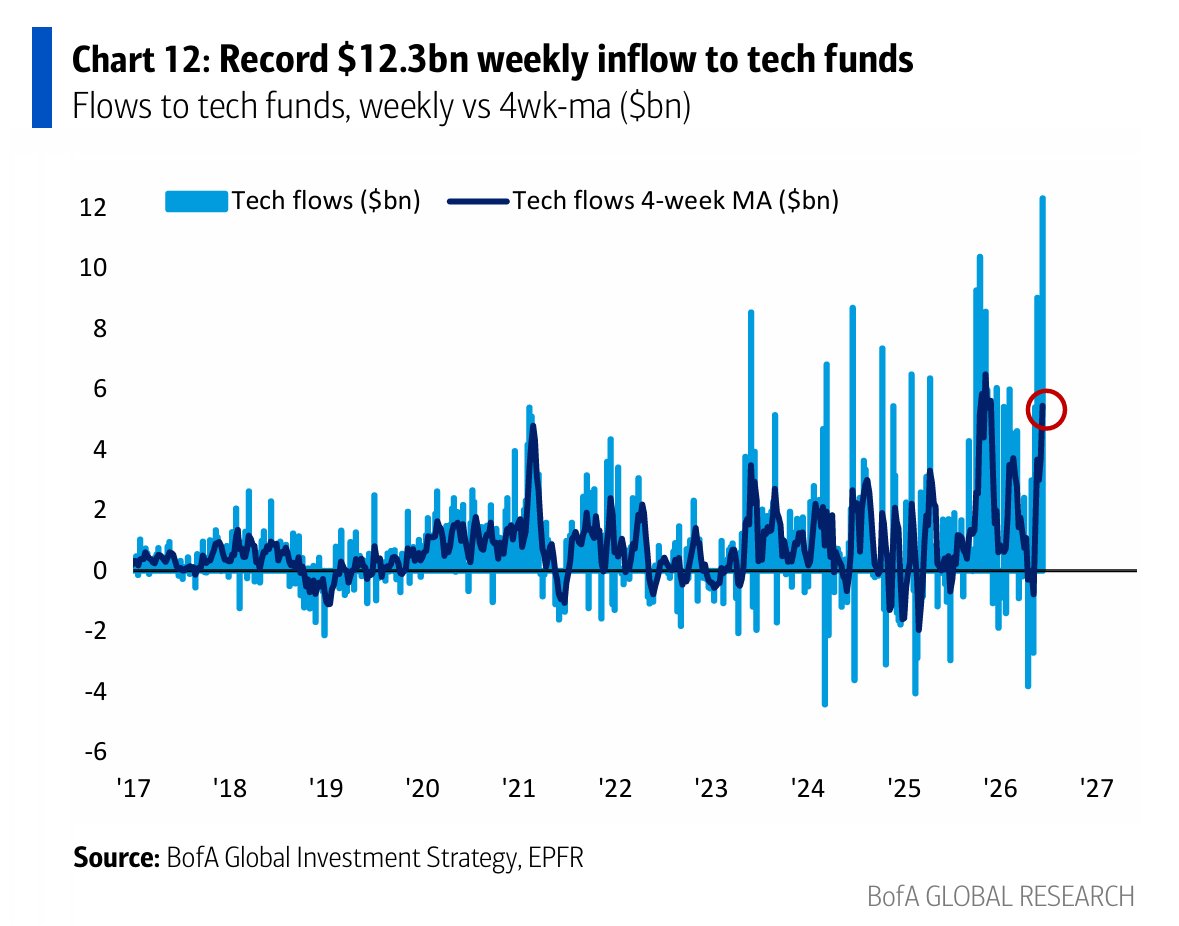

And we are so back at the first glance...

AI or nothing

$12.3b into tech funds, the BIGGEST weekly inflow ever, including $3.0bn into $SOXL and $2.9b into $SOXX.

However, that is a very late-cycle chase signal I think. A market still willing to chase winners, but increasingly vulnerable if bonds or inflation force tighter financial conditions.

2

2

513

Jun 12

Liquidity danger zone ahead

Late June

Quarter‑end balance‑sheet constraints repo demand UST settlement = short bursts of tight liquidity.

Not trend‑changing, but volatility spikes

July 10–31 (the big one)

TGA pushing toward $1T

Short‑term bill supply jumps

Corporate tax inflows fade

FOMC at month‑end

Big Tech earnings

If AI earnings are just very good instead of insanely good, profit‑taking risk is high

Early–mid August

Supply eases, but risks shift:

Lagged July tightening

Post‑earnings positioning

Summer liquidity drop

Crowded trades get deleveraged

163

Jun 12

We are very far from AI replacing us

Because enterprises can’t quantify AI productivity (only 2% can)

If enterprises don’t quantify AI productivity, markets can’t price it.

