Joined December 2007

- Tweets 20,082

- Following 3,662

- Followers 17,564

- Likes 15,605

779 Photos and videos

Pinned Tweet

21 Oct 2025

Shared some recent thoughts with @drnovac for his excellent @sundaycet newsletter:

sundaycet.beehiiv.com/p/inse…

6

3

14

2,768

Jun 12

I emailed legal to include.

Jun 11

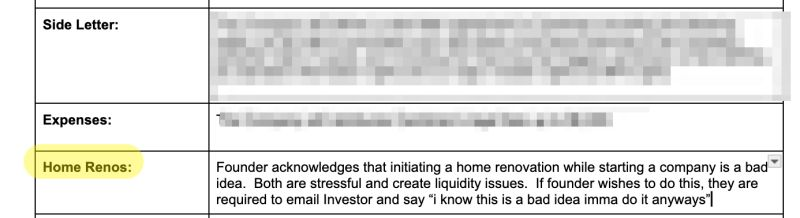

my biggest value as a VC is this clause in my standard TS. iykyk.

1

274

🤗

Jun 8

Exciting news to kick off London Tech week: Londoners can now sign up to experience @wayve_ai autonomous rides on @Uber which are launching soon (pending final regulatory approval). 🇬🇧

Join our interest list today: uber.com/gb/en/autonomous/wa…

1

857

Going to Super Venture in Berlin Next week? Got an open Wednesday night?

If you want a very fun evening with people & not companies; are ready to commit & not bail; leave the suit & promise to put on your dancing shoes… DM, text, email, etc.

Very limited in size for extra fun.

7

1

28

4,039

95% sure this is across the street from the nicest office in Berlin.

2

28

19,591

Deutschland hat echt eine weirde Beziehung mit der Vergangenheit...

Keinen Nazi in der Familie gefunden? Hier sind 5 Wege, auf denen Sie noch ein wenig mehr Schuldgefühle aufbauen können.

(Ist natürlich für Nachbarn und Kollegen, nicht für die eigene Familie...)

4

502

May 29

Really thoughtful way of analysing AI’s invisible economic output.

We all know it’s there.

May 29

AI Dark Output: The Visible Cost of Invisible Output

Why AI's increasing output is going to be one of the hardest economic measurement problems in history.

AI "Dark Output" could end up being the majority of economic activity, but a challenge to measure.

newsletter.semianalysis.com/…

2

2

426

May 29

Elite hardware founder tweet.

May 29

Asking for a friend: How to reset my environment in the real world? (pic for inspiration)

3

292

May 29

American houses are so unfair. Like, you can just cut through your roof and put a window in...

