Avantis and Alpha Architect fanboy. Some day it'll pay off. Some day...

Joined February 2021

- Tweets 660

- Following 151

- Followers 188

- Likes 57,054

54 Photos and videos

FactorDork retweeted

Apr 10

Our quarterly commentary for the Return Stacked® suite of ETFs is now available.

returnstackedetfs.com/quarte…

4

2

35

13,848

FactorDork retweeted

Apr 3

Look at the troughs on this chart:

* 2000–2002 (post-tech bust)

* 2008–2009 (financial crisis)

* 2011 (GFC second bottom)

* 2016 (global slowdown / China deceleration)

* 2020 shock

* Today

All were the tail ends of late-cycle slowdowns right before small, value and cyclicals ripped.

Apr 3

Copper is up over the last decade but trading at an almost four-decade relative low against hard money gold.

Chile's Escondida mine in the Atacama desert is the world's biggest copper mine. The world needs eight new Escondidas by 2030.

4

9

55

11,493

FactorDork retweeted

Feb 5

Chart shows cumulative performance (since ~2000)

* SPYG (S&P 500 Growth) on top

* SPYV (S&P 500 Value) below it

Rising line → Growth outperforming Value

Falling line → Value outperforming Growth

Over ~25 years, Value has slightly outperformed Growth in absolute cumulative return (≈495% vs ≈438%).

2023-2025 Growth countertrend now seems to be breaking down.

Value isn’t exciting, but it’s quietly doing what it always does: surviving cycles and compounding.

1

1

10

2,484

FactorDork retweeted

It’s a great day to be part of the SCV GANG 🗣️🔊

5

4

28

1,382

FactorDork retweeted

Our quarterly commentary for the Return Stacked® suite of ETFs is now available.

returnstackedetfs.com/quarte…

2

3

35

17,241

FactorDork retweeted

Hadn't seen anyone else post it yet today...

Great start to the year!

6

3

38

1,643

FactorDork retweeted

3 Oct 2025

"Mid caps."

8

1

23

8,801

FactorDork retweeted

20 Aug 2025

YieldMax has 26 ETFs with 1 year returns through 7/31/25 ($15.5B AUM).

Multiplying each ETF’s AUM by its trailing tax cost (reminder: driven by distributions, not returns) and you get a $4.6B run-rate tax bill.

Forget DOGE… YieldMax is single handedly balancing the deficit.

19 Aug 2025

A YieldMax fund ($ULTY) was featured in Morningstar today. Not mentioned was post-tax returns...

Since inception (2/28/24) annualized returns as of 7/31/25:

-Pre-tax: 8.98%

-Post-tax pre-liquidation: -24.59%

DO NOT OWN THESE IN TAXABLE ACCOUNTS

x.com/MorningstarInc/status/…

9

7

61

14,330

FactorDork retweeted

11 Jul 2025

Our quarterly commentary for the Return Stacked® suite of ETFs is now available.

returnstackedetfs.com/quarte…

5

5

24

29,748

FactorDork retweeted

30 Apr 2025

We now have two economically far left (and economically ignorant) parties, they just differ in their preferred pronouns.

29 Apr 2025

Batya Ungar-Sargon: “What we are seeing right now is the market reorienting itself around American prosperity.

As Americans, we owe something to the common good. And I think it is hard for an elite that has gotten used to getting rich off the backs of the working class to understand that.”

81

174

1,172

141,464

FactorDork retweeted

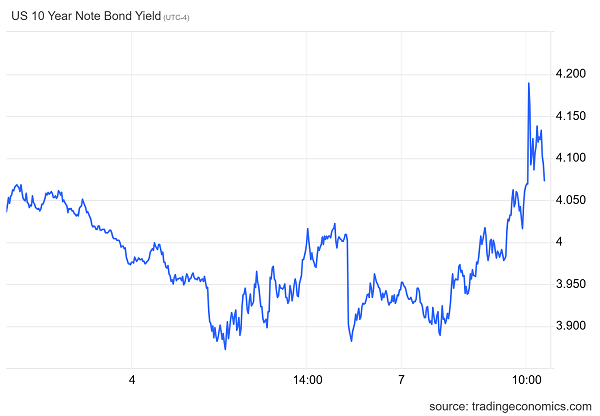

7 Apr 2025

The most notable thing in today's market isn't what's happening in stocks, it's that bond yields went up despite what's happening in stocks.

