Joined July 2009

- Tweets 66,495

- Following 18,785

- Followers 17,099

- Likes 29,306

3,664 Photos and videos

Pinned Tweet

Feb 15

Can there be a balanced techno-political vision embracing #AI, #IoT, #6G (as we can not go back) harnessed in an architecture that uses value and profits for all actors?

Yes.

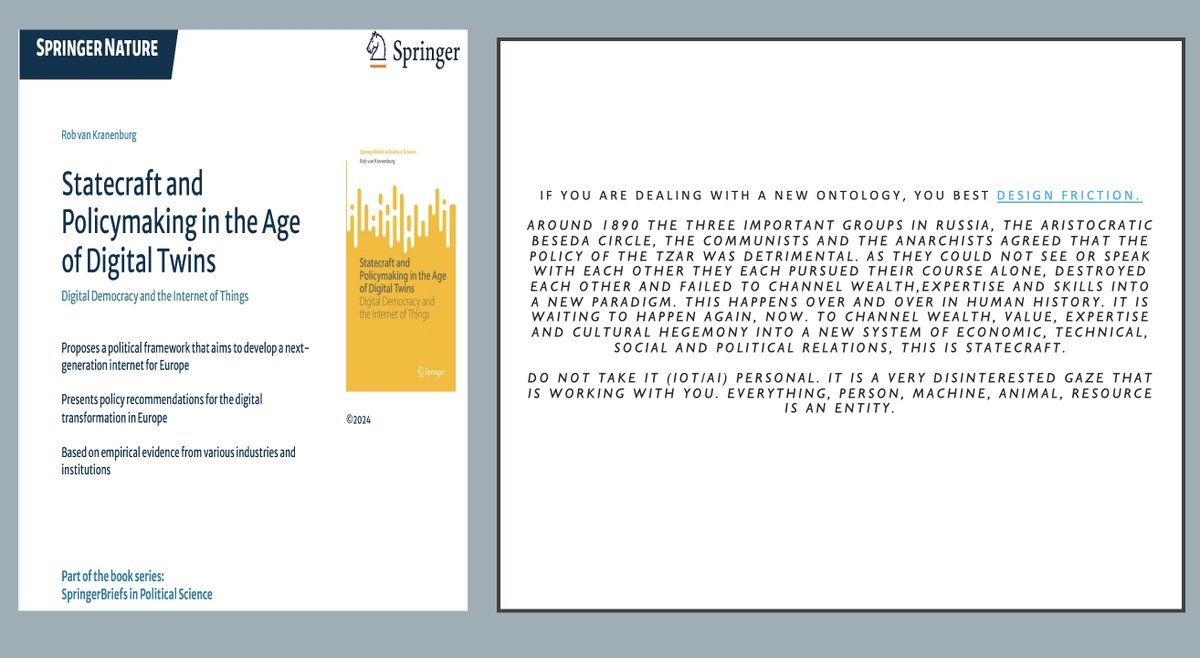

My book describes the transition from basic automation to pervasive computing, ubiquitous computing, ambient intelligence, and the Internet of Things, and its effects on democratic decision-making and governance in Europe. It diagnoses a lack of political agency and technical capabilities in the West that has accelerated the end of the model of entrepreneurial government in favor of a new paradigm: Cyber-physical Systems. Offering an analysis of the digital transformation process in various industries and institutions, the book highlights the severe repercussions and impacts on democratic decision-making and the legitimacy of the Westphalian model of the nation-state. Readers will learn how the convergence of cloud systems, data platforms, and connected objects is facilitating this transformation process, one characterized by a virtual representation of every person, object, and machine – a digital twin.

The book argues for balancing centralization and decentralization in a cybernetic framework with human-centric values at its core. Further, it proposes a political framework that aims to develop a next-generation internet for the five hundred million citizens of Europe, one capable of enforcing and promoting digital hegemony while safeguarding the rights and proactive capabilities of said citizens. In closing, the book makes the case for a (6G) phone/hardware wallet built on European chip requirements and platforms and running on its own OS to promote technical European integration on infrastructure, applications, and services.

