All things tech

Joined April 2022

- Tweets 89

- Following 21

- Followers 30

- Likes 199

Photos and videos

Sulagna retweeted

1 May 2025

What yesterday’s Qualcomm, Meta, and Microsoft results may infer about what we will see today from Apple and Amazon. My call yesterday on @BloombergTV 👇🏻

$AAPL $AMZN

6

2

16

2,731

Sulagna retweeted

30 Apr 2025

Exciting news! We're thrilled to announce that @MichaelDell, Founder, Chairman, and CEO of @DellTech, will deliver the Show Opening Keynote for The Six Five Summit: AI Unleashed 2025.

This fully virtual event, taking place June 16-19, is free to attend and will explore the rapidly expanding AI landscape and its impact on enterprise, life, and work across 14 focused tracks.

Mark your calendars & register for access: sixfivemedia.com/summit

5

8

23

103,791

Sulagna retweeted

7 Apr 2025

✨ BIG NEWS! ✨ The Six Five just leveled up with a brand new, media-first website, designed to give you a deeper look at who we are and what we do! Discover our story and explore our revamped flagship podcast featuring @PatrickMoorhead & @danielnewmanUV. 👇 Check it out: sixfivemedia.com

1

3

13

110,281

Sulagna retweeted

15 Jan 2025

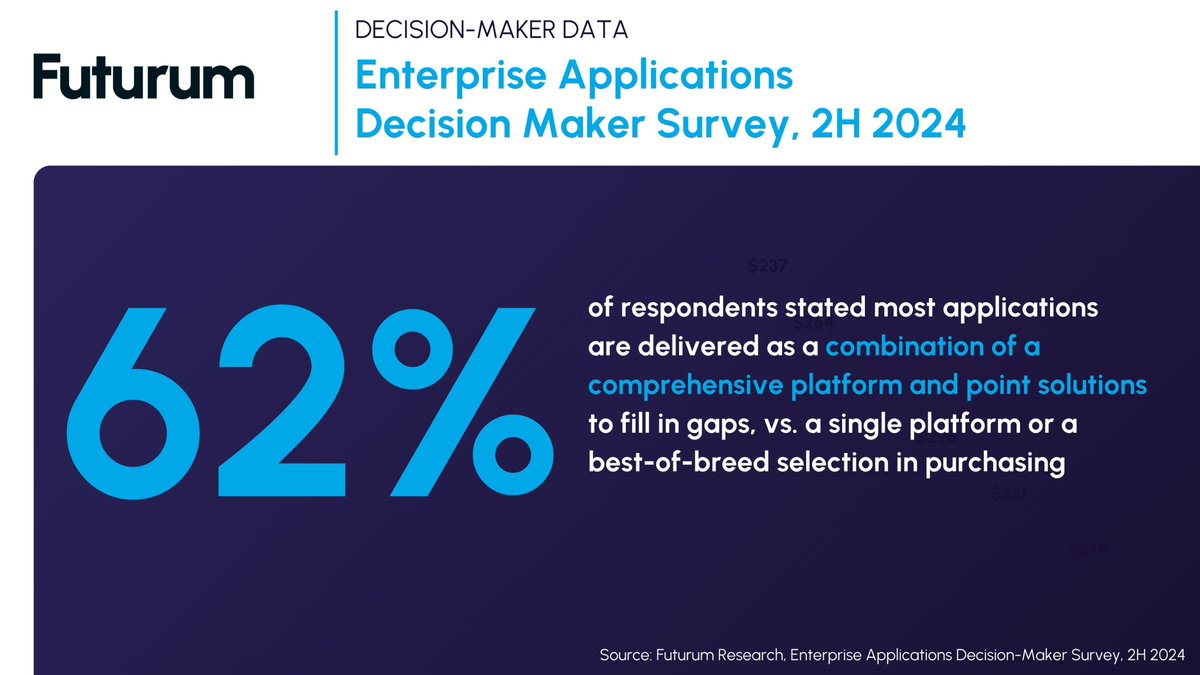

🚨 New Data Alert! 🚨 62% of Enterprise Application Decision Makers prefer their applications to be delivered as part of a comprehensive single platform with point solutions to fill in gaps.

Gain valuable insights from our latest research covering 150 vendors. Download the full report with data from @Google , @Microsoft , @Oracle , & more in the Futurum Intelligence Platform.

Lead analyst: Keith Kirkpatrick @Keith_Kirkpat

6

5

417

Sulagna retweeted

15 Jan 2025

🟡 DAILY RIP LIVE - OPENING BELL W/ SHAY BOLOOR & JORDAN LEE DANIEL NEWMAN x.com/i/broadcasts/1dRKZdEno…

5

5

31

59,065

Sulagna retweeted

21 Nov 2024

🔐What could “The New Tier 0” unlock for tiered storage?

