Joined July 2011

- Tweets 14,693

- Following 762

- Followers 12,093

- Likes 23,878

6,381 Photos and videos

Max Altschuler retweeted

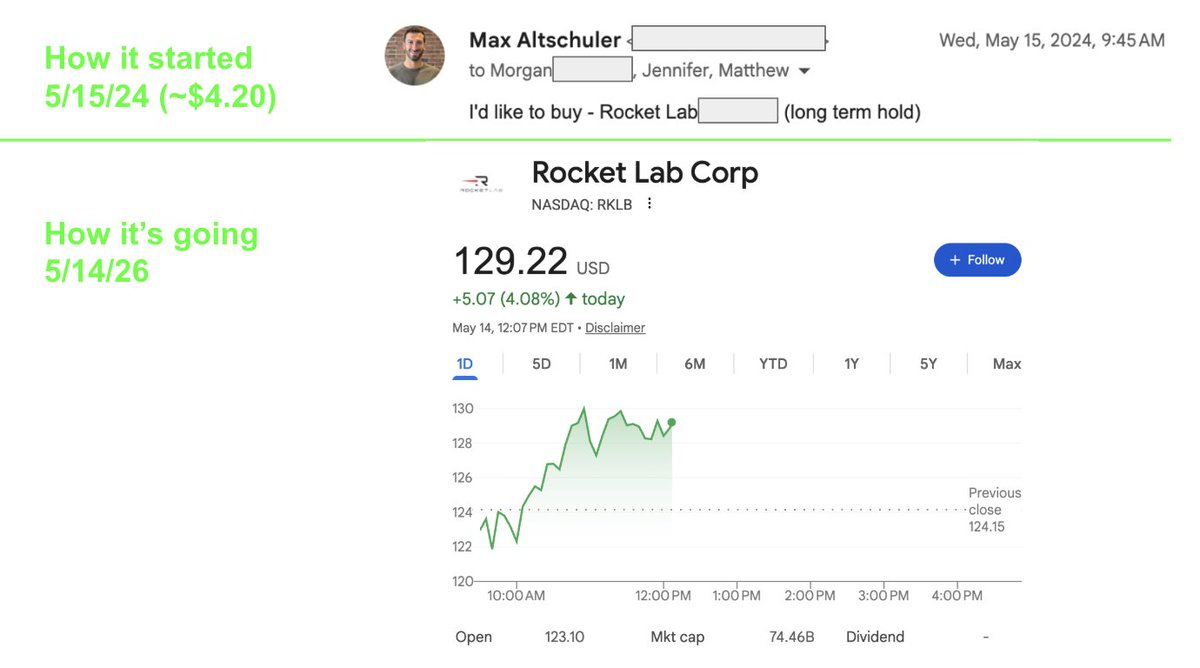

California’s next set of leaders should take notes from Greg Abbott on how not to chase off a golden goose that can fly to space, create wealth, and build local industrial capacity from scratch

Jun 13

Thanks, Elon.

And thanks to you too, Gavin.

10

9

214

24,838

The league tried their best to extend the series by not holding one of the future faces of the league accountable. 3 missed flagrant foul calls. In doing so, they made him unlikeable.

“We absolutely dominated for most of the series”

Victor Wembanyama after the Spurs lost 4-1 in the Finals

1

42

Max Altschuler retweeted

The best part of this video is the last 5 seconds. The host asks him about becoming a millionaire

"Do you feel like you've achieved the American dream?"

"Yeah, but that's no reason to stop."

Incredible. That's the actual American mindset. More American than half of America.

Jun 12

bro immigrated from Mexico and took a $28/hr contract welding job in 2015.

didn't even know what SpaceX was.

they gave him $10,000 in stock and let him buy more through payroll deductions.

that stake is now worth $880,000.

and he's one of 4,400 employees who became millionaires on Friday. welders. technicians. cafeteria staff.

43

220

3,267

85,973

Max Altschuler retweeted

14h

“Hernandez has roughly 6,500 SpaceX shares. On Friday, SpaceX stock closed at $160.95, valuing his holdings at $1,046,175.”

Capitalism is a miracle. God bless it. It is the only thing that has ever overcome the poverty default.

Before Juan Hernandez became a welder at SpaceX, he had never heard of the company.

But just over 10 years later, that leap of faith is paying off following the company's $75 billion initial public offering. cbsn.ws/445TrCm

2

1

60

5,504

Jun 11

Another new VC episode on @GTMnow is live! I sat down with @BenjLerer , Managing Partner and co-founder of @LererHippeau , one of New York's defining Seed funds.

Ben co-founded Thrillist, built it into Group Nine, and wrote some of the earliest angel checks into companies like Warby Parker and Casper before turning Lerer Hippeau into a nine-fund firm with roughly $1.5B in AUM. We get into how he runs his investment committee, why he wants to be the worst investor at his own fund, and how AI is changing the way they pick and back founders.

