LR embeds full-time offshore inv analysts with asset managers to take on all the grunt work so inv teams can focus on high-value work like inv strategy & ideas

Joined May 2023

- Tweets 112

- Following 48

- Followers 34

- Likes 3

52 Photos and videos

20 Nov 2025

𝗚𝗹𝗼𝗯𝗮𝗹 𝗘𝗰𝗼𝗻𝗼𝗺𝗶𝗰 𝗢𝘂𝘁𝗹𝗼𝗼𝗸 𝟮𝟬𝟮𝟲: 𝗔𝗜, 𝗧𝗿𝗮𝗱𝗲, 𝗮𝗻𝗱 𝗧𝗿𝘂𝘀𝘁 𝗨𝗻𝗱𝗲𝗿 𝗣𝗿𝗲𝘀𝘀𝘂𝗿𝗲

2026 will be a sorting year when structural pressures clarify their direction across the global economy.

Our latest analysis examines three converging forces:

𝗔𝗜 𝗚𝗿𝗼𝘄𝘁𝗵 𝗖𝗼𝗻𝗰𝗲𝗻𝘁𝗿𝗮𝘁𝗶𝗼𝗻 – Hyperscaler capex has surged to $518B, but gains remain narrow. The top 10% of US households now account for 49% of consumption, up from 41% post-GFC.

𝗖𝗵𝗼𝗸𝗲𝗽𝗼𝗶𝗻𝘁 𝗗𝗶𝗽𝗹𝗼𝗺𝗮𝗰𝘆 – Trade strategy has evolved beyond tariffs. The US Entity List grew from 1,500 to 20,000 firms, while China restricted 12 of 17 critical rare earths.

𝗜𝗻𝘀𝘁𝗶𝘁𝘂𝘁𝗶𝗼𝗻𝗮𝗹 𝗧𝗿𝘂𝘀𝘁 𝗨𝗻𝗱𝗲𝗿 𝗣𝗿𝗲𝘀𝘀𝘂𝗿𝗲 – US yields rose while the dollar weakened, a rare signal. Institutional credibility is no longer a backdrop; it's become a pricing factor.

How these systems respond in 2026 will shape what gets priced and trusted in the decade ahead.

𝗥𝗲𝗮𝗱 𝘁𝗵𝗲 𝗳𝘂𝗹𝗹 𝗼𝘂𝘁𝗹𝗼𝗼𝗸: leanrs.com/insights/global-e…

#EconomicOutlook #MacroAnalysis #InvestmentResearch #GlobalEconomy #LRInsights #LeanResearch

1

12

19 Nov 2025

𝗚𝗼𝗹𝗱 𝗶𝗺𝗽𝗼𝗿𝘁𝘀 𝗷𝘂𝗺𝗽𝗲𝗱 𝟭𝟬𝟬% 𝗮𝗻𝗱 𝗽𝘂𝘀𝗵𝗲𝗱 𝗜𝗻𝗱𝗶𝗮’𝘀 𝘁𝗿𝗮𝗱𝗲 𝗱𝗲𝗳𝗶𝗰𝗶𝘁 𝘁𝗼 𝗮 𝗿𝗲𝗰𝗼𝗿𝗱.

Gold, weak exports, and US tariffs explain more than the headline number.

India posted a USD 41.7bn goods trade gap in Oct-2025. It looks huge. But the drivers tell a far richer story.

Gold was the swing factor. Gold buys jumped more than 100% in size and 50% in price. Festive demand and a soft base from last year made the spike look even larger. Take gold out and import growth was only 1.7%.

So the jump does not mean hot demand at home.

Exports were the real weak link. 25 of 31 sectors fell. The slide is broad. And the US tariff hit is now clear. Shipments to the US fell 8.8% in Oct after an 11.9% drop in Sep. Without a trade deal, this drop will cut deeper and fast.

One bright spot kept the month from looking worse: services. India’s services surplus hit a record USD 19.4bn. Tech and global work orders held up well, and this helped soften the blow from goods.

The rupee felt the weight. Strong import bills and short-INR trades pushed USD/INR toward the 88.8–90.0 zone. The RBI stepped in again. But without a tariff deal by month-end, the line may not hold for long.

The “record” gap is not a demand shock. It’s gold and tariffs. The core goods gap is wide but stable. The risk sits with exports — and the trade talks will set the tone for the rupee.

#IndiaEconomy #TradeDeficit #FXMarkets #GlobalTrade #INR #EmergingMarkets #EconomicOutlook #Exports #Imports #InvestmentResearch #LRInsights #LeanResearch

29

14 Nov 2025

𝗕𝗶𝘁𝗰𝗼𝗶𝗻 𝗠𝗶𝗻𝗲𝗿𝘀 𝗖𝗼𝘂𝗹𝗱 𝗦𝗼𝗹𝘃𝗲 𝗔𝗜’𝘀 𝗣𝗼𝘄𝗲𝗿 𝗖𝗿𝗶𝘀𝗶𝘀

As AI demand skyrockets, Bitcoin miners have the power solution.

AI’s rapid growth is pushing the limits of compute power, and it’s creating a serious bottleneck in data center infrastructure. According to Morgan Stanley - By 2028, the US could face a 44 GW power shortfall for data centers, which will impact AI development.

But Bitcoin miners are sitting on a solution. They already control power-rich sites and can quickly repurpose them for AI workloads. Here’s how:

𝟭. 𝗧𝗵𝗲 “𝗡𝗲𝘄 𝗡𝗲𝗼𝗰𝗹𝗼𝘂𝗱” 𝗠𝗼𝗱𝗲𝗹: 𝗙𝗮𝘀𝘁 𝗮𝗻𝗱 𝗙𝗹𝗲𝘅𝗶𝗯𝗹𝗲

Miners like IREN are turning mining sites into full-service data centers with GPUs, which they lease to hyperscalers like Microsoft. The leases are short-term (5 years), generating high equity IRRs (~23-27%) but with execution risk.

• High Returns: Quick deployment, high equity IRR

• Flexibility: Ideal for fast-moving AI firms

• Risk: Shorter leases limit long-term stability

𝟮. 𝗧𝗵𝗲 “𝗥𝗘𝗜𝗧 𝗘𝗻𝗱𝗴𝗮𝗺𝗲” 𝗠𝗼𝗱𝗲𝗹: 𝗦𝘁𝗮𝗯𝗹𝗲 𝗟𝗼𝗻𝗴-𝗧𝗲𝗿𝗺 𝗩𝗮𝗹𝘂𝗲

Other miners, like APLD, are building “powered shells” and leasing them long-term (10-15 years) to hyperscalers or neoclouds. This model focuses on steady cash flow and is attractive to REITs and infrastructure investors.

• Steady Income: Long-term contracts with high-credit customers

• Stable Valuation: Appealing to infrastructure funds

• Lower Returns: But less risky with long-term contracts

𝗪𝗵𝘆 𝗧𝗵𝗶𝘀 𝗠𝗮𝘁𝘁𝗲𝗿𝘀 𝗳𝗼𝗿 𝗔𝗜

Miners with ready-to-deploy power are positioned to solve AI’s most pressing challenge — time to power. While traditional data centers face delays in securing grid access, miners are already set up. As AI’s compute needs 10x by 2026, those who can provide rapid power solutions will dominate.

Miners with power-rich assets will play a critical role in the future of AI. Time to power is the new bottleneck, and Bitcoin miners are ready to lead.

#AIInfrastructure #BitcoinMining #PowerSolutions #DataCenters #AICompute #EnergyForAI #TimeToPower #GridShortfall #AIRevolution #TechInnovation #PoweringAI #BitcoinToDataCenter #AIgrowth #EnergyCrisis #NextGenCompute #AIandEnergy #SustainableTech #LeanResearch #LRInsights

8

12 Nov 2025

𝗔𝗜’𝘀 𝗳𝘂𝘁𝘂𝗿𝗲 𝘄𝗼𝗻’𝘁 𝗯𝗲 𝗰𝗼𝗱𝗲𝗱 - 𝗶𝘁’𝗹𝗹 𝗯𝗲 𝗰𝗼𝗻𝘀𝘁𝗿𝘂𝗰𝘁𝗲𝗱. $𝟭.𝟮 𝘁𝗿𝗶𝗹𝗹𝗶𝗼𝗻 𝗶𝗻 𝗖𝗮𝗽𝗲𝘅 𝗽𝗿𝗼𝘃𝗲 𝗶𝘁.