@TheSixFiveMedia host David Nicholson (@daven007) and @Hammerspace_Inc's @Molly_J_Presley discuss the announcement of The New Tier 0 storage and what it means for:

- Unleashing the power of unused NVMe drives in GPU servers

- Powering AI workloads with blazing speed and massive capacity

- Cost savings and real-world applications for enterprises

#Tier0 #NVMe #AI #HPC #DataManagement

1

3

5

41,939

Sulagna retweeted

1 Nov 2024

🔥@TheSixFiveMedia is at #CiscoPS24 in LA! @CiscoPartners

@PatrickMoorhead and @danielnewmanUV are joined by @Cisco's CPO @jpatel41 to discuss the power of #AI, #security (#Hypershield), #networking, and how $CSCO is paving the way to thrive in the digital era. Tune in for insights on:

- Cisco's AI-first strategy 🚀

- Responsible AI in security 🛡️

- Hypershield and recent acquisitions 🤝

- The future of networking 🌐

2

16

53,570

Sulagna retweeted

29 Oct 2024

From defining project scope to achieving #scalability - @IBMConsulting is leading clients through the journey. On this @TheSixFiveMedia, @danielnewmanUV & $IBM @KellyChambliss5 share their thoughts on @IBM 's approach in consulting projects.

1

9

155,639

Sulagna retweeted

27 Oct 2024

Link: SonicWall Doubles Down on Edge Security With Risk-Based Connectivity and Threat Protection @WriterOfTech1 @SonicWall #XFD12 @SecurityBlvd buff.ly/4dWKGxa

2

1

167

Sulagna retweeted

21 Oct 2024

Just added an interview with @SamsungMobile Director of Smartphone Product Management Blake Gaiser to our Galaxy AI Lab Insights page. We talk all about the hardware and software that create Galaxy AI on the S24 family of devices. Full interview here: signal65.com/research/ai/lea…

3

7

1,514

Sulagna retweeted

15 Oct 2024

I had the chance to talk to @AMD’s @LisaSu and @Intel’s @PGelsinger yesterday about this huge announcement on the extension of X86. It has support from the CEOs of Broadcom, Dell, Google Cloud, HP, HPE, Lenovo, Microsoft, Oracle, IBM’s Red Hat, Tim Sweeney of Epic Games and Linus Torvalds of the Linux Foundation. Analysis 👇🏻Six Five Video incoming.

$INTC $AMD $AVGO $DELL $GOOG $HPQ $HPE $MSFT $ORCL $IBM

14

56

392

64,928

Sulagna retweeted

14 Oct 2024

CEO @AMD @LisaSu sat down w/ @danielnewmanUV & @PatrickMoorhead at their #AdvancingAI event to discuss $AMD's advancements in #CPUs #GPUs (5th Gen EPYC & Instinct MI325X), software stack #ROCm, data center, #AI, and overall computing performance.

5

13

67

250,977

Sulagna retweeted

14 Oct 2024

Stay tuned for the latest in #DevOps, #AIOps & #GenAI w/ @BMCSoftware's leaders & partners at #BMCConnect.

Learn more 👉 bmcconnect.bmc.com

#BMCConnect2024 #DiscoverTheNewBMC

14 Oct 2024

We're headed to Las Vegas for live, on-site coverage of BMC Connect! Stay tuned for the latest in #DevOps, #AIOps & #GenAI w/ @BMCSoftware's leaders & partners.

Learn more 👉 bmcconnect.bmc.com/

#BMCConnect #BMCConnect2024 #DiscoverTheNewBMC

2

4

499

Sulagna retweeted

8 Oct 2024

I'm in London for #CommvaultShift this week, and I just had to call out the location: Halfway between MI-6 and Parliament! Metaphorically speaking, this is exactly where @Commvault itself sits: Between cybersecurity and compliance.

8 Oct 2024

We're here in London where #CyberSecurity and #CyberResilience is a big topic. Between MI-6 and Parliament, the subject is more relevant than ever, making it the perfect place for @Commvault to hold their #CommvaultShift event this week. Tune in and register for the event today!

1

2

4

414

Sulagna retweeted

19 Sep 2024

Link: Cisco Aims to Operationalize GenAI in Enterprises With AI-Ready FlexPod With NVIDIA NIM CVD @Cisco @WriterOfTech1 #AIFD5 @TechstrongAI buff.ly/3zgGuKu

1

3

3

260

Sulagna retweeted

6 Sep 2024

Great way to start Friday chatting to @YahooFinance anchors @MadisonMills22 and @thebradsmith about Broadcom Earnings, the future of AI Chips (GPUs vs. ASICs), and China Chip Controls.

While Broadcom saw some selling pressure in the wake of its recent quarter, I feel that the overall direction and the health of the business is really good.

