Feb 23

2/6

AI compresses the gap between idea and implementation ⚡

But prototypes can quietly become production dependencies

#AIinSoftware #TechLeadership

1

18

Plug-and-Play AI Autocomplete for Blazor

nuget.org/packages/EasyAppDe…

github.com/mashrulhaque/Easy…

#Blazor #DotNet #PostgreSQL #AIinSoftware #SmartSearch #Autocomplete #OpenSource #DeveloperTools #TechInnovation #WebDevelopment

2

3

55

Jan 25

MS || Software (North America)

4Q25 SaaS Preview – Staying Selective

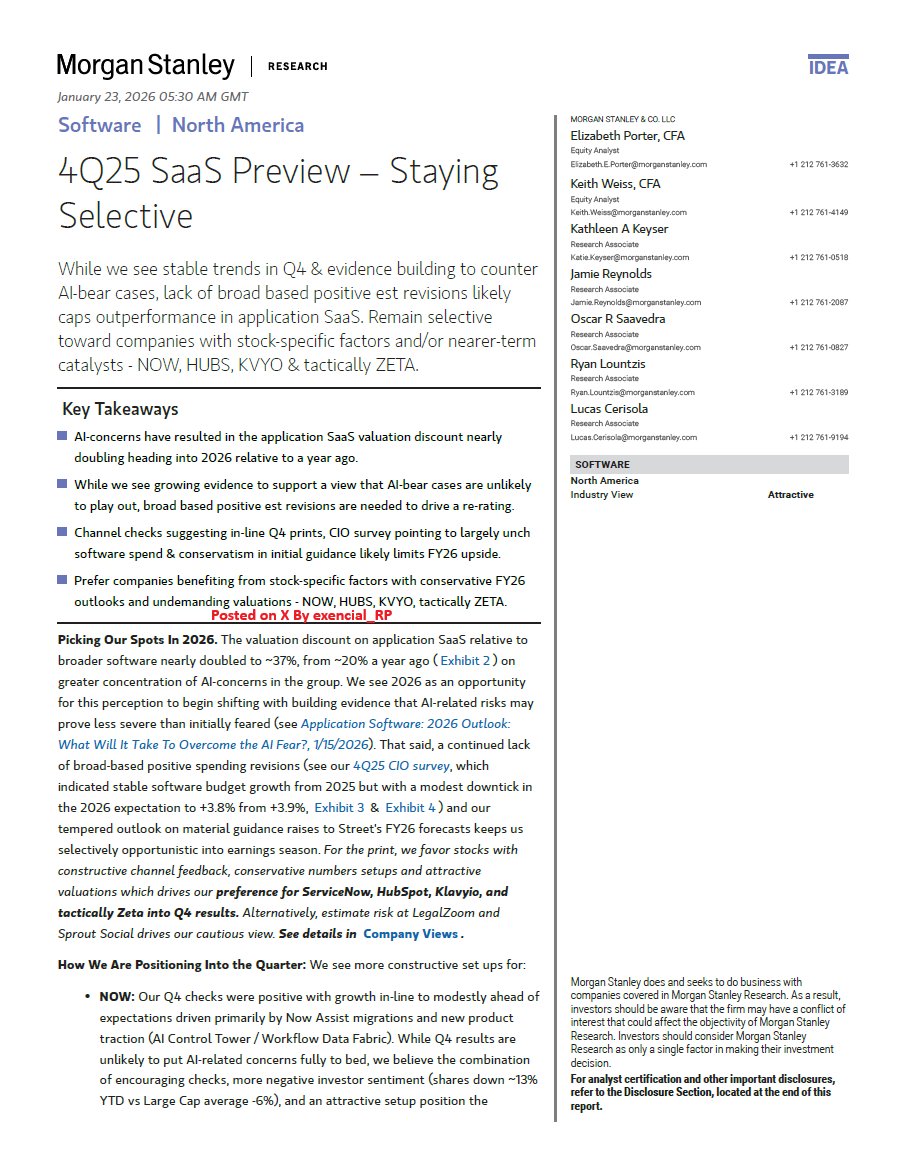

We see stable demand trends in 4Q25 and growing evidence that AI-bear cases may prove less severe than initially feared; however, the lack of broad-based positive estimate revisions is likely to cap near-term outperformance across application SaaS. While the valuation discount of application SaaS versus broader software has widened materially.

