Learner | Investor | Traveller | Fitness

Joined January 2011

- Tweets 26,541

- Following 216

- Followers 8,222

- Likes 29,618

1,982 Photos and videos

Pinned Tweet

Mar 14

The market hasn't been oversold this bad since COVID crash of 2020. Arguably market was not expecting another war and it is getting priced in. No one knows, what will be the consequences of US Iran conflict and when will the Crude price stabilize?

Similar sentiments were there in 2020, when global lockdown happened during Covid. That time it seemed most businesses would shut or report huge losses. What actually followed was longest bull run in recent times, exceeding the expectations of all and sundry.

Those who were pessimistic paid huge opportunity cost that time.

Stock price would always follow the earnings growth momentum, come want may. With at least 2 year time frame, this fall is another great opportunity to accumulate quality companies with PEG ratio of around 0.5. Many opportunities exist in this range today.

Lastly, I will not be biased this time that only small caps can generate alpha. I am not ignoring quality mid and large caps.

1

1

20

6,534

Tushar Sarkar retweeted

GADKARI APPROVES LEGAL USE OF 100% ETHANOL, CALLS IT A MAJOR ALTERNATIVE TO PETROL

INDIA CLEARS 100% ETHANOL FUEL AS AUTOMAKERS PREPARE TO LAUNCH COMPATIBLE VEHICLES

TOYOTA, SUZUKI, HYUNDAI AND MG TO ROLL OUT 100% ETHANOL-COMPATIBLE CARS AFTER POLICY APPROVAL

166

102

1,106

202,314

Very insightful podcast on micro cap investing framework and on investing psychology by @Apurva1406

youtu.be/Y0UBr5MopQQ?si=sxmC…

6

1,390

Jun 10

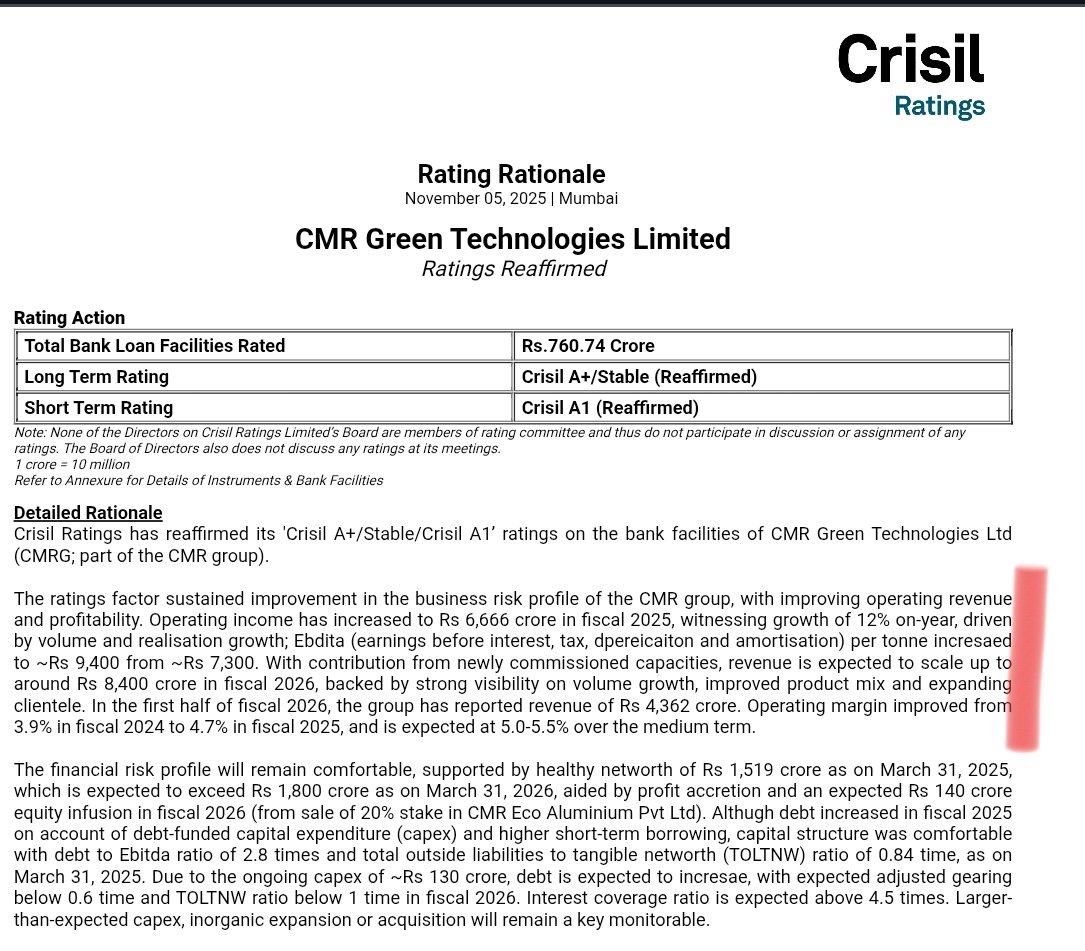

CMR Green Technologies 9MFY26 revenue is ₹6,275.52 crore and PAT of ₹162.39 crore. EBITDA margin at ~5.1%.

Crisil report implies, Q4 revenue will be ~₹2,125 crore (as full year is expected to be ₹8,400 crore).

Jun 10

CMR Green Technologies

#CMRGreen

Listed today at 268Rs vs issue price of 192rs

Closed at 241Rs

Q4FY26 yet to be declared

CRISIL report points to strong Q4FY26

Was oversubscribed crazily

Valuations were reasonable vs peers

Listed with a big premium of 43% and witnessed a sharp profit booking after listing

Block deal:

Goldman Sachs India Equity Portfolio buys 19,41,018 shares at 256.64Rs

Strong anchor names in IPO

CRISIL rating expects a good FY26 growth

Expects FY26 revenue to be at 8400cr

EBITDA/ton increased from 7300 Rs to 9400 Rs

Expects margins to expand gradually going forward and expects margins to reach 5-5.5% in medium terms

