Canadian Energy. Former sell side scrub, IR punching bag, corporate schmuck.

Joined October 2014

- Tweets 4,780

- Following 219

- Followers 6,619

- Likes 13,692

692 Photos and videos

Pinned Tweet

1 Nov 2021

Capital discipline in the Canadian Oil & Gas industry? Let’s find out. A thread.

18

27

190

Need more details to determine if this new carbon tax agreement is better or worse than current; less bad is still bad, and bad is bad.

1

3

720

Canadian Energy Analysis retweeted

I asked AI to write a haiku for $TOU:

Tourmaline drifts low,

Charts whisper unmet promise—

Patience thins like fog.

3

2

33

3,702

Golfing with a couple of juniors:

Them: you’re really good

Me: I used to be

Them: what happened?

Me: I got old

Them: oh

Me: ☠️

9

1,136

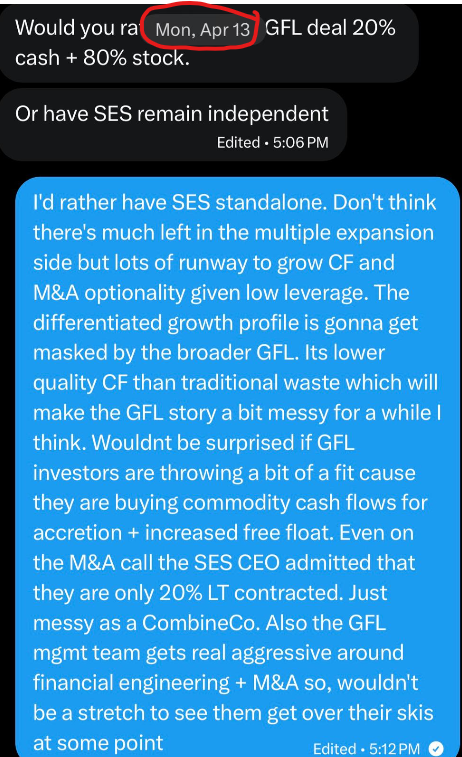

This guy is one of the few on here who is actually taking an objective view of $SES. It should not trade at 16-18x; 11x is a gift.

The $GFL / $SES.TO merger getting this contentious wasn't on my bingo card.

My position is unchanged: this isn't the optimal outcome for either party. That said, $SES.TO shareholders are getting a good price today. At 11x forward (announced price) or ~10.5x using current $GFL price, investors should take their ball and go home. For continued energy beta via OFS, I'd point you to $CEU.TO, a best-in-class specialty chemicals biz trading at 9.5x that's tied to production (vs. drilling activity), much like $SES.TO's base biz.

My comment below on preferring $SES.TO standalone is b/c a combo with $GFL is sub-optimal for both sides.

$GFL shareholders want truly non-cyclical CFs. Adding OFS pressures the multiple by muddying the story and weakens $GFL's ability to do accretive SW M&A, especially opportunistic M&A in economic downcycles.

For $SES.TO shareholders, the standalone growth profile gets watered down by the broader $GFL. That's not to say $SES.TO is a "waste" biz whose chart will grind up and to the right, as many suggest. When the next energy downcycle hits (and it will), the multiple will compress dramatically. But $SES.TO holders should be given the chance to trade around that growth profile and energy cycle volatility.

My near-term view on $SES.TO is positive: the Iran situation should inject a geopolitical risk premium into oil that we haven't seen in a decade . Layer on renewed focus on security of supply, which will point major crude and products buyers to NAM. $SES.TO's core business will benefit because it supports Canada's long-life resource base and an oil price anywhere close to US$80 is great for basin-wide profitability and will support healthy activity levels.

If $SES.TO's multiple keeps grinding higher as generalists conflate commodity CFs in a constructive oil price environment with business quality, this opens the door to accretive M&A of actual waste assets and a longer-term pivot. That's the additional optionality in the $SES.TO thesis, but it requires that the oil price remains high enough for long enough. Once again, this highlights $SES.TO's exposure to energy beta.

