Rolling recession since 2022. Liquidity turning. AI | Energy | Infrastructure Capital cycles | Family offices | Long-duration capital.

Joined August 2014

- Tweets 2,737

- Following 282

- Followers 780

- Likes 10,245

42 Photos and videos

Pinned Tweet

Feb 25

The world isn’t short on ideas.

It’s short on infrastructure.

AI isn’t just software.

It’s power.

It’s water.

It’s transmission.

It’s capital cycles.

We are entering a decade defined by:

• Energy re-industrialization

• AI compute buildout

• Monetary regime stress

• Infrastructure bottlenecks

• Capital reallocation into hard assets

I focus on the intersection of:

Macro cycles × AI infrastructure × Energy × Alternative assets.

If you’re thinking in 10–20 year horizons instead of 10–20 day trades, we’ll get along.

5

6

48

36,716

Jun 12

The interesting part isn’t the AI.

It’s the bet that AI can finally lower the cost of physical production.

If that happens, the next productivity boom won’t come from software.

It will come from factories, energy, and infrastructure.

Jun 12

Jeff Bezos just bet $12 billion that you'll be able to support your whole family on a single paycheck again.

his reasoning: AI will let companies make more stuff with fewer people and less money.

and when something gets cheaper and easier to produce, and lots of companies can do it, they compete and the price drops.

it's why a flatscreen TV that cost $2,000 a decade ago is $300 today.

bezos thinks AI will do that to almost everything you buy.

in his words, it raises "the basket of goods people can afford."

your paycheck buys more without anyone handing you a raise.

the problem: look at which prices have actually dropped.

so far, AI has only made *digital* things cheap, like code and content.

but the stuff that really eats your paycheck is *physical*.

rent, cars, medicine. cheaper code doesn't lower your rent.

that's exactly what bezos just spent $12B on.

Prometheus, his new company, is building AI tools that help engineers design and manufacture physical products faster

things like cars, machines, and medicine.

the goal is to make building physical things as fast and cheap as writing software.

if it works, 1 income starts covering what used to take 2.

which is when his prediction kicks in:

"perhaps one of those earners will choose not to be in the job market, so they'll become a one-earner household." or "some people who are working overtime will stop working overtime, because they don't want to."

one paycheck covering a whole family again, like the 1950s.

49

Jun 11

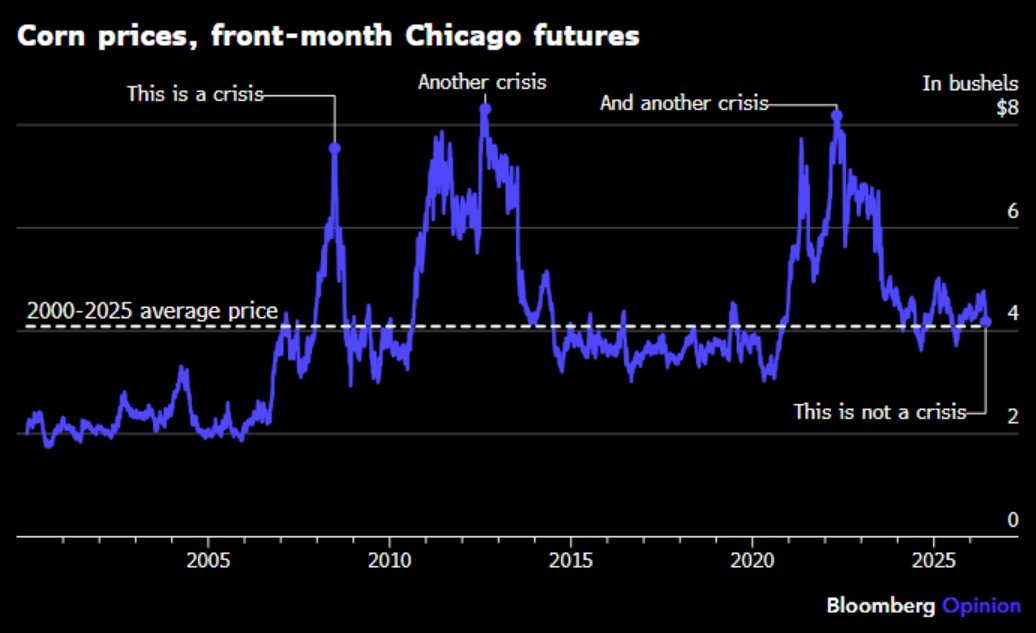

The market has a habit of pricing permanent shortages that turn out to be temporary bottlenecks.

