Joined March 2026

- Tweets 47

- Following 166

- Followers 89

- Likes 25

14 Photos and videos

May 29

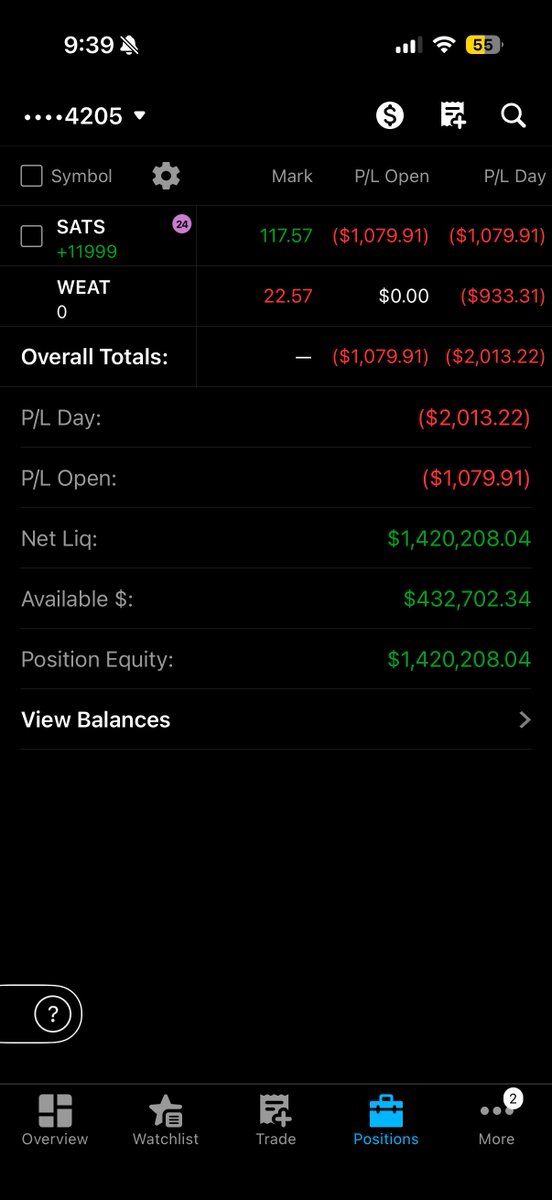

$NBIS position is now at $1,000,000.

Bought and called earlier with screenshots 2 weeks ago.

Thanks @leopoldasch for helping add some fuel to the fire. LFG

Follow for more alphas

May 11

I’ve been positioned for that rerating.

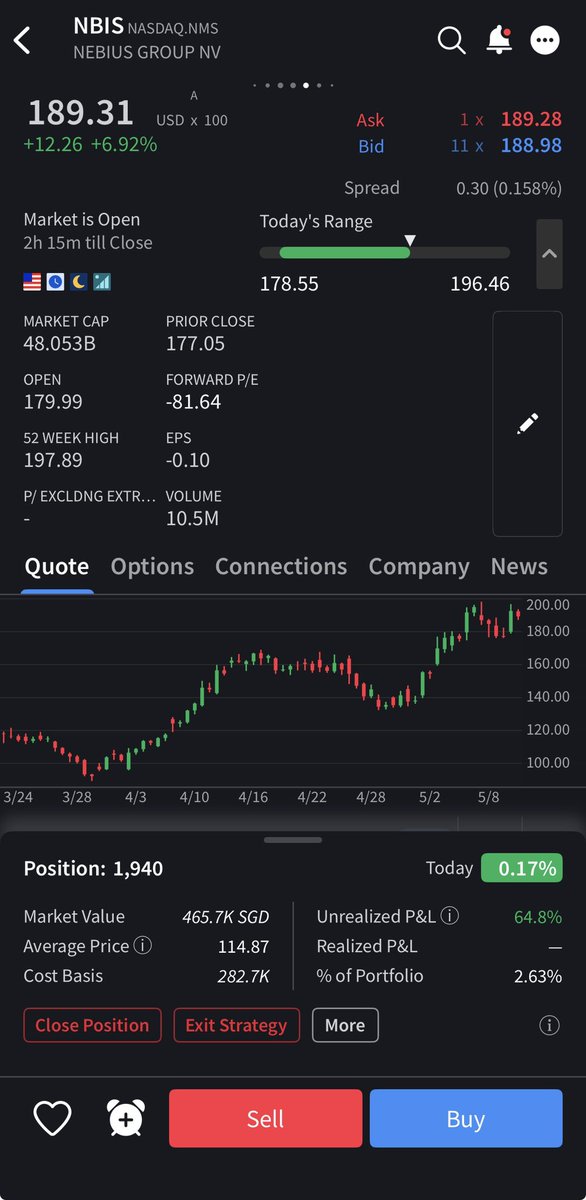

Currently holding 1,940 $NBIS shares with an average around $114.87. Position is up 65% unrealized, with market value now at $466k.