2

2

780

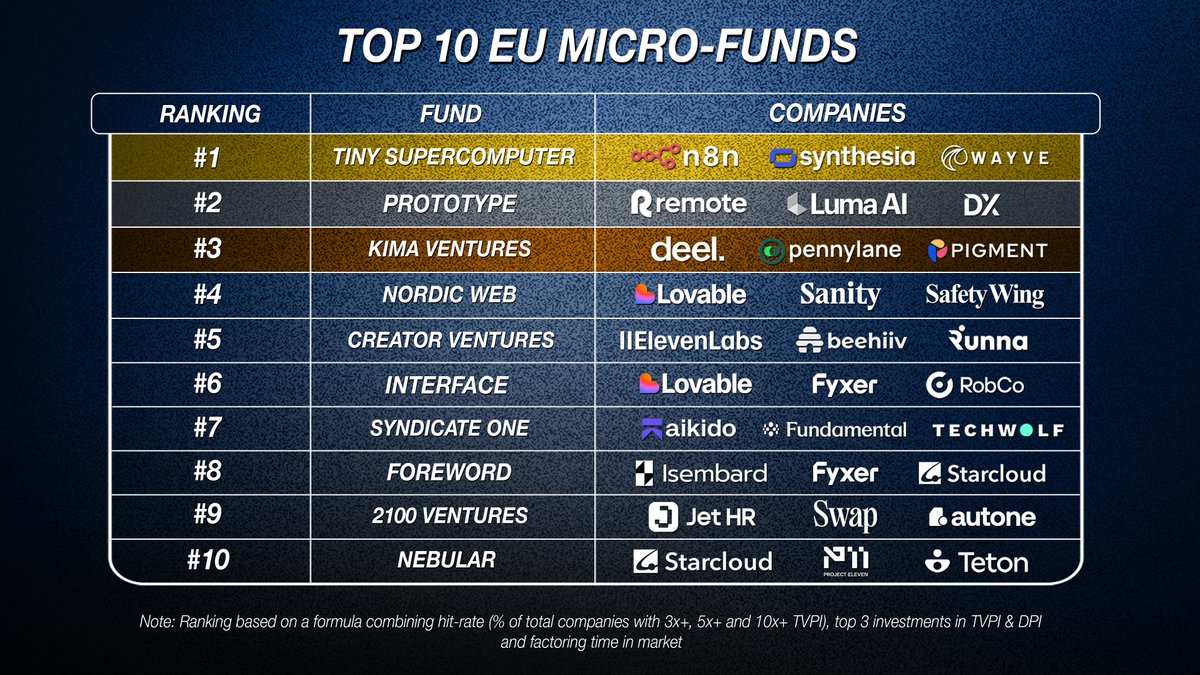

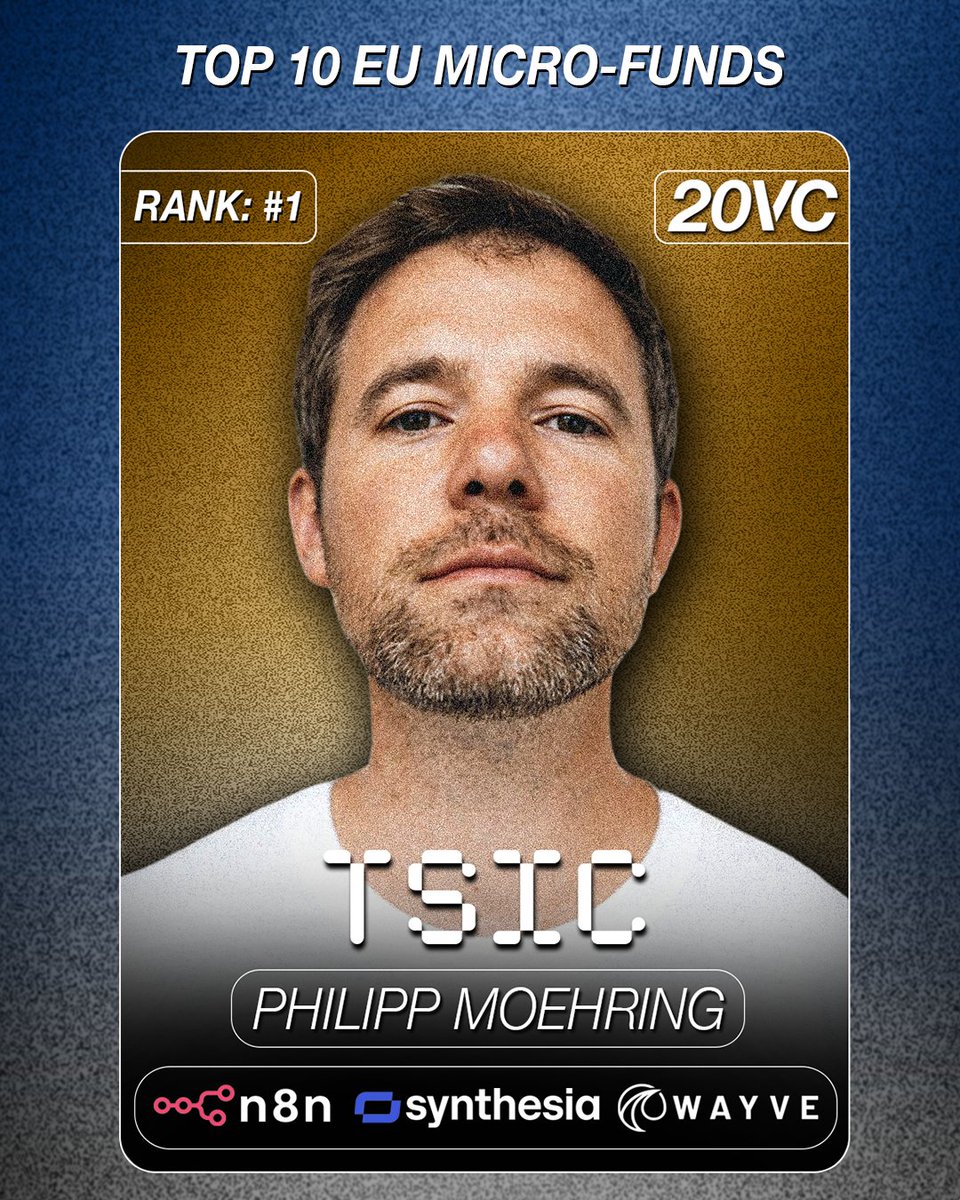

Philipp Moehring - tiny.vc retweeted

May 29

Today we’re launching @wayve_ai Labs, dedicated to advancing frontier Embodied AI and accelerating the path to general-purpose intelligence in the physical world.

