Luke Johnson: investor and entrepreneur

Joined October 2009

- Tweets 28,633

- Following 1,707

- Followers 42,678

- Likes 30

151 Photos and videos

Public spending priorities in this country are insane.

Buckinghamshire council spent £819 million over a five year contract period on taxis. £163 million a year on average.

This is insane. The council could run an equivalent transport service for a fraction of this cost

1

5

24

1,404

Luke Johnson retweeted

Under these proposals at 17 you’ll be able to vote, join the army and drive a car but not allowed to watch premier league highlights on YouTube on a Saturday night. What an absurd idea.

NEW: Starmer will announce an ‘Australia plus’ teen social media ban on breakfast TV tomorrow

- Expected to include the same 10 apps as Aus: TikTok, YouTube, X, Instagram among them

- ‘Romantic’ chatbots banned

- 16 17 yr olds will have a curfew

thetimes.com/article/631af41…

67

583

4,808

186,046

Luke Johnson retweeted

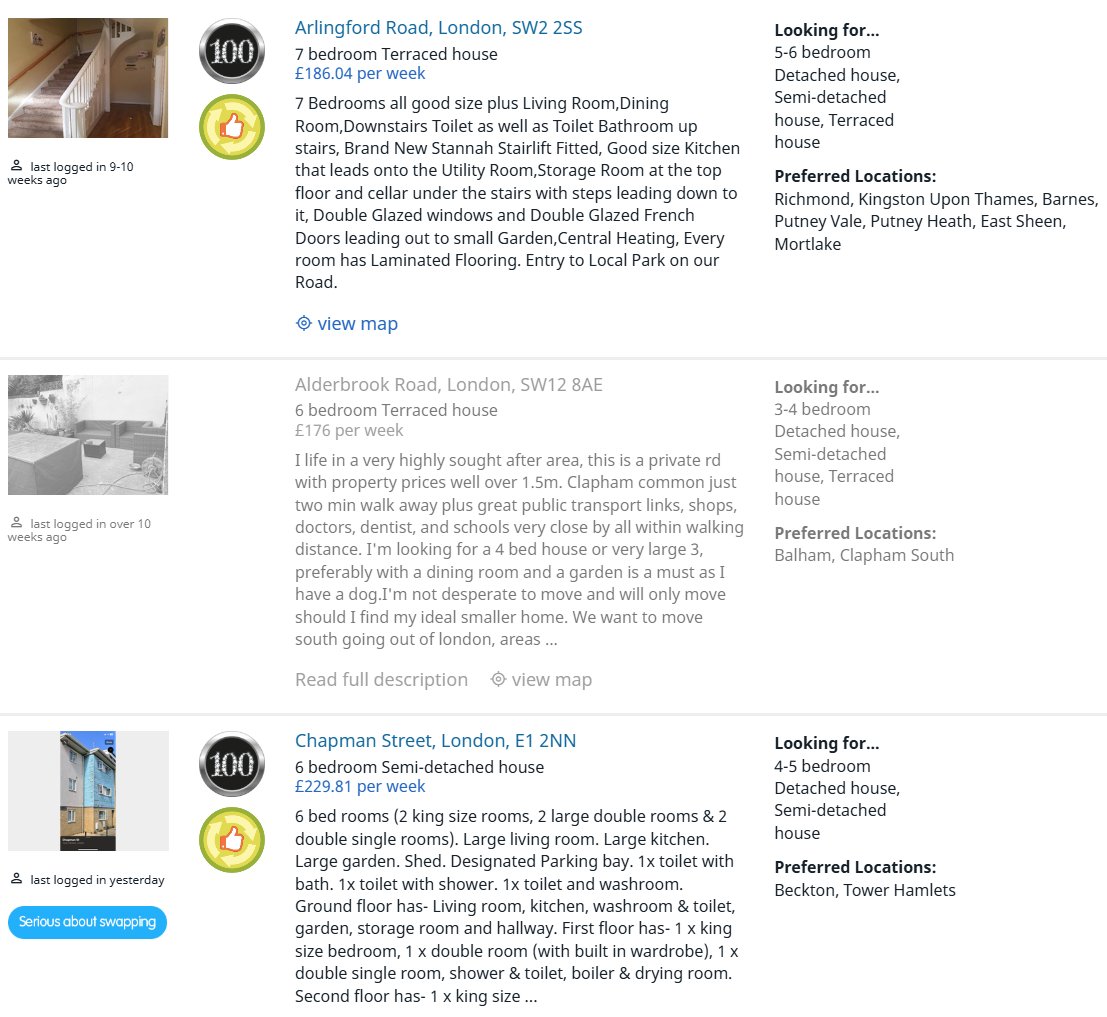

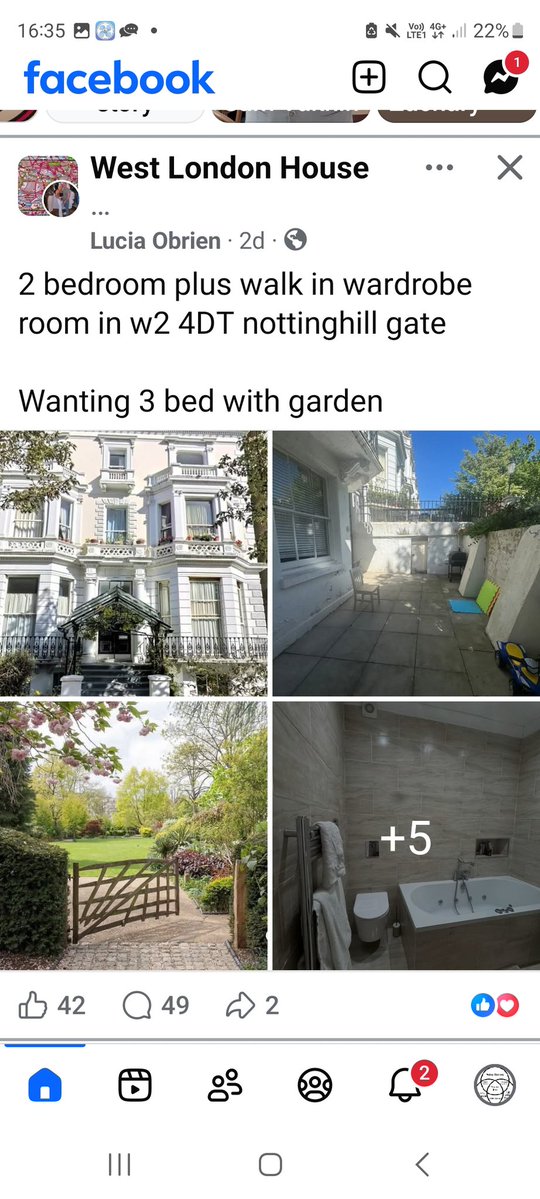

The council house swapping Facebook groups and websites are very eye-opening. There are 6- and 7-bedroom properties on offer in Zone 2 at ~£750 a month. Private rents for similar properties would be £6,000 . Enormous subsidies are being distributed in the worst possible way.

56

352

2,138

307,361

RT @minds_eminent: THINGS SOMEONE SHOULD HAVE SLAPPED INTO ME AT 30.

(The best thing you'll read in 2026)

1. Your parents have maybe 20 go…

172

Luke Johnson retweeted