971

1,424

14,917

2,126,013

FactorDork retweeted

6 Apr 2025

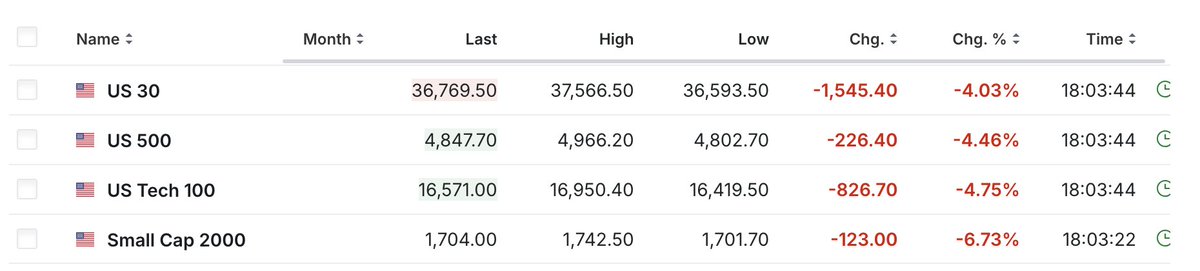

Front-running it is.

6 Apr 2025

In 45 minutes, we find out whether crypto is "catching down" to Friday's equity move, or front-running the equity open...

