Joined October 2024

- Tweets 77

- Following 79

- Followers 6,376

- Likes 24

5 Photos and videos

Jun 12

Our current thesis remains unchanged: PTFE is merely a secondary, non-mainstream solution that is highly unlikely to achieve commercial mass production. Instead, the M10Q configuration remains the clear preferred choice, primarily because it offers a broader pool of qualified suppliers and commands strong deployment support from tier-1 PCB fabricators.

1

1

34

4,383

Jun 10

Driven by the non-stop price hikes in E-glass ( 60% to 90% YTD), Taiwan's Glotech has hit record revenues, and Nan Ya keeps growing its revenue month-over-month. If you want to track the actual performance and profit conversion of the E-glass rally, looking at these two companies is your most direct bet

2

35

13,583

kokycpcb retweeted

Jun 5

Nobody is asking who makes the <$1 multi-layer ceramic capacitor (MLCC) that keeps voltage stable across every chip in the rack, that every AI server needs tens of thousands of, that has long extended lead times, and going through an unprecedented price hike. AI server MLCC demand is growing ~5x by CY27. New production lines take 2 years to build. The bottleneck is spreading.

85

103

836

300,257

Jun 5

理想是這樣...要用美系的..就接受比較高的價格..

亞洲系的板廠,配合度還是好的

這是現實問題

PCB是所有電子產品的核心基板,卻幾乎隱形存在。在 AI 熱潮中,Nvidia 等大廠的高階 AI 伺服器電路板,絕大部分由中國製造,全球約 60% PCB 產能來自中國,美國本土市占率已從過去 30% 暴跌至僅 4%,形成嚴重國家安全風險。

中國製 PCB 可能被植入惡意元件,導致資料外洩、系統效能降低,甚至飛彈導引失靈。美國國防部因此高度警覺,要求關鍵採購必須來自國內。國防官員警告,這是最容易被破壞的供應鏈環節。

為解決危機,美國國會兩黨正推動《保護電路板與基板法案》,提供選擇美國製 PCB 的企業 25% 稅務抵免,並擬撥款 30 億美元補助本土廠商。 $TTM Technologies 與 Sanmina 這兩家美國上市 PCB 廠商,正加速擴張國內產能:TTM 將在紐約州與威斯康辛州新建大型工廠,完工後美國將擁有 18 座廠。

AI 需求爆炸性成長,導致 PCB 價格大漲 5%~40%,TTM 執行長表示「晶片不會漂浮」,所有先進晶片都必須靠高階 PCB 才能運作。儘管 Nvidia 已透過 X 光與 AI 檢測降低風險,但供應鏈過度依賴中國仍被視為重大漏洞。

在美中科技戰升級之際,此議題凸顯美國重建關鍵電子供應鏈的急迫性。專家呼籲,唯有發展具競爭力的本土 PCB 產業,才能確保 AI 與國防科技的長期安全。

cnbc.com/2026/06/03/beneath-…

2

2

23

6,244

kokycpcb retweeted

Jun 4

No, people are misinterpreting $AVGO CEO comments.

Demand is insatiable in general, but hyperscalers don't want to be bottlenecked, so it's inevitable $GOOGL and others multi-source.

Broadcom's bottom line keeps increasing, but because the pie keeps increasing, Mediatek, Marvell, AlChip, and all the others will benefit too.

But the latter much more than Broadcom.

