Crypto Researcher on All Chains | L1, L2, L3 & Coin Expert.. building @Velvet_Capital

Joined June 2009

- Tweets 35,842

- Following 2,111

- Followers 52,249

- Likes 90,307

2,649 Photos and videos

Pinned Tweet

21 Jun 2024

When some top chads post their portfolio, some people ask questions "what are they doing, that I'm not doing?"

It's diversification mate!

Many people flock to overpriced crypto assets, overlooking the vast landscape of innovative projects emerging.

While diversification can improve risk-adjusted returns through metrics like the Sharpe ratio, its benefits go deeper.

In a dynamic market like crypto, it's crucial to gain exposure to the diverse applications and other crypto sectors.

Think of returns like a power law distribution. A few investments deliver exceptional results, while many yield lower or negative returns. This is similar to venture capital, where success hinges on identifying a few breakout startups.

Diversification in crypto serves the same purpose, it increases your chances of capturing the "runner" that'll propel your portfolio upwards.

In the last 24h, AI tokens surged 15% outperforming other crypto sector. This is because Nvidia is close to becoming World’s Most Valuable Company.

If you had spread your investment into AI tokens also, your portfolio would've added gains despite this week's bloodbath.

➭ 𝗕𝗲𝘆𝗼𝗻𝗱 𝘁𝗵𝗲 𝗧𝗼𝗽 𝟭𝟬: 𝗔 𝗕𝗿𝗼𝗮𝗱𝗲𝗿 𝗖𝗿𝘆𝗽𝘁𝗼 𝗨𝗻𝗶𝘃𝗲𝗿𝘀𝗲

A portfolio concentrated solely on the top 10 cryptocurrencies by market cap might seem diversified, but it only captures a limited scope.

These are primarily Layer 1 blockchain protocols. While these tokens may appear less risky, they miss the wave of innovation happening across the crypto landscape.

Expanding your portfolio to include the other top crypto sector paints a more dynamic picture. This encompasses:

• AI: $ARKM, $GRT, $BOTTO, $DEAI, $KAI

• RWA: $PENDLE, $OM, $LNDX, $TRADE, $PRCL, $SOIL

• Layer 2: $ARB, $OP, $STRK, $METIS, $MANTA

• DePIN: $OPSEC, $FIL, $AIOZ, $IOTX, $GPU

• GameFi: $PIXEL, $APE, $SAND, $NAKA, $KARRAT, $MYRIA

The crypto market's rapid evolution necessitates an active approach to portfolio management. Diversification isn't simply buying more assets.

It's about taking a long-term view and strategically allocating your investments across different sectors and project sizes to capitalize on diverse potential outcomes.

RWA Market Cap Expected to Reach $16 Trillion in 2030. DYOR and find your best RWA project pick, buy and HODL!

✍️ 𝗖𝗼𝗻𝗰𝗹𝘂𝘀𝗶𝗼𝗻

Think of diversification not as weakening your portfolio, but as giving it more firepower. It increases your chances of capturing the winners while managing risk.

In essence, diversification gives you more opportunities for success, for less.

140

74

824

495,574

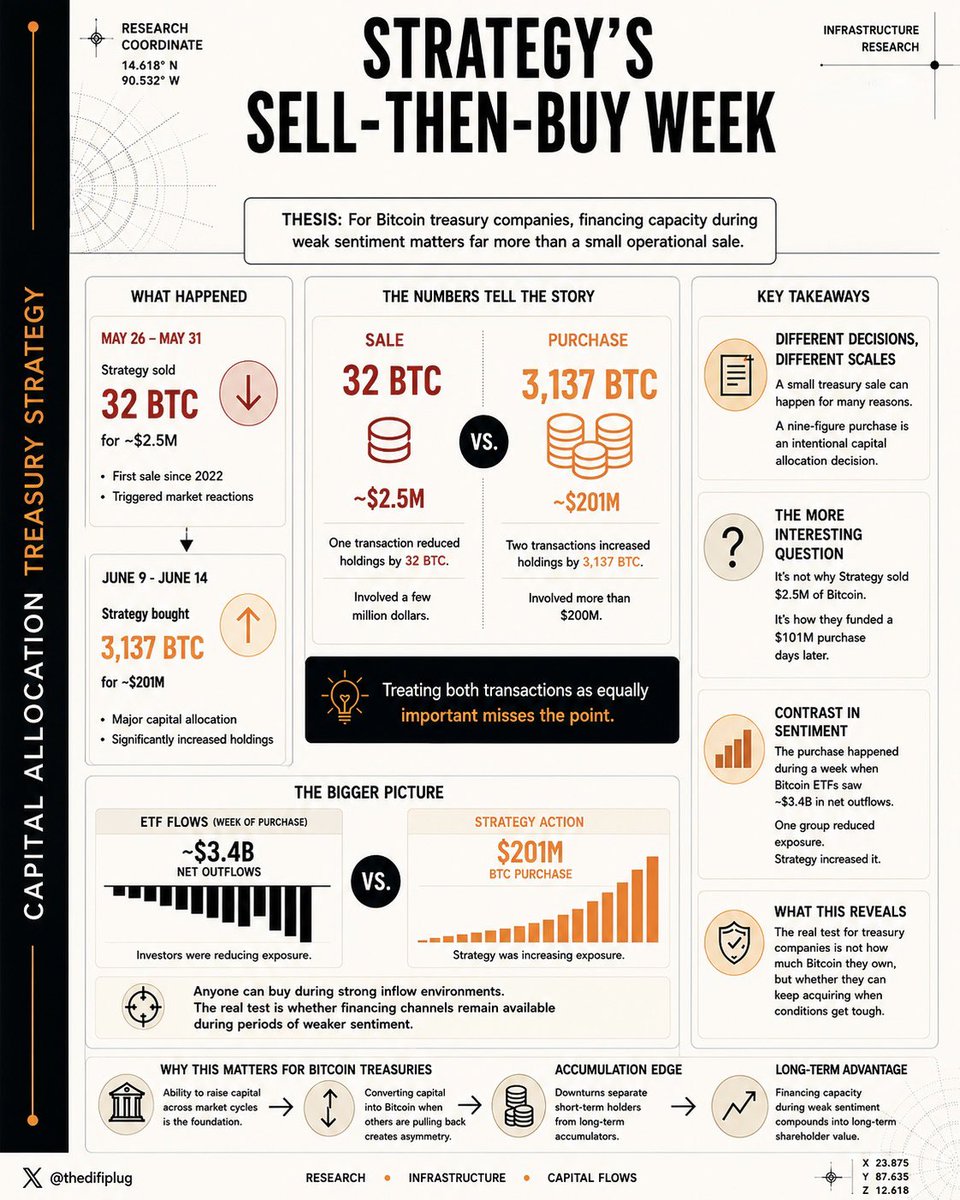

Strategy sold 32 BTC.

Over the next two weeks, it bought 3,137 BTC but most people focused on the sale.

I think the purchases are the real story.

When headlines emerged that Strategy had sold Bitcoin for the first time since 2022, the reaction was immediate.

“Strategy is selling.”

“Saylor broke his pledge.”

“The biggest Bitcoin bull is taking profits.”

