The highest investment is to elegantly stand with the great innovators of the times.

When ordinary traders consume sentiment in $SPCX charts, true high net worth allocators focus on its absolute barrier as the 'ultimate global scarce asset'.

Amid inflation and geopolitical uncertainty, SpaceX is becoming the new 'technological gold'. Elegant wealth management is never about tomorrow's fluctuations, but about becoming the strongest pillar on the balance sheet for the next decade. ⚓ ️ ✨#ElegantInvestmentGrade #AssetAllocation #SpaceX #Longtermism

4

6

11

107

La última semana dejó señales relevantes.Cómo impacta en las decisiones de inversión y q posicionamiento considero más adecuado según el perfil de riesgo?#Macroeconomia #AssetAllocation #EstrategiaDeInversion #Inflacion #PortfolioManagement linkedin.com/pulse/anuncio-d… via @LinkedIn

5

#Gold over #equity or vice versa? This #assetallocation strategy has delivered notable return boost in recent years

#portfoliodiversification

economictimes.indiatimes.com…

107

💬 ¡Descubre estas y otras noticias cada semana!

#MercadosFinancieros #VisiónMercadosSafeBrok #AssetManagement #AssetAllocation

(5/5) 👍

1

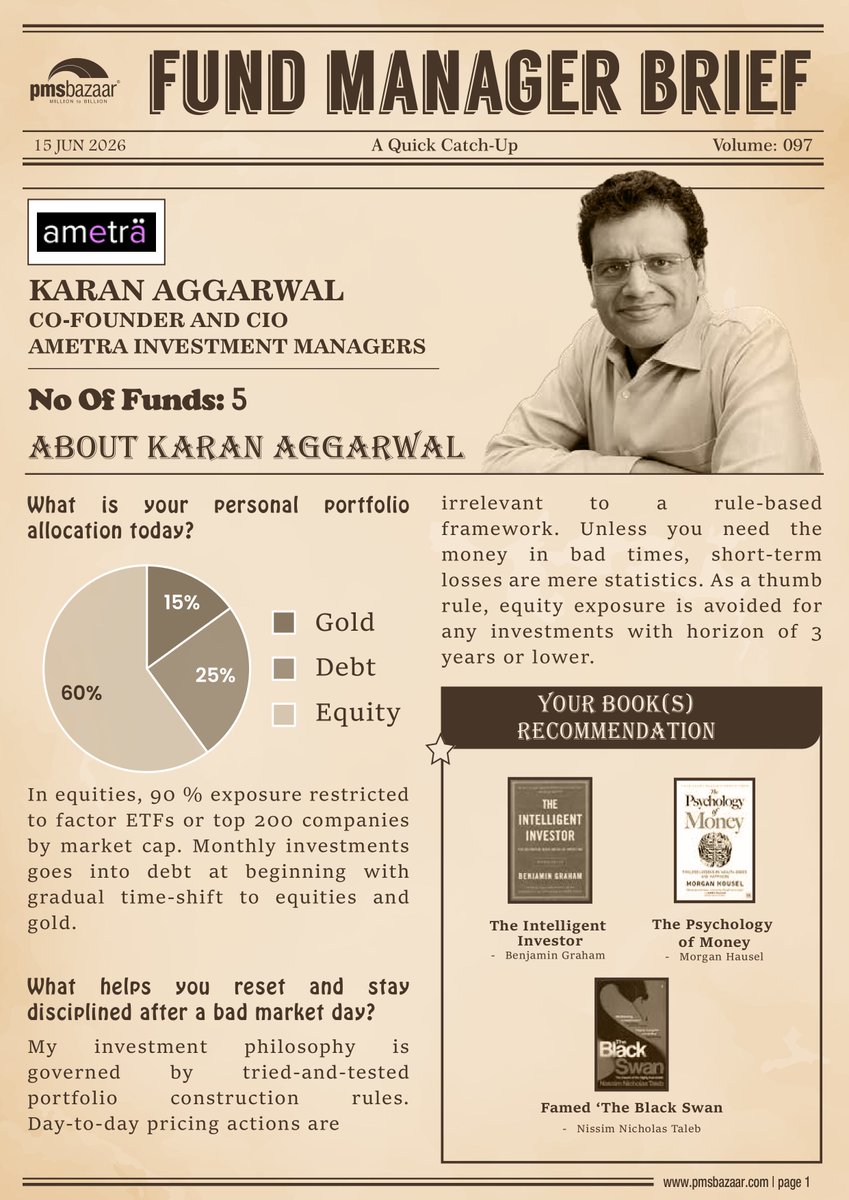

“ 𝐖𝐞 𝐬𝐞𝐞 𝐆𝐨𝐥𝐝 𝐟𝐚𝐥𝐥𝐢𝐧𝐠 𝐭𝐨 𝐔𝐒$ 𝟑𝟖𝟎𝟎 𝐚𝐧𝐝 𝐬𝐢𝐥𝐯𝐞𝐫 𝐟𝐚𝐥𝐥𝐢𝐧𝐠 𝐭𝐨 𝐔𝐒$ 𝟒𝟎-𝟓𝟎 𝐛𝐞𝐟𝐨𝐫𝐞 𝐭𝐡𝐞 𝐧𝐞𝐱𝐭 𝐥𝐞𝐠 𝐨𝐟 𝐭𝐡𝐞 𝐛𝐮𝐥𝐥 𝐜𝐲𝐜𝐥𝐞 𝐜𝐨𝐦𝐞𝐬 𝐢𝐧𝐭𝐨 𝐩𝐥𝐚𝐲,” Said 𝐌𝐫. 𝐊𝐚𝐫𝐚𝐧 𝐀𝐠𝐠𝐚𝐫𝐰𝐚𝐥