Before the conversation, @Paul Irving and I also talk through the modern IC process, conviction versus consensus, and the debate every fund is having right now between the young AI-native founder and the second-time operator with deep domain expertise.

A few takeaways from the conversation that are particularly worth noting:

1. Conviction beats consensus, every time.

Lerer Hippeau doesn't make decisions by groupthink. Someone has to pound the table and drag a deal across the line, and it doesn't have to be the person who sourced it. No scoring, you're either in or you're out. The best early-stage companies are usually non-consensus, so you need one person willing to stake their reputation on it.

2. Own your own deals. Don't hand them off.

Ben's biggest regrets came from passing deals to more junior people on the team, where the diligence turned confirmatory. The classic example is Peloton. He had the relationship, kicked it to a colleague, got a quick pass, and watched it walk. With his recent deal Magic, he did the opposite. He made the customer calls himself, called the founder's college classmate to understand her character, and won the deal with the lowest term sheet on the table.

3. Every dollar into a good company is a dollar stolen from a great one.

Ben's job is to find people who are a little crazy, not people who want to build good companies. If the best case for a company isn't a real multi-fund returner, he'd rather pass. That discipline is hardest to hold when a deal is durable, beloved, and obviously fundable.

4. The goal is to be the worst investor at your own fund.

As Ben says, if he's the rainmaking investor at 55, they screwed up. His actual job is to build a team better than him, give them capital and air cover, and get out of the way. He'll be 45 next year and the oldest person on the investment team, by design, because the most interesting founders keep getting younger.

5. AI is now a (non-voting) member of the investment team. They've fed years of fund data, portfolio context, and Ben's own thinking into a system that effectively sits in the room. It knows their check sizes, ownership targets, pacing, and portfolio ranking. When a company comes back for a follow-on, it can tell them where it ranks, how much reserve is mapped against it, and how that stacks against companies that just beat or missed plan. It doesn't get a real vote, but it makes them bolder and better educated in real time.

6. Half your deal flow should be unfair.

Ben splits their pipeline roughly in half. One side is proprietary: repeat founders, partner-level relationships, deals taken out of market early. The other side is competitive and in-market, where everyone sees the same companies and you win on speed, conviction, and being the partner of choice. His media background is part of the unfair half. Top founders give Lerer Hippeau access specifically because they want that media expertise.

7. The founder profile keeps splitting in two.

Ben sees a real bifurcation right now. There's the young, fast-moving, AI-native founder out of central casting, and there's the second or third-time operator with deep domain expertise and a clear right to win. He's not picking a side. He's building access to both and letting the company and the market decide which one fits.

—

Catch the full episode on YouTube or wherever you get your podcasts. Big thank you to our series partner, @AngelList, who have been instrumental in helping GTMfund scale since the early days.

5

389

Jun 11

Downside of the Knicks in the finals is I can’t sleep in London from 130-5am basically. What a game!

2

9

309

Max Altschuler retweeted

Jun 5

There has simply never been a better time to be an elite, AI-enabled Enterprise Sales rep in history.

2

6

839

Max Altschuler retweeted

Jun 4

Fifteen years ago, the most valuable companies in the world were worth $300b to $400b . Today, several are worth $4t to $5t . The distance between planting a seed of an idea and building something truly legendary has grown by more than 10x. There is no reason to think the trajectory will slow.

Meanwhile, the average human lifespan has barely moved. We have roughly the same number of moments, chapters, and pages as our predecessors did. To build something legendary, we now have to cover more than 10x the distance in that same fixed time, and in the next 15 years, we might have to cover an additional 10x the distance.

If the game has gotten harder, the question is not how to work more hours. The question is which moments, chapters, and books are worth writing at all. Every choice to work on one thing is a choice not to work on something else. The opportunity cost of our attention has never been higher.

13

23

293

45,971

Jun 3

We closed a competitive deal on the Friday of Thanksgiving week and the founder said we picked you to lead because you work founder hours. Always on.

Jun 2

I was once pitching in a board room at a top 3 VC firm for a $15M Series A.

12 people in the meeting. One of the GPs fully fell asleep. Out cold for 30 minutes. Nobody acknowledged it. Everyone just kept going.

I kept presenting my Series A slides to an unconscious man in a Herman Miller chair and somehow that was considered normal. That's venture capital.

You might fly across the country to perform for people who may or may not be conscious.

It's a dance.

And sometimes you lead and sometimes you follow and sometimes your partner is unconscious.

If you're raising right now, just know: every founder has a story like this. The process is weird. The power dynamic is weird. You're not crazy for thinking it's weird.

No one talks about it because they want to continue raising. But I'm happy to stick my neck out there.

It is weird.

