Lawyer, Interested in Economy & Markets!

Joined November 2021

- Tweets 7,810

- Following 1,244

- Followers 1,846

- Likes 55,892

1,749 Photos and videos

#WATCH | On RBI keeping repo rate unchanged, Chief Economist for India at Bank of America (BofA), Rahul Bajoria says, "I think this was along expected lines. I think the message from the Reserve Bank today was one of assurance that, as far as the macroeconomic situation is concerned, obviously, the current West Asia crisis is having some impact on inflation, and it is going to have some negative impact on growth, but things are under control. I think the expectations of measures on stabilising the rupee, they are going to add a lot of confidence in the system. So broadly we think that this was a policy meeting where the central bank has kind of given assurance that they are looking at the macroeconomic situation and they will be agile to the evolving outcomes, but there is no need to panic, or there is no need to be very concerned."

2

4

7

3,893

Anika retweeted

Jun 5

FII को टैक्स छूट के बड़े फायदे :

📌Foreign investment in longer-tenor government securities provides a relatively stable

source of capital, supporting government spending and investment in key areas.

📌 G-sec yield curve enhances price discovery, strengthens interest rate signalling, and improves the effectiveness of open market operations across different maturities.

📌Foreign participation broadens the investor base, increases competition in both

primary auctions and secondary markets, and compresses term premia, thereby

reducing the government's borrowing costs.

📌Greater foreign participation improves liquidity and price discovery in the G-sec

market, enhancing the efficiency of the broader financial system, as G-secs serve as

key benchmark rates for pricing corporate bonds, bank lending, and infrastructure

financing.

📌Well-developed and liquid G-sec markets, including at the longer end of the yield

curve, facilitate the effective transmission of monetary policy by enabling policy rate

adjustments to be reflected more efficiently in medium- and long-term borrowing

costs.

📌Market-opening measures, including the Fully Accessible Route (FAR), have facilitated

the inclusion of Indian government securities in global bond indices in the past,

attracting passive and long-term foreign capital inflows while enhancing the credibility

and global integration of the domestic bond market

#FII #sharemarket #investing

14

4

34

4,225

Anika retweeted

Did the Reserve Bank of India (RBI) secretly sell USD 12 BILLION of its gold reserves to defend the Rupee?

A recent Bloomberg report claimed exactly that.

The RBI and Indian Govt stepped in, calling the report "FAKE". So, who is right?

Let’s break down the exact math that Bloomberg and other so called Economist used to fool the public. 🧵👇

7

168

426

55,595

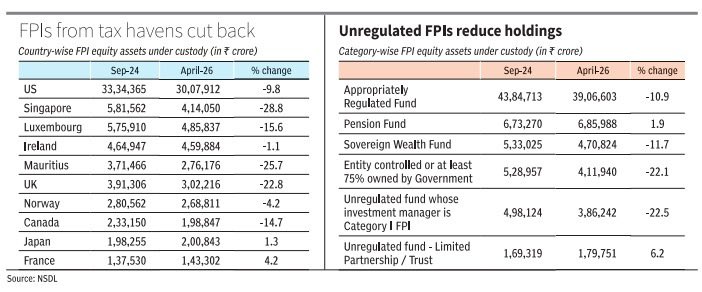

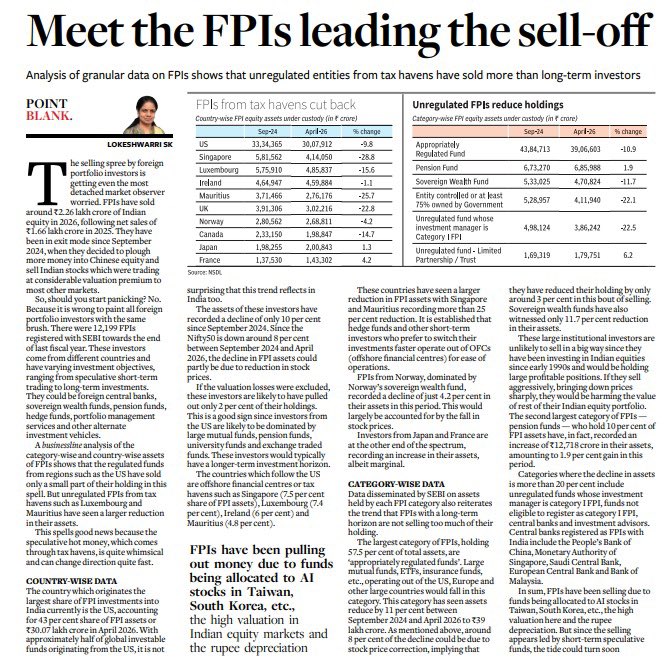

The headlines about a catastrophic FPI exodus look incredibly different once you look at the actual data.