The numbers suggest something different.

Between May 26 and May 31, Strategy sold 32 BTC for roughly $2.5M.

On June 9, it acquired 1,550 BTC for approximately $101M.

Then between June 8 and June 14, it acquired another 1,587 BTC for approximately $100M.

One transaction reduced holdings by 32 BTC but the next two increased holdings by 3,137 BTC.

Treating those transactions as equally important misses the point.

● Different Decisions, Different Scales

The mistake is assuming every Bitcoin transaction reflects the same decision.

Corporate treasury management includes tax obligations, operational requirements, and administrative activities.

Those decisions are very different from discretionary capital allocation.

A small treasury sale can happen for many reasons.

More than $200M deployed into Bitcoin over two weeks is an intentional capital allocation decision.

The market treated both events as if they carried the same informational value.

They don’t.

● The Financing Question

The bigger question isn’t why Strategy sold $2.5M of Bitcoin.

It’s how Strategy funded more than $200M of Bitcoin purchases shortly afterward.

Those purchases occurred during a period when Bitcoin ETFs reportedly experienced roughly $3.4B in weekly outflows.

One group of investors was reducing exposure.

Strategy was increasing it.

That’s a more interesting contrast.

● What This Reveals About Treasury Companies

Bitcoin treasury companies are often judged by how much Bitcoin they own.

A better measure is whether they can continue acquiring Bitcoin when conditions become less favorable.

Anyone can buy during strong inflow environments.

The real test is whether financing channels remain available during periods of weaker sentiment.

If a treasury company can keep raising capital and converting it into Bitcoin during drawdowns, the accumulation strategy remains intact.

As of June 14, Strategy held 846,842 BTC acquired for approximately $64.07B at an average purchase price of $75,656 per BTC.

● My Take

The sale generated the headlines.

The purchases generated the takeaway.

Strategy sold $2.5M of BTC and then deployed more than $200M into additional Bitcoin. For treasury companies, financing capacity during weaker sentiment tells you far more than a small operational sale.

40

13

48

7,430

Jun 15

The challenge for a stablecoin isn’t getting issued.

The challenge is getting noticed.

Crypto-native users already know where to find USD1.

The question is how the asset reaches people outside that circle.

That’s why this partnership makes sense to me.

➤ $250,000 in USD1 contributed to the UFC Freedom 250 bonus pool

➤ WLFI announced as a presenting partner

One expands visibility, while the other expands reach.

Different objective from yield campaigns.

Different objective from exchange listings.

Same long-term goal:

Getting the asset in front of more people.

41

9

44

4,276

Jun 14

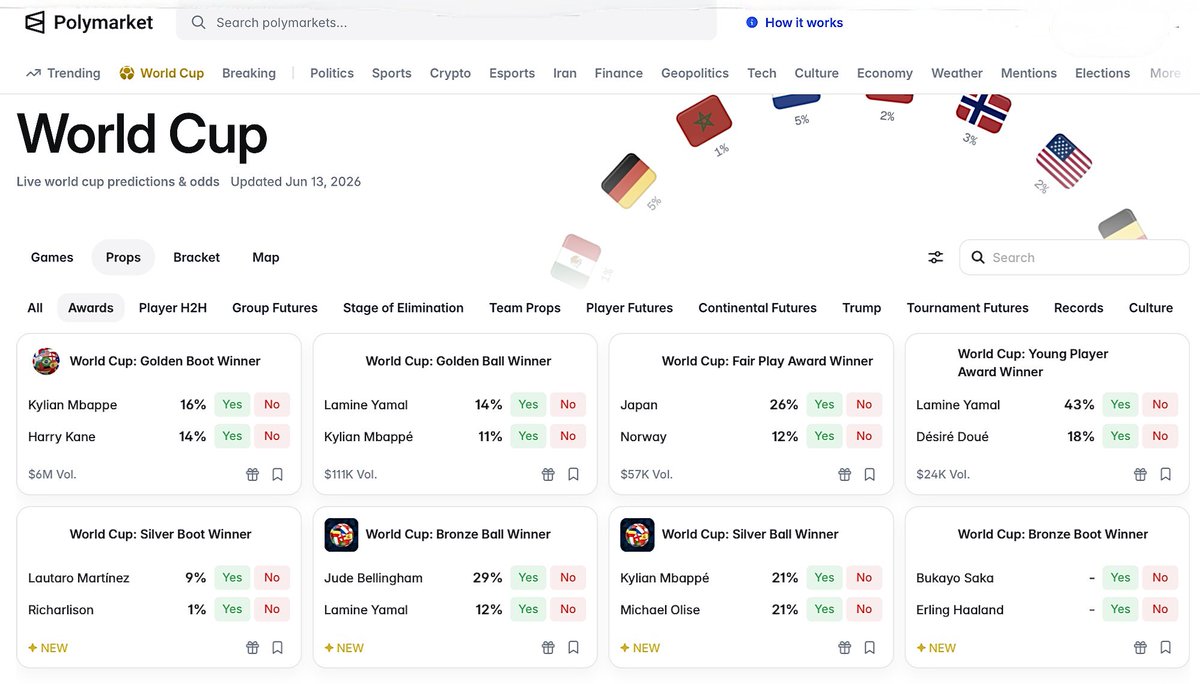

Everyone is watching the $2.1B World Cup Winner market.

Personally, I think the more interesting trade sits one layer below.

Player markets on @Polymarket.

● Golden Boot ($6M volume)

- Mbappé: 16%

- Kane: 14%

- Oyarzabal, Haaland, Olise, and Yamal close behind

● Golden Ball ($111K volume)

- Yamal: 14%

- Mbappé: 11%

At first glance, these markets look insignificant next to a $2.1B outright contract.

That’s exactly why they’re interesting.

Winner markets become more efficient as tournaments progress but players markets don’t.

Every goal, injury, tactical adjustment, or rotation decision becomes a repricing event.

Where the winner market is trying to answer one question the player markets are trying to answer dozens and creates a very different information environment.

A national team’s title odds might barely move after a group-stage match.

A striker’s Golden Boot odds can change dramatically in 90 minutes.

That’s why the sharpest information often shows up here first.

Not because these markets are larger.

Because they’re less efficient.

The winner market is increasingly a macro trade but player markets are micro trades.

And during the group stage, micro usually moves faster than macro.

