Just a bear sharing information.

Joined October 2021

- Tweets 19,353

- Following 3,697

- Followers 3,736

- Likes 38,316

4,338 Photos and videos

Boodle retweeted

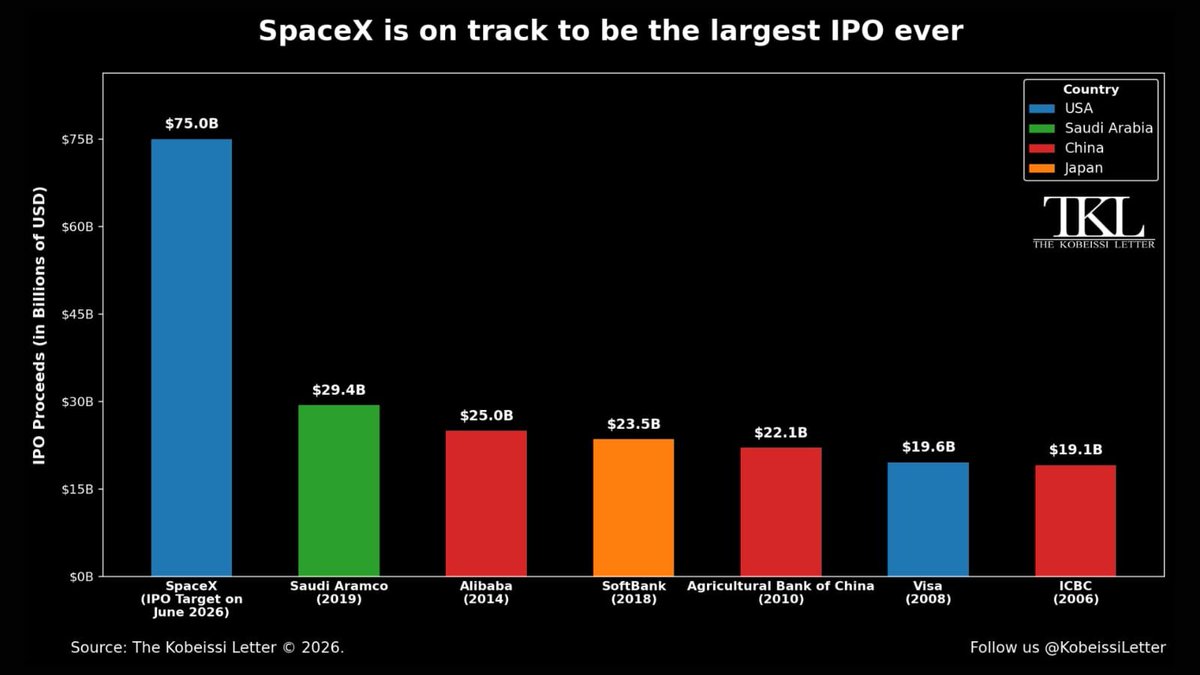

BREAKING: SpaceX is now expected to raise as much as $75 billion in its IPO which could debut as soon as June 12th.

That's 2.5 TIMES larger than Saudi Aramco's IPO, the current largest IPO ever.

Nothing in history has ever come close to what SpaceX is about to do.

