Joined June 2020

- Tweets 40,952

- Following 1,526

- Followers 3,720

- Likes 197,436

7,750 Photos and videos

Pinned Tweet

May 17

Ajinomoto Co. Inc. 🇯🇵

Der nächste Hidden Champion in der AI-Kaskade 🏘️

Die Firma, die du mit „Ajinomoto“ und Umami-Gewürz (MSG, Hondashi, Gyōza) assoziierst, ist einer der krassesten versteckten AI-Profiteure. Sie halten ca. 95 % Weltmarktanteil am Ajinomoto Build-up Film (ABF) – dem essenziellen Isolier- und Aufbauschicht-Material für High-End-Semiconductor-Substrates/Packaging.

Ohne ABF keine dichten Kupfer-Leiterbahnen in den Substraten von Nvidia H100/B200, AMD, Intel, Broadcom Switch-Chips oder AI-Servern. Es ist der unsichtbare Flaschenhals in der AI-Supply-Chain.

Unternehmen & Produkte

- Gegründet 1909 in Japan, Weltmarktführer bei Aminosäuren und Umami-Produkten (Food & Seasonings ~ Hauptumsatz, aber nicht mehr der Gewinn-Treiber).

- Diversifikation: AminoScience (Biotech/Pharma), Healthcare und vor allem Functional Materials / Electronic Materials

- Das AI-Killer-Produkt: ABF (seit 1999) – ein dünner Film aus Aminosäure-Chemie (Nebenprodukt der Gewürz-Produktion!). Wird schichtweise in Substrates für CPUs/GPUs/AI-Chips aufgebaut. Ermöglicht höhere Layer-Counts, bessere Signal-Integrität und thermische Performance – genau das, was AI-Data-Center brauchen.

Wo in der Supply Chain? Optics

Sehr weit oben / ultra-kritisch, aber unsichtbar.

Nvidia/AMD/Intel → OSATs (z. B. TSMC, Amkor) → ABF-Substrate (Ajinomoto liefert den Film) → fertige AI-Chips/Server.

ABF ist de-facto-Standard für High-End-Anwendungen (AI/HPC/Data Center).

Keine qualifizierten Alternativen in Sicht, Monopol-ähnliche Position. Nachfrage explodiert durch AI-Server-Boom, Kapazitätsengpässe bis mindestens 2027.

Ajinomoto hat Kunden-spezifische Preiserhöhungen für ABF gestartet (bestätigt Mai 2026), plus Weitergabe von Rohstoffkosten – das ist neu und ein Game-Changer (Aktivist Palliser Capital drängt seit Monaten darauf: „most under-monetized AI infrastructure monopoly“).

Margen im Electronic-Materials-Bereich >50 %.

Langfristig: Kapazitätsausbau bis 2030 ( 50 %) neue Fabrik 2032 signalisieren Vertrauen.

Analysten-Konsens (14 Analysten): Outperform / Moderate Buy Durchschnittliches Kursziel ~4.939 JPY (leichte Unterbewertung zum aktuellen Kurs), High 5.500–6.000 JPY. Einige sehen aber deutlich mehr Potenzial durch Preiserhöhungen AI-Demand (EPS-Wachstum massiv).

Fundamentals: FY2026 stark (Gewinn fast verdoppelt durch ABF). FY2027 Guidance: weiteres Umsatz-/Gewinnwachstum. Hohe Cashflow-Generierung, progressive Dividende.

Risiken: JPY-Stärke, Makro. Aber AI-Tailwind überwiegt massiv.

Ajinomoto ist kein „Food-Stock“ mehr – es ist ein reiner AI-Play mit defensiver Food-Basis.

Monopol-Position Preismacht Kapazitätsausbau = asymmetrisches Upside. Genau das, was in der AI-Kaskade (nach Chip-Designern, Foundry, OSATs) als Nächstes re-pricing wird.

