Joined October 2017

- Tweets 11,229

- Following 4,142

- Followers 1,180

- Likes 63,045

303 Photos and videos

Jun 16

RT @cristiannmillo: Esto es espectacular como se movió Marruecos defensivamente. Esto se entrena. No es aleatorio. Tremendo bloque corto de…

6,945

Jun 15

China is Mogging Western Auto, and that’s Bad for Semis, National Security & War

If you live anywhere outside the US, you've noticed it: the streets are filling up with cars you've never seen before. Chery? Jaecoo? Zeekr? Leapmotor? BYD? No, you didn't miss a decade of car launches. They're Chinese. And they're everywhere. (1/10)🧵

30

34

315

67,907

Jun 15

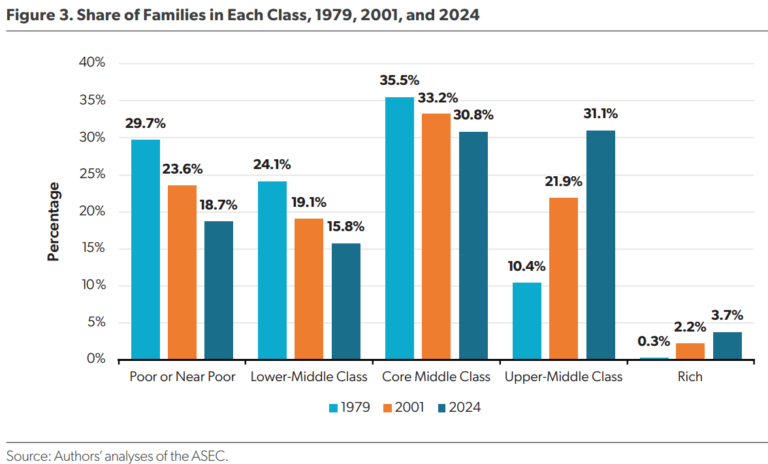

The middle class in America is shrinking

But it's happening b/c more ppl are moving into the upper middle class

American households are getting richer but the rich are getting richer at a faster pace

Wealth inequality is complicated

awealthofcommonsense.com/202…

28

38

216

33,142

Jun 14

When I said this throughout my campaign, CNN people called me cruel and unhinged. Now, after they helped secure the election for the 2 dorks responsible for all these problems, CNN is now echoing my campaign talking points as gospel. Fascinating!

1,181

14,806

83,363

1,196,437

Jun 14

None of this was some weeks long back and forth. I was at Anthropic's HQ on Friday reporting when this all unfolded. Dario is not at a wellness retreat. The Feds seemed to be scrambling to try and make an example of Anthropic again.

This is not technical. It's petty.

38

125

1,979

241,928

Jun 14

Anthropic has pushed AI forward dramatically over the past two years. It's currently the crown jewel of US AI tech.

The Feds don't like @DarioAmodei because he won't do all their bidding. And so, we've now entering the Soviet-style propaganda portion of the program with the White House feeding every reporter it can find with laughable claims like Dario is unreachable at a wellness retreat. Come on.

I'd hoped the US would not be self-defeating on AI, since it's kinda one of the last hopes the US has versus China. But here we are . . . . already

118

142

2,066

155,266

Jun 13

NEW: Inside the 24-hrs before WH slapped export controls on Anthropic

- Last Thursday, Amazon CEO Andy Jassy raised concerns about Fable jailbreak to Trump admin

- Friday AM, Sean Cairncross, Bessent, Susie etc. held WH call to discuss

- Then White House started reaching out to Anthropic to speak with Dario Amodei, who was at a wellness retreat.

- When Amodei was finally available past 1pm, he had three tense phone calls with a combo of ppl including Cairncross, Bessent, Lutnick, Kessler, Will Scharf, Richard Walters, and Walker Barrett.

-Amodei tried to clear up what he assumed was a misunderstanding. He defended the guardrails and distinguished between universal and non-universal jailbreak

- Cairncross and Bessent were unmoved and asked Amodei to take down Fable and work with the admin to fix the vulnerabilities. (A WH official said Amazon’s findings were run past the NSA and they felt they had “proof.”)

- Amodei asked for more time and info, but he made no commitments to pull the model

- Bessent told Amodei directly at one point that he was making a “bad decision”

- By Friday evening, the Trump admin imposed its export controls.

- “Export controls were a last resort after begging them for hours to work with us,” senior WH official said.

W/ @cheyennehaslett

politico.com/news/2026/06/13…

203

533

3,842

2,461,131

Jun 8

Really fun to interview my old friend Bret Johnsen in Mission Control.