37

10

48

6,121

Jun 12

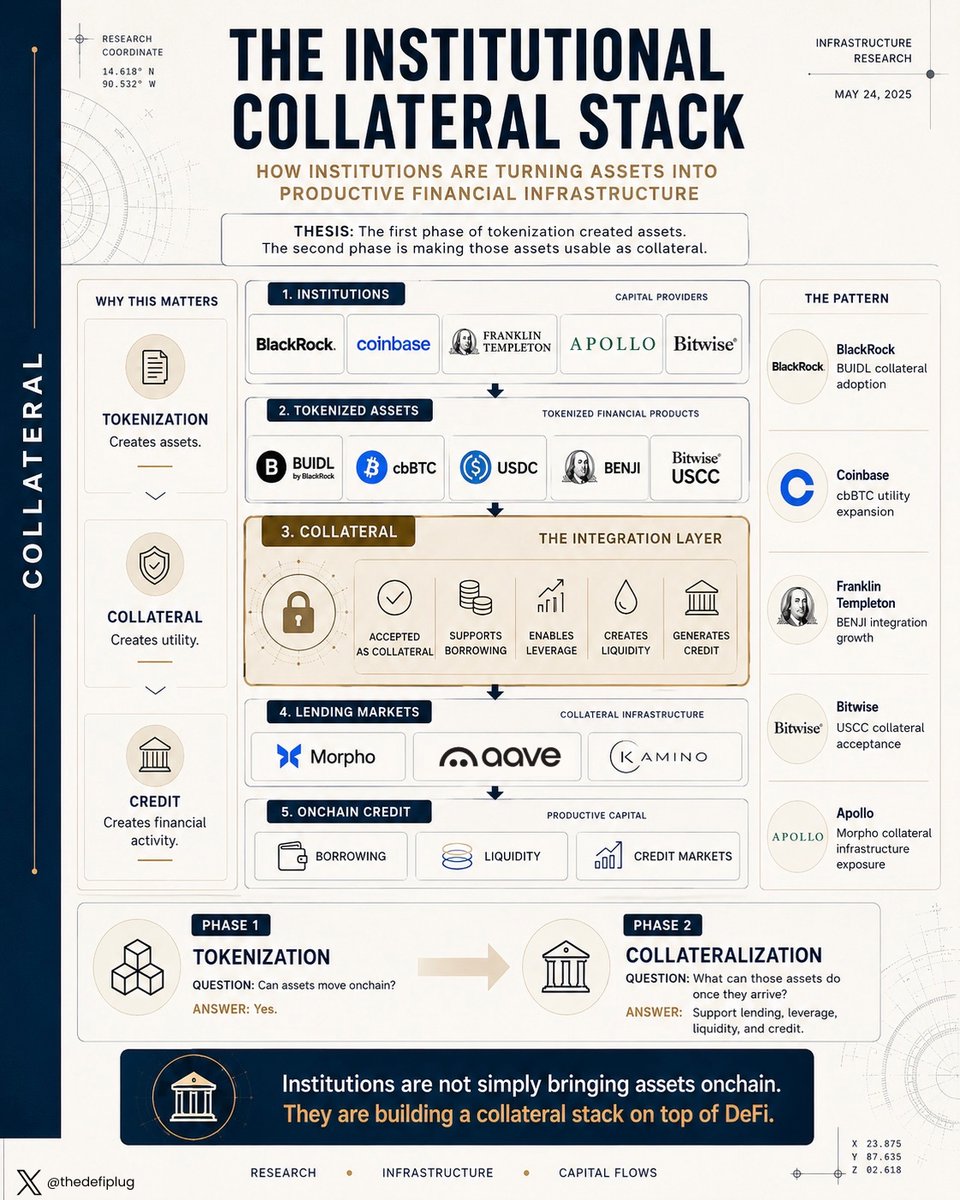

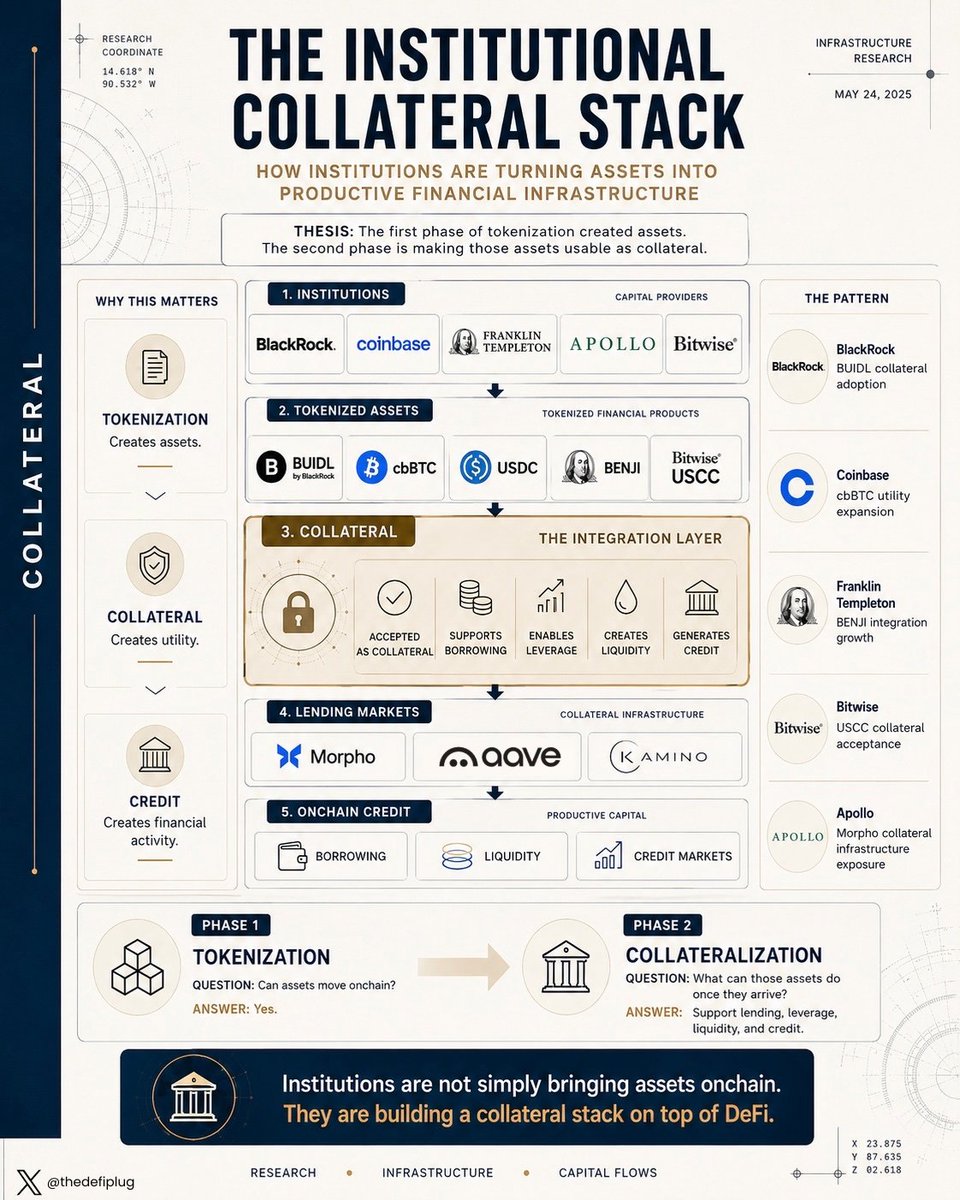

Over the past year, several large institutions have expanded their presence in DeFi.

@BlackRock launched BUIDL. @Coinbase expanded cbBTC and USDC integrations. @FTI_US expanded BENJI’s onchain reach. @apolloglobal and @Morpho announced a strategic partnership that includes up to 90 million MORPHO tokens vesting over 48 months.

At first glance, these look like separate initiatives.

The common thread is easy to miss.