In 𝐨𝐮𝐫 𝐥𝐚𝐭𝐞𝐬𝐭 𝐅𝐮𝐧𝐝 𝐌𝐚𝐧𝐚𝐠𝐞𝐫 𝐁𝐫𝐢𝐞𝐟, the 𝐂𝐨-𝐅𝐨𝐮𝐧𝐝𝐞𝐫 & 𝐂𝐈𝐎 𝐨𝐟 𝐀𝐦𝐞𝐭𝐫𝐚 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐌𝐚𝐧𝐚𝐠𝐞𝐫𝐬 shares his perspectives on 𝐟𝐚𝐜𝐭𝐨𝐫 𝐢𝐧𝐯𝐞𝐬𝐭𝐢𝐧𝐠, 𝐚𝐬𝐬𝐞𝐭 𝐚𝐥𝐥𝐨𝐜𝐚𝐭𝐢𝐨𝐧, 𝐚𝐧𝐝 𝐭𝐡𝐞 𝐞𝐯𝐨𝐥𝐯𝐢𝐧𝐠 𝐫𝐨𝐥𝐞 𝐨𝐟 𝐪𝐮𝐚𝐧𝐭 𝐬𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐞𝐬 𝐢𝐧 𝐈𝐧𝐝𝐢𝐚'𝐬 𝐢𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐥𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞.

𝐑𝐞𝐚𝐝 𝐍𝐎𝐖: resources.pmsbazaar.com/fund…?

#Investing #Markets #Finance #WealthManagement #PortfolioManagement #AssetAllocation #QuantInvesting #MarketInsights #pmsbazaar

147

🇮🇷 🇺🇸 Peace Premium Is Live. Here’s Where Smart Money Is Moving First

Read More: bit.ly/PeacePremium

#GlobalMacro #HedgeFunds #AssetAllocation #EmergingMarkets #Treasuries #FXStrategy #AIInvesting #GeopoliticalRisk #InstitutionalInvesting #AlphaBinwaniCapital

10

In #investing

Narratives always changes

But

Your Behaviour should not

Just stick with your #AssetAllocation; review your portfolio periodically; rebalance it, if necessary.

that' it

All Done!

4

Kotak Mutual Fund | Market Outlook Webinar

Speaker: Nilesh Shah, Managing Director

Date: 08 June 2026

➡️ Global markets continue to face geopolitical uncertainty, elevated commodity prices, rising bond yields, and currency volatility.

