Growth // @pendle_fi Pendlin the DeFi yield layer.

Joined March 2016

- Tweets 252

- Following 483

- Followers 1,046

- Likes 836

30 Photos and videos

Pinned Tweet

22 Nov 2024

I believe in TN's hair.

21 Nov 2024

Believe in something

1

10

2,250

Dan retweeted

Happy New Year!

In the last 5 months that @boros_fi has been running, we have observed:

- $7B in cumulative trading volumes

- peak OI at $250M (prior to Xmas maturity)

- large counterparties swapping 8-figures in OI to capture FR spreads up to 7% across exchanges ie BN/OKX/HL

8

10

52

3,963

4 Sep 2025

I have since flipped to the other side and getting toast by the market. 💀

5

10

1,360

Dan retweeted

23 Mar 2025

How to earn $358,478 USD in 2 months with Pendle.

⬇️⬇️

14

3

50

8,302

Dan retweeted

6 Feb 2025

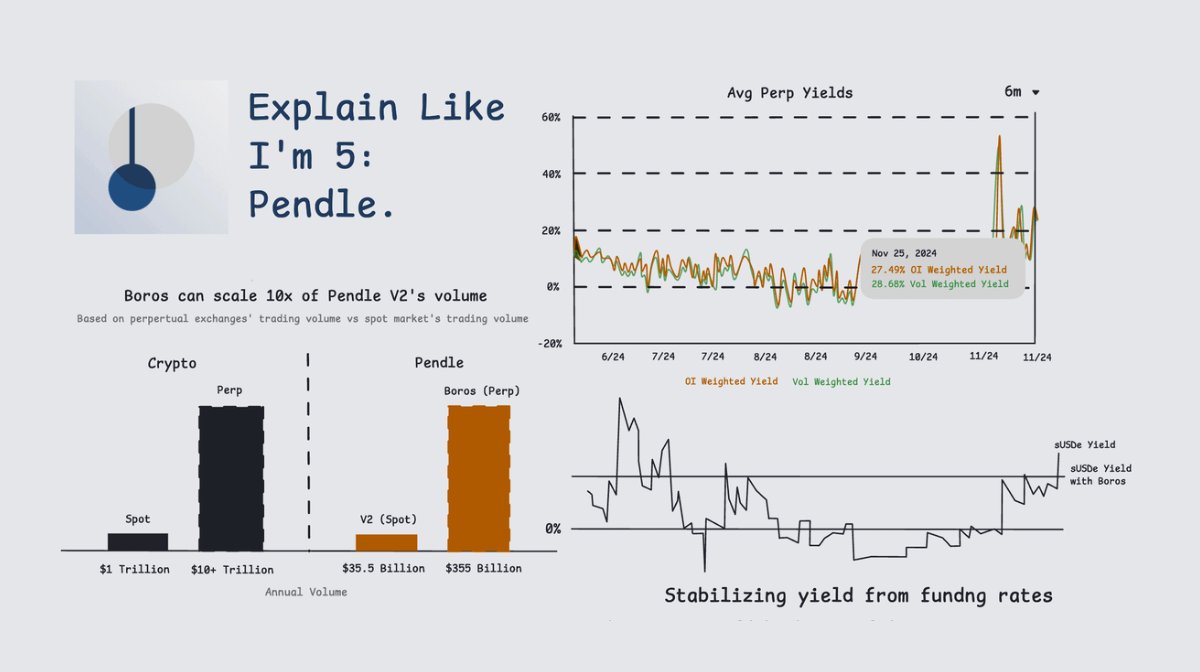

Explain Like I'm 5: @pendle_fi.

🧵: What is Boros (trading funding rates).

43

101

541

85,457

4 Feb 2025

Big fat busy times ahead

4 Feb 2025

Pendle 2025: Zenith

In this post, I've outlined the highlights for Pendle V2 in 2024, our future roadmap for the 3 pillars of Pendle - V2, Citadels and Boros, as well as The End Game.

