Part-time swing trader, photographer and dog lover. Learning all I can from the X investment community. My posts aren't investment advice to buy or sell stocks!

Joined August 2024

- Tweets 5,152

- Following 241

- Followers 503

- Likes 23,684

20 Photos and videos

Michael Deitsch retweeted

Jun 8

In Rush's first show without Neil Peart since 1974, Geddy Lee and Alex Lifeson made grown men cry, and new touring drummer Anika Nilles absolutely killed.

See our review of the Fifty Something Tour kickoff: rollingstone.com/music/music…

38

191

1,021

46,250

Michael Deitsch retweeted

This brought a tear to my eye. My god she’s good.

540

727

8,267

971,980

Michael Deitsch retweeted

When I die, DON’T LET ME VOTE DEMOCRAT.

42

371

2,956

83,257

Michael Deitsch retweeted

Jun 8

MORNING MARKET BRIEF

Monday, June 8, 2026

TL;DR

1/ Middle East risk has real supply-side teeth this time: simultaneous Hormuz and Bab el-Mandeb closure threats have WTI through $95 and that energy reprice feeds directly into Wednesday's CPI, which is already expected at 4.2%.

2/ Friday was a positioning reset, not a clearing event: record SPX put volume, $17B in forced leveraged ETF selling, and a 99th-percentile cap-weight vs. equal-weight divergence confirm the structural fragilities are now actively expressing.

3/ Gamma is back to neutral, the dealer hedging buffer is gone, and below SPX 5735 dealers flip negative and become forced momentum sellers.

4/ Dip buyers need either a clean ceasefire confirmation or a sub-4.0% CPI print to have conviction, and right now they have neither.

5/ Fade the bounce: the buyback bid is a decelerant, not a reversal mechanism when you have a geopolitical supply shock, neutral gamma, residual CTA deleveraging risk, and a record-put-volume hangover all running simultaneously.

KEY THEMES

Middle East risk is back at the top of the macro hierarchy, and this time it's arriving with real supply-side teeth. Iran's reported closure of both the Strait of Hormuz and the Bab el-Mandeb simultaneously, if sustained, would represent the most disruptive chokepoint event in decades, and energy markets are repricing accordingly, with WTI north of $92 and Brent briefly touching $94. Ceasefire noise is tempering the initial spike, but the structural bid under crude isn't going away on rhetoric alone: with Wednesday's CPI expected to print at 4.2% year-over-year, every dollar higher in WTI feeds directly into the Fed's calculus, and rate markets are already beginning to price hikes back into the curve. That's a nasty headwind for an equity market whose gamma stabilizers just broke down. Friday's session left a tell-tale mark: record SPX put volume, $17 billion in forced leveraged ETF selling, and a 99th-percentile divergence between cap-weighted and equal-weight returns all signal that the structural fragilities flagged in recent weeks are now actively expressing. With gamma back in neutral, the market has lost the dealer hedging buffer that kept realized vol compressed during the AI-driven melt-up. The setup into this week's event stack, Hormuz headlines, Wednesday's CPI, a $58 billion 3-year auction Tuesday, and Apple's WWDC as the last remaining AI sentiment anchor, is one where dip buyers will need either a clean ceasefire confirmation or a soft inflation print to have conviction, and right now they have neither.

MARKET SNAPSHOT

The Treasury market is telling the more honest story: yields 2-3bp cheaper across the curve with a bear steepening bias, the 10-year holding near 4.55% after printing 4.58% intraday, and rate swaps now pricing at least one Fed hike by December. With Fed officials in blackout and a $30B IG issuance slate concentrated front of week ahead of CPI/PPI, technical supply pressure into a risk-off macro backdrop is a headwind for duration.

Equity futures rebounding 0.6%-1.3% off Friday's lows reflects reflexive dip-buying instinct intact, but the setup into Wednesday's CPI print, consensus 4.2% YoY and a three-year high, combined with open-ended Middle East risk and $58B in Treasury supply argues for fading the bounce rather than chasing it. As one Bloomberg strategist put it bluntly: both AI and energy, equities' two key drivers, have simultaneously turned negative.

MACRO

Iran's central military command declaring the operation against Israel ended provides a tactical de-escalation signal, though the conditional warning, "much harsher and more crushing actions" if Israeli strikes continue in Lebanon, leaves the ceasefire highly conditional and the risk premium in crude and vol far from fully reversible.

The convergence of Israeli strikes on Beirut, Iranian missile waves targeting military sites including Ramat David Airbase, US strikes on Iranian surveillance assets, and Houthi maritime interdiction marks a multi-front escalation that has broken out of the contained Israel-Hamas frame. This is now a regional conflict with meaningful tail risk to the supply infrastructure underwriting global energy prices.

Barclays estimates the gas price increase translates to roughly $942 in incremental annual fuel costs per consumer, a roughly 1% pre-tax income drag that falls disproportionately on rural, lower-income households. That creates a meaningful headwind for names like Tractor Supply, Dollar stores, and auto parts retailers while leaving high-income urban-focused retailers relatively insulated.