22

3

74

15,186

FactorDork retweeted

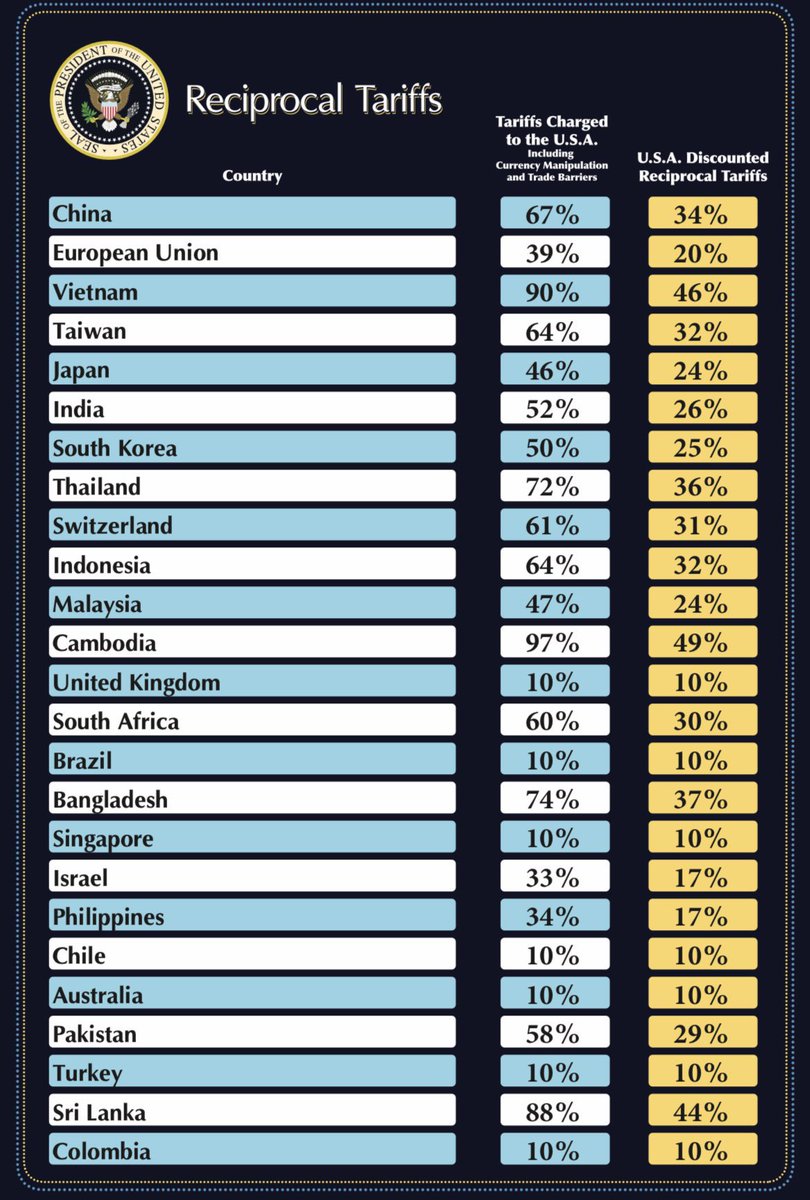

2 Apr 2025

Just figured out where these fake tariff rates come from. They didn't actually calculate tariff rates non-tariff barriers, as they say they did. Instead, for every country, they just took our trade deficit with that country and divided it by the country's exports to us.

So we have a $17.9 billion trade deficit with Indonesia. Its exports to us are $28 billion. $17.9/$28 = 64%, which Trump claims is the tariff rate Indonesia charges us. What extraordinary nonsense this is.

2 Apr 2025

It's also important to understand that the tariff rates that foreign countries are supposedly charging us are just made-up numbers. South Korea, with which we have a trade agreement, is not charging a 50% tariff on U.S. exports. Nor is the EU charging a 39% tariff.

2,346

21,000

91,959

19,768,596

FactorDork retweeted

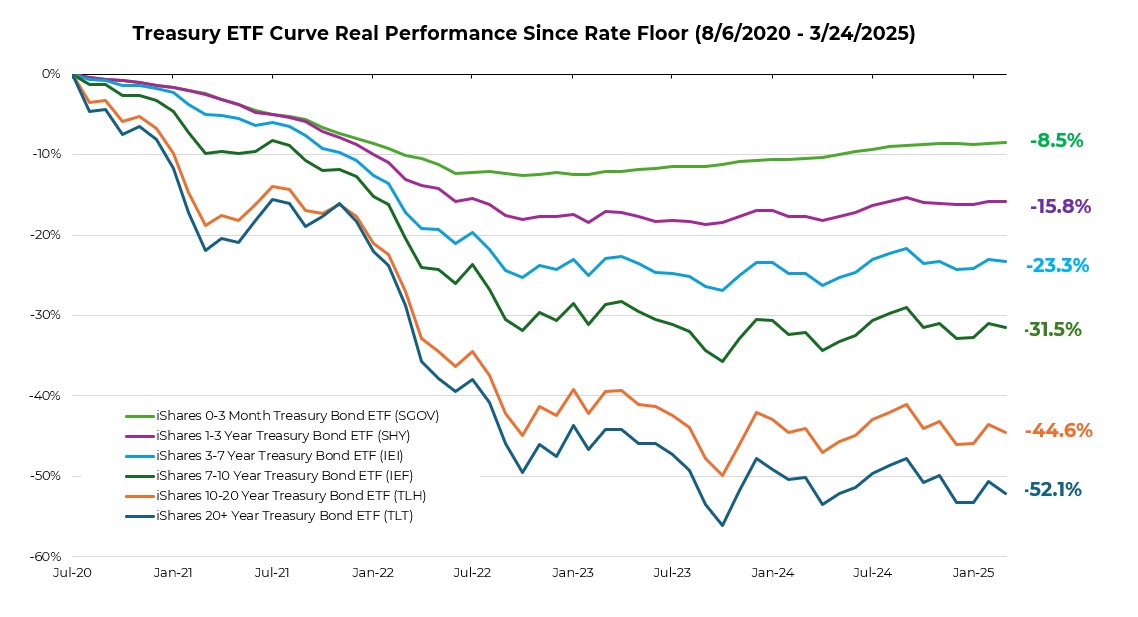

25 Mar 2025

Whoof whoof in real terms... an investor in TLT may NEVER break-even in real terms