If markets can’t price it, capital stays stuck in infrastructure.

If capital stays stuck in infrastructure, the AI rally stays narrow.

Nothing changes until enterprises start measuring AI productivity instead of just talking about it

2

3

21

2,007

Jun 11

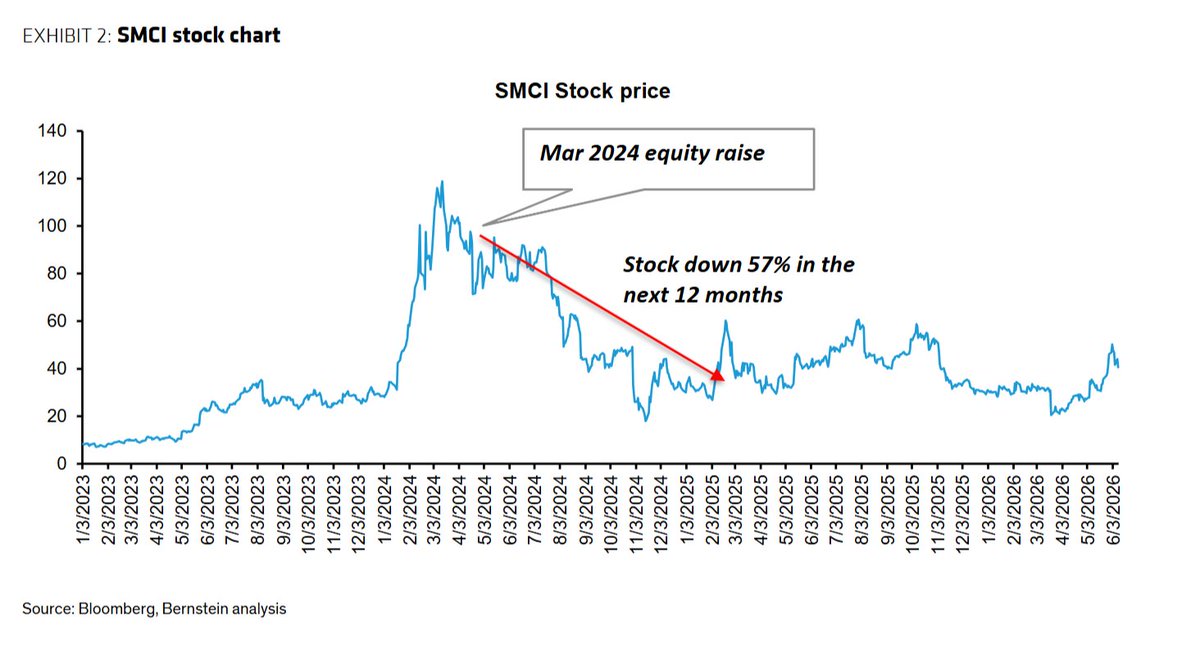

Interesting insights from Bernstein

A $7B equity raise from $SMCI, by far the largest ever, means shareholders are staring at 27% dilution.

And remember

The last time SMCI tapped equity markets, the stock sank 57% over the next 12 months… for just 3% dilution.

So why now?

Because SMCI’s balance sheet is flashing warning signs: Working capital is exploding

Net debt leverage has pushed past 3×

AI server orders require massive upfront cash

SMCI is bragging about $39B of AI server orders but are these even real orders?

These orders not firm commitments and are all subject to cancellation

BTW That’s not how Dell defines an order. $DELL requires a firm PO that can’t be cancelled.

It looks like survival liquidity ahead of even bigger cash demands.

> From me, not Bernstein

On the other hand, $INTC doesn't need to raise capital.

What it really needs is committed customers, which they already have, and stronger government incentives to accelerate the U.S. manufacturing roadmap.

The fabs are coming online either way.

The REAL question now is how fast America wants them.