BofA just raised its PT on $NBIS from $175 to $205 and reiterated a Buy rating.

The market is starting to realize Nebius is becoming one of the more credible AI infrastructure plays outside the hyperscalers.

The key debate now is execution:

• How fast they can bring new data center capacity online

• Whether revenue growth can outpace the massive capex ramp

• And if margins can eventually inflect as utilization scales

What stands out to me is the stock keeps absorbing higher valuations because the AI compute demand backdrop remains extremely strong. The Street is increasingly rewarding companies that can actually deliver GPU capacity and infrastructure at scale instead of just selling the AI narrative.

Still think the story here is early if execution continues. The next leg higher probably depends on:

• Faster capacity deployment

• Large enterprise / hyperscaler wins

• Evidence operating leverage improves over time

• Continued scarcity in AI compute supply globally

AI infra remains one of the strongest themes in the market right now, and NBIS is starting to get taken more seriously as a scaled player in that stack.

213

May 29

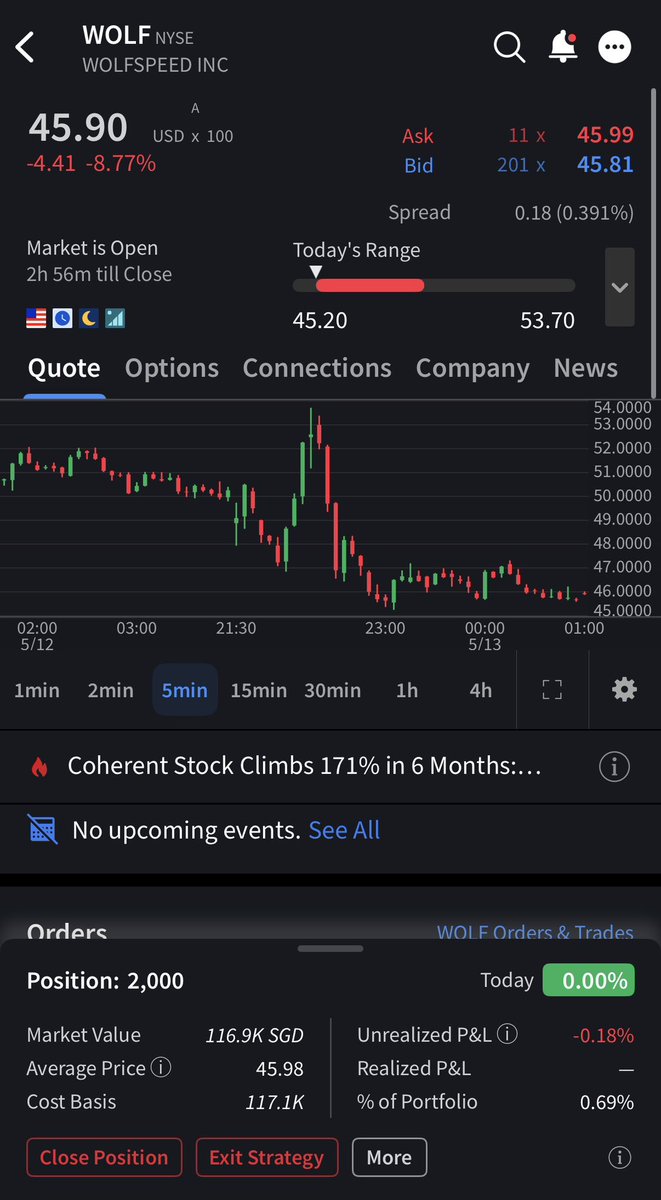

Up close to 50% on my $WOLF position in just 2 weeks.

Thesis still the same.

Follow me for more calls like these. Also made some calls on $NBIS and $DELL too

May 12

Bought $110k worth of $WOLF at $46/share. Downside capped but upside at least a 3x from here.

$WOLF simplified bull thesis:

Wolfspeed nearly went bankrupt building out massive Silicon Carbide capacity too early for the EV market.

But post restructuring, they now own some of the most strategic semiconductor infrastructure in the US:

• The only commercial scale 200mm SiC fab globally

• One of only two companies in the world to demonstrate 300mm SiC capability alongside Coherent ($COHR)

• Fully US based manufacturing at a time America is pushing hard for domestic semiconductor independence

The market still sees WOLF as an EV story.

The bigger opportunity may actually be AI infrastructure.