Return ratios should progressively get better

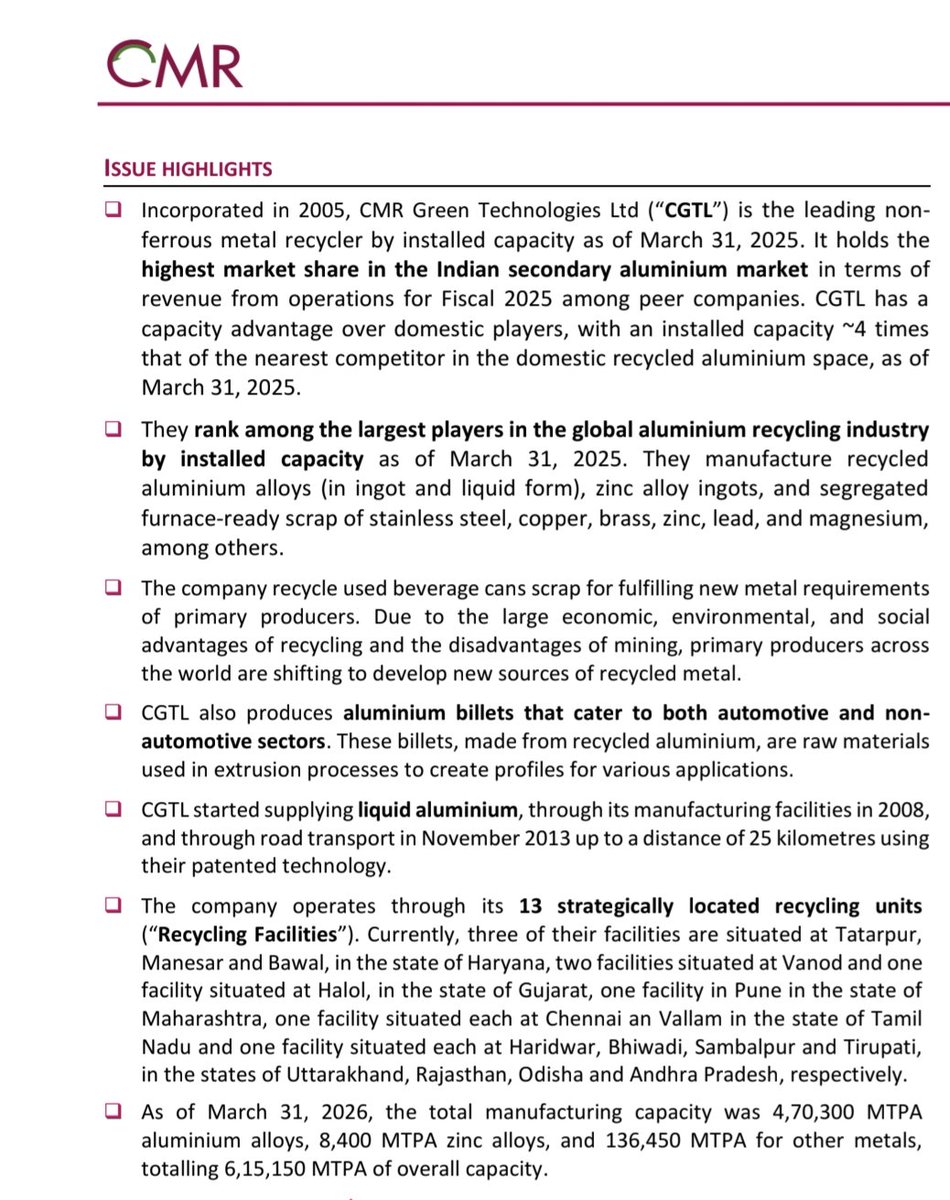

Leading non ferrous metal recycler by installed capacity

Highest market share in Indian secondary Aluminium market in terms of revenue

Has big capacity advantage vs peers

Installed capacity of 4x over the nearest competitor in recycled aluminium market

Provides aluminium billets that cater to automotive and non automotive sectors

6,15,150 MTPA overall capacity

13 recycling units

1

1

14

2,480

Jun 13

CMR Green Technologies

> Largest Capacity of 6 lakh MTPA.

> Only player with multiple Japanese joint venture partners.

> Largest player in liquid aluminium category. Supply requires plants to be situated within ~25 km of the customer

Risk ~ Raw material price volatility

Jun 13

Aluminium used to Each-every industry 🔖

Aerospace sector ~60-70% uses

4W & EV ~30-50% aluminium composite used

2W & EV ~Typically account of 12-31% of the total weight

Consumers electronic & Drone ~6-12% of the product total mass

Armoured Vehicles & Tanks: Aluminium plating is used extensively to reduce total combat weight by 25% to 40%.

Server Racks & Cabinets: Aluminium extrusions are used in roughly 30-40% of structural containment units because they are non-magnetic and dissipate heat efficiently.

Heat Sinks & Thermal Management: Accounts for 50-60% of specific thermal module assemblies for high-wattage GPUs.

AI controls smelters to reduce energy consumption by **up to 95 and optimize alloy compositions by lowering correction material needs by **30% to 50%.

Second precious metal after copper .

The world's aluminum needs cannot be met through mining alone.

Last option is "Recycling industry"♻️♻️

#Aluminum #Recyling #Baheti

1

4

621

Jun 13

Corporate earnings to GDP ratio is another macro parameter which is on the rise since 2020 after a tepid decade (2009-2020).

This cycle is expected to continue with govt focus on capex across multiple sectors.

Nifty 500 corporate profit/GDP ratio surged to an all time high of 5.2% in FY26

This is a major milestone, as corporate profitability has now surpassed the previous peak of 5.2% seen in FY08

Corporate profits grew 15.6% YoY in FY26 while Nominal GDP grew 8.9% YoY in FY26

The key point is that corporate profit growth continues to outpace nominal GDP growth

The journey has been quite interesting

From 5.2% in FY08, the ratio declined consistently & bottomed at 2% in FY20

src : MOFSL

2

12

1,058

May 11

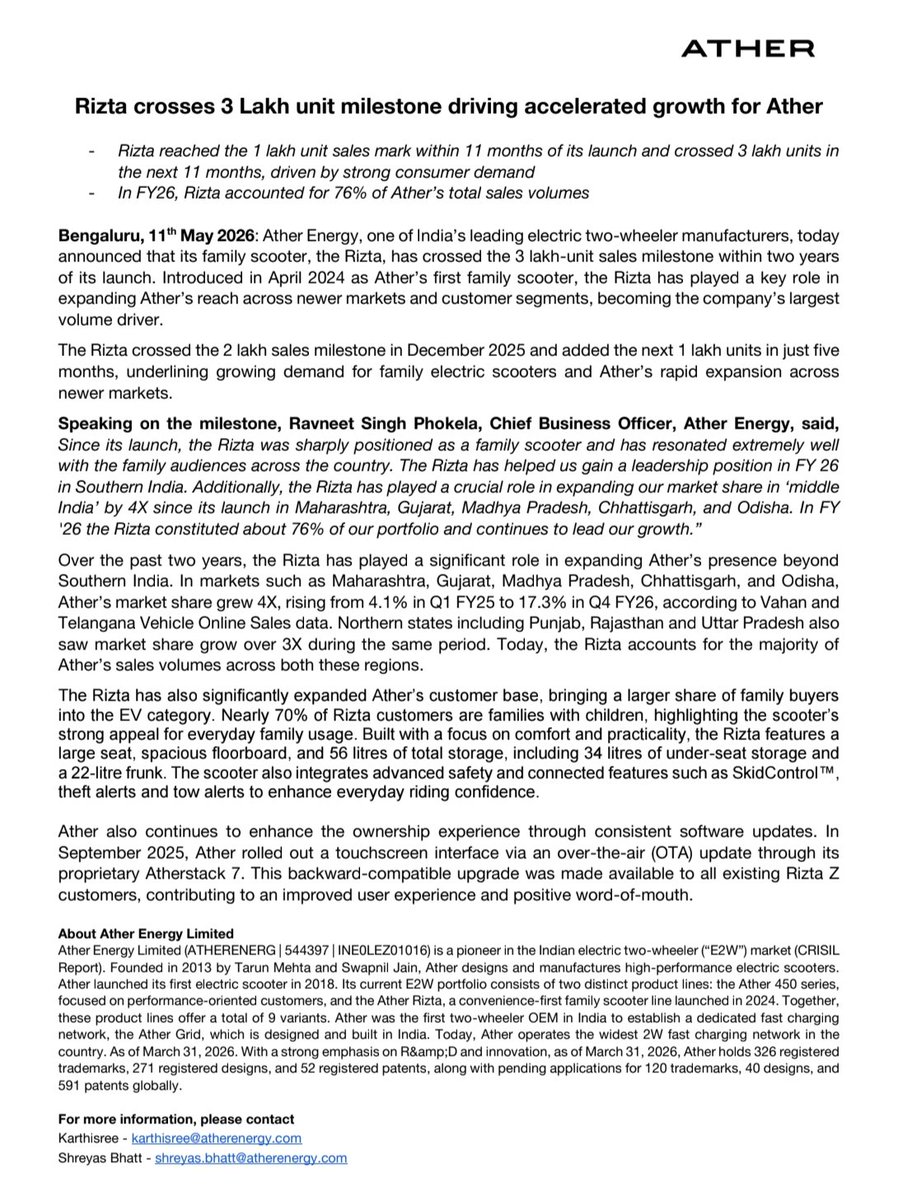

Ather Energy Ltd.

