TWEETS ≠ ADVICE | Fiduciary | Retirement Planner | Annuity research | Mathematical Finance PhD | Adjunct prof @ UF MSF | Author: amazon.com/dp/1453889280

Joined November 2010

- Tweets 4,329

- Following 270

- Followers 1,007

- Likes 10,809

265 Photos and videos

Pinned Tweet

24 Apr 2023

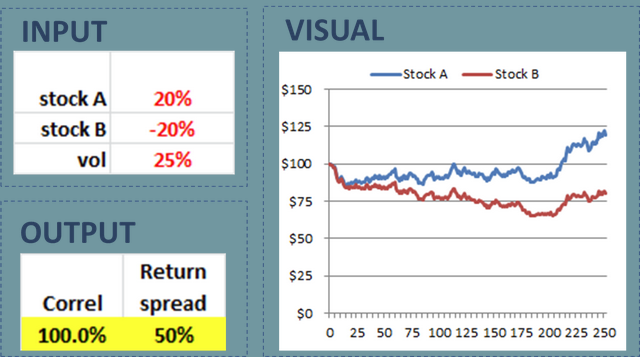

Wrapping up my (3) previous threads on the good, bad, and ugly aspects of annuities, I now highlight one last aspect of the UGLY side.

This topic is a bit technical. So I've tried to make it as intuitive as I can.

Note: This topic also applies to life insurance (e.g., IUL).

20 Apr 2023

Following up on my two previous discussions, this thread will start to focus on the UGLY side of annuities.

Given the length of my previous annuity threads and the plentiful negative press on annuities that is already out there, I will try to keep this section brief.

1

1

8

3,976

May 13

For example, I think this could be a $bn idea: x.com/DudespostingWs/status/…

May 13

Robert Reich forgot the 6th and most common way:

6) Build something millions of people actually want

273

Aaron Brask, PhD retweeted

May 12

A news reporter asked Michael Jordan if he thought the ’90s Bulls could beat LeBron’s Lakers.

MJ: Yes.

Reporter: By how much?

MJ: Two or three points.

Reporter: Why so close?

MJ: Most of us are almost 60 now.

533

5,454

60,750

1,585,769

Is this AI?

Ric Flair, at the age of 77, still deadlifting this weight is incredible

1

166

Apr 18

100%. I'd add beneficiary tax rate (e.g., kids'); it's esp important w no stretch IRA. eMoney et al do what they're told. I have eMoney but use other software for strategizing around those SS Roth withdrawal decisions. Also get more surgical w brackets/thresholds each year.

I just reviewed every single input in my financial planning software (eMoney).

Here are the details most likely to be missed by financial advisors:

• Life expectancy

• Default investment growth rates

• Advisory fees

• Beneficiaries and community property rules

• State income tax assumptions (current vs. future)

• Tax carryforwards

• Custom tax deductions, credits, and adjustments

• Living expenses (vs. payments with start/end dates)

• Tax basis of investments and property

• Ex-spousal Social Security benefits

• Taxable vs. non-taxable Income

• Retirement plan contribution limits

• Inherited IRA RMD rules

• Roth IRA established year

• Exceptions to the 10% early withdrawal penalty

• Premium Tax Credit eligibility

• Liquidation strategy

• Asset location

Since the outputs are only as reliable as the inputs, why are we so quick to plug and play, print, and present?

Many advisors are learning the software before they fully understand which inputs matter (and why). Using a tool without education is dangerous, especially when the outputs promote precision instead of general direction.

At least eMoney provides The Learning Center and a certification program for new users. I think all fintech providers should require this; otherwise, it's like handing a chainsaw to a child.

1

177

Aaron Brask, PhD retweeted

Apr 15

THIS IS BETTER THAN ANYTHING ON THAT PIECE OF SHIT CALLED NETFLIX RIGHT NOW.

22

52

376

29,034

Corey's best post ever

Mar 31

Don't even ask the question. The answer is yes, it's within the collar. Think the S&P is going to rip to new all-time highs? Sorry, there's a short call at 7155 capping your upside. The hedge fund already sold it. You think you found alpha? You found the ceiling of a put spread some quant structured three months ago in a conference room overlooking Park Avenue.

