📈 Exploring #Investing, #Options, #Equities, #Forex. Question everything! Join for insights & growth. #FinancialEducation. Education and research NOT ADVICE

Joined July 2009

- Tweets 195

- Following 1,467

- Followers 638

- Likes 206

39 Photos and videos

🚨 Micron may be getting punished for the wrong reason today 👀

$MU sold off after the market reacted to Google’s TurboQuant announcement, but this feels a lot more like fear and headline pressure than a real break in Micron’s long-term story.

Here’s why: Google’s technology is being talked about like it suddenly changes everything for memory, but compression techniques like this are not new. TurboQuant is aimed at KV-cache compression for AI inference, which is a much narrower issue than the market is making it out to be. It does not suddenly eliminate the need for DRAM, NAND, or HBM across the much larger AI infrastructure buildout.

And while the stock gets hit, Micron is still executing at a very high level:

🚀 Record fiscal Q2 results

📈 Record Q3 guidance

🔥 2026 HBM supply already committed

⚡ Micron has already begun volume shipment of its HBM4 36GB 12H designed for NVIDIA Vera Rubin

💰 Valuation still looks compelling relative to the growth the company is delivering.

That does not sound like a broken story.

If anything, Micron looks like a company preparing for the next leg of the AI hardware cycle, not one getting left behind. The market is reacting as if one efficiency improvement wipes out the need for advanced memory, but the broader AI buildout is still happening, memory demand remains tight, and Micron is already positioning itself for the next generation of Nvidia’s AI platform. This is why today’s move feels more emotional than fundamental.

Micron is no longer just a basic memory name. It is now deeply tied to AI servers, high-bandwidth memory, and next-generation accelerator platforms. If that demand story stays intact, today’s selloff may end up looking like an overreaction instead of a real change in the company’s earnings power 🔥

Sometimes Wall Street sells first and asks better questions later. This might be one of those moments.

Micron still has the AI tailwind.

Micron is already preparing for Nvidia’s next-gen platform. And Micron still looks like one of the more overlooked names in large-cap semis right now 📈

FOR EDUCATIONAL PURPOSES ONLY. THIS IS NOT A RECOMMENDATION TO BUY OR SELL SECURITIES. YOU MUST DO YOUR OWN RESEARCH AND CONSULT A PROFESSIONAL.

#alphatitancapital #stockmarket #education #spy #spx #qqq #ndx #dia #djx #finance #economic #bitcoin #wallstreet #nasdaq #sp500 #treasury #ai #artificialintelligence #cnbc #bloomberg #FT #foxbusiness #forex

2

218

Micron is becoming harder to ignore 👀

$MU is delivering the kind of growth and profitability that usually gets rewarded with a much higher multiple:

🚀 Revenue growth: 196.29%

💰 ROE: 21%

🏦 EBITDA: $18.48B

📊 Gross profit: $17.75B

And that is where the peer comparison starts getting interesting.

Compared with many semiconductor names, Micron still does not look overly stretched on valuation. Its P/E of 19.08 sits well below names like NVIDIA at 35.84, Broadcom at 62.87, Marvell at 29.37, Monolithic Power at 83.70, Astera Labs at 101.53, and Credo at 57.75.

Its price-to-sales ratio of 7.89 also remains far below NVIDIA at 19.94 and Broadcom at 22.98, even though Micron is putting up dramatically stronger growth than many of those same peers.

On the profitability side, Micron’s 21% ROE is stronger than Broadcom, Qualcomm, Marvell, Monolithic Power, NXP, GLOBALFOUNDRIES, ON Semiconductor, Astera Labs, First Solar, Tower Semiconductor, MACOM, and Lattice. Only a few names in the group, including NVIDIA, are clearly ahead on that measure.

Then look at the scale.

Micron’s $18.48B in EBITDA is not just strong. It is massively ahead of most of the field outside of the very largest players. The same goes for its $17.75B gross profit, which puts it in rare company across the group.

This is what makes the setup so interesting.

You have a company producing elite growth, strong returns, and very serious operating scale, yet it is still trading at a valuation that looks more grounded than many of the market’s favorite semiconductor names.

This is not just a memory recovery story anymore.

Micron is showing improving fundamentals, major operating leverage, and the kind of financial momentum that can continue drawing attention if execution stays this strong 🔥

In a crowded semiconductor space, Micron is starting to stand out for all the right reasons.

The story is getting stronger.

The numbers are getting louder.

And relative to many of its peers, the valuation still looks surprisingly reasonable 📈

FOR EDUCATIONAL PURPOSES ONLY. THIS IS NOT A RECOMMENDATION TO BUY OR SELL SECURITIES. YOU MUST DO YOUR OWN RESEARCH AND CONSULT A PROFESSIONAL.

98

📊 Micron Technology (NASDAQ: $MU) Just Delivered One of the Most Powerful Earnings Prints in the Entire AI Trade — And It’s Accelerating 🚀

Micron just reported Q2 FY2026 results, and the numbers weren’t just strong…

they fundamentally reshape how the market may need to think about memory going forward.

This wasn’t a typical beat.

This was a step-change.

⸻

✅ Earnings Explosion — Far Beyond Expectations

Micron delivered:

• EPS: $12.20 vs $9.19 expected

• Revenue: $23.9B vs $20B expected

• YoY Revenue Growth: 196%

• Gross Margin: Surging toward record levels

To put that into perspective:

• EPS up from $1.56 last year → $12.20

• That’s nearly an 8x increase year-over-year

This marks one of the most aggressive earnings accelerations seen across large-cap semiconductors.

⸻

✅ Guidance Signals Even Stronger Acceleration Ahead

If the quarter was strong, the forward outlook is even more notable.

Micron guided:

• Q3 Revenue: ~$33.5B

• Gross Margin: ~81%

• EPS: ~$19.15

That implies:

• ~900% EPS growth YoY next quarter

Management made it clear:

The growth is not slowing — it is accelerating.