Job's not done - but it'll be.

5

30

1,270

Dan retweeted

4 Feb 2025

Pendle 2025: Zenith

In this post, I've outlined the highlights for Pendle V2 in 2024, our future roadmap for the 3 pillars of Pendle - V2, Citadels and Boros, as well as The End Game.

Job's not done - but it'll be.

134

119

676

616,158

Dan retweeted

28 Jan 2025

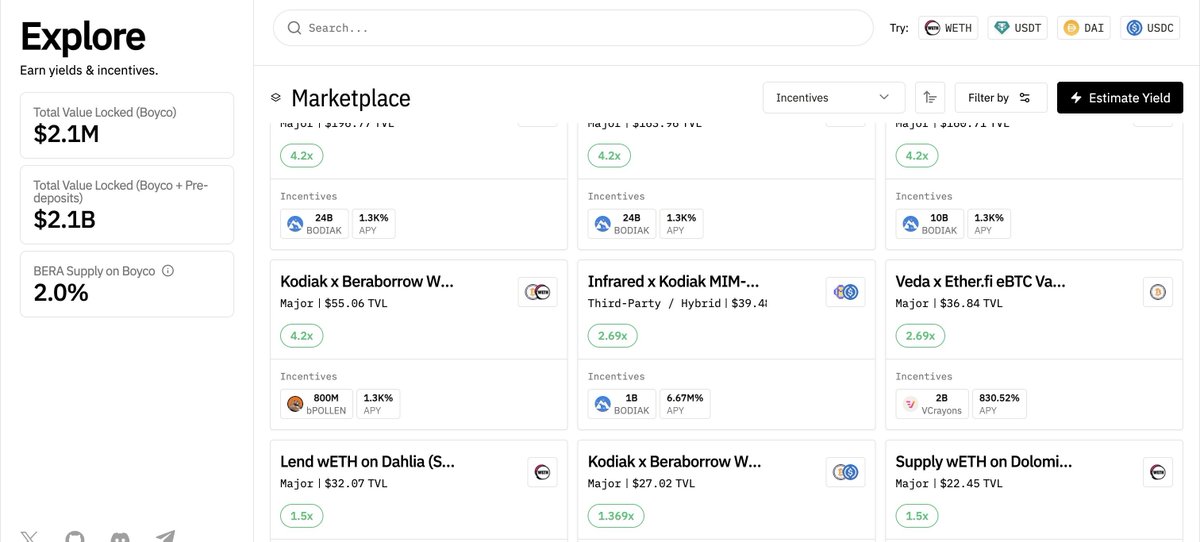

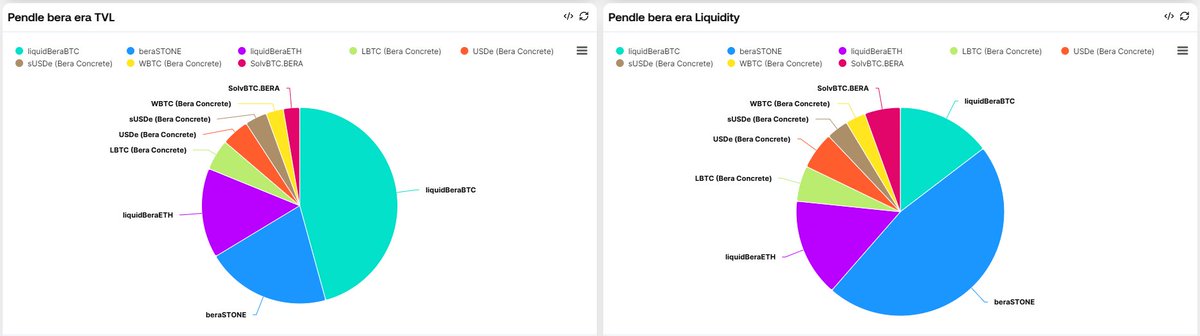

Currently, Boyco by @berachain is officially live. However, the community was quite surprised when the project allocated 2% of the total $BERA supply to Boyco instead of the previously announced 1.5%.