254

645

5,081

605,388

Boodle retweeted

May 16

Taiwan Index Cash

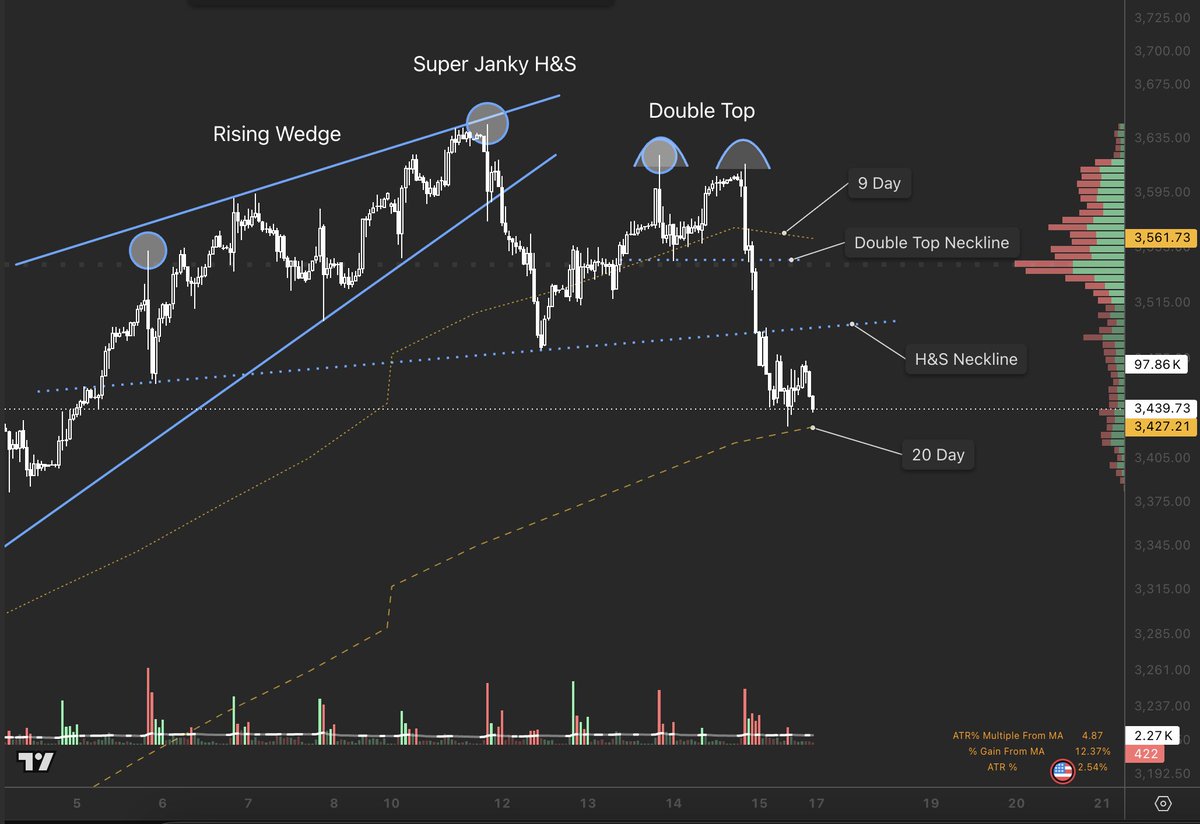

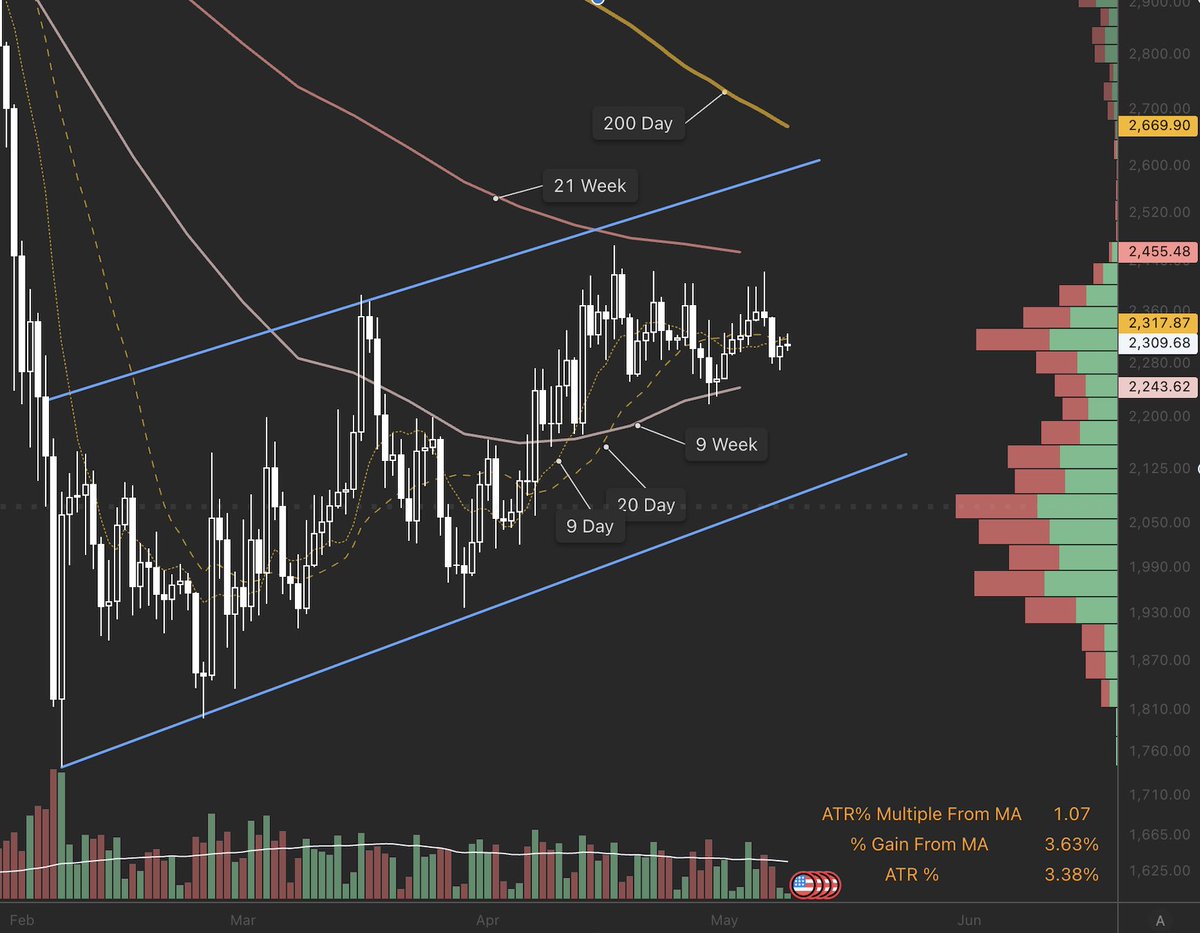

First Image: I see a rising wedge that spilled over into a double top, which also formed a rather janky head and shoulders pattern. I'm perfectly fine if you disagree with the head and shoulders pattern. The main point is that at least two bearish patterns have played out. This suggests some fading in the bullish trend. That said, it did bounce off the 20 day moving average, which is a positive sign for now.

Second Image: This was what initially caught my attention (after watching the KOSPI and NIKKEI). It’s a concerning candle. It doesn’t scream a full trend reversal, but it does indicate a shake up in the market.

