Head of Financial Markets @Notabene_id. Finance and blockchain. Financial Engineer from @UCBerkeley.

Joined May 2021

- Tweets 206

- Following 418

- Followers 368

- Likes 840

38 Photos and videos

Stablecoins are just fiat

1

47

!!!

May 12

The stablecoin sandwich is just correspondent banking on different rails.

Same bilateral agreements, same pre-funded positions, same corridor-by-corridor expansion. The costs don't disappear - they shift.

I wrote a piece about how we got here and what I think we should be building towards instead 👇

Looking forward to the conversation on "Killing the Stablecoin Sandwich" at @thestablecon EMEA with @sytaylor and @TeddHuff next week in Amsterdam - will see some of you there.

31

Proud of what we’re building!

Apr 21

When I show people Notabene Flow in action, there's always a lightbulb moment.

Create an invoice → send a payment link → recipient picks their provider → authorized, settled on-chain, reconciled. Real time.

No chasing payments. No manual reconciliation. Invoice data travels with the payment end to end.

I'll be hosting a live demo next Thursday 4/30. Join to see more uses and ask any questions you have — link in the replies.

1

1

137

Tarek retweeted

Apr 10

88% of companies receiving stablecoin payments convert to USD immediately.

These companies are using stablecoins as payment rails and converting on arrival because the infrastructure to do anything else isn't there yet.

Which means the real product gap isn't "can I pay with stablecoins" — it's "can I pay with stablecoins and have it feel like every other payment my finance team processes."

That's the infrastructure problem we're solving with @notabene_id Flow.

5

1

28

3,372

Tarek retweeted

Mar 31

Excited for us to partner with Better Money on bringing their infrastructure into Notabene Flow, the only stable coin native pull payment network at @notabene_id

3

1

8

1,212

Tarek retweeted

20 May 2025

1/ US has finally chosen again to be leaders in the area of crypto regulation.

With this it will start moving quickly. I believe that by the end of this decade the vast majority of value being moved globally will be #stablecoins. This is the first step to continued US currency dominance in the future.

US were actually the first back in 2013 at offering clarity. This was the FinCEN guidance from 2013 that allowed @brian_armstrong to turn @coinbase into a rocket ship.

19 May 2025

The GENIUS Act is

✅Pro-innovation

✅Pro-consumer

✅Pro-America

We need the GENIUS Act!

1

3

7

702

Most interesting DeFi apps operating today:

- @ethena : A synthetic dollar protocol backed by ETH and BTC. It stabilizes its value through delta-hedging.

- Curve.fi (duh!): A decentralized exchange for stablecoins. I believe there will be huge adoption for this type of application.

- @AerodromeFi : A mix of trading and swapping. I love the interface!

1

264

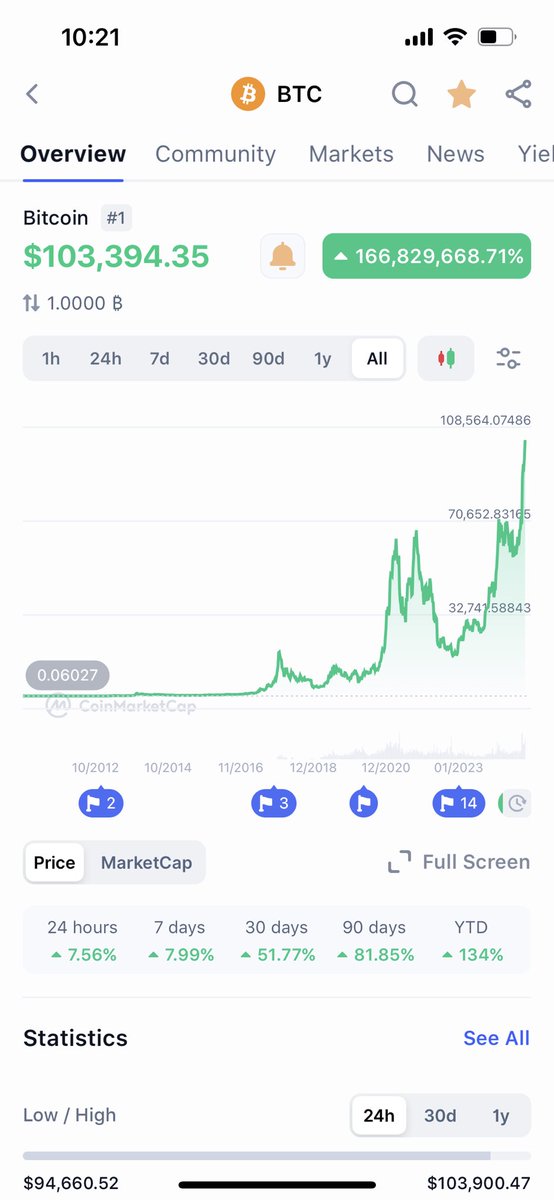

aged worse than milk

8 Nov 2019

Keep dreaming. Bitcoin is never going to hit $100,000!