In fact, Q3 revenue alone is expected to exceed Micron’s full-year revenue from any year prior to 2024.

⸻

✅ AI Demand Is Driving a Structural Break in the Memory Industry

The core driver behind this transformation is clear:

AI data center demand.

Key data points:

• Data center revenue up 181% YoY

• Non-data center segments up 219% YoY

• Severe shortage in high-end memory and storage

This is being driven by:

• AI training clusters

• Hyperscaler infrastructure buildout

• Massive increases in memory per system

And most importantly:

High-Bandwidth Memory (HBM) has become a critical constraint in scaling AI.

⸻

✅ Pricing Power Supply Constraints = Exceptional Margins

Micron is now benefiting from a rare combination:

• Explosive demand

• Limited supply

• No major new capacity until ~mid-2027

That dynamic is pushing:

• Memory prices sharply higher

• Gross margins toward historically unprecedented levels (~81% guide)

This is a completely different setup from prior cycles.

In past cycles:

Supply would catch up quickly → prices collapse

Now:

Demand is accelerating faster than supply can respond

⸻

✅ A Structural Shift — Not Just a Cycle

For years, memory was viewed as:

• Highly cyclical

• Commodity-driven

• Dependent on PCs and smartphones

That model is changing.

AI has introduced:

• Durable, long-term demand

• Higher-value products (HBM)

• Increased pricing stability

• Stronger visibility through contracted supply

Micron is transitioning from a cyclical player into a strategic AI infrastructure company.

⸻

✅ Capital Strength and Shareholder Confidence

Micron also announced:

• 30% dividend increase

This signals:

• Confidence in sustained cash flow

• Strong balance sheet positioning

• Management conviction in forward earnings power

⸻

✅ The Bigger Picture

What Micron just showed is not just strong execution.

It is evidence of a much larger trend:

Memory is becoming one of the most critical bottlenecks in AI infrastructure.

As AI systems scale, demand for:

• Faster memory

• Higher bandwidth

• Larger capacity

continues to increase at an exponential rate.

Micron sits directly at the center of that demand.

⸻

✅ A Setup Worth Paying Attention To

When you combine:

• Explosive earnings acceleration

• Record-breaking margins

• Forward guidance well above expectations

• Structural AI demand

• Supply constraints extending into 2027

• Increasing institutional focus

You get a setup where the narrative, fundamentals, and positioning are all moving in the same direction.

⸻

🔔 DISCLOSURE: THE FOLLOWING IS FOR EDUCATIONAL PURPOSES IT IS NOT A RECOMMENDATION TO BUY OR SELL SECURITIES YOU MUST DO YOUR OWN RESEARCH AND CONSULT A PROFESSIONAL.

⸻

#alphatitancapital #stockmarket #education #spy #spx #qqq #ndx #dia #cnbc #finance #wallstreet #nasdaq

213

📊 Broadcom $AVGO just reminded the market why it sits at the center of the AI infrastructure boom.

The company reported Q1 results that beat expectations, and the numbers continue to highlight how powerful the demand cycle for AI hardware has become.

Broadcom delivered $2.05 in adjusted EPS, slightly above analyst estimates.

Revenue reached $19.31B, growing 29% year-over-year.

But the headline number investors are paying attention to is AI.

Broadcom generated $8.4B in AI semiconductor revenue, which represents an incredible 106% increase from last year.

That surge is coming from hyperscale data center buildouts. The largest technology companies in the world are pouring billions into AI infrastructure, and Broadcom’s custom AI accelerators and networking chips are becoming a critical piece of that ecosystem.

And the outlook suggests this demand isn’t slowing.

Management expects Q2 revenue to reach about $22B, well above Wall Street expectations around $20.5B.

Even more interesting, the company believes AI semiconductor revenue could climb to $10.7B next quarter alone.

The profitability metrics remain just as impressive.

Broadcom produced $13.1B in adjusted EBITDA, representing 68% margins, while generating $8B in free cash flow during the quarter.

That level of profitability is rare even within the semiconductor industry.

The company also announced a new $10B share buyback authorization while continuing its quarterly dividend, signaling strong confidence in long-term cash generation.

Markets have been debating whether the AI spending cycle can continue at this pace. But the demand numbers coming from companies building the backbone of AI infrastructure keep telling the same story.

The buildout is still accelerating.

Broadcom has quietly positioned itself as one of the most important suppliers behind the global AI expansion, providing the silicon and networking technology that allows these massive data centers to operate.

When you step back and look at the bigger picture, this is not just a semiconductor company reporting earnings.

It’s another datapoint showing how quickly the AI infrastructure economy is scaling.

THE FOLLOWING IS FOR EDUCATIONAL PURPOSES IT IS NOT A RECOMMENDATION TO BUY OR SELL SECURITIES YOU MUST DO YOUR OWN RESEARCH AND CONSULT A PROFESSIONAL.

#alphatitancapital #stockmarket #education #spy #spx #qqq #ndx #dia #djx #finance #economic #bitcoin #wallstreet #nasdaq #sp500 #treasury #ai #artificialintelligence #cnbc #bloomberg #FT #foxbusiness #forex

1

16,158

📊 Sterling Infrastructure (NASDAQ: STRL)

Some stocks move because of hype.

Others move because earnings force institutions to act.

STRL is in the second category.

This company has quietly positioned itself at the center of one of the most powerful capital cycles in the market right now: AI-driven data center construction and U.S. infrastructure expansion.

Let’s break it down.

🔥 Earnings Power

Q4 adjusted EPS came in at $3.08.

Full-year 2025 adjusted EPS reached $10.88, up 53% year over year.

Margins are expanding.

EBITDA now exceeds 20%.

Backlog surged to over $3 billion, up 78% year over year.

That backlog is not theoretical demand. It represents contracted work already in place. Institutions pay attention to visibility like that.