Iran claims full closure of both the Bab el-Mandeb and Strait of Hormuz simultaneously, with explicit threats of strikes on Gulf energy infrastructure. If credible, this represents the most severe geopolitical shock to global energy supply chains in decades, with roughly 35% of seaborne oil trade at risk and immediate implications for crude, LNG, and shipping markets.

CORPORATE

LLY's 4.3% pop on ADA obesity data and the MRVL/FLEX S&P 500 inclusion trade offer isolated long setups with specific, near-term catalysts that are relatively insulated from the macro cross-currents dominating the tape this morning. The Roche/Nurix deal at up to $2.3B also keeps biotech M&A as a live theme.

Apple's WWDC starting today is a binary catalyst for the stock and for broader Magnificent Seven sentiment. After two years of AI delays and execution concerns, a credible Siri overhaul could validate the iPhone upgrade cycle thesis and provide a much-needed positive narrative in a tape where the AI trade just suffered its worst single-day concentration unwind on record.

COMMODITY

Iran-backed Houthis declaring a total maritime ban on Israeli-linked vessels in the Red Sea formalizes the southern chokepoint blockade. Combined with the Hormuz closure threat, global tanker routing is facing simultaneous disruption at both critical exit points, sharply tightening effective seaborne crude supply independent of production levels.

WTI surging through $95 and Brent approaching $98 is a regime shift that fundamentally changes the inflation and rates narrative. OPEC 's 188K bpd July increase is entirely irrelevant against the backdrop of potential dual-strait closure, and Saudi OSP cuts are noise drowned out by hard supply disruption risk.

FLOWS AND POSITIONING

Goldman Prime data showing hedge funds bought global equities at the fastest pace in four months through June 4, just days before a 4.2% Nasdaq flush, means the institutional community entered Friday's selloff with elevated gross and net long exposure. The unwind is likely incomplete given the speed and concentration of the move.

Gamma has rotated to neutral, eliminating the mechanical stabilizer that dampened realized vol during the recent rally. Below SPX 5735, dealers flip negative gamma and become forced momentum sellers, creating a non-linear vol amplification risk. Last Friday's record 4.4 million SPX put contracts (64% 0DTE), $17B in leveraged ETF forced selling, and a 99th-percentile SPX/equal-weight return spread confirm the structural fragility is real and not yet fully cleared. CTA and vol-control funds remain the next shoe to drop should weakness become directional rather than episodic.

FLOWS REGIME ANALYSIS

Regime: Fragile

The Fragile regime flagged 72 hours ago has not resolved, it has metastasized. Friday's session converted the theoretical fracture points into realized damage, and the setup arriving into this week is materially worse on almost every dimension. Gamma has retreated from its stabilizing long position into a neutral range, stripping out the dealer hedging buffer that kept realized vol compressed through the AI-driven melt-up. The market now sits roughly 50 basis points above the 5735 strike where dealer positioning turns actively negative and vol amplification becomes the base case rather than the tail.

The geopolitical overlay complicates the picture severely. Simultaneous reported closures of the Strait of Hormuz and the Bab el-Mandeb have driven WTI north of $95 and Brent briefly to $98, and while ceasefire signaling is tempering the initial spike, the structural bid under crude does not go away on rhetoric alone. That energy reprice feeds directly into Wednesday's CPI, already expected at 4.2% year-over-year, meaning every dollar higher in WTI tightens the Fed's bind further and makes the rate-hike repricing already showing up in the forward curve more durable rather than episodic.

The open buyback window is the one structural bid still operating cleanly, but corporate repurchase flow is a decelerant, not a reversal mechanism when a geopolitical supply shock, a neutral gamma environment, residual CTA and vol-control deleveraging risk, and a record-put-volume hangover are all present simultaneously. Apple's WWDC is the last standing AI sentiment anchor this week, but the bar for that event to meaningfully offset the macro headwind stack is extremely high given that the AI narrative itself was already repricing on Friday's concentration unwind. The $58 billion 3-year auction Tuesday adds another test before CPI even prints, probing whether demand holds as the market begins pricing hikes rather than cuts. Friday was a positioning reset, not a clearing event, and the event stack from here requires dip buyers to earn conviction with clean data they do not yet have.

Cross-Asset Divergence: Partial divergence. Credit spreads remaining stable is the one cross-asset anchor still withholding full bearish confirmation, but the dollar's stable bid tilts incrementally toward the risk-off side of the ledger. The combination of a crude shock, hike repricing in the forward curve, and neutral gamma is the kind of macro configuration that has historically pulled credit spreads wider with a lag rather than in real time.

Positioning: Maintain defined-risk downside via SPX or NQ puts targeting a move through 5735, with Wednesday's CPI as the primary binary and the buyback bid providing the tactical ceiling on any pre-CPI drift higher.