5

9

2,852

Jun 11

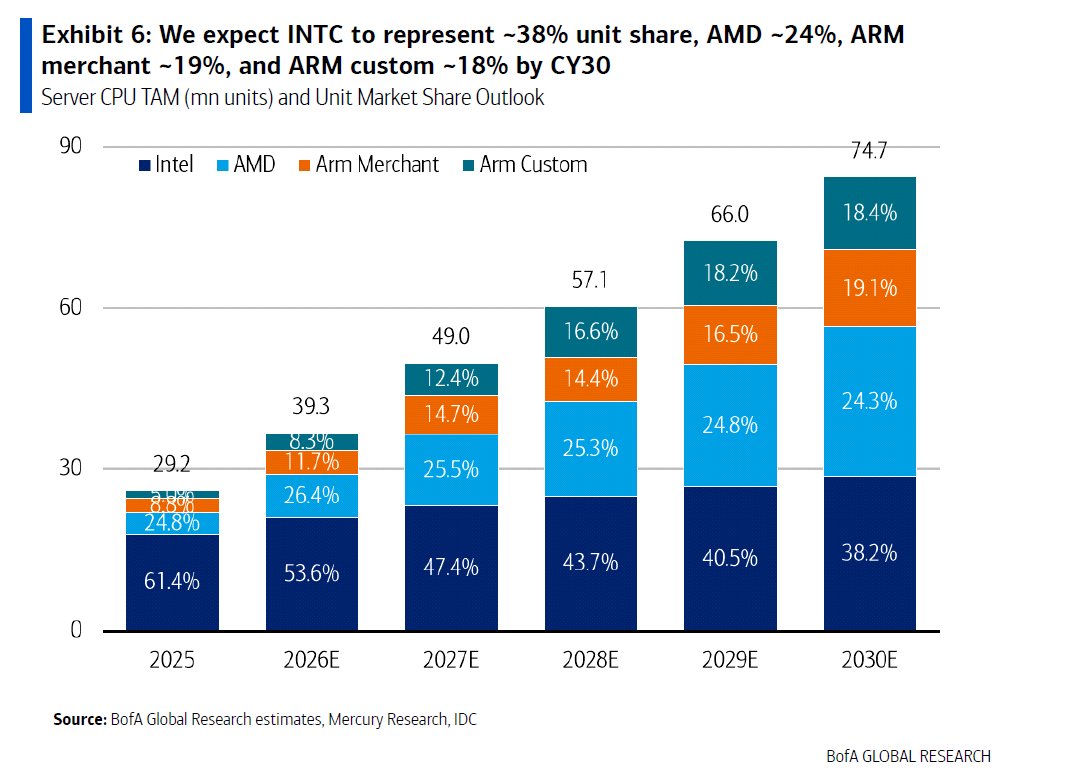

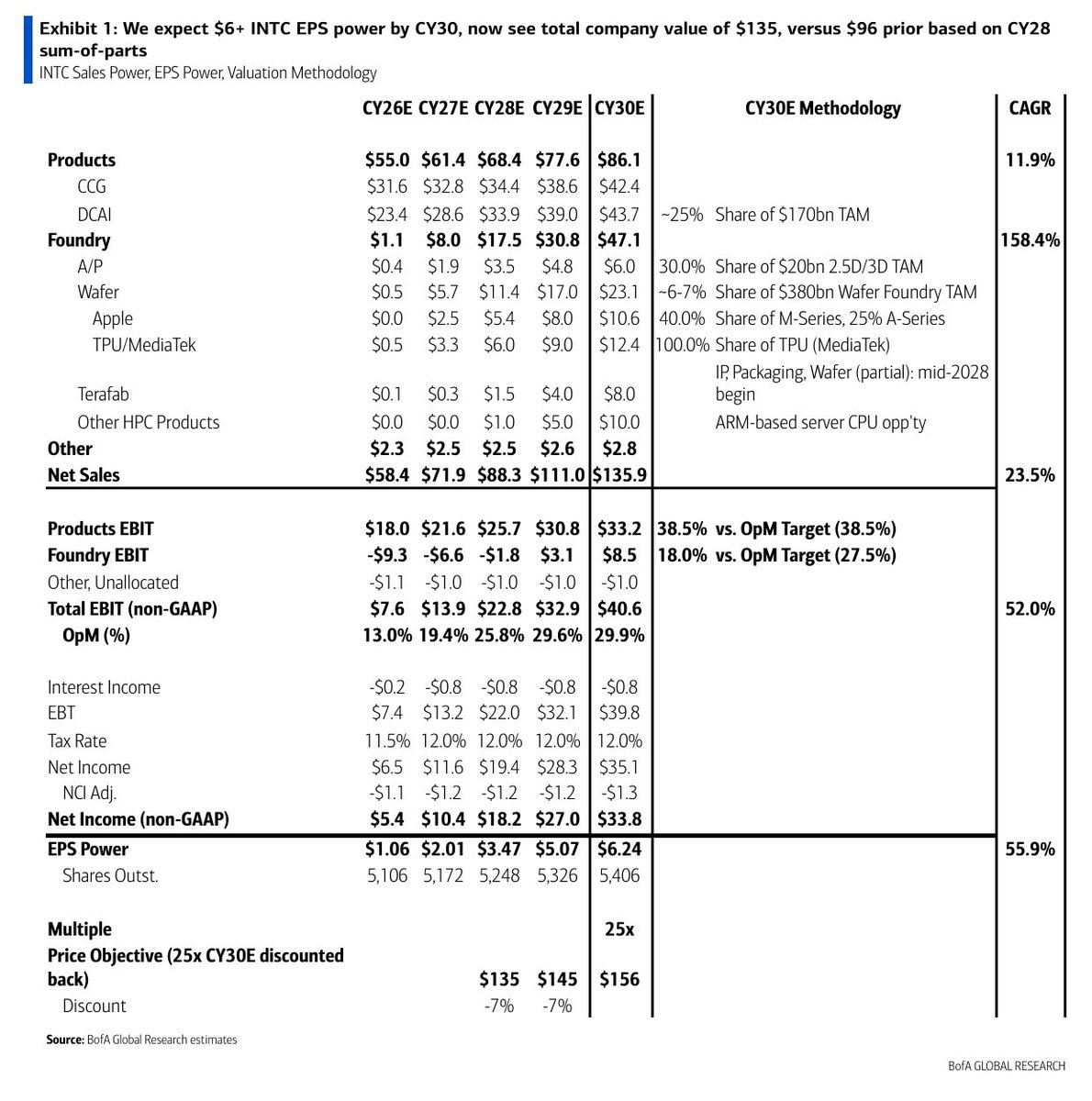

Before any bears come out

B of A is not assuming $INTC reclaims server CPU dominance. It expects Intel’s server CPU value share to so slightly decline to about 24% by CY2030 from about 41% in CY2025

Yet Intel CPU revenue still grows because the total server CPU TAM expands sharply.

So, the thesis again is not Intel wins share. It is the pie gets so much bigger that Intel can lose share and still grow materially.

