Joined April 2009

- Tweets 35,352

- Following 345

- Followers 320

- Likes 19,814

2,603 Photos and videos

Not all wealth is created the same. While the scale IS extraordinary, the source matters far more. Musk isn’t running a hedge fund, engaged in high-frequency trading, or speculating in options where one person’s gain is literally another’s loss.

He built companies that employ hundreds of thousands of people, created transformative technologies, and delivered real value to society.

That is much closer to productive stewardship than parasitism.

There is no way to morally justify having a trillion dollars

9

I was very much afraid that @NickJFreitas would say, "China could dump our debt," but to his credit, he focused instead on telecommunications and grid vulnerabilities. Impressive.

However, I think he underestimates the inherent fragility and long-term unsustainability of China's export-driven model. Every nation has a finite debt capacity, and the more the Chinese double down on an inefficient and unproductive trade model, the faster those trade and subsequent capital flows will reverse.

While it is difficult, perhaps nearly impossible, to predict exactly when that happens, I suspect it will occur much sooner (and faster) than most people expect.

@MrWinMarshall and @NickJFreitas talk geopolitics and culture. Great interview, well worth the watch.

youtu.be/fip95-Sb3AY

4

I'd be careful with "because Americans want to own stocks." Equity valuations are heavily reliant on global asymmetries that are ultimatatly unsustainable.

Market has had a good run, but even if you ended up on the winning side of the K-shaped economy, that is a fragile position that will one day correct.

18h

The reason anyone gets insanely rich is almost always because of the stock market. It certainly how @elonmusk did.

And the reason they get rich from the stock market, is because 150m Americans decided they wanted to own shares of stocks directly, or through their retirement plans, or through other approaches as a way of building their net worth and trying to create a better life for themselves.

One Hundred Fifty Million Americans. About 60% of adults.

Effectively believing that @elonmusk and many billionaires could make them wealthier and help them achieve a better life.

If you want @elonmusk , and most billionaires to no longer be that rich, convince those 150m to sell their stocks, funds, ETFs whatever.

Of course you would wipe out the net-worth of most of those people, and everyone else’s savings, as the markets crashed and brought down the economy and created the worst depression we have ever seen.

Alternatively

There are ways to improve healthcare access and eventually make it available to all.

To start -

If you want @elonmusk and all billionaires to improve healthcare for everyone , ask them to stop doing business with the enormous healthcare conglomerates and to work directly with transparently priced care providers.

It’s the behemoth HC conglomerates that make HC so bad for so many. (Check my timeline for more detail)

Removing them would push the cost of healthcare down for everyone. Their corporate decisions impact our healthcare cost and availability.

Of course if they do that, not only would our HC costs go down , and the quality of care for their employees and the entire country go up

But

They would see their corporate cash flow increase dramatically and we would have more millionaires, billionaires and maybe even another trillionaire when that cash flow moved from the big health care conglomerates to their bottom line, so would the net worth of the 150 million American adults that own public stocks

Capitalism is better than socialism because 150m Americans can influence exactly what happens in this country.

7

"Global oil demand entering the crisis looks to have been weaker than anyone realised."

My very contrarian take on why oil prices are resisting a breakout over $100

Iran war is a smokescreen for a looming oil demand crunch telegraph.co.uk/business/202…

14

Jun 13

If you're a problem solver, money is a byproduct, just another tool in your kit. If you're not, no amount of money will ever make you one. Giving a trillion dollars to a non-problem solver is a waste of $1 trillion.

@elonmusk identified problems and executed real solutions.

If he had to start from scratch tomorrow, he'd end up with $1 trillion again. It wasn't lightning in a bottle, but an outcome driven entirely by the person.

Jun 12

I really don’t understand true greed. If I was worth $1 trillion, you’d have to physically stop me from solving as many of the world’s problems as possible.

Everyone would have a home, food on the table, proper healthcare, happiness.

I just don’t get it.