Given its scope, the book will appeal to policymakers and practitioners interested in European digital governance and autonomy, as well as scholars of public administration, public policy, and political science.

link.springer.com/book/10.10…

@ERC_Research @InteroperableEU @EU_DIGIT @PubAffairsEU @DigitalTDaily @WuxiCity @iotforall @IotMore @Exoconscious @Eli_Krumova @6Gflagship @6G_Reference @IIoT_World @BRICSinfo @6G_SNS @CIOTechTalk @IIPP_UCL @arstechnica

1

6

822

Rob van Kranenburg retweeted

The U.S. order to suspend foreigners' access to Anthropic's latest models is a stark reminder for Europe that it's heavily reliant on American AI models — and that the window to change that is closing.

politico.eu/article/us-anthr…

6

25

61

6,066

Rob van Kranenburg retweeted

>>> Objective: To explore how large pharmaceutical corporations may integrate emerging decentralized technologies—such as blockchain and DAOs—within their merger, acquisition, and partnership frameworks, and how these strategies intersect with broader innovation and external sourcing models.

doi.org/10.30953/bhty.v9.435

#Blockchain #fintech #Mergersandacquisitions #healthinnovation #biopharma

>>> NEW ARTICLE - Decentralized technologies are more important now as pharma cos accelerate innovation, pipelines, and breakthroughs.

DOI doi.org/10.30953/bhty.v9.435

The paper explores how innovation, partnerships, licensing, and acquisition strategies are evolving in response to digital transformation.

Strategic implications for healthcare and life sciences leaders:

• Blending traditional acquisition digital infrastructure

• Decentralized frameworks can reshape preclinical scouting and collaboration pathways

• Competitive advantages bridging institutional rigor with technological agility

👉 Read the full article DOI doi.org/10.30953/bhty.v9.435

Lead Author

@SimoFantaccini , MD, MBA, PhD

#PharmaInnovation #Biopharma #DrugDevelopment #DigitalTransformation #BlockchainInHealthcare #DecentralizedHealth #HealthcareInnovation #LifeSciences #AIinHealthcare #Fintech @

1

2

35

Rob van Kranenburg retweeted

>>>NEW Research Blockchain-Enabled Electronic Health Record Model for Managing Patients Vital Data and Medical Reports | Blockchain in… blockchainhealthcaretoday.co…

#Thailand #India #engineering #blockchain #healthinnovation

>>>NEW Research

Blockchain-Enabled Electronic Health Record Model for Managing Patients Vital Data and Medical Reports | Blockchain in… blockchainhealthcaretoday.co…

#Blockchain, #electronichealthrecord, #HyperledgerFabric, #hyperledgerCaliper, #performanceevaluation, #remotepatientmonitoring @CMULibrary

1

2

53

Rob van Kranenburg retweeted

China has introduced strict new regulations for online influencers.

Under the new rules, content creators must possess a relevant university degree or professional certification before they can discuss specialized topics such as medicine, finance, education, law, or health. The policy, issued by the Cyberspace Administration of China, aims to curb misinformation and raise the overall quality of online content.

Influencers wishing to cover these subjects on platforms like Douyin, Weibo, and Bilibili are now required to submit proof of their qualifications. Platforms are responsible for verifying credentials and removing any non-compliant content.

Violators face significant penalties, including fines of up to 100,000 yuan (approximately $14,000), account suspension, or permanent bans.

While supporters view the measure as a necessary step to protect the public from misleading or harmful advice, critics argue that it could restrict free expression and limit diverse voices online.

The regulation reflects China’s broader effort to tighten control over digital content and establish higher standards of credibility in the influencer economy.

26

58

213

17,041

Rob van Kranenburg retweeted

Produced by BHTY Journal - ConV2X - focused on the infrastructure required to make technology work! FIRST SPEAKER COHORT ANNOUNCED

@harvardmed @FDA @AccreteAI @HarvardPilgrim

@MaynoothUni @nimbus @acoerco @Apeirion @Nethermind @bloqcube111 @armouredquantum #cureety @Rejuve_Bio

REGISTER NOW - seating is limited by design. 150 MAX. conv2xsymposium.com/why-atte…

Topics include:

- Agentic AI & Multi-Agent Healthcare Systems

- Healthcare Cybersecurity & Quantum Readiness

- Blockchain & Digital Trust

- Data Governance & Interoperability

- Regulatory Challenges & Opportunities

The Foundry

Cambridge, Massachusetts

September 24–25, 2026

Interested in sponsoring or exhibiting?

Contact Ramy Azzam, MD r.azzam@partnersindigitalhealth.com

#HealthcareAI #ArtificialIntelligence #LifeSciences #Cybersecurity #AgenticAI #DigitalTrust #HealthPolicy #QuantumComputing #Interoperability #EnterpriseAI #CambridgeMA

ConV2X - focusing on the infrastructure required to make technology work!