Double upgrade is not about more CPUs

It is about Bank of America now values Intel as a fully integrated IDM by CY2030 with EPS power of about $6.24

7

15

88

10,387

Jun 11

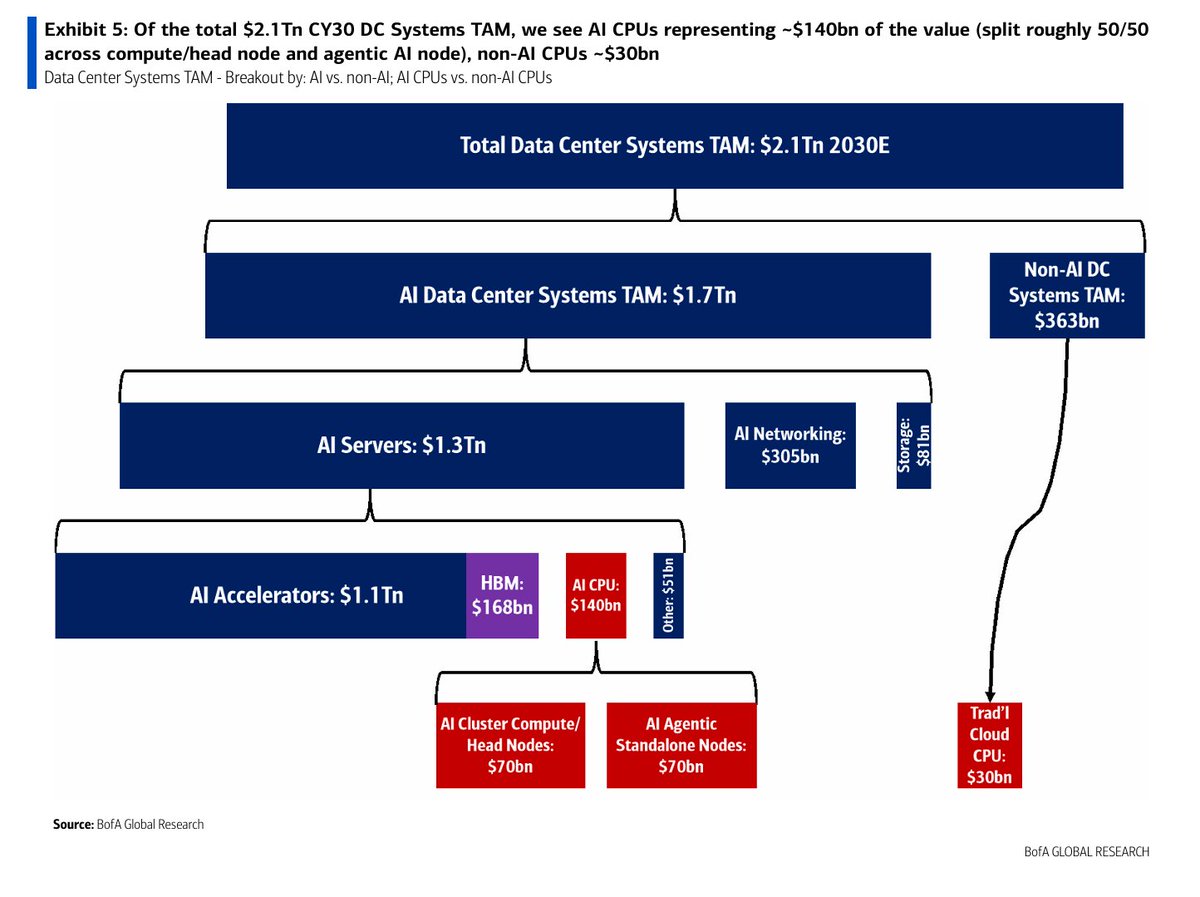

I think this is the most interesting chart from the B of A $INTC report

AI CPUs are almost as large as HBM by 2030. (This is huge, I will try to explain my view at the bottom of this post)