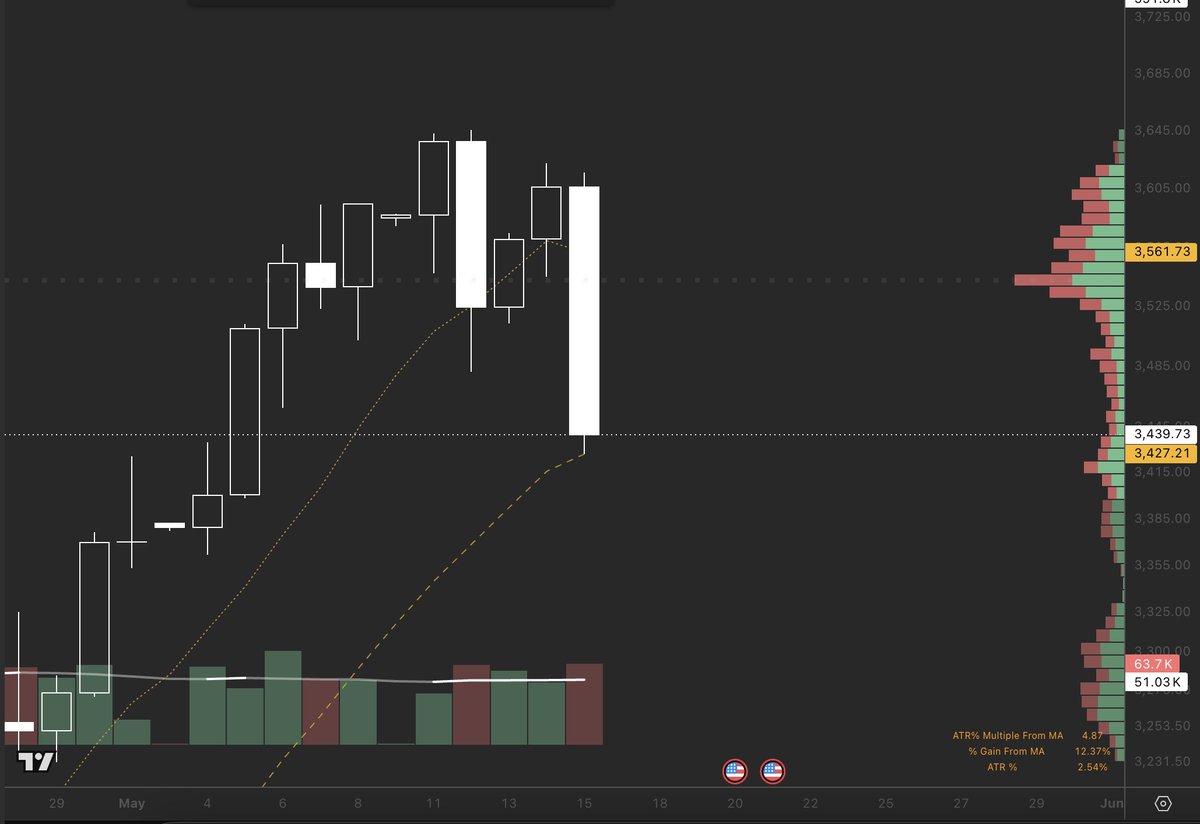

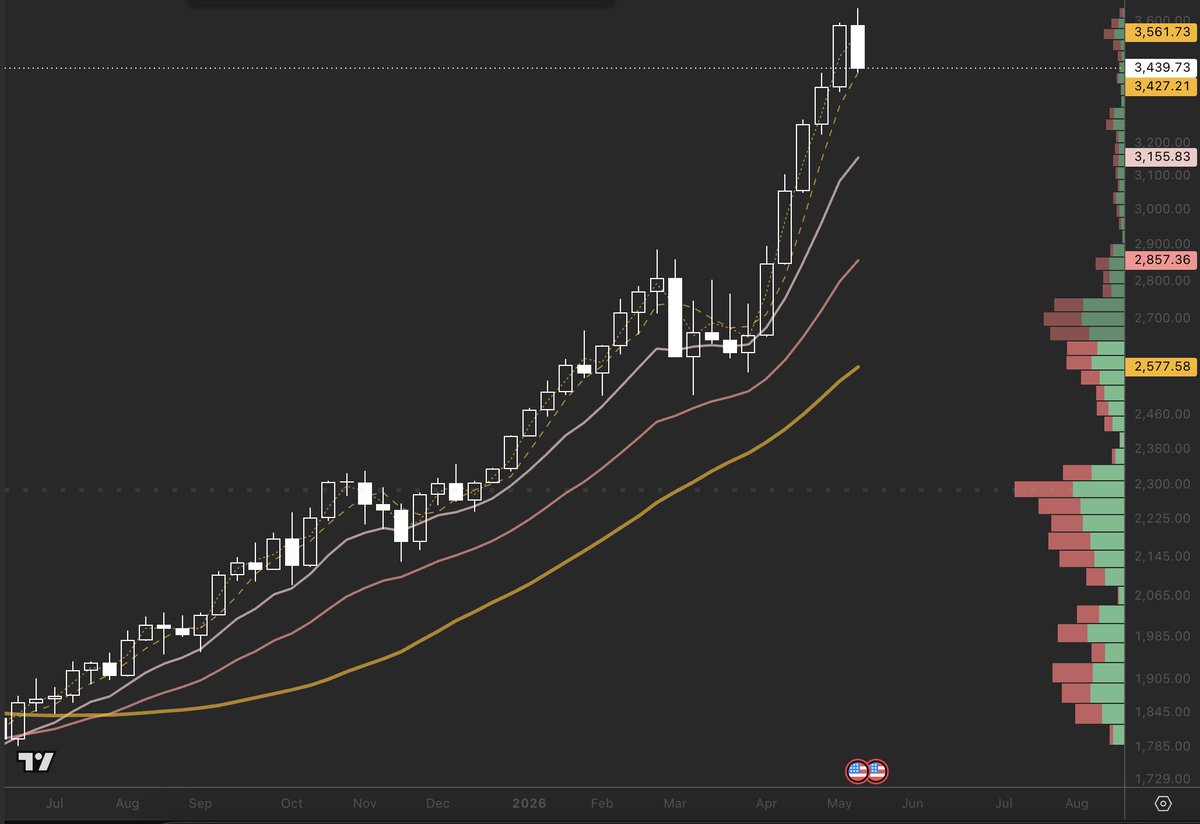

Third Image: This is the one I really wanted to show you. My main concern is: if it fails to hold above the 20 day moving average, where does it go next? Where is the next support level? The index has been in a steep, explosive uptrend with very little consolidation. The closest resting area appears to be around the $3,250 level. That would represent just shy From a 10% pullback from its all time high.

Best case: the 20 day holds as support and the uptrend continues.

Bear case: it heads down toward the 9 week moving average.

One important point ...the moving averages on this index are currently very far apart, so the last thing you want to see is a bearish breakdown.

Feel free to share your thoughts. I am always open to other views.

ALT Taiwan Cash Index with bearish signals.