Corn isn’t the only example.

Cycles usually break the consensus eventually.

Jun 11

CHART OF THE DAY: Corn prices have fallen now to an 8-month low of $4.17 a bushel (it's down ~50% from its 2022 peak).

Quite a contrast with the apocalyptic warnings of a food crisis, shortages and even famine made by many armchair experts (and the odd university professor).

53

Jun 11

Something changed.

Bitcoin isn’t just going up.

It’s building an entirely new ownership base.

The amount of capital flowing into new whale wallets is accelerating, not fading.

That usually happens when larger pools of money decide an asset belongs in the system.

18

Jun 11

Rare capitulation signals have historically looked more like exhaustion than the beginning of major bear markets.

71% of the time the S&P was higher a year later.

The catch?

The average path still included another ~10% drawdown.

Markets rarely make turning points comfortable.

SwiftMacro Rare capitulation signal. On the ~41 prior instances (24 episodes), SPX was higher 12 months later 71% of the time ( 9.7% avg), though with ~−10% interim drawdowns.

These have mostly marked panic lows/exhaustion rather than major bear starts. Short-term rebounds common after such sharp drops. Exact 1w/1m/3m/6m averages vary by study but tilt positive. Macro context key. Not advice.

60

Jun 10

The interesting number here might be productivity.

If productivity is accelerating while labor costs stay contained, this may not be the inflation cycle people think it is.

Jun 10

Employment Friday delivered one of the strongest jobs reports in recent memory. Non-farm payrolls came in at 172,000, blowing past the 88,000 expectation. Upward revisions added another 93,000. Wages grew at ~0.3%.

The market sold off anyway.

@CathieDWood thinks investors have the story backwards. Productivity is running near 3%. Unit labor costs are near half a percent. She says that is not an inflationary setup but a boom with contained costs.

The yield curve is flattening despite a ~55% surge in oil prices over three months. The bond market is not buying the inflation narrative. Neither are we. If the Iran war resolves and oil pulls back, inflation could go negative this year.

Capital spending has broken out of a 30-year range. The AI infrastructure buildout is creating a ripple effect across manufacturing. SpaceXAI built Colossus for roughly $30 billion and Anthropic is paying $15 billion a year to use it. We believe the returns on this infrastructure are unlike anything in prior technology cycles.

On the dollar, gold, and the inflation trade: prediction markets are pricing in a US Dollar Index reversal toward 101.9, gold peaked the day Kevin Warsh was appointed, and Cathie Wood believes the inflation trade may already be over.

From where we sit, the economy is healthier than the headlines suggest, inflation is lower than people fear, and the AI infrastructure cycle is just getting started.

25

Jun 10

Inflation was 2.4% in January. Now it’s 4.2%.

But this doesn’t look like 2022.

Core inflation is cooling. The economy is slowing. Most of the pressure is coming from energy and a war-driven supply shock.

The Fed can destroy demand.

It can’t produce oil, reopen shipping lanes, or end a conflict.

That’s the uncomfortable part.

The policy tool and the problem may not be the same thing.

12

Jun 10

Markets keep treating inflation like a demand problem.

Lately it’s looked much more like a logistics problem.

If shipping, insurance, and energy normalize, a lot of that pressure disappears with them.

Jun 10

CORE INFLATION SIGNALS PEAK MAY BE PASSING

John Briggs, head of US rates strategy at Natixis North America, says the softer month-on-month core inflation reading may indicate the peak of war-driven inflation has passed. He adds this could support a more favorable inflation outlook ahead, but warns the trend depends on oil prices remaining stable and not reigniting inflationary pressure.

41

Douglas Swift retweeted

Jun 9

The market sold off on the strongest jobs report in months.

@CathieDWood thinks the bears are looking at the wrong data. Productivity has been crushing labor cost pressures. The yield curve is currently flashing deflation. And the day Kevin Warsh was appointed, gold peaked.

One framework sees a trap. Ours sees a boom.