4

2

22

6,189

Max Altschuler retweeted

Jun 2

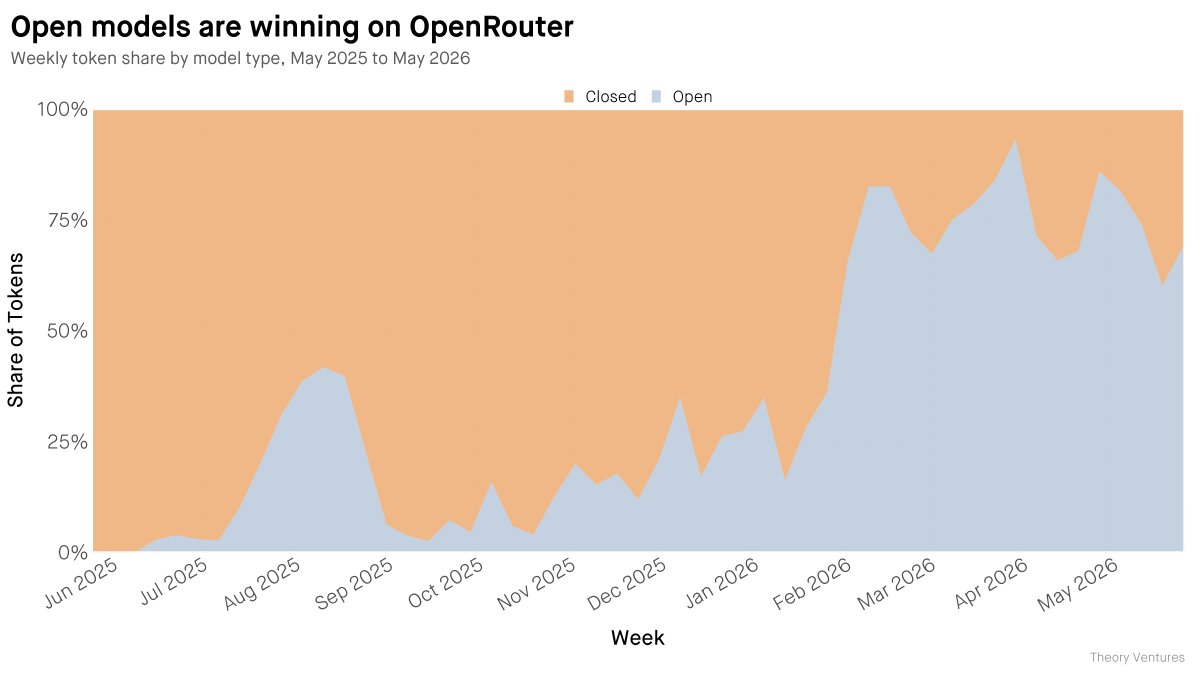

Open-weight models have overtaken closed models on OpenRouter.

69.1% of token volume now goes to open-weight models. 30.9% to closed.

Competition is a discovery procedure — and developers are discovering the value of open models.

🧵

14

36

156

31,672

Max Altschuler retweeted

Jun 1

All you had to do to make life changing wealth was to invest in ~every public company along the 237

148

274

5,488

500,607

Max Altschuler retweeted

May 30

Legal AI superempowers normal individuals with no legal background to fight big institutions in bureaucracies and in courts on a level knowledge/skill playing field, for the first time in human history. As such, it is one of the most inspiring applications of AI.

May 29

Legal AI is probably the least inspiring application of AI

change my mind

318

285

3,884

429,213

May 30

Heard he already got a seed round done

May 29

Shrey spelling 32 words in 90 seconds to win the Spelling Bee is the new greatest athletic accomplishment of 2026. I don’t even know how he said the letters that fast. Got a “Holy Mackerel” out of

@minakimes

6

1,019

If he were starting a data company today, this is what @ttunguz would build:

Images and video.

The reason behind this is in the math.

"An image is probably 1000X to 10000X bigger than a text file. And a video is two or three orders of magnitude larger than that."

Text is already straining the infrastructure we have.

Custom video is coming, robotics is coming. Both run on data volumes the current stack cannot move.

"We need much bigger infrastructure to be able to support it."

NEW: The AI data center buildout will be the fifth largest infrastructure project in history this year. Bigger than either world war.

The General Partner at @Theoryvc, Tomasz Tunguz (@ttunguz), joined GTMnow to break down the $575B infrastructure bet, the fusing of the data and AI stacks, and why there is now a second buyer in every enterprise deal.

For every $1 hyperscalers make from AI, they are spending $12 on infrastructure. Data centers hit 3.5% of US GDP this year and could reach 6 to 7% by 2030.

Highlights:

00:35 Why AI data centers are the 5th largest infrastructure project ever

01:26 "The demand for inference is infinite": the road to 2030

02:17 The $575B game of chicken: how the infrastructure bet plays out

03:48 Why the data stack and the AI stack have fully fused

05:33 What founders need to know about positioning now

06:37 Why product market fit is no longer binary

07:43 The new buying committee: marketing to humans and agents

12:03 AI agents that can influence and change your decisions

18:25 The underrated pattern behind successful founders

19:53 Tomasz's hot take: AI will rewrite org design entirely

3

9

2,190

May 30

“Maybe CNN if we’re feeling frisky”

374