Joined April 2020

- Tweets 729

- Following 71

- Followers 2,022

- Likes 644

103 Photos and videos

Pinned Tweet

27 Oct 2025

A B2B Insurtech SaaS platform focused on financial needs analysis with hyper-personalization. The engine helps our clients engage better with end customers, sell more while selling right, and shorten the sales cycle.

We are currently live with a handful of insurance brokers, wealth advisors, and will soon go live with an insurer.

1

3

375

ProtectMeWell retweeted

Feb 14

The RBI’s latest draft directions on Responsible Business Conduct are a game-changer for how financial products are sold in India.

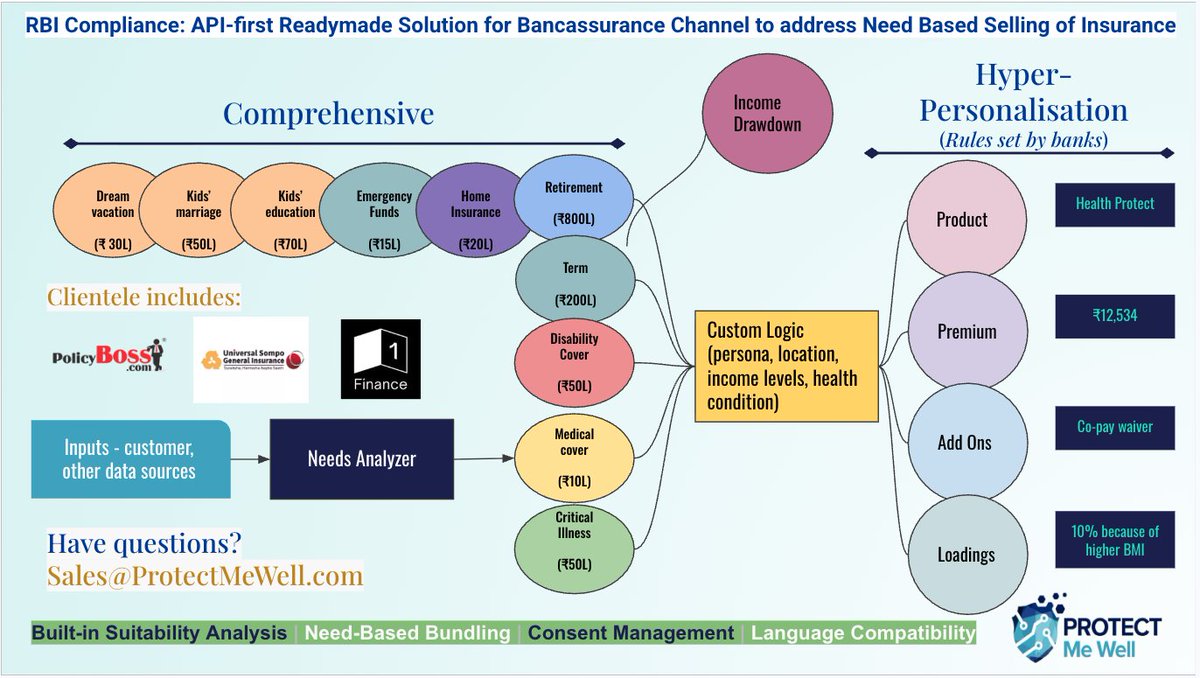

At @ProtectMeWell, we have an API-first solution (currently used by insurance brokers, insurers and wealth advisors) that addresses the following key issues identified in the RBI Direction

✅ Suitability First

✅ Explicit, Un-clubbed Consent

✅ Ethical Bundling

✅ Goodbye Dark Patterns

Need help? DM Me

3

10

3,320

ProtectMeWell retweeted

Feb 14

Thinking of insurance? Think of all the assets that you have. Include you and your family too!

4

13

707

ProtectMeWell retweeted

Feb 5

क्या नई गाड़ी लेते समय शोरूम से इंश्योरेंस लेना जरूरी है?

डायरेक्ट लेने पर इंश्योरेंस कितना सस्ता पड़ता है?

देखिए 'Insurance मंत्र' में खास चर्चा

#InsuranceMantra #MotorInsurance #InsurancePolicy @anuragshah_ @ACKOIndia @ProtectMeWell

x.com/i/broadcasts/1zqJVdYLg…

1

2

335

ProtectMeWell retweeted

Feb 5

#Watch | क्या है हाइपर पर्सनलाइज्ड इंश्योरेंस?

कैसे ये छोटे-छोटे कवरेज को बड़ा बनाता है?