4

5

45

14,927

Douglas Swift retweeted

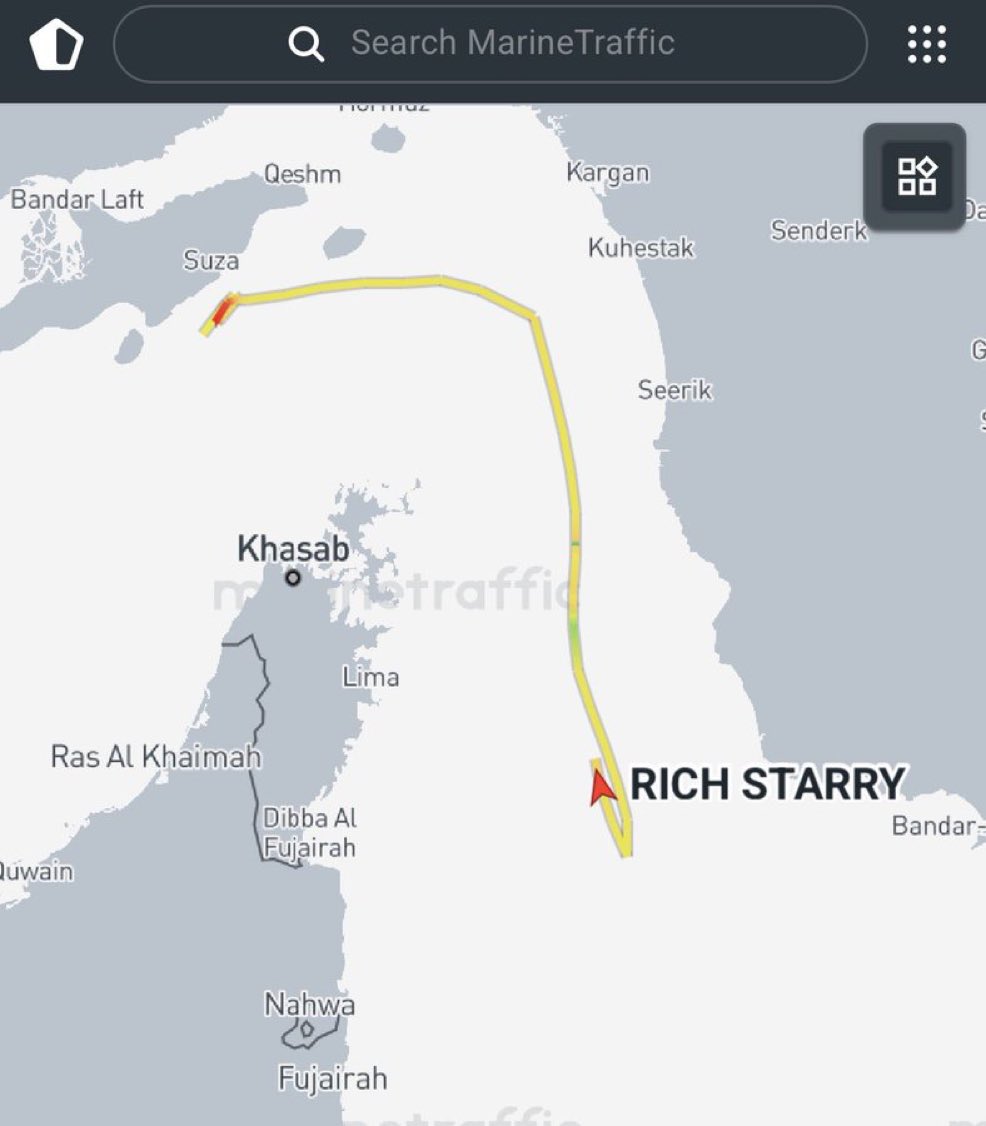

Iran shut the Strait of Hormuz to choke the world.

100 days later, the economy choking hardest is its own.

Iran is losing on every front that can be measured, and its one piece of leverage is quietly failing. Oil has fallen about 20% from its wartime peak even with the strait still closed, OPEC has opened the taps, and Asia is running on stored barrels. Meanwhile Iran’s own crude exports have collapsed to under 300,000 barrels a day, from 1.7 million before the war. It is strangling itself harder than anyone else.

Its supreme leader is dead. By Trump’s own count nearly 80% of its missiles are spent, the factories that built them in ruins. And the asking price gives the game away. Tehran now says there is no peace without the release of $12 to $24 billion of its own frozen money, half of it upfront, as a test of trust. Trump said no. Not a dollar before a deal. And the deal on the table requires Iran to clear its own mines from the strait within 30 days and reopen the very chokepoint it shut.

