780 Photos and videos

CJ retweeted

Jun 12

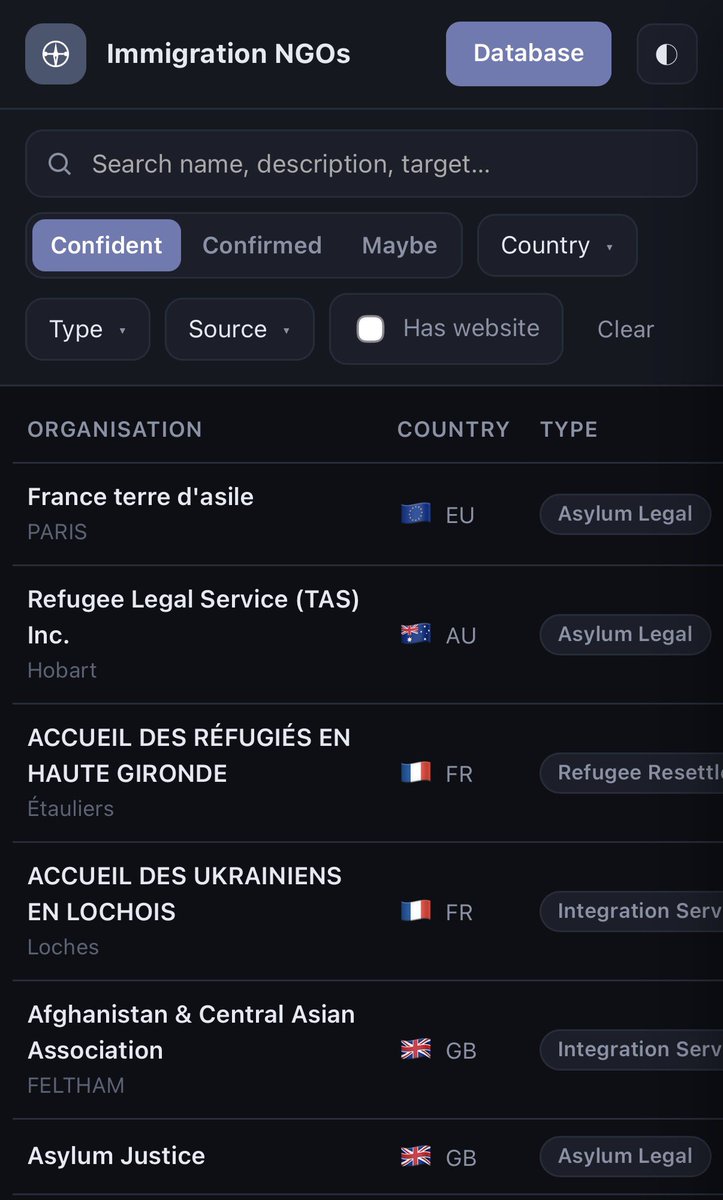

My friend just created a website that tracks every single immigration NGO in the west with their funding $ numbers, phone number, names and addresses

asylum.ngo

262

4,289

18,081

220,296

CJ retweeted

So basically, you've been paid to say a great many things about BTC that you don't understand.

Worse, you've applauded something that is profoundly negative for it the moment anyone bothers to think past the slogan.

The issue is governance.

Who controls the protocol? Who changes the rules? Who coordinates policy? Who benefits from those changes?

BTC’s great trick was pretending governance vanished because everyone agreed not to look at it.

A marvellous political theory, really: close your eyes, clap for commodities, and hope the law gets bored.

4

20

126

2,466

CJ retweeted

“Can’t be taken from you.”

Adorable.

There have just been multiple announcements about so-called BTC Core "Bitcoin" being seized or frozen, but sure, keep chanting the nursery rhyme.

And if developers can change the protocol, then the system is governed. Controlled. Managed. Administered. Pick the word you like. It is not set in stone, and it is not Bitcoin. It is BTC.

Calling that “decentralized money” is like calling a bank account self-sovereign because the website has orange branding.

Society is not moving slowly. It is merely taking time to notice that you bought a committee-controlled token and mistook the marketing brochure for monetary theory.

7

10

64

1,361

CJ retweeted

May 20

It's probably due to extreme uncertainty risk for short sellers.