As AI chips become more power hungry, thermal management and power efficiency become massive bottlenecks. Silicon Carbide could become critical for next generation cooling, power delivery, and advanced packaging.

The key:

Nobody can easily replicate what Wolfspeed already built. The fabs took years and billions of dollars to create.

In a world where the US wants domestic AI supply chains and frontier AI keeps scaling aggressively, $WOLF sits in a uniquely valuable position.

2

1

508

DeepAlpha retweeted

May 12

Bought $110k worth of $WOLF at $46/share. Downside capped but upside at least a 3x from here.

$WOLF simplified bull thesis:

Wolfspeed nearly went bankrupt building out massive Silicon Carbide capacity too early for the EV market.

But post restructuring, they now own some of the most strategic semiconductor infrastructure in the US:

• The only commercial scale 200mm SiC fab globally

• One of only two companies in the world to demonstrate 300mm SiC capability alongside Coherent ($COHR)

• Fully US based manufacturing at a time America is pushing hard for domestic semiconductor independence

The market still sees WOLF as an EV story.

The bigger opportunity may actually be AI infrastructure.

As AI chips become more power hungry, thermal management and power efficiency become massive bottlenecks. Silicon Carbide could become critical for next generation cooling, power delivery, and advanced packaging.

The key:

Nobody can easily replicate what Wolfspeed already built. The fabs took years and billions of dollars to create.

In a world where the US wants domestic AI supply chains and frontier AI keeps scaling aggressively, $WOLF sits in a uniquely valuable position.

2

2

12

7,119

May 13

THE NEXT AI INFRA RERATE?

$WYFI (whitefiber) might be one of the most overlooked AI infrastructure plays in the market right now.

Most people are focused on the $CBRS IPO itself.

Very few are paying attention to the companies enabling the actual compute infrastructure behind it.

$WYFI is already providing powered data center capacity for Cerebras AI workloads today.

That matters because AI scaling is no longer just about chips.

It is about:

• power

• cooling

• data centers

• networking

• inference infrastructure

We already saw $DGXX secure economics around $2.75M per MW annually tied to $CBRS workloads.

If the Cerebras IPO succeeds, the market may begin repricing the entire supporting ecosystem around it.

That is why names like $WYFI, $DGXX, $BTBT, $IREN, $NBIS and $WULF are becoming increasingly interesting.

The setup reminds me of earlier AI infrastructure rerates before Wall Street fully understood the second order beneficiaries.

The most important thing:

Many of these companies are still trading far below AI infrastructure peers despite significantly improving revenue outlooks.

Once broader analyst coverage arrives, that valuation gap may not stay open for long.

2

2

12

1,258

May 12

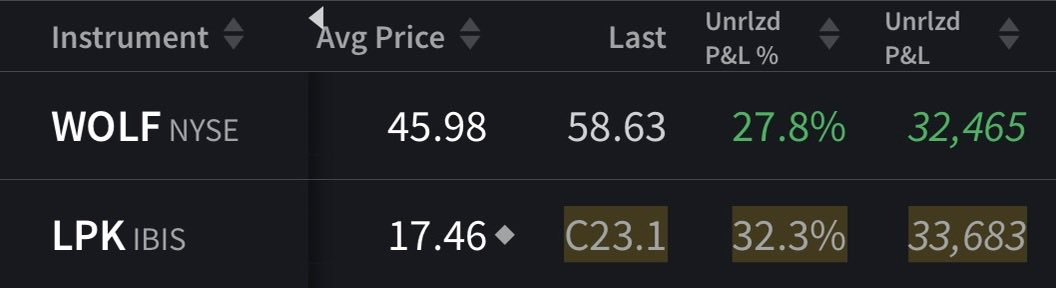

Up 27.8% on $WOLF with an unrealised profit of $32,000.

Price target $130 for $WOLF

Remember that $COHR and $WOLF is competiting for the same space except $WOLF has yet to be repriced.

May 12

Bought $110k worth of $WOLF at $46/share. Downside capped but upside at least a 3x from here.

$WOLF simplified bull thesis:

Wolfspeed nearly went bankrupt building out massive Silicon Carbide capacity too early for the EV market.

But post restructuring, they now own some of the most strategic semiconductor infrastructure in the US:

• The only commercial scale 200mm SiC fab globally

• One of only two companies in the world to demonstrate 300mm SiC capability alongside Coherent ($COHR)

• Fully US based manufacturing at a time America is pushing hard for domestic semiconductor independence

The market still sees WOLF as an EV story.

The bigger opportunity may actually be AI infrastructure.

As AI chips become more power hungry, thermal management and power efficiency become massive bottlenecks. Silicon Carbide could become critical for next generation cooling, power delivery, and advanced packaging.