🚀 The Real Catalyst

AI does not live in the cloud. It lives in data centers.

And data centers require:

• Electrical infrastructure

• Power grid expansion

• Concrete and site development

• High-capacity utility buildout

STRL sits directly in that pipeline.

This is not a short-term theme. It is a structural capex cycle that could last years.

📈 Leadership Metrics

Composite Rating: 97

EPS Rating: 99

Those numbers place STRL among the strongest growth profiles in the market. The stock has dramatically outperformed the major indices over the past year, which is exactly what true leaders do before their next major advances.

⚡ Supply and Demand

Roughly 30 million shares in the float.

Strong institutional participation.

Short interest meaningful enough that momentum could amplify if price pushes higher.

When fundamentals strengthen and supply remains tight, price movement can accelerate faster than most expect.

📊 Technical Structure

The stock is consolidating after a powerful run. Resistance sits near the 475 area. Support around 392. The 50-day zone near 350 is major support.

This is not a broken chart. It is digestion after strength.

Late-stage bases require discipline, but they also tend to occur in names that institutions already trust.

💡 Big Picture

Yes, valuation is elevated near 45 times earnings. But premium multiples are typically assigned to companies showing premium growth and expanding margins inside structural demand cycles.

The broader market remains under pressure, which always adds risk. But when the market stabilizes, capital usually flows first into companies with:

• Real earnings acceleration

• Expanding margins

• Strong backlog

• Institutional sponsorship

• Structural tailwinds

STRL checks those boxes.

Sometimes the story is complicated.

This one is straightforward: execution backlog AI infrastructure.

Now it simply needs price confirmation to reflect the fundamentals already in place.

THE FOLLOWING IS FOR EDUCATIONAL PURPOSES IT IS NOT A RECOMMENDATION TO BUY OR SELL SECURITIES YOU MUST DO YOUR OWN RESEARCH AND CONSULT A PROFESSIONAL.

#alphatitancapital #stockmarket #education #spy #spx #qqq #ndx #dia #djx #finance #economic #bitcoin #wallstreet #nasdaq #sp500 #treasury #ai #artificialintelligence #cnbc #bloomberg #FT #foxbusiness #forex #STRL #infrastructure #datacenters #IBD #CANSLIM

56

Oil isn’t just a commodity right now.

It’s leverage. 🌍🛢️

If the Strait of Hormuz closes, the first shockwave doesn’t hit Texas. It hits Asia.

~20 million barrels per day move through Hormuz.

About 84% of that crude heads to Asia.

China, India, Japan, South Korea.

Now layer in Venezuela.

Venezuela holds ~300 billion barrels in reserves. But production is barely ~1 million bpd after decades of mismanagement and sanctions.

Here’s where it gets strategic:

More than half of Venezuela’s recent crude exports have ended up in China, often routed through “shadow” shipping networks. Those barrels feed China’s small independent “teapot” refineries that rely on discounted sanctioned crude to survive.

Now the U.S. is tightening control over Venezuelan oil flows through OFAC licensing and “authorized channels.” 🇺🇸

At the same time, Washington has openly framed Latin America as a strategic zone where it intends to limit Chinese influence.

Think about the positioning:

• Hormuz = China’s largest external oil chokepoint

• Venezuela = discounted heavy crude lifeline

• U.S. policy = tightening control over Western Hemisphere energy flows

If Hormuz gets disrupted and Venezuelan barrels are restricted, the pressure lands disproportionately on China’s energy security.

And here’s the twist most miss:

Venezuela cannot meaningfully move global oil prices in the short term. Years of underinvestment and infrastructure decay mean recovery will take billions and time. ⏳

So this isn’t about “flooding the market.”

It’s about strategic leverage.

Energy is being used as foreign policy again.

Are markets pricing that geopolitical risk correctly? 👀📈

#alphatitancapital #stockmarket #education #spy #spx #qqq #ndx #dia #djx #finance #economic #bitcoin #wallstreet #nasdaq #sp500 #treasury #ai #artificialintelligence #cnbc #bloomberg #FT #foxbusiness #forex

93

10 Nov 2025

📊 BigBear.ai $bbai (NYSE: BBAI) Expands Its Secure AI Footprint With Ask Sage Acquisition — A Potential Catalyst for Future Momentum 🚀

BigBear.ai just delivered one of its most strategically important updates yet, announcing a definitive agreement to acquire Ask Sage, a fast-growing Generative AI platform already deployed across highly regulated sectors, national security operations, and mission-critical government environments.

This move signals a powerful step forward in positioning BigBear.ai as a top-tier provider of secure, integrated AI solutions for defense and enterprise customers.

✅ Transformational Ask Sage Acquisition

Under the agreement, BigBear.ai will acquire Ask Sage for $250M, subject to standard adjustments. Ask Sage is expected to generate ~$25M ARR in 2025, representing ~6x annual growth from 2024.

Key advantages:

Serves 100,000 users

Deployed across 16,000 government teams

Used by hundreds of commercial enterprises

Purpose-built for secure LLM delivery, agentic AI, and classified environments

CEO Kevin McAleenan summarized it clearly:

“We are creating what the market has been asking for — a secure, integrated AI platform that connects software, data, and mission services in one place.”

This acquisition arrives at the exact moment government agencies are accelerating demand for trusted, secure AI technologies.

✅ Financial Strength Hits a New Peak

BigBear.ai ends the quarter with remarkable liquidity strength:

Record cash balance: $456.6M

Sequential improvement to the balance sheet

Backlog: $376M

With this level of liquidity, BigBear.ai is well-positioned to scale faster than at any time in its history.

✅ Q3 2025: A Strategic Transition Quarter

Although revenue declined YoY due to timing of Army program volumes, the company delivered meaningful positive signals:

Revenue: $33.1M

Gross margin: 22.4%

Net income turns positive:

$2.5M, compared to ($15.1M) last year

SG&A increases tied to growth initiatives and Ask Sage alignment

BigBear.ai remains on track to achieve:

2025 Revenue: $125M – $140M

Ask Sage is not included in current guidance, leaving room for future upside.