> Rizta sold 3 lakh units in 2 years, launched April 2024

> Rizta sales form 76% of total volumes in FY26

> Market share expanded significantly in mid and northern India

> Family scooter appeals to households with comfort features

Ather Energy is literally on a dream run

Market share has expanded from 8% to 19% in Q4

Never ignore market share gains.

2

3

24

3,163

Jun 13

Ather Energy board approves Rs 2,500-crore fundraising plan

m.economictimes.com/tech/tec…

3

297

Jun 13

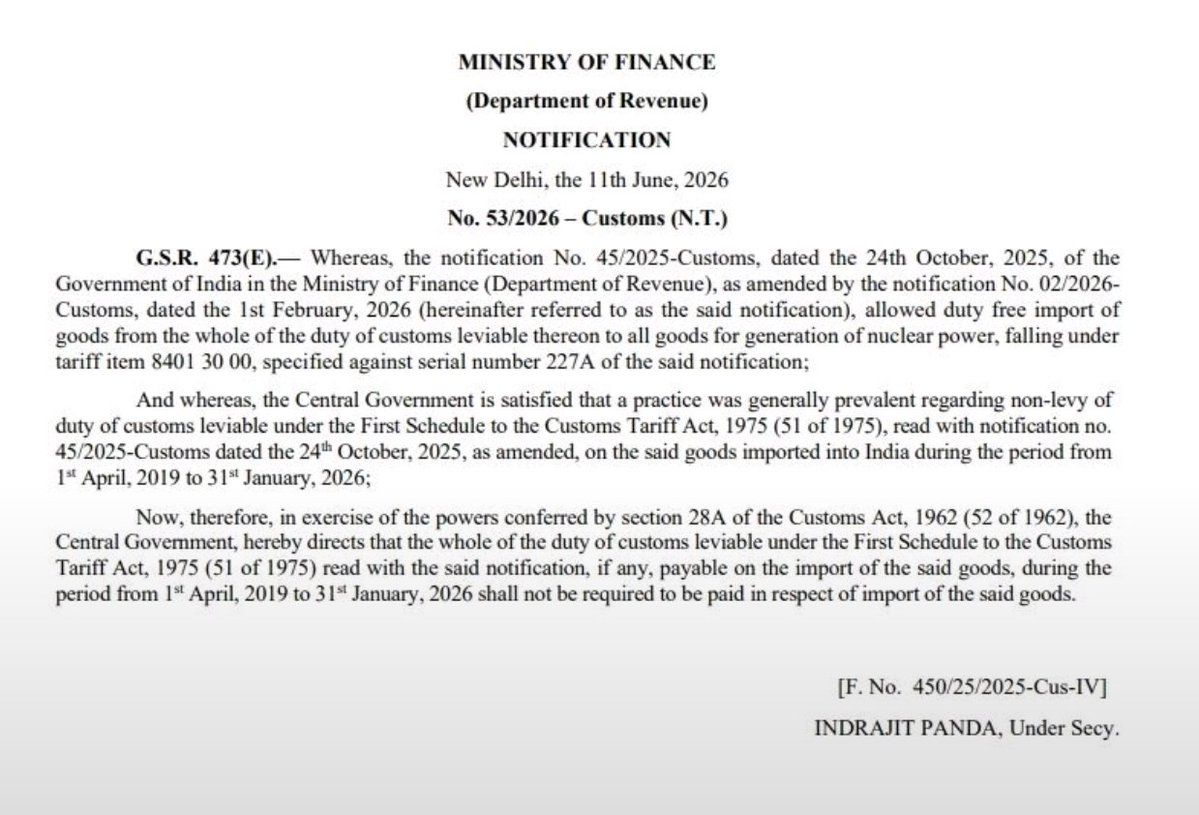

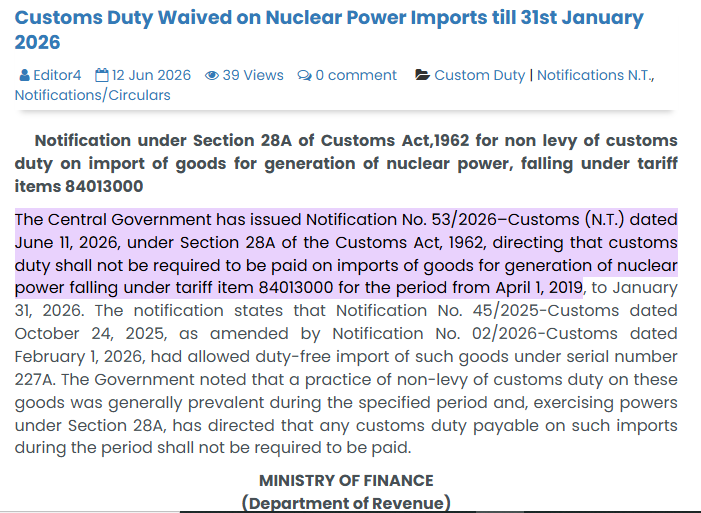

Ministry of Finance has waived off duty on specified nuclear power goods imported Apr '19-Jan '26.

Good article on what will be the implications and which players will benefit from this.

Jun 12

India just made nuclear power equipment imports tax-free, backdated seven years to April 2019.

Read that again. The government went back in time to erase a tax.

No government cleans up seven-year-old liabilities without a reason.

So, which market opportunities should we watch out for? Here is the full value chain, top to bottom…

1/12

1

20

2,313

Tushar Sarkar retweeted

Nifty 50 PE ratio today is at 19.98 times which Below average range of its trading history.

Data from @stockscansin

20

27

481

43,997

Jun 12

Today was a unique and remarkable day as 100% of PF stocks closed positive

Jun 12

Portfolio companies that are significantly up today (> 2%)

BSE

Raymond Realty

Senores Pharma

Kernex Micro

Skygold

Sansera Engineering

Shree Refrigerations

FCL (added this week)

Northern Arc

Vidya Wires

OBSE Perfection

Hind Copper

10

2,017

Jun 12

Portfolio companies that are significantly up today (> 2%)

BSE

Raymond Realty

Senores Pharma

Kernex Micro

Skygold

Sansera Engineering

Shree Refrigerations

FCL (added this week)