The easiest way to interpret these developments is through adoption.

Institutions are entering DeFi.

The more important question is integration.

How are institutions choosing to participate once they arrive?

A pattern is starting to emerge.

Institutions are not entering DeFi by becoming crypto-native.

They are entering by making their assets usable as collateral.

That distinction matters because financial systems are built around collateral, not assets.

The first phase of tokenization focused on issuance.

Can Treasuries be tokenized?

Can institutional funds exist on public blockchains?

Can private credit move onchain?

The answer is increasingly yes.

The more important question now is:

What can those assets do once they arrive?

Several developments point in the same direction:

➤ Apollo: Strategic partnership with Morpho involving up to 90 million MORPHO tokens over 48 months

➤ BlackRock: BUIDL accepted as collateral across lending venues

➤ Coinbase: Expanding cbBTC and USDC integrations

➤ Franklin Templeton: Expanding BENJI’s utility across public blockchains

➤ Bitwise: USCC fund tokens accepted as collateral across Morpho, Aave, and Kamino

Different firms.

Different products.

Same objective.

Make institutional assets usable inside DeFi.

This is why the Apollo-Morpho relationship stands out.

The market tends to view it as a token investment.

It is better viewed as exposure to collateral infrastructure.

Morpho provides modular lending infrastructure that allows credit markets to be built around specific collateral assets.

The opportunity is not tokenization itself.

The opportunity is collateralized credit.

BlackRock’s BUIDL illustrates the same shift.

The interesting development is not that BUIDL exists.

It is that BUIDL can now secure loans and participate in lending markets.

Once an asset can support borrowing, leverage, and liquidity, it stops behaving like a passive investment product.

It becomes infrastructure.

The same logic applies to cbBTC.

The value is not issuance alone.

The value comes from expanding where Bitcoin can be deployed productively.

The market still underestimates this distinction.

Most tokenization discussions focus on assets.

Financial systems focus on collateral.

An institutional asset sitting in a wallet creates limited value.

An institutional asset that can secure credit and circulate through lending markets becomes significantly more useful.

That is why collateral integrations may ultimately matter more than token issuance.

The first phase of tokenization created assets.

The second phase is turning those assets into productive financial infrastructure.

Viewed through that lens, the Apollo-Morpho relationship is important not because Apollo is simply buying a token.

It is important because it signals institutional interest in the infrastructure layer that makes collateral productive.

The easiest interpretation is that institutions are entering DeFi.

The more useful interpretation is that they are building a collateral stack on top of it.

55

17

95

6,749

THEDEFIPLUG retweeted

Jun 11

Seeing @ethena select @centrifuge as its strategic tokenization partner made me think about how protocols evolve as they scale.

When protocols are small, growth solves most problems.

When protocols become large, diversification becomes more important.

That’s the stage Ethena is entering.

The partnership with Centrifuge isn’t just about RWAs.

It’s about expanding the set of assets supporting USDe.

x.com/centrifuge/status/2064…

Crypto-native collateral remains important.

Institutional credit now joins the mix through JAAA.

Different assets.

Different return drivers.

Different risk profiles.

The larger a system becomes, the more valuable those distinctions are.

Growth gets attention.

Collateral construction tends to happen in the background.

But over time, the quality and diversity of the asset base become increasingly important.

That’s usually what larger financial systems look like as they mature.

Jun 9

Ethena has selected Centrifuge as a strategic tokenization partner.

Following an in-depth RWA RFP, @Ethena chose Centrifuge to support the next phase of USDe's backing diversification.

The partnership launches with an allocation to Centrifuge’s JAAA fund, managed by @JHIAdvisors, bringing institutional credit into Ethena’s expanding real-world asset collateral strategy.

A major step for Ethena. A major step for RWAs.

Powered by Centrifuge.

15

22

66

4,779

Jun 11

The path from institutional capital to onchain yield is getting shorter.

A few years ago the process looked something like:

custody → bridge → protocol selection → risk assessment → deployment

Now @sparkdotfi sits between custody and credit markets as an allocation layer.

Institutional capital can be deployed across multiple credit venues through a structured highly secure framework rather than remaining tied to a single market.

To me, that’s where the product differentiates itself, not that institutions can access yield, that part already existed.

The product is making onchain credit easier to access.

Same destination but different much simpler workflow.

That is where a lot of future adoption will come from.

Jun 9

Institutional capital held in custody can now now access on-chain credit markets through structured allocation via Spark.

Through BitGo, capital can be deployed into Spark Savings vaults, where it is allocated across multiple credit venues within a single, structured system.

Most on-chain lending requires selecting a single market or pool.

Spark takes a different approach:

Capital is deployed across venues based on predefined liquidity, exposure, and allocation parameters, rather than remaining fixed within one market.

Reducing exposure to high-utilisation conditions where liquidity becomes constrained.

This is a new path for institutional capital into on-chain credit markets.

Spark is now available via @BitGo institutional wallets.

24

5

52

5,415

THEDEFIPLUG retweeted

Jun 11

31

18

75

3,263

THEDEFIPLUG retweeted

Jun 10

Tokenized equities are no longer a small RWA experiment.

According to RWAxyz, tokenized stocks now hold $1.47B in distributed value, with $4.20B in monthly transfer volume and more than 347K holders.

That puts the category at roughly 10% of the tokenized Treasury market, which currently stands at $14.82B.

The important part is not just growth.

It is concentration.

Ondo currently leads the market with $911.2M in tokenized stock value, representing 60.3% market share.

xStocks follows with $416.8M, or 27.6% share.

Together, the two platforms control nearly 88% of the market.

That tells us two things:

1. Tokenized equities are scaling quickly.

2. The market is still highly concentrated.

The first phase was issuance.

Backed Finance helped establish the category through xStocks.

Ondo expanded it with a broader tokenized equity platform.

That phase is largely complete.

The market already has tokenized versions of major equities and ETFs.

The next bottleneck is utility.

➤ Can tokenized equities be used as collateral?

➤ Can lending markets support them?

➤ Can traders borrow against them?

➤ Can perp venues and DeFi protocols build around them?

That is where the next phase begins.

Tokenized Treasuries did not become a $14.82B market because investors wanted Treasury tokens.

They became collateral.

They became yield products.

They became balance sheet tools.

They became infrastructure.

Tokenized equities have not made that transition yet.

The market has already identified the issuers.

What it has not identified is the infrastructure layer.

The first phase was creating tokenized equities.

The next phase is making them useful.

The protocols that integrate them first may capture the next major wave of RWA growth.

The caveat is regulation.

Without clearer treatment of tokenized equities, particularly around securities classification and U.S. distribution, institutional adoption remains constrained.

But the direction is already visible.

The first phase proved tokenized equities can attract capital.

The second phase will determine whether they become productive financial assets.

The easiest takeaway is that tokenized equities reached $1.47B.

The more useful takeaway is that issuance is no longer the bottleneck.

The next winners may not be the protocols creating tokenized stocks.

They may be the protocols that make those stocks useful.