In 1863, the Transcontinental Railroad was dismissed as fantasy.

By 1871, US railroad investments reached 6% of GDP - a national obsession that redefined trade, cities, and finance.

Fast forward to today:

AI and cloud infrastructure are the new railroads.

The Big Five (Microsoft, Google, Amazon, Meta, Oracle) now plan to spend a combined $404 billion in 2025 on AI and cloud infrastructure - a 78% YoY increase.

That number rises to $551 billion in 2026 and $643 billion in 2027.

In other words, over just two years, they’ll deploy more than $1.2 trillion - more CapEx than in the previous six years combined.

𝗖𝗮𝗽𝗘𝘅 𝘀𝗻𝗮𝗽𝘀𝗵𝗼𝘁 (𝗚𝗼𝗹𝗱𝗺𝗮𝗻 𝗦𝗮𝗰𝗵𝘀):

• Microsoft: $117.5B ( 55% YoY)

• Google: $92B ( 75% YoY)

• AWS: $91B ( 40% YoY)

• Meta: $71B ( 81% YoY)

• Oracle: $32B ( 200% YoY)

𝗧𝗵𝗲 𝗰𝗼𝗺𝗽𝗮𝗿𝗶𝘀𝗼𝗻 𝗶𝘀𝗻’𝘁 𝗷𝘂𝘀𝘁 𝗽𝗼𝗲𝘁𝗶𝗰:

The 19th-century railroads connected physical economies.

Today’s AI infrastructure connects digital intelligence.

Each data center expansion, GPU cluster, and power-hungry AI supernode is a modern equivalent of a new track being laid across continents.

And just as the railways created enduring winners (steel, coal, logistics), the current AI investment wave will crown its own champions - semiconductors, datacenter REITs, and energy infrastructure.

It’s premature to call it a bubble when the groundwork for the next 50 years of compute power is still being poured.

#AI #Infrastructure #DigitalEconomy #CapEx #ArtificialIntelligence #NVIDIA #GoldmanSachs #CloudComputing #Microsoft #Meta #Google #AWS #Oracle #IndustrialRevolution #Investing #LeanResearch #LRInsights

7

28 Oct 2025

𝗜𝗻𝗱𝗶𝗮’𝘀 𝗢𝗶𝗹 𝗧𝗶𝗴𝗵𝘁𝗿𝗼𝗽𝗲: 𝗦𝗮𝗻𝗰𝘁𝗶𝗼𝗻𝘀, 𝗧𝗮𝗿𝗶𝗳𝗳𝘀, 𝗮𝗻𝗱 𝘁𝗵𝗲 𝗥𝘂𝗽𝗲𝗲

New US sanctions on Rosneft & Lukoil - which supply ~60% of India’s Russian crude - put Delhi’s bargain barrels at risk. India gets ~35% of its crude from Russia; Reliance (the biggest buyer this year) is reportedly pivoting to the Middle East & US while the government and state refiners await formal guidance.

𝗪𝗵𝘆 𝗶𝘁 𝗺𝗮𝘁𝘁𝗲𝗿𝘀 (𝘁𝗵𝗲 𝗺𝗮𝘁𝗵):

• Discount at risk: Losing the $2–4/bbl Russian discount lifts India’s oil import bill (down 1% YoY in H1 FY26 after ~4% in FY25).

• Tariffs-for-oil trade-off: US-India talks reportedly explore cutting US tariffs on India to 15% if India tapers Russian oil and buys more US energy (US had imposed an extra 25% penalty on Russian oil above a 25% merchandise tariff).

• Macro sensitivity (RBI): A 10% crude rise → 30 bps CPI, –15 bps GDP (with pass-through). A 5% INR depreciation → 35 bps CPI, 25 bps GDP via export impulse.

• Policy backdrop: RBI cut FY26 CPI to 2.6% and raised GDP to 6.8%. Retail fuel prices frozen since Mar ’24, so consumers missed the down-cycle; refiners benefited.

• Trade & flows: Sep ’25 trade deficit hit a 13-month high (first full month of 50% US tariff impact). Exports to the US (India’s largest market) –12% YoY; imports surged on high gold.

• FX risk: USD tariffs, oil and foreign selling weigh on the INR. RBI intervened in early Oct to pull it off record lows, but pressure is back.

𝗪𝗵𝗮𝘁 𝘁𝗼 𝘄𝗮𝘁𝗰𝗵 𝗻𝗲𝘅𝘁:

• Supply remix speed: Middle East/US barrels replacing Russia without spiking landed costs.

• Deal or drift: A tariff-for-energy deal could offset CPI/CAD pain and steady INR.

• RBI reaction: With inflation below projections, space remains for a Q4’25 25 bps cut if FX stays orderly.

• Sector impacts: Refiners cushioned by sticky retail prices; import-heavy sectors need hedges. INR path = oil tariffs RBI’s FX line.

India can diversify fast; the question is price. Without a tariff reset and US energy offtake, the shift reads inflationary and INR-negative. With one, it’s manageable.

#IndiaEconomy #EnergySecurity #RussiaSanctions #USIndia #Tariffs #RBI #Inflation #INR #Macro #TradePolicy #Refining #Commodities #EmergingMarkets #LeanResearch #LRInsights

16

23 Oct 2025

𝗖𝗵𝗶𝗻𝗮’𝘀 𝗕𝘂𝘁𝘁𝗲𝗿𝗳𝗹𝘆 𝗘𝗳𝗳𝗲𝗰𝘁 - 𝗮𝗻𝗱 𝘁𝗵𝗲 𝗖𝗼𝗺𝗶𝗻𝗴 𝗖𝗼𝗺𝗺𝗼𝗱𝗶𝘁𝗶𝗲𝘀 𝗖𝗵𝗲𝘀𝘀 𝗚𝗮𝗺𝗲 ♟️🌏

In the 1990s, Deng Xiaoping said:

“𝗧𝗵𝗲 𝗠𝗶𝗱𝗱𝗹𝗲 𝗘𝗮𝘀𝘁 𝗵𝗮𝘀 𝗼𝗶𝗹, 𝗮𝗻𝗱 𝗖𝗵𝗶𝗻𝗮 𝗵𝗮𝘀 𝗿𝗮𝗿𝗲 𝗲𝗮𝗿𝘁𝗵 𝗺𝗲𝘁𝗮𝗹𝘀.”

Three decades later, that prophecy defines global geopolitics.

🔹 China controls 90% of global rare earth processing, giving it the power to move markets — and governments — with a single export restriction.

🔹 The rare earth market is small (~$6B) compared to copper’s $213B, but strategically far more potent — rare earths are essential for EVs, defense systems, and clean energy.

🔹 The U.S. needs $87B in investments to secure its domestic battery and mineral supply chain by 2030.

🔹 Goldman Sachs estimates $75 trillion will be needed by 2070 to fund the global green transition, driving demand for copper ( 25%), aluminum ( 30%), and critical metals like lithium, nickel, and cobalt.

But here’s the real risk: the world’s “green future” depends on a single point of failure - China’s processing plants.

This is how empires are built - not through land, but through control of bottlenecks.

𝗔𝗺𝗲𝗿𝗶𝗰𝗮 𝗶𝘀 𝗿𝗲𝘀𝗽𝗼𝗻𝗱𝗶𝗻𝗴:

• The Pentagon invested $400M in MP Materials, the only major U.S. rare earth magnet producer.

• The White House has identified 10 critical mineral projects for accelerated development under the national security mandate.