The key:

Nobody can easily replicate what Wolfspeed already built. The fabs took years and billions of dollars to create.

In a world where the US wants domestic AI supply chains and frontier AI keeps scaling aggressively, $WOLF sits in a uniquely valuable position.

4

308

May 11

I’ve been positioned for that rerating.

Currently holding 1,940 $NBIS shares with an average around $114.87. Position is up 65% unrealized, with market value now at $466k.

BofA just raised its PT on $NBIS from $175 to $205 and reiterated a Buy rating.

The market is starting to realize Nebius is becoming one of the more credible AI infrastructure plays outside the hyperscalers.

The key debate now is execution:

• How fast they can bring new data center capacity online

• Whether revenue growth can outpace the massive capex ramp

• And if margins can eventually inflect as utilization scales

What stands out to me is the stock keeps absorbing higher valuations because the AI compute demand backdrop remains extremely strong. The Street is increasingly rewarding companies that can actually deliver GPU capacity and infrastructure at scale instead of just selling the AI narrative.

Still think the story here is early if execution continues. The next leg higher probably depends on:

• Faster capacity deployment

• Large enterprise / hyperscaler wins

• Evidence operating leverage improves over time

• Continued scarcity in AI compute supply globally

AI infra remains one of the strongest themes in the market right now, and NBIS is starting to get taken more seriously as a scaled player in that stack.

3

653

May 11

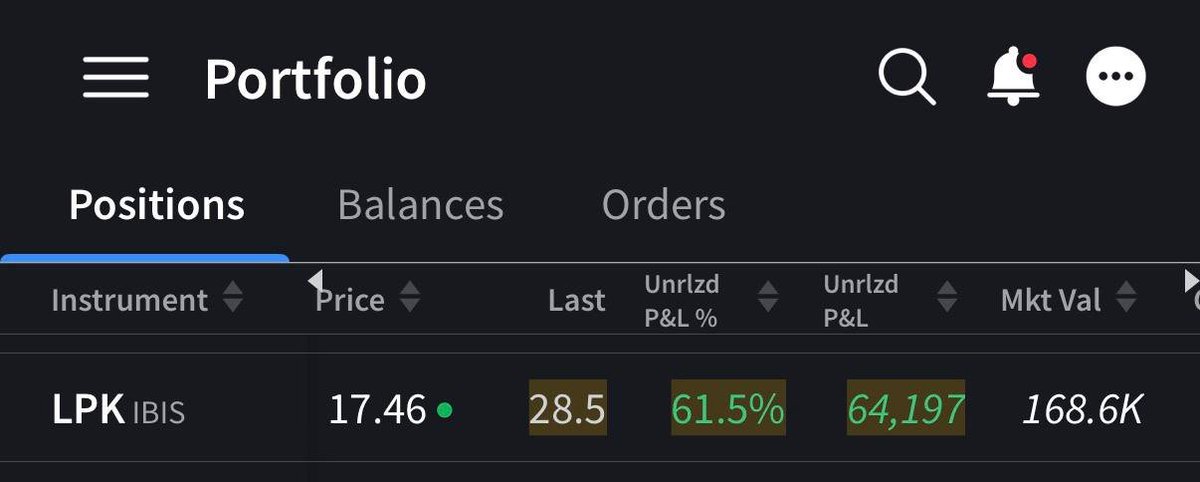

Started building my $LPK position around 17.46.

Now sitting at 28.5 and up roughly $64K on the position so far.

What keeps me bullish is that $LPK just confirmed discussions around initial production system orders tied to advanced packaging.

The speculation coming out of Germany points to a potential tier 1 US semiconductor customer.

$INTC continues to be the most heavily connected name here. Earlier patents referenced LIDE based glass via architectures for CPO, Korean industry reports linked LPKF and SCHOTT to Intel’s glass substrate efforts, and management previously mentioned years of exclusive paid CPO development work with a major US semiconductor partner.

$MSFT is another name that would make sense given their custom silicon ambitions and aggressive push into co packaged optics.

As AI networking scales toward 1.6T and beyond, glass substrates are increasingly viewed as one of the best solutions for signal integrity, thermals, and density.

And if glass wins, LPKF owns one of the critical manufacturing layers behind it.