You think the market is going to crash? Priced in. There's a long put at 6475 and market makers are going to buy futures all the way down to defend it. You think you're being clever buying puts at 6400? Congratulations, you just paid premium to bet against the gamma hedging flows of the largest bank in the United States.

The JPM Collar is an all-powerful, all-encompassing being that knows the very inner workings of every retail trader's Robin Hood account before they even open it. Your portfolio was structured decades ago when JHEQX was valuing its expected quarterly roll based on implied volatility that would lead to your birth, what age you would discover options, how many times you would get wrecked on 0DTEs every week, how many times you would stare at SpotGamma charts pretending to understand them, etc.

Anything you can think of has already been collared, even the things you aren't thinking of. You have no original trades. Your "conviction" is just an illusion, a product of the omniscient put spread.

Free will is a myth. The collar sees all, knows all, and will be there from the beginning of time until the end of the universe (the collar has already priced in the heat death of the universe and set strikes accordingly, long put at Entropy-5%, short put at Absolute Zero).

Every quarter, like clockwork, the high priests at 383 Madison Avenue roll their positions. They sell calls. They buy puts. They sell lower puts. And the entire S&P 500 bends to their will. You think Powell controls the market? Powell wishes he had the gamma exposure of JHEQX.

You want to go long? Cool. The ceiling is the short call. You want to go short? Also cool. The floor is the long put. You want to make money? That's the 980 point range they've already defined for you. Stay in your lane. The collar has spoken.

So please, before you make a post on wsb asking whether SPX is going to break out, or whether we're going to crash, or what strike to buy, just look up the JPM collar strikes for the quarter. That's your range. That's everyone's range. We're all just trading inside JPMorgan's hedged equity terrarium.

Don't fight the collar. The collar is inevitable. The collar is eternal.

1

214

Aaron Brask, PhD retweeted

Mar 4

have you said ‘thank you’ once for your capital losses

Mar 4

Then you generated capital losses. Did you use those yet??

95

481

11,155

554,132

Just like @jockowillink, except 100% opposite. Negative ownership of bad outcomes. The reply re: "did you use your capital losses?" says it all ...

Mar 4

What happened at Social Capital was several things:

1) Personally, I was going through a divorce. It was a very hard time.

2) My ostensible “cofounders” spent more time jostling for board seats and credit for deals with outsiders vs doing good work and mentoring a team. They made the place a political snake pit - something that I had unfortunately allowed to happen. So I killed the snake.

3) It was increasingly clear that my returns were sporadic but gargantuan and didn’t fit in a classic fund with LPs. I was a home run hitter in a business where raising new funds invariably led you to hitting singles and doubles. In other words, I was making suboptimal portfolio decisions so I would return capital in order to keep raising funds. This was important to stack the compensation of my team who had far less capital than I did.

I’m in a much better place now personally and professionally. We invest only my capital and so far, so good.

Long live Social Capital.

1

235

Feb 17

Wait, are going to have to call "derivatives" something else?

Feb 14

Options are the true underlying….

Asset values are the simply the derived expected value of the probability distribution.

Asset price is a derivative.

124

Publicly owned wealth management firms have 12B-1 fees and revenue-sharing agreements with the funds and portfolio managers they use in client accounts. #conflictsofinterest

Private equity owned dental offices have sales target meetings every morning

“Ok team, let’s get 5 dentures today!”

And bonus structures that incentivize staff to nudge you towards night guards, retainers and whitening etc.

2

166

31 Dec 2025

You don't pay 23.8% cap gain tax every year on the principal amount, but you do pay interest every year. Need to consider investment growth rate vs int rate potential capital calls if collateral declines. No?

29 Dec 2025

This is a no brainer.

Here’s why.

The “buy, borrow, die” strategy is the single biggest loophole in the American tax code, and Ackman just proposed the cleanest fix anyone has ever put forward.

Let me walk through the mechanics.

Step 1: You build $10B in company stock. You never sell it. No taxable event occurs because capital gains only trigger on realization.