1

21

7,321

Canadian Energy Analysis retweeted

Apr 10

Are you serious? I don’t know your CAGR and you don’t know mine — nor do I care. You could be -99% or 9,999% on the year and I’d still engage because this is my sector.

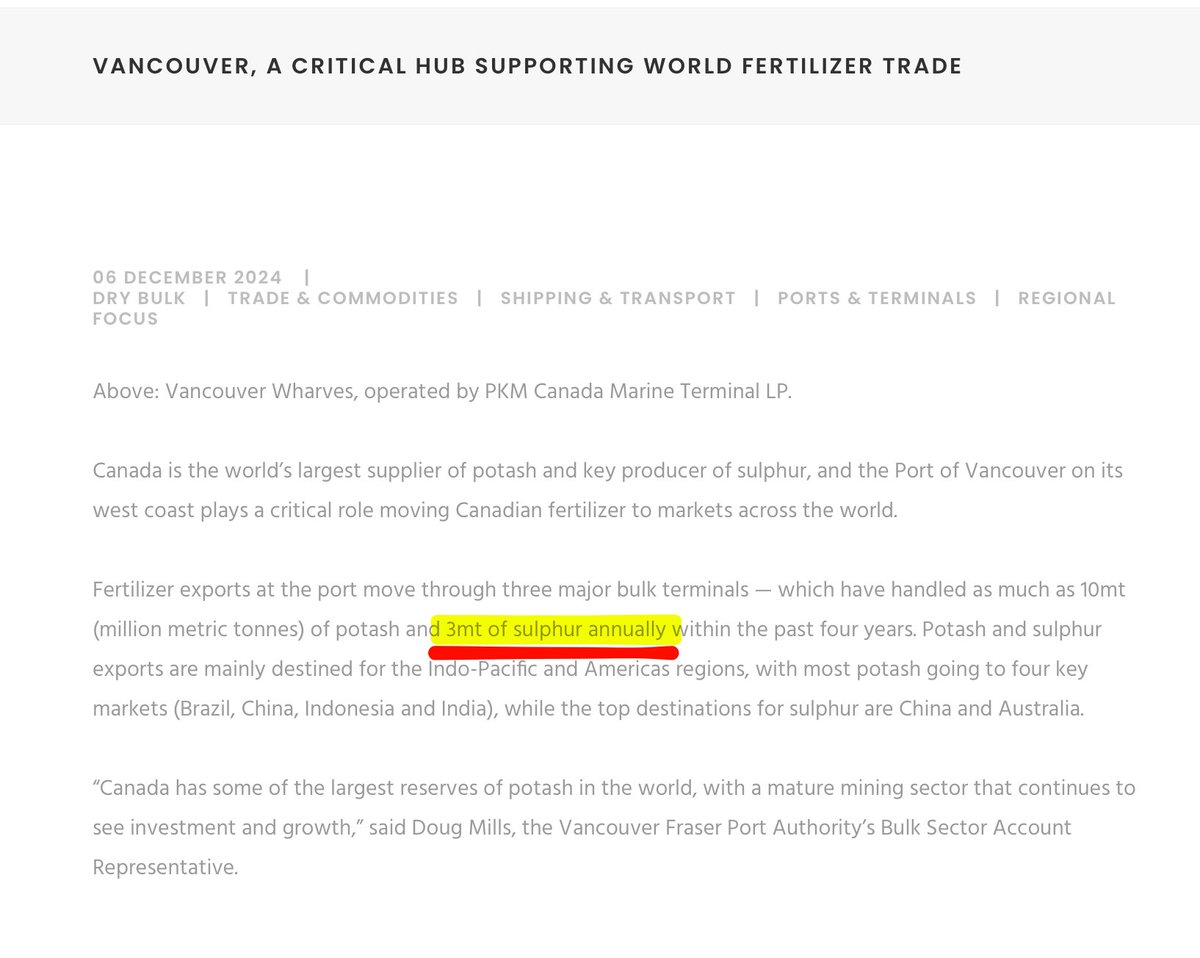

Why not take a minute to wonder why it's just accumulating there? In January of 2026, FOB Vancouver pricing was ~$500/t, that 10 million tonne pile would be $5 billion! So why weren't they selling it then?