That is not a power dictating to the world. It is a cornered regime negotiating the terms of its own retreat.

It is also why Washington has spent months holding Israel back rather than letting it loose. Even after Iran’s missiles flew this week, the US pressed its closest ally to stand down, and the fighting paused within a day. That restraint is not weakness. It is the patience of the side that is already ahead.

Iran is not holding the world hostage. It is bargaining for the exit, and the West is setting the price.

184

111

560

95,916

Jun 9

Markets tend to underestimate infrastructure.

Semiconductors are only one layer.

You still have to build the power plants, transmission lines, substations, data centers, and supply chains.

That’s why this cycle may last a lot longer than Wall Street expects.

Jun 9

This bull cycle will last far longer than Wall Street expects.

There is no bubble. AI infrastructure and semiconductor demand are still in the early stages, supporting S&P 500 earnings growth toward $650 by 2031.

Inflation is not the issue many claim; a supply shock simply changes relative prices. Why does everyone forget their undergraduate economics?

Warsh is not a hawk.

We are also heading toward a constructive Iran deal that restores risk-on momentum.

Ignore the doomers. This cycle has substantial room to run.

39

Jun 8

People keep talking about inflation.

I’m watching production.

Steel imports are falling, domestic output is rising, and manufacturers are expanding capacity.

Cycles turn long before the headlines do.

