Chiefs | Finance | Tech | Data

Joined June 2013

- Tweets 22,147

- Following 526

- Followers 707

- Likes 270,967

1,305 Photos and videos

Pinned Tweet

16 Apr 2024

🧵 After first learning about modern portfolio theory and construction, I settled on the typical Boglehead Three-Fund Portfolio: Total US Stock, Total International Stock, Aggregate US Bonds. Adjust stock/bond ratio to match risk.

Here are my "improvements" so far:

4

2

39

11,834

Levi 🧢 retweeted

Apr 26

let the doctor cook

Apr 25

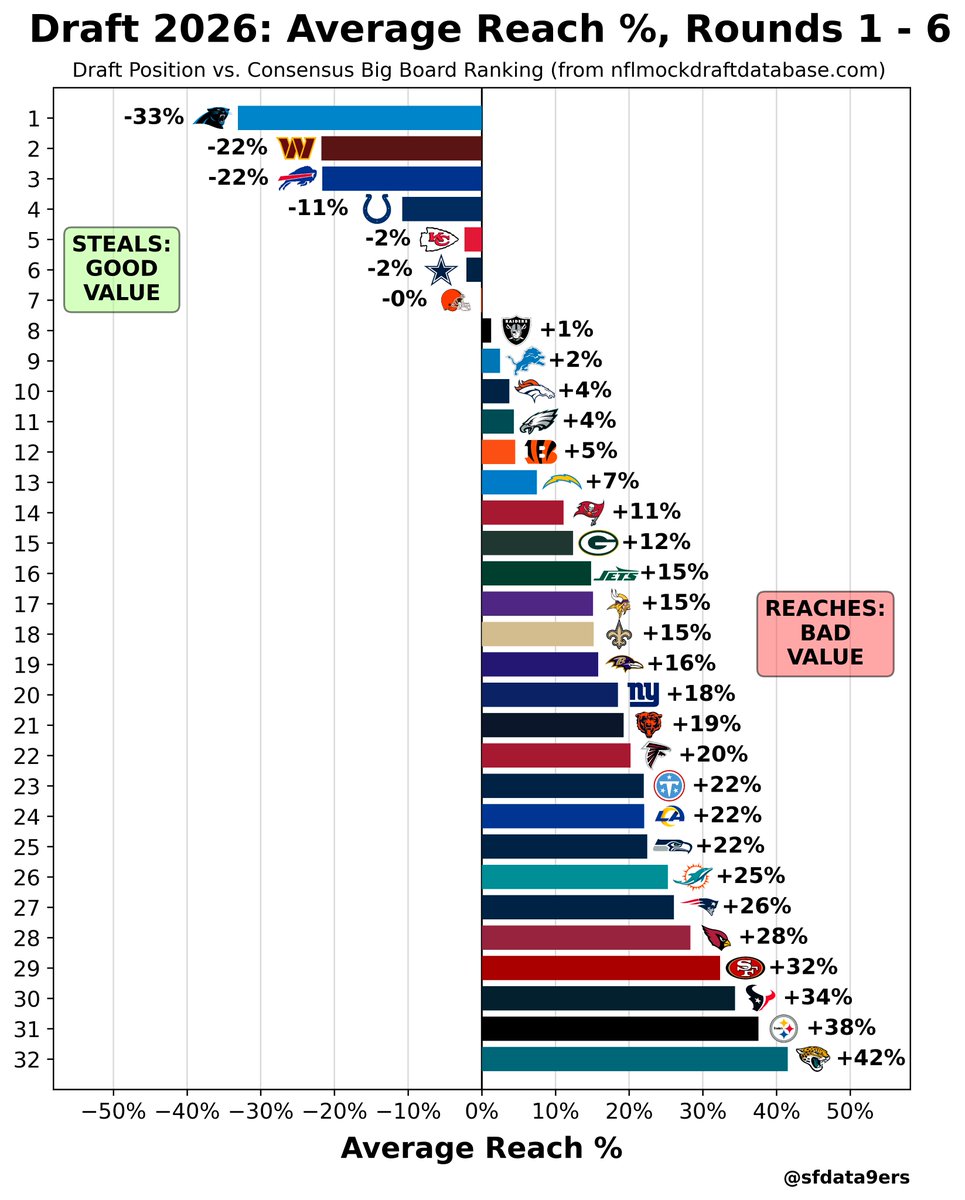

Best value vs. biggest reaches (Rounds 1–6)

1. CAR -33%

2. WAS -22%

3. BUF -22%

...