2

4

257

Boodle retweeted

May 16

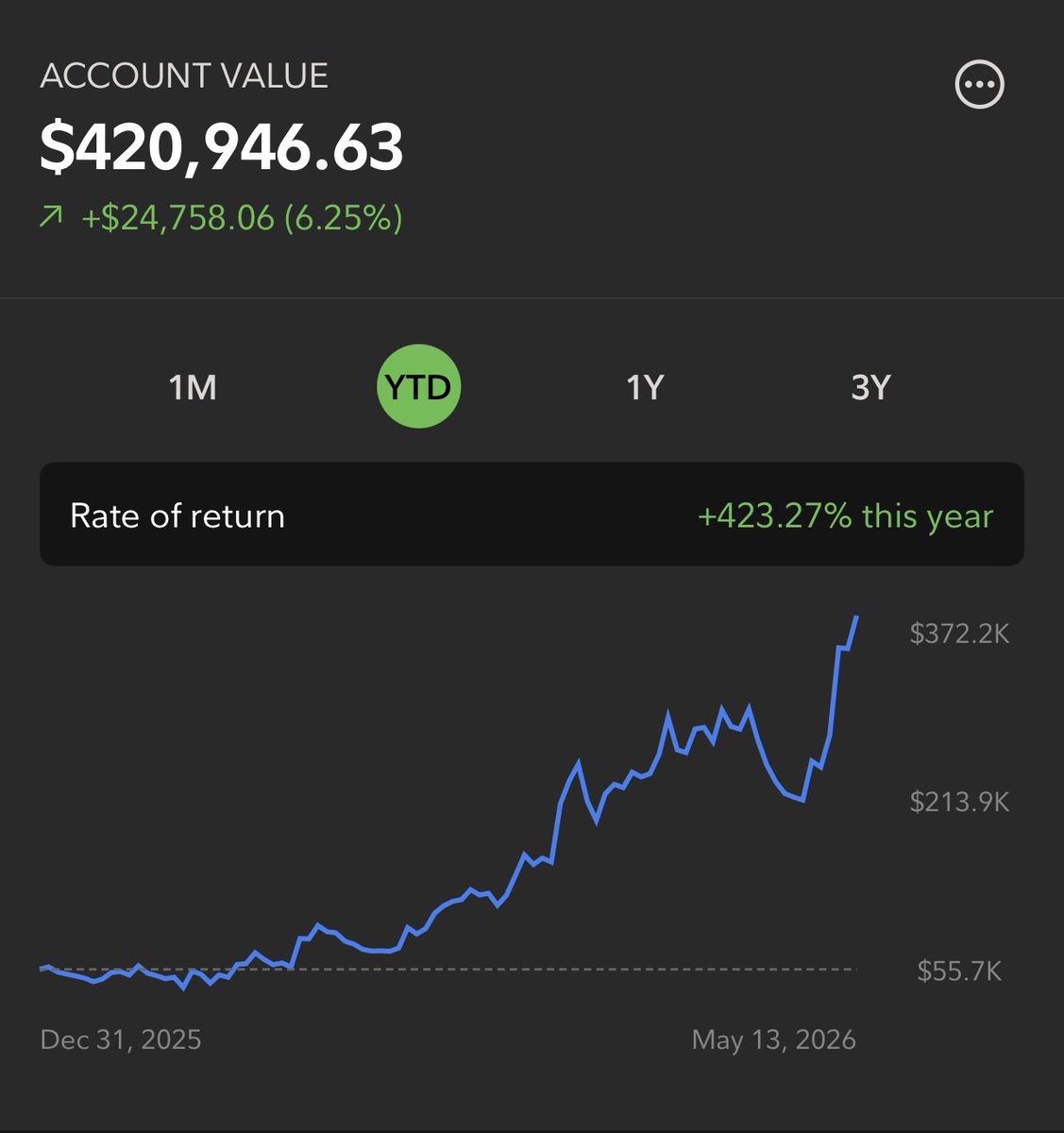

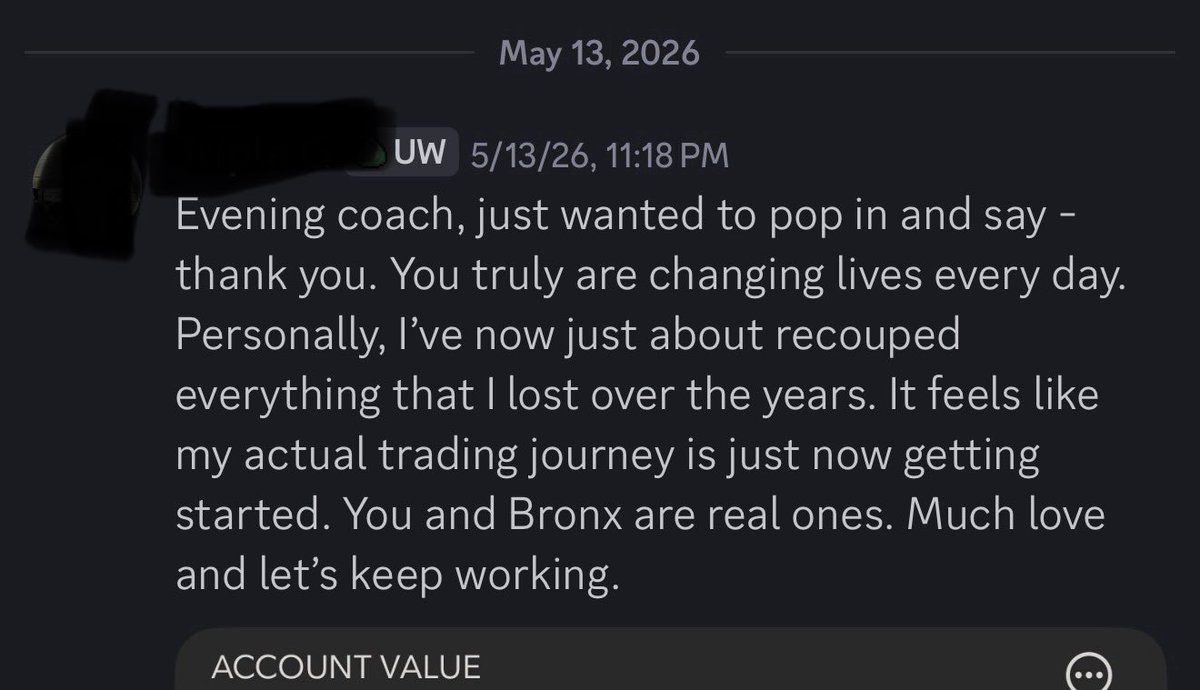

“Recouped everything I lost over the years”

That’s what I’m all about.

Blue sky territory ahead.

5

4

182

12,625

Boodle retweeted

May 9

$HIMS

Last breakout like this made a 66% move.

Earnings on Monday!

25

13

408

25,403

Boodle retweeted

Typically, I only show a limited number of indicators on a chart to prevent overcrowding. I worked on a new color scheme and a way to display more indicators like volume and ATR while keeping the main moving average on every chart. There are still other moving averages and indicators I might fit in, but this is what I have so far.

Since Ethereum is on the chart, let’s review what’s being shown right now.

Ethereum is in a flag pattern. This pattern is bearish. Let’s discuss what I like for a bullish outlook on Ethereum. I like that it is above the 9 week. If I’m short term holding, I want it to stay above that average. From an RSI (weekly) perspective, it went into oversold territory a while back and has recovered since. There’s still plenty of room to run up from a weekly outlook.

A bearish outlook: I don’t like that it’s still under the 200 day, 21 week and short term averages like the 9 day and 20 day. I also don’t like that it’s in a bearish flag pattern while all this is going on. The 21 week is also acting as a major ceiling for Ethereum. Notice the highest volume for this range is under the flag. I would believe if it loses the 9 week then it will gravitate towards that area.

2

3

9

39,019

Boodle retweeted

Mar 31

🚨Giveaway time 🚨

Special guest from the Anaheim meetup, @BROKENCRAY0NS was so generous with many physical giveaways and he wanted to share some love to the fam that couldn’t be with us in person, so I have 2 signed & dated art pieces to give away.

Rules:

- Like & Repost

- Tag someone in the comments and say something nice to them to brighten their day. ❤️🧡💛💚💙💜🖍️

Winner will be drawn in approximately 48 hours. First winner chooses the piece they want, second winner will receive the other piece.

30

38

57

2,432

Boodle retweeted

Feb 6

Somehow I agreed to have @MollySOShea shadow me for the day of our Financial Open House.. any questions you want her to ask?

Anything is fair game. Cupcakes, swords, etc ⚔️

89

23

403

33,249

Boodle retweeted

Jan 21

If you want to understand where the future is headed, start here: Big Ideas 2026.

Download: ark-invest.com/big-ideas-202…

51

312

1,377

725,936

Boodle retweeted

Jan 16

We're building a mortgage product at @Opendoor, fully AI-native from Day 1.