Step 2: You need $500M to buy a yacht, fund a foundation, or just live large. Instead of selling stock and paying 23.8% federal capital gains, you walk into Goldman Sachs and borrow $500M against your shares at 5-6% interest. Under federal tax code, loan proceeds are not income. You now have $500M in liquid cash and owe zero income tax.

Step 3: You keep borrowing. Year after year. The interest payments are trivial compared to the tax savings. A 6% interest rate on $500M is $30M annually. The capital gains tax you avoided? $119M. You’re saving $89M per year by borrowing instead of selling.

Step 4: You die. Here’s where the magic happens. Your heirs inherit the stock at “stepped-up basis,” meaning the cost basis resets to current market value. That $9.9B in appreciation that was never taxed? It vanishes from the IRS’s perspective forever. Your heirs sell a small slice to pay off your outstanding loans, keep the rest, and start the cycle again.

This is generational tax avoidance at scale.

Elon Musk had 238 million Tesla shares pledged as collateral in a 2024 SEC filing. That’s one-third of his total holdings. Larry Ellison has $24 billion in Oracle stock pledged. The research firm Audit Analytics found Musk’s pledged shares alone account for more than a third of all shares pledged across the entire NYSE and Nasdaq combined.

These aren’t edge cases. This is standard operating procedure for anyone with nine or ten figures in appreciated stock.

Now here’s what Ackman proposed:

If you borrow against company stock in excess of your cost basis, treat the loan as a deemed sale for tax purposes.

Example: You bought $100M in stock. It’s now worth $1B. You borrow $600M against it. Under current law, you owe nothing. Under Ackman’s proposal, you’d owe capital gains on $500M because that’s the amount exceeding your basis.

The IRS would treat it as if you’d sold $500M worth of stock. You’d pay the 23.8% federal rate. You’d still have your shares. You’d still get future appreciation. But you couldn’t extract the economic value of gains while pretending no realization occurred.

The elegance is in what this proposal avoids.

Wealth taxes require annual valuation of every asset, including illiquid private companies, art, real estate. The compliance costs are enormous. The legal challenges are real. The constitutional questions around taxing unrealized gains haven’t been settled.

Ackman’s approach sidesteps all of that. It doesn’t tax wealth. It doesn’t tax unrealized gains sitting quietly in a brokerage account. It only triggers when you borrow against those gains. The moment you access the economic value, you pay tax as if you’d sold.

The counter-argument is that this would discourage leverage. Ackman addresses this directly: that’s a feature. Encouraging billionaires to take massive margin positions against their own companies creates systemic risk. When Tesla dropped 30% in 2022, Musk faced potential margin calls that could have forced selling into a falling market. The tax code shouldn’t subsidize that behavior.

The political math works too. Wealth taxes poll well but die in Congress and courts. This targets only the people using a specific loophole. It doesn’t touch the doctor who borrowed against her house or the small business owner with a line of credit. It’s narrow, defensible, and hard to frame as class warfare.

One shouldn’t be able to live and spend like a billionaire while paying no tax. If you’re extracting value from appreciation through borrowing, you’re realizing the economic benefit.

The tax code should recognize that.

2

114

Aaron Brask, PhD retweeted

8 Nov 2025

BREAKING NEWS: Trump plans to introduce a 100 year mortgage loan.

He's going to call it "renting" its absolutely revolutionary!

32

76

728

24,669

8 Nov 2025

Isn't this how used car salesman make cars *cheaper*?

8 Nov 2025

🚨 BREAKING: President Trump appears to announce his intention to normalize 50 YEAR MORTGAGES, to make it easier for young people to buy a home via lower monthly payments

He cites FDR as when the 30-year mortgage started to spread nationwide

👀

2

165

29 Sep 2025

I dunno. Democratize trading for drunks coming home after the bar? Weekday/daytime trading trading hours haven't exactly crippled mankind over the last century. On the plus side, those lonely institutional forex traders might finally get some company in the off hours.