✅ A Potential Short-Squeeze Setup: Why the Stock Could See Upward Momentum

While this is not a prediction or recommendation, it is important to highlight a market structure dynamic that could support upward momentum:

BigBear.ai has a high short-interest rate relative to float

The stock now has:

Strong liquidity

A game-changing acquisition

Clear government tailwinds

A significantly improved balance sheet

Growing demand for secure, classified AI systems

When a company strengthens fundamentals at the same time shorts are heavily positioned, the setup can create conditions where short covering accelerates upside price movement.

This is not guaranteed, and investors must always perform their own analysis — but the data suggests this added factor could help fuel momentum as BigBear.ai transitions into a materially stronger business model for 2026 and beyond.

✅ Long-Term Vision: Building the Secure AI Operating System for National Defense

BigBear.ai is constructing a unified ecosystem that integrates:

Generative AI

Agentic AI systems

Data fusion

Mission analytics

Secure deployment environments

Defense-grade compliance layers

The Ask Sage acquisition reinforces BigBear.ai’s path toward becoming the centralized, secure AI platform for the U.S. defense community, border-security operations, and mission-critical government partners.

With:

A record cash position

Expanding ARR pipeline

Strong demand for secure AI

Government contracts expected to accelerate post-shutdown

A full integration of Ask Sage ahead

BigBear.ai enters 2026 with powerful tailwinds.

🔔 Disclosure: This post is for educational purposes only and does not constitute financial advice. Always conduct your own research before investing.

#alphatitancapital

#BBAI #BigBearAI #AskSage #AI #DefenseTech #NationalSecurity #SecureAI #MachineLearning #ArtificialIntelligence #DataAnalytics #DoD #BorderSecurity #StockMarket #WallStreet #Nasdaq #SP500 #Economic #Technology #GenerativeAI #AgenticAI #CNBC #Bloomberg #FoxBusiness #treasury #forex

146

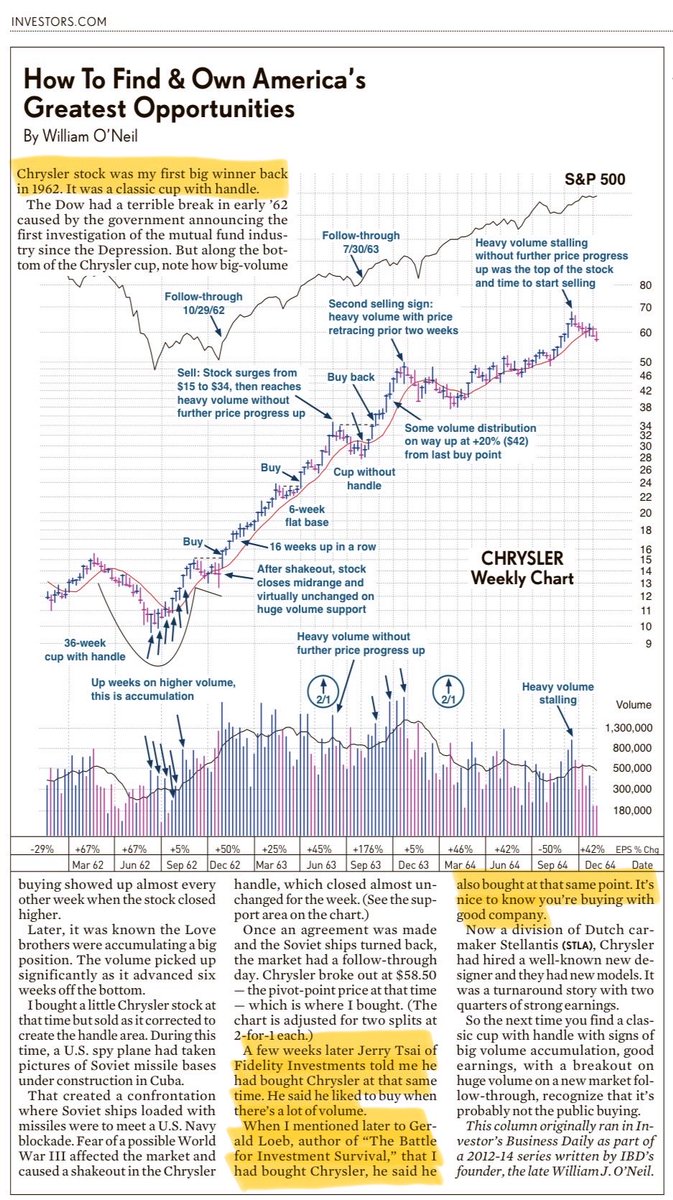

Alpha Titan Capital retweeted

26 Jul 2025

From IBD this weekend. O’Neil’s first big Monster Stock. Loeb also landed this big winner as well.

12

30

196

18,725

6 Aug 2025

📊 Zeta Global (NYSE: ZETA) Q2 2025 Earnings Highlight AI-Driven Momentum and Strategic Growth 🚀

Zeta Global closed at $15.87 on August 5, 2025, and traded higher in after-hours at $17.33, up 9.2%, reflecting strong investor confidence following robust Q2 results.

Key Financial Highlights:

•Revenue surged 35% year-over-year to $308 million, beating guidance by $11 million.

•Net cash from operations grew 35% to $42 million.

•Free cash flow soared 69% to $34 million.

•The company utilized $85 million of its $100 million share repurchase authorization and announced a new $200 million buyback program.

•Zeta ended Q2 with zero net dilution versus Q1 2025, showcasing disciplined capital management.

Consistent ‘Beat and Raise’ Performance:

For the 16th consecutive quarter, Zeta has exceeded expectations and raised guidance, a testament to its strong operational execution and growing demand for AI-powered marketing solutions. CEO David A. Steinberg points to the transformative impact of their AI platform, “Zeta Answers,” as a key growth driver.