Here is the quick breakdown of the reasons for a positive Broadcom thesis

1. Continued top and bottom-line performance while delivering 60 % EBITDA across a diversified business.

2. $12 Billion dollar AI business (ASIC, XPU, Networking) is compelling with several key hyperscale wins and new ops ByteDance, OpenAI etc. XPU will compliment GPU but will grow faster (CAGR) because of the price/performance for inference.

3. Core business (non-AI semi) is in a macro lull that should pivot substantially with the AI device cycle as well as enterprise DC build out.

4. Beyond 3 above, Broadcom will be one of, if not the largest semi content providers to Apple for the new iPhone and across Apple as Intelligence roles out.

5. VMware will play out better than most expect. The cost structure is already improved, and the top customers are sticky (whether happy or not. The Private Cloud offer is interesting and the competition as Hock sees it is more public cloud than other private or on-prem solutions.

$AVGO

6 Sep 2024

"The AI business is performing," The Futurum Group CEO @danielnewmanUV says. $AVGO's "in the driver's seat."

Full comments:

4

5

11

5,632

Sulagna retweeted

5 Sep 2024

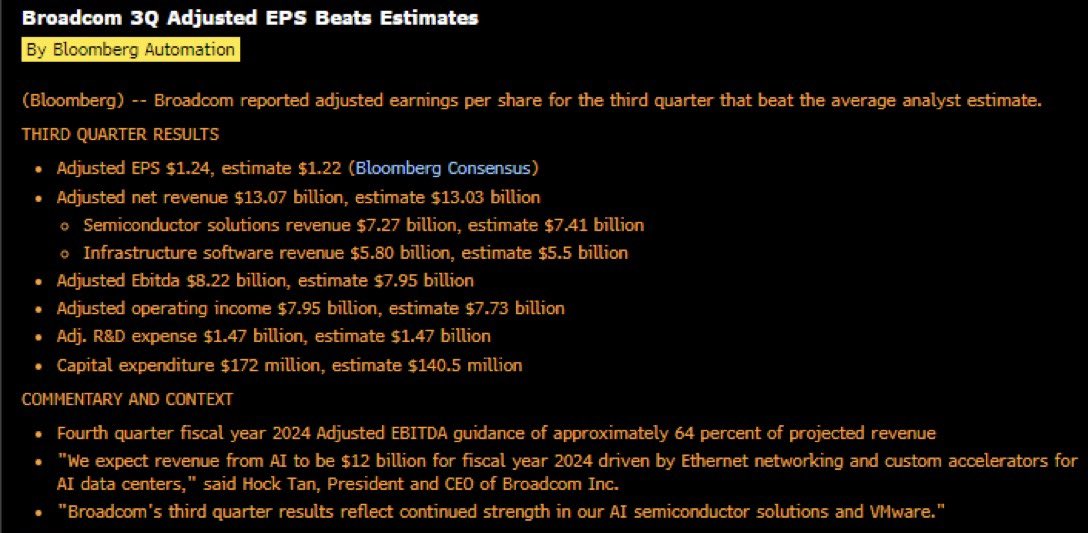

Broadcom doing Broadcom things in Q3 👇🏻

Beating on top and bottom and a solid on par guide.

The standout quote from Hock Tan was the $12 Billion in AI revenue from networking and customer AI chips. This part of the business is growing really quickly and Broadcom has the lead on winning the AI chips (XPU), which we have pegged to grow about 15-20% faster than GPU sales over the next 5 years.

Beat on the software side was robust while Semi came in a bit below consensus.

The company delivered $8.22 Billion of EBITDA on $13.07 Billion in Revenue. Such an incredible bottom line output. Capex stays lean and R&D a bit above 10%.

$AVGO

3

4

33

3,009

Sulagna retweeted

29 Aug 2024

Another tech name that dropped yesterday was @PureStorage

The company showed a mixed result with an earnings beat and a narrow revenue miss.

The big standout reason for the selling pressure on the result for me was the slowing SaaS growth that saw TCV estimates drop to $500 million from $600 million.

What I like, despite some of the immediate negativity about Pure Storage is its power efficiency versus other storage modalities and the company's continued strength in its best-in-class customer success profile (NPS)

The company is also evolving to offer more value-added services as AI proliferated as well as cyber resilience capabilities on the expanding platform.

$PSTG

2

1

7

1,128

Sulagna retweeted

28 Aug 2024

Great debut on @SquawkCNBC by our very own @OABlanchard breaking down today’s NVIDIA earnings.

Arguably one of the most anticipated market moments in years as we see the most important AI name trying to keep its incredible momentum and maintain the strong confidence in the long-term prospects for AI downstream. (video👇🏻)

$NVDA

2

5

23

3,234