13

18

327

92,081

Jun 4

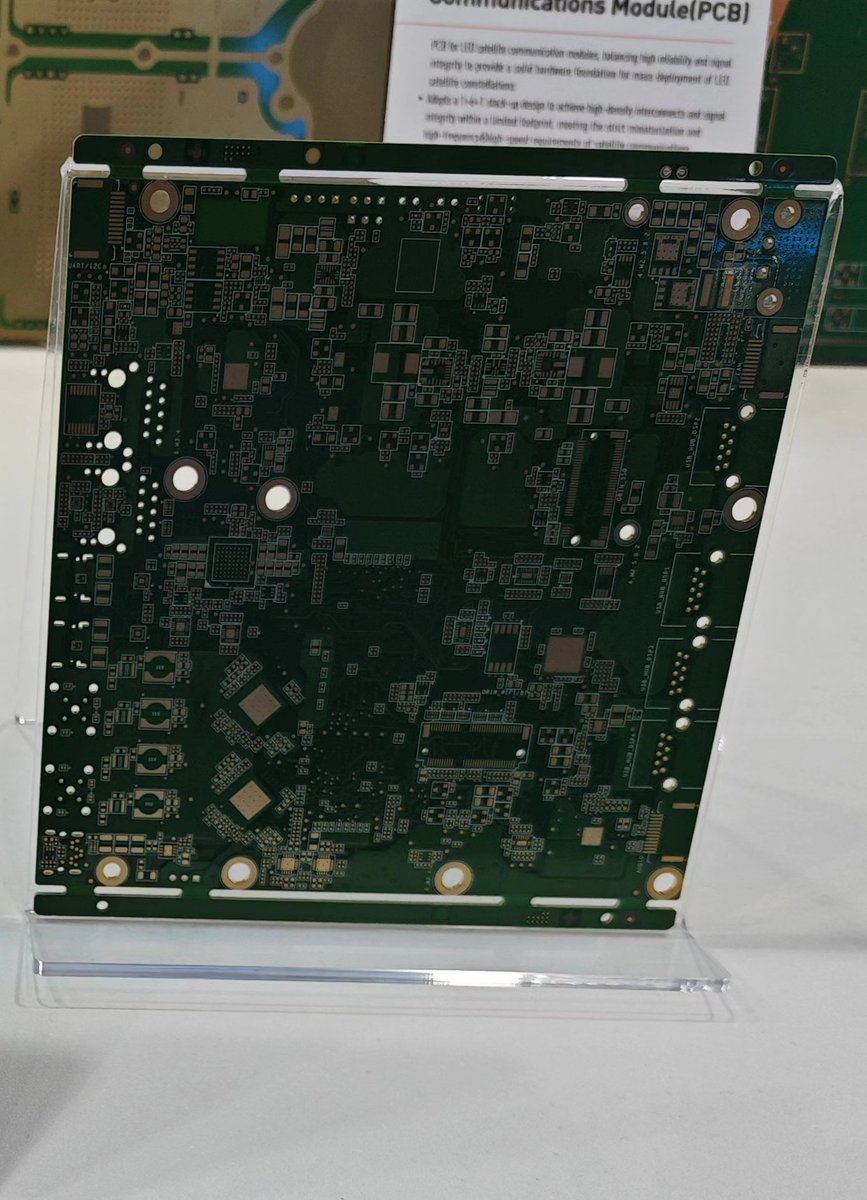

It has been highly rewarding to gather tangible insights at this year's COMPUTEX, particularly regarding the emerging roadmap for Humanoid Robotics PCBs

3

36

4,122

Jun 4

The market always loves to think Taiwanese players are taking the biggest piece of the pie. In reality, for the Vera CPU, Ibiden is still the heavyweight supplier—taking up more allocation than both Taiwanese suppliers put together....ha

Computex 2026:Agentic AI 時代來臨

Vera CPU 與 Agent Toolkit 為 NVIDIA 布局 Agentic AI:在 Oracle 大單支持下,GF認為 NVIDIA 單獨 Vera CPU 的年營收可見度達到 200 億美元是合理的。

⇒ Vera CPU 供應鏈:景碩科技、AMKR

Vera Rubin 系列用於 AI Agents:NVIDIA 宣布 Vera Rubin 平台已進入量產,預期 Rubin Sept 將在 9 月、Vera Rubin NVL72 將在 10 月進入大幅拉貨階段。

NVIDIA RTX Spark 為 AI Agent PC 提供動力:GF相信這將擴大 NVIDIA 在 AI PC 市場的地位,但由於 ARM 相容性持續存在問題,仍將屬於利基市場,對 Intel 與 AMD 的影響有限。

⇒ 根據GF先前的報告,預期 NVDA 不僅與 ARM 合作,也會與 Intel 合作。

NVIDIA 財務分析師 Q&A 會議:NVIDIA 宣布將返還至少 50% 的自由現金流。管理層認為 Vera CPU 是開拓全新市場,而非搶奪既有市占,其 CPU 長期出貨量機會將超過 GPU。

Intel 在 18A 良率良好下恢復 CPU 重要性,已有 3 款 CPU SKU 進入量產。

2

9

58

14,765

Jun 3

The market thinks the lack of a beat-and-raise is disappointing, but here is a highly likely alternative scenario: due to severe upstream material shortages, clients are using hyper-inflated forecasts—well above what CoWoS capacities can actually turn out—to force the supply chain to hoard materials for at least the next two years. But over at Broadcom, you simply won't see that massive gap between phantom forecasts and real chip numbers.