Quellen: Company Data, Nikkei, WSJ, Analystenreports,

May 17

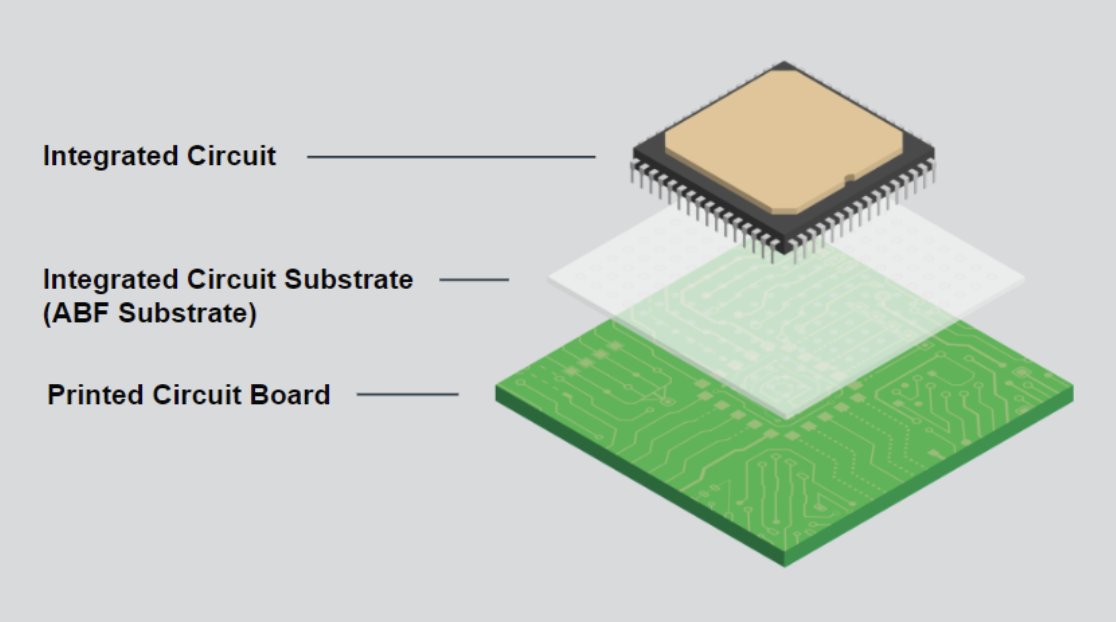

The strangest AI bottleneck might be ABF.

Ajinomoto is better known for MSG, but its build-up film (ABF) is a critical dielectric layer inside the package substrates used for high-end GPUs.

the moat isn't chemical secrecy alone..

it is qualification lock-in process integration reliability history.

and the fact that no chip company wants to risk a $30,000 AI accelerator package to save pennies on dielectric film.

is it a permanent monopoly? Probably not.

but it looks cycle-durable.

if you ask me:

- 1-3 yrs: very hard to replace in high-end AI substrates

- 3-5 yrs: glass substrates and alternatives gain in specific packages

- 5 yrs: package architectures probably shift

To see this, i'm tracking closely whether Nvidia, AMD, Broadcom, TSMC, Ibiden, Shinko and Unimicron show signals for moving away from ABF.

1

2

20

4,360

Björn Sickel 🌍🌏🌎 retweeted

Jun 14

🚨🇬🇧BREAKING: UK Police just arrested a crying 5-year-old boy while taking away his father.

Starmer's police dragged the terrified child into a car, then pepper-sprayed and the father and the man filming everything.

What the hell is happening in Britain?

6,225

24,078

66,118

3,202,499

BLUE SKY SZENARIO für SK Hynix – mit realen Q1-2026-Margen

SK Hynix wird in den nächsten Jahren eine 9.000.000 – 14.000.000 KRW-Aktie

Im Q1 2026 hat SK Hynix bereits Rekordmargen erreicht:

Bruttomarge ~79 %, Betriebsmarge 72 %, Nettomarge 77 %. Das ist kein Zufall – das ist der HBM-Supercycle in Aktion.