Invalidation: A clean, verified ceasefire confirmation that materially reverses the crude bid ahead of Wednesday's CPI print, or a CPI print below 4.0% that removes the hike-repricing narrative and stabilizes the rate overlay while credit spreads hold or tighten.

10

4

22

3,288

Michael Deitsch retweeted

Iran and Israel are at it again. South Korean markets triggered a circuit breaker overnight and the KOSPI plunged over 8% at the open. Semis got torched on Friday and the Indexes did something we've seen a lot of over recent years; grind higher in a trend and then unravel all at once.

Was Friday the start of an unraveling that has legs? We do not know yet. What we do know is that for now you have a two-way tape in the equity indexes. A short-term top is at least in and the question this week is whether the bears can build on it. Wednesday's CPI data is going to be critical in answering that.

From a price structure standpoint, here is how I am looking at it. We are in a battle between the monthly opens and the weekly opens. All the monthly charts on the indexes are currently negative for the month. But the weekly opens from Sunday night have since pushed higher. So let us keep it simple. If we can go positive on the month in the Nasdaq, S&P, Dow, and Russell at some point this week, I think that brings us right back up toward all-time highs. If we rally back to unchanged on the month and then fail and go negative on the week, that is a very bearish signal and I think we could be headed meaningfully lower from there.

The key levels I am watching across all the indexes are the one standard deviation levels off the year to date anchored VWAP. We were hanging up near three standard deviations, have since crossed below two standard deviations, and if we are going to continue trending higher I would not be surprised to see a dip all the way down to one standard deviation first. That comes in at 7,300 on the ES and 28,450 on the NQ. Any quick flush down to those areas I am looking for long opportunities for at least a rotation trade.

On metals, copper remains my favorite in the space above everything else. Silver and gold charts look sideways and choppy to me, and if indexes continue to struggle I do not love either of them. Copper got hit hard on Friday when semis got whacked but I think that is an opportunity to buy the dip. As long as copper holds above $6 I think it continues to push higher and I think we see a $7 handle on it. I am currently long copper via ETFs and will continue to look to buy dips in futures during the day as well. Not an easy market to hold futures in so I am using a combination of ETFs and intraday futures positions.

The bond market still looks heavy but it is a tough call right now because CPI Wednesday could change the picture entirely. Let us also get through the first meeting with Warsh and see where his head is on all of this. There is no question inflation is still a problem but President Trump said this week there is no reason to hike rates, which essentially telegraphs that the Fed is not going to hike. So there is that.

Ease your way into this week. The markets are busy even though it is summer. Stay focused, stay disciplined, and keep it light and tight.

Catch me live at 8 ET on @NTLiveMedia — full market breakdown, what I'm watching, and what's next.

🎥 Watch live here: youtube.com/live/pTmp6Qqx2x0…

Want this in your inbox every morning? It's free: anthonycrudele.com/newslette…

Cheers, DELI

2

6

47

9,264

Michael Deitsch retweeted

Jun 5

Many semiconductor, rare earth, space, and quantum stocks are down over 20% this week.

I told you EXACTLY when it was going to happen.

Nobody on Fin𝕏 calls tops and bottoms more accurately than me.

32

9

221

30,987

Michael Deitsch retweeted

Jun 3

Starting to think this is SpaceX IPO liquidity rebalancing.

A lot of random moves out there today

34

10

512

84,591

Michael Deitsch retweeted

Jun 1

On Wednesday, I shared 16 breakout charts with my subscribers.

After just 4 trading days later, the results are amazing.

Imagine what we could achieve in an entire year.

x.com/BeardoTrader/creator-s…

16

3

65

8,401

Michael Deitsch retweeted

May 28

The Trump Administration Is in Talks to Fund U.S. Drone Companies: WSJ

155

205

2,803

942,640

Michael Deitsch retweeted

May 27

"If breaking even is a loss for me, I'm going to live a very wealthy life."

@paxtrader777

2

24

2,713

Michael Deitsch retweeted

May 27

The stock market over the last couple months

5

4

46

6,380

Robotics is picking up but we’ve seen nothing yet.

Quantum, nuclear, flying taxis, and the other speculative themes have been fun but I strongly believe robotics will be bigger than every theme we’ve seen so far in this AI driven bull market.

57

42

712

87,973

Michael Deitsch retweeted

May 21

MORNING MARKET BRIEF

Thursday, May 21, 2026

TL;DR

1/ Iran's Supreme Leader blocking uranium exports has killed the clean Hormuz reopening thesis, and the oil supply case is structurally more bullish than spot positioning reflects.

2/ Momentum factor exposure at the 95th percentile is now synonymous with the AI trade and the index itself, and NVDA's failure to spark a fresh leg higher means the crowded long has no remaining catalyst to hide behind.

3/ The regime is Fragile and fully exposed: OPEX, VIX expiry, and earnings are cleared, so markets now have to price yields, sticky inflation, and unresolved geopolitical risk on their own.