Broadcom $AVGO Q2:

-Revenue: BEAT, $22.187B vs $22.13B, 0.3%

-Non-GAAP EPS: BEAT, $2.44 vs $2.40, 1.7%

-Guide: BEAT, Q3 revenue guide $29.4B vs $28.47B consensus, 3.3

A beat-and-raise where expectations were already high. AI semiconductor revenue $10.8B up 143% YoY, above guide, on custom accelerators and AI networking, and Q3 AI semis guided to $16.0B, over 200% YoY.

Adjusted EBITDA 69% of revenue. Stock off about 2.7% AH, so the bar was set high into the print.

The insatiable need for AI connectivity and custom compute continues.

Will be monitoring the call. That’s where the action is.

1

2

25

7,177

Jun 3

I take this with a grain of salt.

The finalized vendor roster consists exclusively of Mitsui Mining and Co-tech..

[Exclusive] Lotte Energy Materials to Supply AI Circuit Foil to NVIDIA Starting This Month

Lotte Energy Materials will begin supplying AI circuit foil used in NVIDIA's next generation graphics processing units (GPUs) in earnest starting this month. The company had originally planned to begin supply in the second half of this year, but moved up the timeline at NVIDIA's request. In preparation for an aggressive capacity buildout, Lotte Energy Materials is understood to have recently placed a bulk order with a partner for more than ten times its previous volume of copper.

According to industry sources on the 1st, Lotte Energy Materials will begin full scale shipments of AI circuit foil from its Iksan plant in North Jeolla Province this month. Circuit foil is an ultra thin metal sheet one twentieth the thickness of A4 paper. It is a foundational material used when AI accelerators process large volumes of data, and its supply price is more than three to four times higher than that of ordinary copper foil for electric vehicle batteries. Having designated AI circuit foil as its next growth driver, Lotte Energy Materials has converted the Iksan plant, which previously produced copper foil for EV batteries, into an AI circuit foil production line.

Once Lotte Energy Materials produces the circuit foil, Doosan Electro Materials BG manufactures the copper clad laminate (CCL) based on it, and Isu Petasys produces the printed circuit board (PCB), which is ultimately supplied to NVIDIA. Both companies will ramp up supply to NVIDIA this month.

Lotte Energy Materials is reducing the share of its core EV copper foil business and shifting its center of gravity toward AI circuit foil. It is currently producing circuit foil using part of the Iksan plant's production line, but next year it will transform the entire Iksan plant into a dedicated AI circuit foil production base. The company plans to increase capacity from 3,700 tons this year to 16,000 tons next year, and to add further production lines after 2028.

The high barriers to entry in the AI circuit foil market are another positive factor. Globally, the only players capable of mass producing AI circuit foil are Japan's Mitsui Mining & Smelting, and Korea's Lotte Energy Materials and Solus Advanced Materials. The frontrunner, Mitsui, has been unable to keep up with explosive demand due to a recently stalled expansion schedule, while Solus Advanced Materials has sold off the relevant subsidiary. An industry official said, "AI circuit foil requires highly advanced rolling technology, so it is difficult to convert a line in a short period of time," adding that "this is effectively an opportunity for Lotte to seize leadership of the market."

The market views this as the Lotte Group, which had been sidelined during the AI boom, making a full fledged entry into the NVIDIA value chain. On the day, Lotte Energy Materials closed at 64,300 won, up 14.62% from the previous trading session.

2

1

25

11,239

Jun 2

Humufish~

Looking ahead, next-generation motherboards will adopt high-layer-count HDI technology, while the required IC substrate surface area will swell to three times its current footprint.