> Since MSCI listing triggers tens of millions of new inflow for $SIVE in a week or two.

> NASDAQ listing could be anytime

> Earnings catalysts, with new pluggable partners

> News about $JBL extreme demand for 1.6T LRO using $SIVE today

> and now more M&A related stuff that can suddenly increase revenue numbers

Spiking short rates is better for long term holders, since it makes it more painful to have short positions, especially when it's 17% of the float.

6

3

126

9,700

CJ retweeted

Apr 16

The next major update we’re planning to release for OTG will be a complete rework of our economy, marketplace, loadouts, crafting, and even an update to the extraction flow.

Unfortunately, Zeroes clearly don’t care about extracting anything other than Purple Hex. It’s time to finally fix that.

This is the missing piece OTG needs to enter the top league we are working so hard to reach.

86

75

248

16,488

CJ retweeted

Apr 15

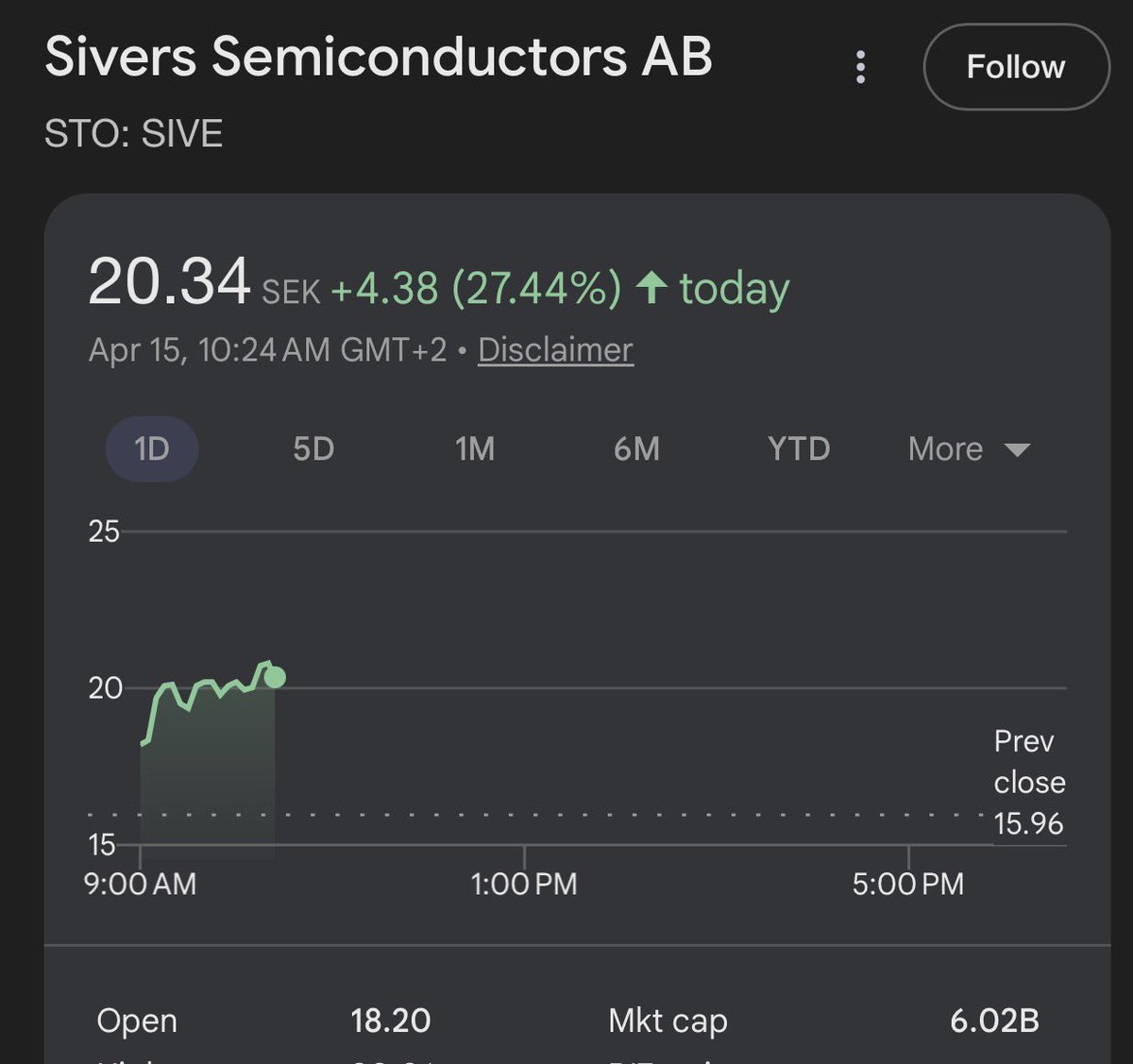

I really meant it when I thought $SIVE could be valued at $2B today.