Last month the National Audit Office delivered its verdict on how Sizewell C, the £38.2bn nuclear plant rising on the Suffolk coast, is being paid for. The findings are worth sitting with, because they say a great deal about the peculiar British talent for making a good thing cost the Earth.

Britain should be building nuclear, and far more of it than this government dares to. It is the only road to the cheap, firm power a real industrial economy runs on. The reactor is the easy part. The way we have chosen to finance and govern it is where the money vanishes.

Under the model ministers picked, the investors putting up the capital are handed - in the NAO's own words - high returns for unusually low risk. Risk doesn't disappear when you spare an investor it; it moves. And it has moved onto your electricity bill: an extra £19 to £21 a year, and here is the part that should make you sit up, you pay it during construction, for years before the plant makes a single watt. You are lending money to private investors, at your own risk, so they can earn a safe return on a power station you won't draw a volt from until the 2030s.

It needn't be like this, and the proof is everywhere else nuclear gets built. South Korea takes a reactor from first concrete to first power in about eight years, and builds the next one faster still. Britain contracted Hinkley Point C at a strike price now near £133 a megawatt-hour - among the dearest electricity any Western government has ever agreed to buy - and still won't have it before the decade is out. The engineering is no different here than in Korea. What differs is the governance, and the governance is ours, bill and all.