2

2

15

11,857

FactorDork retweeted

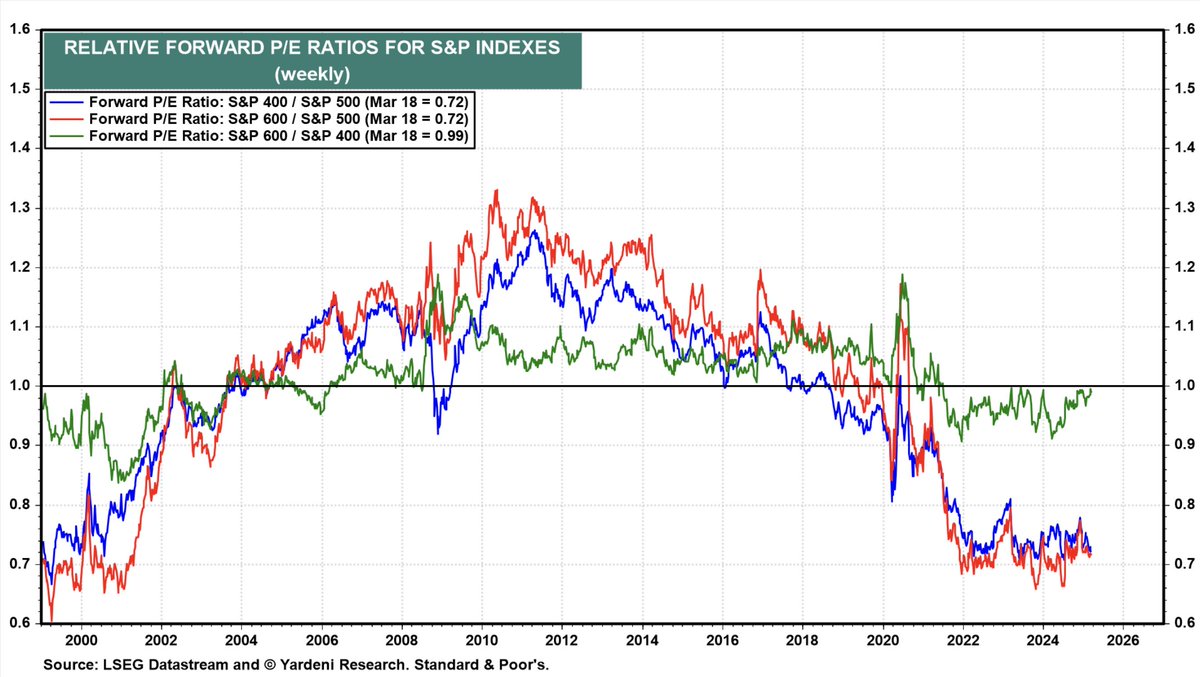

19 Mar 2025

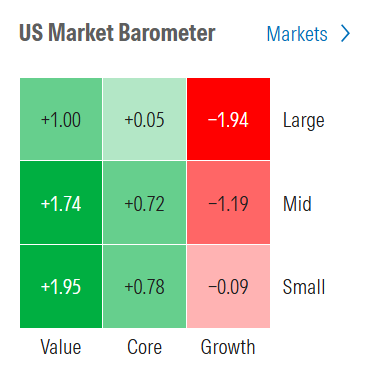

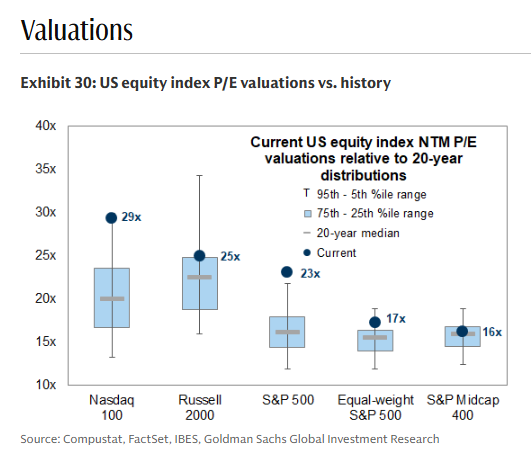

Relative forward PE ratios of small, mid and large caps.

Small and Mid are trading at a late 90s discount from Large.