When do you ever find a critical laser supplier to $MRVL, $JBL, and Hyperscaler supply chains...

At $620m MC?

You can't... Since there's only a few in the world.

And the rest in hyperscaler supply chains from $LITE to $MTSI are in the tens of billions...

Apr 15

$SIVE is the next $LITE at $560m MC.

Institutions just got full confirmation today:

Sivers is now the light source in hyperscaler supply chains and the direct supplier of $JBL optical transceivers.

It’s only a matter of time.

99

76

926

268,175

CJ retweeted

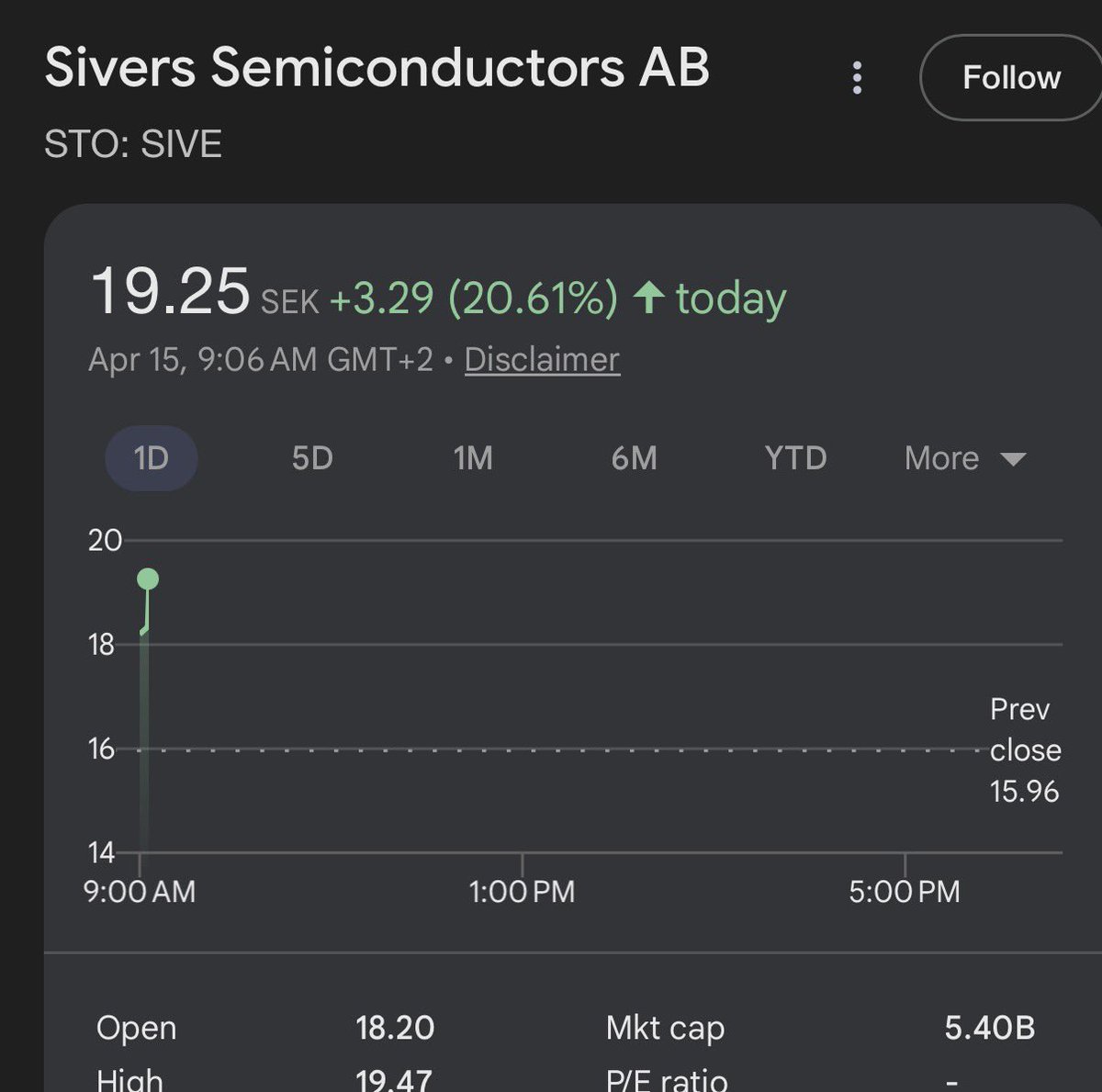

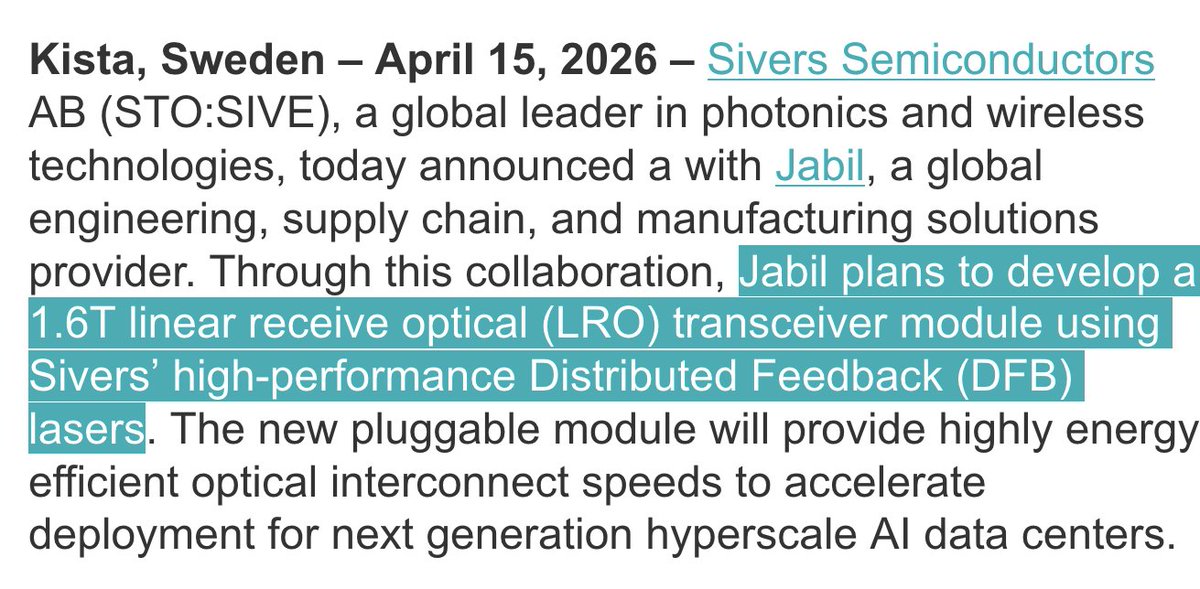

Apr 15

IT'S OFFICIAL: $JBL to use $SIVE Lasers for their optical transceivers.

Today: "Jabil plans to develop a 1.6T linear receive optical (LRO) transceiver module using Sivers’ high-performance Distributed Feedback (DFB) lasers"

Jabil Photonics: :Working with Sivers will allow us to deliver a 1.6T LRO solution that meets both data center performance and power targets at scale"

Where have you seen the LIGHT SOURCE for hyperscaler supply chains...

At a $500m MC? We had this hinted from physical sources at OFC, but many institutions needed actual confirmation like this.

77

85

1,130

414,789

CJ retweeted

Apr 9

While people who have never played OTG and have never built a business sit and spread FUD to farm a few views — targeting the biggest web3 game ever created, a game that represents not only itself but the entire web3 gaming industry in front of traditional gaming — we will keep building for the millions of players who actually love our product.

And we are deeply grateful for that support. Many choose to show it by becoming paid OTG Pro subscribers (100k users signed in 2025 alone).

Every single day, 3,000 new players join OTG.

And for those still spreading FUD — we’re happy to set up a live dashboard so you can see every new player joining in real time.