4/ Fade equity strength into the 9:45 US PMI print with shorts concentrated in the highest-skew AI and megacap names; use the buyback window to avoid aggressive index-level shorts, not as a reason to add longs.

5/ Euro area PMI collapsing to 47.5 guts the hawkish ECB narrative and the stagflation read is hardening, not softening.

KEY THEMES

Crude's bid-side volatility this morning says everything about where macro risk is concentrated: Iran's Supreme Leader reportedly blocking the export of near-weapons-grade uranium has punctured the market's embedded assumption of a clean, near-term Hormuz reopening, and with Brent already 40% above pre-war levels and global inventories drawing at a record pace, the asymmetry on oil to the upside remains uncomfortably real. That's particularly true as China's crude imports track toward a 10-year low, suggesting demand destruction is already doing some of the work the diplomats aren't. The Hormuz repricing is feeding directly into European stagflation dynamics, where this morning's euro area composite PMI collapsed to 47.5 and France cratered to 43.5 -- a data set that guts the hawkish ECB narrative and forces a reassessment of how aggressively Frankfurt can tighten into an energy-driven recession. Layered on top of all of this is a fragile equity structure: momentum factor exposure sitting at the 95th percentile is now explicitly synonymous with the AI trade and therefore with index performance itself, with both Morgan Stanley and Goldman flagging a multi-week unwind cycle that has historically run 6-7 weeks and cost the long leg roughly 21%. Nvidia's failure to spark a fresh leg higher overnight confirms the crowded long is looking for an exit, not a catalyst. For futures traders, the setup favors fading equity strength into the US PMI print at 9:45 while watching crude for any incremental headline resolution from Tehran that could violently reprice the vol embedded in energy contracts.

MARKET SNAPSHOT

The post-NVDA price action is telling: a clean earnings beat failed to catalyze fresh AI-driven equity gains, S&P futures are down 0.4%, and oil has rebounded 2% above $107. The asymmetry between fading equity momentum and rising commodity and yield pressure is the dominant overnight setup heading into the cash open.

MACRO

Iran's acknowledgment that it is actively reviewing and responding to a U.S. proposal -- combined with accelerated Pakistani mediation -- signals the most tangible diplomatic progress yet, though the pace remains deliberate rather than imminent. Watch oil for a knee-jerk move if any formal announcement of understanding emerges.

The Eurozone composite PMI collapsed to 47.5 in May, with France cratering to 43.5. The data confirms the ECB is caught in a classic stagflationary trap, and the hawkish rate path currently priced by markets looks increasingly at odds with a region that may already be in contraction.

CORPORATE

Deere's construction and forestry outperformance offsetting agricultural weakness reflects a deliberate diversification that is working as designed, though the narrowed $4.5-5B full-year guidance range signals management caution on the farm economy recovery timeline.

Lilly's retatrutide Phase III data showing ~28% average weight loss at the high dose -- with 45% of patients hitting bariatric surgery-level outcomes -- meaningfully raises the efficacy ceiling in the GLP-1 space and strengthens Lilly's competitive positioning against Novo Nordisk ahead of any potential approval catalyst.

Walmart's 4.1% comp beat offers a cautiously constructive read on the U.S. consumer, but management's own commentary draws a sharp bifurcation: high-income households spending with confidence while low-income consumers are in "financial distress." Top-line resilience may be masking underlying demand stress at the margin.

SpaceX's IPO -- the largest public offering on record -- is extending retail access at institutional pricing across major brokerages, a structural shift that could generate significant inflows and retail momentum. Watch for outsized demand dynamics given the brand's cult following relative to traditional IPO price discovery.

COMMODITY

Chinese crude imports tracking toward a 10-year low in May, running over 4 million b/d below pre-war levels on a four-week average, is the single most important demand-side offset to the Hormuz supply shock. Without China re-entering as a buyer at scale, any supply normalization scenario faces a significantly softer price floor than bulls anticipate.

Iran's Supreme Leader directive to retain near-weapons-grade uranium domestically is a significant negotiating red line that directly undermines the market's base case for a swift Hormuz resolution. Combined with ADNOC's assessment that full flow recovery extends into 2027 and Goldman's data showing record inventory drawdowns, the structural oil supply case is far more bullish than spot positioning implies.

Oil market complacency around a clean Hormuz reopening remains the key risk. The market is essentially pricing a short, contained disruption, but McNally's warning flags a potential repricing event if negotiations stall or the closure extends materially beyond consensus expectations.

FLOWS AND POSITIONING

Momentum factor exposure sits at the 95th percentile per MS Prime Brokerage, with historical analogs pointing to a 6-7 week unwind of ~21% on the long leg. Critically, since Momentum is now effectively the AI trade and the AI trade is the index, any sustained factor mean-reversion carries systemic market risk well beyond quant desks.

KEY EVENTS

Key data and event risk today: Initial Jobless Claims and PMIs at 08:30/09:45 will set the tone for growth expectations, while Fed's Barkin at 12:20 and the 10-Year TIPS auction at 13:00 provide dual read-throughs on the rate and real-yield outlook.