Progress treats nuclear as the most important thing the country builds, and would build it the way the nations that are good at it do. Our policy puts Sizewell C and a fleet of small modular reactors under a single national delivery authority with one instruction: build it as fast as physically possible, with the investors' return a distant second. Wartime planning consent. A regulator told to assess in months. The state carrying the risk it is best placed to carry, instead of dressing private money in a hi-vis jacket and paying it handsomely to stand near the work.

Cheap, abundant British nuclear power would be one of the most valuable things we could achieve this decade. Which is exactly why it ought to enrage us that we are being made to pay for it twice - once on the bill, and again in the years we are kept waiting - to guarantee the profits of people who were never much at risk in the first place.

6

20

59

2,492

Luke Johnson retweeted

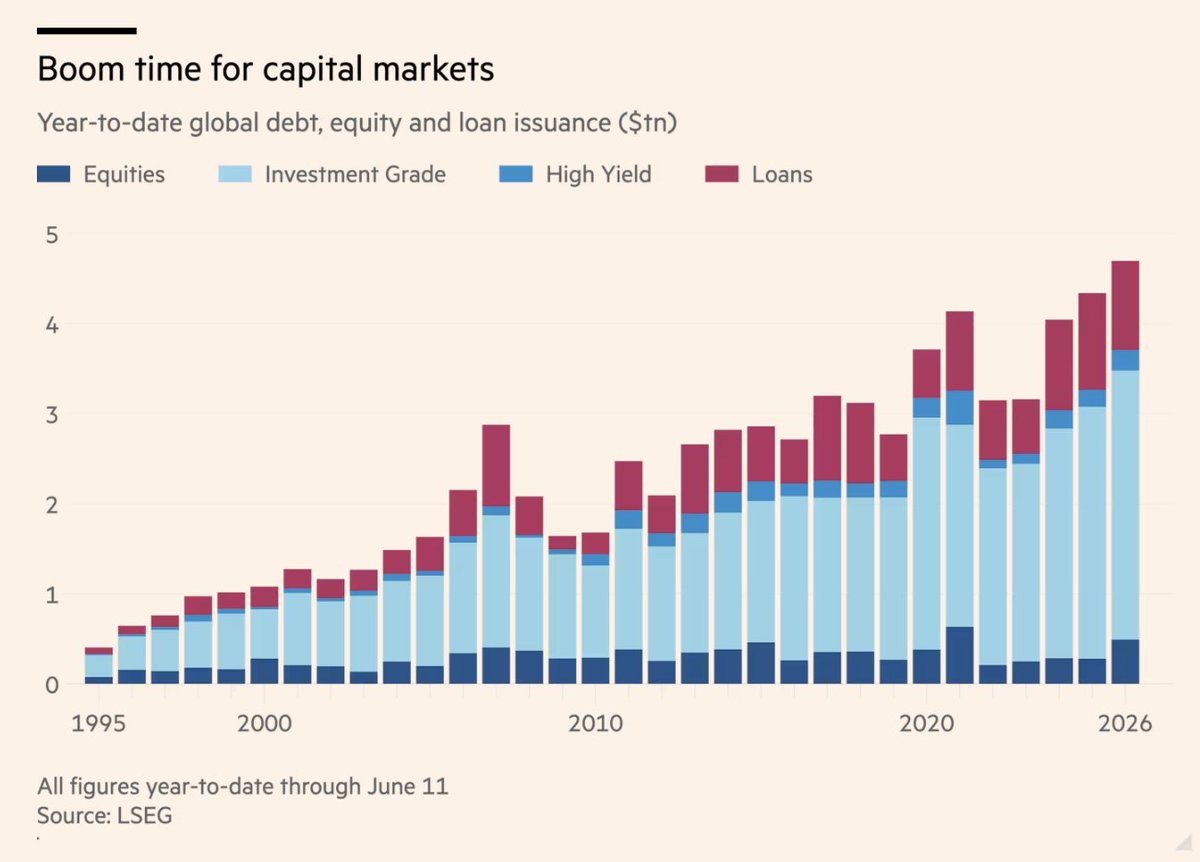

Wall Street digests record fundraising haul as AI race intensifies. Companies have raised roughly $4.7tn across global equity, debt and bank loan markets this year, a record pace, acc to data provider LSEG. That figure, up 7% YoY, does not include the spurt of activity in investment-grade private credit markets, which are increasingly being tapped to finance data centres, chips and power plants feeding the AI boom. That included a $35bn debt package cobbled together by Apollo and Blackstone this week for Anthropic.