What almost everyone sees

AI accelerators = $1.1T

HBM = $168B

CPUs = $140B

What everyone may miss is

GPUs create a second CPU boom

Just look at the split:

AI Cluster / Head Node CPUs = $70B

AI Agentic Standalone Node CPUs = $70B

Every GPU cluster needs CPUs.

Agentic AI creates an entirely new CPU market the size of today's cloud CPU market multiple times over.

That's a huge bet.

This actually also has implications for $AMD

If BofA is right:

Intel wins of course

AMD wins

ARM server CPU vendors also win

Because the pie becomes much larger.

Roughly $170B by 2030.

For the part AI CPUs are almost as large as HBM by 2030, this is ultra huge

The market often treats HBM as the second largest AI winner after GPUs.

However, it may not be the case, CPUs could become nearly as economically important as HBM.

So If that happens, investors may have underestimated $INTC relative to memory.

Early AI cycle = GPU GPU GPU but we are not in the early cycle anymore

Next (or now) AI cycle = GPU HBM CPU Packaging Networking Power

2

13

59

4,721

Jun 11

Bank of America just DOUBLE upgrade Intel to buy!!!

Yes, DOUBLE UPGRADE $INTC

BofA is modeling Intel as a future AI infrastructure company where foundry packaging contribute nearly half of the growth story.

BofA is no longer valuing Intel as a turnaround. They're valuing it as a future AI infrastructure platform.

The foundry numbers are far larger than most people realize (very important)

Apple wafers = $10.6B

MediaTek TPU = $12.4B

Terafab = $8B

Other ARM server CPUs = $10B

Packaging may actually be more important than wafers

(that is ultra pro max important

The Cadence 14A mention is actually a bigger signal than many investors think

The CPU thesis is much more aggressive than people realize

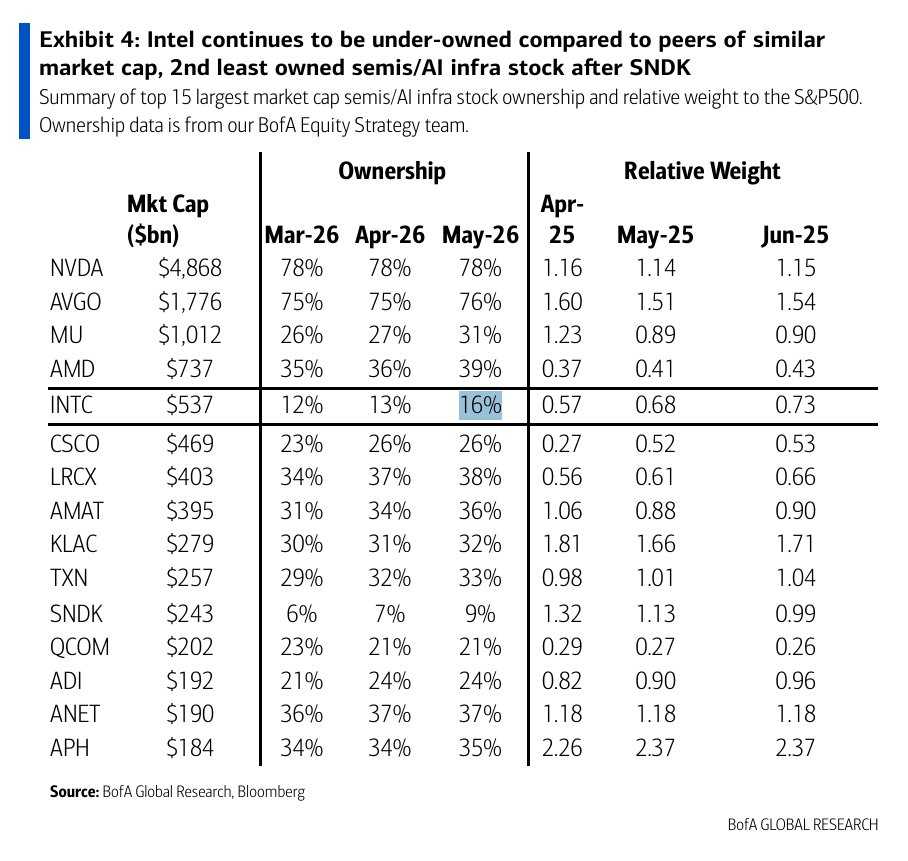

Ownership may be the most important near-term catalyst

BofA says Intel is only:

16% institutionally owned, despite being the fifth-largest semiconductor/AI infrastructure company by market cap.