Nearly a decade ago, Wayve was founded on a contrarian conviction: AI would have its greatest impact when it could perceive, reason and act in the real world. Since then, we’ve pioneered many of our field’s key breakthroughs: the first world model for driving (2018), video generative models for simulation (2022), and vision-language-action models for embodied reasoning (2023).

Over the past decade, we’ve built an organization which brings together the global scale of automotive talent with frontier AI science. Wayve is the best place to work on frontier Embodied AI science, while seeing your work deployed in mass production in the physical world. At Wayve, idea -> global deployment is measured in hours.

Now, our commercial progress enables us to increase our ambition even further. We want to create the best environment for Embodied AI research. Wayve Labs combines global-scale driving data, real-world deployment, and frontier-scale compute to create a uniquely powerful environment for Embodied AI research.

6

13

128

21,303

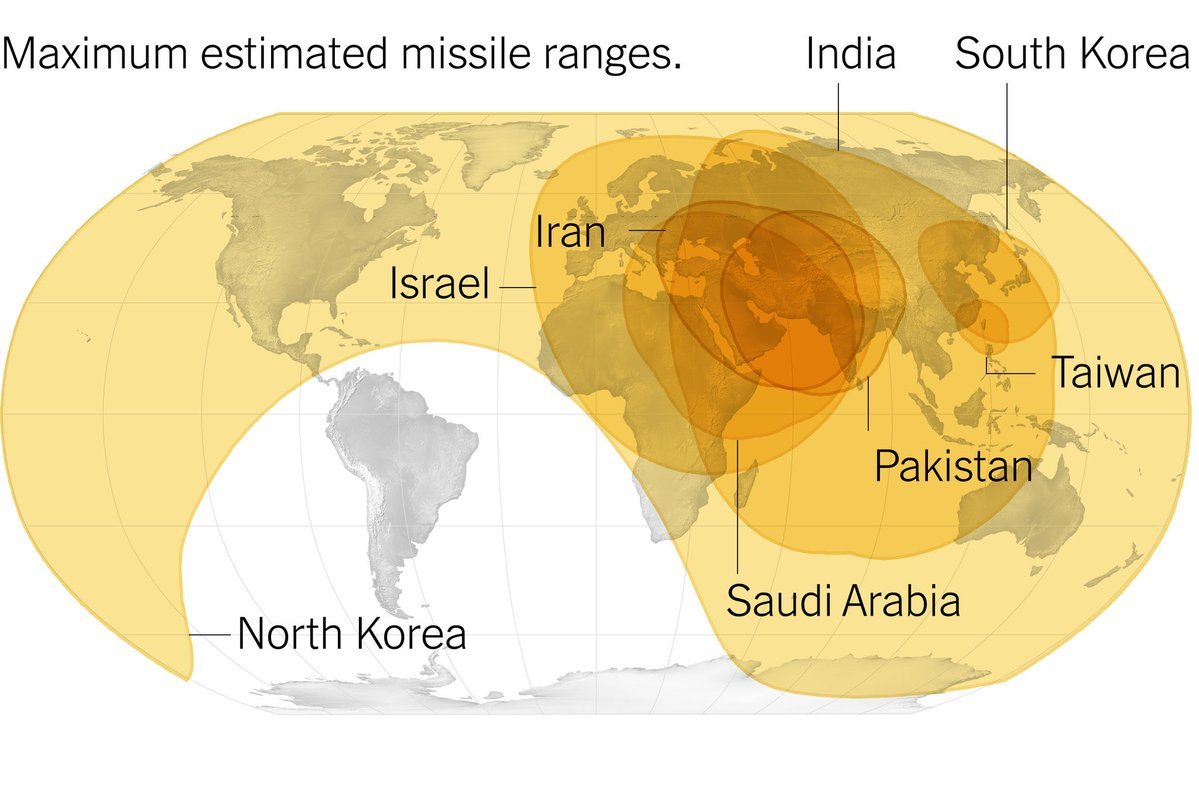

May 29

Missile ranges matter, but so does fallout - Argentina wins. Here's a fun book about a non fun topic (nuclear fallout): goodreads.com/book/show/3818…

1

135

Philipp Moehring - tiny.vc retweeted

May 28

I’m incredibly grateful to have learned from Ron during my years at @svangel. I wrote a short note reflecting on a few lessons from him that I believe are increasingly important in today’s startup ecosystem: ronconway.carrd.co

We are all behind you, @RonConway.