Strategic Growth Drivers:

•AI-Centric Innovation: Leveraging advanced machine learning and vast data analytics, Zeta delivers superior consumer insights and marketing automation, driving customer acquisition and retention for enterprise clients.

•Expanding Market Penetration: New platform deployments, agency expansions, and strategic wins continue to grow Zeta’s market share.

•Shareholder Value Focus: Aggressive stock repurchases underline management’s confidence and commitment to maximizing shareholder returns.

•Transparent Investor Relations: Engagements such as Investor Day and the Zeta Live conference highlight the company’s long-term vision and innovation roadmap.

Raised Guidance Reflects Strong Confidence:

•Q3 2025 revenue guidance increased to $327M - $329M (22-23% YoY growth).

•Q3 adjusted EBITDA guidance raised to $70.3M - $71.0M (31-32% YoY growth).

•Full-year 2025 revenue forecast now at $1.258B - $1.268B (25-26% growth).

•Full-year adjusted EBITDA projected between $263.6M - $265.6M (37-38% growth).

•Free cash flow expected to rise 52-56% YoY to $140M - $144M.

Financial Strength & Valuation:

•Market capitalization near $1.84 billion with a strong cash position of $559 million, ensuring ample liquidity and strategic flexibility.

•Top institutional holders include CEO David Steinberg with ~11.6% ownership, Vanguard Group at 10.4%, and BlackRock holding 7.1%, reflecting deep institutional confidence.

Long-Term Growth Outlook:

Zeta Global is well-positioned at the cutting edge of AI-driven marketing technology, an industry set for significant expansion as enterprises adopt data-driven approaches to consumer engagement. With its innovative platform, disciplined execution, and robust financial health, Zeta is poised for sustainable growth and expanding market leadership in the years ahead.

⸻

🔔 Disclosure: This post is for educational purposes only and does not constitute financial advice. Please perform your own due diligence before making investment decisions.

⸻

#alphatitancapital #ZETA #ZetaGlobal #AI #MarketingTech #CloudPlatform #StockMarket #Finance #SP500 #Nasdaq #WallStreet #Investing #DataDriven #ArtificialIntelligence #CNBC #Bloomberg #FoxBusiness

96

6 Aug 2025

📢 Opendoor Technologies Inc. (NasdaqGS: OPEN) — A comprehensive update on Q2 2025 earnings and outlook. #alphatitancapital #stockmarket #education #finance #economic #wallstreet

• Opendoor reported Q2 revenue of $1.6B, beating forecasts by 6.67%, reflecting continued momentum despite market challenges.

• Earnings per share came in at a loss of $0.04, slightly missing the expected loss of $0.03, highlighting profitability pressures amid strategic shifts.

• The company achieved its first quarter of adjusted EBITDA profitability in three years, reporting $23M adjusted EBITDA vs. -$5M in Q2 2024.

• Inventory stands at 4,538 homes valued at $1.5B, positioning Opendoor well to capture future market opportunities.

• Strong liquidity with unrestricted cash of $789M, supporting operational needs and strategic investments.

• Free cash flow remains under pressure but showed signs of stabilization, important for ongoing capital allocation.

• Opendoor is expanding its go-to-market strategy by partnering with real estate agents, introducing a diversified sales platform that combines cash offers with agent listings to improve conversion and asset-light revenue.

• Focus remains on pricing discipline, operational efficiencies, and optimizing marketing spend to reduce costs and improve margins.

• Macro headwinds persist: elevated mortgage rates and a cooling housing market continue to pressure buyer demand and home acquisitions.

• The company projects Q3 2025 revenue between $800M-$875M with a planned slowdown in home acquisitions to 1,200 homes due to market uncertainty.

• Despite beating revenue expectations, Opendoor’s stock fell sharply by 24% in after-hours trading to $1.90, reflecting ongoing investor caution.

• Top institutional holders include:

•Vanguard Group: 9.1% (~66.4M shares)

•Access Industries: 7.3% (~53.6M shares)

•T. Rowe Price Group: 3.0% (~21.6M shares)

•Vanguard Total Stock Market ETF: 2.7% (~19.8M shares)

•Vanguard Real Estate ETF: 2.5% (~18.1M shares)

• Financial fundamentals:

•Market Cap: $1.84B

•EV: $3.8B

•Gross Margin: 8.2%

•EBITDA Margin: -4.3%

•Operating Margin: -5.2%

•Net Margin: -7.2%

•Strong current ratio of 2.99, indicating solid liquidity.

• Growth drivers include leveraging agent partnerships, pricing discipline, and operational efficiencies to drive revenue growth and margin expansion.

• Key risks remain macroeconomic uncertainty, housing market volatility, pricing accuracy, competition, and reliance on debt financing.

• CEO Carrie Wheeler emphasizes a strategic shift towards a distributed platform model providing customers more selling choices, aiming for long-term scalability and relevance.

⸻

Disclosure: This is an educational overview only, not a buy or sell recommendation. Always conduct your own research or consult a financial advisor before investing.