Three parts of the @SpaceX story that I wish were more widely discussed:

SpaceX has created thousands of good blue-collar jobs: welders, machinists, electricians. Everyone talks about the need to bring high-paying, blue-collar jobs back to America. SpaceX and Tesla are making that happen. To the best of my knowledge, they have created more manufacturing jobs in the US than just about any other American company over the last ten years. It’s hard to imagine our nascent industrial renaissance succeeding without these companies.

SpaceX was started with the goal of putting humans on Mars. And along the way, they have massively improved life for many humans on Earth. Mars may be a starter planet, but Earth is our planet, and the technologies developed at SpaceX are already in use today connecting and safeguarding the people of Earth. Starlink is a really efficient way to bring internet to low-income countries. In Kenya’s remote Murang’a County, Starlink has made it possible for patients in rural villages to consult with medical specialists via telemedicine. In the rainforests of Brazil, Starlink has connected schools to reliable high-speed internet that will provide more educational opportunities to students. Here in America, Starlink has proven vital to emergency teams responding to natural disasters. During Hurricane Helene, the Starlink hubs dropped into North Carolina and East Tennessee were often the only contact point between cut-off towns and the outside world. Literally life-saving.

This IPO will be a big milestone for the company. It’s important to celebrate this, while also remembering that making humanity multi-planetary is the ultimate goal. Going to Mars is really hard. There have been many setbacks thus far, ranging from fiery explosions to failed landings. There will be many more. Ad Astra Per Aspera. But SpaceX is at its best *after* a setback imo. Their first 3 launches were “failures”. Had the 4th not succeeded, there might not be a SpaceX today. The company’s success in the face of such daunting odds is a testament to the resilience of the culture and absolute commitment to the mission shared by every employee I’ve ever spoken with. Some of the world’s most talented engineers have chosen to live in Airstreams at Starbase away from their families for weeks on end in service of this goal. I will never forget the welders who told me they signed every weld because they wanted to be accountable if they were responsible for a failure. True missionaries, all of them.

I am grateful to every single person at SpaceX for helping to make the future as inspirational as possible. And I will be even more grateful if I get to see a blue sunset on Mars!

More info on spacexipo.com

142

531

3,261

18,920,370

Jun 8

China's Unitree Will Dominate Global Robotics

The Fastest Iteration Cycle In Next-Gen Robotics Should See Unprecedented Acceleration

newsletter.semianalysis.com/…

52

172

1,133

472,700

Jun 6

🚨 BILLIONAIRE RAY DALIO JUST LAID OUT HIS CONCERNS ABOUT BITCOIN ON THE ALL-IN PODCAST

And he is not dismissing it. He is sizing it honestly. x.com/saylordocs/status/2062…

On privacy:

"Bitcoin does not have privacy. Any transactions can be monitored and then indirectly perhaps controlled."

On central banks:

"Central banks are not going to want to buy Bitcoin and be able to hold it."

On quantum:

"The development of new technologies like quantum computing... can there be issues regarding that?"

On correlation:

"It tends to have a pretty high correlation with tech stocks. If somebody gets squeezed on whatever else they have, those dynamics affect Bitcoin."

On size:

"It's a relatively small market that's relatively controllable. As money, it's small in relationship to gold."

Dalio is not saying Bitcoin goes to zero. He is saying the risks are real and the market is smaller than the narrative suggests.

Hard to dismiss when it comes from the founder of the world's largest hedge fund.

26

23

136

39,978

Jun 7

It's matter of time before GLP-1's are prescribed like statins. The sheer VE impact of GLP's across spectrum of conditions (obesity, addiction, CKD, heart etc) outweigh any costs associated.