At the same time, the TVL of Bera Era pools on @pendle_fi has approached ~$600M, accounting for more than 25% of the total TVL in Boyco Vaults, demonstrating the high demand for utilizing those assets with Pendle.

And to make it easier to track Bera Era metrics on Pendle, I have compiled a dashboard that includes the fees collected and TVL breakdown by asset type in each pool.

You can access the full dashboard here (Bera Era Fee & Bera Era Liquidity): flipsidecrypto.xyz/neo_nguye…

P/S: Latest update - users can now farm up to 10 types of points instead of just 8 as before on Pendle (as shown in the image below).

The choice for farming points will also be more diverse, depending on each individual's preferences.

Tagging chads are bullish on both Pendle and Berachain:

@tn_pendle @Rightsideonly @PendleIntern @0xlenn @btclin @Jonasoeth @crypto_linn @quant_sheep @0xTindorr @phtevenstrong @LisaFlorentina8 @Hirohnguyen @0xTrablo @2lambro @JasonvuTech @Chris_Insights @chutoro_au @ViNc2453 @NaveenCypto @kenodnb @EthereumThaila1 @Milk_Trudge @JiraiyaReal @monosarin @DeFi_Perryy @YashasEdu @TheDeFinvestor @ellaqiang9 @Alvin0617 @jackvi810 @web3_alina @sortition1337 @0xCheeezzyyyy @Frogling68 @TheDefiDog @eli5defi @captainjack @SmokeyTheBera @hanztrinh @Berasearch @splinter0n

48

19

133

28,502

Dan retweeted

16 Dec 2024

The upcoming @pendle_fi airdrop was 4.2M$ a few weeks back, now it is already at 8M$... and we might have some really good weeks ahead of us leading up to the end of the year.

hm.

hmmmmm.

HMMMMMMMMMMMMMM.

Pendlicious.

vePendle holders:

2

5

49

8,422

Dan retweeted

16 Dec 2024

Christmas came early for @pendle_fi ❄️

2024 has been a great year and we thank you for being a part of this incredible journey with us!

But the best is yet to come. 2025 is shaping up to be even better, and we can’t wait to share what’s in store!

JOB'S NOT DONE 🎄

23

25

153

25,010

11 Nov 2024

Boros

11 Nov 2024

Introducing Boros by Pendle: Yield Trading with Margin

Based on the ancient Greek word meaning “to eat”, Boros is Pendle’s newest platform. Developed from scratch in our conquest to consume every yield in the world, both onchain and offchain, starting with funding rates.

Of Boros, tokenomics and more, check out pendle.medium.com/boros-by-p…

1

16

481

Dan retweeted

11 Nov 2024

Introducing Boros by Pendle: Yield Trading with Margin

Based on the ancient Greek word meaning “to eat”, Boros is Pendle’s newest platform. Developed from scratch in our conquest to consume every yield in the world, both onchain and offchain, starting with funding rates.

Of Boros, tokenomics and more, check out pendle.medium.com/boros-by-p…

88

153

709

276,231

Dan retweeted

10 Oct 2024

Pendle PT tokens from @pendle_fi are increasingly being used as collateral in lending markets to create high-yielding positions.

Yet there are substantial challenges for creating and managing these kinds of markets using existing solutions.

Here’s how Euler vaults can make life simpler, safer, and more efficient.

--

Pendle PT tokens represent the principal of a yield-bearing asset. They typically trade at a discount to their underlying, giving rise to a fixed interest rate for the period over which they mature.

For example, a PT token for sUSDe which matures on 24th October currently yields ~12.5% APY.

Using this as collateral to borrow, for example, USDC, enables borrowers to earn a multiplier on their earned interest.