#alphatitancapital #stockmarket #education #finance #economic #wallstreet #nasdaq #SPX500 #realestate #housingmarket #investment #investing #stocks #earnings #OpenDoor #OPEN @ericjackson @Opendoor @CNBC @Vanguard_Group @TRowePrice @

190

6 Mar 2025

📊 Broadcom (AVGO) Reports Record Q1 Revenue & AI Growth 🚀

Broadcom Inc. (NASDAQ: AVGO) just delivered blowout Q1 2025 earnings, driven by massive AI semiconductor demand and infrastructure software expansion. Here’s what you need to know:

✅ Revenue: $14.9B ( 25% YoY)

✅ AI Revenue: $4.1B ( 77% YoY)

✅ Infrastructure Software Revenue: $6.7B ( 47% YoY)

✅ GAAP Net Income: $5.5B vs. $1.3B last year

✅ Non-GAAP Net Income: $7.8B vs. $5.3B last year

✅ Free Cash Flow: $6.0B ( 28% YoY)

✅ Quarterly Dividend: $0.59 per share

💡 Q2 2025 Guidance:

📈 Expected revenue: ~$14.9B ( 19% YoY)

📊 Adjusted EBITDA: ~66% of revenue

⚡ AI Revenue Forecast: $4.4B, driven by strong hyperscale demand for AI XPUs & connectivity solutions

🔥 Key Takeaways:

Broadcom is firing on all cylinders, with AI demand accelerating and infrastructure software expanding rapidly post-VMware acquisition. The company’s record-high adjusted EBITDA of $10.1B ( 41% YoY) underscores strong operational execution and cash flow generation.

After a challenging start to 2025 for AI stocks, Broadcom’s guidance is the kind of upside the market needed. With hyperscalers ramping up AI investments, AVGO remains a key player in AI infrastructure.

📉 Stock Movement:

After dropping 6.3% Thursday, AVGO jumped 9.6% in after-hours trading on this bullish report. Is this the next AI stock to watch?

🔎 What’s Next?

Broadcom’s strategic focus on AI semiconductors & software integration is paying off. With a strong balance sheet and record-setting profitability, the stock could be poised for a recovery after its recent pullback.

🚨 Disclosure: This post is for educational purposes only and does not constitute financial advice. Do your own research before investing.

#alphatitancapital #AVGO #Broadcom #AIstocks #stockmarket #semiconductors #earnings #finance #economic #Sp500 #nasdaq #wallstreet #treasury #CNBC #bloomberg #foxbusiness #investing

1

119

2 Mar 2025

📊 March Market Trends: What History Tells Us About the S&P 500 📈

As we enter March 2025, let’s take a look at how the S&P 500 has historically performed during this month and what it could mean for investors.

📅 March Returns Over the Last 5 Years:

✅ 2024: 3.10%

✅ 2023: 3.51%

✅ 2022: 3.58%

✅ 2021: 4.24%

❌ 2020: -12.51% (Pandemic market crash)

📊 Long-Term March Trends:

🔹 Last 10-Year Average: 1.97%

🔹 Last 20-Year Average: 1.50%

🔹 March 2009: Biggest gain at 8.54% (Post-recession bounce)

🔹 March 2020: Sharpest decline at -12.51% (COVID-19 crisis)

What This Means for March 2025:

🚀 Historically, March tends to be one of the stronger months for the S&P 500. Over the past 20 years, it has delivered positive returns nearly 70% of the time.

📈 The S&P 500 is coming off a strong January 2025 ( 2.70%), which is above its long-term monthly average (0.59%). If this momentum continues, March could see another positive month—but market conditions remain key.

🔍 Key Factors to Watch This March:

⚡️ Interest rate policies from the Federal Reserve

💰 Earnings season updates from major S&P 500 companies

🌎 Macroeconomic data releases (inflation & jobs reports)

📊 Investor sentiment & technical market trends

🚨 Final Thoughts: While history suggests March can be a bullish month, past performance is not a guarantee of future returns. The market remains dynamic, so investors should always do their own research and manage risk accordingly.

#MarketAnalysis #MarchOutlook #SP500Performance #StockMarket #Investing #WallStreet #Finance #AI #EconomicTrends #AlphaTitanCapital

📢 Disclosure: This post is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal.

8

17,653

19 Feb 2025

📈 Cheesecake Factory (NASDAQ: CAKE) Reports Strong Q4 Earnings—Record Growth and Expansion Plans! 🍰🚀

Cheesecake Factory (CAKE) delivered another quarter of strong financial performance, reporting Q4 earnings of $1.04 per share, beating estimates of $0.92 by 13.04%. This marks a 30% YoY increase, demonstrating the company’s continued strength in the casual dining sector.

Key Q4 Financial Highlights:

✅ Revenue: $921M ( 5% YoY), surpassing analyst expectations

✅ Net Income: $41.2M, with adjusted earnings of $1.04 per share

✅ Comparable Restaurant Sales: 1.7% YoY, outpacing the casual dining industry

✅ Operating Margin Growth: Driven by customer demand, efficiency, and expansion

💡 Growth & Expansion Strategy

The Cheesecake Factory is capitalizing on its brand strength by:

🍽️ Opening 23 new restaurants in 2024, surpassing development expectations

🍽️ Announcing up to 25 new openings in 2025, including North Italia and Flower Child locations

🍽️ Investing in guest experience, digital marketing, and loyalty programs to drive traffic and sales

💰 Financial Strength & Shareholder Value

🔹 Total Liquidity: $340.7M (cash & credit availability)

🔹 Debt Management: $455M in total principal debt

🔹 Dividend Growth: $0.27 per share declared for March 2025

🔹 Stock Buybacks: 11,800 shares repurchased in Q4

🔥 Why CAKE Looks Promising in 2025

🔹 Strong Market Share: Outperforming the casual dining sector

🔹 Operational Efficiency: Expanding margins & revenue growth

🔹 Consumer Demand: Premium dining experience remains in high demand

🔹 Expansion Strategy: Up to 25 new locations planned in 2025

The company’s record-breaking year and ambitious expansion plans signal confidence in continued revenue growth, margin expansion, and customer loyalty in 2025 and beyond.

📊 Final Thoughts:

Despite market volatility, Cheesecake Factory continues to outperform expectations, solidifying its position as a leader in experiential dining. Investors looking for consistent growth and strong fundamentals should keep an eye on CAKE as it scales operations and expands its market presence.