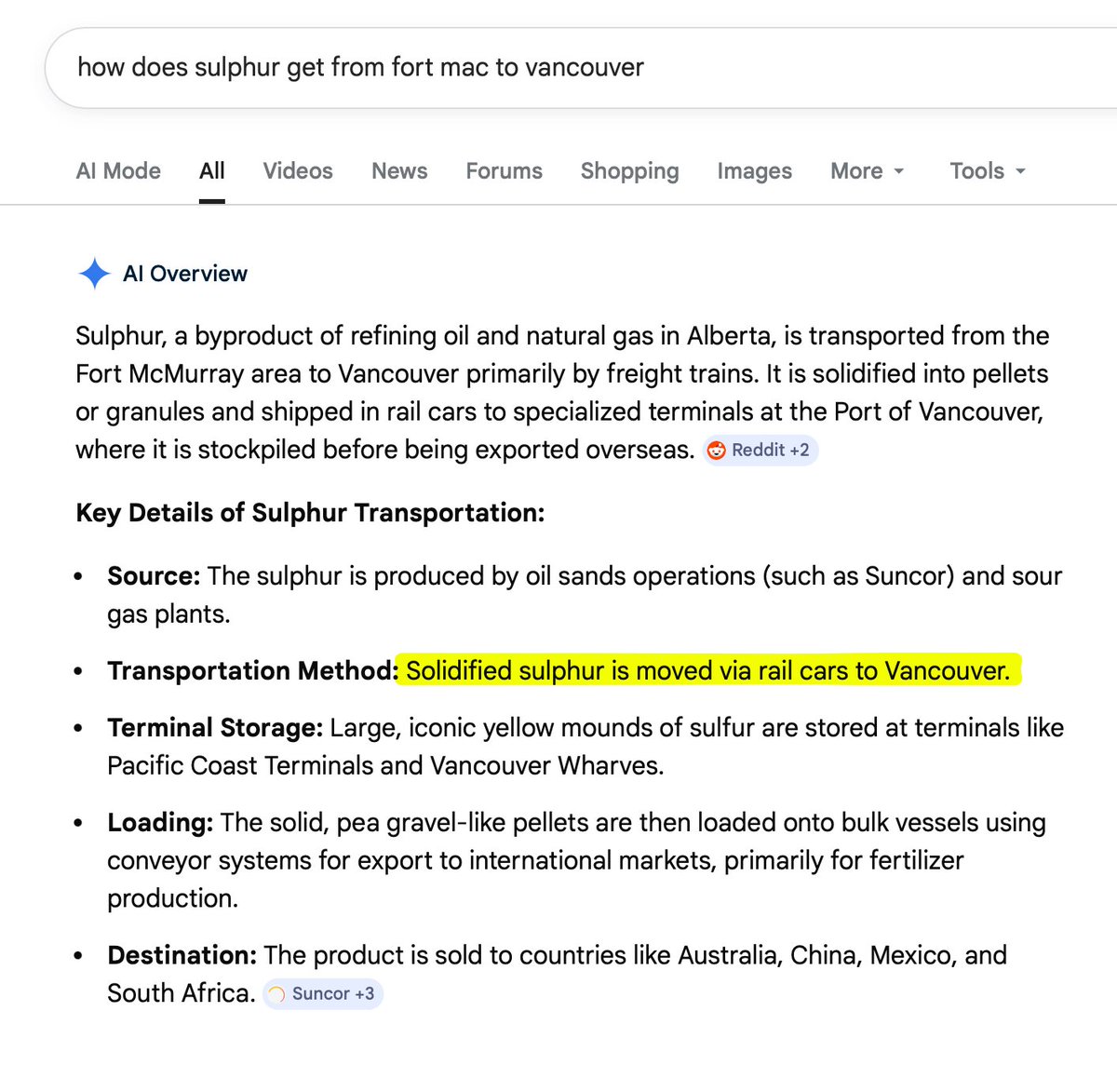

There’s a reason that it sits there; because you transport sulphur via rail to Vancouver, and then you need space at a dry bulk terminal. The Port of Vancouver can handle 3 million tonnes a year of sulphur exports. At that rate, if *just* Suncor owned the terminal (they don't), it would have >3 years to export their Suplhur.