Access will cost you 100k GUN — so you can finally put real weight behind your words.

Through all of the noise, OTG now has the highest player retention we have ever seen — 2.5x higher than in October 2024, reaching industry-record D1 retention.

A year ago, the same voices were claiming the game didn’t have enough players for fast matchmaking. Since then, we have launched multiple new modes — Ranked, Solos, and Custom — something that is only possible with a rapidly growing player base.

The same haters who posted thousands of times that we would never appear on Xbox, PlayStation, or Steam — were wrong. It happened.

We are now the only web3 game to date available on PlayStation and Xbox.

They said we wouldn’t ship the narrative campaign — we already shipped it to players in Q3 last year, and we keep expanding it with every new seasonal update.

They said we wouldn’t keep delivering — yet every single month we ship more updates, more features, and more content.

Just open our YouTube channel — the track record is public.

Haters keep making predictions.

We keep delivering.

OTG is a game built by a company of over 400 people, developed over 6 years, where the founders invested tens of millions of dollars before raising a single dollar externally.

Within 6 years, there has never been a single day where anyone worked in a “work-life balance” mode — it has been a day-and-night fight to ship a project of the scale of Call of Duty, built by an independent studio.

And we made it.

Through top streamers, we put a web3 game in front of hundreds of millions — doing more for this space than anyone.

Off The Grid today is not just part of web3 gaming — it defines it, whether some people like it or not. Being named Web3 Game of the Year two years in a row.

Today there is a new narrative from haters — that Gunzilla incorrectly laid off contractors or paid them with delays.

Yes, we are optimizing costs — like every company in gaming, crypto, and tech is doing right now. We have been doing this for over a year.

And yes, to not disrupt company operations, some payments may be scheduled in a way that works for the company’s cash flow — not always for everyone individually. That’s the reality of the world we live in.

But to protect the interests of our players and our full-time official employees — whose salaries, over 6 years, have never been delayed by more than a week — we operate at a pace that ensures the company continues moving forward.

And of course, we honor every obligation.

We apologize for any inconvenience this may have caused.

It’s also worth noting that one of the loudest voices — a contractor who finished working with us just a week ago — was repaid immediately.

OTG has been live for over 1.5 years, and we’re still here — despite how much some people would love to see otherwise. Sorry, we won’t be giving you that privilege.

And while our dear haters keep trying to find new reasons why Gunzilla should fail — we will keep responding with achievements.

Including being recognized by one of the most reputable business media outlets in the world as one of the most innovative companies in gaming in 2026 — for bringing new life into the largest printed gaming magazine in the world, Game Informer, which we continue to grow day by day.

fastcompany.com/91497218/gam…

Community note

Multiple Gunzilla employees, including a Talent Acquisition Lead and Senior VFX Animator, have publicly reported unpaid salaries for several months on LinkedIn, contradicting claims that full-time employee pay has never been delayed more than a week. insider-gaming.com/gunzilla-games…

215

78

279

131,583

CJ retweeted

Apr 2

Hydrograph $HGRAF has all three supports aligning plus the 50 day sma. I’d see this as a good buying opportunity NFA.

7

16

144

8,949

CJ retweeted

Mar 31

Hydrograph $HGRAF is one of the best looking charts in the market right now.

17

26

224

14,921

CJ retweeted

Mar 27

I just bought ~.5%-1% of $SIVE as a company.

I said their future CW laser chokepoint is grossly mispriced.

And I put my money where my mouth is.

Especially when they're the confirmed light source for Jabil, $MRVL Celestial, O-Net, and other hyperscalers.

Mar 27

This is why you need to have conviction before entering a trade.

If you knew $SIVE positioning in the CW laser space to Jabil, $MRVL Celestial, and others for CPO.

$250M MC as the light source chokepoint would be a joke.

High confidence we’ll see this end up like $AXTI in a years time since it this will be the architectural paradigm for cpo scale up.

Don’t care about volatility in the way up because I have conviction in how this plays out with photonics.

147

59

1,025

377,010

CJ retweeted

Mar 25

$SIVE has gotta be the highest upside stock I’ve seen in this market since $AXTI?

No way markets missed the CW laser light source for Jabil, Marvell (Celestial via $POET), O-Net, Ayar ( $NVDA, Mediatek backed)…

At a $140M valuation. ($350m now)

Not only do you get the most direct laser exposure to future CPO scale up?