What actually left? Volatile hot money from tax havens like Singapore, which dropped 28.8% to chase short-term AI hype elsewhere.

The bedrock capital is completely safe; regulated US funds command 43% of the total share and pulled a microscopic 2% after adjusting for market corrections.

The structural foundation remains entirely secure.

Don't fall for fear mongering.

521

Anika retweeted

Narrative buster

This actually destroys the narrative run by the opposition that Foreign Investors are abandoning India.

The selling is heavily concentrated in offshore financial centres and speculative pools of capital:

- Singapore: -28.8%

- Mauritius: -25.7%

- UK: -22.8%

These are jurisdictions widely used by hedge funds and fast-moving investors for tactical allocation shifts.

Now look at long-term capital:

- Pension funds actually increased holdings by 1.9%

- Japan increased holdings

- France increased holdings

- Norway’s sovereign wealth-linked investments barely declined

Even the largest category the Appropriately Regulated Funds holding 57.5% of all FPI assets saw only limited real selling once market correction effects are adjusted.

So what is happening?

After Indian markets delivered nearly 2x returns in the last 5 years, some hot money is rotating toward AI-heavy markets like Taiwan and South Korea.

This AI boom is going to burst even the messiah of Piddi's Raghuram Rajan has admitted that and when that happens the hot money will come back again.

That is normal global capital rotation, not a collapse of confidence in India.

Meanwhile India’s macro fundamentals remain strong:

- Fastest growing major economy

- Strong GST collections

- Healthy banking sector with record profits and low NPAs

- Strong domestic demand all macroeconomic Indicators remains strong.

- Massive infrastructure push

- Stable financial system

Long-term investors follow fundamentals. Speculative money follows momentum.

The composition of FPI flows matters. Serious capital is largely staying invested in India.

25

138

386

14,674

Anika retweeted

May 26

Fuel, fertilisers and forex are immediate external pressure points arising from global instability and affecting all nations.

Crude prices, fertiliser prices and forex volatility are “imported risks”. A responsible government flags them and acts on them. Pretending these are secondary issues shows how casually the Congress treats macroeconomic vulnerability.