manufacturingdive.com/news/s…

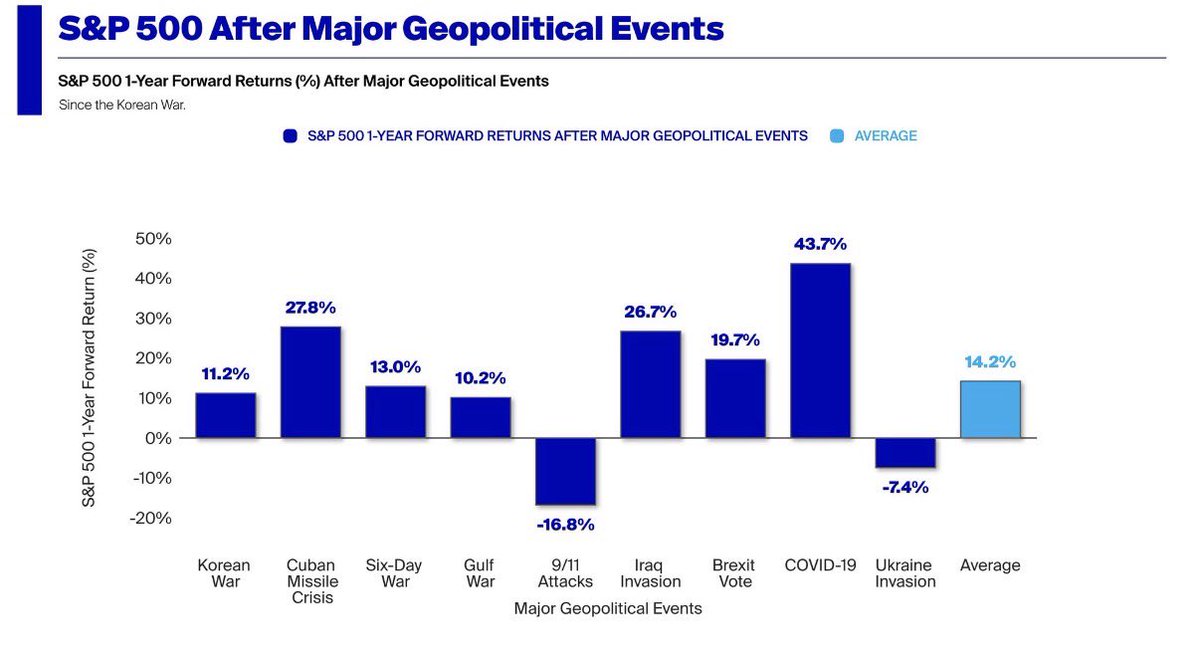

70

Jun 8

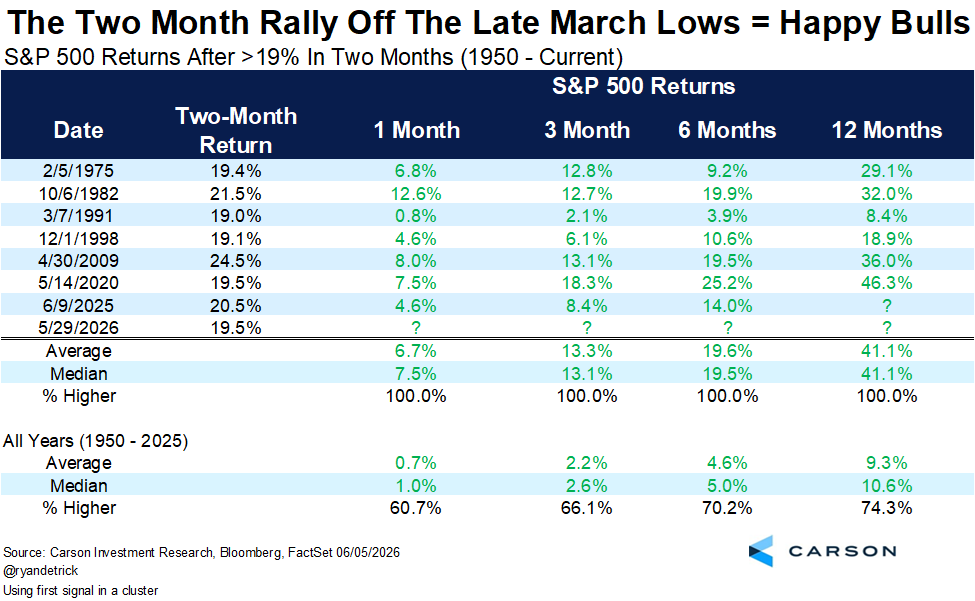

Something doesn’t line up.

The consensus spent months preparing for a recession while the market put together one of the strongest two-month rallies in history.

Maybe the recession didn’t disappear.

Maybe it already happened.

The S&P 500 recently was up more than 19% in two months.

You ready for this one? That has only happened seven other times and stocks were never lower 1 month, 3 months, 6 months, or a year later.

In fact, up more than 40% on average a year later. My oh my.

1

43

Jun 7

The labor market story has quietly flipped.

2023-24 relied heavily on government hiring and later suffered massive downward revisions.

Now government hiring is fading, private sector services are driving job growth, and revisions are improving instead of deteriorating.

A lot of people are still trading the old narrative.

In 2023, government added ~734k jobs out of ~2.5M total nonfarm payroll gains (~28-30%). Private sector led via health/education services ( 1.16M) and leisure/hospitality ( 487k).

In 2024, government slowed to 453k out of ~2M (~23%).

Today, government hiring has further decelerated (e.g. 66k over Mar-May 2026 per BLS), while private services—healthcare ( 198k) and leisure/hospitality ( 144k)—continue driving the majority of gains, matching the pattern in recent reports. (Note: later benchmark revisions lowered 2024 figures substantially.)

1

87

Jun 7

And unlike 2023-24, revisions are no longer consistently moving lower after the fact.

That’s a subtle change, but these shifts usually matter near turning points.

29

Jun 7

The interesting part isn’t USD/JPY at 160.

It’s that a yen carry unwind can create forced selling across global assets even when domestic fundamentals haven’t changed much.

Liquidity events tend to look like economic events until they don’t.

Last time USD/JPY broke above 160 (July 2024), the BOJ intervened and later hiked rates. This fueled a sharp yen rally and unwind of yen carry trades.

US impact was mostly short-term market volatility: equities sold off (Nasdaq saw steep drops in early Aug), VIX spiked, and bond yields fell before markets stabilized.

On trade, weak yen made Japanese imports cheaper (helping US consumers/importers in autos/electronics) while pressuring US exporters to Japan. No major lasting damage to the broader US economy.

67

Jun 7

People keep pricing the headlines.

Markets price the system.

If Hormuz can be disrupted and oil still struggles to hold a panic bid, that’s telling you global energy infrastructure is becoming more resilient than the consensus narrative.

Capital usually figures that out before economists do.

Jun 7

IRAN WAR UPDATE & WHY THE PRICE OF OIL KEEPS DROPPING

The media has not been covering this.