🚨 Disclosure: This information is for educational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

#CheesecakeFactory #CAKE #StockMarket #Earnings #Investing #CasualDining #Finance #WallStreet #GrowthStocks #MarketTrends #alphatitancapital #stockmarket #spy #spx #qqq #ndx #dia #djx #economic #wallstreet #nasdaq #s&p500 #treasury #ai #artificialintelligence #cnbc #bloomberg #FT #foxbusiness #forex #alphatitancapital

1

1

14

752

19 Feb 2025

📈 Carvana (CVNA) Reports Record Earnings – The Growth Story Continues! 🚗💨

Carvana (NYSE: CVNA) just delivered explosive Q4 results, crushing expectations and setting records across the board! 🔥

Key Highlights:

✅ EPS: $0.56 (Beat by 166.67% vs. $0.21 expected)

✅ Revenue: $3.55B ( 46% YoY) 🚀

✅ Full-Year Revenue: $13.67B ( 27% YoY)

✅ Net Income: $404M – Highest in company history

✅ Retail Units Sold: 416,348 ( 33% YoY)

✅ Adjusted EBITDA Margin: 10.1% – Industry-leading

Why This Matters:

💡 Carvana is now the most profitable public auto retailer in U.S. history (by Adjusted EBITDA margin).

📈 50% YoY growth in Q4 retail unit sales – a clear sign of strong demand.

🔮 2025 Outlook: Management expects continued growth in units sold and EBITDA, reinforcing long-term confidence.

CEO Ernie Garcia summed it up best:

“With just ~1% market share today and many opportunities to improve and expand, we know this is just the beginning of our journey to change the way people buy and sell cars.”

Market Impact:

🔹 CVNA stock surged after earnings, reflecting investor optimism.

🔹 Strong execution is fueling profitability alongside aggressive expansion.

Carvana is proving that its digital-first e-commerce model is revolutionizing the used car industry while driving unprecedented growth and profitability.

🛑 Disclosure: This is for educational purposes only and not financial advice. Always do your own research before investing.

#Carvana #CVNA #Earnings #StockMarket #Investing #Finance #Automotive #GrowthStocks #WallStreet #SPX #QQQ #AI #Nasdaq #Treasury #CNBC #Bloomberg #Forex #StockTrading #Economic #alphatitancapital 🚀

1

3

721

18 Feb 2025

🚀 Arista Networks (ANET) Delivers Strong Q4 Earnings & AI-Driven Growth! 📈🔗

✅ Revenue: $1.93B ( 25% YoY) – Beat expectations

✅ EPS: $0.65 vs. $0.57 expected ( 25% YoY)

✅ Cash Flow: 95% YoY, boosting strategic investments

✅ Guidance: Q1 revenue outlook of $1.93B-$1.97B, ahead of estimates

✅ AI & Cloud Expansion: Driving long-term growth with partnerships like Meta & Microsoft

💡 Why This Matters?

Arista is a leader in high-performance networking solutions, powering AI-driven data centers. With AI adoption surging, demand for Arista’s infrastructure solutions remains strong.

📊 Technical Strength:

🔹 Relative Strength Rating: 96/99

🔹 IBD Composite Rating: 98/99

🔹 A/D Rating: B- (steady institutional support)

💰 Key Takeaways:

✅ Beating top & bottom-line expectations

✅ Expanding presence in AI, data center, and enterprise markets

✅ Strong cash flow supports continued innovation & expansion

AI demand = long-term tailwinds for Arista! 🌎💡

#alphatitancapital #Arista #ANET #AI #Networking #CloudComputing #StockMarket #Investing #TechStocks #Earnings #Nasdaq #Finance #ArtificialIntelligence #alphatitancapital #spy #spx #qqq #ndx #dia #djx #bitcoin #wallstreet #bloomberg #cnbc #foxbusiness #treasury #forex

🛑 Disclosure: This is for educational purposes only and not financial advice. Do your own research before investing.

1

1

6

530

3 Feb 2025

📉 Stock Market Reverses as Trump’s Tariff Move Rattles Investors; Jobs Report & Economic Data in Focus 📈

The stock market ended lower Friday as President Donald Trump’s new tariffs on China, Canada, and Mexico drove uncertainty across financial markets. Treasury yields ticked higher as investors adjusted expectations for economic growth, inflation, and Federal Reserve policy ahead of a critical January jobs report and key economic data this week.

🔻 Market Overview: Volatility Returns

•Nasdaq Composite: Dropped 0.3%, staying above the 50-day moving average, but posted a 1.6% weekly loss.

•S&P 500: Fell 0.5%, yet held above 6,000 and remains up 2.7% YTD.

•Dow Jones Industrial Average: Declined 0.8%, though it rose 0.3% for the week and 4.7% in January—outperforming other major indexes.

•Russell 2000: Small caps fell 0.8%, struggling at the 50-day moving average, but ended the month up 2.5%.

•Trading volume increased, signaling institutional selling pressure, as decliners outpaced advancers nearly 3-to-1 on the NYSE and 2-to-1 on the Nasdaq.

🚨 Trump’s Tariffs Send Shockwaves Through Markets

•The White House announced 25% tariffs on Mexico and Canada and a 10% tariff on Chinese goods, effective Saturday.

•Treasury yields rose as markets priced in potential inflationary pressures and the impact on trade-dependent industries.

•Canada & Mexico are expected to retaliate, adding further uncertainty to global trade relations.

Markets are now grappling with the impact of protectionist policies, as well as the long-term implications for supply chains, corporate earnings, and economic growth.

📰 Key Economic Data This Week

•Monday: Construction spending & auto sales data

•Tuesday: Factory orders & Job Openings (JOLTS) report

•Wednesday: ADP Employment Report & final U.S. services PMI reading

•Friday: January Jobs Report – Analysts expect 256,000 jobs added, with wage growth and labor force participation in focus.

💡 The Federal Reserve’s next steps will likely hinge on labor market strength, inflation trends, and wage growth, as policymakers assess whether further interest rate adjustments are needed.