Borrowers can deposit the sUSDe PT token as collateral, borrow USDC at a cost of e.g. 5%, and then loop.

At a loan-to-value of 0.75, this enables a multiplier of around 4x, meaning borrowers can earn an upper limit of 4x * (12.5 - 5) ~= 30%.

Meanwhile, lenders of USDC benefit from receiving yield on a relatively low risk market. They earn 5% whilst lending to the holders of a collateral asset which is highly correlated in price (and therefore relatively unlikely to trigger liquidations). As the PT token matures, the value of the collateral increases over time as well.

Overall, one can see why it is a popular trade.

Today these kinds of positions are typically being created on lending protocols using ungoverned isolated pairs. There’s several reasons why that is a sub-optimal approach in terms of simplicity, risk management, and efficiency.

--

First, creating and managing lending pairs for this kind of trade is deeply inefficient and will require a lot of housekeeping. If there are several high-yielding PT tokens USDC lenders want to lend to, a separate USDC pool is required for each PT token.

This means USDC lenders need to fragment and manage their liquidity inside multiple pairs at once. This is especially challenging when considering that new PT-USDC pairs need to be recreated every time a PT token is close to maturity, with lenders having to migrate frequently between pools.

In a best case scenario, all borrowers will repay their loans close to maturity, but in practice this never happens. For some lenders, this means their USDC could be stuck inside an illiquid pool for a prolonged period of time after maturity. Earning yield, yes, but still unable to withdraw.

Even if lenders use a risk curator to manage this process on their behalf, the fragmented liquidity across different USDC vaults creates uncertainty for borrowers, with more volatile rates making profit calculations harder.

Euler vaults can be used to overcome the inefficiencies of pairs very easily. A single vault can be created that is designed to accept any number of collateral assets. This means a vault creator can add multiple PT tokens as collateral at once, or gradually add and remove PT tokens as they are born or reach maturity.

This makes life much easier for both lenders and borrowers, who can more easily roll their positions as the world moves on.

--

Second, using ungoverned markets for PT tokens raises challenges for risk management. In the rare event that something goes wrong, USDC lenders might appreciate having additional checks and balances on vaults to help manage risk.

Euler vaults can be deployed in an ungoverned manner if people wish, but they also allow risk curators to govern and help manage risk. A governor would have the option to be able to slowly ramp down LTVs, switch interest rates, modify supply and borrow caps to curb further borrowing activity. Alternatively, vault creators can add custom hooks which can be used to allow permissioned deposits or liquidations, withdrawal delays, and more.

These governance and more advanced risk management features are completely optional and likely won’t to everyone’s taste, but for many users will add value.

--

Third, using isolated pairs with fixed LTVs and liquidation bonus parameters can pose risks to both lenders and borrowers.

In the event of liquidation, borrowers should have to pay no more than is needed for someone to close out their position. Yet on the vast majority of lending protocols, the liquidation bonus paid to liquidators is a fixed percentage of the borrower’s collateral – typically more than 5%!

This means borrowers who have looped 4x stand to lose up to 20% of their collateral, just to pay for the privilege of being liquidated by an MEV bot.

This is obviously bad news for borrowers, but it poses risks to lenders too. If 20% of a borrower’s collateral is going towards liquidation costs, that’s 20% that is no longer helping to secure loans. Fixed liquidation bonuses can, in some circumstances, therefore elevate the risks of bad debt to lenders as well as punishing borrowers.

In contrast, Euler uses a Dutch-auction based approach to price the liquidation bonus. This leads to much fairer liquidation bonuses that tend to only be a little higher than the fixed cost to liquidate someone. I wrote about how this is the fairest liquidation mechanism in DeFi recently here: x.com/euler_mab/status/18414….

--

Finally, most people building and managing looped positions on PT tokens today are doing so manually. This costs gas and takes a significant amount of time. Unwinding positions in a hurry is a nightmare.