According to the U.S. CENTRAL COMMAND, approximately 1,000 commercial vessels have crossed through the Strait of Hormuz in the last two months.

Iran has not been able to do anything about it. And commercial traffic through the Strait is slowly increasing.

Meanwhile, the U.S. blockade on Iran's use Strait of Hormuz is costing the Iran Regime $500 MILLION per day. The Regime's entire annual budget is about $56 BILLION. The Regime can no longer pay its soldiers or security police.

Mass protests against the Regime are now starting up again in cities across Iran, as the people are now sensing the Regime can's do much about this.

U.S. Treasury Secretary Scott Bessent has announced that the $24 BILLION in Iranian assets that we have frozen will be used to reimburse and compensate countries in the region Iran keeps hitting with its missiles and drones.

The damage Iran has done to airports, power grids, buildings, and infrastructure, as well as casualties inflicted by Iran in the region, will be billed to Iran's account.

Iran has been saying any deal Iran strikes with the U.S. hinges on the U.S. unfreezing $24 BILLION in Iran assets.

Welp, so much for that idea. This $24 BILLION will be used to compensate Iran's victims in the region.

There is no reason for the U.S. to negotiate anymore with Iran's Regime.

It's quite cheap for the U.S. Navy to keep patrolling the Strait of Hormuz, escorting ships in and out. Our Navy has to be somewhere. Might as well be there, conducting occasional target practice on whatever is left of Iran's military capabilities.

No one fears the Iran Regime anymore. It's proven itself to be a toothless tiger.

Meanwhile, the rest of the Arab World has joined with the United States and Israel in an alliance against the Iran Regime, which is now completely isolated.

That's pretty amazing. Thanks to President Trump, the rest of the Arab world is now allied with Israel.

Who would have thought that possible?

We should allow Israel to do whatever it wants to do to the Iran Regime. We should also continue arming the Kurds and pro-freedom groups inside Iran.