Der Markt

Der HBM-Markt explodiert von ca. 35 Mrd. USD (2025) auf 168 Mrd. USD bis 2030. SK Hynix hält aktuell 50–60 % Marktanteil (teilweise bis 69 %) und wird bei HBM4 für NVIDIA Rubin sogar auf ~70 % gesehen.

Die gesamte HBM-Produktion ist bereits durch langfristige Verträge ausgebucht. Engpässe halten voraussichtlich bis mindestens Ende 2027 – wahrscheinlich länger.

Detaillierte Blue-Sky-Rechenlogik (2030)

Umsatz

HBM-Anteil SK Hynix: 55 % von 168 Mrd. USD = 92 Mrd. USD

Rest (DRAM NAND eSSD): 65–75 Mrd. USD

Gesamtumsatz-Potenzial: 160–170 Mrd. USD pro Jahr

Bruttogewinn

Blended Bruttomarge (HBM-dominiert): 74–78 % (nahe den aktuellen 79 %)

Bruttogewinn: 118–133 Mrd. USD

Nettogewinn

Im Blue-Sky-Fall (hohe Auslastung Pricing-Power über Jahre): Nettomarge 50–65 % (deutlich unter dem Q1-2026-Peak von 77 %, aber strukturell hoch)

Jährlicher Nettogewinn: 80–105 Mrd. USD

Bewertung

Als unangefochtener HBM-Weltmarktführer mit dauerhaft hoher Profitabilität: 40–60x Forward P/E

→ Bei 85–95 Mrd. USD Nettogewinn ergibt sich eine Market Cap von 6–9 Billionen USD

Ergebnis:

Blue-Sky-Kursziel 9.000.000 – 14.000.000 KRW (bei ca. 710 Mio. Aktien). Das ist 4–6,5x vom aktuellen Niveau.

Warum das möglich ist

HBM wird zum „Öl des AI-Zeitalters“ – SK Hynix sitzt an der Quelle

Strukturelle Knappheit hoher HBM-Mix halten Margen auf hohem Niveau

Operating Leverage aus den neuen Mega-Fabs wirkt über Jahre

Geopolitischer Vorteil als einer der wenigen High-End-HBM-Produzenten mit direkter NVIDIA-Anbindung

Das ist kein normaler Memory-Zyklus mehr. Das ist ein multi-jähriger struktureller Supercycle – und SK Hynix ist der klarste Gewinner.

Micron will be a $4,000 stock within the next few years and here is why (Save this).

Let's start with the BofA semiconductor forecast in the chart above.

Bank of America models total semiconductor sales reaching $1.3 trillion in 2026, a 65% year over year jump and growing to $2 trillion by 2030.

But strip out the headline number and look at what is doing the work, it's memory.

Memory sales are forecast to grow 168% in 2026 alone, versus just 25% for core semis ex-memory meaning the entire semiconductor supercycle is essentially a memory supercycle, and it is being driven by one product.

That product is high-bandwidth memory, and BofA projects the HBM market to explode from $35 billion in 2025 to $168 billion by 2030, a 37% compound annual growth rate that makes it one of the fastest growing markets in the history of the semiconductor industry.

Now zoom into Micron specifically.

Micron's entire 2026 HBM output is already contracted under long-term supply agreements.

The company has locked in six major AI and cloud customers at fixed prices, meaning the revenue is largely booked.

And despite that, CEO Sanjay Mehrotra has said Micron can only fulfill 50% to two-thirds of what its key customers actually need in the near term.

The supply crunch is not expected to meaningfully ease until late 2027 at the earliest.

Management guided Q3 to $33.5 billion in revenue with 81% gross margins and if achieved, that single quarter would generate over $27 billion in gross profit.