29. SF 32%

30. HOU 34%

31. PIT 38%

32. JAX 42%

11

16

303

80,226

Levi 🧢 retweeted

Apr 24

Seahawks with a Clyde Edwards-Helaire memorial pick to wrap up Night 1

31

118

5,722

224,999

Levi 🧢 retweeted

Apr 24

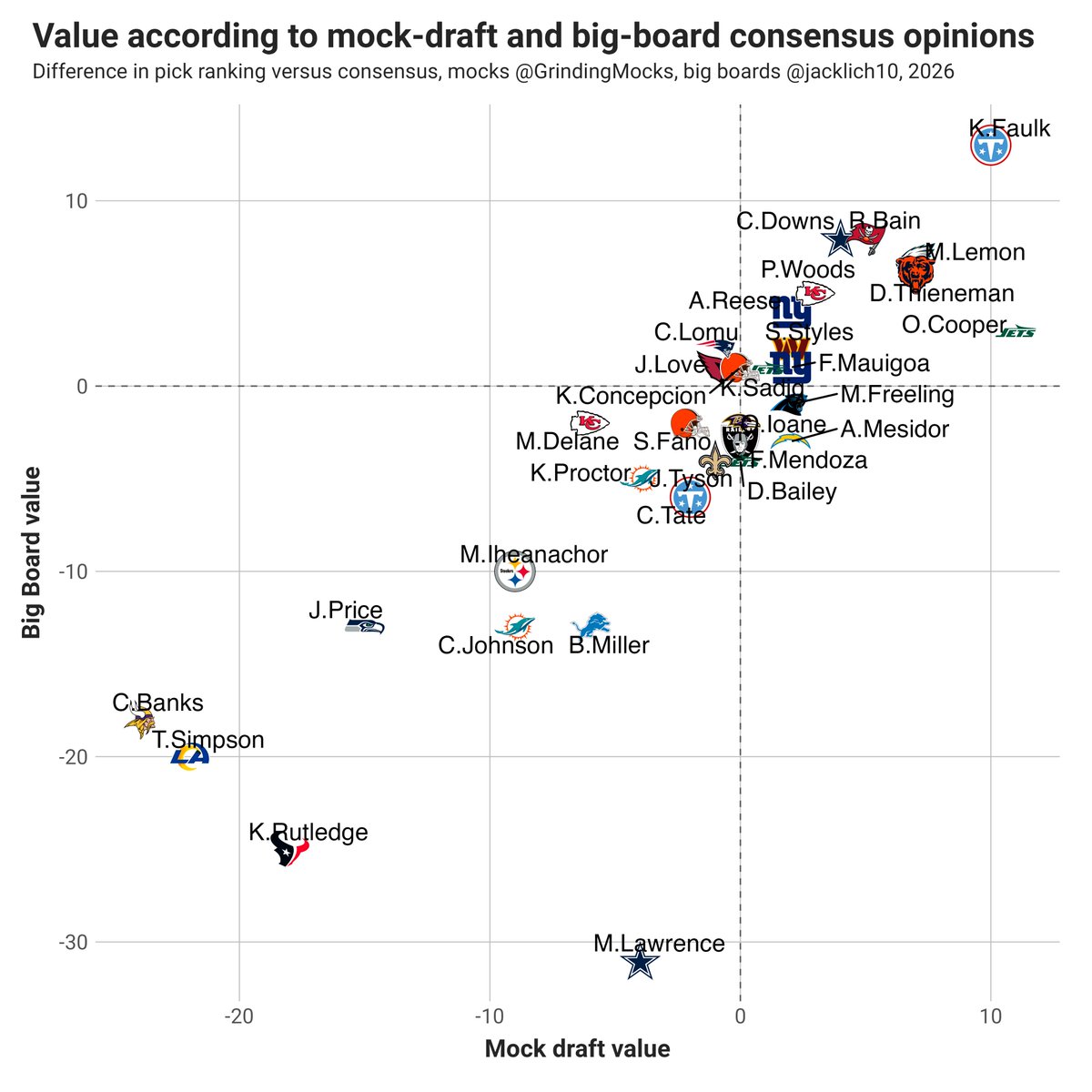

Biggest "reach" in the first round according to the consensus big board: Malachi Lawrence