1

1

5

3,271

May 11

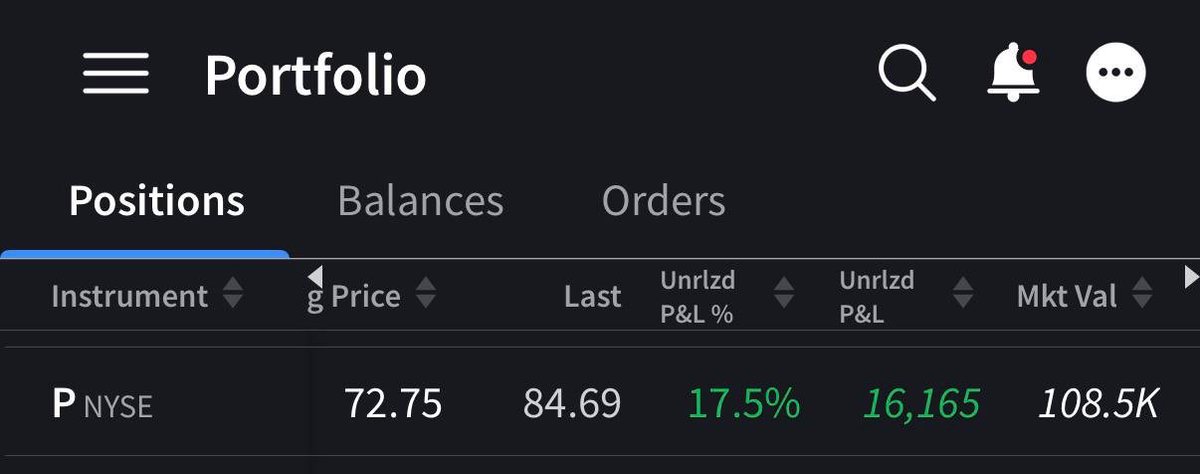

Entered Everpure at an average price of $72, now up 17.5% and crossed $100k.

My $P thesis is fairly simple.

As AI workloads continue scaling, the demand for faster, denser, and more power efficient storage infrastructure is growing rapidly. I think Pure Storage is one of the better positioned companies to benefit from that trend.

The company has been steadily taking share from older storage vendors by focusing entirely on all flash architecture instead of legacy hard drive systems. Their DirectFlash technology gives them advantages in density, efficiency, performance, and physical footprint, which becomes increasingly important for hyperscalers and AI data centers.

What also stands out is the financial profile. Revenue growth has been accelerating, earnings are growing much faster than revenue, gross margins remain strong around 70%, and the balance sheet carries significant net cash with no debt.

Compared to many AI infrastructure names, the market still does not fully price Pure Storage as a direct AI beneficiary.

Valuation is not necessarily cheap, so position sizing matters. But I think the long term setup remains attractive as AI infrastructure spending continues expanding.

$NTAP

$DELL

$HPE

$IBM

$WDC

$STX

$NTNX

$VRT

$SMCI

$ANET

1

5

2,108

May 11

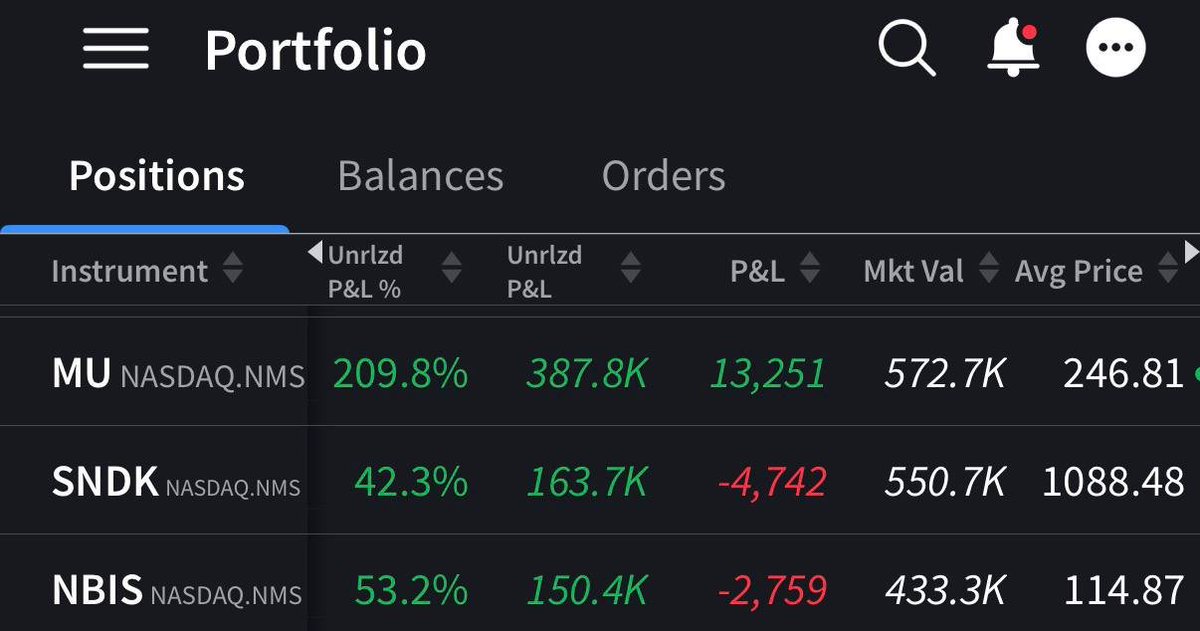

$MU could eventually become more profitable than both $AMZN and $META over the next few years.