Apr 18

I want to share some difficult news. I was recently diagnosed with a rare form of cancer and I want you to hear it directly from me.

Treatment is starting immediately and will include multiple strategies over the course of about a year. While I will be stepping back from some of my usual activities, I will continue to support SV Angel founders, who I love with a passion.

SV Angel remains unchanged. Topher has made all of our investment decisions for the better part of the last decade, and Ronny joined as Managing Partner in 2024. They bring experience from nearly every major technology cycle in Silicon Valley and are now focused on partnering with founders building the future of AI. SV Angel has a deep, experienced team that remains fully focused on supporting exceptional founders.

With a more focused and balanced schedule, I can prioritize treatments while helping SV Angel founders at inflection points like we always do!

I’ve chosen not to share the specific type of cancer since I don't want speculation about my prognosis. I appreciate your understanding and respect for this.

I am optimistic about my prognosis. I am fortunate to have the best/amazing team of UCSF doctors in San Francisco, and as you know, I never back down from a fight.

Thank you for your support, it means a great deal to me.

4

2

41

10,901

May 21

This is probably a great deal for YC companies, and definitely a great group to lock in for OAI.

May 20

Sam Altman makes ‘mic drop’ offer to every Y Combinator startup techcrunch.com/2026/05/20/sa…

2

3,065

Philipp Moehring - tiny.vc retweeted

May 21

Adding to the Tesla/Rivian/Lucid example described below, another interesting data point:

Of the top 10 US companies by secondary market demand, SpaceX and Neuralink have the most conservative funding trajectory.

A 24-year-old company launching huge rockets into space (and catching them) has raised significantly less per year than a payment processor and an enterprise data platform.

A 10-year-old company building brain-computer interfaces that are helping manage serious disabilities has raised less per year than two gambling platforms.

There is a lesson here about the way Musk approaches financing his companies.

May 20

"Because funds have become larger in real dollar terms, many venture capital organizations have invested larger amounts of money in each portfolio company. Firms have attempted to do this in two ways. First, there has been a movement to finance later-stage companies that can accept larger blocks of financing. Second, venture firms are syndicating less. This leads to greater competition for making later-stage investments.”

The Venture Capital Revolution, by Paul Gompers and Josh Lerner

The pathology of venture capital is not hard to unravel.

The market expanded, with more capital chasing deals, creating larger and later investments. Companies now stay private longer, and more future growth is priced into each financing event.

The metrics to attract investment in private markets are revenue, growth rate and gross margins.

As companies raise more private capital, they spend longer focusing on these metrics. This mirrors what what Startup Genome described as "premature scaling", where a company overdevelops along one dimension, at a cost to others.

Indeed, revenue, growth and gross margins do not provide a full picture of company health. As implied by 'Goodhart's Law', as these metrics became a target they can mask a deeper financial malaise.

Imagine, for example, if the NBA understood a good basketball player purely by how tall they were and how fast they ran. The league would be packed with frenetic 7-foot-tall monsters and a terrible quality of play.

As a result, companies with an extended life in private markets become structurally and almost inevitably overvalued. While investors can protect against this with additional terms, to an extent, those terms do not extend to common stock holders.

“Reported unicorn post-money valuations average 48% above fair value, with 14 being more than 100% above. [...] Common shares lack all such protections and are 56% overvalued.”

Squaring Venture Capital Valuations with Reality, by Will Gornall and Ilya Strebulaev

As a result, venture backed companies (particularly those that have raised the most) now struggle to find a profitable exit.

Exits are where rubber hits the road. It's where venture marks, which are notoriously unreliable, suddenly have to match up with real-world expectations. This is especially difficult in hot markets or hot categories.

"We show that an increase in the supply of venture capital (VC) leads to a decline in the quality of firms going public. ... both post-IPO operating profits and post-IPO sales growth are lower when the supply of VC capital is high."

The Rise of Venture Capital and IPO Quality, by Amrita Nain, Jie Ying and Joseph Arthur

This structural overvaluation makes venture-backed companies less appealing targets for acquisition, but it's harder to see the consequence of that beyond sluggish M&A.

Where it's more obvious is in IPOs, where not only are there fewer public offerings but those companies also more obviously struggle once public thanks to the visibility on their share price.

A substantial post-lockup dip is now a feature of most venture-backed IPOs, and where companies have raised multiple billions that dip lasts longer and is increasingly negative.