14

12

26

3,957

THEDEFIPLUG retweeted

Jun 9

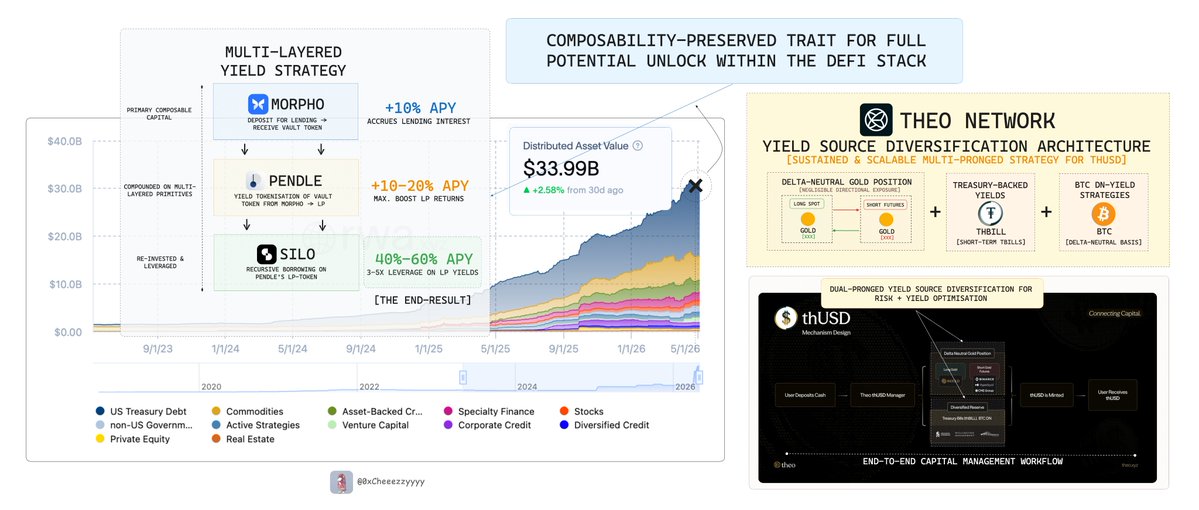

RWA-Fi now sits at ~$34B in distributed assets, growing ~420% in just ~1.25 years (h/t @RWA_xyz), with commodities already accounting for ~20% of that stack.

Within this ~$7.1B segment, gold dominates almost entirely.

That alone is honestly telling, tokenised gold has already achieved a state primed to be one of the next major primitives on-chain.

As the world’s primary SoV asset, gold has always been positioned for preservation and not productivity. But that dynamic starts to change the moment it enters DeFi.

The real unlock isn’t just access, but what you can do with it.

Through composability, gold can evolve from a passive reserve into a capital-efficient asset that can be:

1. deployed as collateral

2. structured into yield strategies

3. integrated into broader financial workflows

And this shift is inevitable imo esp. as liquidity from established issuers continues to scale.

The constraint today isn’t supply.

It’s the lack of on-chain financialisation and meaningful DeFi opportunities around it.

That’s where I personally think @Theo_Network starts to stand out.

With $thGOLD and $thUSD, it introduces structured exposure derived from gold-linked strategies which effectively turning gold into a yield-bearing primitive rather than just a tokenised wrapper.

More interestingly, the yield itself isn't dependent on crypto market activity.

Under the hood, thUSD monetises three long-standing sources of return within institutional gold markets:

🔸 Physical gold leasing demand from refiners, dealers and retailers

🔸 CME futures basis capture, where gold futures trade in contango ~99.5% of the time and converge toward spot at expiry

🔸 Treasury collateral yield from the underlying reserve assets

The result is a DN structure where returns are derived primarily from carry rather than directional exposure to gold itself.

This is an important distinction because the yield originates from established real-world market activity that has existed for decades across commodity and treasury markets which makes it both scalable sustainable.

Early signals already reflect strong demand w/ $100M cap filled in under 14 hours, with DeFi integrations on the horizon.

That positions it as a potential first strong mover in defining how gold behaves within DeFi. This isn't just mirroring TradFi exposure, but extending it.

If this direction holds, the implication is clear:

Gold doesn’t just remain a SoV, it becomes a productive unit of capital within a programmable financial system.

And whichever protocols successfully bridge that gap will likely set the precedent for this entire vertical moving forward.

May 22

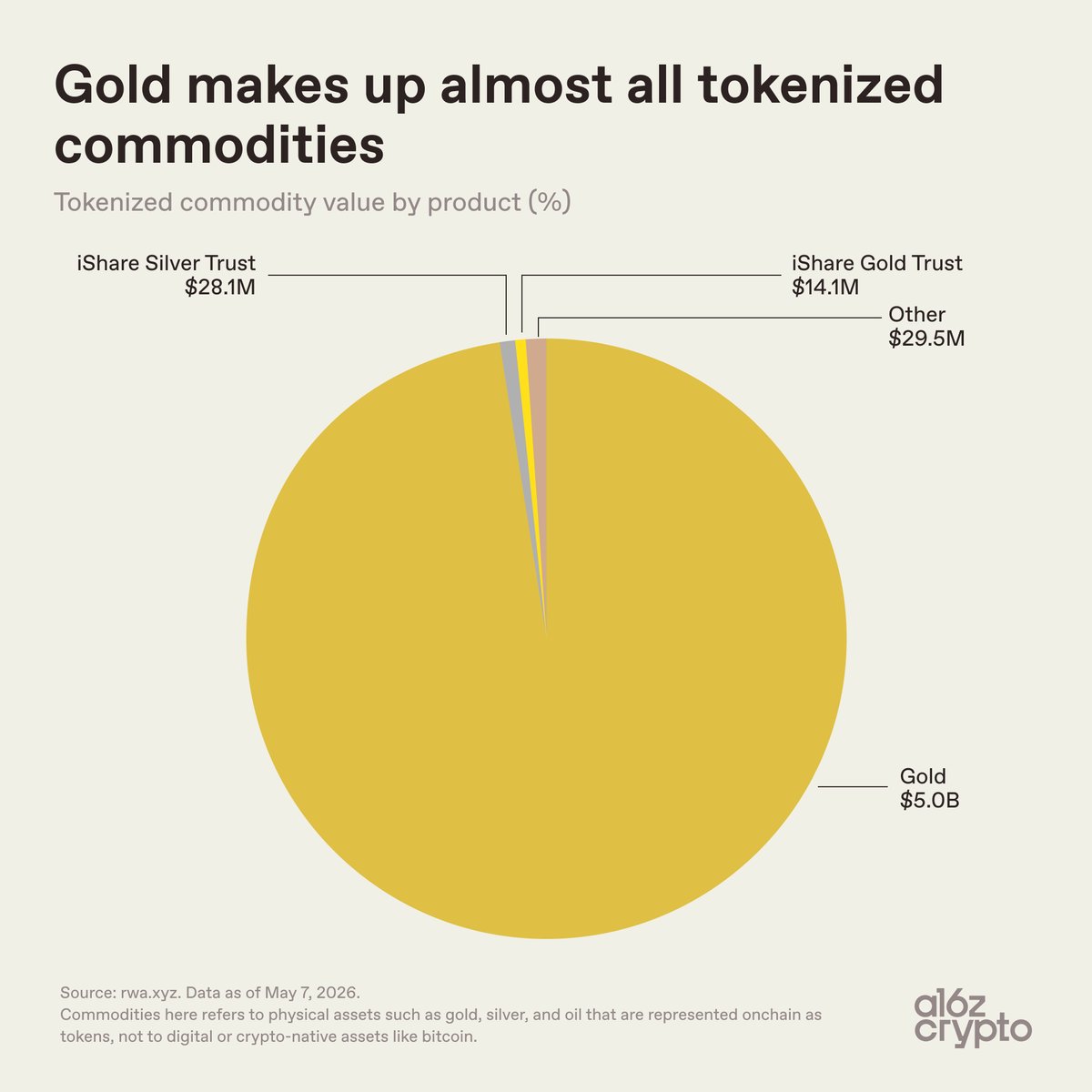

The tokenized commodity market is almost entirely gold.