इंश्योरेंस की बारीकियां बता रहे हैं ProtectMeWell के Actuary & Co-Founder, सुमीत रमानी

#InsuranceMantra #HyperPersonalizedInsurance #InsurancePolicy #InsuranceSector @anuragshah_ @ProtectMeWell

1

2

346

ProtectMeWell retweeted

20 Nov 2025

Thrilled to join the Insurance Summit 2025 @officialNIAPUNE for a lively panel on “The Distribution Renaissance — Digital Ecosystems & Future of Insurance Delivery”!

Teamed up with Animesh Das (@ACKOIndia), Mahavir Chopra (@themahavir of @BeshakIN), Sumit Ramani (@RamaniSumit of @ProtectMeWell), & Mohammed Anzy S (@anzieee of @Guidewire_PandC). Stellar moderation by Amit Roy @PwC_IN—loved his Q: "What's the 10-min quick commerce equiv in insurance?"

Dived into AI, trust-building, & customer-centric distribution. Epic event—thanks NIA! 🚀 #InsurTech #InsuranceFuture

@IndiaInsurtech

4

8

728

ProtectMeWell retweeted

29 Oct 2025

I am Sumit Ramani, an actuary and a computer science engineer. I will be live-tweeting the @IndiaInsurtech Annual Event 2025. Follow this thread for the live updates and summary of sessions as the event unfolds

I run two businesses -

1⃣ @ActuariaConsult An actuarial consulting firm with 4 qualified actuaries, focused on insurtechs and have served clients in 20 geographies.

2⃣ @ProtectMeWell A B2B Insurtech SaaS platform focused on financial needs analysis with hyper-personalization. The engine helps our clients engage better with end customers, sell more while selling right, and shorten the sales cycle.

We are currently live with a handful of insurance brokers, wealth advisors, and will soon go live with an insurer.

Some notes & disclosures:

✅If you are a speaker/presenter at the event, do drop your Twitter handle here or DM me. Will try and tag you.

✅Sorry if I missed tagging you or tagged the wrong individual, please assume it was unintentional

✅The event has three parallel tracks, and the tweet may not always be in chronological order. However, I will try and cover every session

✅This is my take on the event and not of the organizations I am associated with

✅Please thank the team that is making it possible to cover the 35 sessions. Many of these are happening in parallel. I had given them the impression that this would be a fun outing with no work 🤦♂️

@vikasorricky @RohitChandak11 @MihirDubal @jasshu7 @NeerPatel_11 @GuptaAayush0 @sridharraghu91

1

7

33

3,505

ProtectMeWell retweeted

5 Oct 2025

FIRE – Financial Independence, Retire Early – sounds like a dream. Yet in many ways, it can also be a fool’s paradise if money becomes the only objective. Because the true goal of life is not just wealth, but living meaningfully.

At the Global Financial Planner’s Summit 2025, we launched the RING OF FIRE by @RamaniSumit, Co-Founder & Actuary, @ProtectMeWell a book that redefines FIRE in the Indian context. It reminds us that financial independence is not the same as retirement, and that luck, choices, and perspective all play a role.

Through stories and insights, this book equips readers to think differently about FIRE, to guide themselves and others with clarity and confidence. Because in the end, FIRE isn’t just about retiring early, but about building a life worth living.

Begin your journey toward a more meaningful version of financial independence, get your copy of the RING OF FIRE here: amzn.in/d/3j7LUz8

#GFPS2025

1

12

2,431

ProtectMeWell retweeted

30 Sep 2025

The book 'Ring of FIRE' by @RamaniSumit, Co-founder & Actuary, @ProtectMeWell, will make its debut at this year’s Global Financial Planner’s Summit.

This book reimagines the concept of Financial Independence and Retire Early (FIRE). While widely discussed in the western world, Sumit offers a fresh perspective tailored specifically for the Indian context.

Join an exclusive gathering of financial advisors, wealth-tech founders and industry leaders who are shaping the future of financial planning.

📅 4 October 2025 |📍Jio World Convention Centre, Mumbai

Register now: gfpsummit.com

#GFPS2025

2

8

1,527

ProtectMeWell retweeted

21 Jun 2025

1/ I walk into my regular coffee shop, and the manager yells, “1 cappuccino, takeaway!” He remembers me, my order, and makes me feel welcome. I’m in and out in 2 mins, coffee in hand.

That’s hyper-personalization.

1

1

7

527

ProtectMeWell retweeted

19 Jun 2025

With hundreds of health insurance options available, choosing the right policy can feel overwhelming.

For many, this leads to being uninsured or underinsured, often without realising it until it’s too late. To change this, we’ve collaborated with @ProtectMeWell.

By combining our deep, unbiased financial research with ProtectMeWell’s actuarial expertise and technology, we’re building a simple and effective insurance recommendation model.