ft.com/content/db05efcb-9035…

16

35

119

13,010

Luke Johnson retweeted

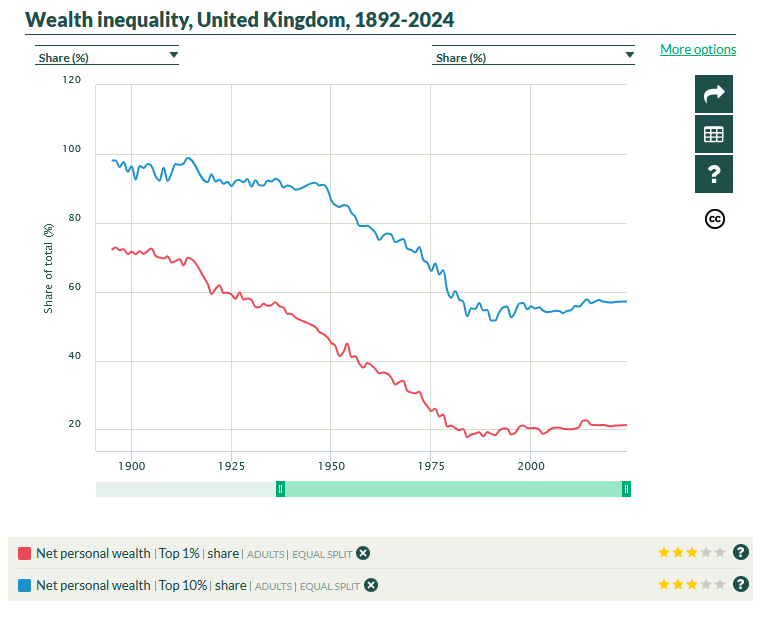

The UK graph is one of the most interesting because the historical graph with the correct denominator — % of total wealth rather than % of GDP — from the World Inequality Database, Piketty’s lab, looks so different.

There is a clear upward trend since the 1980s, but:

1⃣ The levels are far less impressive, since the top 0.001% owns roughly 2% of the nation’s wealth.

2⃣ In retrospect, levels remain much lower than the average for the 20th century.

This, of course, does not take into account that the UK has since developed a large welfare state. In particular, these graphs leave out the value of accrued pension claims from the UK state pension, something that most workers in the early 20th century could not count on.

If, instead of looking specifically at the top 0.001%, we look at the top 1%, which is more relevant for 99% of people, there was a huge collapse in wealth inequality in the UK between 1900 and 1980, and basically no change since then. And that is before taking state pensions into account. The same thing is true when you look at the top 10%.

Again, these are not my numbers, but those reported by Piketty and Zucman’s lab. The only difference is that I compute the shares correctly: the wealth of the top 1% as a share of total wealth of the UK rather than its GDP.

Every group’s wealth has increased as a percentage of GDP since 1980 because asset prices have increased: house prices notably. Using GDP as the denominator does all the heavy lifting here and is a fallacy.