Homeownership should be easier, especially when it comes to mortgage. We're working together with our partners at @Lennar to make that future a reality - on Opendoor.com and off it. More soon

164

220

1,765

316,752

Boodle retweeted

It’s been a big week for Eos, and the momentum is only building! As we set our sights on Davos, now is the perfect moment to catch up on what's powering this next chapter. If you missed our Indensity™ launch event, you can watch it below and experience the energy, vision, and innovation defining the new era of Indensity!

28

47

421

53,933

Boodle retweeted

25 Dec 2025

✅ Ugly Christmas 🎄 Sweater

✅ Emotional Support Feline

✅ TRUP Limited Edition Hat

✅ Elektra by my side

✅ Wishing you 🫵 Happy Holidays!!

May the season’s Magic 🪄 find you! 😊💙🙏

#VeVe

28

17

80

1,990

14 Dec 2025

I’m getting close to deleting my 𝕏 account. It’s nothing but videos on my timeline and I’m telling 𝕏 I’m not interested.

The algorithm is fried because I stopped hitting the like button and commenting for the last couple of weeks. I think it’s trying to send me different topics to keep me interested but it’s making it worse.

I am a reader and I strongly believe short videos fry the mind.

2

80

Boodle retweeted

30 Nov 2025

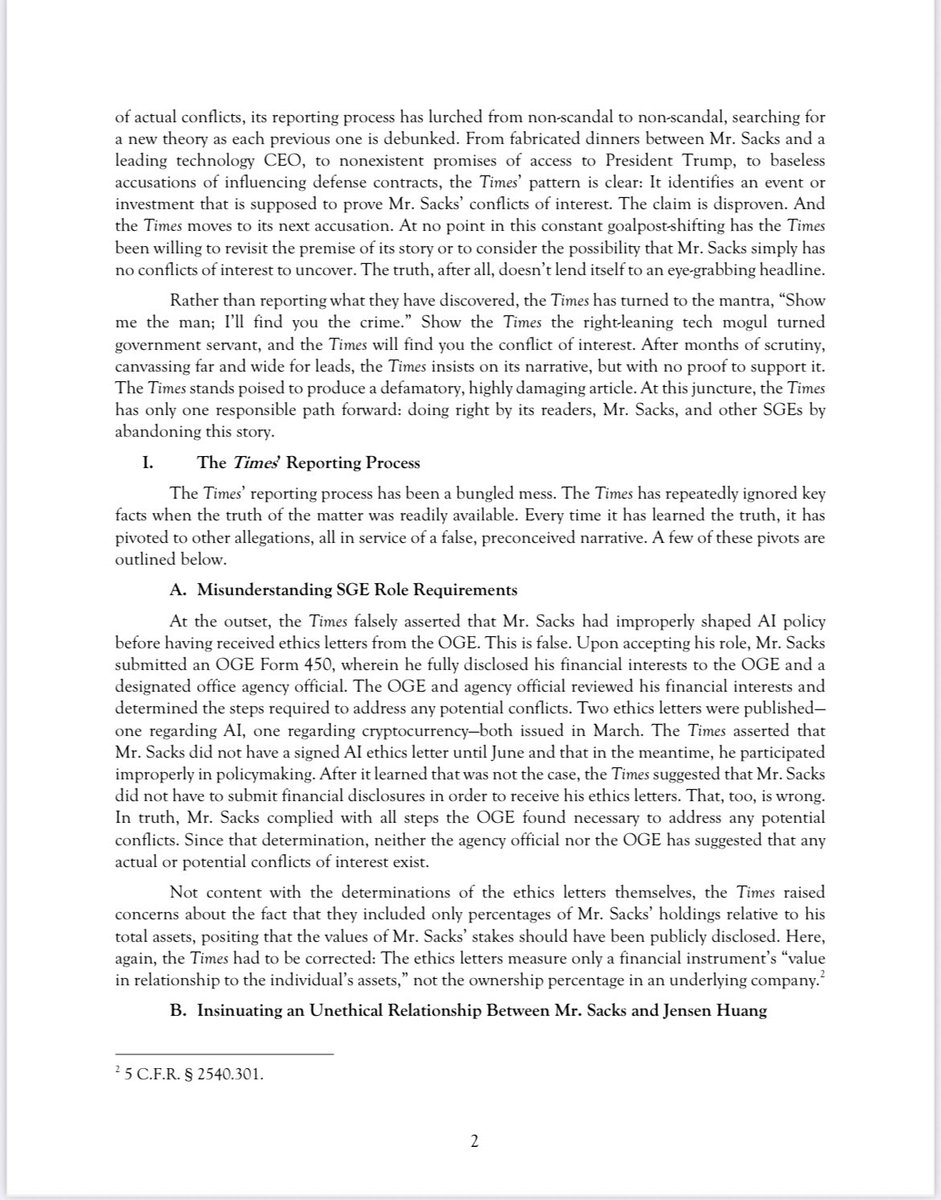

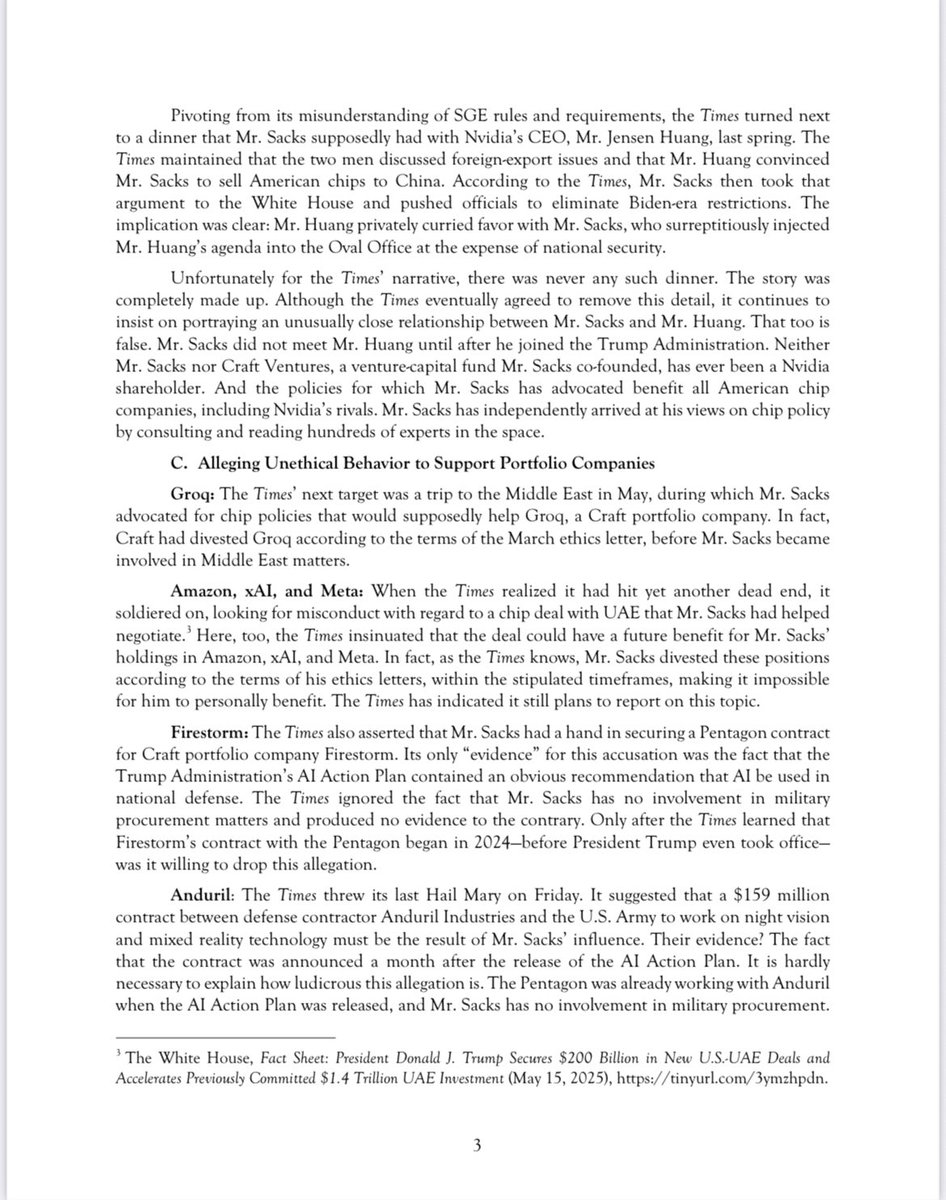

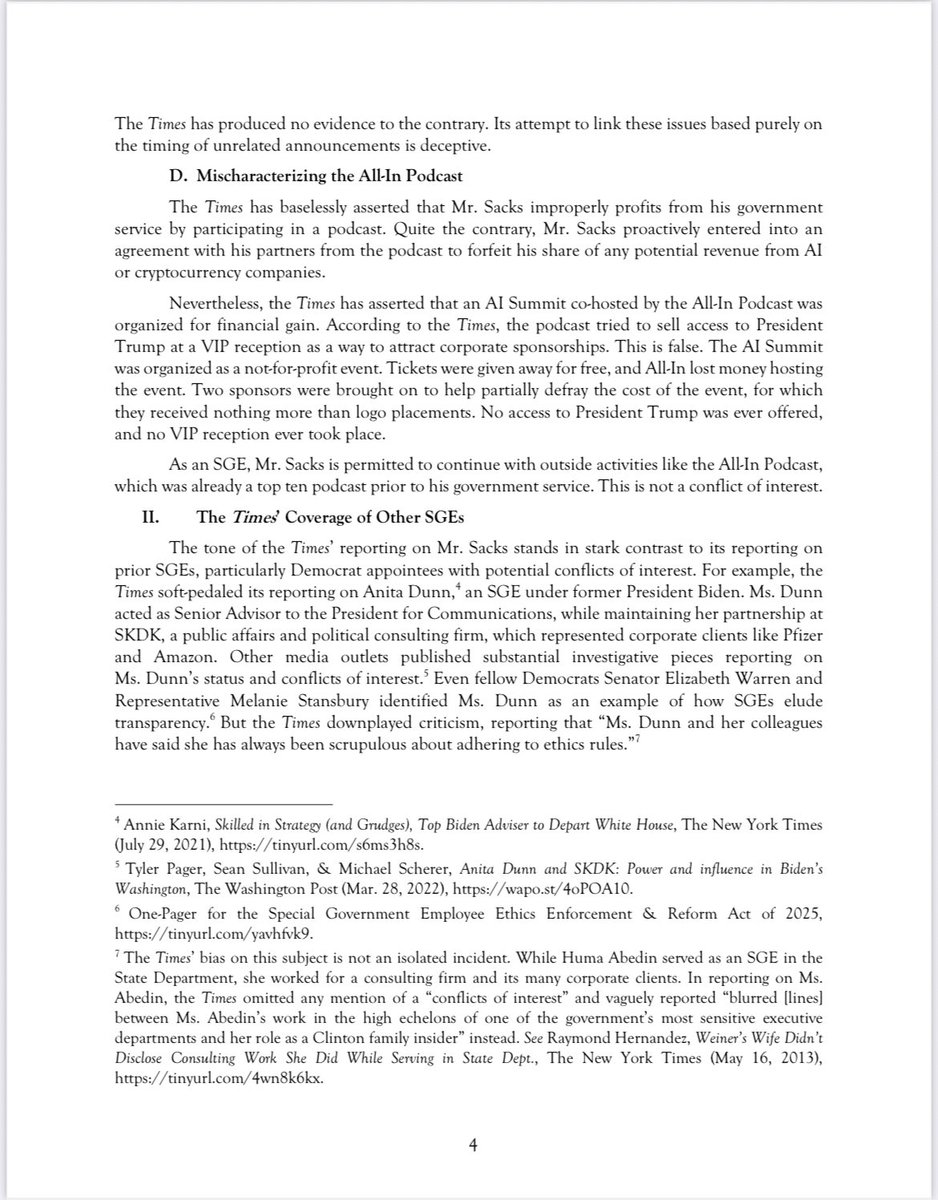

INSIDE NYT’S HOAX FACTORY

Five months ago, five New York Times reporters were dispatched to create a story about my supposed conflicts of interest working as the White House AI & Crypto Czar.

Through a series of “fact checks” they revealed their accusations, which we debunked in detail. (Not surprisingly the published article included only bits and pieces of our responses.)

Their accusations ranged from a fabricated dinner with a leading tech CEO, to nonexistent promises of access to the President, to baseless claims of influencing defense contracts.

Every time we would prove an accusation false, NYT pivoted to the next allegation. This is why the story has dragged on for five months.

Today they evidently just threw up their hands and published this nothing burger. Anyone who reads the story carefully can see that they strung together a bunch of anecdotes that don’t support the headline. And of course, that was the whole point.

At no point in their constant goalpost-shifting was NYT willing to update the premise of their story to accept that I have no conflicts of interest to uncover.

As it became clear that NYT wasn’t interested in writing a fair story, I hired the law firm Clare Locke, which specializes in defamation law. I’m attaching Clare Locke’s letter to NYT so readers have full context on our interactions with NYT’s reporters over the past several months.