Yet the lesson is larger than metals. Whether it’s AIG in 2008, AWS cloud dependence, or Taiwanese chips, modern finance and technology systems remain dangerously centralized.

As Paul Tudor Jones reminds: “The first rule of trading is to play great defense, not great offense.”

And as Warren Buffett said: “Predicting rain doesn’t count; building arks does.”

True diversification means building arks before the storm - across assets, supply chains, and systems.

Because the next global shock may not start on Wall Street - but in a mine in Inner Mongolia.

#China #RareEarths #Commodities #Geopolitics #GreenTransition #Investing #MacroStrategy #CriticalMetals #SupplyChain #RiskManagement #Diversification #HardAssets #LeanResearch #LRInsights

2

17 Oct 2025

𝗕𝗶𝘁𝗰𝗼𝗶𝗻 𝗠𝗶𝗻𝗲𝗿𝘀 𝗗𝗼𝘂𝗯𝗹𝗲 𝗶𝗻 𝗩𝗮𝗹𝘂𝗲 𝗮𝘀 𝗛𝗣𝗖 𝗪𝗮𝘃𝗲 𝗥𝗲𝘄𝗿𝗶𝘁𝗲𝘀 𝘁𝗵𝗲 𝗣𝗹𝗮𝘆𝗯𝗼𝗼𝗸 ⚙️💰

The High-Performance Computing (HPC) boom is reshaping the crypto mining landscape.

In just six weeks, the 14 leading U.S.-listed bitcoin miners and data center operators have added $40 billion in market cap — reaching a record $79 billion, more than double their late-August valuation.

🔹 Mining Meets AI Infrastructure

Deals like Cipher x Fluidstack and Iris Energy’s (IREN) GPU fleet expansion have accelerated the shift from pure bitcoin mining to hybrid HPC infrastructure. This diversification is driving a record 3.5x valuation versus miners’ proportional share of the four-year block reward — well above the 1.65x average since 2022.

🔹 Bitcoin Price and Profitability

• Average BTC price in early October: $119,400 ( 6% m/m

• Up ~75% since the halving, ~68% y/y

• Network hashrate eased slightly to 1,030 EH/s, improving profitability

• Estimated gross margins up 250 bps to 55.6%

🔹 U.S. Miners Taking Share

• U.S.-listed miners’ capacity: 390 EH/s ( 101% y/y)

• Share of global network: ~38%, up 130 bps from last month

• Top performers : Bitfarms ( 129%), Hive 3.6 EH/s, Bitdeer 5 EH/s

🔹 Valuations Decouple from Reserves

The total proved block reward opportunity fell 5% to $120B - but valuations surged.

The market now prices miners as HPC operators, not just bitcoin extractors.

Crypto mining has entered a new cycle - one powered by compute demand, not block rewards.

As miners evolve into next-gen data centers, HPC may become the new alpha engine for the digital asset sector.

#Bitcoin #CryptoMarkets #DigitalAssets #HPC #BlockchainInfrastructure #CryptoMining #InstitutionalInvesting #AI #DataCenters #MarketTrends #AssetAllocation #MacroInsights #LeanResearch #LRInsights

19

15 Oct 2025

𝗨𝗦 𝗘𝗰𝗼𝗻𝗼𝗺𝘆 𝟮𝟬𝟮𝟱: 𝗚𝗿𝗼𝘄𝘁𝗵 𝘃𝘀. 𝗟𝗮𝗯𝗼𝗿 𝗠𝗮𝗿𝗸𝗲𝘁 𝗧𝗲𝗻𝘀𝗶𝗼𝗻 🇺🇸

The U.S. economy is powering ahead, yet labor market softness and tariff pressures could shape 2026.

𝗦𝘁𝗿𝗼𝗻𝗴 𝗚𝗿𝗼𝘄𝘁𝗵, 𝗕𝘂𝘁 𝗦𝗹𝗼𝘄𝗶𝗻𝗴 𝗝𝗼𝗯𝘀

• Q3 GDP: 3.5%, year-end projection: 1.2%.

• Job creation: only ~50K/month vs. 216K in 2023.

• Unemployment: up to 4.3%, forecast 4.5% by 2025-end, 4.9% in 2026.

• Risk: rising layoffs could squeeze real income and consumption.

𝗧𝗮𝗿𝗶𝗳𝗳 𝗜𝗺𝗽𝗮𝗰𝘁 𝗦𝘁𝗶𝗹𝗹 𝗙𝗹𝗼𝘄𝗶𝗻𝗴

• Effective tariff rate: 16%, ~$400B lost annually to the Treasury.

• 70% of firms delaying price increases (Richmond Fed).

• Key exposure: $58B in consumer goods from China could see up to 45% tariffs.

• Historical insights: tariffs on solar panels, washing machines, and other goods have consistently translated to higher consumer prices.

𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 & 𝗙𝗲𝗱 𝗥𝗲𝘀𝗽𝗼𝗻𝘀𝗲

• Core PCE expected: 3.4% by end-2025, stabilizing at 2.4–2.5% in 2026.

• Core CPI: 3.7% by end-2025.

• Fed cuts: projected 3.6% in 2025, 2.9% in 2026, aimed at labor market support rather than inflation.

𝗙𝗶𝘀𝗰𝗮𝗹 𝗖𝗼𝗻𝘀𝘁𝗿𝗮𝗶𝗻𝘁𝘀

• Recession scenario: deficit could spike to 9–10% of GDP.

• Automatic stabilizers alone could add ~0.5% to the deficit, with discretionary measures potentially adding another ~1%.

• Fed remains the critical backstop if labor weakness deepens.

Inflation isn’t the main threat - the cooling U.S. labor market is. Tariffs are delaying price adjustments, and monetary policy will be central to maintaining growth. Watch jobs, tariffs, and Fed signals closely.

#USEconomy #LaborMarket #Tariffs #FedPolicy #Inflation #MonetaryPolicy #GDPGrowth #RecessionRisk #InvestmentStrategy #LeanResearch #LRInsights

4

3 Oct 2025

𝗧𝗵𝗲 𝗖𝘆𝗰𝗹𝗲’𝘀 𝗠𝗶𝘅𝗲𝗱 𝗠𝗲𝘀𝘀𝗮𝗴𝗲𝘀: 𝗥𝗲𝘀𝗶𝗹𝗶𝗲𝗻𝗰𝗲 𝘃𝘀. 𝗖𝗮𝘂𝘁𝗶𝗼𝗻

𝗚𝗹𝗼𝗯𝗮𝗹 𝗺𝗮𝗿𝗸𝗲𝘁𝘀 𝗮𝗿𝗲 𝘀𝗲𝗻𝗱𝗶𝗻𝗴 𝗰𝗼𝗻𝘁𝗿𝗮𝗱𝗶𝗰𝘁𝗼𝗿𝘆 𝘀𝗶𝗴𝗻𝗮𝗹𝘀. U.S. GDP is tracking 3.9% annualized in Q3, equities are near all-time highs, and emerging markets are outperforming, led by Japan’s TOPIX ( 25% YTD), North Asia, and LatAm. Yet key cycle indicators suggest caution: job growth has slipped below 200k/month, the breakeven level to hold unemployment steady. Should layoffs accelerate, real income and consumption could come under pressure. Tariff effects remain in the system, with the heaviest impact expected in the next quarter.

𝗦𝗵𝗼𝗿𝘁 𝗿𝗮𝘁𝗲𝘀 𝗮𝗻𝗱 𝗶𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗲𝘅𝗽𝗲𝗰𝘁𝗮𝘁𝗶𝗼𝗻𝘀 𝗮𝗿𝗲 𝗰𝗼𝗻𝗳𝗹𝗶𝗰𝘁𝗲𝗱. The 2-year Treasury yield hovers near 3.6%, despite stronger data and GDP upgrades—historically, similar growth pushed it much higher. 1-year inflation swaps sit at 3.2%, even as commodity prices hit two-year highs. Long-term yields have retreated from near 5.0% to around 4.7%, driven more by supply adjustments than easing policy risks.