7

9

80

14,838

Jun 11

What do you think? @imnotharsh @Mar364503 @WayWLeung @awakenowzone @Mojo_flyin @Alex_Intel_ and I am sorry for not remembering all the Intel OG

3

3

440

Jun 11

2027 was too optimistic.

2028 is where the real story may begin.

SoIC yield is still around 50–60%, and downstream assembly yield is only 20–50%.

So the near-term CPO trade may stay weak because the supply chain simply cannot ramp as fast as investors hoped.

One more thing

$INTC advanced packaging may get more customers

3

16

1,442

Jun 11

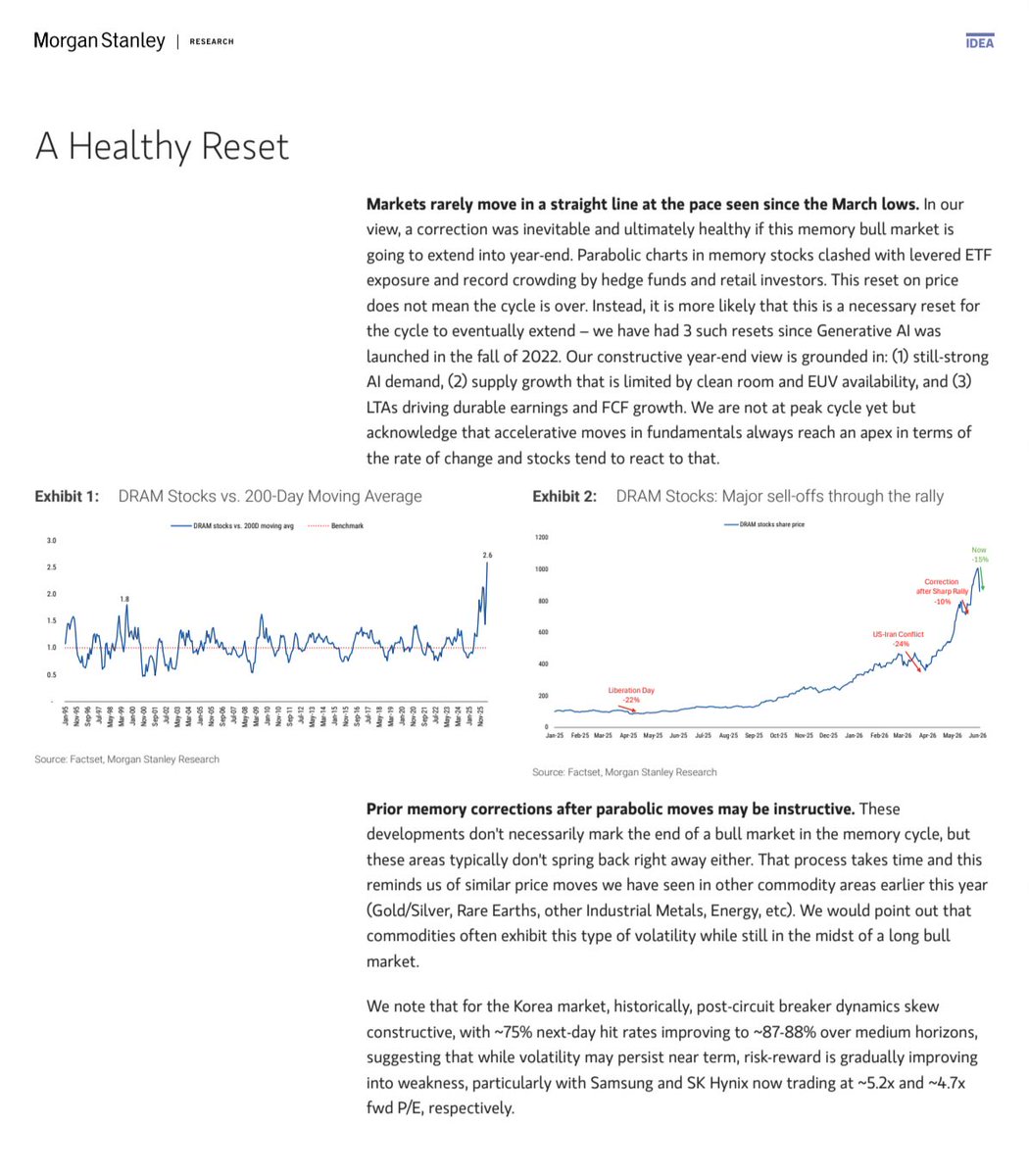

I tend to agree with this

This pullback on memory is a healthy reset, not the top.

