Healthcare Executive. Girl Dad x2, family guy, soccer fan, boating and snow ski enthusiast.

Joined March 2020

- Tweets 1,123

- Following 1,016

- Followers 292

- Likes 4,923

462 Photos and videos

Bill Ruff retweeted

17 Jan 2025

Davos is calling! 🏔️ Keep an eye out for @danielnewmanUV and @PatrickMoorhead next week as they delve into the most pressing conversations shaping the future of business. #Davos2025

17 Jan 2025

Looking forward to another incredible week ahead as we embark on beautiful Davos, Switzerland to attend this year's WEF event.

Last year was my first trek and was one of the most fruitful weeks I have spent. The meetings, sessions, sit-downs, and events all focusing on the most important topics that impact our businesses and industries.

This year, we are now wily veterans, and we are greatly expanding the scope and activities at WEF. A few of the things I'm most excited about...

1. The launch of the largest of its kind CEO Survey on AI in partnership with Kearney and my friend Bharat Kapoor

2. Six Five Media will be on the ground, and I'll be joined by Patrick Moorhead for a series of amazing conversations with CEOs, Executives, and Global Business Leaders.

3. The Futurum Group will be sponsoring an Axios Freedom of the Press event at Qualcomm House.

4. I'll be moderating a WEF / MIT Panel in partnership with panelists including Åsa Tamsons and several other key executives focused on Edge AI

5. So many other great conversations on and off the record.

8

2

10

531

Bill Ruff retweeted

1 Oct 2024

I enjoyed watching today's Cosmos Event from @VAST_Data.

There is a clear trend in the data/storage space that is removing complexity and layers of software extractions and using the power of AI and next generation compute platforms to enable applications to point directly to storage or what I now call next generation data platforms for instant insights.

Historically, there has been tiered storage and then data warehouses and a cadre of data analytics software tools and data preparation tools to deal with the complexity of a data ecosystem that includes block, file, object, and in the AI era Vector.

In the future the applications will point to data in all forms and the system can be designed to deal with the various formats and deliver an insight without all of those abstractions. This is exciting times.

And of course, always fun to hear from Vast Data CEO and NVIDIA CEO Jensen Huang. Strong showing today from Vast, which has been a leader in this trendline and we are seeing similar innovation paths from the likes of NetApp and Pure Storage as well.

$NVDA $PSTG $NTAP

1 Oct 2024

VAST Data and @nvidia are redefining how enterprises process and retrieve data in real-time. With InsightEngine with NVIDIA, organizations can now extract actionable #AI insights from all data types—instantly and securely. No more data silos, outdated information, or batch processing delays.

This groundbreaking technology supports trillions of embeddings and scales across #exabytes of data, empowering businesses to make faster, smarter decisions with complete #data consistency and #security.

Ready to unlock the future of AI? Read the full press release now: vastdata.com/press-releases/…

2

13

1,429

Bill Ruff retweeted

1 Oct 2024

VAST Data and @nvidia are redefining how enterprises process and retrieve data in real-time. With InsightEngine with NVIDIA, organizations can now extract actionable #AI insights from all data types—instantly and securely. No more data silos, outdated information, or batch processing delays.

This groundbreaking technology supports trillions of embeddings and scales across #exabytes of data, empowering businesses to make faster, smarter decisions with complete #data consistency and #security.

Ready to unlock the future of AI? Read the full press release now: vastdata.com/press-releases/…

1

5

18

2,667

Bill Ruff retweeted

20 Sep 2024

The future of AI will be unveiled Oct 1 at @VAST_Data's online event Oct 1. Here's what @danielnewmanuv and @ashimmy have to say about experiencing the cosmos.

Register today: bit.ly/3MqYvZy

3

19

106

3,643

Bill Ruff retweeted

19 Sep 2024

On-site coverage coming soon from @TheSixFiveMedia at #SmartsheetENGAGE. @CTOAdvisor & @daven007 will be sitting down w/ @Smartsheet executives and partners to get the inside scoop. Find out more: smartsheet.com/engage/seattl…

2

7

604

Bill Ruff retweeted

13 Aug 2024

On this ep of The Main Scoop, @MoorInsStrat CEO @PatrickMoorhead joins hosts @GregLotko from @Broadcom and @danielnewmanUV to chat about the current IT investment📊 trends and how to maximize business value through strategic investment: hubs.ly/Q02L6pk70