Northern Arc

Vidya Wires

OBSE Perfection

Hind Copper

5

5

84

11,221

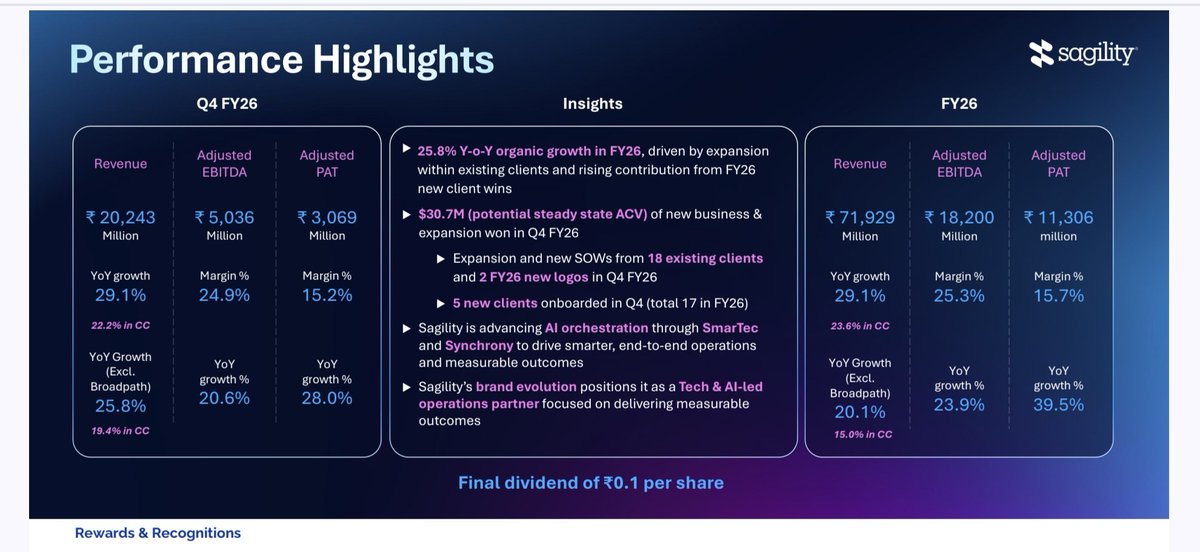

May 8

Sagility

Strong Q4 results are expected on 12 May, stock price has moved well from 41 levels.

Company is healthcare-focused technology-enabled solutions and services primarily to U.S.-based clients in the payer and provider segments.

Mar 28

Some more companies that I am studying and tracking

JNK India

Sagility

Redington

2

13

2,178

May 12

Sagility

Very good Q4FY26 nos. YoY basis

🔹Revenue 2049 crore, ⏫ 29%

🔹PAT 257.7 crore, ⏫41%

🔹QoQ almost flat, margin slightly down

2

3

653

Jun 12

Sagility Ltd

Step down subsidiary acquires US-based healthcare analytics firm CareSeed.

CareSeed specializes in HEDIS reporting, medical record review, and regulatory analytics. It serves 30 US payers, with strong Medicare Advantage presence

Acquisition expands Sagility's healthcare quality and Al capabilities.

260

Jun 11

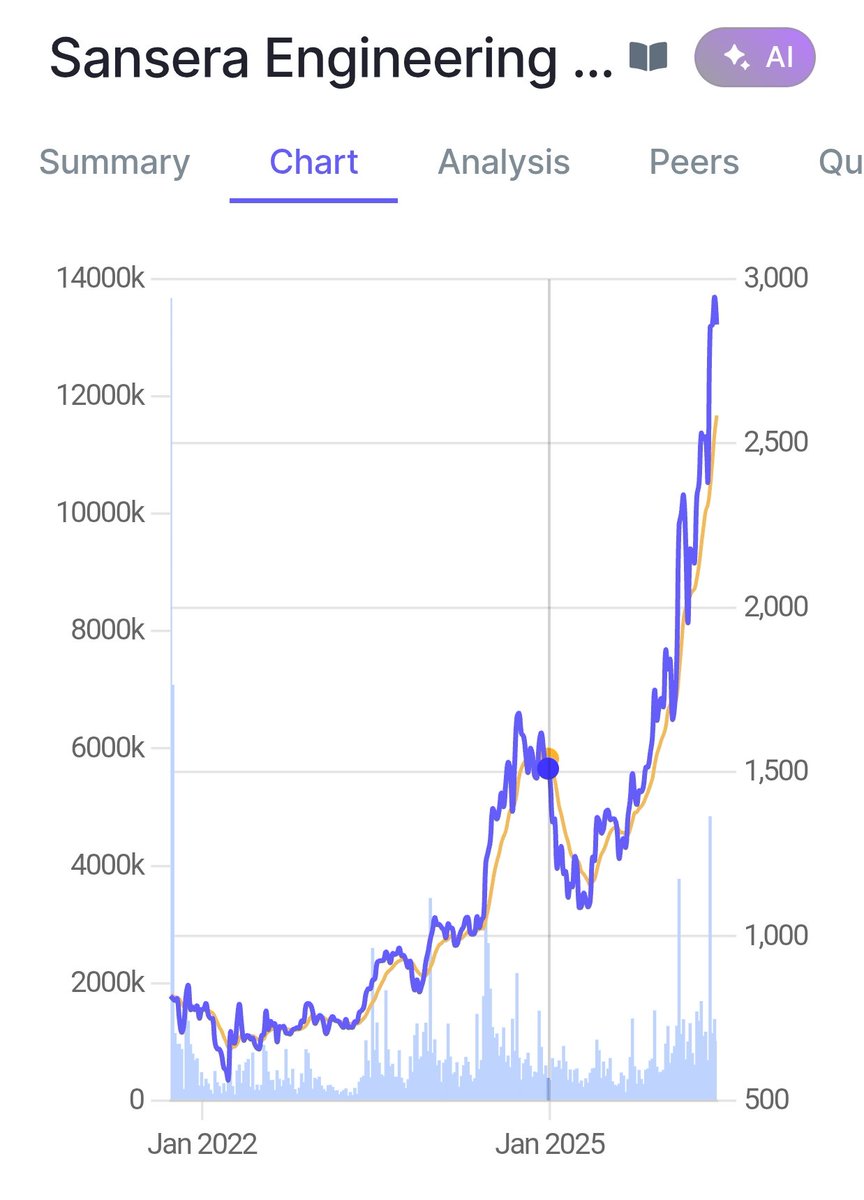

Sansera Engineering

Good article to understand the company & it's road ahead

Sansera Engineering: FY27 Could Be an Inflection Year

Sansera Engineering delivered its strongest year ever in FY26, but the bigger story lies ahead.

Here's everything you need to know about why FY27 could be an inflection year for Sansera Engineering.🧵👇

1

1

38

3,786

Jun 11

Football World Cup starts in next few hours. Probably last time to see the legends play.