1

9

Mind The Gap ☘️⛈️ retweeted

Jun 12

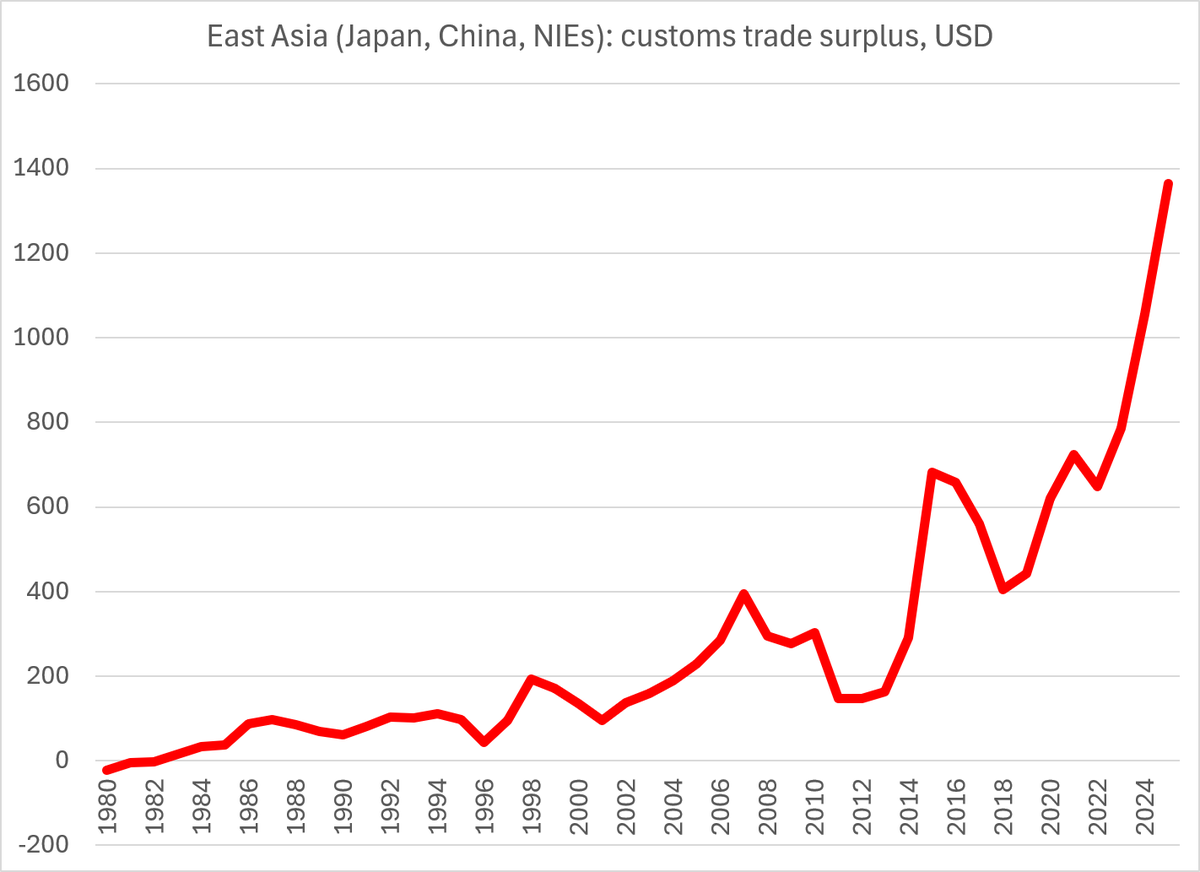

But the claim that imbalances are only now "starting to look excessive" runs salt on a still open wound --

The surge in Asia's surplus didn't start in 2025 ... the IMF just missed it for several years (unfortunately)

2/

2

2

19

2,067

Jun 13

No, you wouldn't. Neither would I.

It's a silly setup about something that doesn't exist. Nobody "denies science." People question hypotheses, challenge evidence, dispute interpretations, and debate conclusions.

Skepticism isn't the opposite of science. It's the foundation of it.

Jun 12

If I were ever abducted by Aliens, the first thing I’d ask is whether they came from a planet where people also deny science.

9

Mind The Gap ☘️⛈️ retweeted

Jun 12

Indeed. A Foreign Affairs article is an essay not an academic article.

I do want to encourage a bit of action rather than watch China grow for another 2 years via net exports while the world waits for a change in its growth model!