But, Suncor isn't the only Sulphur exporter from Vancouver; and they're not the only oil sands mine in Fort Mac. In terms of free terminal space, there's ~2,000 tonnes a day of export capacity, if you're lucky, or 0.73mt/yr, so at that rate it'd take Suncor almost 15 years to sell their Fort Mac inventory.

But Suncor isn't the only Oil Sands mine with Sulphur, nor the only Sulphur producer in Alberta! So they're competing with everyone else for that terminal space.

And to even get to the Vancouver terminal; you need to rail your Sulphur. So you have 3 bottlenecks to get your Sulphur from Fort Mac to the Port of Vancouver; your rail terminal/transloading capacity, your ability to book rail cars, and your actual dry bulk terminal capacity in Vancouver.

And every single Sulphur producer in the province (i.e. everyone with an oil sands mine, refinery, or sour gas plant), is trying to export their Sulphur.

So you end up with highly depressed local prices for Sulphur (why Cavvy/Pieridae did their infamously poor deal with Shell) -- much like AECO gas, it's trapped in the province. You're effectively using TTF pricing to mark AECO reserves in the ground with no ability to land that gas in Europe. It's ridiculous and a fundamental misunderstanding of commodity markets.

Again, I don't know your returns, nor do I care; but if you're going to be so freaking cocky about a claim so bold, and tell me to "google it" -- at least make sure you're right, and have done at least one second-order google search yourself.

17

7

354

63,629

Trying to implement AI at a big bureaucratic organization:

Me: Copilot is useless, can we get Claude instead?

IT: No.

Me: but we could cut so many people if you let us use Claude.

IT: No. Case resolved. Ticket closed.

IT email: Please complete this short survey.

1

7

1,358

Canadian Energy Analysis retweeted

Mar 9

Please for the love of everything holy if you are an E&P do not do anything stupid.

Do not buy back your shares after running your cashflow at $110/bbl WTI. No they're not cheap. The time to buy back stock was every day over the last year.

Do not buy new assets. The time to buy new assets was every day over the last year.

Do not grow. If you couldn't grow over the last year economically, you are almost certainly not going to be able to maintain your new-found production levels when the market reverts. You are not the low cost producer.

27

12

273

31,657

Has there ever been a more ADHD company with respect to M&A than $OVV? 🤦♂️

3

1

27

7,123

Hearing $SCR has asked shareholders to give back the $10/sh special dividend they just paid out.

Bullish.

2

1

45

28,249

Not a source of pride, but posting my 24 year equity curve for full transparency.

Few.

1

16

2,998

Canadian Energy Analysis retweeted

29 Jan 2024

A thread with some thoughts on $GFR Greenfire Resources Ltd.

TL/DR: I think their 12% notes offer a better risk/reward than the equity.

3

1

22

6,671

8 Dec 2025

Mosaic theory: witnessed Mr. Rose buying coffee at Analog (instead of Tim’s) & generously giving to “spare enough for a coffee guy”.

—> Q4 results will be an absolute banger and you should buy my deep OTM $TOU call options that I’m desperate to unload