6

615

Jun 11

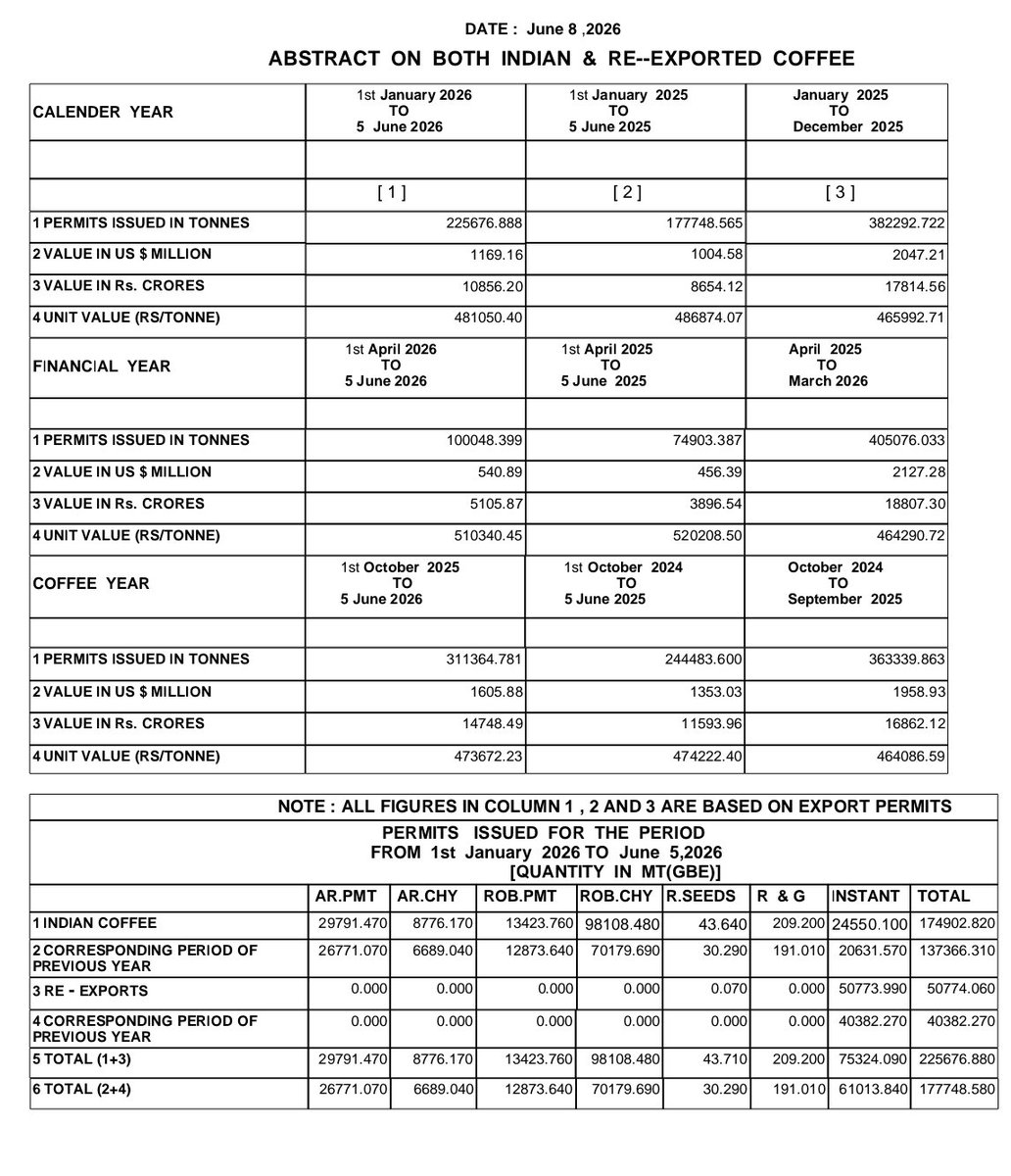

Vintage Coffee bulk deal

SBI Fund Management bought almost 85 crore (~55.3 lakh shares) worth of stake today at 153.3 and 158

@Financially_In

@YourShami @Asset_Architect

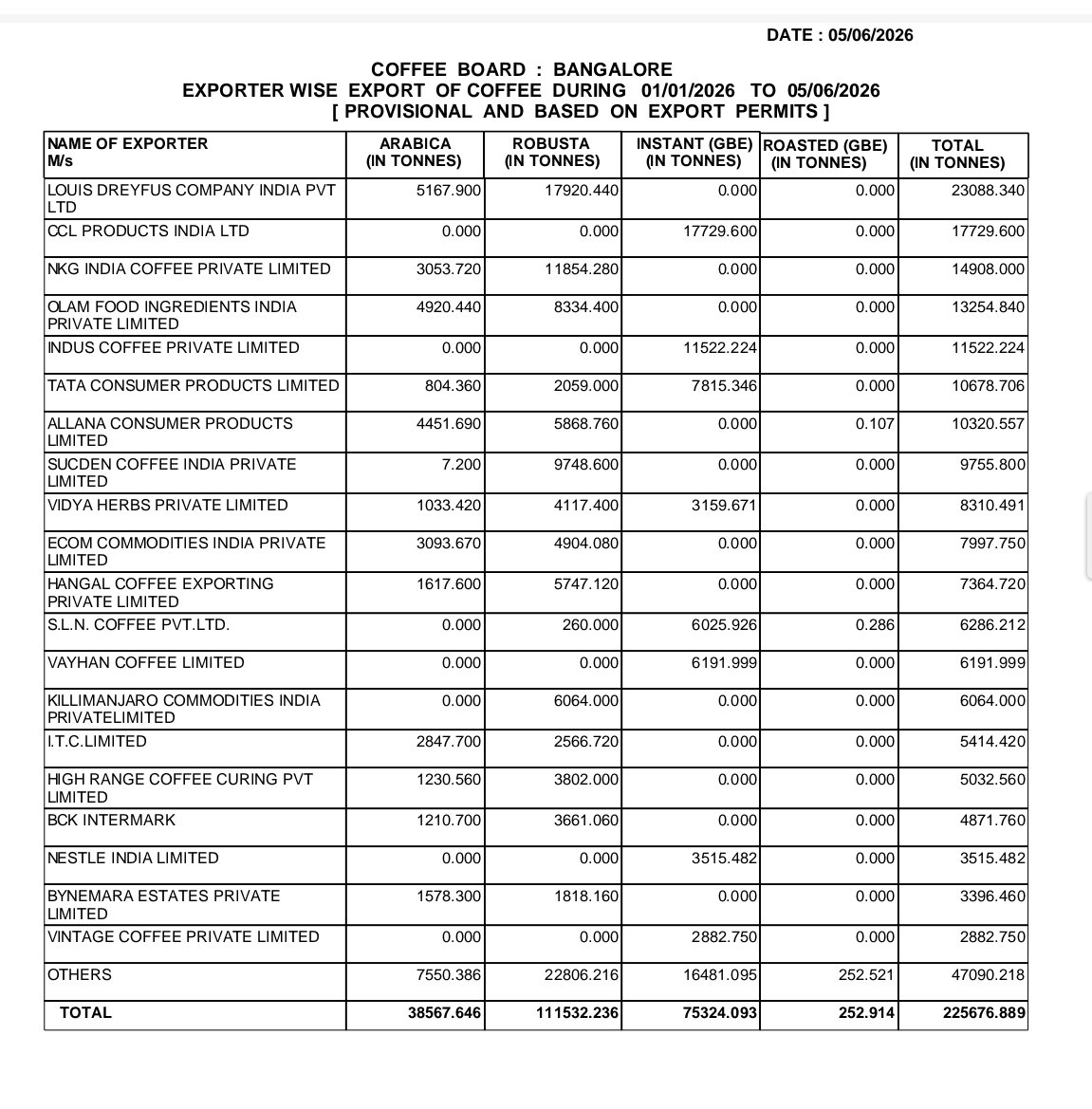

Jun 10

Vintage Coffee and Beverages

Export data released till 5 June also suggests strong growth YoY

2

3

35

3,526

Jun 11

Hospital Index on the rise

Fastest growing in mid and small cap space

> Yatharth Hospital

> Park Medi World

> Artemis

> Asarfi Hospital

> Unihealth Hospital

Large cap

> NH

> Maxhealth care

> Fortis

> Apollo

The Hospital Index is starting to move into Stage 2

It remains one of the recession-proof themes out there.

Source - @stockscansin

Link - stockscans.in/charts/PCI:HOS…

1

5

42

3,716

Jun 10

Pharma Sector is going to double as India cements it's position in CDMO and CRDMO space.