3

5

320

Bill Ruff retweeted

14 Jun 2024

Day 1 of #SixFiveSummit24 brought keynote speaker @markmader, President and CEO of @Smartsheet. He & @danielnewmanUV cover the power of GenAI, its impact on businesses, and how to get an edge in today's business environment. Watch on demand now: hubs.ly/Q02BXrvf0

2

8

567

Bill Ruff retweeted

11 Jun 2024

Industry leaders and policymakers, this one's for you! Don't miss Devavrat Shah, PhD from @IkigaiLabs at #SixFiveSummit24, where he shares guidelines for responsibly navigating the transformative potential of Gen AI. 🆓

Register now! buff.ly/3VnWYIL

4

5

509

Bill Ruff retweeted

9 Jun 2024

Long post alert—⏳

Many SaaS companies got obliterated the past two weeks as earnings for some of the biggest, most notably @Salesforce revealed some weakness in the sector and questions around the long-term viability of SaaS and enterprise software in a rapidly changing landscape powered by Gen AI.

Is the SaaS bubble bursting? 👇🏻

I’ll come back to that in a moment, but perhaps first, it is important to look at the current market and what has driven the overall market up while the broad are economy is largely flat. Want to challenge this notion in terms of the market, remove NVIDIA from the S&P YTD and you will take away ~34% of the ascent of the S&P.

But put that aside for even a moment and what you will see is the AI trade is almost all hardware. And moreover, all NVIDIA, with a few other surprise winners (DELL and Supermicro come to mind).

And this actually makes sense. Because we are in the front loading phase of the AI boom. Building out infrastructure and data centers to support accelerated compute. This is why GPUs have become such a scarce resource and why we are seeing the big cloud hyperscalers like Meta, Amazon, Microsoft, Oracle, Google, and soon Apple gobbling up GPUs and investing big to develop homegrown AI chips.

Effectively, we are building the next generation “App Store” supported by AI, and it won’t be possible if the infrastructure is missing. But, while this is happening, the dollars are flowing from other parts of IT to AI infrastructure and projects. Our intelligence is showing this in almost all of our readings—and you can see if in numbers for OEMS shifting from CPU to AI Servers AND system integrators shifting from other IT projects to almost exclusively AI projects.

But, I think the tide will turn and I do think SaaS companies will be VERY INTERESTING as part of the AI movement and this will happen sooner than some think. And this is what I think the market is getting wrong.

What people are getting wrong?

The TLDR of this long post is that companies like Oracle, SAP, Salesforce, and ServiceNow to name a few have giant moats and deeply entrenched customers. Well over 100k customers each that depend on these software companies to run their business and deliver the best and most capable features in a regular cadence. Switching is horribly difficult and expensive and generative AI will take years to get to the point where it can render a UX from a mere voice or text prompt.

Therefore, in the next 2-3 years, at the very least, the consumption layer of enterprise software, much like the consumption of AI infrastructure will be led by as a service offerings that enable companies to quickly adopt AI. At our @TheSixFiveMedia Summit that starts this week, we will feature conversations with CEOs like Bill McDermott of @ServiceNow and Mark Mader of @Smartsheet and I will discuss with both of them “Where AI will be consumed.” And for most companies outside of the mega scale cloud companies and the largest industry centric companies it will be in the cloud and/or in a SaaS like consumable model.

Despite our unparalleled excitement for the AI infrastructure that NVIDIA is selling, it has a small number of really big customers. If I’m an investor I would like companies that have a 100k users that can consumer more with the ability to raise prices by adding valuable features.

The monetization of AI has been limited to a few software players and this has been part of the reason the prices were hit so hard (IMO). Salesforce and others haven’t proven beyond a doubt that subscribers will pay substantially more for their offerings because of Gen AI/AI and that is a gap that needs to be filled.

But, I think the revenue is durable, the customers are sticky, and AI consumption will be done in software at scale really quickly. The big SaaS players have market and resource advantages and I don’t see them failing to pivot.

$NOW $CRM $SAP $ORCL $IBM $SMAR $NVDA $SNOW

9

15

54

10,139

Bill Ruff retweeted

7 Jun 2024

Very excited to watch our interview with @Qualcomm CMO @donnymac about the @Snapdragon brand's evolution and what's next.

In Taipei with @anshelsag - part of our week-long #computex and #snapdragonXseries coverage.

I would watch, bookmark and share this one, but that's just me.