By consensus mock drafts: Caleb Banks

Biggest "steal" by both metrics: Keldric Faulk

16

122

1,148

211,300

Levi 🧢 retweeted

Apr 24

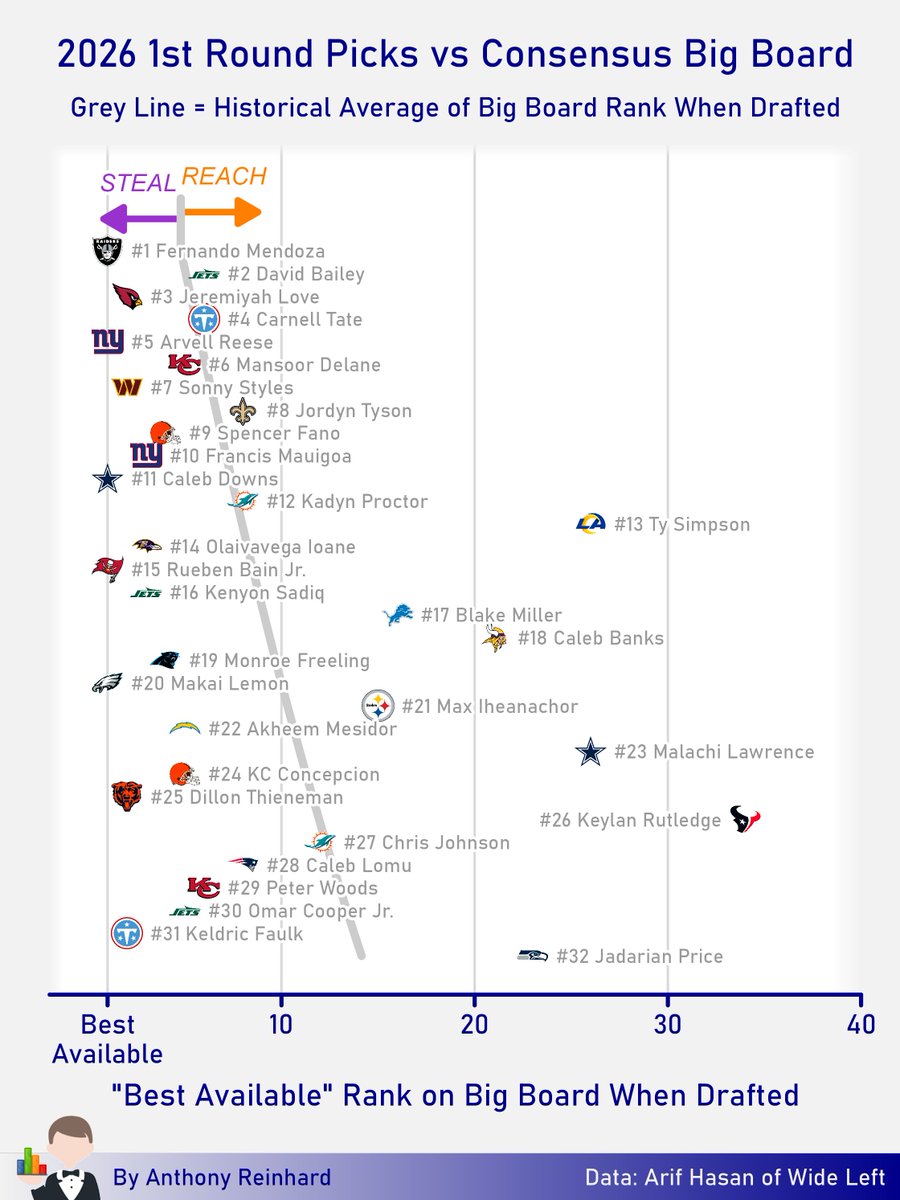

Here is where each of tonight's 1st round picks sat on @ArifHasanNFL's consensus big board at the time they were drafted. The grey line indicates the average "best available" rank from previous drafts.

18

75

663

139,277

Levi 🧢 retweeted

Apr 24

I wonder which one is his agent

235

1,735

92,051

4,248,779

Levi 🧢 retweeted

Apr 24

At the time of pick No. 6, there was a 90% chance Mansoor Delane would make it to pick No. 9, per the Draft Day Predictor.

Even if that number is a little high, that's the hidden cost of trade-ups: there's a substantial chance the Chiefs gave up a 3 and a 5 for nothing!

38

52

403

63,357

Levi 🧢 retweeted

Apr 23

This will make a fine addition to my collection

Apr 22

British Cabinet Ministers Losing Confidence in PM Keir Starmer: "It's Bleak" as Coup Talks Heat Up — iPaper

112

3,154

45,467

1,213,582

Levi 🧢 retweeted

Apr 23

Made an impact both on the field and off of it. Can't wait to see your name in our Ring of Honor, DJ 🫡

17

217

1,685

83,549

Apr 23

Was looking out at a pond a couple minutes then heard a guy yelling behind me. I didn't think anything until hearing a growl...a pit bull literally wearing a "service animal" vest charged me.