Tracking and invested in some

Kwality Pharma

Senores

SGRL

Sakar Healthcare

Gujarat Themis

Concord Biotech

Solara Active

Jun 9

Indian Pharma: $60B → $120B Opportunity in 5 Years

Commerce Minister Piyush Goyal expects India's pharmaceutical industry to grow from ~$60 billion to $120 billion over the next five years.

Growth is expected to be driven by innovation, higher-value products, and alignment with global manufacturing standards, rather than just volume expansion.

Government is pushing pharma companies to move beyond low-cost generics and invest in innovative drugs, complex formulations, specialty therapies and biopharmaceuticals.

India already supplies 65-70% of WHO vaccine requirements, 10 out of 25 largest generic companies operate from India, and highest number of US FDA-approved plants outside the US.

Despite tariff concerns and geopolitical shifts, India remains one of the fastest-growing pharmaceutical exporters globally.

Beneficiaries -

Large Pharma:

=> Sun Pharmaceutical Industries

=> Dr. Reddy's Laboratories

=> Cipla

=> Lupin

=> Aurobindo Pharma

CDMO / CRAMS

=> Divi's Laboratories

=> Syngene International

=> Sai Life Sciences

=> Suven Pharmaceuticals

Biologics/Innovation

=> Biocon

=> Gland Pharma

API & Specialty Chemicals

=> Laurus Labs

=> Neuland Laboratories

=> Granules India

=> Solara Active Pharma Sciences

India's pharma industry is entering a multi-year growth cycle driven by innovation, biologics, exports and global supply-chain diversification, creating a credible pathway to double from $60 billion to $120 billion by FY31. 🔥

🔍Do add companies which you feel like can be benefitted.

Follow @DhawalDoshi5 for more updates.

@vishan_29 @Anvith_ @TrendSpark420 @InvestmentVeda @Dynamicinvstr

2

3

45

4,007

Jun 11

Pharma sector is now core focus sector for govt

Jun 10

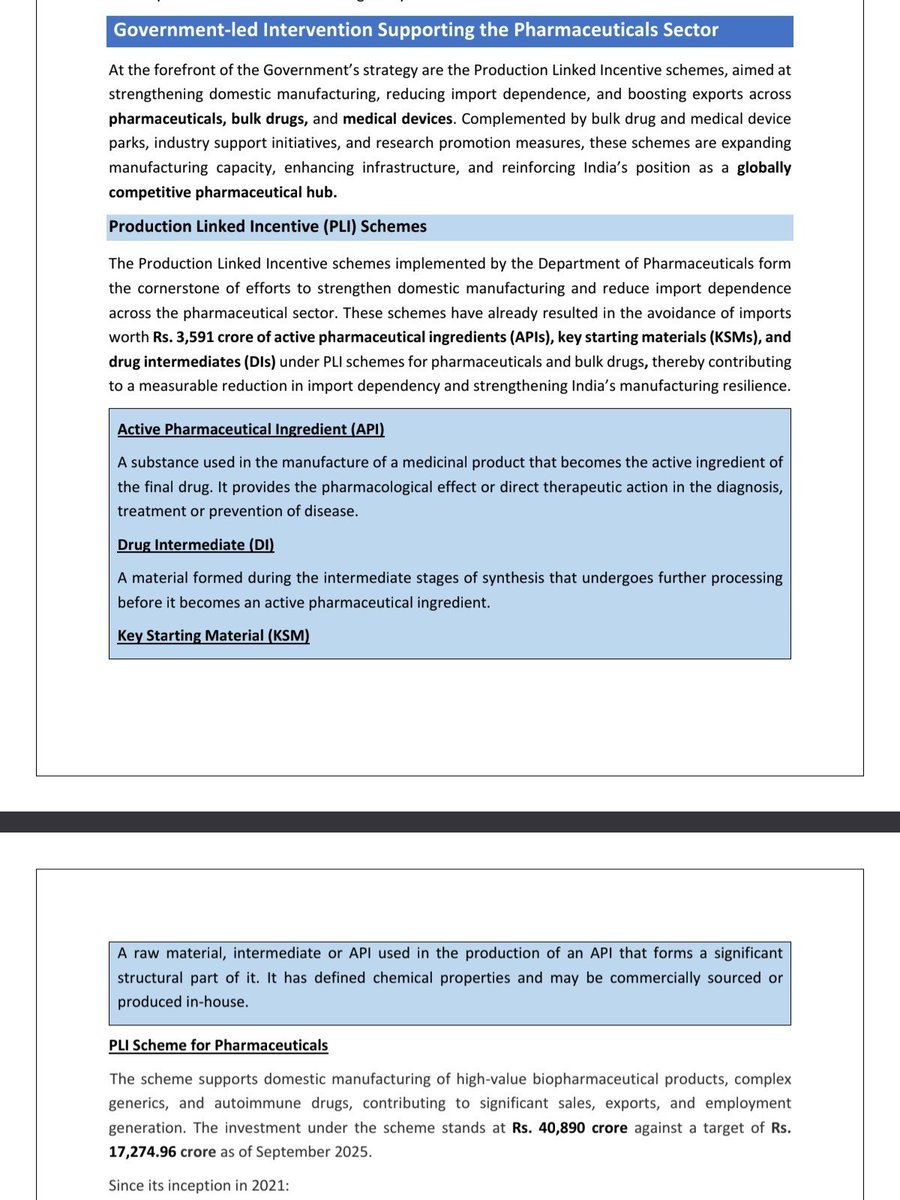

Govt led intervention supporting the Pharma industry 🧐

•PLI Scheme:- These schemes have already resulted in the avoidance of imports

worth Rs. 3,591 crore of active pharmaceutical ingredients (APIs), key starting materials (KSMs), and

drug intermediates (DIs) under PLI schemes

• PLI Scheme in medical devices;- The cumulative sales under the scheme stand at Rs. 12,344.37 cr,including exports worth Rs.

5,869.36 cr

•Biopharma shakti:- to be launched with on outlay of 10,000 cr over next 5 years

•medical device Park :-The total project cost of these Parks is ₹871.11 crore, with a Central grant-in-aid of

₹100 crore each for the creation of common infrastructure facilitie

#CDMO #API #Pharma #Medicaldevice

1

731

Tushar Sarkar retweeted

Jun 10

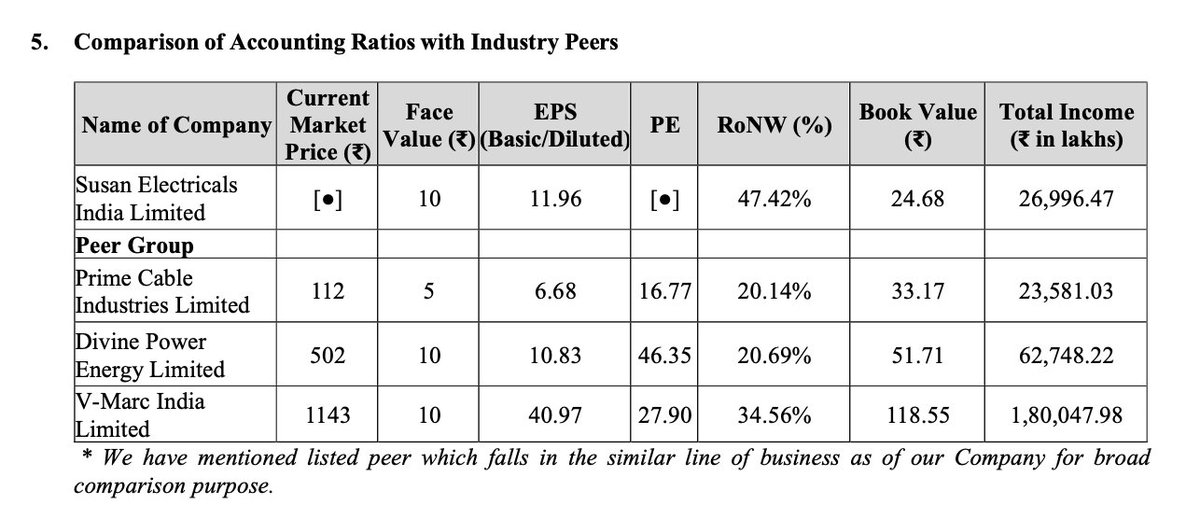

Susan Electricals India IPO - 📅 IPO Opens: 11 June 2026

■ About the Company

Susan Electricals India is engaged in manufacturing aluminium and copper-based electrical winding wires, conductors and cables used across power transmission, power distribution, industrial infrastructure and utility applications.