Together, we’re enabling insurance intermediaries, InsurTechs and RIAs to navigate the health insurance space with better insights, through a research-backed model, so they can recommend solutions that genuinely meet their clients’ needs.

@RamaniSumit @manju_dhake

2

2

6

784

ProtectMeWell retweeted

18 Jun 2025

Buying insurance is important, but having the right cover is just as critical.

Too often, people choose policies that do not suit them due to a lack of transparent and unbiased advice.

In fact, only 27% of India’s population has adequate health insurance coverage.

Our collaboration with @ProtectMeWell brings together research, actuarial insight, and technology to decode the fine print and cut through complexity.

This gives RIAs, InsurTechs, and intermediaries a research-backed model to evaluate and recommend insurance more effectively — ultimately giving the end consumer the real benefit of the right protection.

@manju_dhake @RamaniSumit

1

1

6

513

ProtectMeWell retweeted

18 Jun 2025

Big news! @1FinanceHQ & @ProtectMeWell (from our #IndiaInsurTech Community) team up to simplify health insurance!

Their new rule engine helps advisors & consumers cut through complexity with hyper-personalized recommendations.

Congratulations to the both teams!

@RamaniSumit

2

5

10

557

ProtectMeWell retweeted

17 Jun 2025

1/

In late 2017, I quit my job and faced a surprising challenge: securing medical insurance for my family as my corporate cover was ending. 🚨

Despite being in the insurance industry, I was completely lost. Here's what I learned and how we're solving it. 👇

1

2

10

2,614

ProtectMeWell retweeted

10 Jun 2025

In social media parlance, "LIC Uncle", refers to insurance advisors selling endowment insurance policies (and not just of one particular company). The phrase is often used to thrash the insurance policies that offer 5-6% guaranteed returns over 10-30 years, which are tax-exempt.

Interestingly, in most cases, the returns are superior to post-tax returns of Fixed Deposits. Plus these policies also have an additional death cover.

Financially speaking, despite higher first-year commissions, these endowment insurance policies are superior to fixed deposits and offer a guaranteed rate of return for 30 years whereas the longest tenure for Fixed Deposits is usually 10 years. Post which the individuals are exposed to reinvestment risk (which bites in the low interest rate environment like we are going through now!)

Objectively, if an individual is happy with Fixed Deposits (many of them are!) and has a long-term horizon, endowment policies are superior.

So the problem of mis-selling boils down to

✅Whether the endowment policies are aligned with the financial goals of the customer

✅Is the customer aware that surrendering the policies would lead to a loss in value

Need-based selling and creating awareness is the solution.