Thankfully didn't have to bring out my knife but was assured "he is usually nice" 🙃

1

1

1

96

Apr 23

I really should report it. If I see them again, it definitely will be.

1

38

Levi 🧢 retweeted

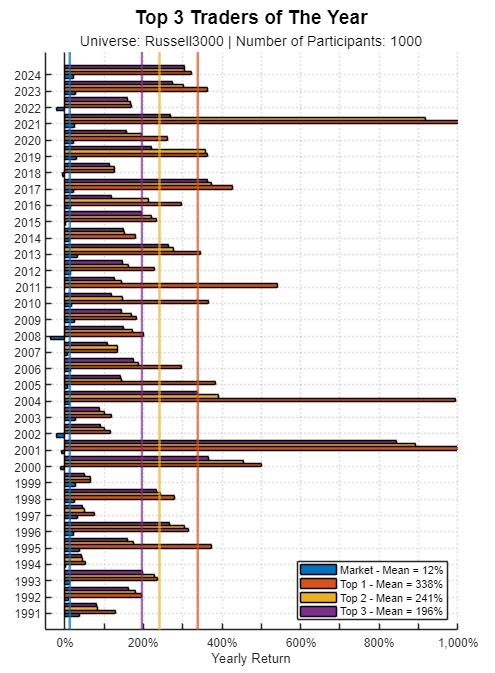

Many legendary traders are celebrated as “Market Wizards.”

But how can we tell whether an extraordinary track record truly reflects skill, or whether it could simply emerge from randomness?

To explore this question, imagine a large group of investors trading the market over many years.

Suppose none of them has any particular skill. They invest in stocks largely driven by intuition or gut feeling.

Even in such a world, probability tells us something remarkable: when enough participants are involved, a small number will inevitably end up with spectacular performance.

This observation becomes even more relevant in environments where many traders compete and are evaluated over relatively short periods of time, sometimes just a single year.

In our study, we simulate exactly this situation.

Thousands of investors start with identical conditions and trade over time with no informational advantage.

We then analyze the distribution of outcomes and focus on the traders who end up at the very top of the performance ranking.

What we find raises an important question about how we interpret exceptional track records in financial markets.

The full analysis and results of the experiment are available here.

(link in the comments)

3

7

35

8,048

Levi 🧢 retweeted

Mar 5

Q—What supplement should you take for heart health?

A—None

washingtonpost.com/wellness/…

"The American Heart Association concluded that there is not enough evidence to support the use of any supplements to prevent cardiovascular disease."

“There are no adequate data that support cardiovascular benefit for supplements in healthy people who eat a healthy diet" (—me)

41

74

257

30,029

"I need to park $50k of cash for 12 months. What are my options?"’

HIghest yields of saving products with a guarantee yield for one year:

52wk T-bill = 3.55%

12mo non-callable brokered CD = 3.80% at Vanguard & Schwab

12mo online bank CD = 4.10% at E*TRADE from Morgan Stanley

12mo online credit union CD = 4.25% at ValorFI Heroes (most states)

12mo credit union CD = 4.33% at Municipal CU (NYC)

To maintain full liquidity AND a rate lock:

13mo No Penalty CD = 3.95% at Marcus by Goldman Sachs

"I need to park $50k of cash for 12 months. What are my options?"

> $VUSXX (Vanguard Treasury MM Fund) or any Treasury equivalent. State/local tax exempt, 3.63% yield

> HYSA (FDIC insured, ~3%)

Don’t invest it, unless 12 months turns into 12 years..

1

12

1,179

Levi 🧢 retweeted

(NEWS/@ClementeLisi) Here’s what you need to know about Sunni and Shi’a Islam — and how it impacts Iran and the current situation there.

1

1

2

221

Levi 🧢 retweeted

Mar 3

Let’s Pray It’s Not What It Sounds Like: This Crime Report Keeps Referring To A Victim As John ‘The Rock’ Doe clickhole.com/lets-pray-its-…