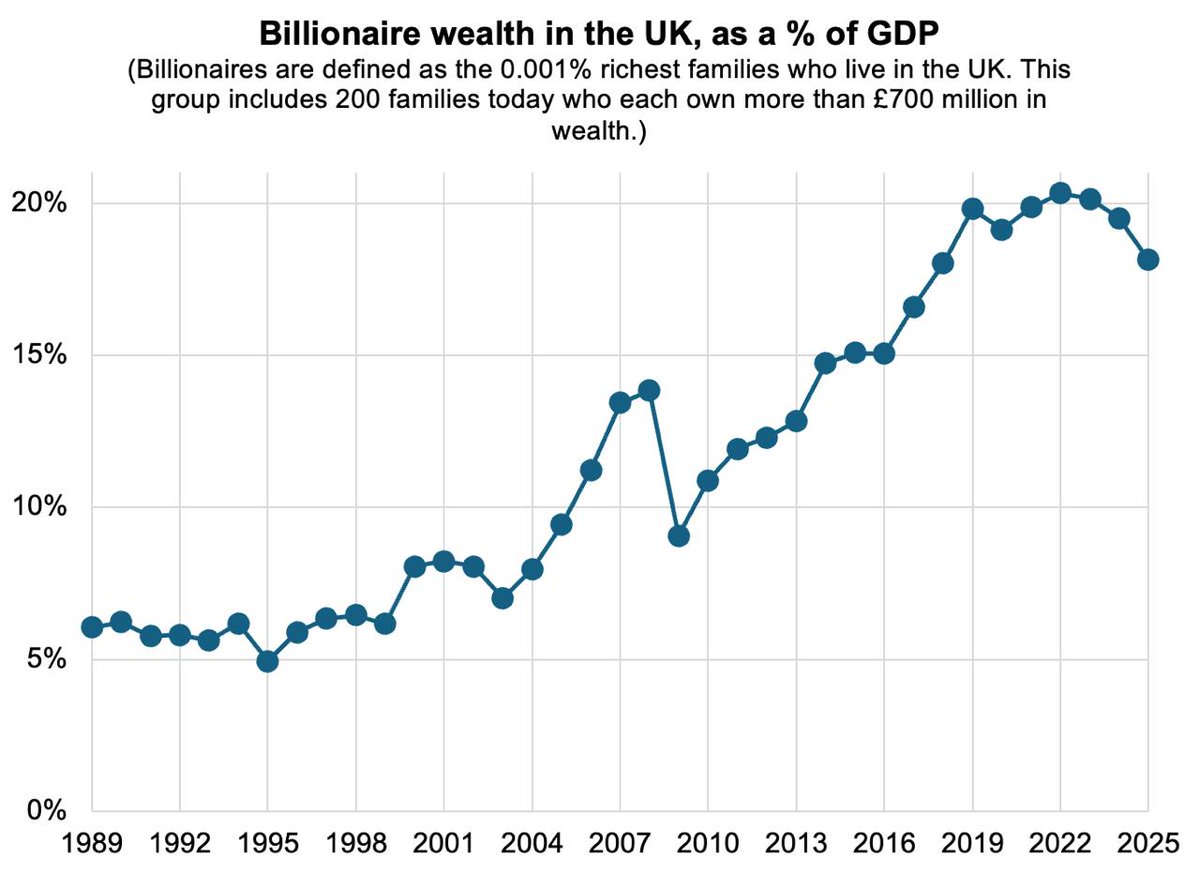

In the 1980s, the 0.001% wealthiest families living in the UK — roughly 200 families — owned wealth equivalent to 5% of UK GDP.

Today: 20% of GDP.

If they spent all their wealth, these 200 families could buy ~1/5 of all the goods & services produced in a given year in the UK.

10

36

139

16,172

Luke Johnson retweeted

It is literally insane simultaneously to think that 16 and 17 year olds are mature enough to vote but not mature enough to look at Instagram at 8:30pm. This is comically absurd.

🚨 NEW: Keir Starmer will introduce nightly social media curfews for 16 and 17-year-olds as part of the Government's social media ban

[@thetimes]

135

1,645

12,346

339,156

Luke Johnson retweeted

Between 1982 and 2020, the number of the 100 richest Americans who got rich from inheritance decreased from 60 to 27. And yet on the left they think the mid 20th century was the good old days, because economic inequality was lower then.

paulgraham.com/richnow.html

73

132

1,505

78,411

Luke Johnson retweeted

Debt-fuelled expansion and marketisation have brought England's university sector to the brink of ruin.

We need a smaller system with higher standards - and a fairer distribution of costs between students and the state.

A closer look at the 40 recommendations:

🧵

2

7

27

7,241

Luke Johnson retweeted

🚀mining margins are around 31%

That is the highest of any major sector

The next best sectors are near 17%

Why this matters now

🔹 Higher interest rates reduce the value of distant future cash flows

🔹 Mining companies generate cash today

🔹 Decades of underinvestment have constrained supply

🔹 AI and electrification need more metals

🔹 Rearmament and infrastructure spending add further demand

🔹 Deglobalization is making secure domestic supply more valuable

Meanwhile, investors continue paying extreme valuations for long-duration growth

Mining offers the opposite

🔸Real assets

🔸Immediate cash flow

🔸Tight supply

🔸Strategic demand

🔸Lower relative valuations

The next market leadership may not come from companies promising profits years from now

It may come from companies producing the materials the world already cannot get enough of.

