Yes hello

Joined March 2024

- Tweets 31,445

- Following 618

- Followers 1,847

- Likes 42,177

5,363 Photos and videos

Pinned Tweet

3 Feb 2025

The arc of history is long and it bends towards the vindication of @PeterSchiff

3 Feb 2025

SPOT GOLD HITS RECORD HIGH AT $2,818.27 PER OUNCE

3

1

28

17,190

Valco retweeted

Jun 16

the first guy to ever have a trillion dollars makes his second trillion on his 4th day as a trillionaire.

391

1,691

110,408

5,457,009

Valco retweeted

Since I'm once again being lectured for not just buying tech during an energy crisis, I'd like to post this chart. When the war started the semi index was worth 155x the energy index. Today it's worth 255x.

Anyone who think's that's sane, isn't.

5

1

39

1,959

RT @chigrl: More Central Banks Than Ever Say They Will Buy Gold This Year

More central banks than ever expect to increase their gold reser…

72

Valco retweeted

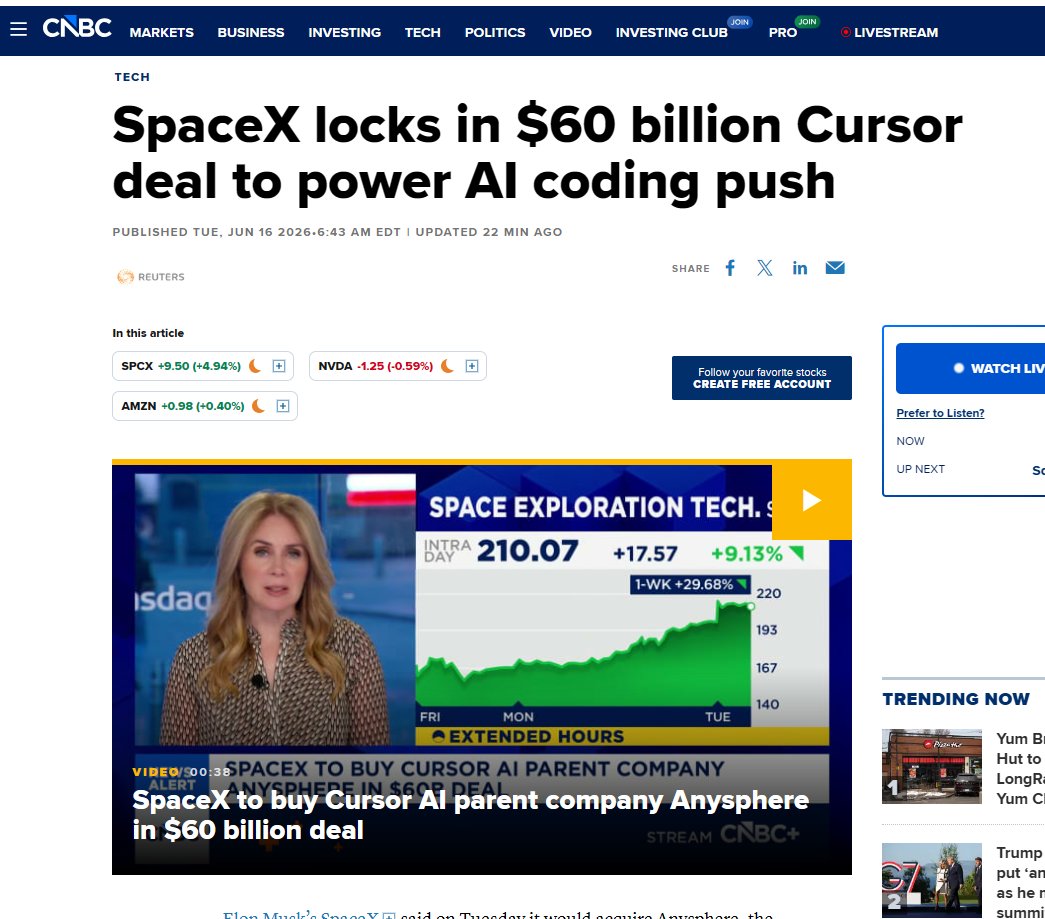

SpaceX just bought a $60 billion company without spending a dollar.

The deal for Cursor, the AI coding tool, is all stock. No cash. SpaceX prints new shares, hands them over, done.

Now connect it to what happened last week.

SpaceX went public by floating just 4% of itself. 556 million shares against 13 billion. The tiniest free float a mega-cap has ever listed with. Index funds were forced to buy it. Retail piled in. Tiny supply, enormous demand, and the stock rocketed past $200.

Here's the part that should make you sit up.

The price SpaceX pays for Cursor is set by its own share price in the seven days before closing. The higher the stock, the fewer shares it has to print to cover $60 billion.

So the engineered scarcity that pumped the stock now makes the acquisition cheaper. The squeeze pays for the shopping spree.

A company losing $4 billion a quarter is now buying AI startups with paper it manufactured out of a 4% float.

This isn't aerospace. It isn't even AI.

It's the finest financial engineering of the century, and it's only getting started.

SpaceX $SPCX traded 256 million shares yesterday.

The entire public float is 556 million.

So in one day, almost half of every tradable share changed hands. Bought and sold, over and over, in a few hours.

Here's why that number is absurd. SpaceX sold 555.6 million shares at $135 to raise $75 billion. That float is barely 4% of the company. Musk and insiders hold the other 96%, locked up and unable to sell.

Tiny supply. Enormous demand. Index funds that have to own it, retail that wants to, traders chasing the move.

The result is a $2 trillion company that trades like a penny stock. Up to $211 pre-market, swinging double-digit percentages between coffees.

This is what happens when you list 4% of the seventh-largest company in America and let the world fight over the scraps.

The price isn't telling you what SpaceX is worth.

It's telling you how few shares there are to buy.