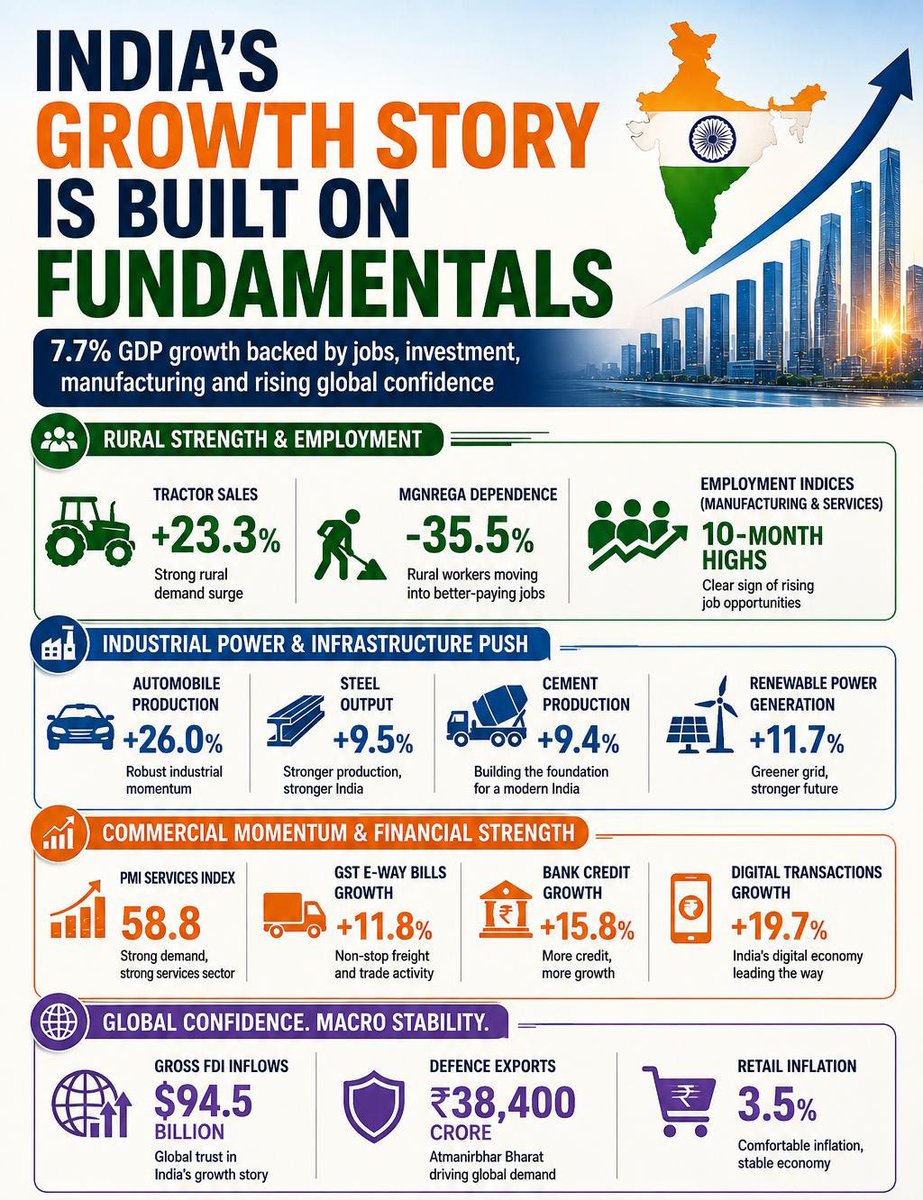

On private investment, the argument is selective. Investment is driven by four things: demand, profitability, credit availability and policy confidence. On all four counts, the current evidence points towards strengthening fundamentals.

Actual private capex is visible. CII’s analysis of nearly 1,200 companies from the CMIE Prowess database showed private sector investment rising 67% year-on-year to ₹7.7 lakh crore in September 2025, from ₹4.6 lakh crore a year earlier. Manufacturing accounted for nearly half of this capex, with services also contributing strongly. Capacity utilisation rose to 75.6% in Q3 FY26, new order books grew 10.3% year-on-year, and bank credit growth strengthened in the second half of FY26.

Similarly, there is a deliberate attempt to mislead on FDI. Low net FDI does not automatically mean low foreign investor confidence. Gross FDI inflows in FY26 rose to around $94.5 billion, while net FDI increased six-fold compared to the previous fiscal year.

The flaw in the comparison is this: the pre-2014 “peak” private investment cycle was heavily debt-fuelled and ended in stalled projects, over-leveraged corporates, stressed banks and the NPA crisis. Using that peak as a benchmark without mentioning the balance-sheet damage it created is dishonest economics.

The banking system today is strong enough to finance growth. Public sector banks closed FY 2025–26 with gross NPAs at 1.93% and net NPAs at 0.39%, historically the lowest levels. Their gross advances grew 15.7% year-on-year to ₹127 lakh crore, with retail, agriculture and MSME advances growing 18.1%, 15.5% and 18.2% respectively. This is the opposite of an economy starved of credit.

Corporate profitability is improving, which is usually the precondition for a fresh investment cycle. A sample of 837 listed companies showed Q4 FY26 adjusted net profits rising to ₹3.24 trillion, up from ₹2.81 trillion a year earlier, while revenue rose to ₹28.65 trillion. Profit growth outpaced revenue growth, and margins reached their highest level in five years.

Indian companies investing abroad also cannot be lazily framed as a flight from India. A stronger Indian corporate sector will naturally acquire assets, build supply chains and expand market access abroad. That is a sign of globalising Indian enterprise. The real question is whether companies are also investing at home. The CII capex data, bank credit data, profit data and capacity utilisation data show that they are.

So the answer is simple: India is watching the 3Fs because external shocks must be managed carefully. Meanwhile, the domestic investment cycle is being supported by clean bank balance sheets, strong corporate profits, rising private capex, broad-based credit demand and record gross FDI inflows.

The Congress wants to convert every macroeconomic risk into a political slogan. The data does not support that alarmism.

May 26

The FM has said that the 3Fs—Fuel, Fertilisers, and Forex—-are matters of great concern.

But she forgets the all-important fourth F: Falling rates of private investment that have been in evidence these past few years. Net FDI flows have declined and private corporate investment as a % of GDP is at half the peak pre-2014 level. Indian businesses are seeking more predictable and profitable ventures abroad and Indian corporate personalities are taking up residence abroad.

Investment is as much a financial decision as it is driven by psychological factors. The lack of broad-based consumer demand growth has disincentivized companies from investing. Similarly, the overall atmosphere of threat, intimidation, and intrusiveness created by the Modi Government is a psychological deterrent, as is the know-it-all attitude and approach of the Modi Govt.

Winning elections through large-scale manipulation of electoral rolls is one thing. But recognising what really ails the economy with humility and sobriety and taking remedial actions is entirely another matter.

18

69

196

9,502

Anika retweeted

May 26

Rahul Gandhi's political career in a nutshell..😂

2

74

364

7,372

The claim that the government is hiding risks or drifting into protectionism is completely false.

The CEA's article shows that Economic Surveys explicitly acknowledge global risks and target regulatory predictability.