But also this cycle’s 1.6T pluggables with $JBL (formerly Intel Silicon Photonics division) coming soon.

With Win Semi bridge capacity scaling needed for hyperscaler supply chains.

Don’t think 99.9% of people realized the sheer scale of this yet.

Mar 25

Every industry leader...

Especially $AVGO (Physical Layer Products division) in this statement today.

Cites Lasers as a bottleneck for semiconductors.

If you aren't long...

-> CW Lasers: $SIVE | $MTSI

-> EML Lasers: $COHR | $LITE

-> or their foundries in $TSEM/Win Semi

Maybe it's time to wake up?

Broadcom Ramachandran: "Even though there are multiple suppliers in the industry today... there is definitely a supply constraint in the laser space,”

49

49

518

267,227

CJ retweeted

Mar 25

TFW institutions realize how important $SIVE is in the CW/EML laser bottleneck.

But have no positions…

Sivers is up 220% so far, but I expect this to be my next personal 10x like $AXTI.

Mar 16

I’m long $SIVE at $140M.

I believe this is the next $LITE that markets and institutions missed.

$SIVE makes InP CW DFB lasers.

Closest comparison is $LITE in the current EML laser bottleneck.

But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles.

They supply the lasers to $POET Starlight, Ayar SuperNova.

And others for the future CPO/silicon photonics architectures spearheaded by $NVDA.

Current valuations make 0 sense to me personally.

$POET is advanced packaging for $SIVE type lasers…

But $POET commands worth 11x more than the company making the laser itself?

It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B.

So now at $130m:

-

- You have a likely mini $LITE like laser supplier to Marvell Celestial hyperscalers through $POET.

- Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI.

And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential.

On top, for revenue, they expected $453M "pipeline next few years”.

And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers."

Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come.

I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt.

It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week.

Best of all, this is their pure play inp laser segment for silicon/photonics cpo.

Their Lidar segment is ramping up and they have $53-138M projected revenue coming in.

Downside risk:

- execution (as always)

- dilution to scale up capacity to compete with $LITE and others.

- $LITE, $COHR competition on scale after $NVDA just gave them $4B

- CPO ramp gets delayed.

I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B MC.

Or how $POET, is worth ~9-10x more than its laser supplier.

When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M.

I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck).

But I do think it will get a lot of institutional attention as Celestial and Ayar scale up.

Especially if $POET and $SIVE gets qualified with other customers.

If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures.

Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated.

Just as how $LITE did today going from $16 -> $622.

This is just my personal thesis I'm sharing, DYOR/NFI.

TLDR:

InP Lasers are the current bottleneck in photonics as seen with $LITE valuations.

$SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp.

I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst).

The upside here just way too compelling for me personally as the next possible $LITE.

45

50

461

132,232

CJ retweeted

Mar 23

$SIVE is starting to play out like my $AXTI thesis round 10?

Up triple digits now.

Really not sure how markets missed this one tbh?

-> Laser supplier to Jabil… for 1.6T pluggable transceivers in the current supercycle.

-> Laser supplier to Ayar / $MRVL celestial for CPO, in the upcoming supercycle.

Literally all your laser suppliers from $MTSI to $LITE are $17-45B companies.

$SIVE?

Now only at ~$310M.

High conviction long.

Mar 16

I’m long $SIVE at $140M.

I believe this is the next $LITE that markets and institutions missed.

$SIVE makes InP CW DFB lasers.

Closest comparison is $LITE in the current EML laser bottleneck.

But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles.

They supply the lasers to $POET Starlight, Ayar SuperNova.

And others for the future CPO/silicon photonics architectures spearheaded by $NVDA.

Current valuations make 0 sense to me personally.

$POET is advanced packaging for $SIVE type lasers…

But $POET commands worth 11x more than the company making the laser itself?

It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B.

So now at $130m:

-

- You have a likely mini $LITE like laser supplier to Marvell Celestial hyperscalers through $POET.

- Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI.

And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential.

On top, for revenue, they expected $453M "pipeline next few years”.

And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers."

Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come.

I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt.

It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week.

Best of all, this is their pure play inp laser segment for silicon/photonics cpo.