Once you read the letter, it becomes very clear how NYT willfully mischaracterized or ignored the facts to support their bogus narrative.

1,311

4,365

26,737

6,542,730

28 Nov 2025

Me while reading this lol

28 Nov 2025

Just in case you’re interested in the way we feel about the people who trust us with their investment capital, I wanted to share…

In December 2024, we bought back 11.76 million shares of $clsk for $145M.

In November 2025, we bought back 30.6 million shares of $clsk for $460M.

We extinguished all equity offerings. We shut off our atm.

We’ve stacked 13,000 Bitcoin—all mined.

We’ve closed on more land.

We’ve secured more power.

We’ve started assembling a world-class AI data center team.

We bet on us.

We now control a significant portion of the most scarce assets on the planet. $btc $clsk and powered land.

@CleanSpark_Inc

Thank you for taking this journey with us.

4

111

Boodle retweeted

26 Nov 2025

Just wrapped with @cvpayne — and said what most won’t.

A new Fed chair means a new regime… and small caps get oxygen again.

That’s where the huge re-ratings live.

IREN, CIFR, BTQ, SANA, OPEN, BETR — built for this moment.

Rising Dynasty isn’t chasing the future. We’re owning it.

33

69

637

69,149

Boodle retweeted

25 Nov 2025

And we’re just getting started.

25 Nov 2025

Today $CLSK reported transformative full fiscal year 2025 financial results (ended 9/30/25), setting the stage for our AI expansion.

*Revenue: $766.3 million (102% growth YoY)

*Net Income: $364.5 million

*Total Assets: $3.2 billion

*Power Under Contract: 1.31 GW (as of 10/31/25)

Full press release here: clsk.news/fy25results

“Fiscal 2025 was the year CleanSpark achieved operating leverage. We surpassed 50 EH/s in operational hashrate, set new revenue records, and demonstrated strategic capital stewardship by choosing accretive capital market tools, such as convertible debt and bitcoin backed revolvers instead of an ATM to finance the business during the calendar year,” said @smatthewschultz, Chairman and CEO of CleanSpark. “We are evolving into a comprehensive compute platform that is prepared to optimize value from both AI and bitcoin workloads. Our deep expertise in power procurement, infrastructure development, and efficient scaling gives us a unique advantage in meeting surging global demand for compute.”

“I’m proud of our results for the fiscal year. Beyond our revenue of $766 million and hashrate growth achievements, we also demonstrated disciplined capital investment and are financially positioned to rapidly become a leading AI infrastructure provider,” said @GaryVec, President and CFO of CleanSpark. “We recently closed a landmark $1.15 billion 0% convertible transaction to accelerate expansion of our power and land portfolio. Our market leading bitcoin mining operations have been supplemented by cash generated from our institutional grade treasury desk. As we continue to execute on our strategies, our goal is to replicate our market leadership across a broader range of compute capabilities.”

25

41

466

51,150

The $UAVS team had a great time at @Milipol_Paris 2025 last week! Looking forward to the next opportunity to showcase our exceptional suite of #drones, sensors and software.

#MilipolParis #UAVS #drone

2

2

17

1,237

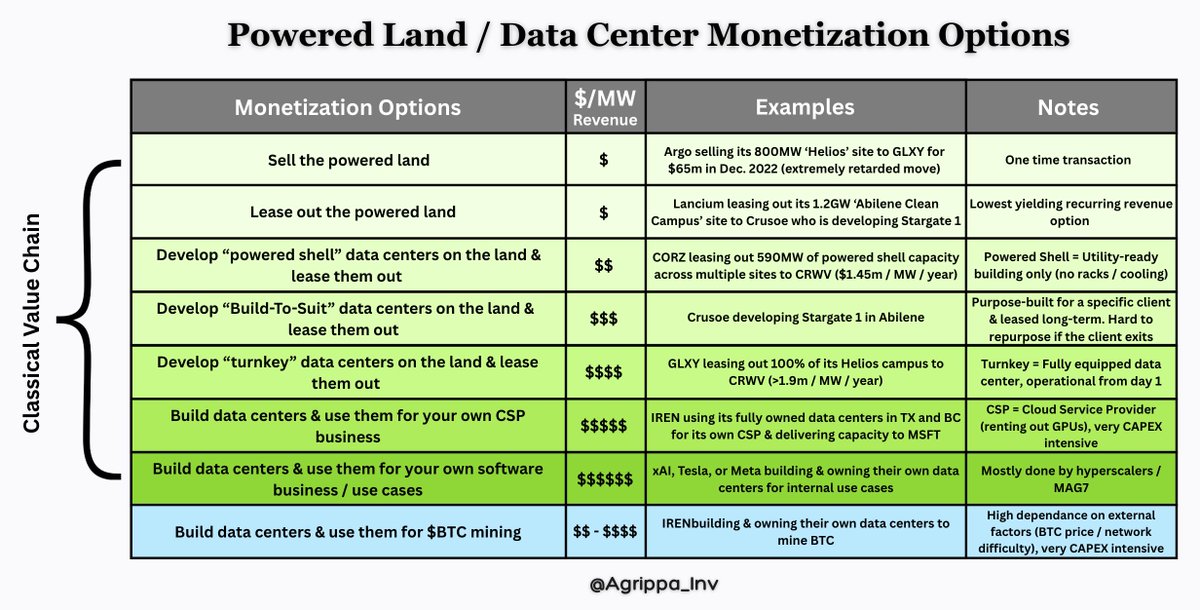

24 Nov 2025

A great breakdown relating to HPC business models

23 Nov 2025

Something fascinating is happening that most people are missing. Bitcoin miners are transforming into AI infrastructure providers. Noone missed this but they're not all doing the same thing.

I spent time mapping 8 public companies across the value chain. What I found was surprising: there are actually 4-5 distinct business models emerging, each with completely different economics, risk profiles, and upside potential.

Let me give you a framework for thinking about this.

I used @Agrippa_Inv Classical Value Chain as a base model for this, from his website (link attached in a reply from me after this post and picture attach to this post is also from his site. Thank you for your work).

The Core Insight

The key question isn't "are they pivoting to AI?"

It's "HOW are they monetizing their power infrastructure?" There are actually 4 distinct business models emerging. Each with different economics, risks, and upside potential.

Category 3 - The Powered Shell Model

Core Scientific $CORZ - 590 MW leased to $CRWZ

The capital-efficient play. They provide:

Building envelope

Power infrastructure

Cooling systems

The customer funds everything else (~$300M for interiors).

$1.5M capex per MW vs $5-10M for competitors.