Micron is ramping HBM4 at twice the speed of its HBM3E ramp, the first HBM4E chip is scheduled for introduction in 2027 and the company has committed approximately $200 billion in planned capacity expansion to meet what it describes as a historic memory supply crunch.

A company generating $130 billion annualized revenue by 2027, with 80% gross margins, sold-out capacity, a 20% HBM market share in a $168 billion market, and a geopolitical moat as the only American HBM supplier and that is how you get to $4,000.

Our milk road subscribers are already up Massively on Micron, come join Milk Road Pro for our full breakdown, our complete Micron valuation model and our full AI trade thesis.

Link below!

1

2

8

850

Björn Sickel 🌍🌏🌎 retweeted

Jun 14

“Flower of Scotland” here in Foxborough. #WorldCup

276

3,264

29,403

7,958,381

Björn Sickel 🌍🌏🌎 retweeted

Jun 11

Investing in 2026 is deciding which cartoon character you trust more

106

119

3,192

205,029

Björn Sickel 🌍🌏🌎 retweeted

Jun 11

The atmosphere is stunning 🏆

665

3,456

36,171

1,051,316

SK Hynix plans to list its shares in the US as soon as August, said two sources familiar with the matter, as the South Korean memory chipmaker seeks to capitalise on strong appetite for AI-linked stocks and broaden its investor base reut.rs/3Qd2GNN

18

63

284

60,251

Jun 10

Optics

📣 Get a first look at the NVIDIA Photonics co-packaged optics switch with @LambdaAPI.

At NVIDIA GB300 NVL72 scale, the network doesn't just move data between GPUs — it determines how fast your cluster thinks. Co-packaged optics cut switch power, reduce failure points, and deliver more tokens per watt.