Gold is an obvious fit for tokenization: It’s global, standard, and already tracked through paper claims

Plus, crypto investors already get it. Bitcoin was called “digital gold” long before tokenized gold took off.

XAUt and PAXG translate a familiar ownership model to blockchains, turning claims on gold held in vaults into onchain tokens held in wallets.

Everything else (tokenized oil, crops, energy, compute, etc.) is much earlier and has a smaller market share.

36

14

71

4,185

THEDEFIPLUG retweeted

Jun 9

The crypto card sector reached $832.8M in monthly volume in May 2026, up 60% from $519.7M in November 2025.

More importantly, the growth is becoming diversified.

What was once dominated by a single provider is now evolving into multiple product categories serving different user needs.

● Sector Overview

➢ Monthly volume grew from $519.7M (Nov 2025) → $635.2M (Jan 2026) → $832.8M (May 2026)

➢ USDT accounts for roughly 72% of settlement volume

➢ Visa now handles approximately 97% of crypto card settlement activity

The category is no longer a niche product for crypto users. It is increasingly becoming a consumer financial layer built on stablecoin infrastructure.

1. @RedotPay

RedotPay remains the largest program in the sector.

➢ $445.4M monthly volume

➢ Roughly 53% market share

➢ 40% growth over six months

The average transaction size sits around $819, suggesting many users treat RedotPay as a capital movement and spending bridge rather than a day-to-day payment card.

Its strength comes from simplicity.

Users deposit stablecoins and gain spending access across more than 130 countries.

The product has built strong distribution across Southeast Asia and Africa, where stablecoin utility often solves practical financial problems.

2. @KASTxyz

KAST reached $174.7M in monthly volume and continues to gain share.

Built on Solana, the product focuses on:

➢ Near-instant settlement

➢ Low transaction costs

➢ Cashback and rewards incentives

➢ Native stablecoin experience

The combination of cheap rails and reward-driven retention appears to be working.

KAST is increasingly positioning itself as the consumer-friendly stablecoin spending account.

3. @ether_fi Cash

EtherFi Cash processed $80.4M in volume during May.

The volume figure alone misses the story.

➢ 6.6M transactions

➢ 81k active addresses

Unlike custodial card providers, EtherFi allows users to borrow against their crypto rather than sell it.

Users maintain exposure to their assets while unlocking spending power.

The result is a very different customer profile: crypto-native users looking to preserve upside while accessing liquidity.

● The Long Tail Is Growing

Growth is not limited to the largest programs.

Several smaller players are scaling rapidly:

➢ Karta: 427%

➢ @KoloHub: 276%

➢ @useTria: continued recovery

➢ @Plasma One: entered the rankings at meaningful scale

While the largest providers continue to dominate volume, niche products are beginning to establish product-market fit across different user segments.

● My Take

The sector is increasingly splitting into two distinct markets.

1. Custodial stablecoin spending networks

Examples: RedotPay, KAST

These products optimize for accessibility, payments, and global stablecoin utility.

2. Non-custodial borrow-to-spend platforms

Examples: EtherFi Cash, Tria

These products optimize for capital efficiency, yield preservation, and crypto-native financial behavior.

Both categories are growing simultaneously.

That suggests the market is not converging on a single model.

It is expanding into multiple financial products built on the same underlying stablecoin infrastructure.

18

9

30

4,272

THEDEFIPLUG retweeted

Jun 8

A single data point breaks the prediction market narrative.

In March 2026, roughly 87% of Kalshi’s trading volume came from sports contracts.

Not elections.

Not inflation forecasts.

Not recession probabilities.

Sports.

That number carries weight because Kalshi has become the flagship example used to prove that prediction markets are evolving into serious financial infrastructure.

The narrative is straightforward.

Prediction markets aggregate information more efficiently than polls. They create real-time probabilities for future events. They represent a new financial primitive for forecasting uncertainty.

The growth numbers appear to support the thesis.

Prediction markets processed a record $29.4 billion in volume during May 2026.

➢ @Kalshi: $17.9B monthly volume

➢ @Polymarket: $8.8B monthly volume

➢ Combined lifetime volume: $180B

At first glance, it looks like information markets are finally reaching scale.

Then you look at what people are actually trading.

● What Traders Actually Chose

Kalshi’s growth has been extraordinary.

In March alone, sports contracts generated approximately $9.9 billion of the platform’s $13.0 billion volume. If that activity were annualized, it would rival some of the largest gambling businesses in the United States.

Meanwhile, Polymarket’s activity remains concentrated around politics, crypto, and current events.

Both platforms are typically grouped together under the same prediction market narrative.

The underlying user behavior suggests they are solving different problems.

One increasingly resembles a forecasting platform.

The other increasingly resembles a sportsbook.

That distinction becomes difficult to ignore when sports represents nearly nine out of every ten dollars traded.

● The Forecasting Paradox

The sector’s growth story is built around information markets.

Academics describe prediction markets as truth-discovery mechanisms.

Investors describe them as forecasting infrastructure.

The financial press describes them as a new asset class.

Yet the category leader derives the overwhelming majority of its activity from sports.

If sports betting drives most volume, then prediction markets may not have found product-market fit through forecasting.

They may have found product-market fit through gambling.

That doesn’t make the volume less real.

It changes what the volume actually represents.

● The Real Product

The real product may not be prediction markets.

The real product may be regulation.

Kalshi operates under a federal CFTC framework rather than the state-by-state licensing model used by sportsbooks.

Viewed this way, its growth becomes easier to explain.

The platform may not be winning because people want macro forecasts.

It may be winning because it found a new route into sports betting.

That is why regulators and courts are now involved.

➢ State regulators see sports betting.

➢ Kalshi sees federally regulated event contracts.

➢ The courts must decide which interpretation wins.

That difference determines who controls a multi-billion-dollar market.

● How New Markets Actually Scale

Financial innovations rarely scale through their original use case.

Stablecoins were framed as payments but scaled through exchange settlement.

DEXs were framed as infrastructure but grew through speculation.

Prediction markets may be following the same path.

The forecasting narrative may be true.

The growth engine appears to be sports betting.

● The Final Discovery

Prediction markets can forecast outcomes remarkably well.

Polymarket increasingly supports that thesis.

But Kalshi’s numbers point elsewhere.

When 87% of volume comes from sports contracts, forecasting demand alone cannot explain the growth.