Jun 12

The article is really a policy mobilization argument dressed in analytical clothing. @Brad_Setser isn't primarily writing for economists — he's writing to shame #G7 finance ministers into action before #Évian chart @ForeignAffairs foreignaffairs.com/china/rea…

8

11

62

17,472

Jun 13

Left, right, or center, if you're not talking about trade, you're not addressing the problem. You're just arguing ideology.

Trade balances, capital flows, and the distribution of production determine where income, jobs, and wealth end up. Any explanation that ignores those factors is describing symptoms, not causes.

Jun 12

But taxing wealth so normal people can afford to see a doctor and not go bankrupt over inhalers is radical left. OK

1

15

Jun 13

Your article touches on something important, but it understates the macroeconomic implications of the asset-ownership divide.

Regards to @michaelxpettis who has done the most to explain how wealth concentration and trade imbalances are two sides of the same coin.

Hopefully, I don't screw it up.

Pettis's central argument, developed in "Trade Wars Are Class Wars" and elsewhere, is that the K-shaped economy isn't just a distributional story; it's a *macroeconomic* one.

1. The savings channel: Why wealth concentration suppresses demand👈

Often overlooked is the rich save a much larger share of their income than the poor and middle class.

As income and wealth become increasingly concentrated, the national savings rate rises "mechanically" not because people are virtuously preparing for retirement, but because a larger share of national income is going to people who don't need to spend it.

The result is a structural demand gap: production consistently outruns consumption.

As Pettis puts it, "the rich save more of their money than do the poor, and households consume a greater share of their income than do businesses or the state".

When too much income flows to high-savers, aggregate demand falls short of what the economy can produce.

2. The external absorption mechanism: How the US became the buyer of last resort👈

This is where the Pettis framework becomes essential.

Excess savings from surplus countries (China, Germany, Japan, South Korea) don't just sit idle; they flow into US financial markets, propping up the dollar and inflating asset prices.

"surplus countries subsidize their manufacturing industries but pass on the costs of these subsidies to deficit countries".

The United States, with its deep and open capital markets, absorbs nearly half of the world's excess savings.

But it comes with a cost, that capital inflow forces the US to run trade deficits by the iron logic of the balance of payments identity.

"Since the US private sector is not wanting for additional financing... this surplus capital flows right back out through the trade channel, in the form of greater imports into the US".

The result is a perfect, destructive loop:

foreign savings inflate US asset prices →

asset owners get richer →

the US runs trade deficits →

manufacturing hollows out →

the households that didn't own assets face stagnant wages and rising costs.

3. The "febezzle" illusion: Why asset wealth isn't real wealth👈

Charlie Munger's concept of "febezzle" or why rising asset prices are so deceptive.

"rising stock or real estate prices can generate income and wealth effects whether or not these rising prices reflect real increases in the earning capacity of these assets".

In other words, financial markets create temporary impressions of false wealth (very similar to Ponzi schemes) without any need for an embezzler.

This is crucial for understanding the "feeling broke" paradox.

Those millionaires who feel poor aren't just suffering from "relative deprivation" or scoreboard envy. In a very real sense, their wealth *is* illusory; as it depends on a continued flow of foreign savings into US assets, sustained by policies abroad that suppress consumption.

If (more like when) that flow reverses, the "wealth" evaporates, consumption collapses, and the economy enters a self-reinforcing downturn.

As Pettis warned in 2021: "If we do see any sharp correction in US stock and property markets, the risk is that this sets off much slower consumption growth (the main driver of economic growth), will cause total growth to drop in a self-reinforcing loop.

4. The "upward mobility" narrative misses the fragility👈

Your point about dual-income households and credential inflation is exactly right, and Pettis would add that much of what looks like "climbing the ladder" is actually a treadmill. When household income growth depends on both adults working longer hours, or on ever-higher educational credentials whose costs have outpaced inflation, the fragility beneath the surface becomes apparent.

The deeper issue is structural. The current global trading system incentivizes surplus countries to suppress household consumption and subsidize manufacturing, forcing deficit countries like the US to absorb the excess through debt and asset bubbles.

This isn't a story about lazy Americans living beyond their means. It's a story about policy choices in both surplus and deficit countries that have systematically transferred income from labor to capital, from households to corporations, and from workers to financial asset holders.