Would recommend @patrick_oshag interview of @alex_karnal

Jun 6

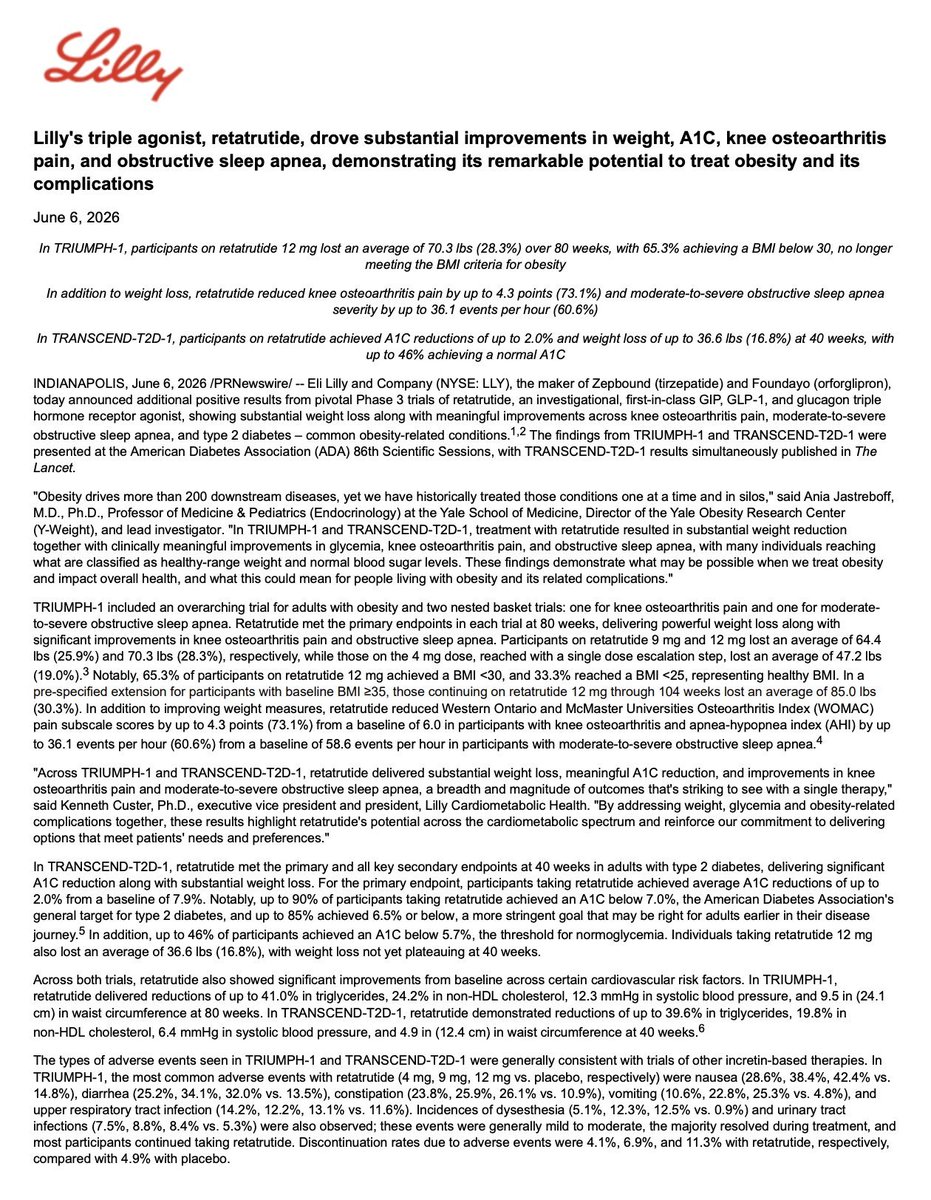

Retatrutide additional phase 3 results are out, and the data keeps getting better:

- 28.3% bodyweight lost on 12mg over 80 weeks (70.3 lbs)

- 30.3% at 104 weeks in higher-BMI patients (85 lbs)

- 65.3% dropped below the obesity BMI threshold

- Knee osteoarthritis pain reduced by up to 75.8% (1 in 8 patients are fully pain-free)

- Obstructive sleep apnea significantly improved

- Major drops in triglycerides (41%), non-HDL cholesterol (24.2%), and blood pressure

- A1C fell up to 2.0% and weight down 16.8% in diabetic patients, in just 40 weeks

For those that are unfamiliar, retatrutide now has Phase 3 data showing it reaches well beyond weight loss.

It directly treats the complications that have historically required entirely separate medications.

This is becoming a new category of medicine, and the data is only getting stronger.

52

Jun 4

RT @lexfridman: I got to spend all day today with Jensen in Taiwan: talking with thousands of engineers and eating street food at a night m…

1,331

Matthew McConaughey reveals sleep was a sin in his household

“Hustle, hustle, hustle. Sleep was sin in my household”

“If it was daylight, you couldn't be inside. 30 minutes of TV a night max”

“Mom would always say, ‘Why are you going to watch someone doing something when you can go out in the world and do it yourself? Turn that damn thing off. Get outside’”

“You had to be outside. Like, go get out in the world. Go hustle. Figure it out. Be home at dark. That was just the understood rule”

280

636

17,274

3,031,348

Jun 3

Echoes 👇🏽 with what @dkhos mentioned in @InvestLikeBest latest interview.