MediaTek at Goldman Sachs Taiwan Day:

“The next-generation program is adopting only EMIB-T, with tape-out targeted for 4Q26 and mass production by 4Q27.”

This is significantly different from what Taiwanese media had reported — that the next-generation program would use both CoWoS and EMIB-T in parallel.

$INTC

2

1

45

43,507

Jun 1

The deployment of PTFE materials is currently confined strictly to exploratory testing and is highly unlikely to achieve commercial adoption in mass production. Investors should entirely disregard the market noise surrounding PTFE, as the clear, non-negotiable mainstream roadmap remains anchored exclusively by M9Q and M10Q materials.

Jun 1

Abstract of Our PCB Note -> PTFE Likely Chosen for Nvidia Kyber Midplane ✅

Key Highlights:

•PTFE likely be selected over M9 Q glass for superior high-frequency performance & lower signal loss

•PTFE supports 337G SerDes requirements

•PTFE has solved past rigidity/drillability issues

Market Impact:

•PTFE CCL market projected to hit RMB 8bn in 2027 for Kyber

•Further ramp expected in Feynman platform

•Mass production likely starts late 2026 due to manufacturing complexity

Stock Beneficiaries:

•Shengyi Tech (600183 CH)

•TPE 台虹 (8039 TT)

•Upstream: Dongyue Group (0189 HK) — main PTFE supplier to Shengyi

•Others: Daikin (6367 JP), Haohua Chemical (600378 CH)

Solid long-term tailwind for PTFE supply chain.

#NVDA #Kyber #Midplane #正交

5

9

64

24,536

kokycpcb retweeted

May 29

What's happening in the MLCC market

First off, MLCC as a whole is a $15B market. MLCCs for servers were a $1.3B market in 2025 ($600m for AI servers, $700m for general servers)

The AI server MLCC market is growing at 80% CAGR, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR)

We will see negative growth in the smartphone/mobile MLCC market for at least 2026-27.

Humanoids are another future high-growth market for MLCCs

Book-to-bill ratio for most MLCC suppliers is over 1 now

Reasons for price hikes-

High Nickel & Silver are affecting all segments

There is a supply-demand mismatch in the high-end (high capacitance, high voltage) segment, which is used in autos & servers

High-end MLCC lead time is over 20 weeks

Spot/distributor prices have increased by 20%-40% for low capacitance & consumer device MLCCs due to hoarding and double booking, especially in China

OEM contracts have not seen large price hikes yet

What's happening now:

Rapid capacity expansion happening across the industry

Murata expects blended ASP prices to remain flat (ASP going down in consumer electronics, expansion in AI server market)

Tier 1 players like Murata, Taiyo Yuden, SEMCO building capacity to serve AI server MLCC market

This will create opportunities for Tier 2/3 and Chinese suppliers to expand in the mid to low end market (Macronix effect)

Future:

MLCC production equiment & raw materials suppliers will be the biggest beneficiary of this CAPEX boom

MLCC producer stocks have performed well, and it is finally spilling to raw material/equipment producers

I expect them to outperform MLCC producers now

30

249

1,491

573,108

May 27

Clients ask about the glass fabric situation constantly. To be frank, we have already laid out the core thesis in our previous notes—the macro trend remains unchanged. A major driver behind the current waves of CCL and PCB price hikes is the rigid cost-push from fabric suppliers. High-end glass fabric has been marking monthly price increases, with low-end grades racking up YTD gains of over 50%. On the high-end spectrum, except for Low-DK Gen 1 which remains relatively stable, Gen 2 and T-glass are all undergoing continuous price adjustments.

Simply put, without the soaring cost of glass fabric, CCL makers wouldn't even have a solid foundation to justify their own price hikes. Without fabric, downstream players can forget about hitting their revenue targets. In fact, certain PCB applications are already facing severe material blindness. Those in the market claiming there is 'no shortage' are simply too disconnected from the actual supply chain reality.

5

14

201

140,032

May 27

It is highly common for TWSE/TPEx-listed companies in Taiwan to pass private placement resolutions annually at their annual general meetings (AGMs) as a routine measure.