AI DRAM demand is elastic

cheaper DRAM → more inference → more demand.

LTAs could re‑rate memory from 5× PE cyclical junk to 10× structural growth.

GPU demand is now memory‑capacity‑driven, not GPU‑count‑driven.

Agent‑based AI = $INTC CPU comeback → massive DRAM uplift.

Edge AI (128GB PCs) is a slow but heavy tail.

Inventories at record lows; HBM 2027 contracts 50–100%.

The ONLY real bear case

a future AI architecture that barely uses DRAM/HBM (which is basically impossible)

14

1,725

Jun 10

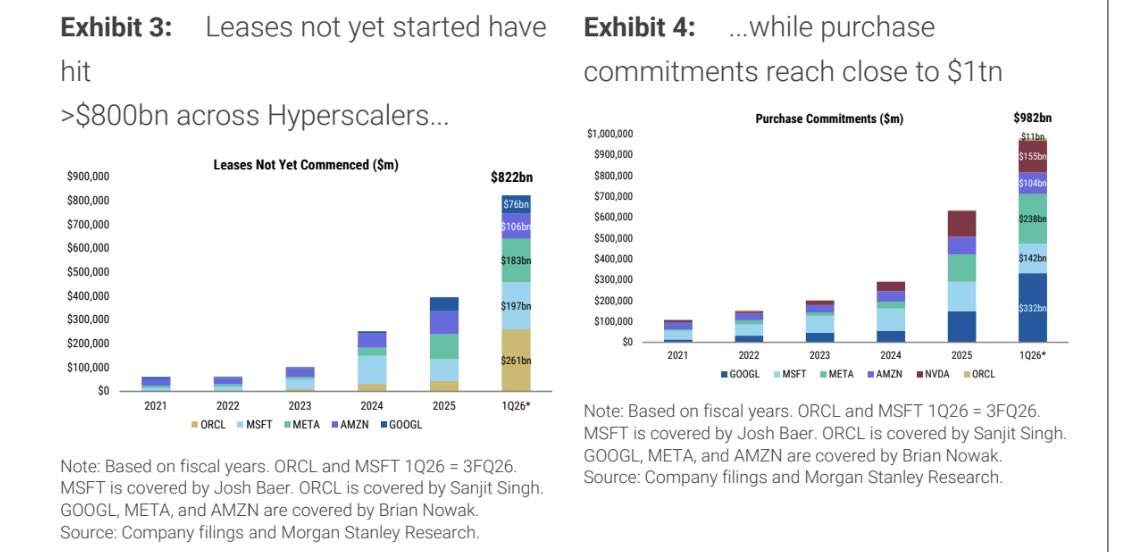

Very interesting and scary report from Morgan Stanley

The financial engineering behind hyperscaler capex

The truly unsettling part of the AI boom isn’t how much money is being spent

It’s how that money is being engineered through accounting

Hidden liabilities (> $1.8T)

Huge obligations sit off‑balance‑sheet: nearly $1T in purchase commitments, $800B in leases not yet started, $2T in RPO.

Future cash outflows that don’t show up as debt.

The coming depreciation hit

Profits look good only because spending is stuck in CIP.

Big Tech faces $520B in depreciation over 3 years.

ORCL’s depreciation ratio: 7% → 28%.

Supplier financing pressure

Unpaid capex is ~$110B.

ORCL’s DPO exploded from 35 → 170 days.

The whole supply chain is effectively financing the AI build‑out.

Lease accounting gray zones

Whether GPU contracts count as leases or services is subjective — and companies use that flexibility to shift billions on/off the balance sheet.

$ORCL = the most aggressive

Largest lease commitments, RPO up 300% , capex‑to‑sales hitting 189%.

Oracle is running the highest financial leverage in the ecosystem.