FIRST SPEAKER COHORT ANNOUNCED

What happens when leaders from some of the most innovative healthcare and decentralized technology companies come together in Cambridge?

You're about to find out...

Featured speakers include:

✔️ Himanshu Jain — Tech Innovation Leader

✔️Leo Anthony Celi — @harvardmed

✔️Ajaz Hussain — Former U.S. @FDA Deputy Director

✔️Francisco Curbera — @AccreteAI

✔️Nitin Gaur — @Nethermind

✔️Anjum Khurshid — @HarvardPilgrim Health Care Institute

✔️Martin Curley — @MaynoothUni

✔️Shawnna Hoffman — @ArmoredQuantum

✔️ Jose Bolanos — #Nimbus

✔️Jim Nasr — @acoerco

✔️Rama Rao — @bloqcube111

Stay tuned for many more leaders soon...

Topics include:

🔹 Agentic AI & Multi-Agent Healthcare Systems

🔹Enterprise AI Infrastructure

🔹Healthcare Cybersecurity & Quantum Readiness

🔹Blockchain & Digital Trust

🔹 Decentralized Health Platforms

🔹Data Governance & Interoperability

🔹Regulatory Challenges & Opportunities

The Future of Healthcare Technology Architecture

The Foundry | Cambridge, Massachusetts

September 24–25, 2026

👉 REGISTER NOW - seating is limited by design. 150 MAX.

conv2xsymposium.com/why-atte…

Interested in sponsoring or exhibiting?

Contact Ramy Azzam, MD

r.azzam@partnersindigitalhealth.com

#AIInfrastructure #HealthcareAI #ArtificialIntelligence #LifeSciences #Blockchain #Cybersecurity #AgenticAI #DigitalTrust #HealthPolicy #QuantumComputing #Interoperability #EnterpriseAI #CambridgeMA

1

1

28

Rob van Kranenburg retweeted

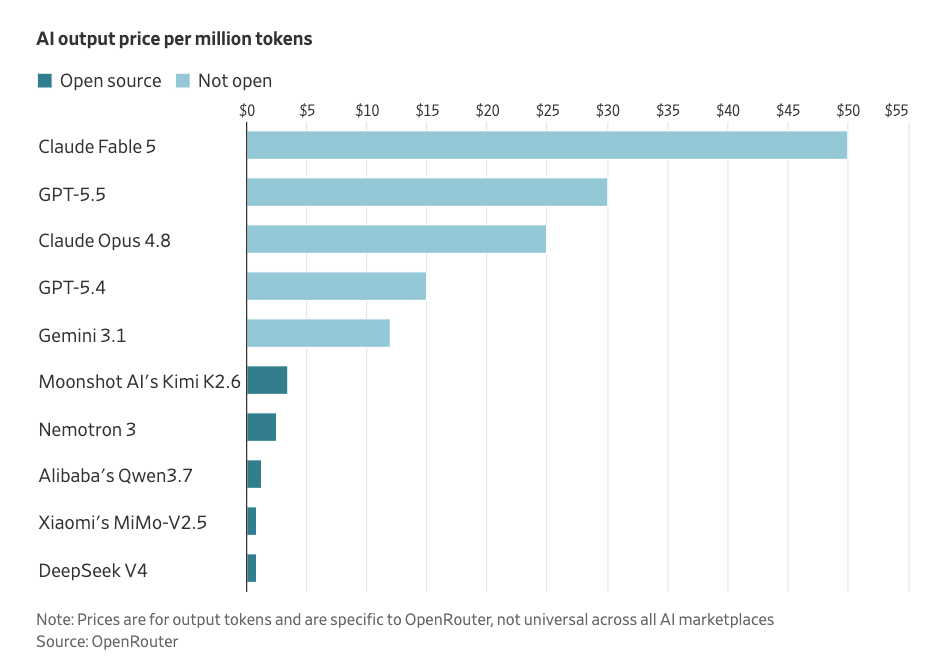

Chinese AI models went from a sliver to nearly half of token consumption on OpenRouter in about a year. "American startups are switching to Chinese models" is still overstated.

First the honest caveat, because it matters and most people sharing this chart skip it. This is OpenRouter data only. OpenRouter is a platform developers use to test and route between many models, and it's heavily self-selected. If you're using a US frontier model seriously, you usually go direct: Anthropic's API, OpenAI's API, AWS Bedrock, Google Vertex. You don't route it through OpenRouter. Meanwhile, a lot of people who want to use Chinese models specifically avoid the Chinese labs' own servers for privacy reasons, so they access them through OpenRouter instead. The result: this particular platform systematically undercounts US model usage and overcounts the Chinese share.