9

2,690

kokycpcb retweeted

May 26

MLCCs had a generational run

Feb 6

Btw, Vishay Intertechnology (VSH) has exposure to high-current inductors and tantalum/polymer capacitors

Both those components are experiencing a shortage due to AI DC demand

VPG was spun out from VSH in 2010

6

11

240

50,909

May 24

While Nittobo is undeniably the global leader in conventional electronic-grade glass fabric, its market share in the Low-DK Gen 2 segment is far less dominant than the consensus assumes, driven by the following structural factors:

1. Client Alignment: Nittobo’s primary Copper Clad Laminate (CCL) clients are concentrated among Doosan, Panasonic, and TUC.

2. Supply Chain Disconnect: The leading suppliers for the dominant GPU camps are currently Doosan, Shengyi Technology , and EMC , while the ASIC camps are primarily anchored by EMC, Panasonic, and TUC. Crucially, EMC, which commands the industry's largest capacity, is not a primary customer of Nittobo. Meanwhile, Shengyi Technology relies heavily on CPIC .

3. Upstream Yarn Sourcing Dynamics: In the transition to Low-DK Gen 2, Nittobo does not supply its premium glass yarn to independent weavers like Asahi Kasei. Consequently, other weavers must source their yarn from the US, Taiwan, and China. This is significant because Asahi remains a critical, foundational supplier to EMC.

4. Penetration Bottlenecks for NER and NEZ: The adoption and market penetration of Nittobo’s next-gen NER and NEZ products are fundamentally tied to the market share trajectories of Doosan, Panasonic, and TUC. However, the current reality is that the tier-1 CCL vendors holding the largest capacity and highest market shares are simply not deploying Nittobo’s solutions.

Market Perspective on Pricing Power:Recently, I have been asked why my stance on Nittobo’s pricing leverage is so conservative. To clarify: while Nittobo can easily initiate price hikes in the Low-CTE segment where it holds undisputed dominance, it has no solid foundation to command price increases in the Low-DK Gen 2 market, simply because its core downstream customers lack the market share dominance to pass those costs along

2

3

44

312,602

May 21

視頻 衍伸更多的算力需求

關注TPU體系

下周博通盈餘會議 /6月Computex前不斷接力演出

May 21

圆满结束了!

Google I/O 2026 第一天的活动已落下帷幕,精彩绝伦。

10 个你必须知道的震撼发布:

1. Nano Banana 视频生成功能,由 Gemini Omni 驱动

1

4

2,692

May 21

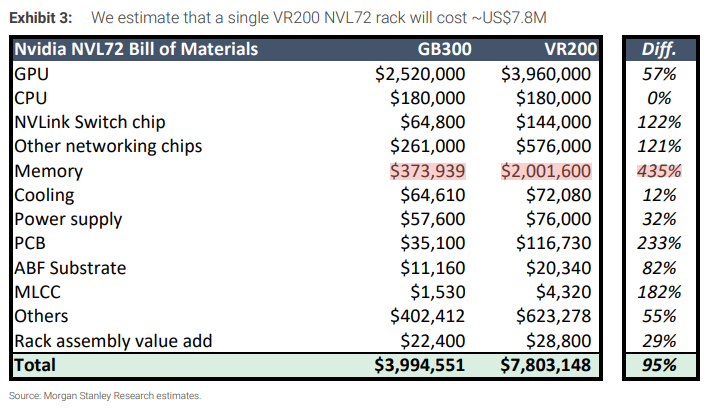

Based on Morgan Stanley’s BOM analysis for Rubin, the most bottlenecked segments of the supply chain are clearly visible. In an environment marked by persistent price hikes, these specific components represent both the highest cost share and the largest price increases across the entire bill of materials.

Perhaps the true focus of the tech giants visiting Taiwan for this year's Computex will pivot toward a few of these critical supply chain bottlenecks.

16

1,557

May 21

看看A股...看看台灣

這種漲幅 這種E-glass等級缺貨

毛利率是可以期待媲美高階布了~

台股趨勢股是很累人的~ 因為會有各種半路出家的替這些電子布安上各種替代鬼故事去打壓股價

玻璃基板很好未來技術有夢,但不解決現實,拿還沒出現的應用來講真的是考驗智商

#遠水救不了近火

4

2,338