Prediction markets may not just be disrupting information markets.

They may be disrupting sports betting.

And if that’s true, the biggest prediction market story of 2026 isn’t forecasting.

It’s who gets to own the sportsbook.

39

10

46

3,621

Jun 6

Crypto’s biggest winners are usually obvious.

Just not when they’re still investable.

One of the most persistent patterns in crypto is that product precedes narrative, usage precedes attention, and revenue precedes consensus.

Uniswap V2 launched in May 2020. Aave V2 launched in December 2020. Neither became immediate consensus trades. The products existed before the market collectively decided they mattered.

That sequence keeps repeating.

Most investors believe they are searching for innovation. In practice, they are searching for validation.

They want to see:

➢ Growing users

➢ Growing TVL

➢ Growing revenue

➢ Growing mindshare

The problem is that these signals arrive at different times.

Product comes first.

Usage comes second.

Consensus comes last.

By the time everyone agrees something is important, much of the asymmetry has already disappeared. Consensus reduces uncertainty. It also reduces opportunity.

That is why some of the most important infrastructure tends to emerge during corrections rather than euphoric phases.

Bull markets are good for distribution. Corrections are good for construction.

When capital becomes selective, builders focus less on attention and more on product quality, retention, and economics. Historically, those periods have produced many of crypto’s defining protocols.

The current market resembles those environments more than many realize. Attention has narrowed around a handful of large-cap assets while speculation has cooled.

Historically, this is where the next generation of infrastructure starts separating itself.

Not through price.

Through usage.

Every cycle creates a discovery gap. A period where a protocol is already working, but the market has not fully processed what it is becoming.

The signals tend to look familiar:

➢ Real users

➢ Real revenue

➢ Product differentiation

➢ Limited attention

➢ Weak consensus

The market struggles to value these periods because there is little social proof.

Only evidence.

Several protocols are already doing what past winners did before the market noticed.

@HyperliquidX is proving a crypto-native exchange can compete directly with centralized venues while generating meaningful revenue.

@Morpho reflects a broader trend where lending becomes infrastructure rather than a destination application.

@JupiterExchange benefits from ecosystem fragmentation. As liquidity spreads across venues, aggregation becomes more valuable.

@AerodromeFi has become a coordination layer for liquidity on Base rather than simply another DEX.

@OndoFinance sits at the center of tokenized capital markets if RWAs continue expanding beyond Treasury exposure.

@opentensor remains one of the few AI networks with measurable economic activity tied to compute demand.

@peaq is building infrastructure for a world where machines become economic participants.

@KASTxyz, @ether_fi Cash, and @gnosispay point toward another structural trend. Stablecoins are evolving from trading collateral into consumer financial accounts. The opportunity may not be the stablecoin itself. It may be owning the distribution layer through which users access them.

What stands out is not the individual names.

It’s the pattern.

Most of these protocols are not winning because of tokens.

They are winning because they own infrastructure, distribution, coordination, or revenue-generating activity.

The names that define 2027 may ultimately be different.

The underlying pattern probably won’t be.

Every cycle produces protocols that look obvious in hindsight. The difficult part is recognizing them while the discovery gap still exists.

History suggests that some of the protocols that define the next cycle are already live today.

The market simply hasn’t reached consensus yet.

23

26

45

3,711

THEDEFIPLUG retweeted

Jun 5

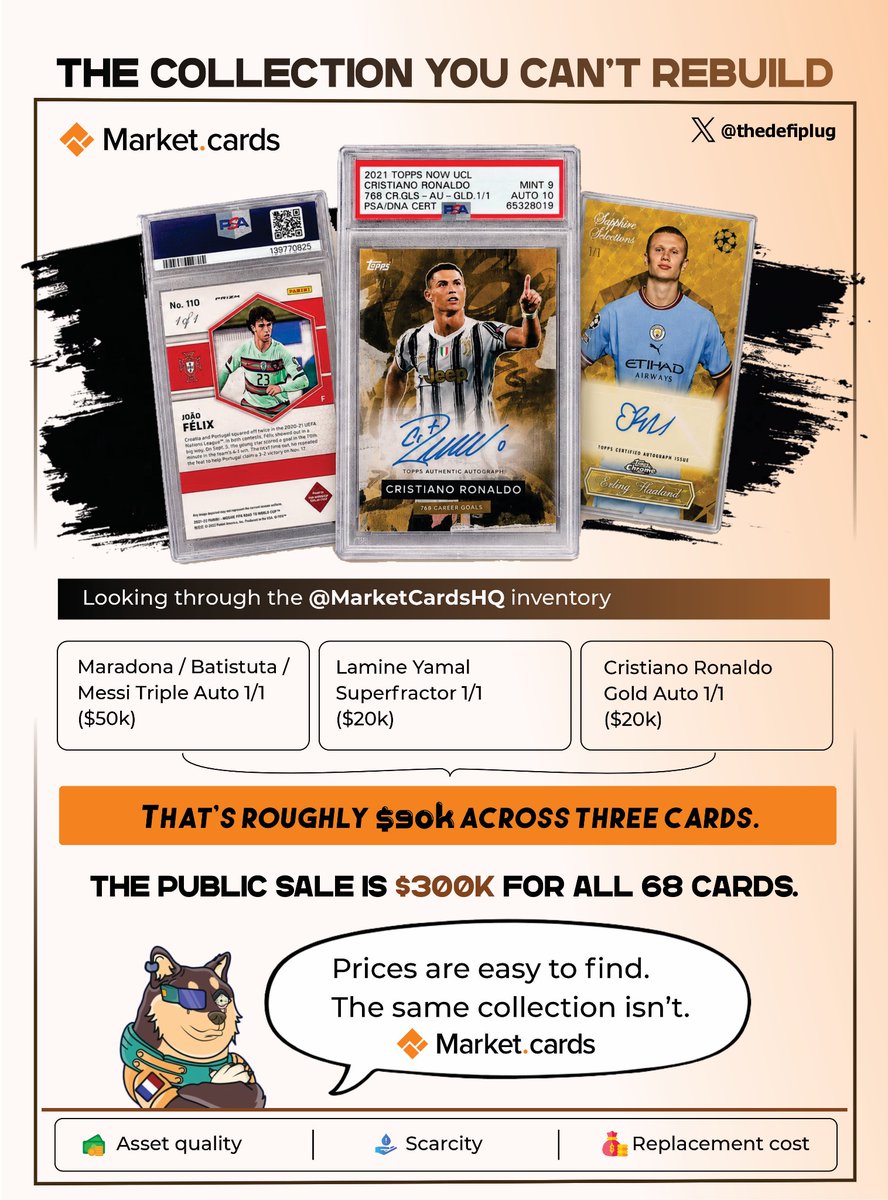

When evaluating collectible portfolios, I look at three things:

➤ Asset quality

➤ Scarcity

➤ Replacement cost

Looking through the @MarketCardsHQ inventory:

➤ Maradona / Batistuta / Messi Triple Auto 1/1 ($50k)

➤ Lamine Yamal Superfractor 1/1 ($20k)

➤ Cristiano Ronaldo Gold Auto 1/1 ($20k)

That’s roughly $90k across three cards.