55

331

1,555

276,810

Jun 10

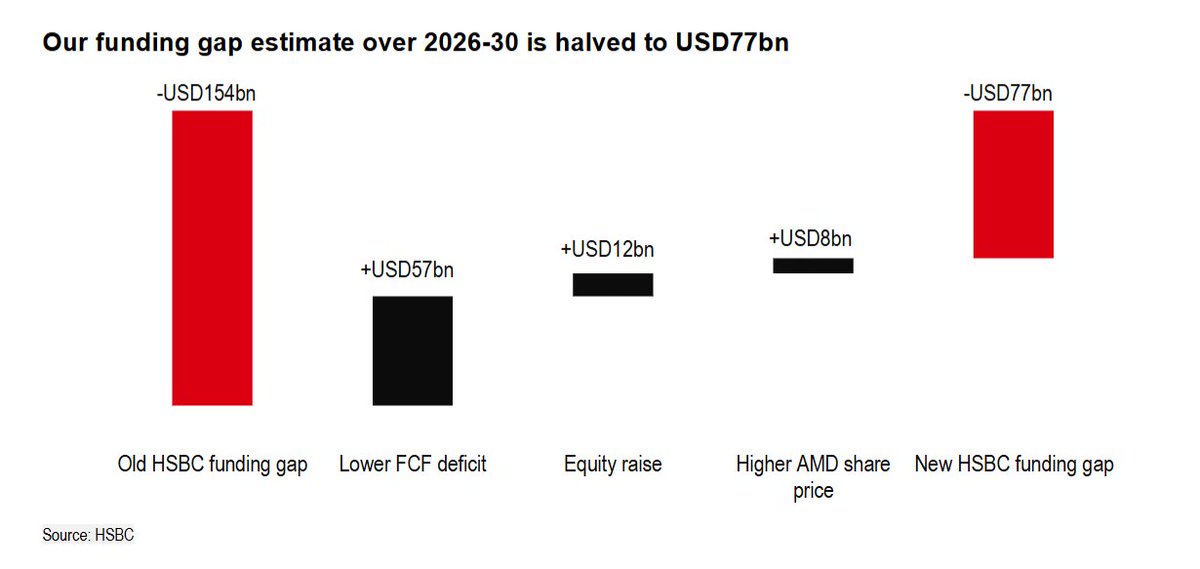

Good news for OpenAI IPO, when OpenAI IPOs, their numbers should look much better than people expected!!!

OpenAI’s revenue forecast came down, but its cash problem also became smaller and that is the interesting part.

Most people will focus on the bad news:

OpenAI’s 2026–2030 revenue forecast was trimmed from about $600B to $580B.

But HSBC also reduced its estimated funding gap from $154B to$77B.

Why does OpenAI need less money even with lower revenue?

Three reasons:

1. Lower cash outflow to $MSFT

The new Microsoft agreement reportedly caps OpenAI’s total revenue share to Microsoft at around$38B. That means OpenAI may keep more cash over time, even if some Azure resale revenue goes away.

2. $AMD stock became more valuable

OpenAI AMD deal includes warrants and options linked to AMD shares.

As AMD’s share price surged, the potential value of those shares also increased.

This improves the funding gap by around $8B.

3. More equity capital

The fundraising round increased from $110B to $122B, adding another $12B of capital.

OpenAI’s revenue forecast came down, but its cash problem also became smaller.

1

1

3

264

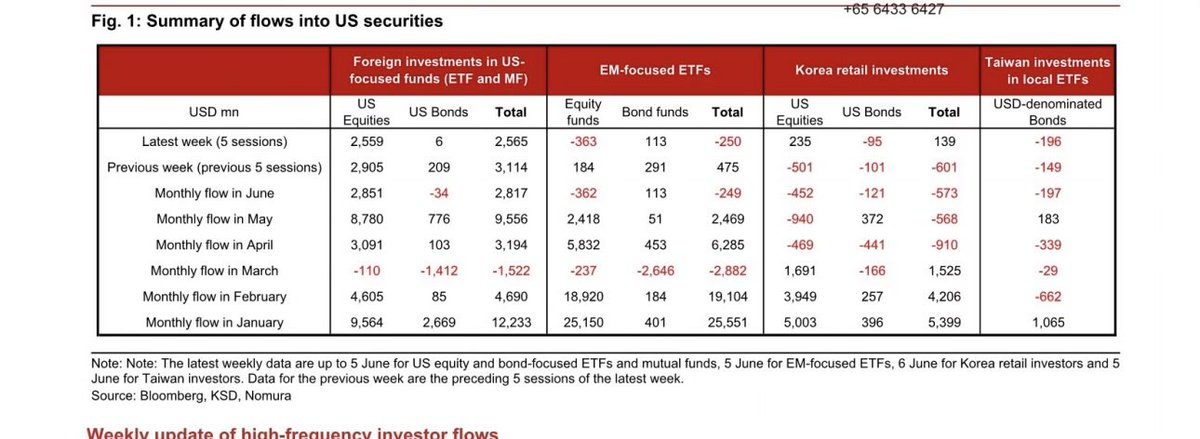

Jun 10

US stocks pulled in $2.56B last week.

US Treasuries? Basically zero.

AI optimism isn’t turning into broad buy America.

It’s tech or nothing.

And the only American company that is capable to make advanced chips is Intel

$INTC will be 1 trillion soon!!!

2

10

758

Jun 10

That could also explain why only chips related companies go up while everything went down

A.I. or nothing

1

2

177