1,000% investment advice

6

50

5,848

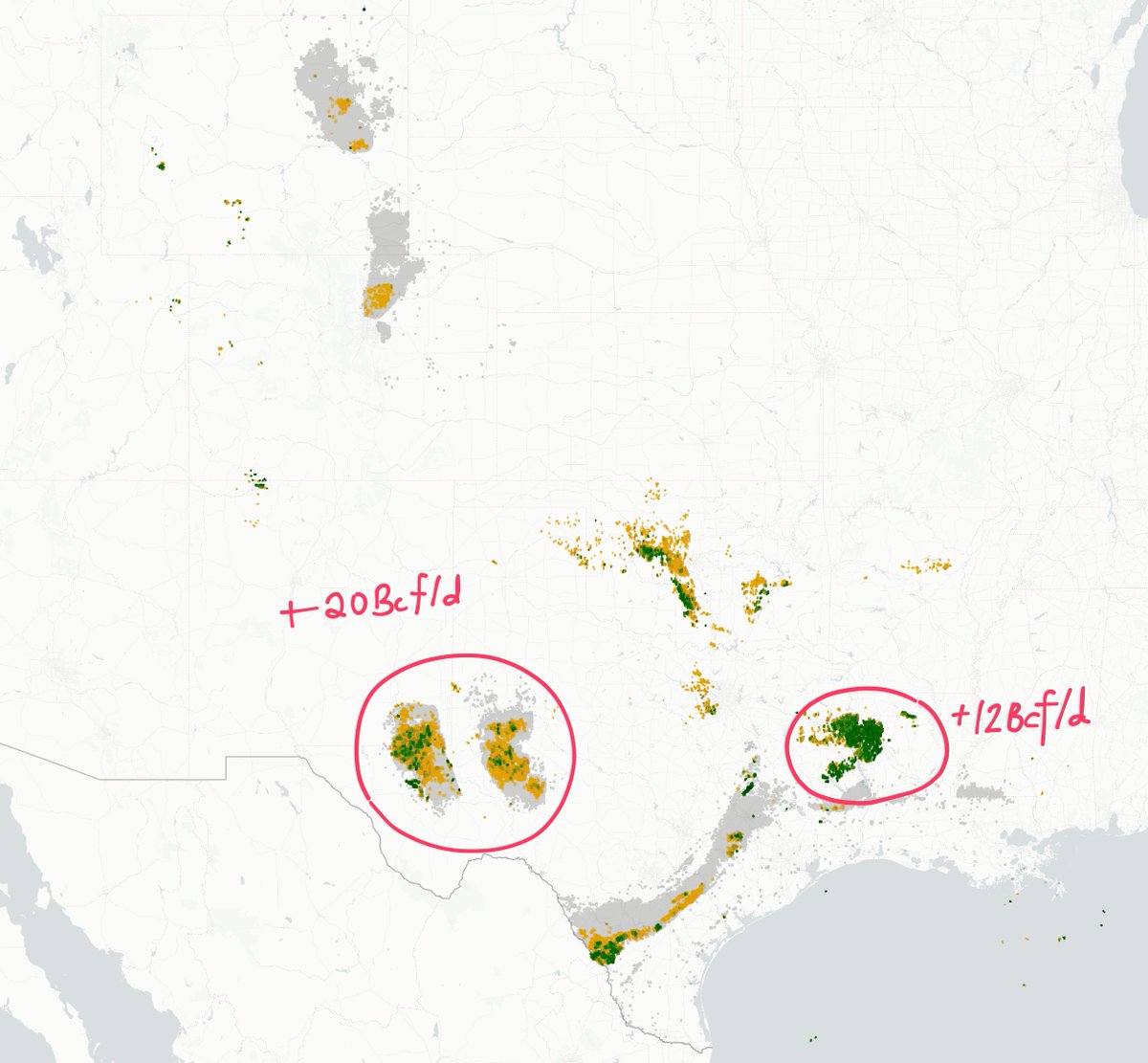

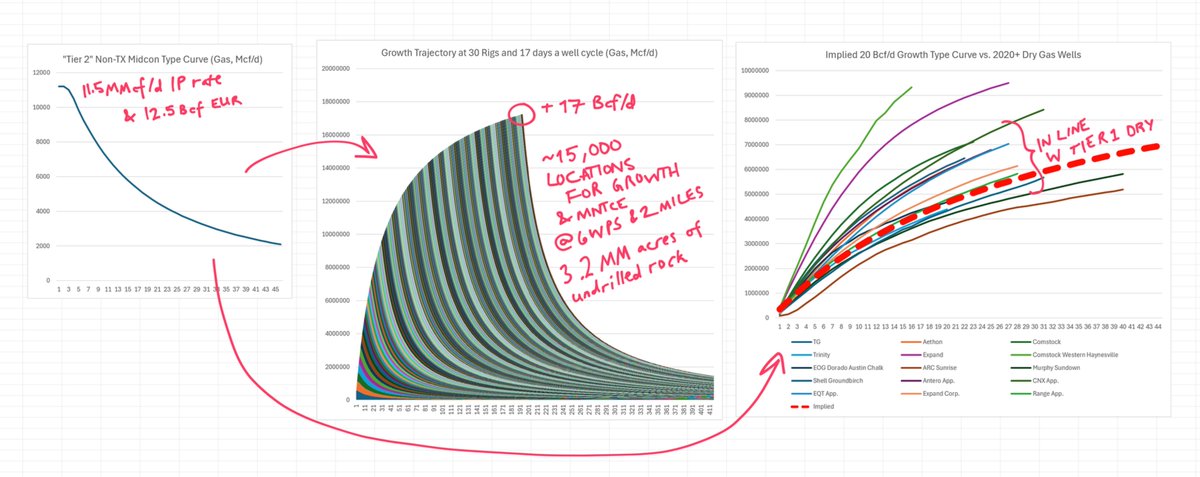

#natgas - for those who care to read an informed back and forth on natgas fundamentals in L48 medium to long term. Read the whole thread (this is the last post in chain atm). Discussion between @ShaleTier7 and @NextWaveEFT .