The company's product portfolio includes:

▪ Low Tension (LT) Cables

▪ High Tension (HT) Cables

▪ Medium Voltage Covered Conductors (MVCC)

▪ Winding Aluminium Wires & Strips

▪ Winding Copper Wires & Strips

▪ Aluminium Conductors

The company operates 3 manufacturing facilities located in Ghaziabad, Uttar Pradesh and has established its presence across 14 states and 1 union territory.

Its products are used in electricity distribution networks, utility projects, industrial installations and power infrastructure projects, making it a direct beneficiary of India's ongoing power sector expansion.

■ Peers

▪ Prime Cable Industries

▪ Divine Power Energy

▪ V-Marc India

▪ JD Cables

These companies operate in similar segments of wires, cables and conductors.

■ Industry Opportunity

The Indian Wires & Cables market is expected to grow from approximately USD 10.32 Billion in 2025 to USD 22.35 Billion by 2035.

Key growth drivers include:

▪ Expansion of transmission & distribution infrastructure

▪ Rising renewable energy installations

▪ Smart grid investments

▪ Urbanization and housing demand

▪ Industrial capex cycle

▪ Data center infrastructure

▪ Railways and metro projects

▪ RDSS scheme

▪ Saubhagya 2.0 electrification initiatives

Government spending on power infrastructure and distribution network strengthening is expected to support long-term demand for conductors, cables and winding wires.

■ Manufacturing Footprint

The company currently operates three manufacturing facilities in Ghaziabad, Uttar Pradesh.

Current installed capacity includes:

▪ 3,307.5 TPA of winding aluminium/copper wires and strips

▪ 7,500 KM per annum of HT, LT and MVCC cables

The company has also received BIS certifications and ISO certifications for quality management, environmental management and occupational health & safety standards.

■ Capacity Expansion

A major portion of IPO proceeds will be used towards expansion of the existing manufacturing facility.

Expansion includes:

▪ Installation of 6–33 KV Triple Layer CCV Line

▪ Installation of rigid stranding machines

▪ Additional manufacturing shed

▪ Supporting infrastructure development

Management is focusing on expanding HT Cable and MVCC Cable capacity, which are relatively higher-value products and are witnessing increasing demand from utility and infrastructure projects.

This expansion can improve both scale and product mix going forward.

■ Financial Performance

Revenue From Operations (FY26)

₹269.36 Cr

Revenue has grown nearly 2.6x in just two years.

PAT (FY26)

₹18.25 Cr

PAT has increased almost 24x over the last two years.

EBITDA (FY26)

₹32.08 Cr

EBITDA has expanded significantly, reflecting strong operating leverage and improving scale benefits.

EBITDA Margin (FY26)

11.91%

Margins have consistently improved due to better product mix, higher manufacturing contribution and operating efficiencies.

PAT Margin (FY26)

6.77%

ROE

64.64%

ROCE

29.05%

The company has demonstrated strong profitability improvement while maintaining high return ratios.

■ Customer Diversification Improving

One positive trend is the reduction in customer concentration.

Contribution from Top 10 Customers:

FY24: 98.0%

FY25: 95.9%

FY26: 63.7%

While concentration remains a risk, the company has significantly diversified its customer base over the last two years.

■ Why Is Expansion Important?

The company recently entered newer product categories such as:

▪ High Tension Cables

▪ MVCC Cables

During FY26, the company generated revenue from these newly introduced products and management intends to further scale these businesses through capacity expansion.

If executed well, these segments can become meaningful growth drivers in the coming years.

■ Utilization Of IPO Proceeds

IPO proceeds will be utilized towards:

▪ Manufacturing capacity expansion

▪ Working capital requirements

▪ General corporate purposes

Working capital support is important because the business is heavily dependent on copper and aluminium inventories.

■ Key Risks

▪ Customer concentration still remains elevated

▪ Raw material price volatility in copper and aluminium

▪ Working capital intensive business model

▪ Execution risk in planned expansion

▪ Competitive industry with larger established players

▪ Demand slowdown in infrastructure spending can impact growth

■ Final View

Susan Electricals is a rapidly growing wires & cables company operating in a sector that is expected to benefit from India's long-term power infrastructure, transmission, distribution and electrification growth.

The company has delivered strong revenue growth, sharp margin improvement, robust profitability growth and healthy return ratios. Capacity expansion into HT and MVCC cables, improving customer diversification and favorable industry tailwinds further strengthen the investment case.

Investors should monitor valuation, customer concentration and expansion execution, but operationally the company appears well positioned to participate in India's growing power infrastructure opportunity.

Disclaimer:

This post is for educational and informational purposes only and should not be considered as investment advice or a recommendation to apply for the IPO.

Apr 8

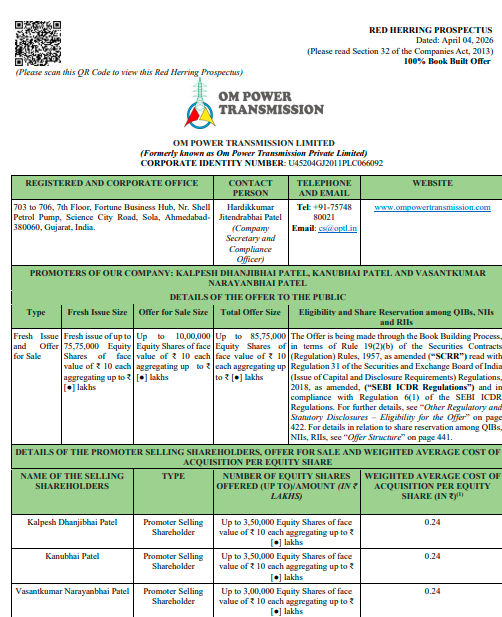

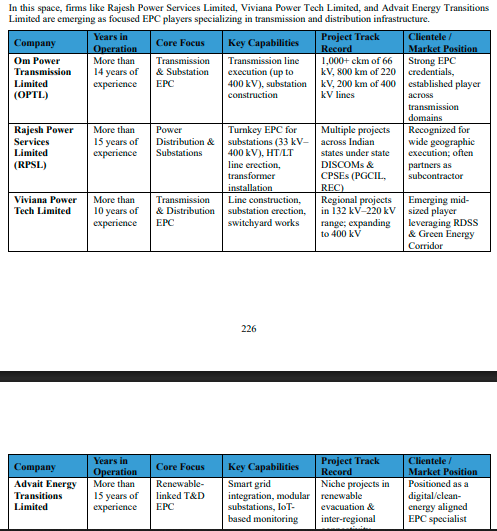

After names like Rajesh Power, Advait Energy, and Viviana Power, a new Power T&D EPC player - Om Power Transmission - is getting listed, adding another emerging company to this fast-growing segment ⚡🔥

Om Power Transmission Limited, an EPC-focused infrastructure company operating in India’s fast-growing power sector has come up with an IPO.