6 Jun 2024

CMO of @Qualcomm @donnymac is at #Computex2024 w/ @OABlanchard & @anshelsag discussing how they are expanding beyond mobile and revolutionizing #PCs with #AI features, aiming to lead the market through disruptive innovation via @Snapdragon X Elite. $QCOM x.com/i/broadcasts/1RDGllgdw…

2

17

716

Bill Ruff retweeted

8 Jun 2024

This list of speakers for next week’s @TheSixFiveMedia Summit is outstanding and truly showcases the depth of our market. From

CEOs to CTOs and from silicon to services, I cannot wait to dive into these sessions.

techstrongevents.com/the-six…

2

7

901

Bill Ruff retweeted

2 Jun 2024

♻️ From energy-efficient data centers to telecom innovations, the Sustainability track at #SixFiveSummit24 covers it all! Join experts from @Lenovo, @Ericsson, @Cohesity, @intel, and others to discover actionable strategies for a greener future.

buff.ly/3VnWYIL

2

8

360

Bill Ruff retweeted

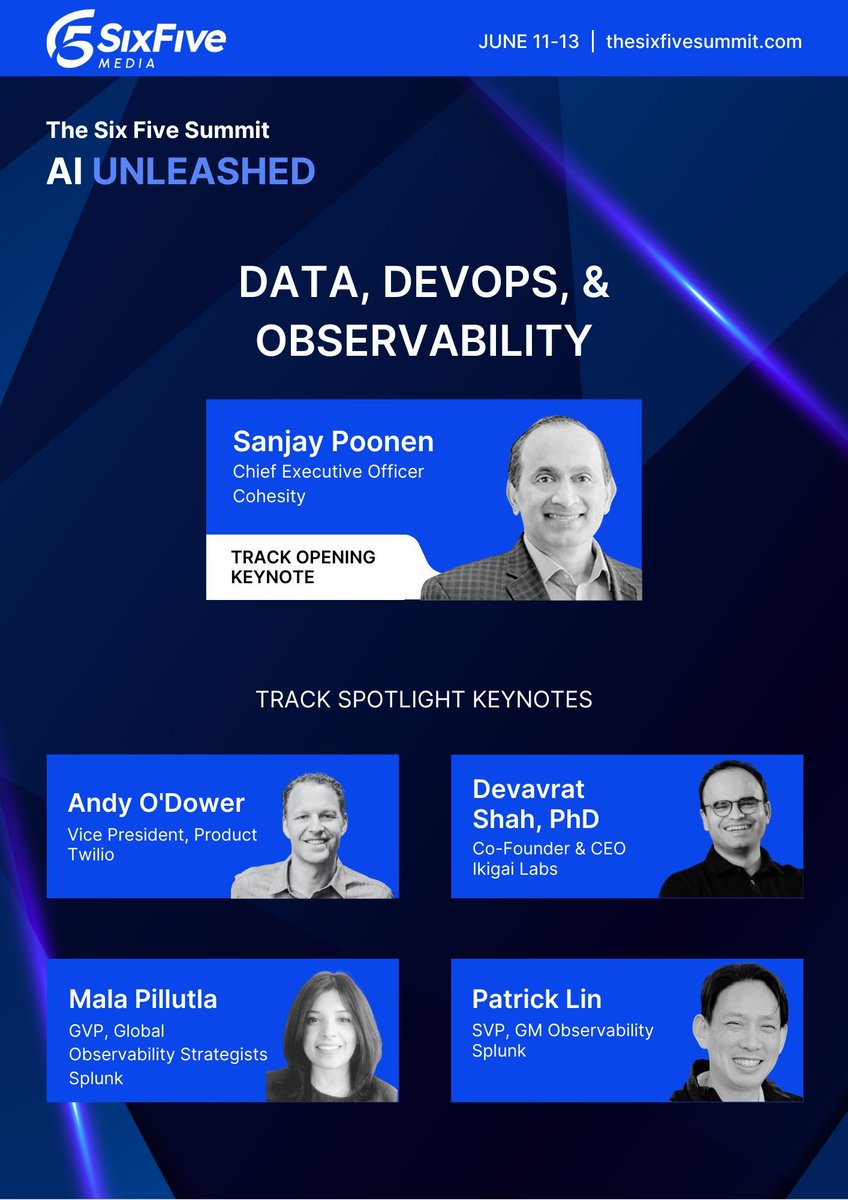

1 Jun 2024

From data management to DevOps and beyond, the Data, DevOps, & Observability track at #SixFiveSummit24 covers it all! Learn how to harness AI for better insights and faster innovation with @Cohesity, @splunk, @twilio, and others. Register now: buff.ly/3VnWYIL

2

7

194

Bill Ruff retweeted

21 May 2024

.@MichaelDell sits down with @PatrickMoorhead and @danielnewmanUV to talk the theme of this remarkable day — AI transformation.