29 Sep 2025

"Crypto is 24/7. There's no reason why options and all sorts of traditional assets shouldn't be as well." - Vlad Tenev

@vladtenev @RobinhoodApp @jam_croissant

👇️ 👇️ 👇️ 👇️

toptradersunplugged.com/podc…

1

189

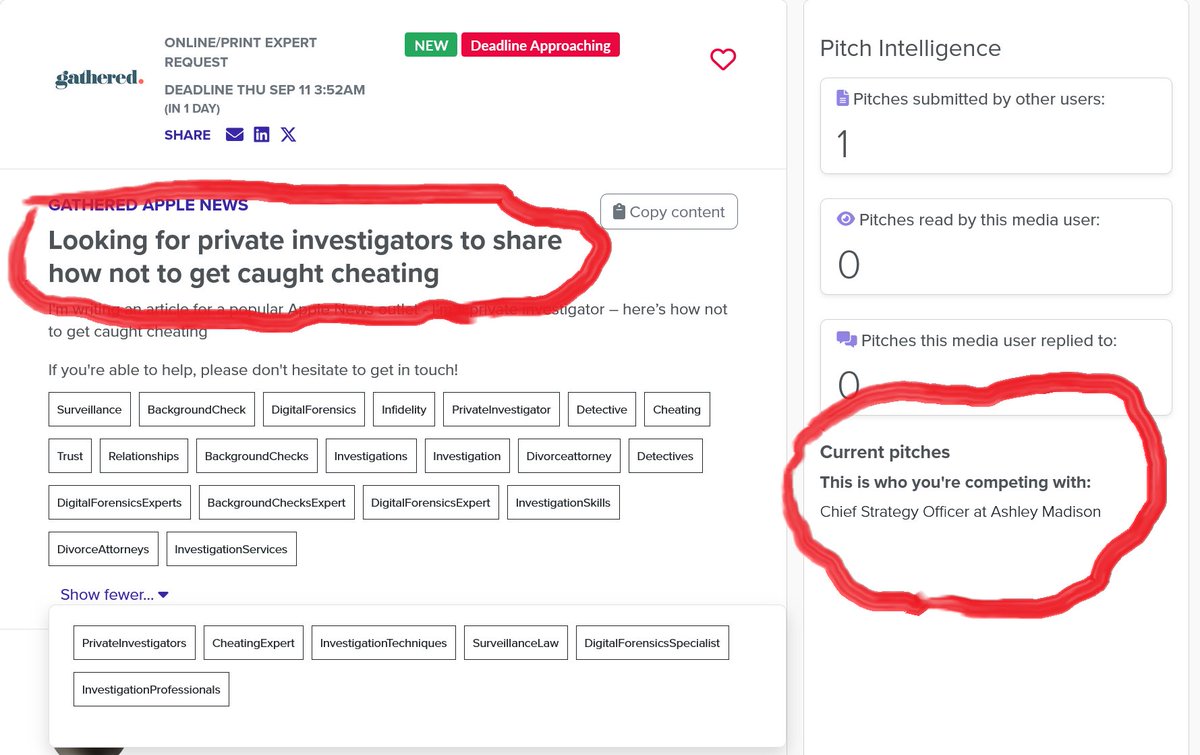

9 Sep 2025

I don't understand why they approached me for a quote on this topic, but I found the one competing pitch entertaining:

1

2

117

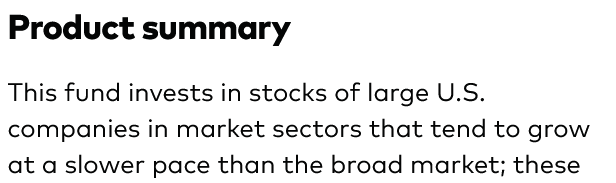

15 Jul 2025

Agree value and growth are not mutually exclusive (Vanguard value description always entertained me), but I thought RAFI's linking portfolio weights to *current* fundamentals systematically underweighted growing companies? What am I missing?

@CliffordAsness @hsu_jason @EconomPic

5

2

828

15 Jul 2025

135

12 Mar 2025

11 Mar 2025

Anyone have a model that can count the letters in this photo? All I have tried failed.

1

273