𝗖𝗿𝗼𝘀𝘀-𝗮𝘀𝘀𝗲𝘁 𝘀𝗶𝗴𝗻𝗮𝗹𝘀 𝗵𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁 𝘁𝗵𝗲 𝗶𝗺𝗯𝗮𝗹𝗮𝗻𝗰𝗲. Investment-grade credit spreads are near 90bps, the tightest since 1998, signaling optimism in corporate credit. Yet gold prices above $2,500/oz remain at record highs, reflecting persistent demand for safety. Equities, credit, and gold are diverging—showing the cycle hasn’t yet cleared its tests. Growth is stronger than feared, policy has shifted to ease, and financial conditions are supportive—but labor market fragility, muted inflation pricing, and record hedging confirm the clock is still ticking.

The market is resilient but cautious. Equity upside exists, yet investors should watch labor, tariffs, and inflation for signals that could recalibrate risk across asset classes.

#MacroMarkets #USGDP #Equities #EmergingMarkets #Treasuries #Gold #Inflation #FinancialMarkets #MarketOutlook #RiskManagement #EconomicCycle #FedPolicy #Investing #GlobalMarkets #MacroInsights

7

18 Sep 2025

𝗙𝗹𝗮𝘀𝗵𝗹𝗶𝗴𝗵𝘁 𝗼𝗻 𝗦𝗲𝗽𝘁𝗲𝗺𝗯𝗲𝗿 𝗙𝗢𝗠𝗖: 𝗣𝗵𝗮𝘀𝗲 𝗜𝗜 𝗼𝗳 𝗥𝗮𝘁𝗲 𝗖𝘂𝘁𝘀 𝗕𝗲𝗴𝗶𝗻𝘀 💡

The Fed appears ready to resume easing. At the September meeting, the fed funds rate is expected to drop 25 bps to 4.00%-4.25%, marking the start of Phase II of the rate-cut cycle.

𝗪𝗵𝘆 𝗻𝗼𝘄?

• Payroll growth has slowed dramatically: 3-month average at 29K vs 150K in July.

• Unemployment has risen to a cycle-high of 4.3%, touching the top of the Fed’s “full employment” range.

• Core PCE inflation remains elevated at 3.1% Q4/Q4, largely due to goods sector reflation, but services inflation is softening.

𝗪𝗵𝗮𝘁 𝘁𝗼 𝗲𝘅𝗽𝗲𝗰𝘁 𝗳𝗿𝗼𝗺 𝘁𝗵𝗲 𝗙𝗢𝗠𝗖:

1. September: cautious 25 bps cut; statement likely to downgrade the labor market without committing to immediate further cuts.

2. October & December: more easing probable, depending on updated data.

3. SEP dot plot: 2025 median now signals 75 bps total cuts (vs 50 bps in June), and 2026 median down to 3.125%, implying additional 25 bps cuts next year.

𝗪𝗵𝘆 𝗶𝘁 𝗺𝗮𝘁𝘁𝗲𝗿𝘀:

• History shows fast Fed response supports equities and lifts yields; delays deepen downturns.

• A dovish tilt in the Committee and stable inflation give the Fed flexibility to pace cuts while watching employment risks.

The labor market slowdown is the key trigger - September could mark the restart of the Fed’s easing cycle, but the pace will remain data-dependent.

#FOMC #FederalReserve #InterestRates #USInflation #FedPolicy #RateCuts #MacroEconomics #FinancialMarkets #CorePCE #EmploymentTrends #InvestingStrategy #LeanResearch #LRInsights

1

7

16 Sep 2025

𝗜𝗻𝗱𝗶𝗮 𝗖𝗣𝗜 𝗔𝘂𝗴𝘂𝘀𝘁 𝟮𝟬𝟮𝟱: 𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝘀𝗶𝗴𝗻𝗮𝗹𝘀 𝗮 𝗽𝗼𝘁𝗲𝗻𝘁𝗶𝗮𝗹 𝗥𝗕𝗜 𝗽𝗶𝘃𝗼𝘁

August CPI data show a calmer inflation landscape, challenging the RBI’s forecasts and hinting at more room for monetary easing.

🔹 𝗖𝗼𝗿𝗲 𝗶𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗲𝗮𝘀𝗶𝗻𝗴: Official core CPI fell to 4.1% y/y, with services hitting a 14-month low of 3.5% y/y. Non-standard measures like persistent and volatility-weighted CPI confirm weaker underlying price pressures.

🔹 𝗙𝗼𝗼𝗱 𝗶𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻: muted but mixed: Overall flat y/y, but seasonally adjusted monthly prices edged 0.5% m/m. Pulses (-14.5%) and vegetables (-15.9%) remain deep in deflation, while edible oils surged ( 21.2% y/y). Persistent items (cereals, pulses, spices) are steady at 2.8%, showing households aren’t feeling broad-based price shocks.

🔹 𝗦𝘆𝘀𝘁𝗲𝗺𝗶𝗰 𝘀𝗶𝗴𝗻𝗮𝗹𝘀: Import-sensitive items added ~1.6ppt to CPI, yet diffusion indices fell—price pressures are narrowing.

🔹 𝗣𝗼𝗹𝗶𝗰𝘆 𝗶𝗺𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀: CPI is already below the RBI’s Q3 forecast, and early September data suggest further downside. Coupled with recent GST cuts, there’s scope for another 25bp repo rate cut in Q4 2025, despite markets betting otherwise after strong GDP growth.

Inflation in India is behaving like a finely tuned system persistent enough to support economic stability, yet soft enough to allow policymakers to nurture growth through targeted rate cuts. For investors, corporates, and markets, the takeaway is clear: monetary easing may still have runway before FY26 ends.

#IndiaCPI #RBI #MonetaryPolicy #MacroInsights #InflationWatch #FinancialMarkets #LeanResearch #LRInsights

1

9

9 Sep 2025

𝗖𝗵𝗶𝗻𝗮’𝘀 𝗘𝗻𝗲𝗿𝗴𝘆 𝗧𝗿𝗮𝗽: 𝗙𝗼𝘂𝗿 𝗦𝘁𝗿𝗮𝗶𝘁𝘀, 𝗢𝗻𝗲 𝗔𝗰𝗵𝗶𝗹𝗹𝗲𝘀 𝗛𝗲𝗲𝗹 🛢

The world’s oil flows through just four chokepoints: Malacca, Hormuz, Suez, Bab el-Mandeb. Three in the Middle East, one in Southeast Asia—Malacca, through which 80% of China’s oil imports pass, sits under the shadow of U.S. naval power.

China is consuming the planet’s resources at an unprecedented pace - 40% of global raw materials today, up from 23% in 2006. Yet its dependence on imports is alarming:

• Copper: 80%

• Nickel: 95%

• Iron Ore: 75%

• Oil: 70%

• Gas: 40%

In 2023 alone, raw material imports cost $810B, nearly all shipped by sea. Malacca isn’t just a strait—it’s a modern strategic chokehold. History offers a warning: in 1941, Japan’s dependence on oil imports led to Pearl Harbor and eventual economic collapse. Technology and industrial might cannot offset strategic strangulation.

𝗖𝗵𝗶𝗻𝗮 𝗶𝘀 𝗱𝗶𝘃𝗲𝗿𝘀𝗶𝗳𝘆𝗶𝗻𝗴 𝗽𝗶𝗽𝗲𝗹𝗶𝗻𝗲𝘀 𝘁𝗼 𝗿𝗲𝗱𝘂𝗰𝗲 𝘃𝘂𝗹𝗻𝗲𝗿𝗮𝗯𝗶𝗹𝗶𝘁𝘆:

• 𝗢𝗶𝗹: Russia, Kazakhstan, Burma → 14% of imports

• 𝗚𝗮𝘀: Burma, Russia, Central Asia → 40% of imports

Energy security defines strategic power. Until China can secure multiple, reliable land and maritime routes, the economy remains exposed - no amount of reserves or innovation can fully offset a blocked strait.