9

23

96

24,778

FactorDork retweeted

11 Mar 2025

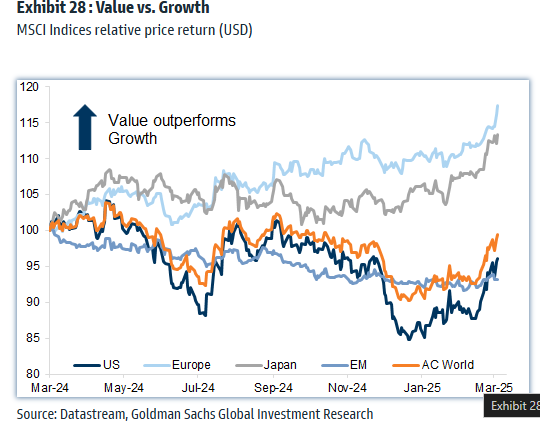

The global rally in value vs growth is something..

2

6

32

4,421

FactorDork retweeted

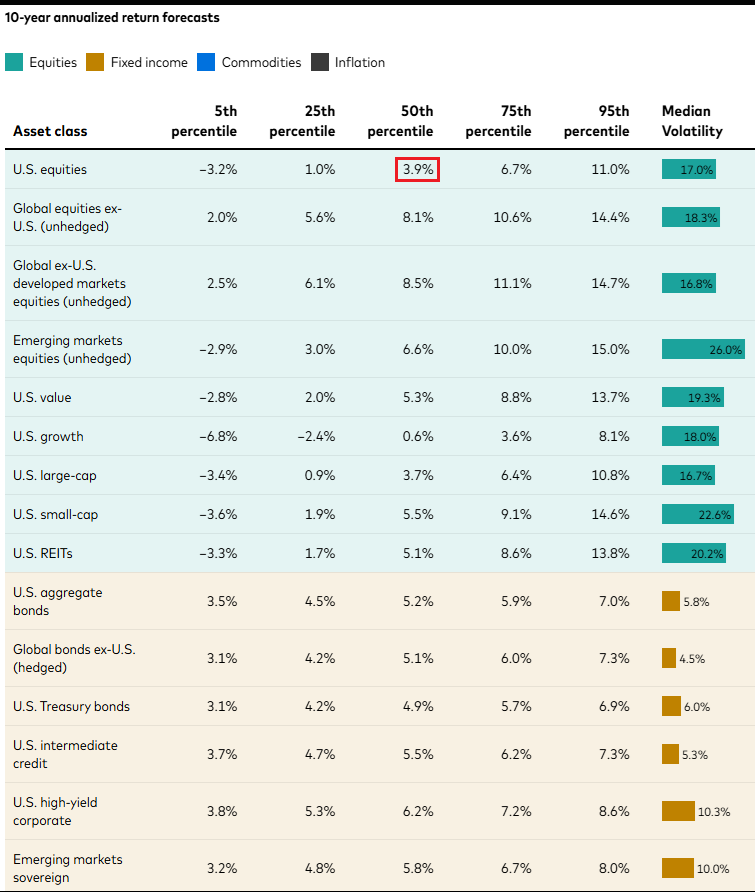

9 Mar 2025

Vanguard forecasts US stocks to return 3.9% annually over the next decade.