The K-shape as a global imbalance👈

Your article treats the K-shaped economy as a domestic phenomenon; asset owners vs. non-owners within the US.

But it is a global phenomenon sustained by a dysfunctional international system. The asset-ownership divide in the US is the mirror image of suppressed consumption in China and Germany.

You cannot fix one of those without addressing the other.

So what you dismisses as "feeling broke" sentiment as a scoreboard problem, it misses the point.

People feel broke not because they're comparing themselves to billionaires, but because the economy is genuinely fragile.

It depends on ever-rising asset prices, ever-growing household (and public) debt, and ever-larger capital inflows from countries that have chosen to subsidize production over consumption.

That's not a scoreboard problem. That's a structural flaw.

As the Trades Union Congress report summarizing Pettis's work puts it: "The global financial crisis and subsequent conditions have been wrongly judged as the public living beyond the means of the economy; instead the economy has operated beyond the means of the public" .

The K-shaped economy isn't a sign of success with a psychology problem. It's a sign of an economic model reaching its limits.

---

*Source note: The citations above draw from Michael Pettis's work as referenced in the search results, including his columns in the Financial Times and Bloomberg, his co-authored work with Erica Hogan at the Carnegie Endowment, and the book *Trade Wars Are Class Wars* co-authored with Matthew C. Klein.*

Jun 12

The Truth About The K-Shaped Economy

While most of the media headlines have grabbed onto the "K-Shaped" economy to frame arguments for economic disparity, the reality is that the middle class shrunk because they moved up the wealth matrix.

open.substack.com/pub/lancer…

3

120

Jun 12

The "Soviet cleanup" justification doesn't explain sustained, broad funding decades later. It's been nearly 40 years. If we haven't cleaned up and secured those sites by now, we never will.

The idea that we can anticipate future variants by creating them in a laboratory is, at best, speculative. A virus's ability to mutate is influenced by the length and structure of its RNA genome, but ultimately you're still guessing. Even if you happen to predict a future variant correctly, any resulting vaccine is likely to have limited effectiveness because these viruses evolve so rapidly.

The risks associated with laboratory leaks outweigh the potential benefits of trying to predict future variants. And if this research is mission-critical, it should be conducted in the United States, where oversight, accountability, and control of the facilities are far stronger.

Jun 12

Today, I’m releasing never before seen intelligence revealing new evidence of past US government funding for more than 120 biolabs in over 30 countries, including Ukraine.

In support of President Trump‘s Executive Order to end federal funding of dangerous gain of function research around the world, and increase transparency and accountability, ODNI will continue working with partners across the Administration to identify where these labs are, what pathogens they contain, and what “research” is being conducted.

odni.gov/index.php/newsroom/…

20

Jun 12

That's one way to give them the finger on the way out the door. 💯

Jun 12

Today, I’m releasing never before seen intelligence revealing new evidence of past US government funding for more than 120 biolabs in over 30 countries, including Ukraine.

In support of President Trump‘s Executive Order to end federal funding of dangerous gain of function research around the world, and increase transparency and accountability, ODNI will continue working with partners across the Administration to identify where these labs are, what pathogens they contain, and what “research” is being conducted.

odni.gov/index.php/newsroom/…

4

Jun 12

It's counterintuitive that Asian economies are hiking rates into an energy shock, but they are doing so to prevent the dollar system from hitting its limits.

The issue is not high oil prices. It's that sharp increases in oil prices create dollar shortages in a system dependent on continuously rolling over and refinancing dollar liabilities.

The risk is the volatility, not the price level.

Jun 12

Four of Asia's central banks are hitting the panic button at the same time. India. Indonesia. South Korea. Japan.

They are calling it a currency crisis. It is really a dollar shortage.

Almost everything that matters trades in dollars. Oil. Food. Materials. The debt everyone borrowed.

When a local currency falls, all of it gets more expensive. That starts a loop. A weaker currency drives more dollar demand. More demand weakens the currency further.

Japan drew a line at 160 yen. It sold $76 billion defending it. The yen is back below 160 anyway.