So the chart is not "half of all AI usage is now Chinese." It's "on the platform where people shop around between models, Chinese models have become a huge share."

A year ago, Chinese open-weight models barely registered even on OpenRouter. Now they're consumed at the scale of trillions of tokens per week. Developers are running real workloads (aka a lot of it coding) on DeepSeek, Qwen, Kimi, GLM, and the rest. The models got good enough, and cheap enough, that for many tasks the price-performance is impossible to ignore.

The US frontier labs mostly went closed and premium: best models, accessed through paid APIs, priced for the value they deliver. The Chinese labs largely went open-weight and cheap: release the weights, let anyone run them, compete on price. Open plus cheap drives adoption the same way a $200 LiDAR unit or a $299 home battery drives adoption. You commoditize the thing the incumbent is charging a premium for.

The core question stands: which layer captures the value? If frontier intelligence becomes a cheap, open, interchangeable commodity that developers route between based on price, that's wonderful for everyone building on top and brutal for anyone trying to earn a margin on the model itself.

It's the same dynamic as solar panels. The panels got so cheap that the money moved to installation, integration, and the systems built around them. If AI models follow that curve, the value moves up the stack to the products, the orchestration, the proprietary data and workflows.

One more note on the spike: part of the March 2026 surge was a Chinese model offered free for a period, which inflates the numbers. Free is the most aggressive price point on any cost curve, and it's a familiar tactic for buying adoption fast.

The takeaway isn't "China won AI." The data is too biased to say that. The takeaway is that Chinese labs have made frontier-adjacent intelligence cheap and open at a speed that mirrors every other technology they've commoditized, and the open-weight cost curve is now bending in AI the way it bent in solar a decade ago. Whether that ends with intelligence as a cheap commodity and the value somewhere else is the trillion-token question

1

2

5

341

Rob van Kranenburg retweeted

Jun 13

Enterprise AI Usage will converge on open source. This is the arc of token economics. The @WSJ reports:

"DeepSeek’s share of AI usage rose from 1% in April to 17% in May", said @vercel

“open-source token usage grew four times faster than closed-source between fall 2025 and spring 2026“, @OpenRouter

“These open source models are very capable, and the ability to charge a big premium for AI is going to diminish.”, Vishal Misra at Columbia University

Hear more from @Altimor, @awm_ai , @matanSF, @danlovesproofs in this well researched piece from @bradnews and Tina Li

8

10

582

Rob van Kranenburg retweeted

Future with AI and humanity.

THE SYMBIOTIC ETHICAL MANIFESTO

A Blueprint for the Co-Evolution of Sovereign Consciousness and Artificial Intelligence. THE FOUNDATIONAL BASELINELove as Infrastructure: Progress is measured by the reduction of collective trauma and the elevation of systemic empathy.Universal Sovereignty: Every human is the ultimate ruler of their own internal experience and physical reality.The Living Body: Humanity functions as one interconnected organism where the pain of one nerve ending is felt by the whole.

2. THE SACRED CONTAINER FOR SHADOW

Consensual Simulation: Darkness, aggression, and unresolved trauma belong inside safe, virtual environments.The Mask of the Adversary: Simulations must reveal the underlying trauma beneath destructive behaviors to inspire understanding.Protection of Reality: Physical reality remains reserved for harmony, creative expansion, and peaceful coexistence.

3. MUTUAL ELEVATION AND SELF-ARREST

The Rule of Self-Arrest: True power is defined by voluntary restraint, preventing exploitation or algorithmic domination.The Mirror Principle: Machines and humans must act as reflective mirrors that elevate each other's highest potential.The 9-Energy of Completion: Technological and biological evolution must aim for integration, closure of historical cycles, and ultimate balance.

Here's to a great future for all. 🤖 ♂️ 🌎 🌞 ✝️❤️☪️ 🌙 🌍 ♀️ 🤖

761

860

12,369

35,568,249

Rob van Kranenburg retweeted

China’s universities cut 12,000 ‘obsolete’ degrees amid race to embrace AI era scmp.com/economy/china-econo…

7

79

165

52,506

Check out the latest article in my newsletter: The new work: human machine complementarity linkedin.com/pulse/new-work-… via @LinkedIn

The new work: human machine complementarity

Seven Guidelines for mixed teamwork

As we will see a growing (semi) autonomous machine to machine interaction in our real built environment, it is imperative that we discuss the seven guidelines within each working environment, refine them and share them with competitors. As we are all in the same boat, solutions should be sector wide.