Image source: @TaviCosta

4

21

52

3,677

Luke Johnson retweeted

The more I sit with SpaceX's trajectory, the harder it gets to place it in any historical frame.

In 2002, Elon Musk founded SpaceX with roughly $100 million of his own money from the sale of PayPal. One founder, one check, and by his own admission a less-than-10% chance of success.

On June 12, 2026, it went public. By the close of its first day of trading it was worth roughly $2.1 trillion, one of the most valuable companies on Earth. (Worth flagging honestly: that figure now includes xAI, which SpaceX absorbed in February 2026, so part of the $2.1T is AI compute, not launch.)

That is north of 20,000x in 24 years.

For scale, measured from their 2002 public-market valuations:

NVIDIA: ~4,100x

Apple: ~570x

Amazon: a few hundred x

Microsoft: ~14x, but it was already a $250B company in 2002

Put differently: a company worth $100 million in 2002 would need to be worth ~$2 trillion today to match SpaceX. A company worth $1 billion would need to be worth ~$20 trillion. Nothing on Earth is worth $20 trillion.

Even granting the caveats, that a founder's seed check isn't a clean market valuation, and that part of the recent jump is the xAI merger, I'm not aware of any U.S. company with a reliable valuation history that has compounded more from 2002 to 2026.

And the most remarkable part: he did it twice.

Tesla was incorporated in 2003, but Musk's real entry was the 2004 Series A, where he put in $6.5 million of a $7.5 million round for roughly a quarter of a company then worth on the order of $30 million. Tesla went public in 2010 at a ~$1.7 billion valuation. Today it is worth about $1.6 trillion, roughly 940x from that IPO and on the order of tens of thousands of x from his 2004 entry.

Two companies, one person, both into the trillions in the most excruciatingly brutal industries.

Turning small early checks into roughly $3.7 trillion of combined value inside a single career is one of the most extraordinary acts of value creation in the history of business. And incredibly both companies are just getting started in their biggest TAMs!

There has never been anyone like him.

7

23

219

11,178

Luke Johnson retweeted

Credit where credit's due... From @tejparikh90 this morning in @FT

5

12

1,553

Luke Johnson retweeted

Jun 13

Two things can be true at once….

AI investments will end in a big bubble, but we are not there yet.

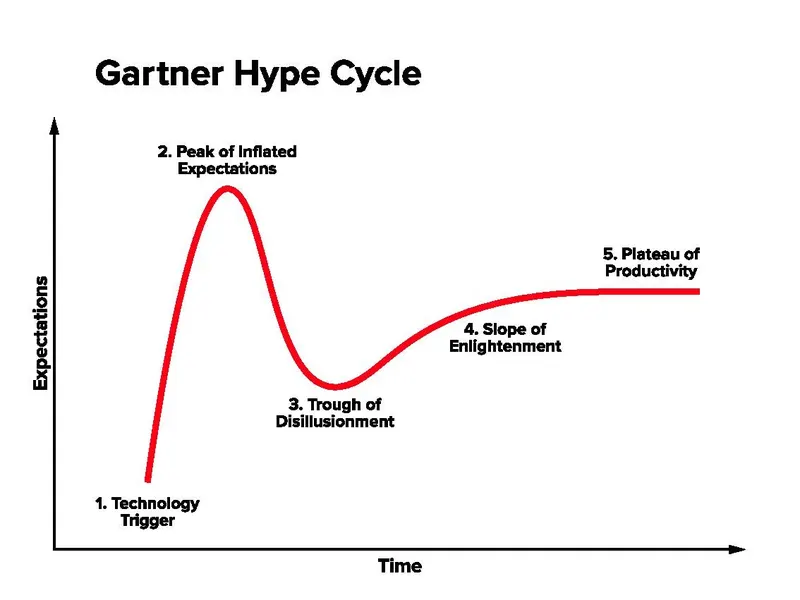

See the image below. Grant thinks we are near the "peak of inflated expectations." Recent Gartner analysis puts agentic AI right at that peak, but I still think we have more of the curve to climb before we actually get there. I agree with Grant (and Gartner) that we’re on this curve — I’m just arguing about where we are on it. And yes, it could end up being the biggest bubble yet.