“Our results do indicate that the deregulation of private markets has played a significant role in bringing about a new equilibrium where fewer high-growth startups go public. Importantly, our results strongly point to the fact that this new equilibrium has not come about by some unfortunate freeze of the IPO market.”

The Deregulation of the Private Equity Markets and the Decline in IPOs, by Michael Ewens and Joan Farre-Mensa

For context, of the 10 US-listed companies that raised more than $3B in venture capital, 8 were negative at lockup expiry and the group has a market adjusted performance of -63%.

And it's completely unnecessary, even for capital-intensive companies. Tesla raised $105 million prior to its IPO, compared to $10.6 billion for Rivian and $3.4 billion for Lucid.

Only one of those companies is clearly a winner today, generating a vastly greater sum of economic value. The other two, however, enabled much greater fee income for their investors.

This explains why some venture firms have responded to this new reality by specifically backing the 'tallest and fastest basketball players', and benefitting from the ease of herding capital into that category. The volume of capital raised is their main metric of success, with scale and predictability are their product on which they charge fees.

Others investors, particularly those with LPs that care about distributions, need to think more carefully about how they steward investments to an exit. That means being conservative with capital and ensuring companies properly develop along all dimensions.

That also neatly aligns with the original description of venture capital, provided by Gompers and Lerner in their 2001 paper, "providing capital to firms that might otherwise have difficulty attracting financing."

If a company can easily raise capital on generous terms, then it's definitionally not a venture investment and is unlikely to produce the required returns.

The only question is, do you care about the returns?

1

14

2,384

May 21

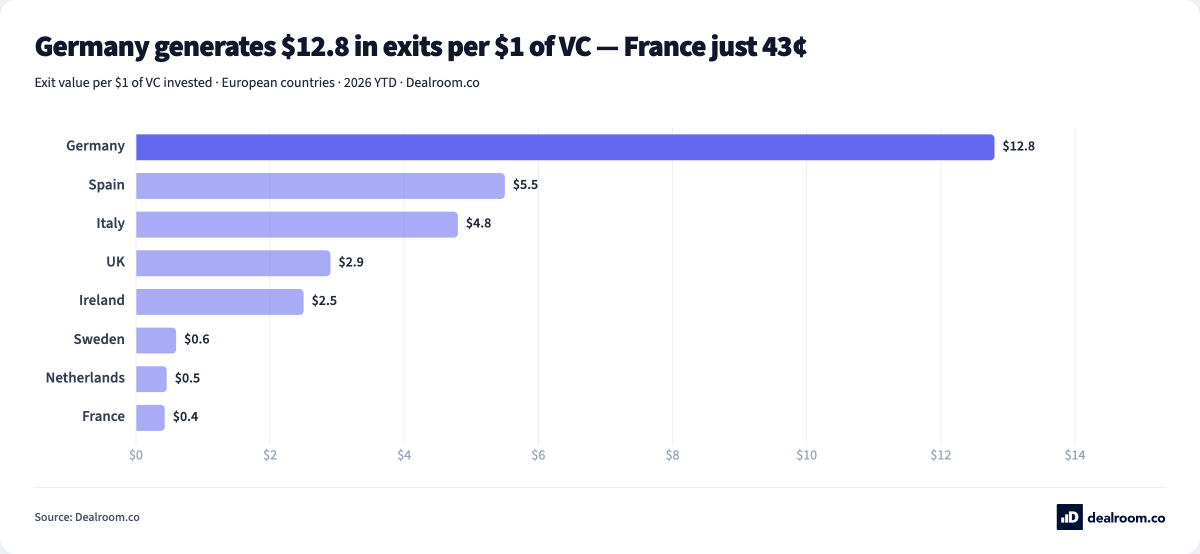

That's German Efficiency, ya know.

May 20

🇩🇪 Germany: $3.6B VC in 2026 → $46B in exits. That's $12.8 per dollar.

🇫🇷 France: $4.2B VC → just $1.8B in exits. 43¢ per dollar.

The UK raised 4× more VC than Germany — and still generated less exit value.