FLOWS REGIME ANALYSIS

Regime: Fragile

The regime remains FRAGILE, but the risk architecture has rotated meaningfully overnight. Yesterday's fragility was centered on sequential catalysts -- the 20-year auction, Fed minutes, NVDA earnings -- that could either validate or reset the setup. Today those catalysts are cleared, which means the market is now fully exposed to the underlying structural vulnerabilities without any near-term event to anchor positioning around.

The window of weakness is fully open. OPEX, VIX expiry, and NVDA earnings have all passed, removing the mechanical volatility suppressants that kept the structure from expressing itself freely. From here, markets are forced to price the fundamental reality of yields moving higher, sticky inflation, and geopolitical strain that has not eased.

NVDA's failure to spark a fresh leg higher is the most important signal from the last 24 hours. The crowded long in AI and megacap names now has no remaining catalyst to justify holding at these upside skew levels, and with momentum factor exposure at the 95th percentile and explicitly synonymous with index performance, the Morgan Stanley and Goldman-flagged multi-week unwind cycle has the conditions it needs to begin in earnest.

The vol regime compounds this. The VIX reading in the 18-25 range reflects a market where fear of missing upside has crushed downside protection to its fourth lowest single-stock skew reading in 20 years. The surface calm is a structural vulnerability, not a genuine stability signal.

The Iran-Hormuz headline is the geopolitical accelerant. The Supreme Leader blocking near-weapons-grade uranium exports has closed the door on a clean Hormuz reopening, Brent sits 40% above pre-war levels with inventories drawing at a record pace, and crude's bid-side volatility this morning is repricing energy risk in real time directly into European stagflation dynamics. The euro area composite PMI collapsing to 47.5, with France cratering to 43.5, guts the hawkish ECB narrative and forces the question of how much tightening Frankfurt can deliver into an energy-driven recession -- which feeds back into global growth expectations and pressure on EM energy importers.

The US PMI print at 9:45 is the next live test. A weak number accelerates the dollar bid against EM FX and validates the global slowdown read, while a strong number creates a momentary confusion trade before yields reassert as the dominant equity headwind.

Cross-Asset Divergence: Credit spreads remain stable with no systemic stress signal -- the one piece of the architecture that argues against a disorderly unwind -- but the dollar's firm bid against energy-importing EM pairs like INR while remaining mixed against DM is a selective pressure signal that hardens materially if the US PMI disappoints and global growth concerns accelerate into a broad dollar bid.

Positioning: Fade equity strength into the 9:45 US PMI print with short exposure concentrated in the highest-upside-skew AI and megacap names where the unwind cycle has the most fuel. Use the open buyback window as a reason to avoid outright aggressive index-level shorts, not as a reason to add longs.

Invalidation: A credible Iran-Hormuz diplomatic resolution headline that reverses crude's bid and removes the geopolitical risk premium from energy, or a US PMI print that meaningfully beats and reframes the global growth slowdown narrative before the momentum unwind builds momentum of its own.

1

4

19

2,451

Michael Deitsch retweeted

May 19

👇

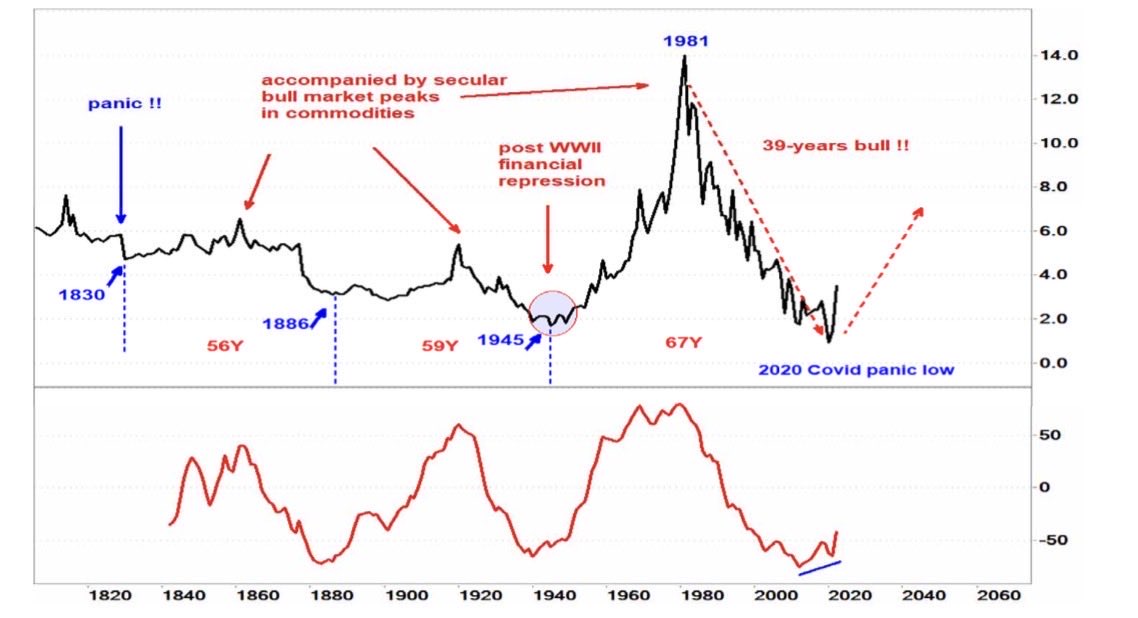

WHAT IF the biggest bubble of our lifetime isn't crypto?