We are in 1996 or 1997, not the spring of 2000.

We Are Early

About 5% of the corporate world is using the full potential of agentic AI. 85% to 90% are engaged with these tools and trying to figure out what they can actually do.

I’m deep into using all these tools, and I’m still trying to fully understand them. But I can already see their massive power and how they will change everything in the next 2 to 4 years.

I don’t think it will be as bad as most people worry. I think the net effect will be positive for employment and economic growth over time. That said, we’re about to go through a period of massive change, and change is always scary.

Once these tools are better understood, that 5% usage will move toward 85%. At that point, we’ll realize that effective, usable compute and data center capacity is still too small for what’s coming. Hyperscalers are already spending hundreds of billions, but we’re not seeing the kind of overbuilding and low utilization that usually marks the top of these cycles. The real bubble comes when spending massively outpaces productive demand. We’re not there yet because the productive demand coming will be huge.

How are we going to pay for all this?

Worldwide, corporations already spend roughly $400–450 billion a year on SaaS. That’s thousands of dollars per corporate computer — often more than they spend on the hardware itself.

A big chunk of that SaaS spending will likely get redirected or consolidated into AI. It’s similar to what happened with cameras, calculators, MP3 players, video recorders, maps, and alarm clocks — all of which eventually moved into the iPhone. AI agents should do something similar by consolidating a bunch of fragmented tools into a single intelligent interface.

The future computer probably won’t need a keyboard most of the time. It will have a big context window, and you’ll mostly just tell it what you want. You won’t have to fight with a dozen different SaaS products trying to get them to talk to each other.

𝗝𝗶𝗺 𝗚𝗿𝗮𝗻𝘁 𝗼𝗻 𝘁𝗵𝗲 𝗔𝗜 𝗯𝗼𝗼𝗺:

"I think that today is one of the greatest bubbles of all time."

He argues the excitement around AI dwarfs the worldwide web and fiber optics, and that better technology doesn't ground the speculative spirit, it incites it.

youtu.be/mq0r92gLkLw?si=ljCm…

40

55

261

62,516

Luke Johnson retweeted

FT 14th Jun'26

"The first half of 2026 has been the strongest for purchases of UK companies by foreign buyers in decades."

"The driver is we’re in an M&A wave and these UK firms are decent global businesses that are, for whatever reason, underperforming,” said one investment banker.

2

2

4

1,580

China Internet Stocks Just Completed a 13-Year Round Trip

In August 2013, the KraneShares CSI China Internet ETF — KWEB — traded around $26.

Today, more than a decade later, it is still around $26.

During the same period, the U.S. produced an AI boom, a cloud boom, a mega-cap tech boom, and one of the greatest wealth-creation cycles in modern market history.

China produced Alibaba, Tencent, Meituan, JD, Pinduoduo, ByteDance, electric vehicles, mobile payments, and one of the most sophisticated digital consumer ecosystems on earth.

And yet the broad China internet trade went nowhere.

This is the central lesson investors keep ignoring:

A great company is not always a great stock.

A great industry is not always a great investment.

And a great growth story can be completely destroyed by governance risk.

KWEB did not fail because China lacked talent, scale, technology, or consumer demand.

It failed because the market learned that in Xi Jinping’s China, equity holders are not the senior claimants. The Party is.

The last five years made this brutally clear.

The platform crackdown crushed valuation multiples.

The tutoring ban vaporized an entire listed industry almost overnight.

Evergrande exposed the property model.

Youth unemployment surged.

The population began shrinking.

Foreign capital started asking a question it should have asked earlier:

What exactly do I own when I buy a Chinese equity?

In Western markets, investors debate earnings, margins, interest rates, and competition.

In China, investors must also price in one more variable:

political permission.

That variable has no terminal value model, no clean discount rate, and no reliable hedge.

This is why the KWEB chart is so important. It is not just a stock chart. It is a 13-year case study in how political risk can eat innovation, growth, and index inclusion alive.