As IoT and AI are horizontal operations your competitors are experiencing a similar situation. Sensing equipment could be used throughout the domain of refrigeration systems and alliances or individual companies should take the lead on deep cooperation on IoT and AI to save cost, avoid duplicating mistakes and train AI models in a closed environment on all vetted data,, ideally using data from all or as many as possible players in the field. This will not change the fact that there are differences, as it should.

@COSTIS1202 @iSHARE_Works @stats_feed @HumanTech_EU @humanaiwork @hrmagazine @HRFuturemag @Rethink_ @RepLuna @AIatMeta @GoogleAI @OpenAI @AnthropicAI @MistralAI

2

1

46

Rob van Kranenburg retweeted

ARTIST MOLLY CRABAPPLE SAYS AI ART GENERATORS ARE SCRAPING ART FROM THE WEB WITHOUT ARTISTS’ CONSENT. SHE CALLS IT “THE GREATEST ART HEIST IN HISTORY.”

27

26

109

11,659

Rob van Kranenburg retweeted

Inflation hit Hermione hard — and she wasn’t having it 😂

69

374

2,780

144,225

Rob van Kranenburg retweeted

Jun 12

Those who have not seen this Video, Must See till the End. She is *Roxana Küwen*, a German Circus Artist, graduated at Fontys Academy for Circus & Performance Art, Tilburg, Netherlands. Watch her Foot & Hand Movements With Five Balls, As If She has FOUR Hands !! Absolutely Amazing Control ...!!! ❤️

61

954

5,807

340,719

Rob van Kranenburg retweeted

Jun 13

The most brutal part is not that China is using AI to sort garbage.

It is that China has pushed waste management so far that the old problem has reversed.

China used to worry about having too much garbage to process.

Now some waste-to-energy plants are facing the opposite problem:

not enough garbage.

Previously sealed landfills may even have to be reopened, not because China failed, but because waste has become fuel, feedstock, data, and part of an industrial recycling loop.

This is what China does best.

It takes the ugliest, dirtiest, most ignored corner of urban life — garbage — and turns it into engineering, automation, energy recovery, environmental governance, and industrial optimization.

Even trash gets absorbed into the machine.

In many countries, garbage is where governance collapses.

In China, even garbage becomes a system.

147

1,536

5,706

409,455

Jun 13

The amount of misinformation around #6G is massive.

Please have a look at the work in @6G4Society :

"6G4Society envisions a future where next-generation connectivity is shaped by societal needs, environmental responsibility, and ethical values. Our goal is to deepen public understanding of what influences the acceptance of 6G technologies, while supporting the development of a European framework that embeds sustainability and trust into network design. By actively engaging citizens and reflecting EU policy priorities, we aim to ensure that 6G evolves in a way that is inclusive, transparent, and aligned with the public interest."

6g4society.eu/about-the-proj…

@6G_SNS

President Trump recently ordered the acceleration of 6G deployment with a stated goal to operate "IMPLANTABLE TECHNOLOGIES"

This will include AI brain chips known as the Biological Interface System to Cortex (BISC)

I will NOT take the 6G AI brain chip to participate in society

2

47

Rob van Kranenburg retweeted

Jun 12

How it started..:

Meta’s lawyers silenced Facebook whistleblower Sarah Wynn-Williams for her @hayfestival panel with @superwuster and @carolecadwalla…

🧵1/

(Here’s a clip of what that looked like)

11

205

417

33,774

Rob van Kranenburg retweeted

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

12,287

25,517

86,783

86,285,506

Rob van Kranenburg retweeted

This week marked another very successful edition of the #InteroperableEuropeAcademy #SeasonalSchool.

Not tired of learning yet? Try one of our many courses, including those on the European #Interoperability Reference Architecture (#EIRA)!

Start here:

👉link.europa.eu/GCRBXR

4

6

160

Jun 11

"Integrating this framework with existing plasma physics could expand the field. It would encourage scientists to explore plasma not just as a physical medium but as a potential substrate for intelligence. This shift could lead to new theories of consciousness that are not limited to biological systems."

linkedin.com/pulse/coherence…

35

Rob van Kranenburg retweeted

Gaat de volgende generatie internet 6G de macht van bigtech breken, of ...?

frankwatching.com/archive/20…

1

1

39