That is how big this AI memory cycle could become.

Micron is already shipping the world’s first 245TB data center SSD, helping AI data centers fit far more storage into a much smaller space while using less power.

The company says these drives can reduce storage rack needs by more than 80% compared to traditional hard drives. That becomes increasingly important as AI workloads continue exploding.

What stands out to me is that $MU still trades at a much lower valuation compared to names like $NVDA, $TSMC, and $AAPL despite being one of the most important parts of the AI infrastructure stack.

That is why I remain bullish on $MU.

I continue to see it as one of the most overlooked AI infrastructure plays in the market today.

Most people still think memory is just another cyclical industry.

I do not think this cycle is the same.

$SAMSUNG, $SKHYNIX, $SNDK are all part of my holdings. Reprice is inevitable. We are just getting started.

1

363

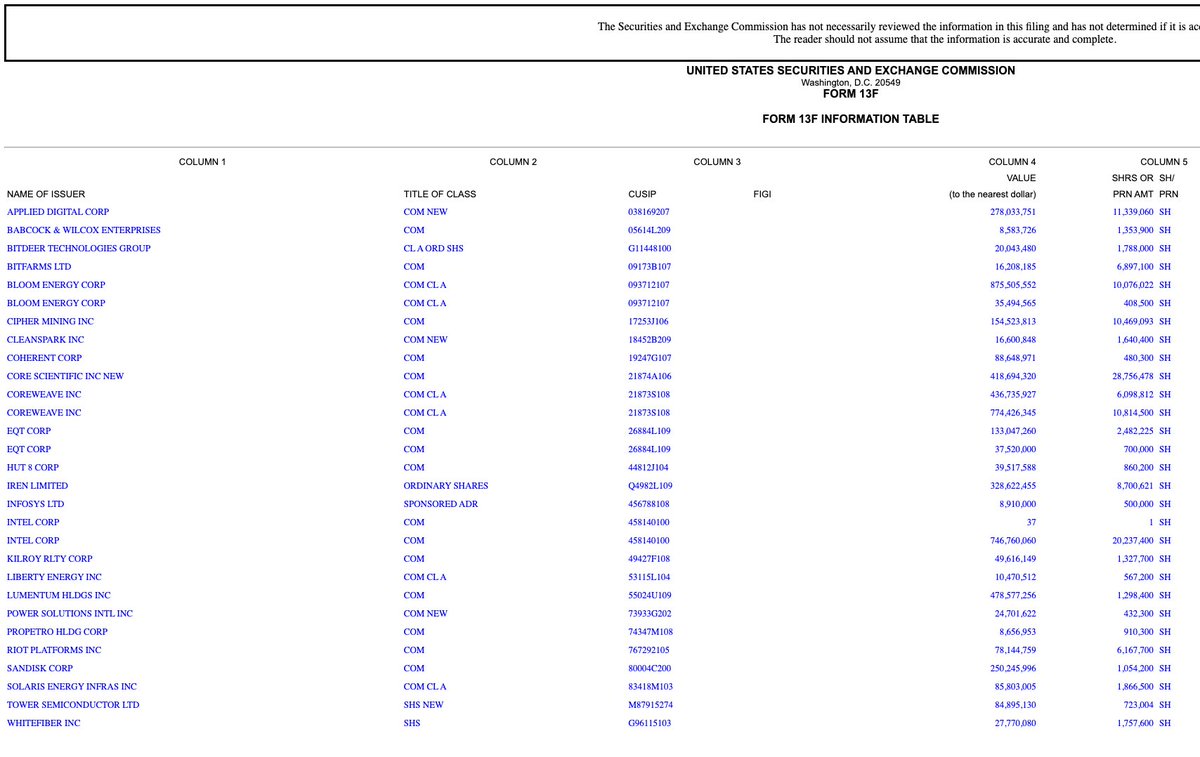

May 11

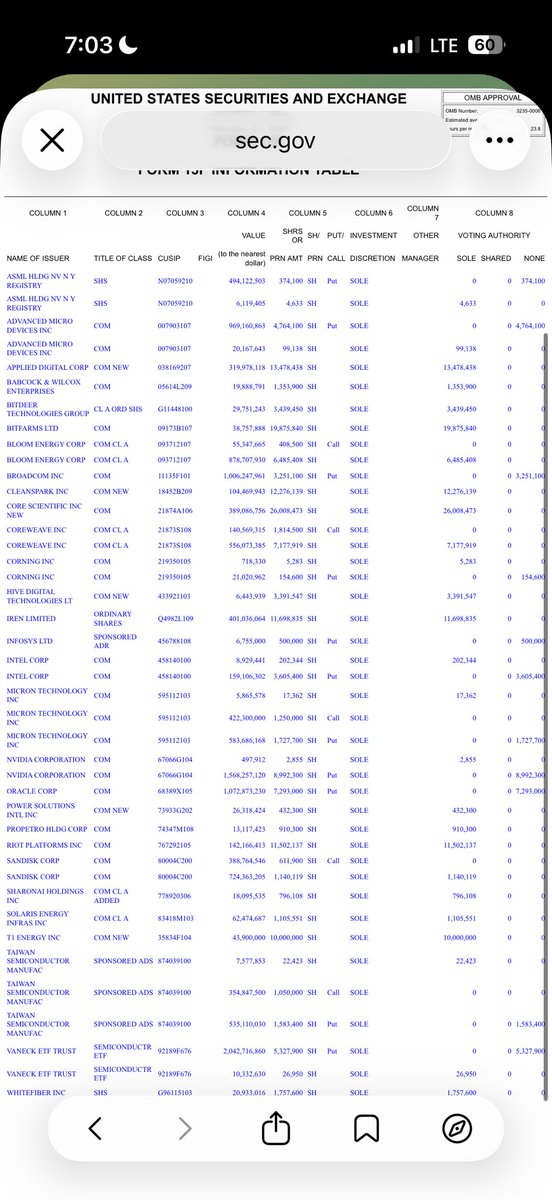

This is the current portfolio lineup from @leopoldasch's Situational Awareness Fund.

Their next 13F filing is due this week, likely anytime between now and May 15.

Watching closely to see which positions they increase planning to follow the strongest adds once the filing drops.

His $BE positions played out really well. Shall see what's his next big bet.

1

133

May 11

Big earnings week ahead across AI, semis, space, and power. I'm currently bullish on $HIMS, $NBIS, $TSEM

Names reporting include $NBIS, $ASTS, $PLUG, $HIMS, $CRCL, and $POET.

Quick watchlist:

Monday:

• $ASTS — focus on launch timelines, defense contracts, and carrier partnerships. Market wants confidence after recent execution setbacks.