#EnergySecurity #GlobalTrade #ChinaEconomy #OilMarkets #StrategicResources #MalaccaStrait #Geopolitics #SupplyChainRisk #RawMaterials #EnergyDiversification #LeanResearch #LRInsights

17

5 Sep 2025

𝗜𝘀 𝘁𝗵𝗲 𝗨.𝗦. 𝗟𝗮𝗯𝗼𝗿 𝗠𝗮𝗿𝗸𝗲𝘁 𝗕𝗿𝗲𝗮𝗸𝗶𝗻𝗴 - 𝗼𝗿 𝗝𝘂𝘀𝘁 𝗙𝗹𝗮𝘀𝗵𝗶𝗻𝗴 𝗮 𝗙𝗮𝗹𝘀𝗲 𝗦𝗶𝗴𝗻𝗮𝗹?

July payrolls rose only 73k vs 109k expected, with prior months revised sharply down. Strip out healthcare, and private hiring is barely moving - raising questions about whether the economy is near stall speed.

Large downward revisions often appear when cycles are turning. Small businesses bear the brunt of tariffs, and since large firms report faster, early data can mislead. Enter the Perkins rule: a payroll drop >1 standard deviation (~68k jobs) signals potential recession risk. Fewer jobs reduce spending and confidence, triggering more layoffs—a pattern seen in every major U.S. downturn.

But the rule isn’t destiny. In 1995, an initial payroll loss of 111k spooked markets. Revisions showed a smaller 46k loss, followed by a 215k rebound - soft landing, not recession.

𝗧𝗼𝗱𝗮𝘆 𝗹𝗼𝗼𝗸𝘀 𝗺𝗼𝗿𝗲 𝗹𝗶𝗸𝗲 𝟭𝟵𝟵𝟱 𝘁𝗵𝗮𝗻 𝟮𝟬𝟬𝟭 𝗼𝗿 𝟮𝟬𝟬𝟴:

🔹No major bubbles

🔹No credit binges

🔹Mild immigration tightening lowers the job-growth breakeven

Even a mild recession would trim employment ~1.5%, lifting unemployment modestly

If payrolls dip, expect fast Fed rate cuts. History shows quick Fed action supports equities and lifts yields, while delays deepen downturns. Right now, a Perkins trigger could extend the cycle rather than end it.

#USJobsReport #LaborMarket #PerkinsRule #EconomicOutlook #SoftLanding #RecessionRisk #FedPolicy #MacroTrends #PayrollData #InvestingInsights #MarketSignals #EmploymentTrends #RateCuts #EconomicCycles #EquityMarkets #LeanResearch #LRInsights

3 Sep 2025

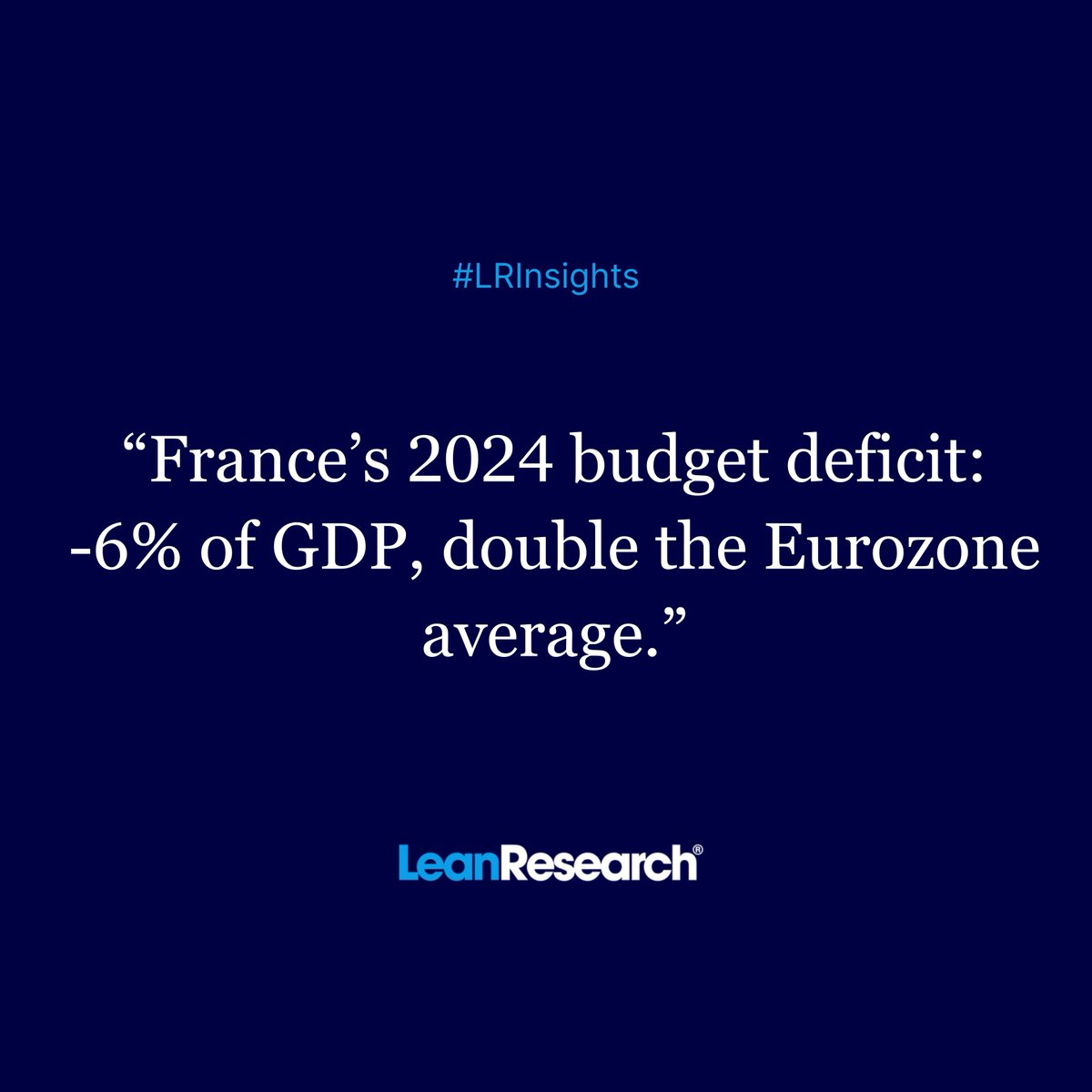

𝗙𝗿𝗮𝗻𝗰𝗲 𝗼𝗻 𝘁𝗵𝗲 𝗘𝗱𝗴𝗲 - 𝗮𝗻𝗱 𝘁𝗵𝗲 𝗟𝗲𝘀𝘀𝗼𝗻𝘀 𝗳𝗼𝗿 𝗗𝗲𝘃𝗲𝗹𝗼𝗽𝗲𝗱 𝗘𝗰𝗼𝗻𝗼𝗺𝗶𝗲𝘀

📉 91% of the French population rates the economy as “bad” - the worst among 30 surveyed countries, even higher than Turkey (78%) and Argentina (71%).

🔹 Budget stress: France’s deficit reached -6% of GDP in 2024, twice the Eurozone average, with debt over 100% of GDP and taxes at 45% of GDP - leaving almost no fiscal room to maneuver.

🔹 External risk: Over half of French government bonds (53%) are owned by non-residents. Without decisive action, confidence risks triggering a cascading sell-off.

🔹 Political volatility: Combined with government collapse and populist pressures, France faces a toxic mix of high debt, low growth, and constrained fiscal tools.

Macro takeaway for investors: France is not alone. Barclays’ financial stability assessment highlights other developed countries under pressure:

Japan 🇯🇵: Debt 237% of GDP, QE reliance 45%

Italy 🇮🇹: Debt 135% of GDP, cyclically adjusted deficit -3.5%

USA 🇺🇸: Gross financing needs 35% of GDP, primary balance -3.9%

Even “safe” economies have cracks. Long-term yields are rising, and credit ratings lag behind reality.