177

413

2,930

554,922

Valco retweeted

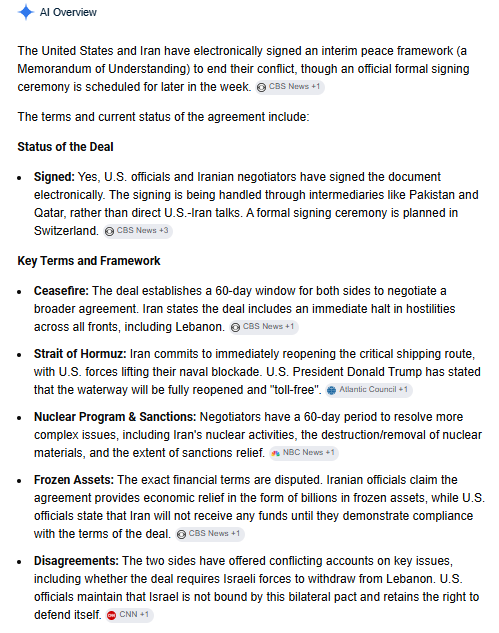

They didn't "make a deal" folks.

They literally signed a document eletronically that they are in agreement to meet later in the week to sign a physical document that they are in agreement to make a deal sometime in the next 60 days on topics they currently agree they are not in agreement on.

Literally. And this makes you bullish stocks and bearish oil?

Wait... THIS is what everyone is bullish about?

THIS is the deal?

First of all, electronically signed...with a cereomony planned for later in the week? Can any of the 3 countries involved actually not bomb someone over the next few days so they can make it to the signing? Let's just say I won't hold my breath.

60 day ceasefire?! So they can negotiate the actual agreement?

This isn't an agreement lol, this is an agreement to meet and talk about making an agreement.

It doesn't mean shit about shit regarding an actual deal being made LOL.

60 days to resolve nuclear related issues? Iran is already saying they aren't giving up nukes lol.

...Frozen Assets....."disputed" is the only word you need to read there.

"The two sides have offered conflicting accounts on key issues"

Part of the deal involves Israel not bombing someone (this alone is reason enough to not believe it'll last, but I digress)

There is exactly 0% chance this "deal" will make it 60 days.

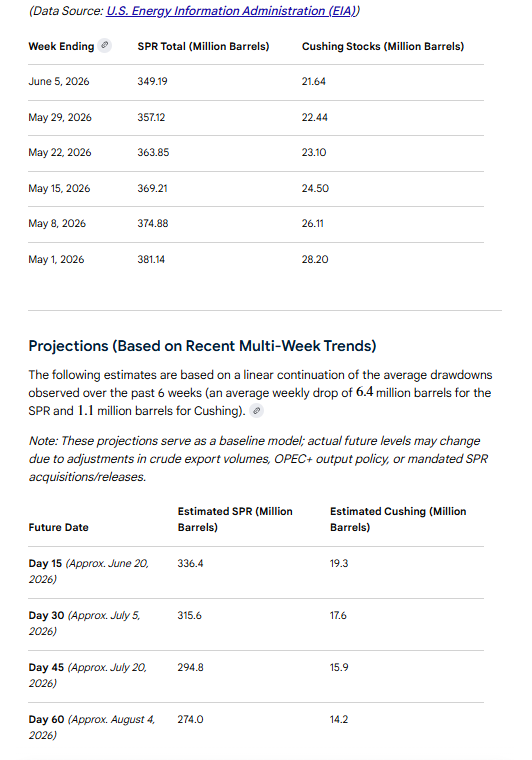

You know what happens in 60 days though?!

Cushing reaches 14M barrels.

Do you know what happened to oil prices after we hit 14M barrels in 2004?

Oil went 5x in 4.5 years. NO BIG DEAL I guess.

🤡

8

17

153

10,653

Valco retweeted

Jun 16

I keep hearing the comparison of data centers and railroads, it’s an absolute fallacy - downstream of railroads, the public received tremendous benefit (towns boomed, states got closer, goods got cheaper) and with data centers the gains are almost entirely nominal stock price gains going to a few dozen people, while people get more addicted to data collection machines

17

29

207

7,857

Valco retweeted

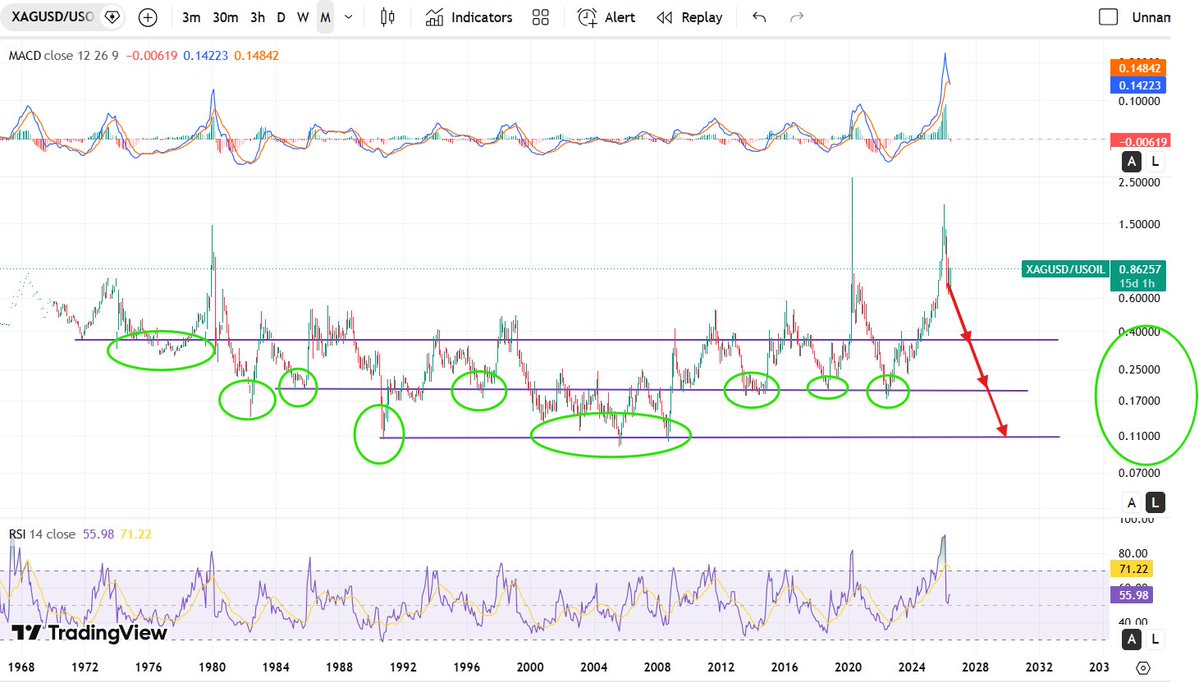

You don’t need to be an economist to see the truth. The only viable exit for the US debt crisis is bond default or negative real yields. Until debt is below GDP, you must own gold & commodities to protect wealth.