Euler’s powerful batch transaction system with liquidity deferral checks enables looping PT token’s as collateral in a single transaction. Moreover, borrowers have the option to use intents to enable operators to manage positions on their behalf, giving them the option to automatically close out positions which are no longer profitable, execute more advanced stop-loss and take profit orders, and much more.

--

Overall, Euler is a very flexible lending platform where builders can deploy vaults that can make life simpler, safer, and more efficient for traders.

Pendle PT integrations with Euler may unlock a whole new world of possibilities.

2 Oct 2024

Euler still has the fairest and most efficient liquidation mechanism for borrowers in all of DeFi in my humble opinion:

- the lowest liquidation penalties

- no liquidation fees

- the option to use intents to customise partial liquidations, stop-losses, and take profit options

Here's how it all works with some discussion of the trade-offs associated with different designs.

Feel free to disagree!

--

When a user is at risk of becoming insolvent, you want liquidators to come in and close out their position. The liquidators aren't going to do this out of the goodness of their heart, they want to get paid. That payment comes in the form of a bonus, taken from the user's collateral.

But how big should the bonus be? In a world of fluctuating gas prices, asset prices, and liquidity, how do we even know how much it will cost to perform a liquidation so that we can compensate people fairly?

We generally don't. So, instead, what most lending protocols do is take a fixed % of a user's collateral and give that to the liquidators. The problem with this is two fold.

First, there is no fixed percetage that works fairly in all cases. Is 10% fair? Well 10% on collateral of $200 often isn't going to cut it, meaning positions won't get liquidated, but 10% on collateral of $2m is a payment of $200k. Imagine paying $200k to your friendly neighbourhood liquidator for the privelege of being liquidated! There are many such cases.

Second, most large bonuses don't even go to the liquidators, they end just generating MEV. Everyone can see a liquidation is coming, and profitable ones will generally get sniped by bots who bid up the gas price to get priority inclusion.

So what we do on Euler to avoid this is use reverse Dutch auctions. These are based on health scores, rather than based on time. A user with health of 0.99 pays a 1% bonus. A user with health of 0.95 pays a bonus of 5%, and so on. As a user's health score falls, the potential profit to liquidators rises. Since anyone can liquidate at any time, there's a Dutch auction on the liquidation bonus, which in a copetitive environment like Ethereum, usually settles close to the marginal level of profitability for liquidation.

This means that if it costs $20 to liquidate, then the liquidation bonus on collateral of $200 will be found at close to 10%, whereas on collateral of $2m, will be found at close to just 0.001%.

--

On Euler there are also no liquidation fees. Many lending protocols implement these as a source of extra revenue. These fees can be incredibly punishing, and create a conflict of interest between the protocol's governors and their borrowers. The protocol wants you to get liquidated so that it can get paid. Sophisticated borrowers should be factoring these fees into their expected cost of borrowing. Something like this:

extraBorrowingCost = P(liquidation) * liquidationFee / initialCollateral

A fee of 1% sounds innocent enough, but for people looping, the fee gets taken on the looped amount. So 1% can quickly become 5% or more. If you're a large borrower why risk paying this?

--

Finally, Euler makes partial liquidations optional by giving borrowers the option to use intents to customise partial liquidations, stop-losses, take profits and more.

Rather than impose an opinionated model for partial liquidations onto borrowers, like we did in Euler v1, in v2 borrowers can recruit operators to perform actions on their accounts under tightly specified conditions.

Example: "if the chainlink oracle for BTC reports a price of $55k or less, close out 50% of my position for me and you will get a reward of 50 USDC"

Operators can be smart contracts or literal people in an office clicking buttons. It doesn't really matter. The allowable actions and incentive to perform those actions on an account is pre-specified by the borrower. In the scenario in which they choose nothing, the only actions that can be taken are through liquidations.

You can even implement a kind of LLAMA-like liquidation using this mechanism. You want an operator that scales out of your position as the price falls, and scales back into the position if it begins to rise again.