📊 app.dealroom.co/curated-heat… @dealroomco

7

14

263

66,656

Philipp Moehring - tiny.vc retweeted

May 19

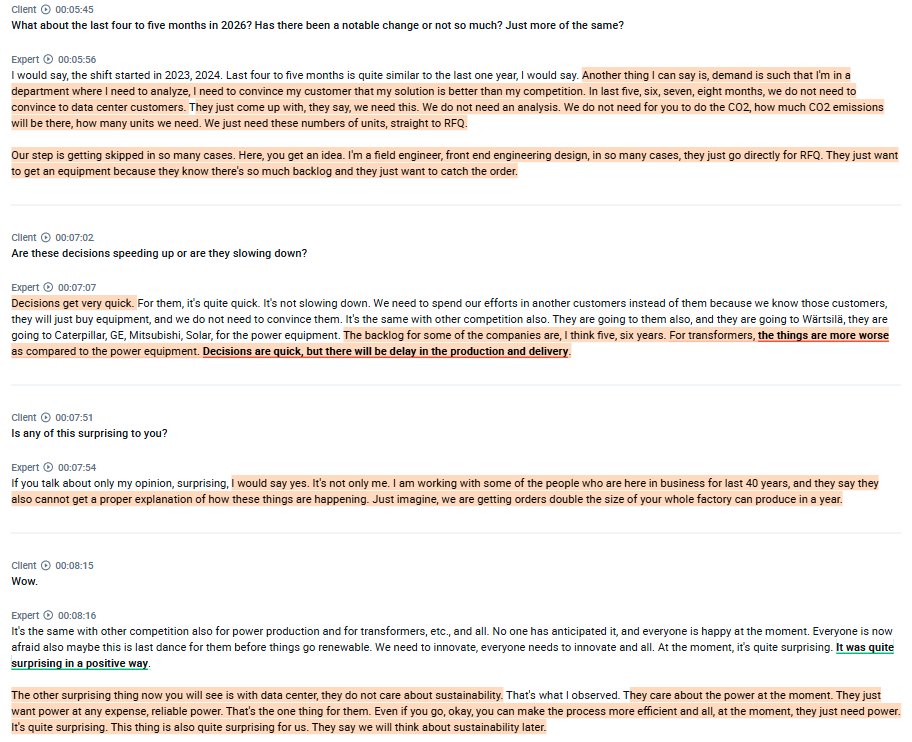

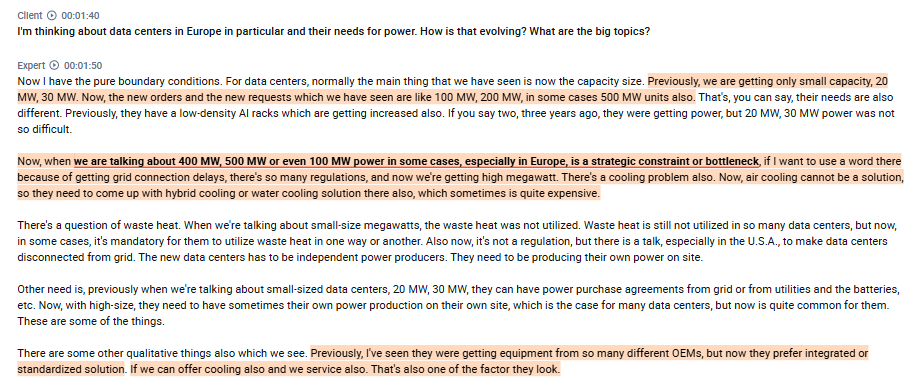

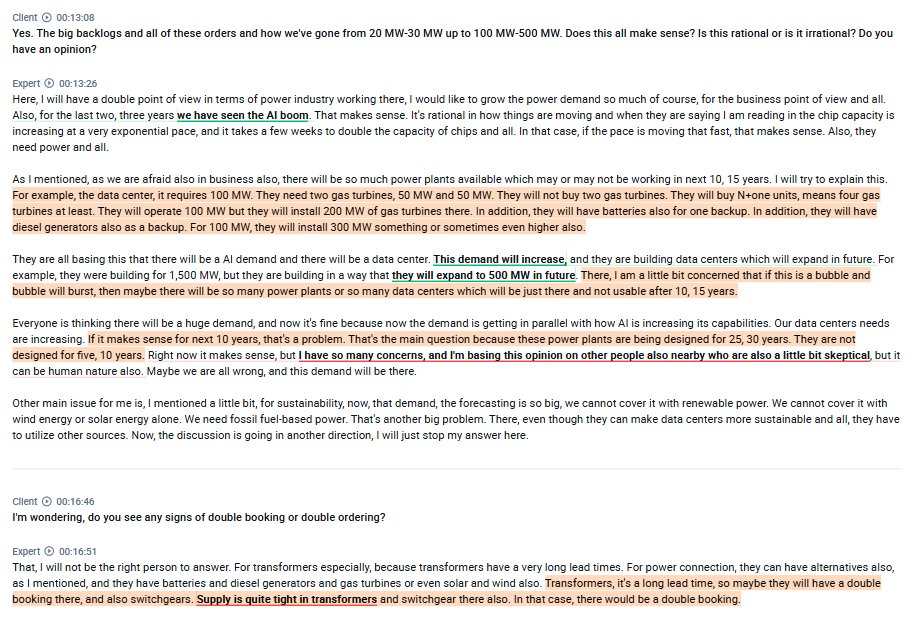

A MUST-read interview with a Siemens employee explaining just how high demand is for energy equipment right now because of AI:

1. The whole situation is shocking even for people who have been in the business for 40 years. They are getting orders that are double the size of what their entire factory can produce in a year.