3

1

6

947

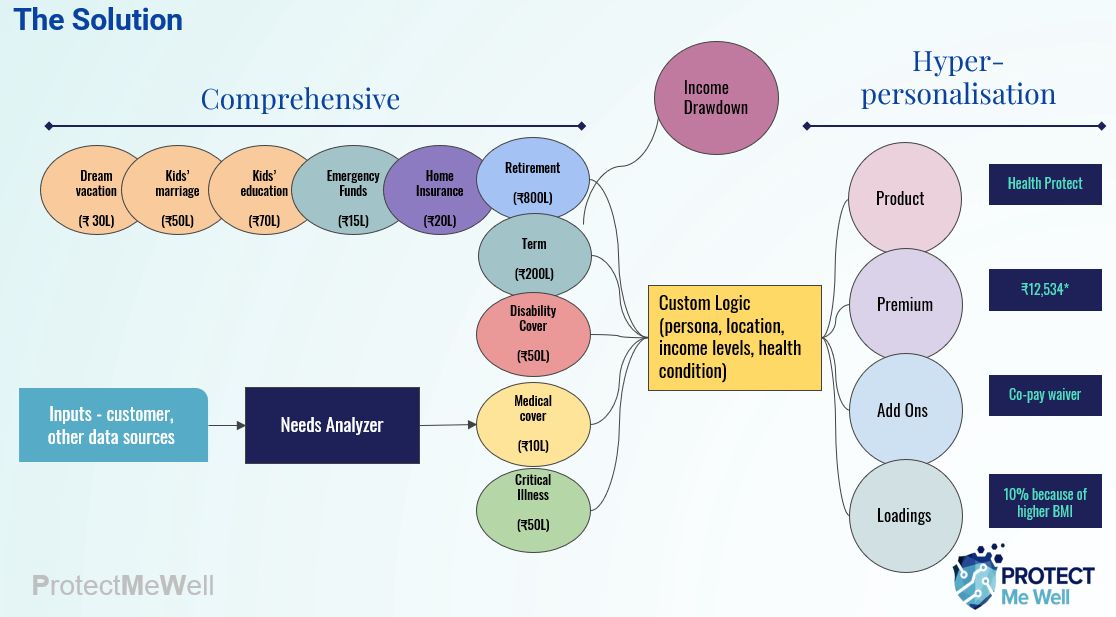

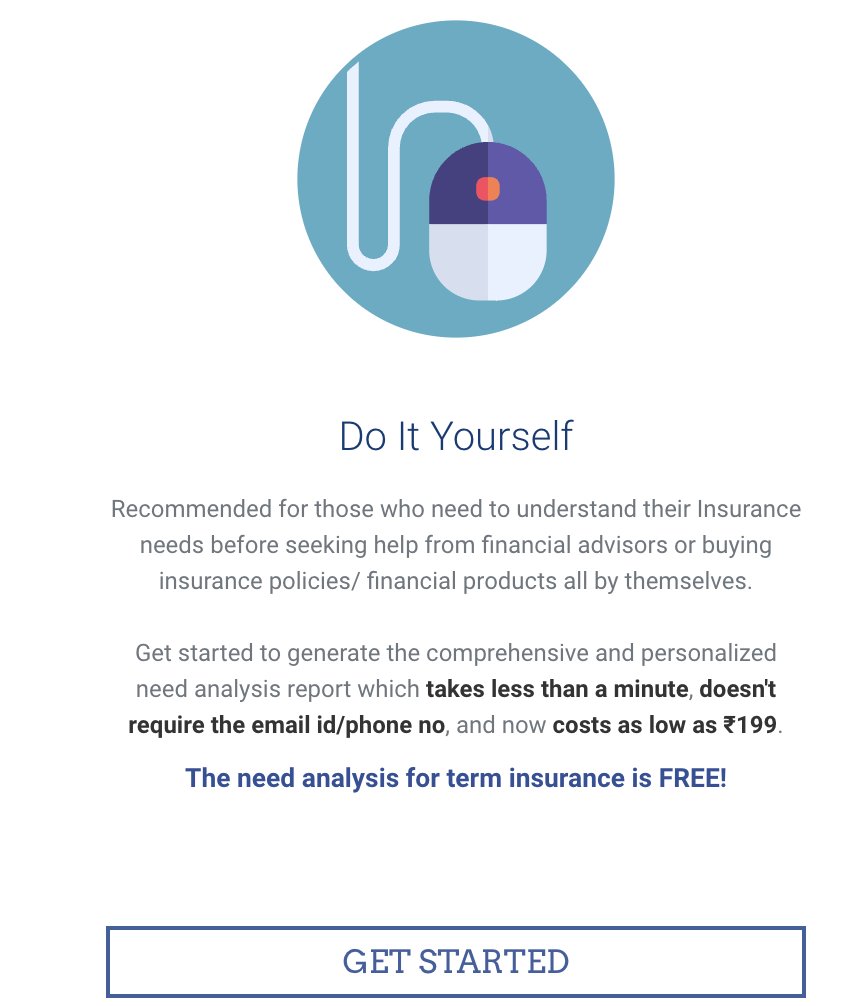

9 Jun 2025

Want to go from left to right? Take this 30-second journey.

Costs ₹99. 100% refundable if you don't like what you get

protectmewell.com/hyper/

2

6

685

7 Jun 2025

Thank you everyone for helping this nano- entrepreneur from rural Madhya Pradesh 🙏

7 Jun 2025

8/

For just ₹99, anyone can access this hyper-personalized engine for medical insurance. And here’s the best part:

100% of the net revenue will go to @WeAreRangDe, a platform for social investing.

2

803

ProtectMeWell retweeted

6 Jun 2025

73% of Indians are underinsured when it comes to health insurance.

Why?

Because of certain contributing factors such as exaggerated features, unclear sub-limits, policies mis-sold for commissions and a lack of understanding about how insurance should truly meet individual needs.

This leads to disappointment and distrust among buyers.

To address this, 1 Finance and ProtectMeWell have launched a hyper-personalised health insurance rule engine to help community of insurance intermediaries, InsurTechs, RIAs recommend the required cover amount and plans by integrating actuarial expertise, data-driven indepth research and evaluation on scoring and ranking to provide better clarity and transparency.

Read the full article on MediaBrief to see how this new framework is helping bridge the gap here: mediabrief.com/1-finance-and…

@ProtectMeWell @manju_dhake @RamaniSumit

1

1

5

1,652

ProtectMeWell retweeted

1 Apr 2025

The 90-second video would help you give a fresh and right direction to your financial planning.

Wish you a great start to the new financial year. 💪

PS: The cameraman struggled to find me in a few seconds. But I eventually showed up!

4

16

46

5,928