--

Some lending protocols group positions into bands so that they can be co-liquidated together, which can lead to gas savings. Something like this could also be built on top of Euler by tokenising user positions and allowing transfers between them. Does this really add value though?

An important consideration here is that this type of banding will only increase the efficiency of liquidations if users naturally choose similar collateralisation ratios for their positions so that they are actually banded together often.

On some pairs of assets this might be common if the lending protocol is popular and the trade has a natural schelling point for collateralisation ratio, but for volatile trades where risk/reward tolerances vary, borrowers will tend to vary in their ratios, rendering banding and co-liquidation less beneficial or potentially more costly than a regular liquidation.

It really depends on the popularity of the trade. With banding, borrowers may be incentivised to look for popular bands they can share with other users in order to optimise and reduce expected costs.

--

All in all, I think Euler has an incredibly flexible and efficient system that is hard to beat in terms of value for borrowers.

18

17

157

44,598

18 Jun 2024

Def not written by @chutoro_au

18 Jun 2024

Intern often gets questions about how marketing/content creation works in this space.

You can't run it like a traditional corpo in this space.

Crypto is an entirely different ball game that demands an entirely different beast.

Keep in mind that Intern's going rogue here and these just some points plucked off the top of my mind before my morning coffee:

1. No plan? No problem

This space moves way too quickly to have a quarterly content schedule. Memes fade, numbers change, and strategies don't last long.

There should be an overarching goal, sure, and product releases/partnerships should be deliberately strategized.

But on a day to day basis, CCs should be able to work on the fly with what's given, a creative who's able to respond to the daily happenings and spin out content relentlessly.

2. Jack of All Trades

There's no time to for your shitpost to undergo the usual lengthy review and approval processes, there's no time for your designer to iron out the details in that graphic till perfection.

Don't get me wrong, important announcements and PR pieces should still be rigorously reviewed by multiple parties to ensure it's well positioned. But those daily, spontaneous threads? CCs should be able to get all things done from start to finish.

That means having the DeFi/crypto knowledge to operate independently when hunting down content/inspiration.

Having basic graphic design skills (i.e. Paint, Powerpoint, Photoshop, doesn't matter) so your graphic design can be freed up for more important tasks. Doesn't have to be pretty, but good enough to get the point across and realize your vision. Basic adherence to branding should be respected where relevant of course.

Having the right tinge of degeneracy, enough to keep things interesting for your protocol, but still maintaining the necessary sense to know when, where and how to toe the line.

3. Trust in a Trustless World

You're handing the social media keys to someone who might have a few screws loose in there, it's the driving force behind both their brilliance and unhinged moments. This can't just be any Tom, Dick and Harry with a Marketing Degree plucked from the streets. There needs to be trust to realize the potential of your chaos unicorn.

Prose, meme preference, taste for humour, communication style...All of these need to be screened and assessed, things that might not always come up in a 20-min interview. Preferably, you'd want someone you already trust but absent of this option, take the time to vibe with the person outside of work. Converse, share memes, go on a food trip together (if available), get to really know this person on a semi-personal basis and see if it's someone you'd want to be the voice of your protocol.

---------

Keep in mind that this so-called formula isn't a one-size fit all solution for ALL protocols. But generally, in a space where attention is so scarce, a paradigm shift away from "marketing product" to "marketing for attention" is needed.

And yes, that means pushing out some stupid memes that have little/nothing to do with your protocol too. Time is of the essence, you won't have time to overlook all things and everything. Stop fighting the chaos and learn to harness it.

What other "X-factors" do you think are needed in this space when it comes to marketing/content creation?

2

3

784

Dan retweeted

10 Jun 2024

GM, great start to the week with $20B cumulative trading volume for @pendle_fi 🌅

More to come - launches, volume, TVL...Team is set on delivering some exciting stuff soon 🤞🏻

JOB'S NOT DONE

26

19

169

84,632