What's needed to make the most of this crucial time in history? Innovation at an extraordinary pace. That's just what @DellTech is delivering with the Dell AI Factory.

The best part, they are dedicated to ensuring GenAI is trained within the parameters of laws and humanity to achieve AI for Human Progress. More to come.

@DellTechWorld $DELL

5

12

31

1,604

Bill Ruff retweeted

17 May 2024

At #RSAC, host @krista_lee and @elastic’s Security VP @hmikenichols share their thoughts on transforming SOCs with AI, highlighting the shift towards AI-driven security analytics and AI's pivotal role in enterprise defense. $ESTC x.com/i/broadcasts/1mnxepQnQ…

2

71

47,555

Bill Ruff retweeted

16 May 2024

What can you expect from #TheSixFiveSummit24? @PatrickMoorhead, @danielnewmanUV, and @ashimmy give you the run down on summit topics, speakers, and the value brought to you by the partnership between @TechstrongGroup and Six Five Media.

Like what you see? Register today: thesixfivesummit.com

3

8

552

Bill Ruff retweeted

4 May 2024

We’re coming at ya, @boomi. Me and @LisaMartinTV. Look for some reax in this space

3 May 2024

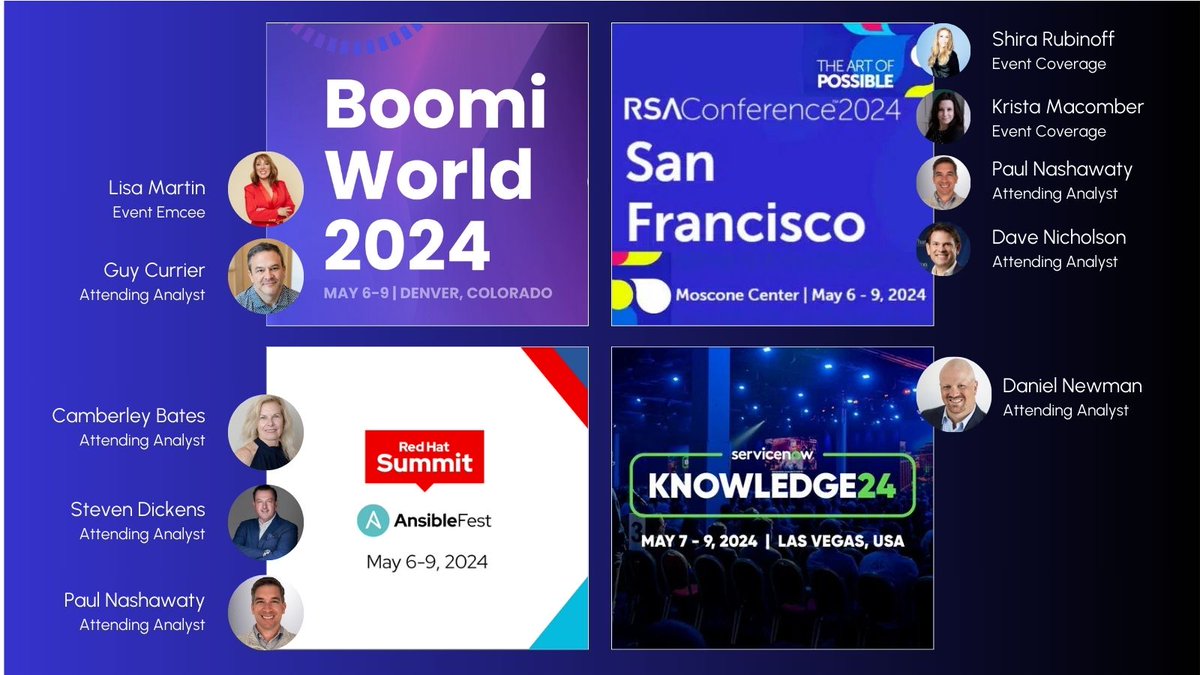

Where will you see the TFG team this week? At these major industry events:

🔹 #BoomiWorld with Emcee @LisaMartinTV

🔹 @HelloKnowledge Knowledge24

🔹 @RedHatSummit #AnsibleFest

🔹 @RSAConference 2024

Who to look for 👀:

@danielnewmanUV, @daven007, @Shirastweet, @camberleyb , @GuyCurriersfeed, @StevenDickens3, @krista_lee, @pnashawaty

Full list of events 👉 futurumgroup.com/about-us/ev…

2

3

106

Bill Ruff retweeted

2 May 2024

Hard to be at CNBC HQ and not feel, just for a moment, like you are in the middle of the season finale of “Succession”

Where is Tom Wambsgans? 🫣🤣

Amazing place. Great show!

2

1

32

1,550

Bill Ruff retweeted

2 May 2024

After 4 years of being on @PowerLunch and @CNBCTheExchange it was really nice to have the chance to sit down in person with Tyler Matheson and @LesliePicker.

Love the energy on set and it was great to have Steve Kovach and @EamonJavers join as we dove into Apple, Microsoft, Qualcomm, Google and so many other names.

From earnings to antitrust to what will fuel market growth and how the macroeconomy is playing a role and impacting investors sentiment. We covered a lot of ground.

$AAPL $GOOGL $MSFT $QCOM

2

3

10

2,060

Bill Ruff retweeted

26 Apr 2024

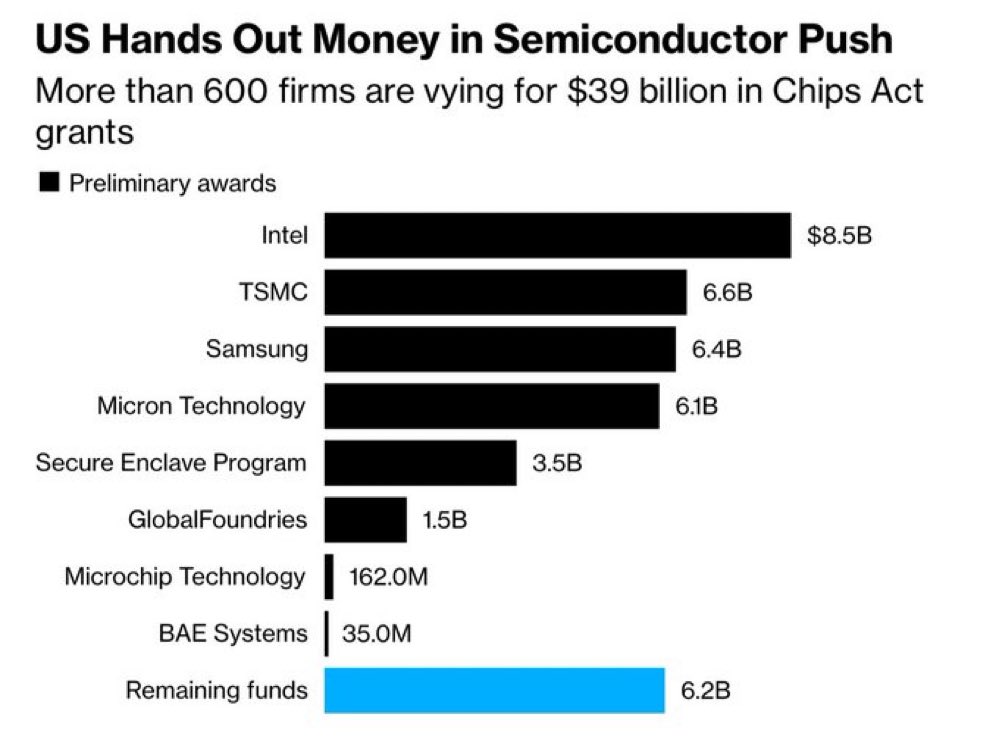

The breakdown of Chips Act Grants to date and how the $39 Billion has been awarded.

Top awards have gone to :

Intel: $8.5 Billion

TSMC: $6.6 Billion

Samsung: $6.4 Billion

Micron: $6.1 Billion

Just over $5 Billion in smaller awards have been approved.

I see the grants and associated commitments helping to achieve the goal of greater domestic production of leading edge Semiconductors. However, I stand by my assessment that U.S. policymakers will need to do more and there will need to be a chips act 2 to maintain tech leadership, build resiliency and provide more geographic distribution. AI is further accelerating this need.

$MU $INTC $GF $TSM

3

6

22

1,645