Not AI stocks.

Not real estate.

What if it's the one asset every pension fund, every retiree, every "safe" portfolio is loaded with?

Bonds.

200 years of rate cycles say the same thing:

Every peak lasts 56–67 years.

The 1981 top was 14% yields.

The 2020 bottom was 0%.

39 years of falling rates just ended.

What if we're now at the start of the next 50-year cycle — upward?

Most investors have never managed money in a rising rate world.

Their entire career happened inside the bull.

The unwind has barely started.

And no one is talking about it.

24

21

338

110,688

Michael Deitsch retweeted

May 19

MORNING MARKET BRIEF

Tuesday, May 19, 2026

TL;DR

- Semis are the macro tell and the unwind is just getting started: record crowding, no downside protection, and leveraged ETF mechanics that turn a 2% down day into $4B of forced selling into the close.

- The BofA FMS is a textbook late-cycle crowding signal: biggest single-month equity allocation jump in history, Bull & Bear at 7.8/8.0, 73% of managers already flagging long semis as the most crowded trade.

- CTAs flipped to modest buyers near-term, but a down month still unlocks $30B of programmatic selling, so they cushion a benign tape and accelerate a drawdown.

- Wednesday's triple stack of the 20-year auction, FOMC minutes, and NVDA earnings is the week's maximum risk density point, and the SOX breakdown is arriving ahead of it, not after.

- Hold reduced gross longs, add targeted short exposure in semis or SMH on any morning bounce, and do not step in front of Wednesday without a hard stop above the SOX trendline break level.

KEY THEMES

Semis are the macro tell this morning, and the unwind is just getting started. Goldman's prime book shows Asia Info Tech net allocations at record highs, BofA's Fund Manager Survey just printed the biggest single-month equity allocation jump in its history with the Bull & Bear indicator at 7.8/8.0, and 73% of respondents are already crowded into long semis, yet almost no one bothered to buy downside protection. Now the SOX is breaking its melt-up trendline with vol skew at the 100th percentile and roughly $100B in leveraged ETF long exposure sitting underneath, meaning the same gamma mechanics that mechanically added $4B on up days can flip into equally aggressive forced selling. A 2% down day doesn't just hurt, it feeds on itself. CTA positioning offers a partial offset near-term (modest buying across flat and up scenarios over the next week), but a sustained drawdown unlocks $30B of systematic selling on the monthly horizon, which is where the real tail risk lives. Against that backdrop, the Blackstone-Google neocloud JV is a structural reminder that AI capex remains the secular anchor even as the momentum trade cracks, while Home Depot's soft top-line miss alongside inventory well below estimates suggests the consumer discretionary backdrop is more fragile than the equity rally has been pricing.

MARKET SNAPSHOT

Semis momentum is rolling over into a positioning and leverage overhang that leaves the sector acutely vulnerable. Gold approaching a major technical inflection adds a safe-haven dimension, while Europe's macro fragility and building geopolitical stress remain underappreciated tail risks for global risk appetite.

CORPORATE

The Blackstone-Google neocloud JV is a major structural signal for AI infrastructure capital allocation. BX's $5B equity commitment combined with direct TPU access outside standard GCP channels creates a new class of institutional AI compute provider, likely pressuring hyperscaler pricing power while validating the multi-year capex super-cycle thesis for data center and power infrastructure plays.

Home Depot's Q1 print is a soft beat on EPS but a miss on revenue and comps. US same-store sales of just 0.4% against a 0.88% estimate signals still-subdued consumer spending on big-ticket home improvement, though the full-year guidance hold and inventory coming in well below estimates suggest management is running lean and protecting margins rather than betting on a demand recovery.

COMMODITY

The Indonesian NPI cut is a supply-side shock in the world's largest nickel producer. With ore shortages and power reallocation to aluminum already straining output since Q1, the rotational maintenance announcement represents structural tightening rather than a one-off disruption, keeping nickel supported and adding upward pressure to stainless steel input costs.

FLOWS AND POSITIONING

Goldman's CTA model has shifted from net seller to modest net buyer across flat and up SPX scenarios over the near term, a constructive evolution from last week. The critical asymmetry remains, though: a down-month scenario still carries ~$30.5B of programmatic selling, meaning CTAs provide a marginal cushion in a benign tape but act as an accelerant in any meaningful drawdown.