Large-cap growth: 0.6%

130

263

1,834

376,602

FactorDork retweeted

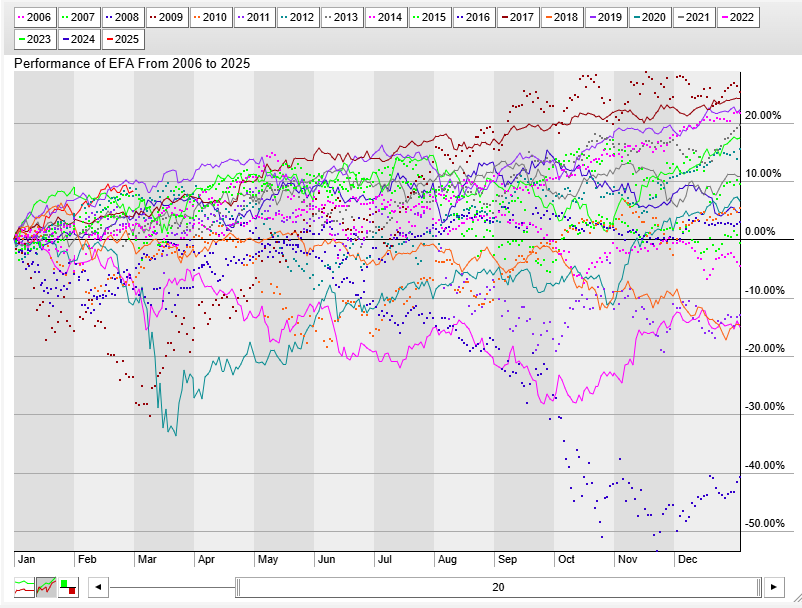

3 Mar 2025

$EFA tied for its best start to a year since its 2001 inception

(2019 was also 10% YTD through March 3)

12

1

6

2,586

FactorDork retweeted

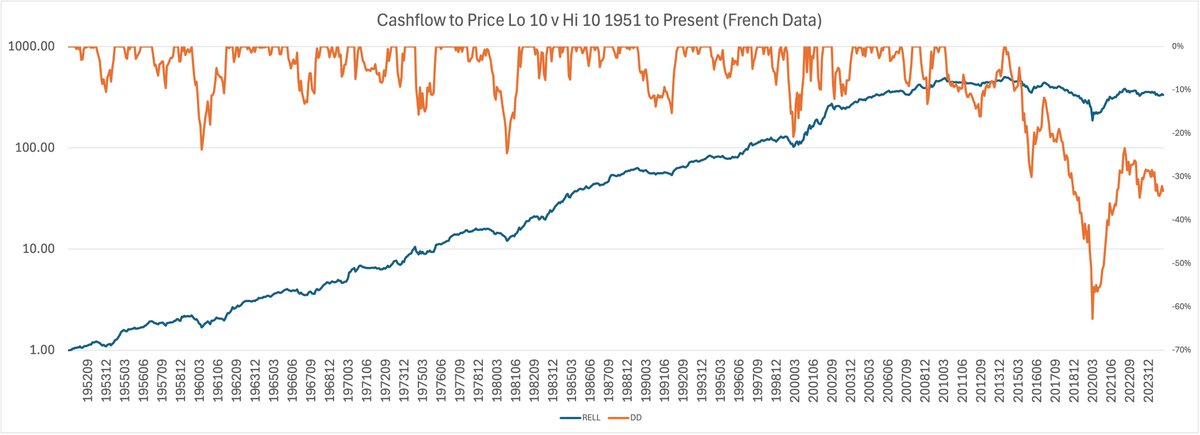

21 Feb 2025

Chart shows the cumulative returns to portfolios formed on cashflow-to-price.

Hi 10 Value vs Lo 10 Expensive 1951 to December 2024.

Value started underperforming July 2014, bottomed March 2020, recovered to May 2022 and has underperformed since.

Value outperformed expensive over the full set by 333x but has now underperformed for more than 10 years.

5

4

23

7,246

FactorDork retweeted

10 Feb 2025

The death of factor returns has been highly exaggerated. Anyone claiming this is probably making these mistakes...

1. Only looking to large-cap or mega-caps

This is by far the hardest place to find alpha. Everyone is competing in this space for an edge. All the common factors do not work consistently here. Value, momentum, sentiment...it works sometimes and in cycles.

2. Factors too diluted

ETFs typically hold way too many stocks for pure factor tilts. If it holds hundreds of stocks or the parent universe is too small, the factor will be like watered down beer. You can't just split the S&P 500 universe down the middle, which is too small to begin with, and call half of it value and the other half growth. So many things wrong with this approach.

3. Information decay

Factors have a half-life. They change over time. Different styles change at different rates. Value is fairly stable for a long time while momentum and investment factors change rapidly. If the optimal rebalance point is 3 months yet your fund only does so annually, you'll have little true factor exposure for 9 months of the year.