67

758

23,647

Levi 🧢 retweeted

22 Jun 2025

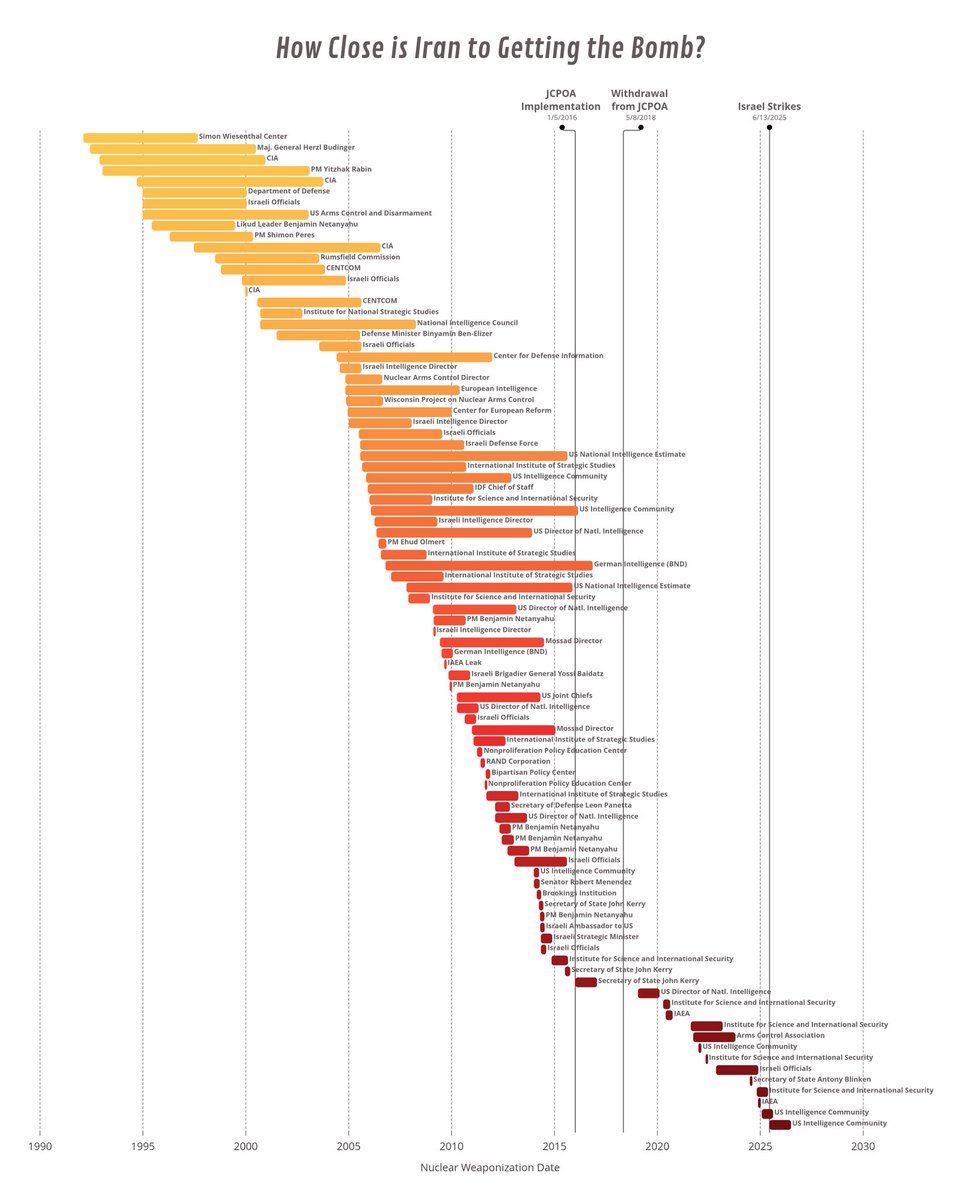

Iran has always seemingly been right around the corner, months away from nuclearizing for over 35 years

22 Jun 2025

Just published at Wide Left: an exploration of our dual domestic and international crises through the lens of someone who is exhausted.

History Fatigue

“Just once, I’d like to live in precedented times”

wideleft.football/p/history-…

5

37

349

51,939

Imagine if a nasal spray could make you immune not only to the viruses that cause COVID-19 and influenza, but to all respiratory diseases

go.nature.com/4rNOZ5B

89

328

1,416

63,288

Levi 🧢 retweeted

Resharing my piece from a few years ago about why I don't use RAS scores, even though they are broadly a pretty good proxy for athleticism wideleft.football/p/15-pro-d…

4

3

37

14,958

Levi 🧢 retweeted

Feb 27

Warren Buffett: "If I want to speak [about politics] as a private citizen, I should resign from Berkshire [first]."

19

51

890

66,020

Levi 🧢 retweeted

Feb 27

I remember.

Feb 26

Remember when this guy came out of nowhere in 2019 and said AI is coming & UBI will be the solution.

Pre-COVID feels like another lifetime.

218

213

3,407

197,840