Here's what that looks like in practice. ➡️ nvda.ws/4otSAoz

2

7

464

Björn Sickel 🌍🌏🌎 retweeted

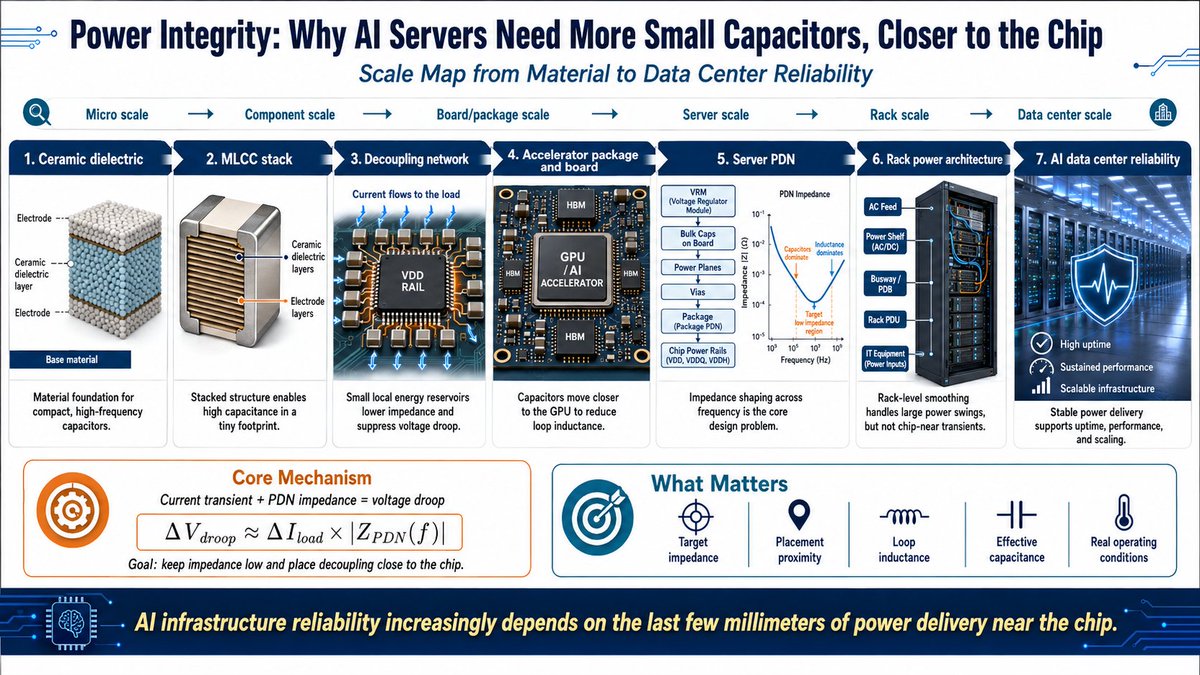

Murata and Japan’s Hidden Electronic Infrastructure

[Part 1. Power Integrity: Why AI Servers Need More Small Capacitors, Closer to the Chip]

Full version: open.substack.com/pub/superp…

The GPU is the chip that does the heavy calculations, but in an AI server the first thing you have to protect is stable voltage. As AI servers get bigger, the power network is no longer just wires. It becomes a system that absorbs sudden power shocks.

When the GPU suddenly pulls a lot of electricity, the system cares more about “keeping the voltage steady” than about raw calculation speed. This is what Power Integrity — power stability — is all about.

1. What matters is not average power, but how fast the power suddenly changes

In AI servers, the real problem is not “how much electricity is used on average.” It is how quickly and sharply the electricity demand changes.

When the GPU starts a big matrix calculation or accesses memory, it pulls a huge burst of current in a very short time. This sudden change causes the voltage to drop for a moment.

If the voltage drops too much, the GPU makes errors or slows down.That is why AI servers need more parts that keep the voltage steady around the GPU.

2. Decoupling capacitors are tiny “electricity reservoirs” right next to the GPU

The main power supply is far away and cannot react instantly when the GPU suddenly needs a lot of current. So engineers place small “electricity reservoirs” right next to the GPU. These are called decoupling capacitors.

When the GPU demands a sudden burst of power, the nearby capacitor quickly supplies electricity and prevents the voltage from dropping. The closer the capacitor is to the GPU, the more stable the voltage stays.

3. Why MLCC (multilayer ceramic capacitors) are so important

The most common capacitor used in AI servers is the MLCC.

It is important for three simple reasons:

It is very small → you can fit many of them on a crowded board

It reacts very fast → perfect for sudden power changes

You can place thousands of them around the GPU

Even though each MLCC is tiny, when you use many together they can quickly supply the electricity the GPU needs. Murata keeps making smaller and better MLCCs specifically for AI servers.

4. Capacitors are moving closer and closer to the GPU

In AI servers, the position of capacitors is changing.

They used to sit far away on the board → then closer to the GPU package → now even inside the package or embedded in the chip.

Why? Because power changes are happening faster and faster. If a capacitor is too far away, electricity takes time to travel and the voltage drops more. So engineers are moving capacitors as close as possible to the GPU.

Murata is also developing silicon capacitors for this exact purpose.

5. Power shocks are solved differently at different layers

Power problems in AI servers do not happen in only one place.

At the whole rack level → big energy storage devices are needed

Right next to the GPU chip → tiny MLCCs and other small capacitors do the job

For example, NVIDIA’s latest AI servers use large storage at the rack level, but still rely heavily on MLCCs right beside each GPU.

The upper layers use higher voltage to send power farther, while the lower layers (near the chip) focus on very low voltage, high current, and ultra-fast changes.