7 Dec 2025

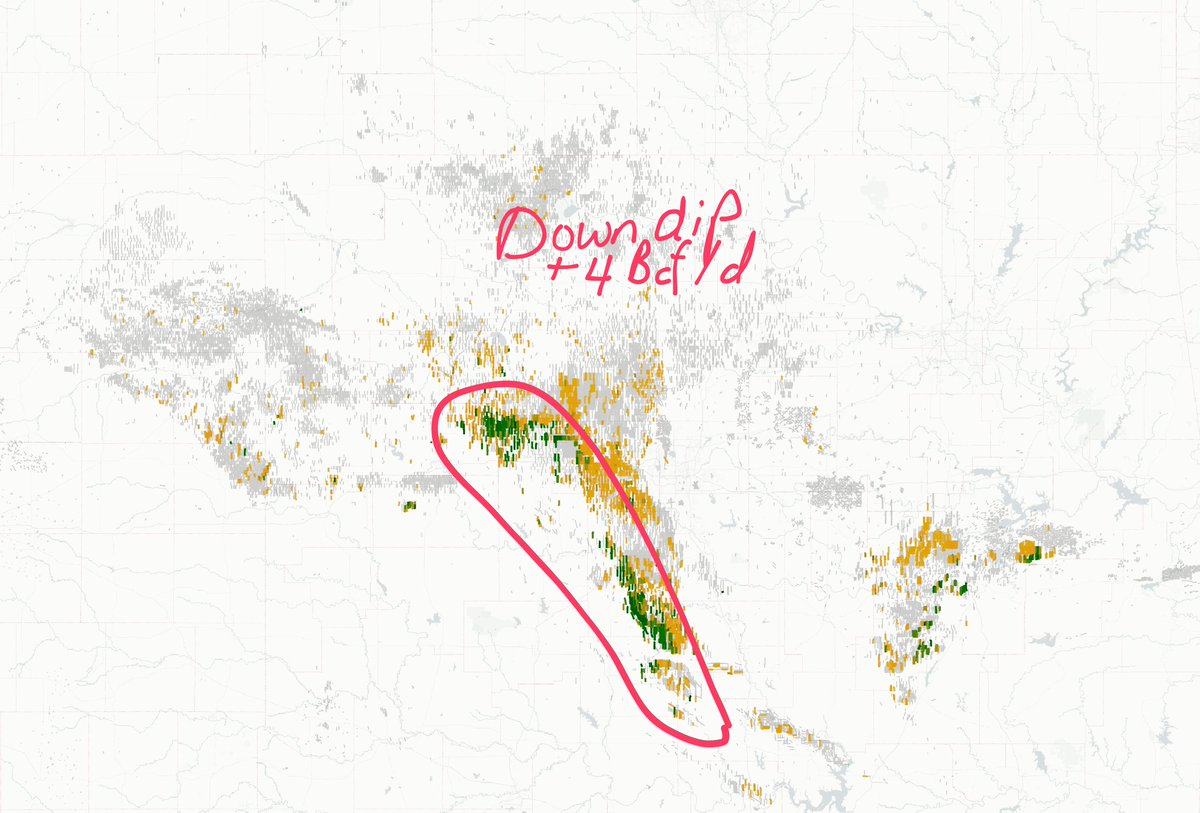

Man, I appreciate the view, and a year ago I would have fully agreed with you, and argued against myself with the same "people miss the Tier 2 rock" case, but you're making some fairly dangerous implicit assumptions that I think you'd even agree are not defensible.

Let's say you're right, and those collective plays get to 17 Bcf/d over the next 10 years, while maintaining current production (so 40 rigs, not 30). I'm assuming a generous 17 day cycle time for 615 wells a year, in reality downdip OK is deeper and has a median spud to rig release of 46 days, so I'm giving you a ~30 day drilling advantage. All-in, that's 15,000 locations and 3.2 million acres of undrilled rock, *on top* of maintaining current volumes.

On an 11.5 MMcf/d IP type curve, and a 12 Bcf sales EUR (14 Bcf raw) you're going to get ~17 Bcf/d of growth running 30 new rigs nonstop for 20 years. But you need 15,000 locations. Where are there 15,000 locations in the midcon that are going to do 1.4 Bcf/1K' and IP at >12 MMcf/d raw -- and why haven't they been drilled yet? Assuming it's rich gas at even 30 Bbls/MMcf that's a 415 MBO EUR.

In OK, the IP90 rate for *only wells with an EUR >0.5 Bcf/1K'* was ~5 MMcf/d, so I'm also giving you an 8 MMcf/d IP advantage and ~0.5 Bcf/1K' advantage. IN DJ/PRB it's closer to 2-3MMcf/d IP90 rate, so I'm giving a massive advantage there. In the Barnett the IP90 average is ~4 MMcf/d. In 2022 the Barnett averaged 3 rigs and grew <50 MMcf/d.