Matthew McConaughey reveals sleep was a sin in his household

“Hustle, hustle, hustle. Sleep was sin in my household”

“If it was daylight, you couldn't be inside. 30 minutes of TV a night max”

“Mom would always say, ‘Why are you going to watch someone doing something when you can go out in the world and do it yourself? Turn that damn thing off. Get outside’”

“You had to be outside. Like, go get out in the world. Go hustle. Figure it out. Be home at dark. That was just the understood rule”

1

59

Jun 3

New statement from Scott Pelley:

There has never been anything in America like 60 Minutes.

The Sunday tradition is the most successful program of any kind in history. For more than a decade, its innovative growth on every major online platform has extended its reach to countless millions around the world. This spring, at the end of our 58thseason, 60 Minutes grew rapidly with an unheard-of 9% jump in viewers on CBS.

“60” has been the number-one program in America for decades because our beloved audience finds integrity, quality, and humanity in our stories. When stewardship of the program passed to my colleagues and me, our responsibility was to expand energetically into a new age of media technology while preserving the values our audience expects. Now, the new owner of our network is casting this legend aside, apparently to curry a moment of favor with the Trump administration.

The waste is heartbreaking.

Last month, 60 Minutes lost its DNA when our entire senior leadership and two of our best on-air correspondents were cruelly fired without cause. Good people were silenced because they stood up for our audience. They stood for fairness against the forces of political bias; they stood for professionalism against chaos.

For my part, new management has instructed me to inject falsehoods and bias into a politically sensitive story. I’ve been told to include assertions that are unverified. To date, in every case, I have managed to ignore these instructions or refuse them. Recently, politicians have been invited to choose correspondents for interviews on the broadcast. Giving politicians control over 60 Minutes interviews is not how this is done. Finally, incompetence and unprofessionalism in the new management have wreaked havoc. In a case involving one of my stories, the entire program came within 19 minutes of not getting on the air at all.

At 60 Minutes, we have fought harder than anyone knows to save the program that became an American icon. We owed that to our millions of viewers. I am deeply moved by the thousands of wishes we have received to “keep up the good fight.” Most of the men and women of CBS News are still in that fight. But now the collapse of values at the top has become untenable. The leadership of 60 Minutes is no longer recognizable. The principles I hold dear are gone, and so I must leave as well.

I depart after 37 years at CBS with one emotion—a heart brimming with gratitude for the men and women of CBS News who encouraged and enriched my work, very often at the risk of their own lives. I pray for a day when those people and their ideals are honored again—a day when sanity, competence, and courage return.

Scott Pelley

2,042

6,288

24,124

2,139,609

Jun 3

Very well said.

As I mentioned on the call with @DimitryNakhla and @DrewCohenMoney, when most people hear the word “bubble,” they immediately think of something like the Dot Com crash, the Financial Crisis, or Covid. They think of stock prices collapsing, businesses struggling, and investors losing money very quickly. That’s certainly one type of bubble, but I don’t think it’s the only type.

Sometimes a bubble doesn’t end with a crash. Sometimes the business continues performing well, revenue keeps growing, earnings keep growing, and management keeps executing. The problem is that investors became so optimistic that they paid a price that already assumed years of future success.

$MSFT is probably one of the best examples. If you had looked only at the business, you would have seen a company becoming stronger, more profitable, and more dominant. Yet despite all that progress, the stock largely went nowhere for more than a decade because the valuation at the starting point was simply too high.

I think this is one of the most important lessons in investing because many people assume that finding a great company is enough. In reality, a great business and a great investment are not always the same thing. Sometimes you can be completely right about the company and still end up with disappointing returns.

There are really two ways to be wrong as an investor. You can be wrong about the business itself, which is the risk most people spend their time thinking about. Or you can be right about the business but wrong about the price you paid, which in my experience is often the more common mistake.

What’s interesting is that time can be just as effective as a crash when it comes to correcting excess valuation. The market doesn’t always need a stock to fall 70% to fix a bubble. Sometimes the stock simply moves sideways for 10 or 15 years while the business slowly grows into the valuation that investors once paid.

The irony is that some of the highest quality businesses can become the most dangerous investments. When everyone agrees a company is exceptional, that quality often becomes fully reflected in the stock price. At that point, future returns become much more dependent on the valuation than on the quality of the business itself.

This is also why opportunity cost matters so much. Imagine owning a company that grows earnings at 15% annually for a decade, yet the stock produces very little return because the valuation falls from 60 times earnings to 20 times earnings.

Sometimes bubbles end with panic and headlines. Sometimes they end with bankruptcies and forced selling. But sometimes they end much more quietly, through a long period of stagnant returns while the underlying business does everything right.

In many ways, that may be the market’s most effective way of punishing excessive optimism. Not through a crash, but through time.

🌹

50