India has burned through more than $110 billion in forex tools. Its banks now pay non-residents 7.1% on five-year deposits. A five-year US Treasury pays about 4.3%. They are paying up just to pull dollars in.

Indonesia hiked rates to 5.5% in an emergency off-calendar meeting. Its reserves are falling at the longest streak since 2018.

South Korea inspected its foreign exchange banks for the first time in 14 years. Its stock market fell 8% Monday, rose 8% Tuesday, fell 5% Wednesday.

That is not policy management. That is desperation.

The problem is not interest rate differentials. It is the dollar itself. There are not enough dollars to go around. And energy keeps raising the need.

Selling reserves and hiking rates can slow a currency for a day. It cannot create new dollars.

This does not stay in Asia. The region sits at the center of global trade and finance.

When the dollar gets this tight, the stress does not stop at the border. It travels.

12

Jun 12

Bravo Zulu on the $1T

27

Jun 12

“It was not the post-1985 rise of the yen that caused Japan’s lost decade. Tokyo had waited so long before the inevitable currency adjustment that policymakers were then forced to choose between a sharp slowdown and a disastrous policy response. They chose the latter.” — @michaelxpettis

Japan's 'lost decades' were baked in because of suppressed consumption /export-led growth. By delaying rebalancing, policymakers made the eventual adjustment far more painful.

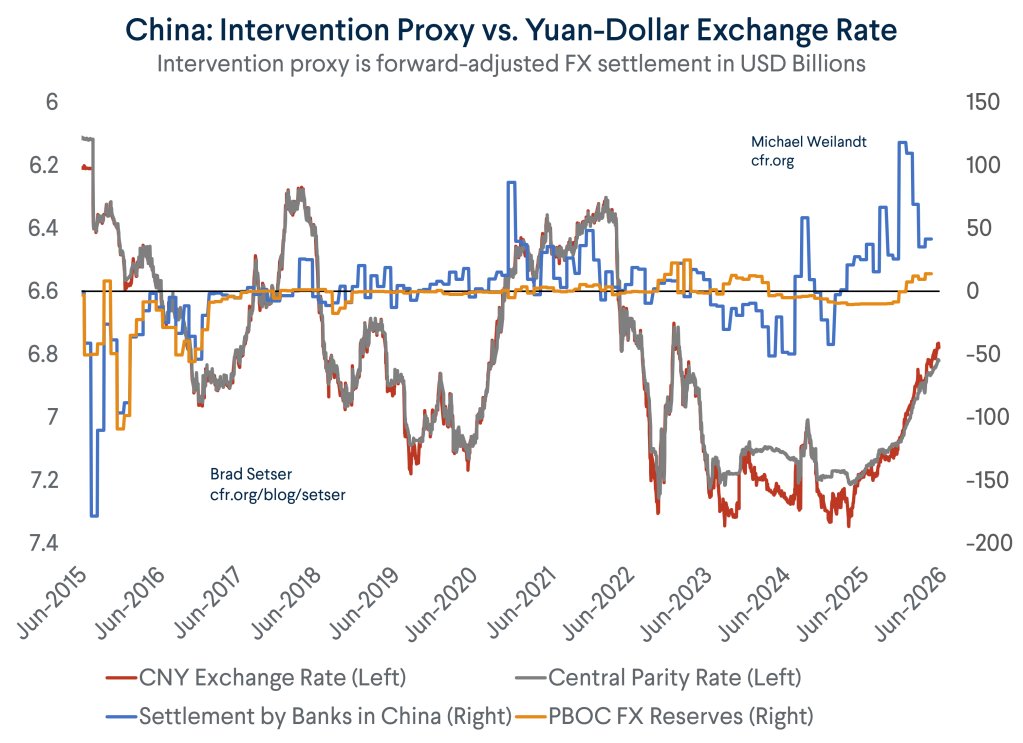

China is repeating the same pattern today. With a record roughly $1.2 trillion trade surplus in 2025 and still massive surpluses in 2026 (May alone was about $105 billion), state banks continue buying foreign currency to limit RMB appreciation (USD/CNY around 6.76).

This is not "resisting weakness"; it is actively capping strength to sustain the export and overcapacity model.