📊 Sector Watch: Energy & Tech Weakness, Consumer Discretionary Gains

•Sectors that Declined:

•Technology & Energy saw the biggest losses as tariff concerns and rising Treasury yields weighed on sentiment.

•Sectors that Outperformed:

•Consumer Discretionary & Communication Services managed to stay in the green despite broader market weakness.

•Industries Facing Headwinds:

•Oil & gas, drugstores, and commodity-sensitive stocks suffered losses amid uncertainty around trade policies and global growth expectations.

•Industries Showing Strength:

•Plastics, fiber optics, and mobile home manufacturers saw resilient demand, bucking the broader market trend.

⏳ Market Outlook: Volatility Ahead

With Trump’s tariff policies, key economic data releases, and shifting Federal Reserve expectations, investors should prepare for increased market fluctuations.

🔎 Key focus areas:

✅ Labor market strength & wage growth trends

✅ Sector rotation—where institutional money is flowing

✅ Inflation expectations & Fed policy signals

✅ Potential impact of trade tensions on corporate earnings

A measured approach remains crucial—staying diversified, monitoring sector trends, and adjusting risk exposure accordingly will be key as markets digest macroeconomic and geopolitical developments.

🛑 Disclosure: This post is for educational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

#alphatitancapital #stockmarket #education #spy #spx #qqq #ndx #dia #djx #finance #economic #bitcoin #wallstreet #nasdaq #sp500 #treasury #ai #artificialintelligence #cnbc #bloomberg #FT #foxbusiness #forex #interestrates

141

29 Jan 2025

📊 Stock Market Update: Key Earnings, AI Stocks & Federal Reserve Decision Ahead! 🚀📉

The markets rebounded Tuesday, with the Nasdaq leading the charge after AI-led losses on Monday. Tech stocks bounced back, and AI software stocks showed strength, signaling new opportunities. 💡📈

🔹 Key Developments:

✅ Nvidia (NVDA) surged 8.8%, reclaiming the 200-day line after Monday’s sharp drop.

✅ Microsoft (MSFT), Meta (META), Tesla (TSLA), & ServiceNow (NOW) report earnings Wednesday—major market movers ahead!

✅ AI software leaders like ServiceNow, Shopify (SHOP), CrowdStrike (CRWD), and Snowflake (SNOW) flashed buy signals.

✅ Dow Jones ( 0.3%) neared all-time highs, while the S&P 500 ( 0.9%) & Nasdaq ( 2%) rebounded sharply.

🔹 Federal Reserve & Treasury Yields

The Fed meeting concludes Wednesday with a 2 p.m. ET announcement & 2:30 p.m. ET press conference by Jerome Powell. Markets are watching closely for clues on future rate cuts and economic outlook. 🏦⚠️

📉 The 10-year Treasury yield fell to 4.53% Tuesday, while oil prices climbed to $73.77 per barrel.

🔹 Earnings Highlights:

🔸 Starbucks (SBUX) and F5 Networks (FFIV) beat expectations.

🔸 Tesla (TSLA) Earnings Watch: Stock is near the 50-day line—a post-earnings breakout could set up new opportunities.

🔸 Meta & Microsoft: Tech sector awaits key insights into AI growth & capital spending trends.

🔹 AI Stocks & Market Shifts:

Monday’s AI hardware sell-off shook the market, but software-focused AI stocks rebounded strongly. 📊

🔹 What This Means for Investors:

The market rally showed real strength Tuesday, but major earnings reports & Fed policy could drive the next big move. 📈💰

📌 Key Strategies:

🔹 Watch for AI stock recoveries and software strength.

🔹 Prepare for earnings volatility—Tesla, Microsoft & Meta are major catalysts.

🔹 Stay flexible with risk management strategies during key Fed announcements.

💡 Your Take? Will earnings push the market higher, or is volatility ahead? Comment below! 👇💬

#StockMarket #Investing #TechStocks #Nvidia #Tesla #Microsoft #Meta #ServiceNow #AIStocks #Earnings #Finance #NASDAQ #DowJones #OptionsTrading #FederalReserve #alphatitancapital #earnings #education #StockMarket

65

19 Nov 2024

📊🔥 Palantir (PLTR) Daily Chart Analysis: Momentum Continues! 🚀💼

$PLTR hit all-time highs within the last few trading days at $66, driven by robust earnings that smashed top and bottom-line expectations last week. After this incredible rally, we’re seeing key levels shaping up on the daily candlestick chart. Here’s the breakdown:

Key Levels to Watch:

🔻 Pullback & Support:

•Retracement to $61.26, finding solid support in the zone of $58.29-$58.12 (a previous support level on the daily chart).

📈 Upside Targets:

•Next Price Target: $71.89 🔥

•Fibonacci Extension: $79.18 🎯

Why the Momentum?

Palantir’s price appreciation is fueled by:

1️⃣ Beating earnings estimates in both revenue and EPS last week.

2️⃣ Continued uptrend momentum confirmed by technical signals.

3️⃣ Positive sentiment in the AI sector, where $PLTR is a dominant player.

Trend Analysis:

•Current Trend: Uptrend remains intact.

•Volume: Strong buying interest supporting the rally.

•Potential Continuation: The trend suggests further gains if $58 support holds.

Final Notes:

Palantir has delivered remarkable growth recently, but remember, trends can shift, and pullbacks are natural. Monitor key levels for opportunities while staying informed about broader market conditions.

🛑 Disclosure: This is for educational purposes only and NOT financial advice. Always conduct your own research or consult a financial advisor before investing.

What’s your view on $PLTR’s momentum? Is $71.89 next, or are we aiming for $79.18? Drop your thoughts below! 👇⬇️

#PLTR #Palantir #StockMarket #QQQ #spy #SPX #alphatitancapital #AIStocks #TechnicalAnalysis #Fibonacci #Investing #Uptrend #FinanceEducation #Tradingeducation

3

2

17

2,702