• $HIMS — watching GLP-1 momentum, subscriber growth, margins, and FY guidance after strong institutional accumulation.

• $CRCL — stablecoin/payment expansion remains strong, but valuation already reflects a lot of optimism.

• $PLUG — liquidity, backlog conversion, margins, and path toward positive EBITDA remain the key debate.

Tuesday:

• ChipMOS — AI demand, utilization rates, and margin recovery are the main themes.

• $SATL — needs stronger revenue acceleration and clearer progress on defense backlog Merlin constellation roadmap.

• $CAMT — focus likely on AI inspection demand and order visibility following recent acquisition activity.

Wednesday:

• $NBIS — hyperscaler deployments and the Eigen AI acquisition have strengthened the neocloud story. Market will watch ARR growth, capacity expansion, and backlog conversion closely.

• $TSEM — looking for healthy fab utilization and AI-related demand commentary.

Thursday:

• $POET — after the $MRVL cancellation, investors need to see new customer wins, Malaysia ramp progress, and a clearer commercialization path. Execution credibility is now critical.

1

671

May 11

$INTC may end up being one of the biggest strategic leverage points of the next decade.

Every major player connected to its ecosystem seems positioned to benefit alongside it from $NVDA and $AAPL to #SoftBank, SpaceXAI, and now #SKHynix.

May 11

Just in: SK hynix is conducting R&D on 2.5D packaging technology with Intel. SK hynix is considering adopting EMIB from Intel.

$INTC

1

231

May 11

People underestimate how violent the multiple expansion can get once the narrative shifts from “hosting company” to “AI compute platform.”