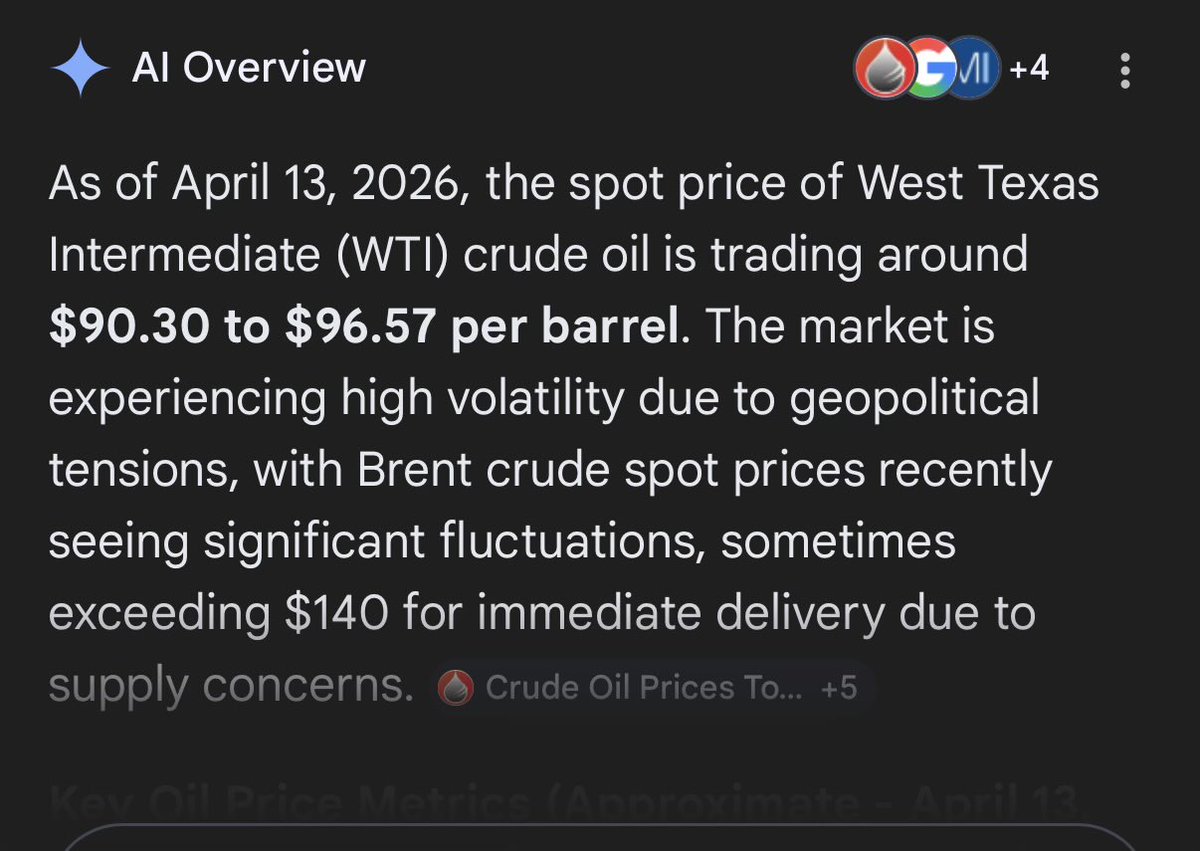

When Epic Fury started, the prediction was that oil would rise above $200 per barrel.

This has not happened. Oil is around $90 a barrel and will continue to drop.