SOX breaking its melt-up trendline and slipping below the 8-day MA is technically significant, but the real risk is mechanical. Roughly $100B in leveraged ETF semi exposure generating ~$2B/day of short gamma means a 2% down day can trigger ~$4B of forced selling into the close, creating a self-reinforcing feedback loop in a sector where virtually no downside protection was purchased at peak implied vol.

The BofA FMS is flashing a textbook late-cycle crowding signal: a single-month equity allocation surge of unprecedented magnitude, cash at near-depleted levels, and a Bull & Bear indicator at 7.8/8.0. With 73% of managers already flagging long semis as the most crowded trade, the marginal buyer is increasingly scarce and the unwind risk is asymmetric.

Asia Info Tech allocations at GS Prime have reached record highs on both a gross and net basis. The buying was overwhelmingly long-driven rather than short-covering, suggesting conviction accumulation rather than technical repositioning, though record concentration amplifies drawdown risk if the sector rolls.

KEY EVENTS

Key events today: Fed's Waller speaks (watch for any recalibration of the rate path given recent data), ADP weekly jobs and Pending Home Sales ( 1% est.) offer incremental read-throughs on labor and housing, and $85B in 6-week T-bill supply tests front-end demand.

FLOWS REGIME ANALYSIS

Regime: Fragile

The regime remains FRAGILE, but the risk profile has sharpened materially overnight as the SOX breakdown and leveraged ETF mechanics introduce a new amplification vector not fully priced into yesterday's read. VIX expiry at the open removes the final near-term pinning mechanism still in place at yesterday's close, and the window of weakness is now fully open with no structural cushion remaining from the expiry cycle. The positive gamma residual that still broadly characterizes equity index positioning is decaying, not reinforcing, and the SOX breaking below its steep trendline while slipping under the 8-day moving average is a direct warning that the sector driving the melt-up is in technical deterioration.

The leveraged ETF structure in semis is the critical mechanical risk: roughly $2B of daily short gamma means a 2% down move triggers approximately $4B of forced selling into the close, and with the crowd still positioned for upside rather than protection (SMH 3-month ATM implied vol at the 100th percentile with no put-chasing), the unwind has no natural offset from defensive positioning. Waller's speech this morning is the first live catalyst: any signal that he has moved toward a more hawkish construct locks in a more difficult path for incoming Fed Chair Warsh to build consensus for easing, and that repricing feeds directly into the MOVE index dynamic that already spiked on Friday. Wednesday's triple-event stack of the 20-year auction, FOMC minutes, and NVDA earnings after the close remains the week's maximum risk density point, and the SOX technical breakdown arriving ahead of that cluster rather than after it is the tape telling you the unprotected structure is already being tested. The buyback window remains the one durable bid, but corporate flow alone cannot absorb the mechanical selling pressure that emerges if semis extend lower and leveraged ETF rebalancing kicks in at scale.

Cross-Asset Divergence: Credit spreads holding stable and the dollar firming (rather than spiking) suggest systemic stress is not yet generalized, but the MOVE spike combined with the SOX breakdown creates a rates-to-equity vol transmission channel that credit spreads have not yet reflected and likely lag.

Positioning: Hold reduced gross long exposure from yesterday's read, add targeted short exposure in semis or SMH on any morning bounce, and do not step in front of Wednesday's catalyst stack without a hard stop above the SOX trendline break level.

Invalidation: Waller's remarks are explicitly dovish and bond markets stabilize ahead of Wednesday's auction, cooling MOVE and capping VIX below 20; or NVDA pre-positioning (options flow, commentary) into Wednesday's close signals the Street is pricing in a beat with enough conviction to reverse the SOX technical breakdown.

2

2

31

3,167

Michael Deitsch retweeted

May 18

$SPX -Closed the day barely down after a big intraday bounce. We have a potential 17 trading day low today which could propel the market to a new ATH by Friday if the market likes NVDA's earnings. On the other hand breaking today's low will confirm that a pullback is in progress.

7

10

161

10,893

Michael Deitsch retweeted

May 18

MORNING MARKET BRIEF

Monday, May 18, 2026

KEY THEMES

Geopolitics is now doing the Fed's work for it - the Iran-Hormuz standoff has Brent above $110 and 30-year yields at levels unseen since 2007, as energy-driven inflation repricing tears through sovereign bond markets globally, with Japan's ultra-long end delivering the sharpest signal that the "higher for longer" regime has room to run further. That bond market message collides directly with positioning: 80% of surveyed fund managers expect equities to outperform, JPM is chasing Nasdaq momentum, and SPX just notched its first back-to-back loss in May - a market structure where gamma flipped neutral at the open after $5.1bn in strikes expired Friday, meaning dealers no longer provide the stabilizing cushion that supported the seven-week melt-up. Hartnett's late-cycle warning deserves weight here: the SOX-led AI euphoria, stretched household equity wealth, and yields breaking decade-plus resistance levels have historically marked speculative peaks, not mid-cycle consolidations - and with Yardeni calling for a July hike and the Fed minutes plus NVDA earnings both landing Wednesday, traders should respect the asymmetry between a crowded long positioned for AI continuation and a macro backdrop that is actively breaking down the rate assumptions that justified those multiples.