Their Lidar segment is ramping up and they have $53-138M projected revenue coming in.

Downside risk:

- execution (as always)

- dilution to scale up capacity to compete with $LITE and others.

- $LITE, $COHR competition on scale after $NVDA just gave them $4B

- CPO ramp gets delayed.

I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B MC.

Or how $POET, is worth ~9-10x more than its laser supplier.

When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M.

I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck).

But I do think it will get a lot of institutional attention as Celestial and Ayar scale up.

Especially if $POET and $SIVE gets qualified with other customers.

If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures.

Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated.

Just as how $LITE did today going from $16 -> $622.

This is just my personal thesis I'm sharing, DYOR/NFI.

TLDR:

InP Lasers are the current bottleneck in photonics as seen with $LITE valuations.

$SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp.

I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst).

The upside here just way too compelling for me personally as the next possible $LITE.

61

53

453

228,631

CJ retweeted

Mar 19

$SIVE <> $SIVEF is now up 165% this week.

Valuation? ~$300M MC.

However; either I’m dumb or Sivers is one of the best opportunities in photonics today.

You get the laser supplier for Jabil, Ayar, Poet ( $MRVL Celestial ), O-Net, and others:

That end up in $GOOGL, $MSFT, $AMZN, $META AI datacenters.

At ~$300M.

The EML laser suppliers today from $LITE to $COHR for reference are $45B

This is one of the most undiscovered yet critical bottlenecks for future upstream photonics supply chains.

That markets have only starting to price in today.

Mar 16

I’m long $SIVE at $140M.

I believe this is the next $LITE that markets and institutions missed.

$SIVE makes InP CW DFB lasers.

Closest comparison is $LITE in the current EML laser bottleneck.

But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles.

They supply the lasers to $POET Starlight, Ayar SuperNova.

And others for the future CPO/silicon photonics architectures spearheaded by $NVDA.

Current valuations make 0 sense to me personally.

$POET is advanced packaging for $SIVE type lasers…

But $POET commands worth 11x more than the company making the laser itself?

It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B.

So now at $130m:

-

- You have a likely mini $LITE like laser supplier to Marvell Celestial hyperscalers through $POET.

- Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI.

And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential.

On top, for revenue, they expected $453M "pipeline next few years”.

And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers."

Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come.

I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt.

It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week.

Best of all, this is their pure play inp laser segment for silicon/photonics cpo.

Their Lidar segment is ramping up and they have $53-138M projected revenue coming in.

Downside risk:

- execution (as always)

- dilution to scale up capacity to compete with $LITE and others.

- $LITE, $COHR competition on scale after $NVDA just gave them $4B

- CPO ramp gets delayed.

I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B MC.

Or how $POET, is worth ~9-10x more than its laser supplier.

When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M.

I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck).

But I do think it will get a lot of institutional attention as Celestial and Ayar scale up.

Especially if $POET and $SIVE gets qualified with other customers.

If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures.

Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated.

Just as how $LITE did today going from $16 -> $622.

This is just my personal thesis I'm sharing, DYOR/NFI.

TLDR:

InP Lasers are the current bottleneck in photonics as seen with $LITE valuations.

$SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp.

I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst).

The upside here just way too compelling for me personally as the next possible $LITE.

60

45

428

162,629

CJ retweeted

KRAKEN UNSTOPPABLE: $24M IN NEW DEFENSE ORDERS! 🦑

While the market slept, $KRKNF / $PNG.V dropped a massive announcement this morning, proving once again they are the undisputed kings of subsea tech.

The Highlights:

- $24 Million in New Orders: A massive haul across 10 customers in 5 different countries.

- Global Expansion: Includes 3 brand-new defense customers, widening their dominance.

- Product Dominance: High demand for SeaPower batteries, KATFISH, and SAS (Synthetic Aperture Sonar).

- Polish Navy Win: Selling a new KATFISH™ to the Polish Navy for their critical mine-hunting program. 🇵🇱

- Production Scaling: Their new Nova Scotia battery facility is going live next month to meet this explosive demand.

Kraken isn't just winning contracts. They are scaling into a global powerhouse in real-time. The acquisition of Covelya these record orders = a perfect storm for shareholders. 🦑🚀

1

7

66

1,849

CJ retweeted

4

2

26

897