The public sale is $300k for all 68 cards.

The valuation is one layer.

The harder part is estimating replacement cost.

Because capital can buy assets. It can’t always buy availability.

Prices are easy to find. The same collection isn’t.

64

11

127

11,426

Jun 4

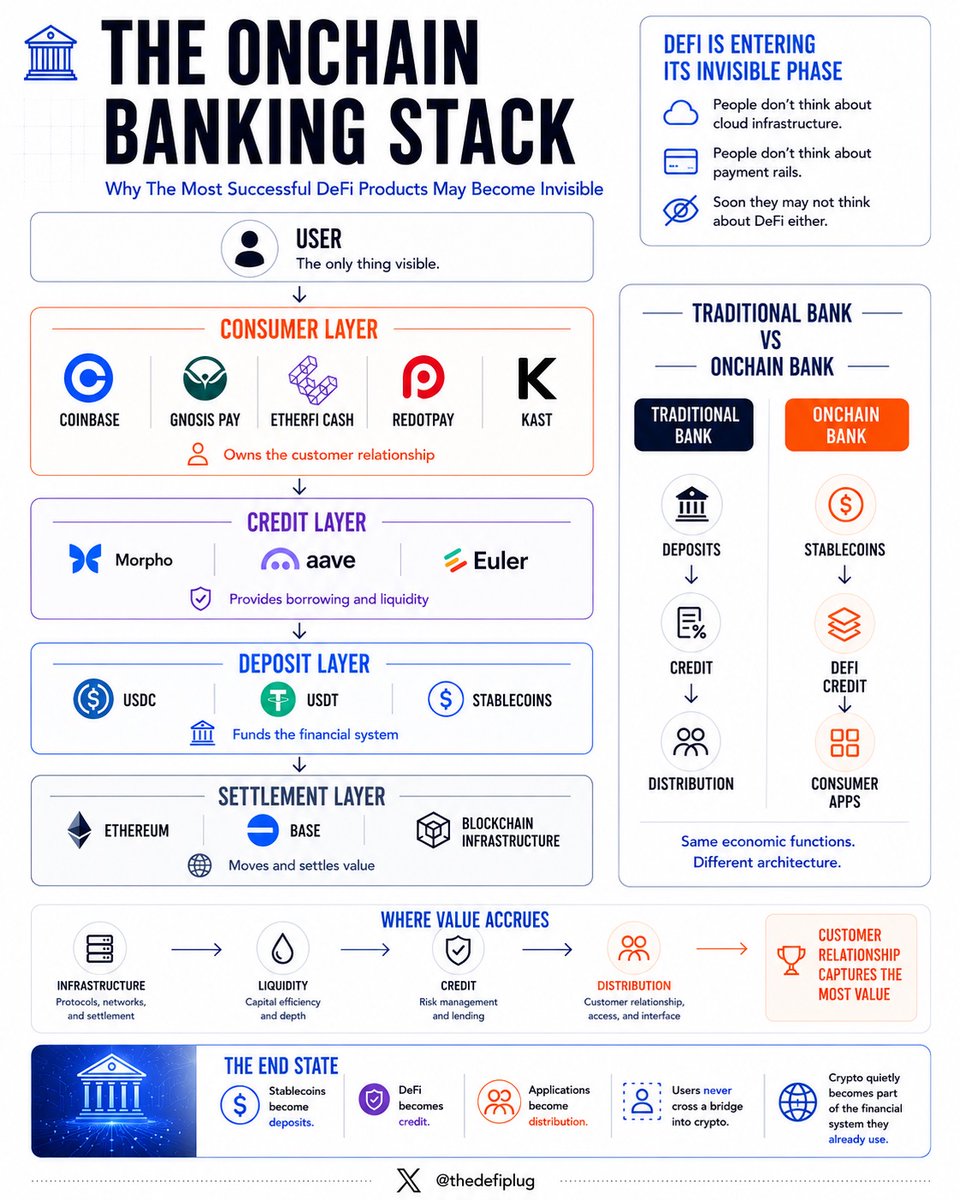

One of the recurring patterns in technology is that adoption often arrives after the technology becomes invisible.

People do not think about cloud infrastructure when opening an app.

They do not think about payment rails when tapping a card.

The underlying system disappears.

Only the experience remains.

DeFi may be entering a similar phase.

For years, the industry assumed mass adoption would require millions of users learning wallets, lending protocols, and on-chain infrastructure.

What if the opposite happens?

What if the infrastructure moves underneath the users?

● Stablecoins Became The Deposit Layer

Every banking system begins with deposits.

Crypto’s version is stablecoins.

Despite a significant drawdown across broader crypto markets, stablecoin supply surpassed $323B by early 2026 and continued growing.

That resilience matters.

USDC and USDT increasingly function as digital deposits for an emerging financial system.

People use them to save, settle transactions, and move money globally.

Stablecoins are no longer just a crypto product.

They are becoming the funding layer for a new banking stack.

● DeFi Finally Found Distribution

For most of its history, DeFi struggled with distribution.

The products existed.

The users did not.

➢ @aave proved users would borrow on-chain.

➢ @Morpho showed lending infrastructure could become modular.

➢ @eulerfinance rebuilt lending around isolated risk and customizable markets.

The technology worked.

Distribution remained the bottleneck.

That is why the Coinbase-Morpho integration is important.

Not because it launched another lending product.

Because it demonstrated a new architecture.

The user borrows through Coinbase.

Morpho provides the lending infrastructure underneath.

The complexity disappears.

The customer never needs to understand vaults, liquidity pools, or smart contracts.

They simply borrow.

● The New Banking Stack Is Already Visible

The pieces are increasingly falling into place:

➢ Stablecoins provide deposits

➢ Morpho, Aave, and Euler provide credit

➢ Coinbase provides distribution

Viewed separately, these look like different sectors.

Viewed together, they increasingly resemble a banking stack.

Not a bank in the traditional sense.

A collection of specialized infrastructure layers performing the same economic functions.

The protocol provides liquidity.

The application owns the interface.

The distributor owns the customer relationship.

Historically, the customer relationship captures the most value.

● The Consumer Layer

The trend extends beyond lending.

➢ @gnosispay is building self-custodial card infrastructure.

➢ @ether_fi Cash is turning staking balances into spendable purchasing power.

➢ @RedotPay and @KASTxyz are building stablecoin-native financial products for everyday users.

At first glance, these look like separate businesses.

They are not.

They are all competing to become the consumer-facing layer for the same underlying financial system.

The user sees a card, a loan, or a savings product.

Underneath, stablecoins and DeFi infrastructure increasingly handle settlement, liquidity, and credit.

● The End State

The original vision of DeFi imagined users leaving traditional finance.

The emerging version looks different.

➢ Stablecoins become deposits.

➢ Morpho, Aave, and Euler become credit markets.

➢ Coinbase, Gnosis Pay, EtherFi Cash, RedotPay, and KAST become distribution.

The user never crosses a bridge into crypto.

Crypto quietly becomes part of the financial system they already use.

And if that happens, the most successful DeFi products may be the ones nobody realizes are DeFi at all.

24

13

37

4,008