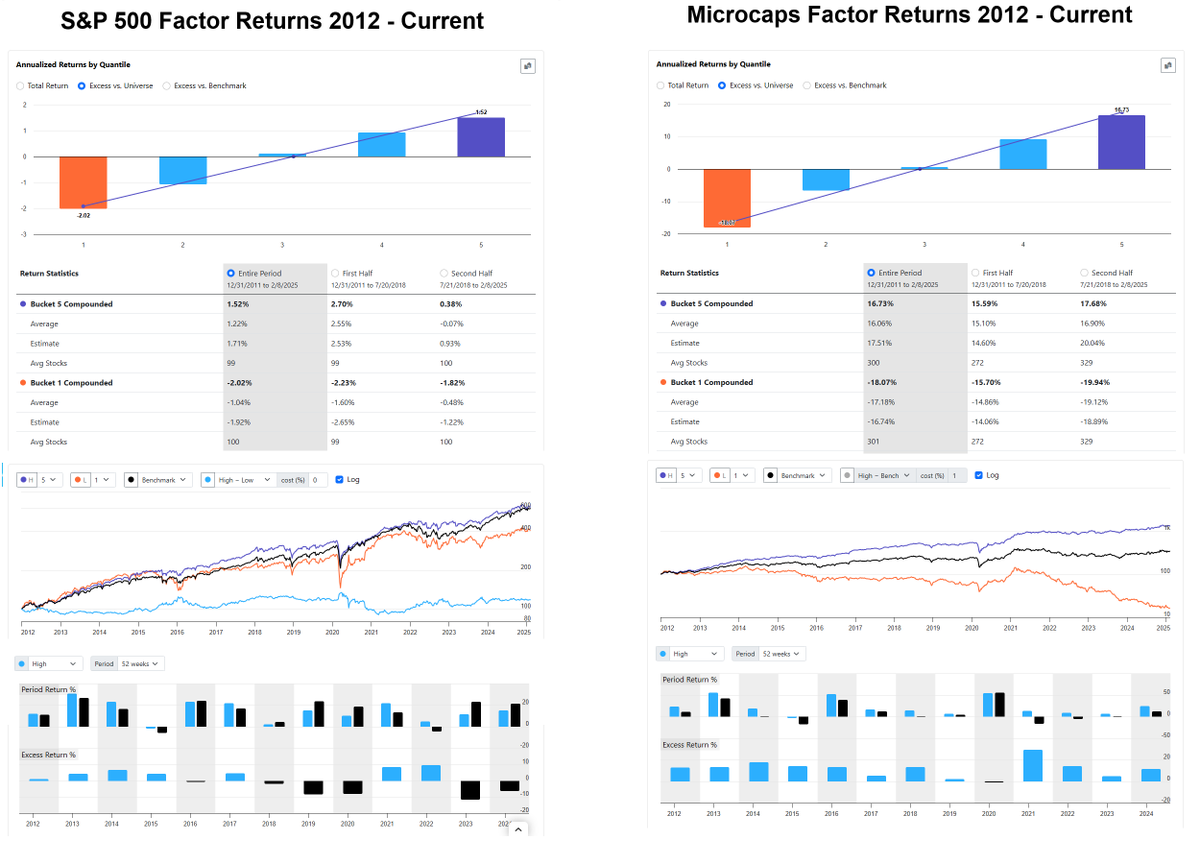

What I have found is that factor returns are by far the strongest in smallcap and microcap stocks. The reason (I think so anyway) is that your average investor is retail. He is not as well informed so having institutional grade data at your fingertips is an edge. Judging from the microcap retail investors I know, they go for the stocks which might 10x. Put another way, they bid up the price on very risky stocks throwing the risk-to-reward ratio out of whack.

Whatever the case, I find that factor investing works VERY strongly in smaller stocks. And institutions cannot go here. If they do, they have to hold for such long periods of time to keep turnover down that they really cannot harvest the factor premiums in a meaningful way.

Factor investing is not dead. Not by a long shot. But it is mostly abundant in stocks that many prefer not to trade. Or they don't have cheap access to a platform which can model it. Typically, institutional grade software and data isn't cheap. That's why I love Portfolio123 for personal portfolios.

The image below is showing a pre-defined multi-style factor ranking system which is available on Portfolio123 called Core Combination. It includes value, growth, quality, momentum, sentiment and low volatility. There is a 35% spread between high and low ranked stocks in microcaps (with liquidity filter) but only 2 - 3.5% spread in the S&P 500.

2

4

42

3,945