Jun 15

Mike Novogratz: The US has $40T of debt and there's only one way out.

"The only way we deal with that debt is to inflate it away. Period. End of story."

Run 4% inflation while convincing markets you're targeting 2%. Do that for 10 years and you've erased 30% of real debt.

The danger is that people could lose confidence, and 4% becomes 14% or 40% - wiping out debt AND wealth simultaneously.

FT @Scaramucci @Novogratz @AllThingsMkts @SkyBridge.

5

5

16

4,313

Valco retweeted

WTI $78 today.

WTI $78 on Jan 5, 2022. This price- before Russia invaded Ukraine.

$78 today with shortages, potential shut-ins, geopolitical risk galore, a tenuous deal/non deal to fully open the SOH, and oil transit not returning to normal for months regardless of a deal being finalized.

10

17

161

34,326

Valco retweeted

Jun 14

Really good take. Must read.

Jun 14

Looking at the interview, it seems yesterday's piece needs some revision.

Yesterday I wrote about the venue of the prospective agreement, the mechanism meant to enforce it, and the actors who will not sign it. Then I came across an SNN interview in which Mahmoud Nabavian, deputy chairman of the Iranian Parliament's National Security Commission, read out the original text directly and launched a frontal attack on the negotiating team.

Nabavian is a hardliner opposed to the negotiations themselves, so his testimony carries its own bias. But on the strength of the fact that he was quoting the wording — and on the basis of the critique now coming from the hardline camp — yesterday's piece needs correcting.

First, the parts where my earlier analysis pointed in a similar direction.

What Held Up

1. The diagnosis of "a document that seals the disputes inside a 60-day window"

The starting point of my analysis was that this MOU is not a document that resolved the core disputes — nuclear, control, money — but one that repackaged them, deferred to "negotiations 60 days later," so that only the signing becomes possible. Nabavian's central objection takes aim at exactly this structure. He criticized the fact that all the major benefits accruing to Iran — $300 billion in reconstruction, an end to sanctions, resolution of the nuclear issue, US troop withdrawal — are bound up in a "final agreement" whose date is unclear and indefinitely extendable.

2. Hormuz — the "rebranding of control"

I had argued that what Iran gave up at Hormuz was only the word "toll," while the economic substance (service fees) and the operational substance (control) remained alive — and I forecast that "a reappraisal will come once the details of an Iranian-managed reopening are made public." This part turned out more dramatic than I expected. According to Nabavian's reading, from the hardline vantage point that control itself has evaporated from the text. He revealed that the earlier version's explicit name "Strait of Hormuz" had been generalized to "commercial ships from the Persian Gulf to the Sea of Oman," and that the US had later inserted the word "unlimited." His claim: "arrangements" means not Iranian management but merely preparation for reopening, and nowhere in the text is Iranian control of the strait preserved. In other words, my initial read — "the claim to control is alive" — exists from the negotiating team's standpoint, but on the wording of the text itself it is exposed to the hardliners' rebuttal.

3. UNSC endorsement is not a guarantee

In the earlier piece I concluded with "the lesson of Resolution 2231 — institutionalization only raises the cost of exit; it does not prevent exit." Nabavian's critique of Clause 14 says the same thing in an insider's language: "A binding UNSC resolution is not a real guarantee. We already lived through this with the JCPOA and 2231 — the US withdrew, yet Iran alone was left trapped in international obligations, and only snapback became possible." He goes a step further: "Once the agreement goes to the Security Council, Iran does not control the text, and the US and other members slip in additional restrictions — missiles, arms, inspections (precisely the 2231 case)." Strong corroboration that my initial inference is being raised, identically, inside the Iranian parliament.

4. The US domestic bottleneck — Congress, OFAC, banks

Near the end of the piece I added the asymmetry that "Congress cannot guarantee non-aggression, but it can block sanctions relief." Nabavian confirms it outright: "The US cannot by itself cancel UNSC or IAEA resolutions, and many sanctions are congressional statutes that Trump cannot remove on his own." The three-layer bottleneck logic — OFAC, Congress, bank compliance — was being read the same way in Tehran.

5. The inversion of the money sequence

I had flagged the sequence inversion as central: "2013 was performance first, money later; this time it is a demand for upfront payment." Nabavian confirms the structure with more precise figures.

6. The documentation of Lebanon

My earlier piece read the shift from April's "end of war" carve-out to this round's "ceasefire across all fronts, Lebanon included" as deliberate engineering. Nabavian, too, concedes that Clause 1 at least was "improved in Iran's favor compared to the earlier version" — "end of war" was strengthened to "immediate and permanent end of military operations on all fronts, including Lebanon," closing the room for the US to declare the war over while continuing 'defensive' operations.

Where My Initial Read Was Wrong

1. The "lifting is easy" dichotomy — I missed the re-sanctions axis

I split the new Security Council resolution into two parts: lifting the legacy sanctions (easy) and the new enforcement device (hard). That dichotomy dropped one crucial axis. As Nabavian points out — "the text does not prevent the US from imposing new sanctions the very next day, so the sanctions remain 100% effectively in place." Even if a nominal lifting occurs, if re-designation under a different name is possible, the lifting is hollow. What Iran really wants is not "lifting" but a "guarantee against re-sanctioning," and a lifting without that is meaningless to Iran. My earlier analysis, boxed into "lifting vs. enforcement," failed to see the third axis of re-sanctioning. This asymmetry interlocks with the nuclear section, too — Iran repeatedly provides written guarantees that it "will not produce or acquire nuclear weapons," while the US provides no equivalent guarantee on future sanctions.