Fiscal space, debt ownership, and political stability matter as much as headline GDP. France is a stark reminder that high taxes high debt political fragmentation = limited buffers in a crisis. Investors should track debt sustainability, non-resident holdings, and primary balance trends, not just growth forecasts.

#Macro #FiscalPolicy #DevelopedMarkets #DebtSustainability #France #EconomicOutlook #InvestmentStrategy #GlobalEconomy #FinancialStability #LeanResearch #LRInsights

11

28 Aug 2025

𝗚𝗼𝗹𝗱 𝗶𝘀 𝗯𝗮𝗰𝗸 𝗮𝘀 𝗮 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗮𝘀𝘀𝗲𝘁 - 𝗮𝗻𝗱 𝘁𝗵𝗲 𝗻𝘂𝗺𝗯𝗲𝗿𝘀 𝘁𝗲𝗹𝗹 𝘁𝗵𝗲 𝘀𝘁𝗼𝗿𝘆.

🔹 Since 2022, central banks and sovereign wealth funds have tripled gold purchases - from ~100 tons per quarter to ~275 tons. Gold now accounts for >20% of global reserves (excluding the US, Germany, France, Italy, it’s just 11%).

🔹 Key buyers in 2024: China, India, Poland, Turkey. 42% of central banks plan to increase gold holdings further (OMFIF survey).

🔹 Developing countries are driving demand, while global investors allocate only ~2% of their portfolios to gold. Meanwhile, countries like Germany, Austria, Poland, and the Netherlands are repatriating gold reserves back home.

🔹 Perspective on scale:

• Total gold ever mined: 216k tons → a cube just 21m per side, yet with a market cap >$12T.

• Daily trading: ~$250B, rivaling S&P 500 turnover.

• China’s gold reserves: 5.1% of total reserves - every 1% increase = ~500 tons (~10% of global annual consumption).

🔹 Analysts are bullish:

• JPMorgan: $3,675/oz by Q4 2025 → $4,000/oz by Q2 2026

• Goldman Sachs: $3,700/oz end-2025

• Citibank: $3,500/oz near-term

• UBS & Deutsche Bank echo strong demand trends

🔹 Why it matters beyond the price : Rising gold can strengthen the dollar system even as a “non-dollar” asset. Gold acts as insurance for crises and de-dollarization trends. Bitcoin and digital assets may complement gold as strategic portfolio anchors, not competitors. If central banks needed to restore confidence in a crisis, greater then $5,000/oz is the math-backed price for a meaningful gold standard today. Trust, liquidity, and hedging against global risk - that’s why gold is strategic again.

#Gold #GoldPrice #Investment #CentralBanks #EconomicUncertainty #FinancialStability #GoldStandard #Geopolitics #Diversification #Commodity #GlobalEconomy #InvestmentStrategy #DeDollarization #HedgeAgainstInflation #LeanResearch #LRInsights

1

4

26 Aug 2025

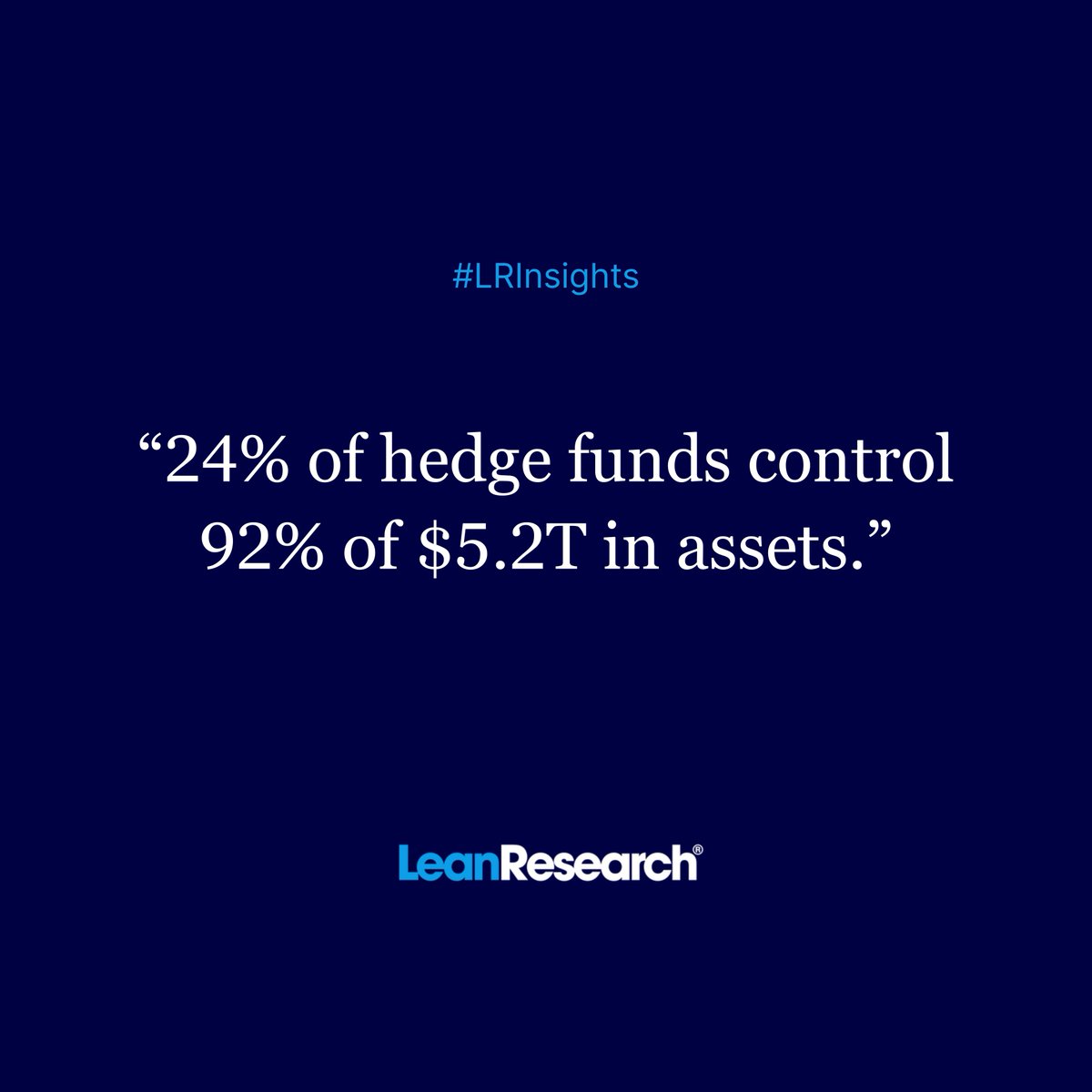

𝗛𝗲𝗱𝗴𝗲 𝗙𝘂𝗻𝗱𝘀 𝟮𝟬𝟮𝟱: 𝗧𝗵𝗲 𝗡𝗲𝘄 𝗥𝘂𝗹𝗲𝘀 𝗼𝗳 𝘁𝗵𝗲 𝗚𝗮𝗺𝗲

💵 Hedge Funds Are Changing—Big Time

The classic “2 and 20” fee model is dying . Many funds lagged indices, and investors got skeptical. Enter passthrough fees: management fees drop slightly, but all operating costs—salaries, travel, data—now fall on investors.

➡️ Impact: Gross returns of 14.6% can shrink to 6% net—less than half of profits reach investors. Yet, elite funds still reward: Citadel returned 60% in 2022, giving 38% net to investors, even as the S&P 500 fell 19%.

Access is exclusive. Entry tickets for top funds range from $100k to $10M. Many funds are closed, with waitlists lasting years.

Fees are climbing. Management fees average 1.77%, performance fees 17.3%, plus 4% in passthrough costs. Over 50 years, fees have gone from <10% of gross income to almost 30%.

Scale matters. Top 100 U.S. funds manage $5.2 trillion, with just 79 employees per fund on average. Globally, 533 mega-funds manage $3.34T. Only a few dominate.