#Murata #MLCC #PowerIntegrity #AIInfrastructure #Decoupling #HiddenAIHardware

3

2

13

1,153

Jun 10

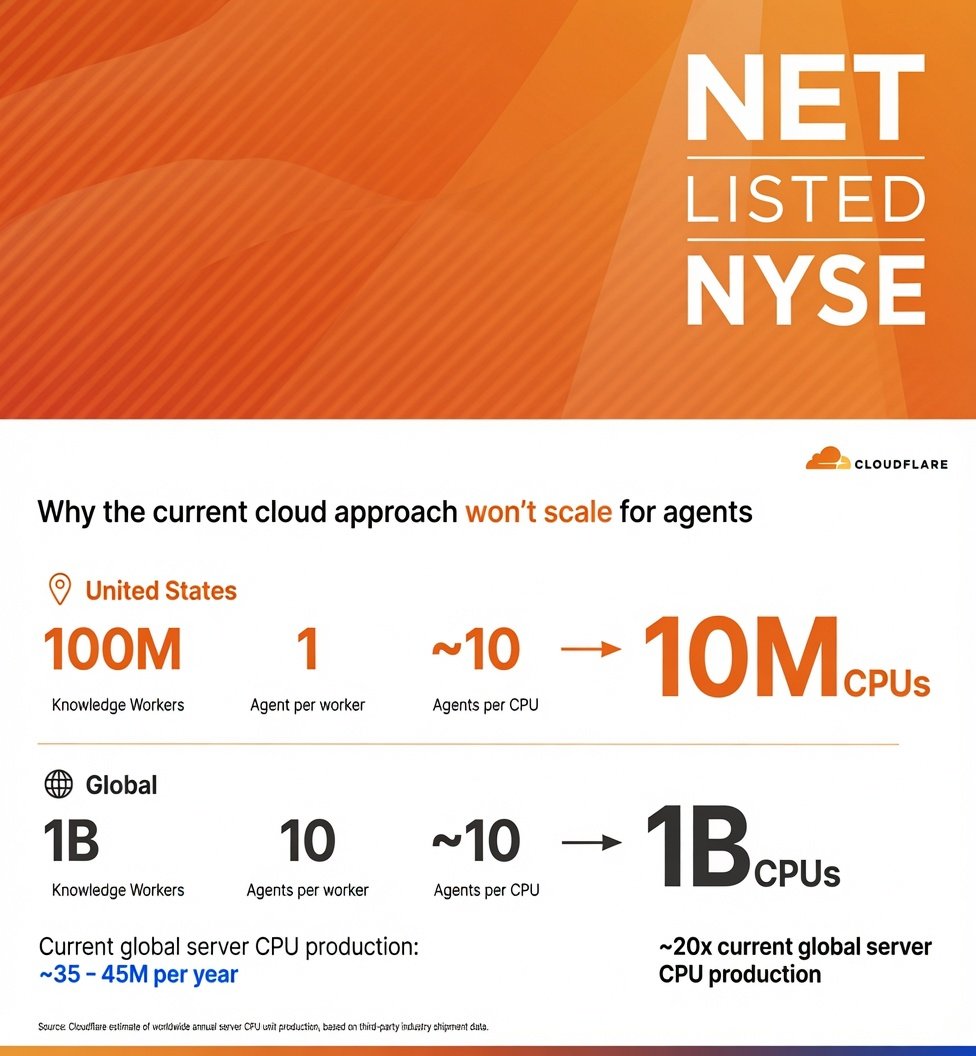

Cloudflare Investor Day – 9. Juni 2026 $NET

Cloudflare zeigt auf diesem Slide sehr deutlich, warum das klassische Cloud-Modell (basierend auf VMs und Containern) bei der Skalierung von autonomen AI Agents an seine Grenzen stößt.

USA:

100 Millionen Knowledge Worker × 1 Agent pro Worker × ca. 10 Agents pro CPU = 10 Millionen CPUs erforderlich

Global:

1 Milliarde Knowledge Worker × 10 Agents pro Worker × ca. 10 Agents pro CPU = 1 Milliarde CPUs erforderlich

Die weltweite jährliche Produktion von Server-CPUs liegt derzeit bei nur 35–45 Millionen Einheiten.

Das globale Szenario würde also etwa das 20-Fache der aktuellen Jahresproduktion erfordern.