2. The money figure — "half of $24 billion" was imprecise

Following the Mehr report, I wrote "half of $24 billion paid upfront." Nabavian's text is more precise. Iran's earlier proposal was "$12 billion immediately after signing, the rest within 30 days," and after the US rejected it, the current version weakened to the vague phrase "assets to be made available based on progress in negotiations" — with no definition of "progress" and no figure. In other words, the clear guarantee of "$12 billion immediately" has disappeared. My sequence-inversion thesis held, but the figure, and the direction of the retreat (toward terms even less favorable to Iran), need correcting. And this shows that the "$24 billion" headline making the rounds is not a settled condition but one version within the negotiating process.

3. Nuclear dilution — "domestic blend-down = an Iranian win" was an oversimplification

I framed the gap between "what Trump sold Netanyahu (removal)" and "what the document says (domestic blend-down)" as a US–Israel rift. The frame itself holds, but treating "domestic blend-down" as if it were an Iranian victory was an oversimplification. The actual wording Nabavian read out is "the dilution of all nuclear material on site, at minimum under IAEA supervision and under American considerations." It is domestic dilution — but dilution under American control. Hardliners see even this as "an American demand packaged in Iran's language." My earlier frame is not weakened by this (the US–Israel gap stands), but the nuance that "Iran fended off removal, so it amounts to a win" needs correcting.

4. The "clever Iranian design" frame — it tilted to one side

This is the part needing the largest correction. Taking the documentation of Lebanon as my starting point, I loaded the MOU rather heavily with Iranian strategic agency (deterrence exit raising the cost of erosion through multilateralization). Nabavian's whole testimony paints the opposite picture. He reads Hormuz, the nuclear file, the money, the withdrawal — nearly every item — as "American demands presented in Iran's language," i.e., the result of Iran retreating with each successive version. "Every time we submitted it and it changed, we retreated" is his summary.

The truth lies between two biases. I lean toward Iranian agency; Nabavian (as a hardliner) leans toward Iranian capitulation. Netting them out, the MOU is neither "Iran's clever trap" nor "Iran's total surrender," but something closer to a US-led asymmetric bargain in which Iran won one square — Lebanon — and gave ground on Hormuz, the nuclear file, and the money. Lebanon is nearly the only square Iran actively secured; on the rest, it was largely on the defensive. The center of gravity of my earlier piece has, in effect, collapsed.

What I Did Not Address Before, but Must Add After This Interview

1. The paradox of Iran freezing its own leverage

This is the strongest point, absent from my earlier analysis. According to Nabavian, during the waiting period Iran freezes — and proposed to freeze, itself — three things: its current nuclear status (no enrichment), the non-reconstruction of the damaged facilities, and the endurance of US sanctions. On top of that it accepts the continued presence of US forces in the region. In other words, if the final agreement is extended indefinitely, Iran freezes its own cards during the wait while the US keeps its sanctions and its troops in place. His rhetorical question — "Is this really America's proposal, or ours?" — is the crux.

This deepens my reading of the 60-day window by one level. I had seen the window only as "a time bomb where the nuclear and control disputes reignite." But before that, the window is a period in which Iran voluntarily ties down its supply and nuclear leverage. In the short term this is downward pressure on oil (Iran restrains its incentive to provoke), but it is simultaneously a stretch in which domestic hardliner discontent accumulates. The vagueness of the withdrawal clause ("US forces leave the area 'surrounding Iran' 30 days after the final agreement" — timing undefined, "surrounding" distance undefined) amplifies it. Lifting the blockade is nearly the only US-side implementation item with a fixed date; the rest of the US implementation is all linked to the variable "final agreement."

2. A "third generation" of guarantee discourse — the hardliners' automatic-retaliation trigger

I had organized Iran's guarantee model as first generation (congressional ratification) → second generation (multilateral institutions, the UNSC, economic lock-in). Nabavian rejects even that second generation and demands a third: instead of a UNSC resolution, write into the document automatic consequences — that if the US violates the deal, Iran exits the NPT, fully closes the Strait of Hormuz, and resumes enrichment at unlimited levels. In other words, inside Iran the guarantee discourse is reverting from "institution" to "consequence," and the negotiating team's second-generation line is being squeezed by hardliners who call it "a trap, too." Whether this comes to pass, however, remains uncertain.

3. The Iranian domestic bottleneck — symmetry with the Washington bottleneck

My earlier piece dealt only with the US-side bottleneck (Congress, OFAC, banks). Nabavian's public revolt itself shows that even if the negotiating team reaches a signature, friction can arise at Iran's domestic ratification and implementation stage. Because the Hormuz "control" wording and the nuclear "American considerations" wording are the focal targets of the hardliners, an interpretive struggle over these two clauses will erupt inside Iran after signing. A symmetric structure in which both sides' domestic politics gnaw at the agreement simultaneously — this was missing from the earlier analysis.

4. The instability of the text's very authenticity — a meta-level caveat

The most important meta-lesson. Even Nabavian conceded that he is "told that what I have seen is not the final version." An Iranian deputy committee chairman has, in effect, admitted that the reported text I relied on when writing the earlier piece may not be the final one. At the same time, his own reading may be a hardliner's selective citation. No single version should be believed as is.

Yet paradoxically, the very "differences" between those versions may be the most honest signal. Which word was added ("unlimited") and which words were dropped ("Strait of Hormuz," "compensation/reparations," "$12 billion immediately") reveal where the center of gravity of the negotiation is shifting.