1

263

Thesis on money movement

As we continue discussing why the future of money, as we perceive it, will change, it becomes clear that the tokenized dollar is no brainer to the evolution of monetary exchange.

Setting aside the commonly shared advantages of the tokenized dollar, imagine a world where money is no longer constrained by banking hours, outdated rails, or human error. A financial system where money transfers come at zero cost. This isn’t a prediction but rather a reality that has yet to be fully realized.

Tokenized dollars will be the fuel for payment processors. When I envision the tokenized dollar, I don’t see it as an additional layer in the current payment stack, though, for the time being, it may coexist with traditional systems in what’s often referred to as the “stablecoin sandwich.” Instead, I view it as the foundation of a completely parallel system that bypasses card network fees and banks.

The card network model has been extensively tried and tested, and countless startups have attempted to disrupt Visa and Mastercard. However, none have yet achieved true product-market fit. Closed-loop payment systems, branded cards, and loyalty programs may work in theory, but they’ve never addressed the core issue.

Do I think banks will disappear? Definitely not. But do I foresee card networks, interbank operations, and closed systems losing significant market share? Absolutely; I am confident in that.

Tokenized dollars will reduce payment margins to near zero. This will made us think of new ways to generate revenue; hence, providing real value!

2

125

Episode 25 is released!

Patrick O'Meara - Part 4: Misconceptions, Founder Experience, Vision

In this episode, Patrick O'Meara and I concluded our discussion on the most common misconceptions regarding crypto, founder experiences, and the future vision of blockchain.

As always, subscribe, like, and share ;)

youtu.be/4eUcYvZlrec?si=I4w3…

1

2

114

Episode 24 is out!

In this episode, I continue the conversation with Patrick where we dive deep into tokenization at a deeper level:

Why is tokenization taking off today and not 4 years ago?

We explore the factors that have driven the recent surge in interest of tokenization.

What are the lowest hanging fruits in the market?

Patrick and I discuss the most promising areas and use cases where tokenization can make an immediate impact.

What kind of exposure are institutions looking at?

Institutions are eyeing the tokenization space closely, but what are their specific interests and concerns? We cover the types of assets, risk appetites, and strategies that are attracting attention.

As always, subscribe, like, and share!

youtu.be/BeWgGS29qAI?si=jy_G…

65

Going back to the stablecoin argument, Nic presents in the second what he refers to as Gorton and Zhangism.

The second argument Nic addresses comes from economists Gary Gorton and Jeffery Zhang, who argue that stablecoins resemble the flawed US “free banking" era (1830s-1860s) and are therefore unlikely to succeed.

Gorton and Zhang claim that stablecoins, like banknotes issued by banks during that period, will face crises and fail to maintain their peg to the dollar, making them an unreliable medium of exchange (MoE).

They emphasize that stablecoins don't satisfy the "No Questions Asked" (NQA) principle, meaning that people will always question their value before accepting them in transactions.

Nic counters by arguing that the US free banking era is a poor analogy. He points out that the instability of US banks during that period was due to regulatory restrictions, such as forcing banks to hold risky state government bonds and prohibiting nationwide branching, which made them vulnerable to failures. In contrast, stablecoins today hold safe, short-term assets like US Treasuries and are not involved in risky lending or maturity transformation, making them much more stable.

Finally, Nic critiques Gorton and Zhang’s view of the NQA principle, noting that even traditional bank deposits have faced scrutiny during crises, such as the 2023 bank runs.

Despite occasional issues, stablecoins have adapted, becoming more resilient over time, and are increasingly treated as money in real-world use cases.

1

130

I recently got my hands on one of the most interesting articles on stablecoins by Nic Carter.

In the upcoming posts, I’ll be summarizing it.

The article mainly presents various arguments against stablecoins and why some believe they won't succeed. Nic counters each argument.

1

69

Nic counters by arguing that stablecoin issuers have become more risk-averse, pointing to improved practices and oversight in recent years.

Moreover, ratings firms now assess stablecoin risks, and regulations are being crafted to reflect their unique nature, rather than forcing them into traditional banking frameworks.

44