MARKET SNAPSHOT

The Treasury market is absorbing dual pressure from oil-driven inflation risk and a heavy issuance calendar ($40bn IG corporate supply, $16bn 20-year auction, $19bn 10-year TIPS reopening this week), while the brief JGB 30-year spike of 20bp is a reminder that the global duration selloff retains the capacity for disorderly moves; US 10-year holding near 4.6% will be the intraday gravity point.

Markets are pricing a coherent risk-off narrative: SPX futures -0.5%, Brent above $110, JGB 30-year 20bp intraday (partially reversed), and dollar set to snap a five-day win streak - the convergence of Middle East stalemate, exhausted AI momentum, and the global bond selloff's belated equity catch-up is the dominant theme heading into Monday's open.

MACRO

The synchronized selloff in 30-year yields globally - U.S. at 2007 highs, Germany at 15-year highs, Japan at all-time highs for the maturity - reflects a structural repricing of the long end driven by energy-fueled inflation expectations and sovereign supply concerns, not a transient technical move; with G7 finance ministers convening against this backdrop and Brent above $110, the risk of a disorderly yield overshoot before a policy response materializes is elevated.

China's retail sales deceleration across 10 of the last 11 months, combined with slowing investment growth and negative new loan creation, confirms that the rebalancing toward consumption-led growth is failing to gain traction - further stimulus is likely necessary to defend the growth target, but monetary transmission remains impaired.

The Bain/StanChart forecast of 100 TWh demand growth and $200bn capex requirements across SE Asian data centers, EVs, and green industrial parks over the next three to four years represents a durable structural tailwind for regional power infrastructure and grid-adjacent plays, with data center operators willing to pay a premium for speed of connection - effectively pricing in supply scarcity.

Yardeni's call for a July hike with a tightening bias flagged at June materially shifts the rate path consensus; if correct, the market's current assumption of a benign Fed pause is mispriced and would pressure duration and equity multiples simultaneously.

Iran's published rejection of U.S. terms - no asset releases, uranium transfer demands, single-facility cap, and cross-front ceasefire linkage - signals the gap between the two sides remains structurally wide, reducing near-term probability of a Strait of Hormuz resolution and keeping an oil risk premium embedded in markets.

CORPORATE

The Musk complex - Tesla and SpaceX - is being sustained by "optionality" valuation frameworks and FOMO-driven analyst willingness to project far-future cash flows, a methodology that historically signals late-cycle speculative excess; a SpaceX IPO targeting $2 trillion would test institutional appetite for transformational-premium pricing at a moment when risk sentiment is already fragile.

COMMODITY

The UNH/Berkshire exit, DAL stake, and REGN trial miss are equity-specific corporate events rather than commodity flows; the Berkshire UNH exit at scale warrants attention as a potential signal on healthcare sector valuation, while the REGN -10% on Phase 3 failure is a binary biotech event rather than a systemic read.

The White House confirmation of $17bn in annual U.S. agricultural purchases by China through 2028 - on top of existing soybean pledges - delivered the specific headline the grain markets required; corn 3.8% and wheat 3.4% intraday represent a direct reversal of last week's trade-detail disappointment and reinforce that U.S.-China agricultural flows are a meaningful geopolitical stabilizer.

FLOWS AND POSITIONING

JPM Cross-Asset maintains a momentum-chase posture in Nasdaq and AI/large-cap quality, but explicitly flags crowding in semis versus software and recommends selective hedges - a nuanced signal that the desk is not calling a top but is trimming tail risk exposure in the most extended names.

With an estimated $5.1bn in SPX gamma expiring Friday versus only $1.1bn rolling, the supportive dealer hedging flow that has suppressed volatility is largely reset; gamma flipping negative below 5,100 means dealers will amplify rather than dampen downside moves from that level, making the strike re-anchoring this week a critical technical watchpoint.

Hartnett's "Door to Doom" framework identifies a 1999-style melt-up dynamic where AI euphoria, surging long-end yields, sticky inflation above 5%, and extreme semiconductor concentration are converging - the risk is not immediate collapse but a fragile boom loop that becomes self-reinforcing until bond market pressure breaks the equity feedback mechanism.

The Bloomberg buy-side survey reveals a crowded consensus: 80% bullish equities, ~50% concentrated in megacap tech/AI, with near-zero allocation conviction in bonds or cash - a positioning setup that historically elevates correction risk when sentiment is the primary driver rather than fundamentals.

KEY EVENTS

Key risk events cluster mid-to-late week: Fed minutes and the 20-year auction on Wednesday are the primary rate market catalysts, NVDA earnings Wednesday after-close will serve as the definitive AI sentiment test, and the Putin/Xi meetings Monday through Tuesday carry geopolitical optionality for energy and broader risk sentiment.

1

10

2,311