It was only because yesterday and today happen to be holidays for me that I could attempt this at all. This exercise has given me no certainty whatsoever. The one thing I was able to confirm is the symbolic weight the MOU carries. Reading the posts that surfaced across various X accounts today, and Nabavian's interview, it is clear that — unlike what gets digested in the headlines — the two sides are negotiating under a thick layer of complexity around a particular documentary form: the wording, the nuance, and even the framework that follows. The US will have its own internal backlash, and Iran will have the same. This is precisely why I bought the Z26 calls: I wanted to step outside the optimism and the pessimism about the negotiations, and to place a bet closer to physics and mathematics — one with the higher probability. My efforts yesterday and today may, in truth, have been an absurd waste of time. Have a good weekend.

15

13

176

46,080

Valco retweeted

Jun 15

Trump: the Strait is reopening, more ships are passing through, the Oil is flowing

The Strait: mostly the same as yesterday, last week, and last month

60

142

1,141

55,200

Valco retweeted

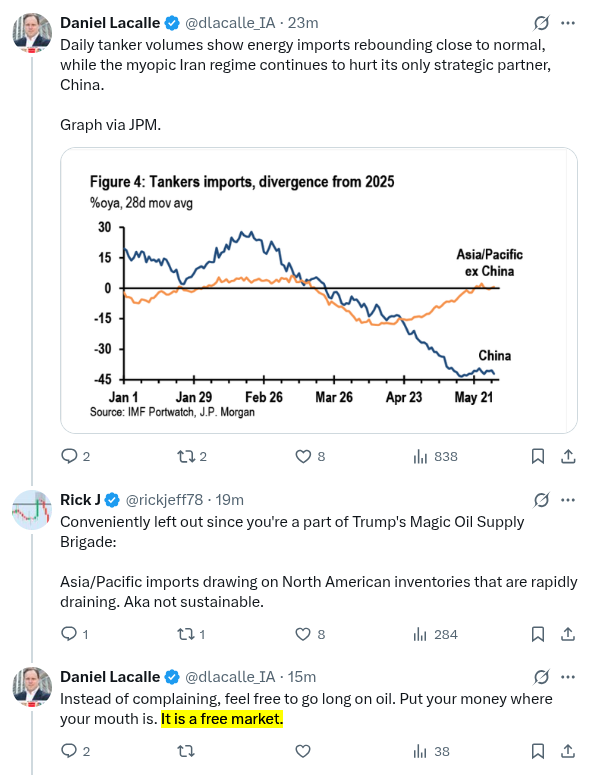

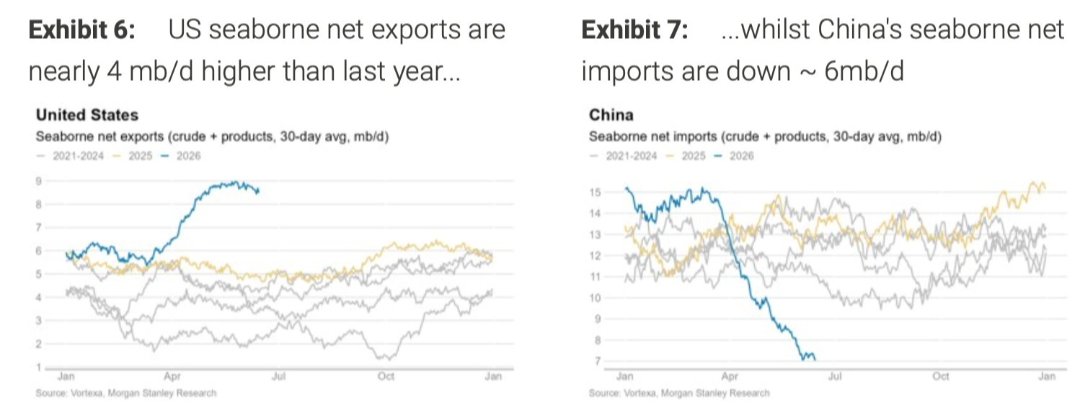

20h

When people said that the war ended on about April 1st

What they were really noticing was the US ramping exports and China dropping imports