Apr 30

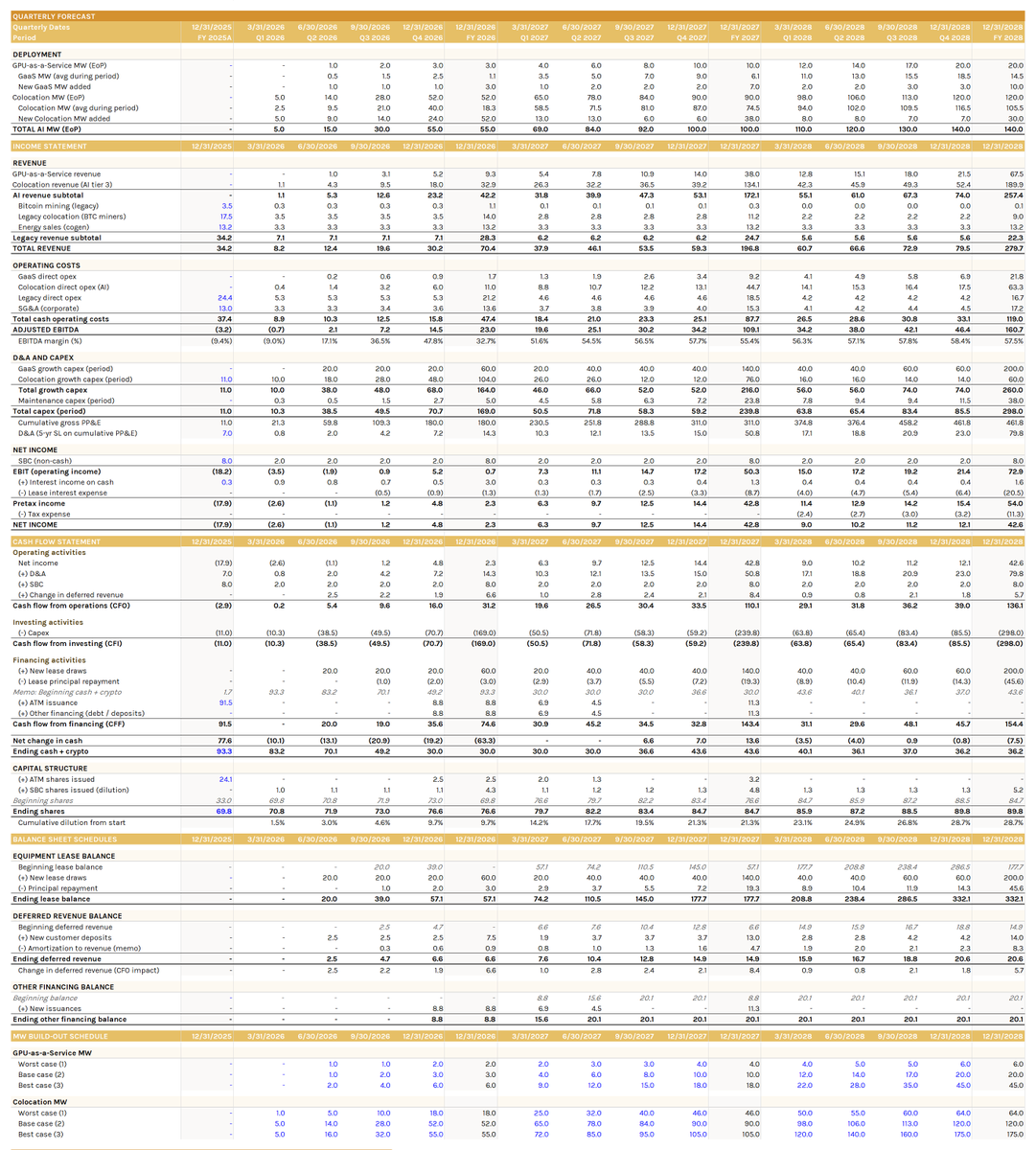

$DGXX is either going to $15 or back under $2, depending on whether they can actually scale beyond the first customer.

So I modeled it out quarter-by-quarter through FY 2028 across three scenarios (worst/base/best).

Here's the breakdown: 👇

1

77

May 11

$DGXX locked in a $1.1B agreement with $CBRS tied to 10% of its planned power capacity yet the company still sits at only a $500M market cap.

Key points:

- $1.1B contracted value, potentially scaling to $2.5B with extensions over a 10 year term

- 40MW deployment with Cerebras represents only ~10% of DGXX’s secured 400MW pipeline

- Initial phase expected online Dec 2026, full 40MW targeted by Q1 2027

Now compare valuation multiples across comparable AI infrastructure / colo transitions:

$NBIS — 10x forward sales

$IREN — 9x forward sales

$CRWV — 6x EV/Sales

$HUT — ~56x EV/EBITDA

$WULF — ~49x EV/EBITDA

Meanwhile:

$DGXX trades around ~2x projected FY28 revenue in the base scenario

Same thematic shift. Similar infrastructure narrative. Dramatically lower multiple.

Feels similar to where $IREN, $NBIS, and $CRWV traded before the market fully repriced the AI infrastructure pivot.

These kinds of valuation gaps rarely stay unnoticed forever.

8

2,218