2. Demand is so high in the last 5-8 months that they don't need to convince or send any analysis (such as CO2 emissions, etc.) to clients because they just want the equipment, because there's so much backlog that they just want to catch the order.

3. Decisions are being made very quickly by clients; the backlog for some of the energy equipment companies is 5-6 years. For transformers, the situation is even more difficult.

4. He mentions that right now, data center builders do not care about sustainability; they just want power at any expense, reliable power. They say they will think about sustainability later.

5. The orders have gone from previous 20-30 MW orders to now 200-500 MW units. Customers have previously wanted to get equipment from different OEMs, but now they prefer an integrated standardized solution.

6. An interesting dynamic is that even though the data center requires 100 MW, the builders are buying N 1 units of gas turbines (so more than just for 100 MW) as backups, as well as having more energy capacity, as they believe they will continue to grow that data center.

7. He does believe there is some double booking going on on transformers and switchgears because of extra-long lead times.

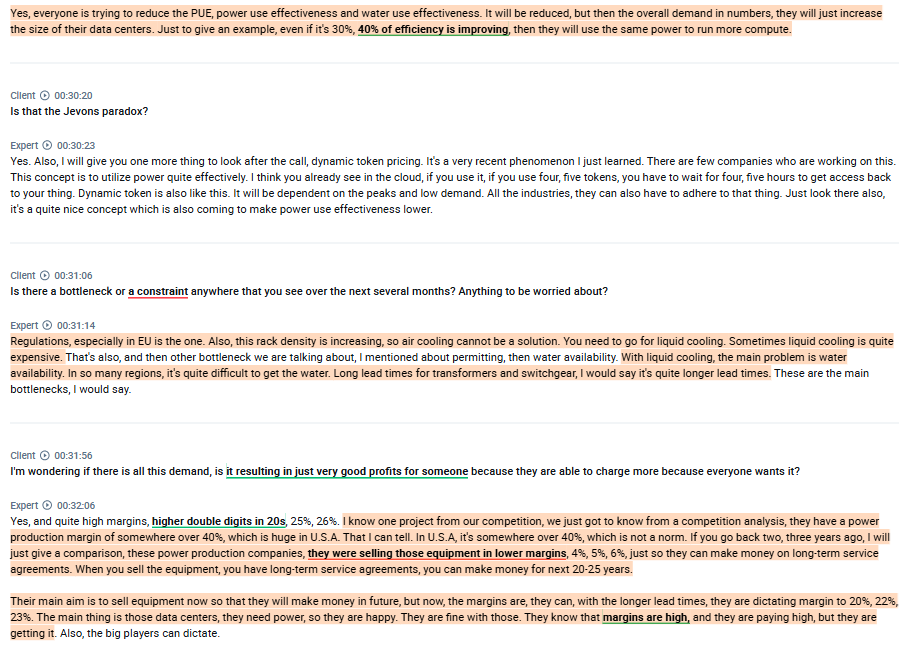

8. Everyone is trying to reduce PUE, and water use effectiveness, but even after improving, they just use the same power to run more compute.

9. The problem is also liquid cooling, as it is expensive, and water availability in many regions is a problem.

10. Margins on equipment in the sector have gone from 4-6%, where they were 2-3 years ago, to 20-23% and in some cases even 40%. The data center builders know the margins are high, but they are fine with it because they just want to get it.

found on @AlphaSenseInc

86

728

3,856

597,839

Philipp Moehring - tiny.vc retweeted

May 12

HOT DAMN - @n8n_io has just been valued at $5.2bn in secondary sale led by SAP.

It's double what it was valued in October.

The company is now doing over €100m ARR

As part of the investment SAP is also signing a multiyear deal to embed n8n’s tools inside its AI agent builder, Joule Studio.

Amazing news - Europe is COOKING

7

8

99

12,431

If you don’t start weird, you better be incredibly excellent on the most commonly valued things.