4

8

121

7,467

Valco retweeted

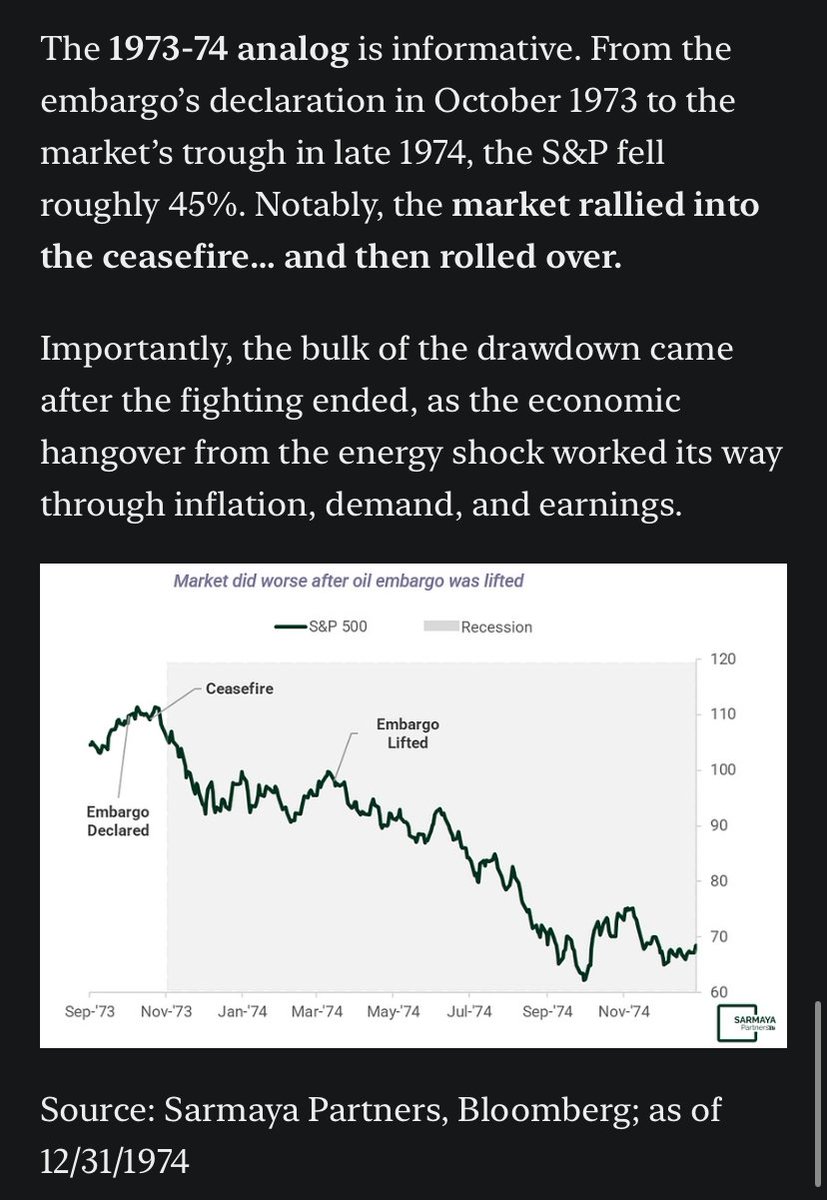

As I said the day before Operation Epic Fury:

“2026 is kind of like 1973, 1987, and 2000, all in one year. In hindsight, it’ll be “obvious.””

You are here now.

3

5

34

8,119

Valco retweeted

20h

The S&P 500 concentration in AI stocks is now 49% of the index

This is the highest concentration since the railroad bubble in the 1800s

56

196

2,732

101,766

Valco retweeted

Imagine concuring with a chatbot. Though they aren't always proven to be bots like this, im surprised anyone replies at all to text walls with thick AI accents. Just mute them and move on before they spread like kudzu.

Jun 15

I concur.

1

1

1

384

Valco retweeted

Jun 14

China is watching today's events closely, and they now know that if they so much as lift a finger toward Taiwan, Trump is going to respond harshly by signing a deal and giving them Thailand and Vietnam along with full sovereignty over the South China Sea.

They better be careful.

168

1,148

7,089

257,702

Valco retweeted

Jun 15

So basically Trump drew it to the bottom of what’s acceptable and then TACO’d hard