Jeder AI Agent erzeugt bei jedem Lauf eine neue, ephemere Anwendungsinstanz. Das passt nicht zum bisherigen Skalierungsmodell der Hyperscaler („ein App-Server für viele Nutzer“).

$NVDA Stark bis extrem bullish – Agents treiben vor allem Inference-Lasten, die direkt auf HBM-bestückten GPUs (Blackwell, Rubin etc.) laufen.

$AMD Deutlich bullish – sowohl bei Server-CPUs als auch bei eigenen GPU/Accelerator-Lösungen.

Intel: Bullish, insbesondere durch den expliziten CPU-Bedarf und die Gaudi-Acceleratoren.

$AMD Sehr bullish – effiziente, skalierbare Architekturen sind für Cloud-native und Edge-Agent-Workloads prädestiniert.

$RMBS Stark bullish – als führender Anbieter von High-Speed-Memory-Interface-IP profitiert das Unternehmen direkt vom HBM-Boom.

HBM-Hersteller (SK Hynix, Samsung, Micron) $DRAM

Extrem bullish – die gesamte HBM-Produktion 2026 ist bereits ausverkauft, Preise und Margen stehen unter weiterem Aufwärtsdruck.

AI Supply Chain

Der Slide unterstreicht nicht nur einen CPU-Engpass, sondern einen strukturellen Nachfrageschock für die komplette Wertschöpfungskette:

Foundries $TSMC

Advanced Packaging (CoWoS etc.), Equipment-Hersteller ( $ASML , $AMAT Applied Materials), Spezialmaterialien, Optik/Interconnects sowie Energie- und Data-Center-Infrastruktur.

Die Skalierung von AI Agents erfordert ein massives Hochfahren der gesamten Halbleiter- und Infrastrukturkapazitäten – weit über das hinaus, was heute verfügbar ist.

1

7

992

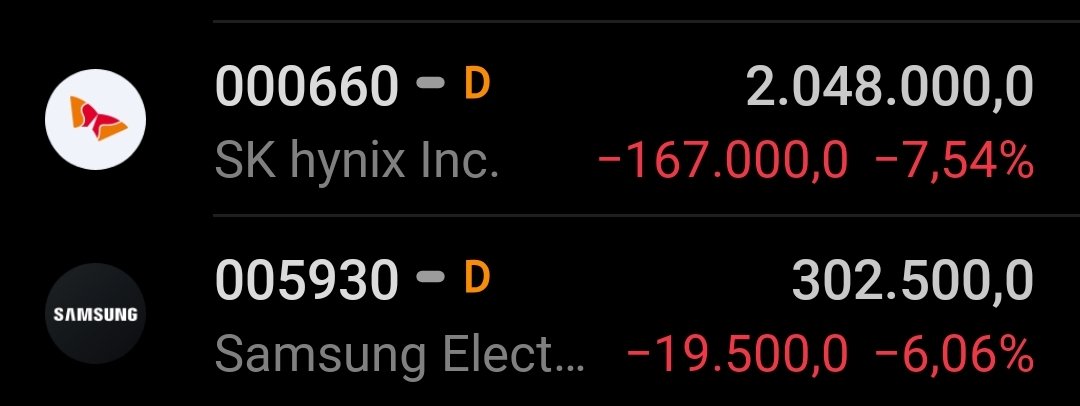

Jun 10

Höchste Zielkurse (inländische Broker)

- Samsung Electronics:

SK Securities mit 610.000 KRW (347 €)

- SK Hynix: SK Securities mit 4.000.000 KRW (2.273 €)

Häufig genannte gemeinsame Annahmen der Analysten

1. Starke Ausweitung der AI-Server-Nachfrage

2. Längerfristige Verknappung des Speicherangebots

3. Steigende HBM-Preise

4. Robuste Preisentwicklung bei Standard-DRAM und NAND

5. Verbesserte Ergebnisvisibilität durch langfristige Lieferverträge (LTA)

6. Neubewertung der Bewertung von Speicherherstellern

Jun 10

[필독] 최근 2개월 내 삼성전자·SK하이닉스 목표주가 리포트 정리 (2026.04.10~06.10, 공개 보도 기준)

같은 증권사에서 여러 번 나온 경우 최신 목표가 기준입니다. 원문 리포트 전수조사는 아니고, 언론/증권사 공개 요약에서 확인된 숫자만 정리했습니다. 투자 권유 아님.