We believe selectivity remains critical given muted CIO budget growth expectations for 2026 and generally conservative initial guidance setups. Our 4Q25 CIO survey points to largely unchanged software spend in 2025, with a modest step-down expected in 2026, reinforcing a more selective approach into earnings.

Into the quarter, we favour names with stock-specific catalysts, conservative setups, and supportive channel checks. In particular, we prefer ServiceNow, HubSpot, and Klaviyo, with a more tactical positive view on Zeta, where upside to preliminary guidance appears achievable.

Conversely, we see less attractive setups where estimate risk skews negative and valuation support is limited. Overall, while 2026 may offer scope for sentiment to improve as AI concerns abate, we expect differentiation at the stock level rather than a broad SaaS re-rating.

Industry View: Attractive

SaaS applications growth and margin expectations

#SaaS #SoftwareSector #4Q25Earnings #AIinSoftware

1

1

72

Jan 19

New blog post ✍️

AI can generate code fast.

But AI cannot guess intent.

In my latest blog post, I explain why system use cases are perfect in the age of AI.

I cover:

• where system use cases come from

• what makes a system use case executable

• a good example and a bad example

• why vague specs break AI-assisted development

👉 Read the blog post: martinelli.ch/why-system-use…

#SoftwareArchitecture #AIinSoftware #RequirementsEngineering #SystemUseCases #SpecDrivenDevelopment

2

10

543

Jan 9

#AI can speed up #coding, but real engineering still needs human judgment.

At 3.0 University, we train professionals to move beyond prompts - to orchestrate AI, evaluate outputs, and build production-grade systems at scale.

#AIInSoftware #EngineeringFirst #SystemDesign #DeveloperSkills #AIProductivity

Jan 8

Yesterday we had a tech town hall in Zoho where we did a code review of the C code generated by the Claude Opus 4.5 model. It went on for hours late evening.

I now have a much clearer understanding of what these models do well: they are able to stitch together systems well, taking data from one system, reshape it and pass it to another system. There is often a lot of such "glue code" in these systems and that is not very complicated but it is very tedious.

In general, AI models have "memorized" all the open source too and they are able to recall patterns from them (with some possibility of hallucination). They are also able to stitch various open source pieces together well.

Our senior engineer had guided ("orchestrated" is the right word) this process. When the AI was stuck he helped "unstuck" it. This was a very vital contribution and without his experienced guidance, the AI output would not be useful.

We examined several C files with thousands of lines of code in each, looking for what I consider complex code. Most of it was straightforward glue code and only a tiny part of it was complex.

I suspect that the AI generated code tended to be needlessly verbose but I have to study it more to be sure.

On the whole, I am both impressed and not super awed. I believe we can do better 😏

2

3

1,123

30 Dec 2025

My Last Certification of the Year 🎉

Closing the year with the GitHub Copilot (GH-300) certification 🚀 🩵

#GitHubCopilot #GH300 #Certification #DevOps #PlatformEngineering #AIinSoftware #DeveloperExperience #EndOfYearWin #Copilot #Microsoft #GitHub @github

3

238

19 Dec 2025

System Use Cases are the perfect specification for Spec-Driven Development with AI

If you want to use AI to support or even create business applications, you need clear and unambiguous specifications.

In my opinion, System Use Cases are ideal for this.

System Use Cases describe the exact interaction flow between user and system. Step by step.

- They avoid technical details, but they are precise enough to remove ambiguity.

- This gives two major benefits:

- They are understood by both business and IT

- They are well suited for AI, because the intended system behavior is explicitly defined

In Spec-Driven Development, System Use Cases become the central source for code and tests.

AI can build on them because the what is clear before we discuss the how.

Good specs are not overhead - they enable meaningful use of AI.