Jun 15

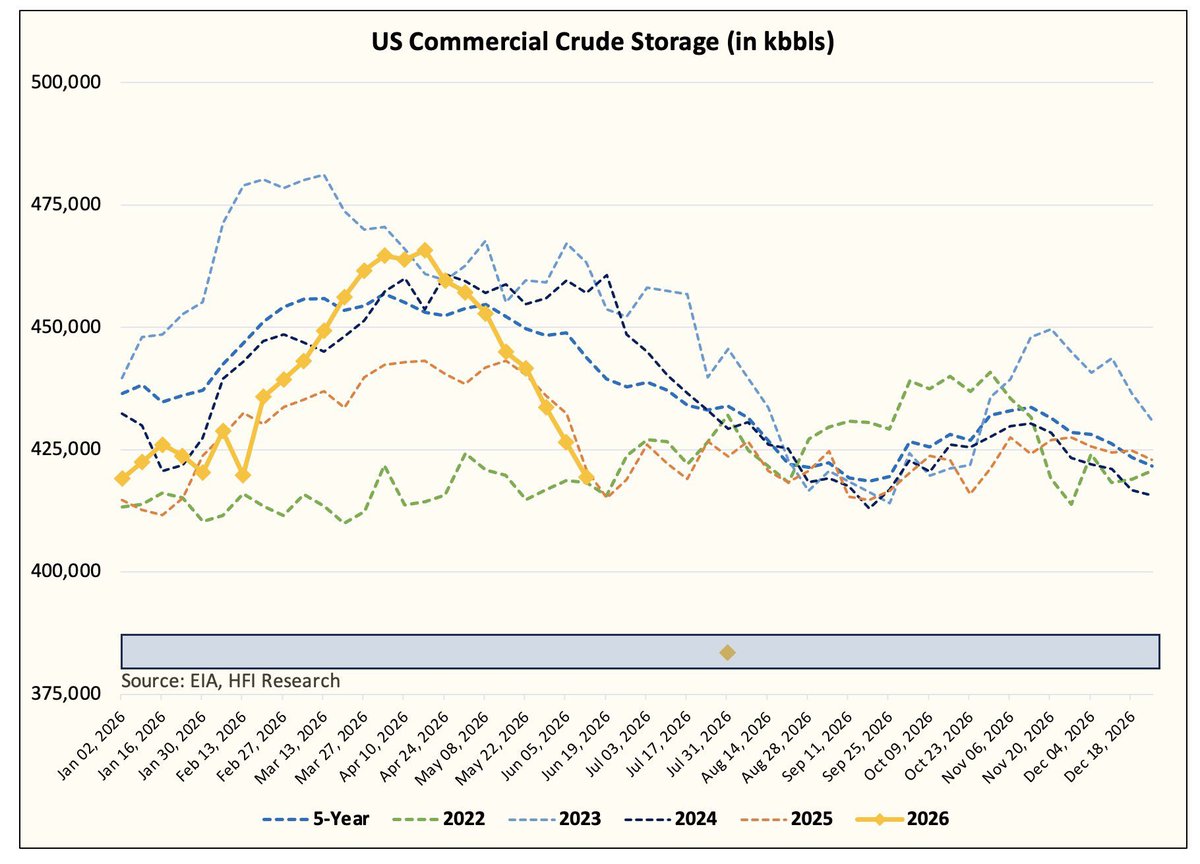

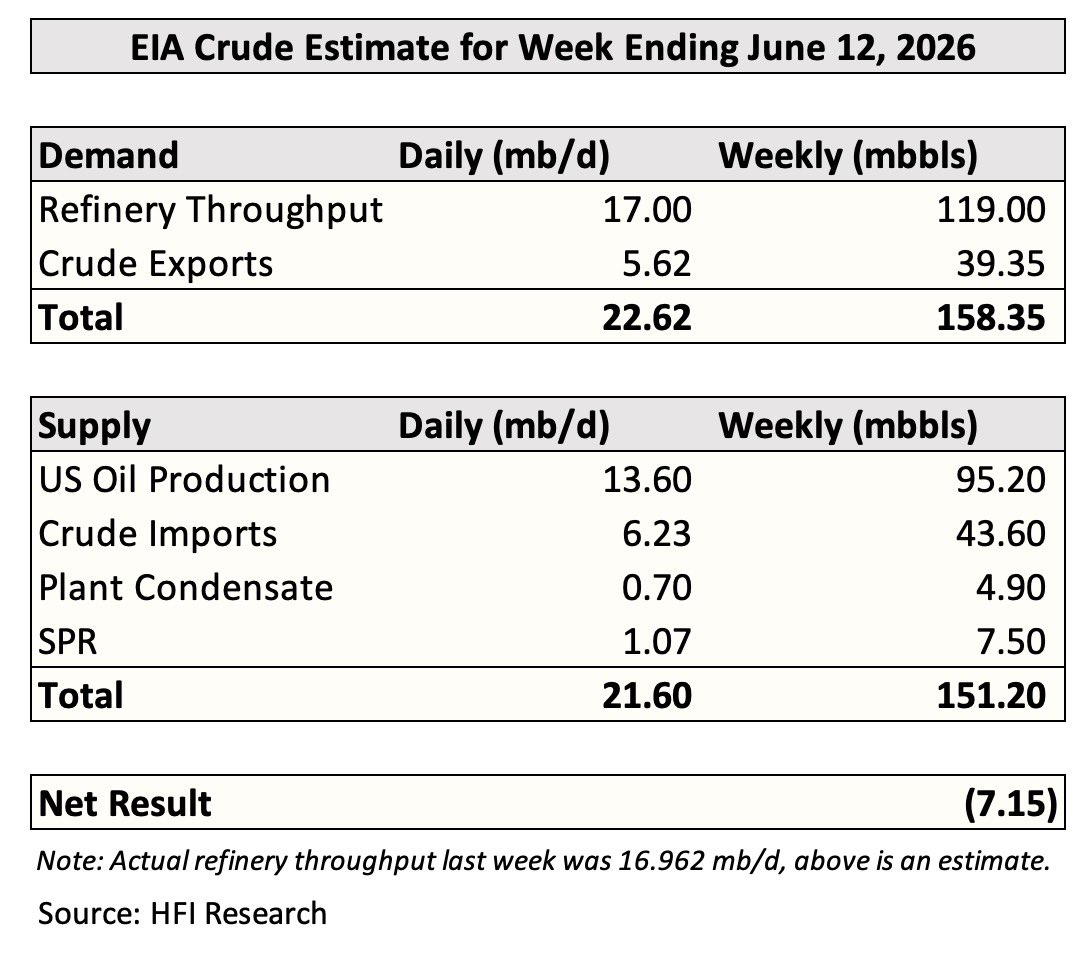

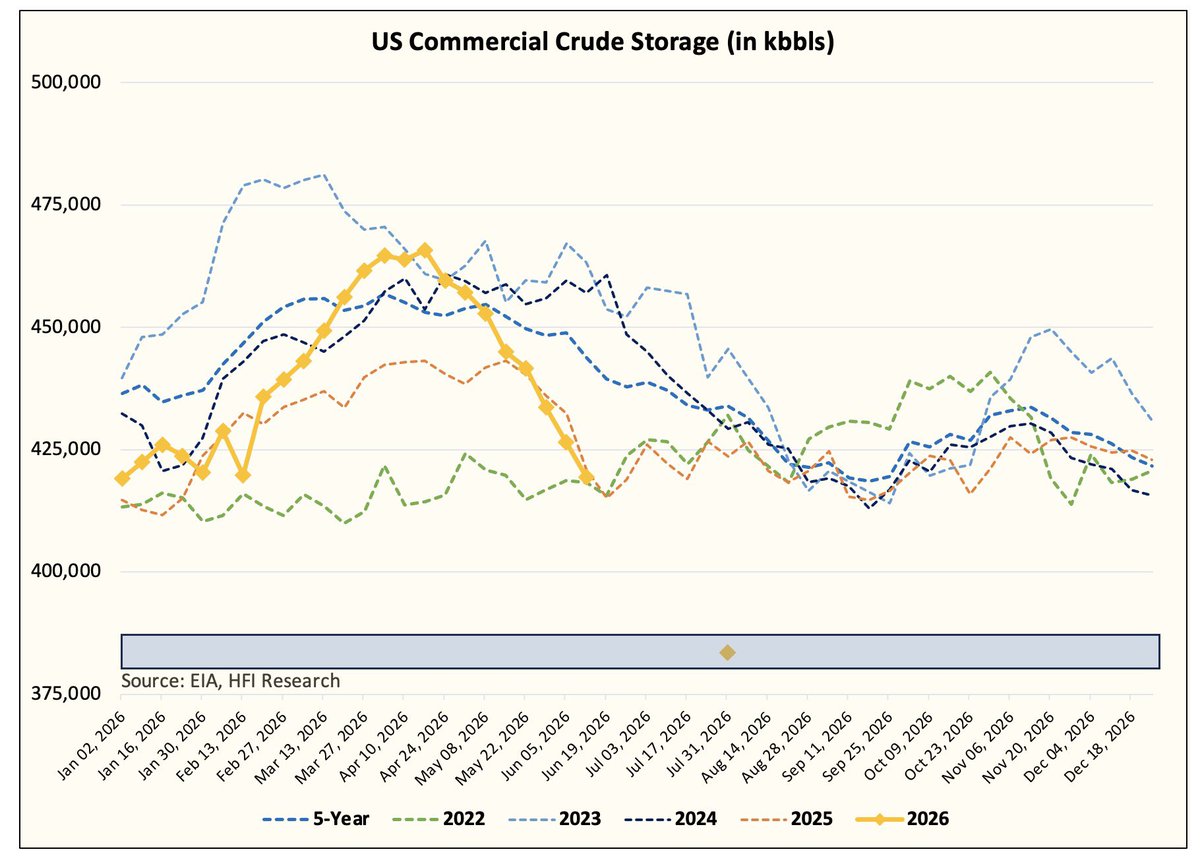

Final crude estimate for June 12 week.