If I slash that type curve in half, and cycle times to 23 days (WAY more reasonable), which is still a 7 Bcf EUR, that growth tops out ~7 Bcf/d, not 17 Bcf/d. The economics on that more reasonable type curve at ~3.2 year pay out and 29% IRR at $3.50 realizing 100% HH ($8MM D&C, $9/BOE GP&T OPEX, 55B/M liquids). And you're right, there needs to be more infra, so that 1.6x recycle ratio well also needs to build new plants, compression, etc.; at $4.50 it's more reasonable, 2.0x recycle, 55% IRR, and at $5 it's definitely doable. But it's absolutely not in the money at $3.50, unless you have a problem with these assumptions.

So the statement that "they will grow 10-20 Bcf/d over the next 10 years" assumes that;

- 30 new rigs are added, ontop of maintaining volumes, and there's inventory to support that growth and that we'll drill wells in 17 days instead of the typical 50 days

- IP rates/EURs are going to be competitive with the Texas Haynesville but didn't breakeven below $3 before but will break even at $3.50

- At 35 Bbls/MMcf, that somewhere there are 15,000 locations that have a 2.5MMBOE EUR that *haven't* been drilled yet despite breaking even in the $2s

- There is enough margin to support the infrastructure required to grow, and the cost structure to reach the USGC all-in is $1.50/MMBtu

I think none of these implicit assumption are correct. The Barnett doesn't have inventory that will do 1.5 Bcf/1K', nor do the other plays have 15,000 locations like that. It's a dangerous generalization IMHO.

6

64

19,145

Last month in our conversation with @sama, he predicted that most new datacenters will be powered by natural gas – at least for now.

Natural gas has become a crazy story recently, as it's central to both AI and LNG, two huge capex builds with geopolitical implications.

We asked Michael Spyker of HTM Energy to teach us everything we need to know about natural gas. Here's part one of his fascinating deep dive: a16z.news/p/gas-fired-intell…

@ShaleTier7

27

58

299

81,630