A band-aid is when you hide the wound, but this government has named the disease and is administering the medicine!

Sadly, @surjitbhalla clearly didn’t read the discharge summary before going on an incoherent rant.

1

3

254

Anika retweeted

May 15

This is from 2024. Same offenders. This time too FM @nsitharaman took them head on and like cowards they deleted the tweet and apologized. As I said, repeat offenders do not deserve any leniency. This is a disgrace.

3 May 2024

Again, wonder where this is come from. Again, was not checked with @FinMinIndia Pure speculation. Sorry, @CNBCTV18Live, particularly during #LokSabhaElection2024

125

323

6,103

Repeat Offender= Timsy Jaipuria and CNBC TV18.

3 May 2024

Wonder where this is come from. Was not even double checked with @FinMinIndia . Pure speculation.

Sorry, @CNBCTV18Live speculation, particularly during #LokSabhaElection2024

5

609

Repeat Offender= Timsy Jaipuria and CNBC TV18.

3 May 2024

Again, wonder where this is come from. Again, was not checked with @FinMinIndia Pure speculation. Sorry, @CNBCTV18Live, particularly during #LokSabhaElection2024

4

360

Repeat Offender= Timsy Jaipuria and CNBC TV18.

3 May 2024

Wonder where this is come from. Was not even double checked with @Finmin. Pure speculation.

Sorry, @CNBCTV18Live speculation, particularly during #LokSabhaElection2024

1

2

310

Anika retweeted

3 May 2024

Wonder where this is come from. Was not even double checked with @Finmin. Pure speculation.

Sorry, @CNBCTV18Live speculation, particularly during #LokSabhaElection2024

64

138

383

61,056

Anika retweeted

3 May 2024

Wonder where this is come from. Was not even double checked with @FinMinIndia . Pure speculation.

Sorry, @CNBCTV18Live speculation, particularly during #LokSabhaElection2024

133

284

952

374,823

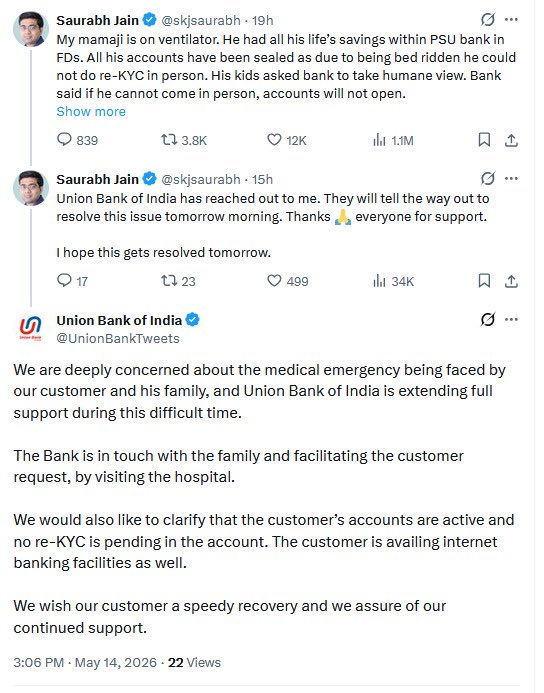

Banks can make mistakes, and customers are right to raise genuine grievances. But amplifying incomplete or unverified claims only creates unnecessary panic.

A recent viral post alleged that a bedridden customer’s accounts were frozen due to pending KYC. Union Bank of India later clarified that no re-KYC was due and the customer’s internet banking remained fully operational.

Half-truths undermine trust and dilute the impact of legitimate consumer concerns. Verify the facts before sharing.

3

213

Big win for BJP as KC Venugopal will continue to advice Pappu Shri @RahulGandhi

#WATCH | Delhi: Congress General Secretary (Org) KC Venugopal says, "The final decision has come, and the Congress high command decided VD Satheesan as the Chief Ministerial candidate for Keralam Government. I am welcoming that decision wholeheartedly. I am congratulating VD Satheesan on this position. I think that people of Keralam have given a big verdict for the UDF. The government and the leadership of VD Satheesan can fulfil the aspirations and promises of the people of Keralam. Certainly, we are totally behind the government of Keralam."

1

210

VIDEO | Tamil Nadu: Clash breaks out between Congress-DMK supporters in Mayiladuthurai.

#TamilNaduNews #DMK #Congress

(Full video available on PTI Videos - ptivideos.com)

672

most developed state saaar

May 8

”நான் தான் விஜய்.. கூட்டணி பேச தான் நான் வந்திருக்கேன்”... தவெக தலைவர் விஜய் வீட்டு வாசலில் புது பைக்கில் வந்த நபர் செய்த செயல்..!

#Neelankarai | #TVK | #TVKVijay | #PolimerNews

427