Business Profile

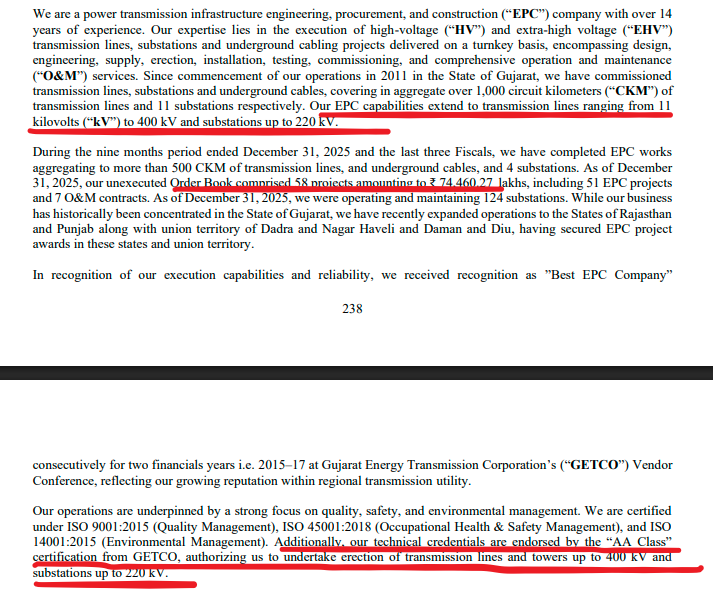

Om Power Transmission is a power transmission EPC company engaged in execution of high voltage (HV) and extra high voltage (EHV) transmission lines, substations, and underground cabling projects.

Om Power Transmission operates on a turnkey EPC model, undertaking end-to-end project execution from design to commissioning, after which it also offers separate O&M services for maintenance and operation of infrastructure.

Working capital heavy model

EPC requires:

Material procurement upfront

Delayed payments from clients (mostly PSU)

👉 This leads to high receivables cash flow pressure

Work

Design & engineering

Procurement of materials

Erection & installation

Testing & commissioning

Operation & maintenance (O&M)

Its execution capabilities span:

Transmission lines: 11 kV to 400 kV

Substations: up to 220 kV

Underground cabling: HV & EHV networks

Since inception, the company has:

Executed 1000 CKM transmission lines

Delivered 11 substations

Key Business Vertical Breakdown:

1. Transmission EPC (core revenue driver)

2. Substation EPC (AIS GIS with SCADA integration)

3. Underground cabling

4. O&M services (124 substations under management as of Dec 2025)

Business Nature Insight:

1. Project-based revenue model

2. High working capital intensity

3. Execution efficiency = key profitability driver

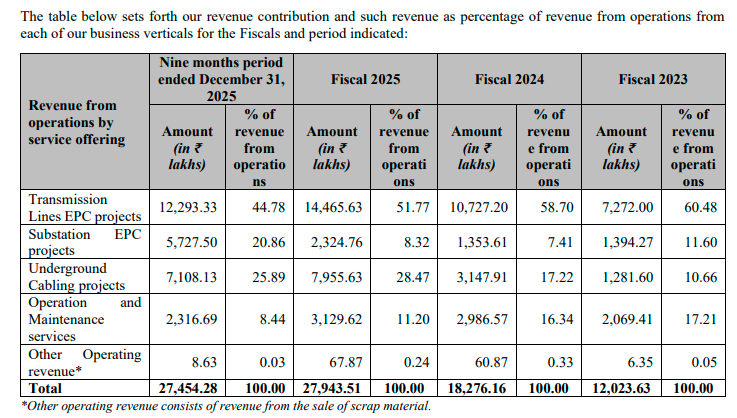

Revenue Mix & Client Profile

Segment-wise (9MFY26):

Transmission: 44.8%

Underground: 25.9%

Substation: 20.9%

O&M: 8.4%

Customer Type:

Public sector: 87.5%

Private sector: 12.5%

Client Concentration:

Top client: ~50–72%

Top 10 clients: ~95–98%

Key Clients & Dependency

Major exposure to state utilities / public sector clients

Extremely high client concentration:

Top client contributes a very large portion of revenue

Top 10 clients = almost entire business

👉 Real Meaning:

Business is relationship-driven

Order inflow depends on:

Government spending

Tender wins

Order Book Strength

Order book: ~₹744.6 Cr (Dec 2025)

Projects: 58

Mix:

Transmission: 69.7%

Substation: 22.7%

Underground: 3.9%

O&M: 3.7%

👉 Strong visibility, but heavily skewed towards transmission EPC.

Geographical Presence

Core market: Gujarat (79% order book)

Expanding to:Rajasthan

Punjab

Dadra & Nagar Haveli

📌 IPO Structure

Total Issue: ~85.75 lakh shares

Fresh Issue: 75.75 lakh shares

OFS: 10 lakh shares (by promoters)

👉 Interpretation:

Majority fresh issue → growth-focused

Small OFS → promoters not exiting aggressively

IPO Details

IPO Size: ~₹150 Cr

Fresh Issue: ~₹133 Cr

Listing Date: 17 April 2026

Use of Funds:

Capex (machinery & equipment)

Debt repayment

Working capital

General corporate purposes

Growth Strategy

Management is focused on:

1. Expanding beyond Gujarat → Pan-India presence

2. Targeting large and complex EPC projects

3. Improving: Execution efficiency Cost control

4. Scaling capabilities in high voltage transmission infra

Peers

As per the RHP, the company has considered peers such as Rajesh Power, Advait Energy, Viviana Power, and other similar EPC players operating in the power transmission and distribution segment.

Key Takeaways (Important for Investors)

Operating in high-growth sector (power transmission infra)

Strong execution experience but still small player

Heavy dependence on: Government clients Limited customer base

Growth will depend on:

1. Order inflow

2. Execution capability

3. Capital efficiency

Disclaimer: This post is for educational and informational purposes only and should not be considered as investment advice. DYOR.

2

5

33

7,098

Tushar Sarkar retweeted

Jun 10

In public markets, seasoned generalists — those who understand fundamentals, technicals, and sentiment — tend to generate the highest time-adjusted ROCE at the portfolio level. Subject matter experts, by contrast, extract their best returns in private markets and consulting, where they're paid by the hour rather than the market's mood.

That distinction matters. Public markets are a multi-layered lock — behind every business is a stock, behind every stock is a price, and behind every price is an emotion. No single key opens all three. Consistent profitability demands sharp focus on every layer, simultaneously. #SDW

1

6

31

3,473

Tushar Sarkar retweeted

Jun 10

Vintage wasn’t on the list of exporter as it was not in top 20 exporters.

Although we can measure the QOQ growth.

In the earning management said Q1 volume s was 1900 MT ,from the coffee board of India you will get roughly 1750 MT.

There will always be some difference in data as coffee board shows data for the permits issued.

Now till June 9 the export volume is about 3155 MT. If you deduce the first 3 month data you will have roughly 1450 and extrapolate it to June 30 , you will get 1941 MT, let’s assume the sale volume is higher than the permit volume as it was the case last Quarter. Of we go with 2000 MT volume with same realisation , the sales no is about 171 cr , considering 5% domestic sales.

This will give you a YOY sales growth of 70%.

1

1

8

947