$10.2B contracted over 12 years.

Category 5 - The Turnkey Model

Cipher $CIFR & TeraWulf $WULF - The landlord model

Fully operational data centers, liquid cooling, ready day 1. Tenant brings GPUs.

CIFR: $8.5B contracts (AWS, Google/Fluidstack), 3.2 GW pipeline WULF: $14.2B contracts (Fluidstack, Core42), zero-carbon energy

Higher capex, higher margins, long-term contracted revenue.

Category 5.5 - The Hybrid

Iris Energy $IREN - The interesting middle ground

$9.7B Microsoft deal. But here's the twist:

$IREN owns the GPUs ($5.8B Dell purchase). They're leasing GPU capacity, not data centers.

Not quite a CSP. Not quite turnkey. Something in between. Managed GPU hosting.

Category 6 - The True Cloud Providers

CoreWeave $CRWV & Nebius $NBIS - The platform plays

These aren't infrastructure providers. They're running actual cloud platforms.

CRWV: $1.9B revenue, 737% YoY growth, Nvidia's golden child

NBIS: Former Yandex team, $17.4B Microsoft deal, proprietary full-stack

Highest margins. Highest complexity.

Some wildcards.

Bitfarms $BITF: Most aggressive pivot. Exiting Bitcoin completely by 2027. $814M war chest. Pennsylvania-focused.

Soluna $SLNH: Completely different thesis. Co-locates at renewable plants, monetizes curtailed energy. MaestroOS software for grid arbitrage.

What This Means

The value chain runs from powered shell (30-40% margins) → turnkey (50-60%) → GPU infrastructure (50-60%) → cloud platform (70% ). More value equals more capex equals more risk equals more upside.

The key distinction between 5.5 and 6: $IREN owns GPUs and leases capacity. Microsoft gets dedicated infrastructure.

$CRWV $NBIS own GPUs and run cloud platforms, customers use APIs and managed services in multi-tenant environments. One is managed hosting. The other is cloud services. Totally different businesses.

Why This Matters

We're watching a real-time case study in asset transformation. Every company here started as a Bitcoin miner. They all have the same foundational assets. But they're monetizing them completely differently based on their strategy, capital position, and execution capability.

The AI infrastructure shortage created massive demand. Miners realized: "We have power infrastructure. That's the actual bottleneck." So they pivoted, but in wildly different directions.

The Investment Framework

Before you touch any of these, ask five questions:

What's their monetization model? (3, 5, 5.5, or 6?)

Who owns the GPUs? (Determines capex risk)

What's the contract structure? (Revenue visibility)

Who are the customers? (Concentration risk)

What's the power cost? (Margin sustainability)

Pick your risk tolerance:

Want proven cloud platform? $CRWV (expensive) or $NBIS (emerging).

Want contracted infrastructure revenue? $CIFR, $WULF, $CORZ.

Want transformation upside? $IREN, $BITF. Want renewable angle? $WULF, $SLNH.

The Risks and Opportunities

Real risks: AI bubble pops and demand evaporates. Hyperscalers build their own and disintermediate. Power costs spike and compress margins. GPU refresh cycles accelerate into a capex treadmill. Customer concentration leaves you exposed.

Real opportunities: AI infrastructure shortage is genuine. Microsoft, Google, and Amazon are 2-4 years behind demand. These companies can deliver in 12-18 months. And they have the one thing that actually matters: power allocation. That creates pricing power.

The Pattern

Everyone talks about GPU shortage. The real shortage is power. Training frontier AI models needs 100 MW. Inference at scale needs gigawatts. These companies have secured 5 GW of power capacity. That's the actual scarce resource.

Most are 12-24 months from full deployment. The next 18 months determines who executes and who doesn't.

The Bottom Line

In 5 years, some of these companies will be worth $50B . Others will be restructured or acquired. The difference won't be who had the most megawatts. It'll be who chose the right business model for their assets and execution capability.

Strategy > Scale. Business model > Assets.

This is capitalism working in real-time. Do the work. Understand the model. Then pick your play.

115

Boodle retweeted

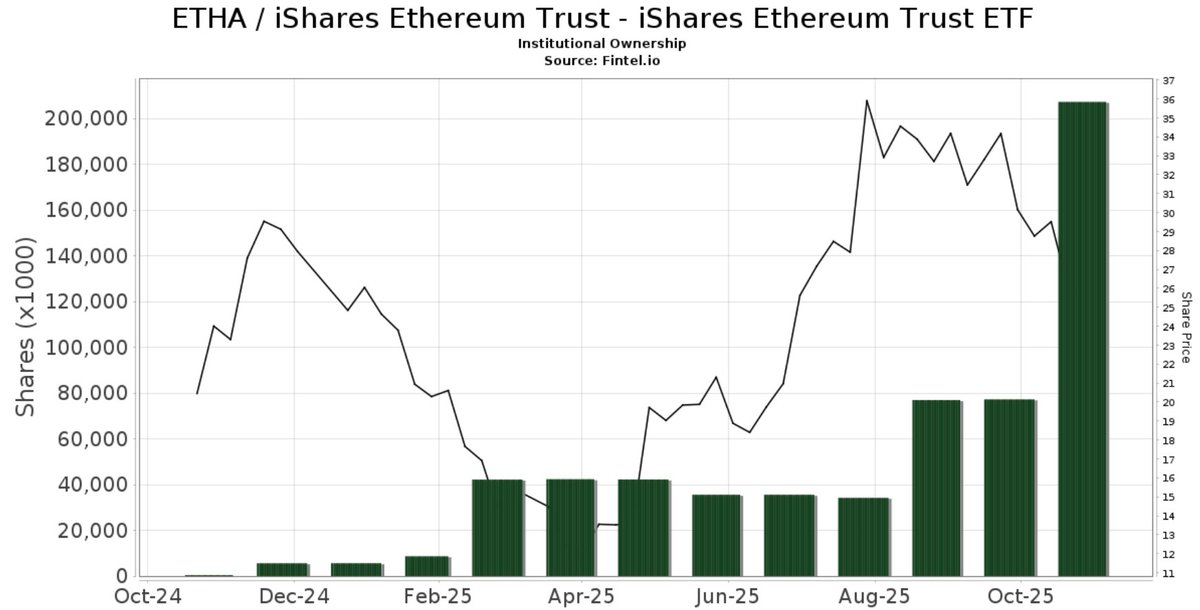

23 Nov 2025

The biggest #Ethereum ETF, $ETHA, has a ton of 13F filings in November of institutions buying in.

It's not just #Ethereum treasuries buying $ETH.

Most institutions are increasing exposure and not selling.

fintel.io/so/us/etha

15

23

282

31,514