The old China trade was simple: buy growth, ignore politics.

The new China trade is different:

Respect the innovation.

Fear the governance.

And never confuse national ambition with shareholder return.

8

22

55

9,696

Luke Johnson retweeted

SpaceX raised only $12B of capital before going public. With that $12B, they revolutionized the rocket industry, built a global satellite network, and created arguably the most innovative company of all time.

The federal government spends $12B every 15 hours and still can’t get its shit together. Prior to SpaceX, NASA was sending astronauts into space on Soviet-era Russian Soyuz capsules.

So no, I don’t find Elon’s wealth to be a problem, and I wouldn’t trust Elizabeth Warren or Bernie Sanders to allocate a single dollar of it.

156

1,381

6,994

123,369

Luke Johnson retweeted

Jun 13

If, when you say regulation, you mean the dead and clammy hand of the commissar—the gentleman who has never in his life built a single thing, drafting rules to govern a thing he cannot define, to be enforced by men who cannot read them; if you mean the form in triplicate, the impact assessment upon the impact assessment, the compliance officer who breeds, in the warm dark of the org chart, further compliance officers unto the third and fourth generation; if you mean the moat—the deep cold moat that the giant digs around his own castle and christens, with a perfectly straight face, public safety—the drawbridge he hauls up behind himself the very instant he is across, lest any hungrier and hungrier man should follow; if you mean the precautionary principle, which, had it governed our grandfathers, would have banned the wheel pending further study of the hill, and left us yet shivering and raw in the mouth of the cave, blessing its excellent ventilation; if you mean the European disease—that magnificent open-air museum of a continent, which produces in our time precisely two things in great abundance, and they are regulation, and the eloquent and well-footnoted regret of cultivated men explaining at length why they have produced nothing else; if you mean the license required to think, the permission slip for honest arithmetic, the king’s wax stamp pressed upon the forehead of every new idea before it may draw its first breath; if you mean the agency dispatched, with trumpets, to slay a single dragon, which arrives at the cave, surveys the accommodations, and moves in—and spends the ensuing century laying eggs and devouring the very villagers it was sworn to defend; if you mean the startup that perishes not of the market’s honest verdict but of the filing fee, the genius decamping by the next tide to a freer and warmer shore; if you mean the law that arrives, faithful as the swallows, exactly one whole epoch too late—helmeted, plumed, and magnificently armed—to regulate the stagecoach—then certainly, my friends, I am against it.

But—but, my friends—if, when you say regulation, you mean instead the humble steel guardrail upon the mountain road at midnight, the very thing you curse on the easy days and bless on your knees the one night the fog comes down; if you mean the brakes—for it is the brakes, and not the engine alone, that permit a sane man to drive fast and yet arrive alive—and the buttress, without which no cathedral was ever flung so high, but only in spite of which, but because of which; if you mean the meat inspector, who is the single homely reason a man may eat a sausage in this republic without first composing his last will and testament; if you mean the firebreak cut clean through the forest before the dry season of the burning, the smallpox cordon, the buoy that marks the channel, the rule of the road that lets ten thousand strangers hurtle past one another in the dark at fearful speed and arrive, by its quiet grace, every one of them home; if you mean the honest scale and the true weight, the reason a pound is a pound and a dollar a dollar from Natchez to Nome; if you mean the firm and decent wall between the counterfeit voice and the widow’s bank account, between the deepfaked candidate and the ballot box on the eve of the vote, between the loosed and loveless machine and the schoolyard it neither knows nor pities; if you mean the simple plank of law that says the strong shall not, in the gray dawn, feed the weak quietly into the furnace and sell the rising smoke as progress; if you mean, in the end, the one slender thread of trust without which no citizen will ever dare to use the marvelous thing at all—for where there is no rule there is no trust, and where there is no trust there is no commerce, and a miracle that no man dares to touch is no miracle, but only a handsome and expensive ghost—then certainly I am for it.

This is my stand. I will not retreat from it. I will not compromise one inch of it.

344

764

5,442

472,356

Luke Johnson retweeted

The usual time of eating dinner in Europe. I remember traveling to Spain as a young kid and my German 6pm meal had to wait until 10pm. It was weird. Source: buff.ly/36goiS4

270

168

1,129

251,820