I would only add that if what China is doing were efficient, why doesn't the rest of the world do the same? What would happen to the global economy if every advanced economy adopted this export-led, surplus-dependent growth model?

If it were efficient and sustainable, we would not be seeing the parabolic rise in Chinese debt required to support it.

(and before you say, "but all the advanced economies debts are rising...". Yes, they are because they are accomidating China's over production and inefficent growth model.)

Jun 12

Two words: dead wrong. Which is unsurprising coming from Setser.

The main reason he is wrong is this: the RMB's weakness is actually market-driven, and China has mostly been resisting it, not engineering it. Since 2021 everything points towards a weaker RMB: the property bust, the Fed with rates at 5% for most of that period while there were very low rates in China, etc.

As such when Setser demands China "allow its currency to appreciate," it's essentially gaslighting. Had China been floating the RMB - the logical endpoint of "stop manipulating" - it would almost certainly be weaker than today, not stronger.

There is also another huge point the article conveniently avoids mentioning: trade balances are made by savings and investment, not exchange rates. When you have a country that spends much more than it should (i.e. the US with its 6% budget deficit) meeting a country that saves too much (China with high national savings), then it's no wonder there's a trade deficit between the two. The exchange rate is downstream of this, not the cause.

Finally, the Plaza analogy actually destroys his own recommendation. The yen roughly doubled against the dollar after 1985, yet Japan's trade surplus persisted. If a 100% appreciation couldn't erase Japan's surplus, a 15% RMB move won't erase China's 🤷♂️

Plus there is the pretty relevant fact that the Plaza accord led to Japan's lost decades, meaning Setser's remedy has been tried and it wrecked the patient without curing the disease.

32

Jun 12

He's right. Accounting identities such as (S-I) can tell you what is impossible, but they do not explain mechanisms or causation.

China has never allowed a market-priced RMB. The entities absorbing external imbalances are central authorities and state-owned banks, not private market participants. That tells us far more than accounting identities ever will.

Currency management by the CCP and the state remains manipulation regardless of the direction of the intervention.

With a roughly $1.2 trillion trade surplus and state banks actively purchasing foreign exchange to limit RMB appreciation, the policy objective is clear: preserve export competitiveness regardless of efficiency.

China is not Japan in the ways that matter here. There is unlikely to be a clean resolution through negotiations.

Nor is the CCP's currency management a solution to China's deflation and weak domestic demand. It represents a doubling down on the same model of overcapacity and suppressed household consumption that created the problem in the first place.

Jun 12

As for the argument that current account imbalances are determined by savings and investment and exchange rates don't matter, well it is dangerous to reason purely from accounting identities ...

5/

21

Mind The Gap ☘️⛈️ retweeted

Jun 12

Amazing how perceptions of China's yuan are sometimes stuck in 2024. Now that the yuan is inching up against the dollar, China (via the PBOC/ state banks) has been buying fx to limit its appreciation. That is literally what the settlement data shows

1/

Jun 12

Two words: dead wrong. Which is unsurprising coming from Setser.

The main reason he is wrong is this: the RMB's weakness is actually market-driven, and China has mostly been resisting it, not engineering it. Since 2021 everything points towards a weaker RMB: the property bust, the Fed with rates at 5% for most of that period while there were very low rates in China, etc.

As such when Setser demands China "allow its currency to appreciate," it's essentially gaslighting. Had China been floating the RMB - the logical endpoint of "stop manipulating" - it would almost certainly be weaker than today, not stronger.

There is also another huge point the article conveniently avoids mentioning: trade balances are made by savings and investment, not exchange rates. When you have a country that spends much more than it should (i.e. the US with its 6% budget deficit) meeting a country that saves too much (China with high national savings), then it's no wonder there's a trade deficit between the two. The exchange rate is downstream of this, not the cause.

Finally, the Plaza analogy actually destroys his own recommendation. The yen roughly doubled against the dollar after 1985, yet Japan's trade surplus persisted. If a 100% appreciation couldn't erase Japan's surplus, a 15% RMB move won't erase China's 🤷♂️

Plus there is the pretty relevant fact that the Plaza accord led to Japan's lost decades, meaning Setser's remedy has been tried and it wrecked the patient without curing the disease.

5

16

71

20,981