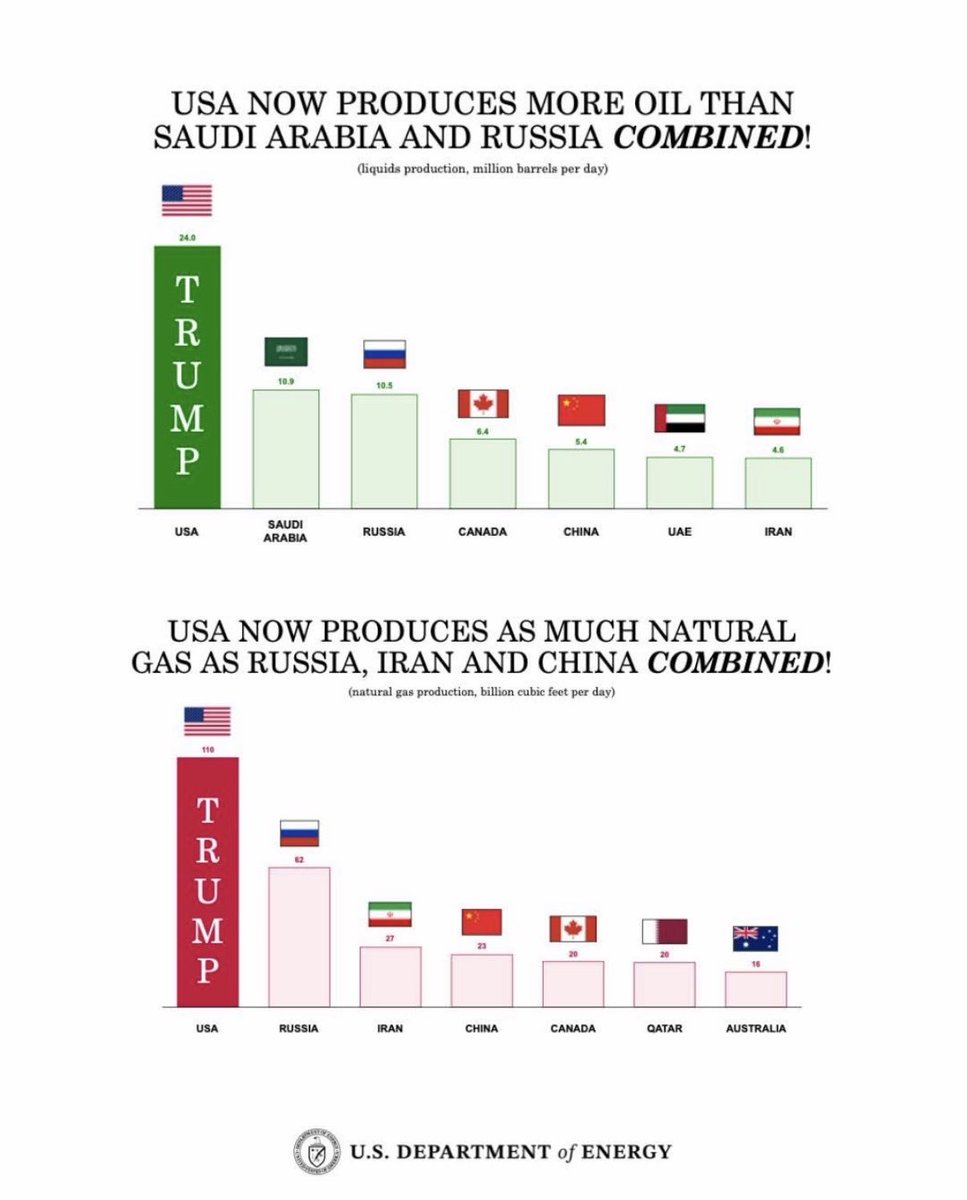

The reason we have not seen anything close to $200 a barrel is the United States has ramped up its oil production.

Thanks to President Trump, the United States is a net oil and energy exporter.

With Trump's arrest of Venezuela's Communist dictator Nicolas Maduro, the United States also now has an oil production partnership with the new government of Venezuela, which as the world's largest oil reserves.

Oil production by Venezuela will only continue to increase.

Trump has also chased China out of Panama. China is no longer running the Panama Canal. We are.

Meanwhile, Saudi Arabia, the UAE, and Kuwait are increasing their pipeline capacity to bypass the Strait of Hormuz, further rendering Iran irrelevant.

Only about 20% of Iran's people are practicing Muslims. The strange theocratic ideology that has been imposed on the Iranian people for 47 years is an alien minority force.

We can just continue to watch the Iran Regime implode financially under this economic pressure we've imposed.

Eventually, the IRGC leadership and Mullahs will receive the Gaddafi treatment.

1

65

Jun 7

BREAKING:

Coinbase says the CLARITY Act is getting close.

This could become one of the most important pieces of financial legislation of the decade.

Why?

Because the biggest constraint on crypto adoption has never been demand.

It’s been regulatory uncertainty.

Large institutions don’t manage billions of dollars by guessing what the SEC might decide next year.

If clear rules are established, the door opens much wider for:

• Banks to expand crypto services

• Asset managers to launch new products

• Pension funds and institutions to increase allocations

• Public companies to hold digital assets on their balance sheets

• Venture capital to flow into the ecosystem with greater confidence

The market may be underestimating what happens when institutional capital can participate with a clearer legal framework.

Bitcoin is still the foundation.

But if institutional adoption accelerates, the largest percentage gains could come from quality digital assets further down the market cap curve as liquidity spreads through the ecosystem.

Markets often price certainty faster than people expect.

If the CLARITY Act passes, the conversation may shift from “Is crypto here to stay?” to “How much exposure do institutions need?”

That would be a very different market than the one we’ve traded for the last several years.

1

85

Jun 7

Everyone wants to own the next OpenAI.

Fewer people are asking what happens when every AI company becomes a tenant paying rent to the same infrastructure providers.

Picks and shovels tend to outperform during gold rushes.

you're telling me anthropic & google are paying spacex ~$26b a year for compute?!!

this is more than half the run rate of openai & anthropic just from compute deals & that doesn't even factor in the rocket launches at all.

elon accidentally ended up owning a significant portion of three of the scarcest assets in ai.. power, chips, & physical deployment capability. the best lesson here is that if you’re selling picks & shovels during a gold rush, you don’t necessarily need to find the gold. you just need everyone else to keep digging. & also non software elon is pretty much unstoppable, like prime michael jordan type thing.

1

52

Douglas Swift retweeted

Jun 5

Jobs apocalypse narrative taking a beating.

BREAKING: The US economy adds 172,000 jobs in May, crushing expectations of 85,000.

The unemployment rate was 4.3%, in-line with expectations of 4.3%.

April's jobs number was also revised UP by 64,000 jobs.

This marks the second strongest US jobs report in 13 months.

383

277

4,435

498,460

Jun 5

People keep waiting for the recession.

What if the recession was the last four years?

Different sectors took turns absorbing the slowdown while aggregate data never fully cracked.

The labor market may be one of the last pieces to turn.

Jun 5

Honestly, it looks like the hiring recession is over.

US average job gains in 2025: 10,000 a month

US average job gains in 2026: 114,000 a month

Job gains in the past 3 months: 188,000

Almost every industry is hiring again except tech and finance. There are a lot of encouraging signs for the labor market heading into summer. (Unfortunately, inflation is a lot worse).

1

139