Active investing still works —if you pick the right conditions. Historically, 10% of active funds beat benchmarks. But in turbulent 2022, 57% did. Active managers shine when markets are volatile or range-bound.

💡 Takeaways:

🔹 Hedge funds = high-fee, high-skill, exclusive platforms

🔹 Hidden passthrough costs can halve investor returns

🔹 Scale, infrastructure, and data = decisive advantage

🔹 Active strategies thrive in volatile markets, struggle otherwise

Investors : read terms carefully, know real costs, check performance history

Hedge funds aren’t just active investing—they’re a complex, evolving ecosystem, where only the best survive.

#HedgeFunds #Finance #Investing #AlternativeInvestments #ActiveManagement #FinanceTrends #WealthManagement #InvestmentStrategy #LRInsights #LeanResearch

3

21 Aug 2025

𝗦𝗵𝗮𝗿𝗲𝗵𝗼𝗹𝗱𝗲𝗿𝘀 𝘃𝘀. 𝗔𝗽𝗽𝗹𝗲: 𝗧𝗵𝗲 $𝟭𝟯𝟳 𝗕𝗶𝗹𝗹𝗶𝗼𝗻 𝗗𝗲𝗯𝗮𝘁𝗲

🔹 10 years ago: Hedge fund titan David Einhorn of Greenlight Capital took on Apple—not as a tech critic, but as a shareholder advocate. Owning just 0.12% of Apple, Einhorn sued the company to unlock its massive $137 billion cash pile—over 30% of Apple’s market cap at the time.

🔹 The demand: Einhorn proposed issuing preferred shares with a 4% yield, dubbed iPrefs, arguing Apple should return more cash to shareholders instead of hoarding it. Apple planned a shareholder meeting that would cancel this issuance and tweak its corporate structure. The court sided indirectly with Greenlight, and the hedge fund withdrew its lawsuit.

🔹 The turning point: Shortly after, Apple made a dramatic shift:

* 2013: Began issuing debt (previously debt-free).

* 2013–2016: Introduced dividends and buybacks, returning capital directly to shareholders.

* 2016: Warren Buffett’s Berkshire Hathaway entered the Apple story, reinforcing the stock’s long-term value case.

🔹 Today: Apple now distributes more than 100% of its Free Cash Flow via buybacks and dividends. Its balance sheet still holds $133 billion (~4% of market cap)—managed by Apple’s enigmatic hedge fund Braeburn Capital, whose exact investments remain a mystery.

💡What started as a small shareholder’s push for cash return reshaped Apple’s capital strategy for a decade. From hoarding cash to rewarding investors aggressively, Apple’s approach shows how corporate governance, activism, and smart capital allocation can align—or clash—with shareholder expectations.

#Apple #ShareholderActivism #CapitalAllocation #TechInvesting #FreeCashFlow #Dividends #Buybacks #ValueInvesting #CorporateStrategy #InvestingInsights #LeanResearch #LRInsights

31

19 Aug 2025

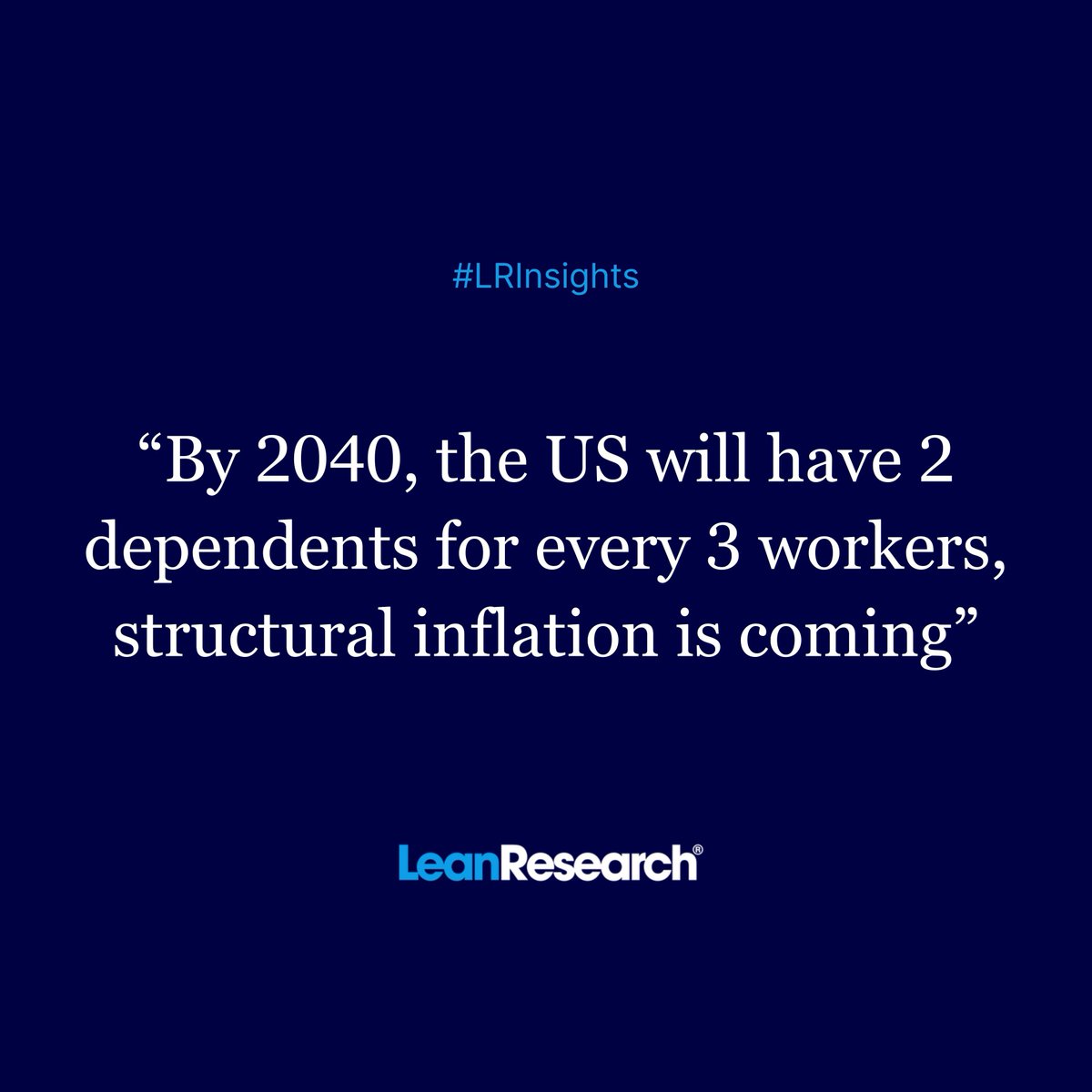

𝗔𝗻 𝗔𝗴𝗶𝗻𝗴 𝗪𝗼𝗿𝗹𝗱 𝗠𝗲𝗮𝗻𝘀 𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗜𝘀𝗻’𝘁 𝗚𝗼𝗶𝗻𝗴 𝗔𝗻𝘆𝘄𝗵𝗲𝗿𝗲

The 21st century lulled investors into a false sense of security: G7 inflation averaged just 2%, far from the 5% of the 20th century. But beneath the calm lies a structural shift that will keep prices on edge.

🔹 Aging populations = fewer workers.

Median ages are rising fast: China 🇨🇳 30 → 40, U.S. 🇺🇸 35 → 39, Japan 🇯🇵 50. Fewer people entering the labor market keeps unemployment artificially low, even when economic growth stalls.

🔹 Labor market illusions.

Japan’s GDP grew only 0.7% annually over 25 years—but unemployment stayed at 2–3%. The shrinking workforce masks weakness and keeps wages sticky, feeding inflation quietly.

🔹 Dependency ratio tells the story.

In the U.S., it’s climbed from 48 (2010) → 53 today, and could hit 65 by 2040. For every 3 workers, 2 dependents—an echo of mid-century inflation pressures.