#SpecDrivenDevelopment #SystemUseCases #SoftwareArchitecture #AIinSoftware #KeepITSimple

1

11

710

13 Dec 2025

On Monday, I will run a Spec-driven Development workshop with a customer.

We will explore the AI Unified Process (aiup.dev) with Claude Clode live and see how spec-driven development works in practice.

We will also talk about opportunities and risks when using AI in requirements and software development.

I am really looking forward to this session. Hands-on, practical, and focused on real projects.

#SpecDrivenDevelopment #AIUP #SoftwareArchitecture #AIinSoftware #KeepITSimple

2

9

909

1 Dec 2025

🎥 New Video Drop: Behind the Scenes of OWASP FIASSE — The Securable Framework

Youtube Link - youtu.be/82ZvPtFqT84?si=c8H8…

#OWASP #FIASSE #SecurableSoftware #AppSec #SecureByDesign #SoftwareEngineering #AIAppSec #AIInSoftware #ShiftLeft #DevSecOps #OWASPProjects @owasp

2

3

1,689

AI can code in seconds.

But what’s the trade-off for your software architecture?

Find out how to balance speed with sound design in our latest article: ait.inc/tech-stuffs/how-ai-g…

#AIT #AsthaIT #AIinSoftware #SoftwareArchitecture

3

27

How is AI redefining software engineering? Read more: bit.ly/3QL6Fhh

#AIinSoftware #SoftwareDevelopment #ArtificialIntelligence #DevOps #FutureOfTech

1

13

28 May 2025

If you are still allocating dev hours to every minor fix, feature tweak, or repetitive task pause.

There is a better way.

@blackboxai's autonomous cloud agents enable you to assign large volumes of software tasks that get handled in the background securely, asynchronously, and intelligently.

This is not about replacing talent. It is about elevating it.

Let your team innovate while these AI agents handle the grunt work.

From startups to scale-ups, thousands are already rethinking how software gets built.

This shift is not coming it is here.

Check out more details

blackbox.ai

#LeadershipInTech #AIinSoftware #DeveloperExcellence

26

18

70

21,007

23 Feb 2025

💻 AI is transforming software development—faster, smarter, automated

🚀 @tammireddy explains how AI is reshaping the role of developers.

💡 Will AI replace developers?

Drop your thoughts!👇

🎥 Full podcast on YouTube #PowerUpWithPradeep

#AI #AIinSoftware #SoftwareDeveloper

1

2

34

31 Dec 2024

Software service industry, beware! Agentic AI is coming to disrupt everything from code review to testing, making developers more efficient & agile #AIinSoftware

1

37

1 Sep 2024

Exploring the rise of #ArtificialIntelligence in #SoftwareDevelopment. AI-powered tools augment coding, testing, debugging, making processes more efficient. Impact? Huge! Expect faster deployments, improved software quality, and increased productivity. #TechTrends #AIinSoftware

2

2

51

29 Feb 2024

'Tech Insights by Internet Soft'

A Total Game-Changer for Businesses. Click here to understand easily the AI Custom Software Development Solutions: lnkd.in/gFSKTWzx

#TechInsights #AiinSoftware #AIDevelopment #AISolutions #InternetSoft #Customsoftwaredevelopment

1

3

55

Explore the potential of AI in software dev! From automation to analytics, it's revolutionizing the industry.

rb.gy/voc7ct

#AI #softwaredevelopment #techinnovation #artificialintelligence #technology #futuretech #digitaltransformation #aiinsoftware #softwaredeveloper

1

1

16

360

22 Feb 2024

Exciting News! Our latest newsletter, 'Tech Insights by Internet Soft'

Stay ahead of the curve with the latest trends! Read the full newsletter here: linkedin.com/pulse/impact-ai…

#TechInsights #AiinSoftware #AIDevelopment #AISolutions #Aidevelopment #InternetSoft #AIApplications

2

3

34

8 Dec 2023

Tech revolutionizes software dev with AI at its core. Do you know how it'll change dev?

Explore our latest article on #AI transforming #softwaredevelopment. 🚀

#aiinsoftware #techrevolution #aitransformation #innovation #artificialintelligence

multiqos.com/blogs/ai-in-sof…

2

37