[삼성전자 목표주가]

SK증권 61만원(6/1)

노무라 59만원(5/15)

한국투자증권 57만원(5/20)

미래에셋증권 55만원(5/27)

신한투자증권 55만원(5/21)

KB증권 53만원(5/28)

JP모건 48만원(5/18)

골드만삭스 48만원(5/31)

씨티 46만원(5/11)

키움증권 33만원(5/11)

LS증권 32만원(5/11)

하나증권 30만원(4/10)

[SK하이닉스 목표주가]

SK증권 400만원(6/1)

노무라 400만원(5/15)

미래에셋증권 380만원(5/27)

한국투자증권 380만원(5/20)

신한투자증권 380만원(5/21)

KB증권 380만원(5/29)

골드만삭스 350만원(5/31)

씨티 310만원(5/11)

JP모건 300만원(5/18)

LS증권 210만원(5/11)

키움증권 190만원(5/11)

하나증권 160만원(4/10)

요약하면 상단은 삼성전자 59~61만원, SK하이닉스 400만원까지 올라왔습니다.

외국계만 보면

노무라: 삼성전자 59만원 / SK하이닉스 400만원

골드만삭스: 삼성전자 48만원 / SK하이닉스 350만원

JP모건: 삼성전자 48만원 / SK하이닉스 300만원

씨티: 삼성전자 46만원 / SK하이닉스 310만원

국내 증권사 상단은

삼성전자: SK증권 61만원

SK하이닉스: SK증권 400만원

으로 확인됩니다.

공통 가정은 대체로 비슷합니다.

1. AI 서버 수요 확대

2. 메모리 공급 부족 장기화

3. HBM 가격 상승

4. 범용 D램·낸드 가격 강세

5. LTA 확대에 따른 실적 가시성 개선

6. 메모리 업체 밸류에이션 재평가

최근 반도체 목표가는 업데이트 속도가 매우 빠른 구간이라 숫자는 계속 바뀔 수 있습니다.

2

2

9

862

Jun 8

🤯

Watch @ElonMusk provide a technical update on SpaceX’s capability to manufacture, launch, and operate AI satellites at scale → spacexipo.com

3

229

Björn Sickel 🌍🌏🌎 retweeted

Jun 8

#NEWS: Another one. 💥

Applied Digital has signed a 210 MW lease at Delta Forge 2, expanding our AI Factory franchise model to a fifth campus. $APLD

⚡ 1.4 GW of total leased capacity

⚡ 5 campuses across multiple states

⚡ Multiple hyperscaler customers

⚡ ~$36B contracted lease revenue

⚡ ~$86B including renewal options

Applied Digital continues to demonstrate that its AI Factory franchise model can be replicated across geographies while maintaining the execution required to support the next generation of AI.

Read the Press Release → ir.applieddigital.com/news-e…

We're Hiring → applieddigital.com/careers

22

36

183

21,584

Björn Sickel 🌍🌏🌎 retweeted

📣 @SKhynix and @NVIDIA announce a multiyear technology partnership to codevelop next-generation memory for the global AI factory buildout.

SK hynix will codevelop memory for NVIDIA's platforms — from NVIDIA Vera Rubin to Jetson Thor — while advancing fab digital twins using @NVIDIAOmniverse libraries and applying NVIDIA CUDA-X and PhysicsNeMo to accelerate semiconductor design and manufacturing.

Read the press release: nvda.ws/4e43e0p

66

239

1,946

259,725