That means you compete with the whole world. Good luck.

mature things tend to get pressured into being less weird over time, so if you're starting from scratch your advantage is that you can be very weird

if you don't start weird you're probably trying to compete inside the local maximum of something more boring than you could be

3

298

I didn’t even realise the missing cars but the quiet streets were great.

Also a hug reason for Tokyo not being super bright at night - which was another welcome difference.

i think not having cars parked literally everywhere is like 75% of the reason why Tokyo (and probably japan in general) looks so nice

4

626

Apr 30

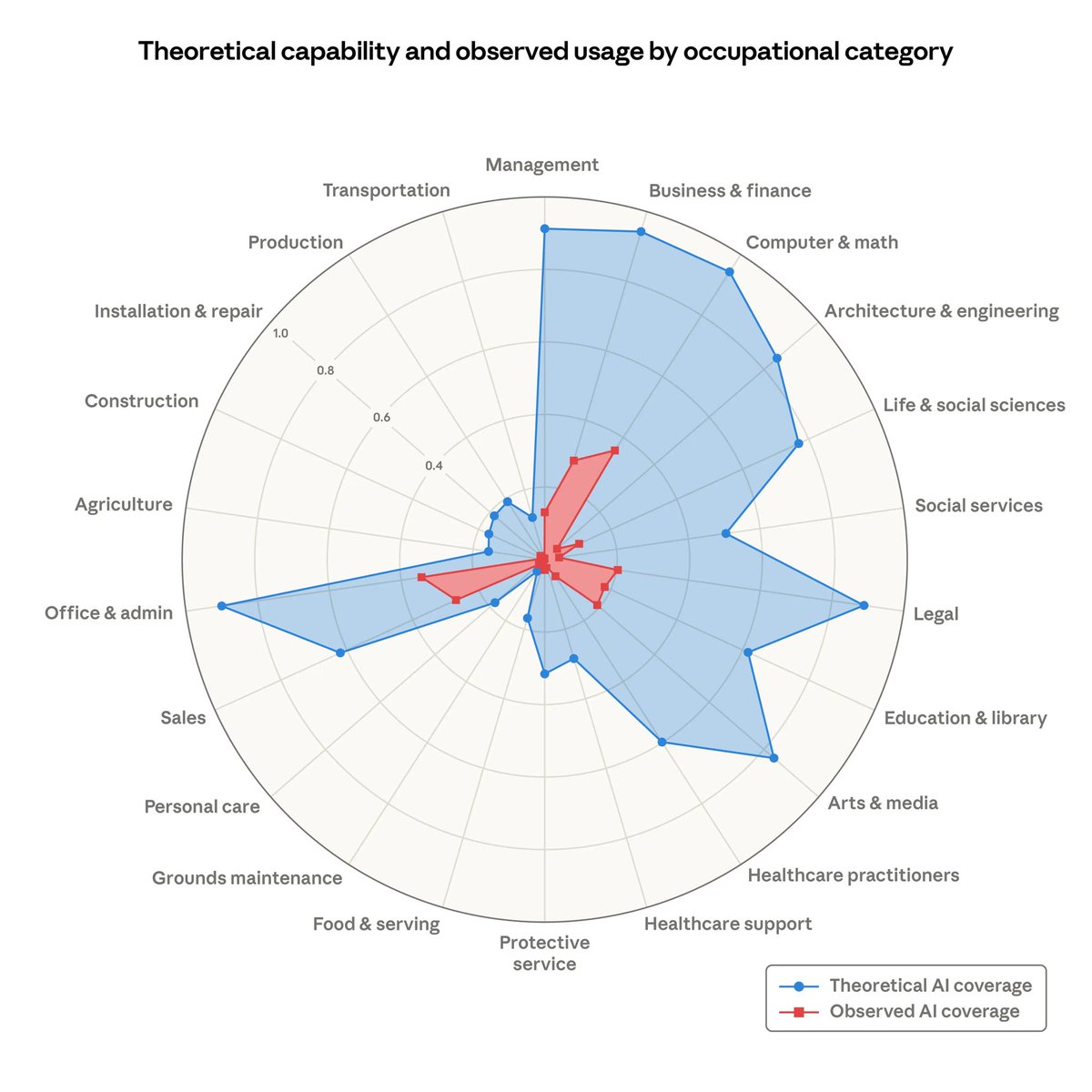

It is bonkers that one of the major technology companies of our time publishes research in which they try to understand… what their product does?

H/t @pkedrosky (who everyone should read).

anthropic.com/research/claud…

3

1

429