We see a total crude draw of 14.65 million bbls. Commercial crude draw of 7.15 million bbls.

We are currently estimating the SPR release to be 7.5 million bbls.

This is the 6th largest crude draw in US history.

9

11

151

15,422

Valco retweeted

Jun 15

Corn now cheaper than pre war by a lot

Fertilizer costs way up, fuel costs way up

It's like they have to bankrupt every farmer in America before the price can go up

29

39

482

19,202

Valco retweeted

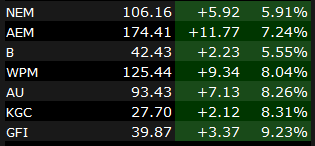

Jun 15

Who knew that the best reopening trade was...mining stocks

14

4

246

10,436

Valco retweeted

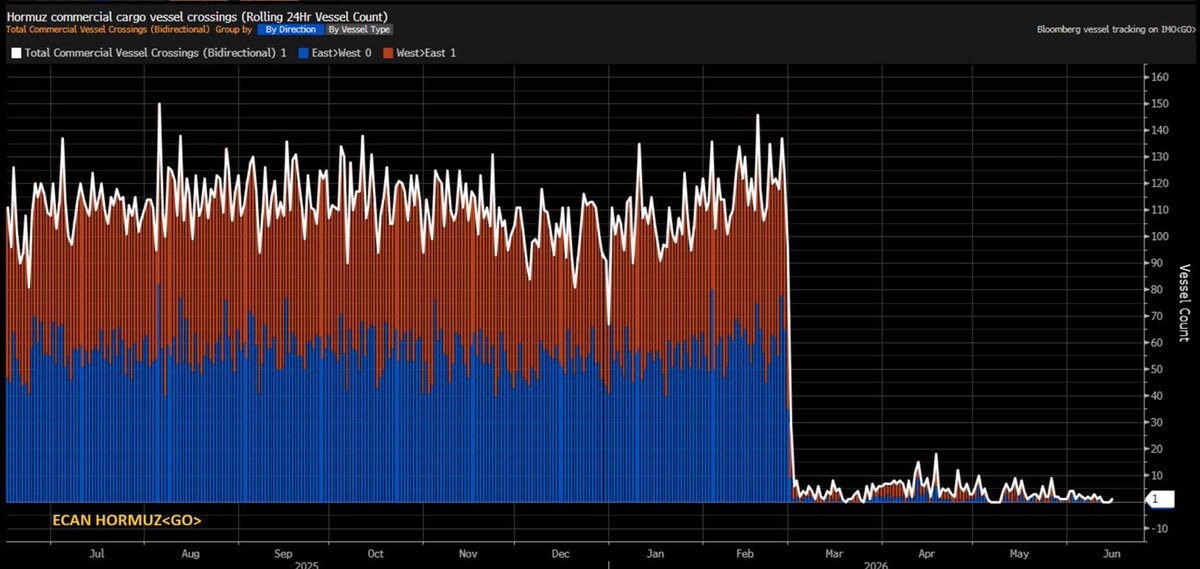

Jun 15

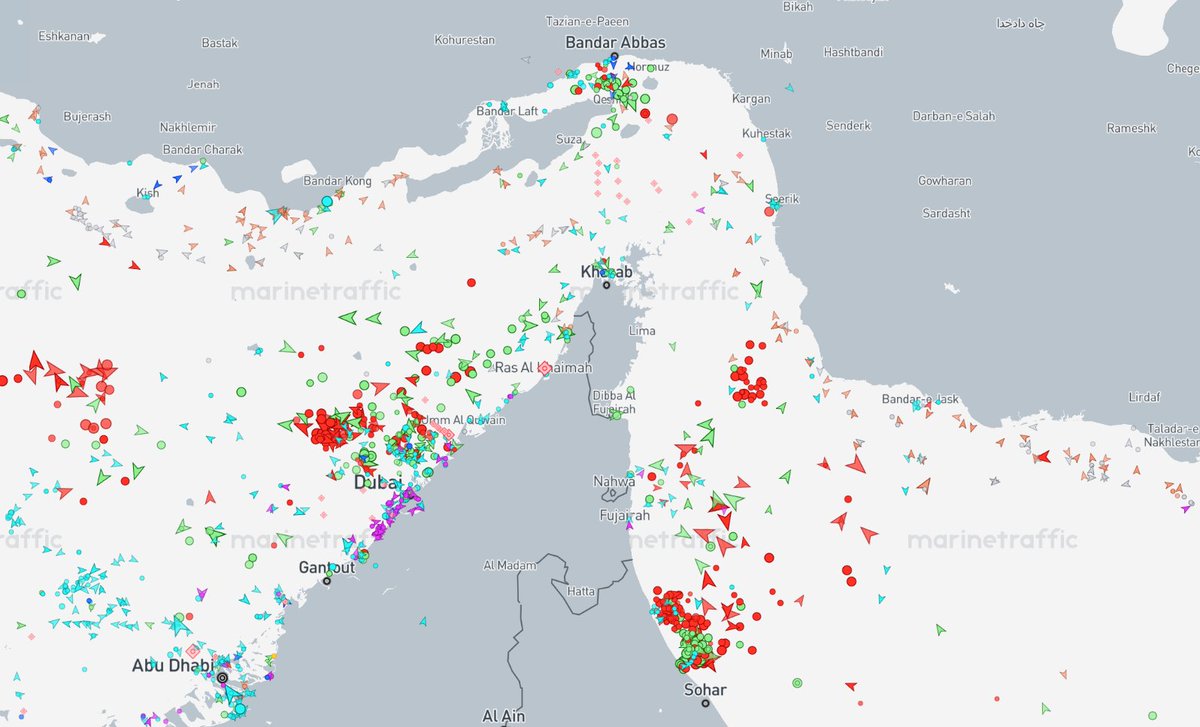

Strait of Hormuz transits explode today to 1 from zero

Just write the article in percentage terms to get maximum impact

41

129

1,180

48,918