🔹 Inflation is now structural.

This isn’t a temporary spike. Aging populations, labor constraints, and rising dependency ratios point to sustained, stagflationary forces. Portfolios need to reflect a world where price growth isn’t an anomaly—it’s the new normal.

#MacroTrends #Inflation #AgingPopulation #Stagflation #InvestingStrategy #GlobalEconomy #LRInsights #LeanResearch

5

13 Aug 2025

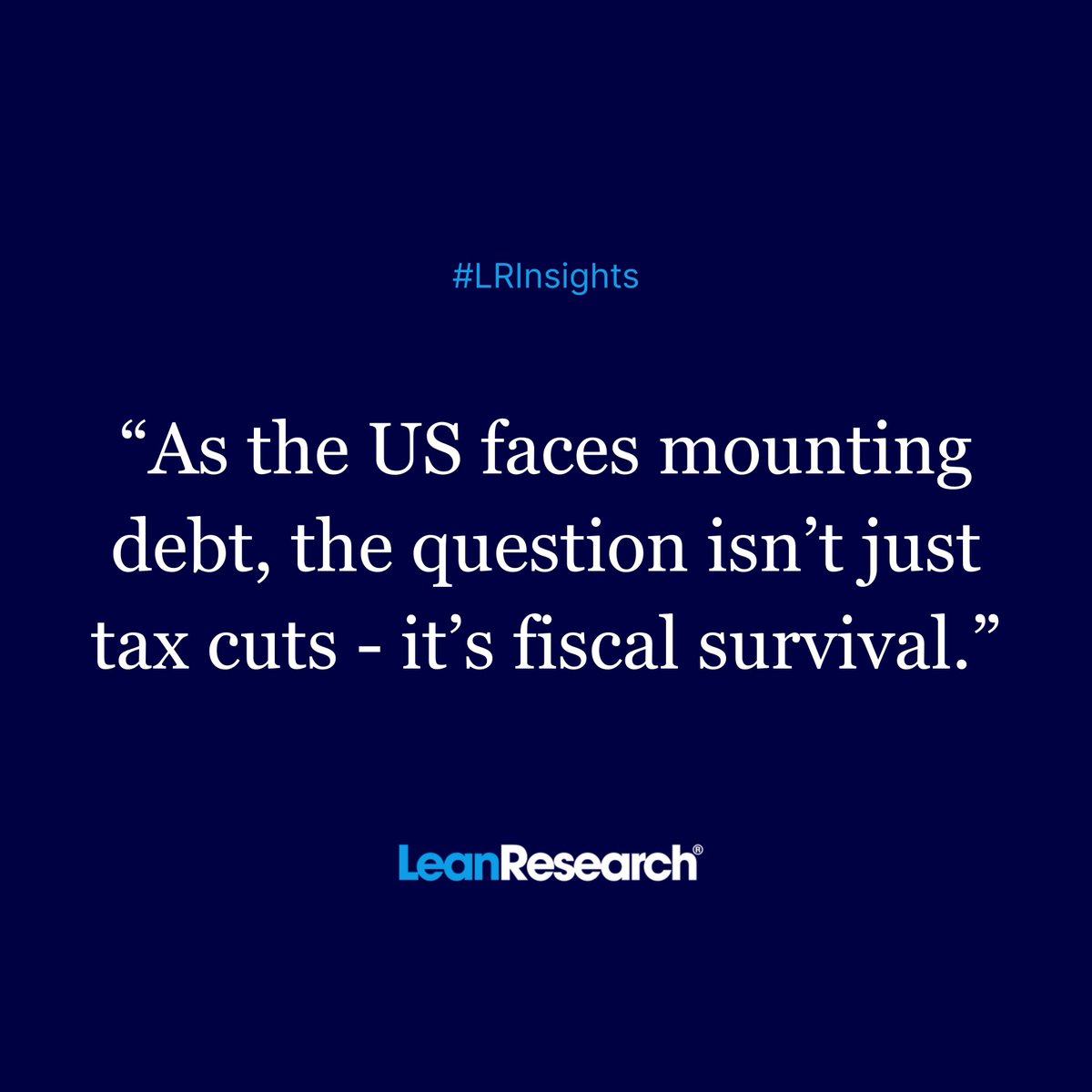

𝗔𝗺𝗲𝗿𝗶𝗰𝗮’𝘀 𝗧𝗮𝘅 𝗣𝗲𝗻𝗱𝘂𝗹𝘂𝗺 𝗦𝘄𝗶𝗻𝗴𝘀 𝗕𝗮𝗰𝗸?

For most of the 20th century, America taxed its wealthiest citizens at staggering rates - up to 94% in 1944, and 91% through the 1950s. That changed with Reagan’s cuts in the 1980s, dropping the top rate to 28%. Since then, it's never climbed back above ~40%.

But with the U.S. now running a $2T deficit (~7% of GDP) and adding $1 trillion in debt every 100 days, tax policy is back in the spotlight - and ripe for reversal.

🔹 Top 1% earn ~25% of all income but pay ~45% of federal income tax

🔹 Most middle-income earners face effective tax rates below 20%, thanks to brackets and deductions

🔹 Trump’s 2025 plan would extend tax cuts, remove taxes on tips and Social Security, and slash corporate rates to 15% for manufacturers

Meanwhile, tariffs are now doubling as revenue tools:

🔹 Proposed 60% tariff on Chinese imports, and 10 - 20% universal base tariff

🔹 Potential revenue: $300 - 500B/year, not nearly enough to offset a recession-led revenue shortfall

📍 If unemployment rises 1 percentage point, the deficit could swell by 1.5 - 2.5% of GDP. In a downturn, only the Fed may be able to step in, with deeper rate cuts and renewed liquidity support.

This isn’t just tax reform - it’s fiscal survival. In today’s fragile macro mix, politics, deficits, and Fed policy are more tightly linked than ever.

#MacroView #USTaxes #FiscalPolicy #TrumpAgenda #USDeficit #RateCuts #USDebt #FedWatch #CapitalMarkets #EconomicOutlook #LeanResearch #LRInsights

6

8 Aug 2025

𝗣𝗼𝘄𝗲𝗹𝗹’𝘀 𝗗𝗶𝗹𝗲𝗺𝗺𝗮: 𝗦𝗼𝗳𝘁 𝗟𝗮𝗻𝗱𝗶𝗻𝗴 𝗼𝗿 𝗦𝘂𝗱𝗱𝗲𝗻 𝗦𝘁𝗮𝗹𝗹?

The July jobs report came in weak. Rate-cut bets surged. It’s déjà vu from 2024 — when soft labor data triggered a surprise 50bps cut. But 2025 is different. Inflation is stickier, deficits are wider, and consensus is fractured.

🔹 Goldman sees five cuts by end-2026, citing higher tariffs and rising unemployment (4.4% by year-end).

🔹 JPMorgan warns of stagflation: soft jobs sticky prices = policy cornered.

🔹 BofA says no cuts in 2025 — this isn’t recession, it’s labor constraints (e.g., immigration-driven supply shock).

The real issue? Fiscal space is shrinking. If a recession hits, the deficit could balloon to 9–10% of GDP. Without tariff revenues, the math breaks. That leaves only one player: the Fed.

But here’s the rub...

Forecasts keep failing.

▪️ Wall Street’s S&P 500 targets have missed for 8 straight years

▪️ Fed rate path predictions? Even worse

▪️ Buffett’s take: "I don’t even trust my own rate forecasts."

📌 Most labor indicators still show strength. But if the cracks widen, Powell will be forced to act — not because the market wants it, but because fiscal policy won’t be able to.

In this cycle, monetary policy isn’t Plan B. It’s the only plan.

#FedWatch #InterestRates #LaborMarket #RecessionRisk #FiscalLimits #Inflation #MacroStrategy #USEconomy #Powell #ForecastingFatigue #BuffettQuotes #PCE #Stagflation #LRInsights #LeanResearch

13