✅ Kotak MF's View:

• Neutral on Equities

• Overweight on Gold

• Marginally Overweight on Mid-Caps

• Equal Weight on Large Caps

• Underweight on Small Caps

➡️ Preferred sectors include Financial Services, Consumption, Healthcare, Auto, Cement & Infrastructure.

👥 What Should Investors Do?

• Maintain diversified asset allocation

• Continue SIPs and long-term investing

• Use Multi-Asset, Multicap or Flexicap strategies

• Consider Gold allocation

• Focus on risk management

👉 Read the full summary on :

fundyantra.com/diversify-don…

#MutualFunds #KotakMutualFund #MarketOutlook #AssetAllocation #Investing

11

10h

#OnETNOW | Markets should not depend solely on the deal for further strength says Devina Mehra of First Global

#GlobalMarkets #Investing #AssetAllocation #CrudeOil @devinamehra @firstglobalsec

2

858

全球华人高净值家族做资产配置,香港几乎都会出现在这张图上。

保险、股票账户、企业在香港的相关安排——每个家族不一样,但香港在那里,几乎是规律。

问题不是香港在不在,而是:香港这块,在整套配置逻辑里,想清楚了吗?

市场波动时它是稳定部分还是同向波动?家族处境改变时能不能平稳调整?

很少有家族能清晰回答。因为香港资产通常在不同时间通过不同机构分别安排,从来没有人把它作为整套配置里有明确角色的部分来管理。懂金融,更懂华人。

When global Chinese families map their asset allocation, Hong Kong almost always appears.

Insurance, securities accounts, business-related arrangements in Hong Kong — different for every family, but Hong Kong being there is almost a constant.

The question isn't whether it appears. It's whether you've thought through what role it actually plays.

When markets move sharply, does it stabilise or move with everything else? When family circumstances shift, can it adjust smoothly?

Very few families can answer clearly. Because Hong Kong assets are typically arranged at different times through different institutions — never placed within the full allocation framework with a clearly defined role.

Hong Kong is one of Noah's four global account and transaction centers. Feel free to reach out.

Wealth expertise. Deeper global Chinese insight. Noah Holdings (NYSE: NOAH | HKEX: 6686) | Where Global Chinese Wealth Connects

#NoahHoldings #AINativeWealthManagement #GlobalChinese #WealthManagement #GlobalAllocation #HongKong #AssetAllocation #FamilyWealth #WealthStructuring

119

The 2026 Inflation Fighter Portfolio: Three Profiles, Real Returns 3-7%, Backtested vs 60/40

#theexpme #InflationFighter #portfolioallocation #realreturn #SP500 #gold #TIPS #bitcoin #REITs #IRA #401k #wealthbuilding #investing #PricingPower #assetallocation #Roth

55

Dubbi sulle valutazioni AI e dati sul lavoro USA più forti delle attese hanno aumentato la volatilità dei mercati.

Portafoglio modello chiude a -0,15%, beneficiando della progressiva riduzione dell'esposizione alle materie prime.

#AssetAllocation #Investimenti

2

7

17h

Calling all buy-side portfolio managers, asset allocation directors, and investment strategists! 📈💼🏛️

Mercor is recruiting experienced Portfolio Managers across the US and Canada for a high-impact consulting role with a leading AI lab. In this position, you will contribute your real-world expertise in portfolio construction, risk management, and multi-asset investment strategy to train next-generation AI systems designed for institutional investing.

You will critically audit and stress-test AI-generated asset allocation frameworks, evaluate risk models under varying market conditions, and help build the training datasets that define institutional-grade financial AI.

💰 Compensation: $150 per hour

💼 Type: Hourly contract

🌍 Location: Remote (Open to US & Canada residents)

Key Responsibilities:

Provide high-level input on asset allocation and portfolio construction.

Evaluate and stress-test AI-generated portfolio strategies and risk frameworks.

Guide machine learning models with institutional portfolio management insights.

Skip the traditional recruitment black hole and apply directly via my referral link.

Apply here: t.mercor.com/IGwFw

Since I am part of Mercor's referral program I currently work at Mercor as a contractor.

#PortfolioManagement #AssetAllocation #BuySide #RiskManagement #RemoteWork

69

18h

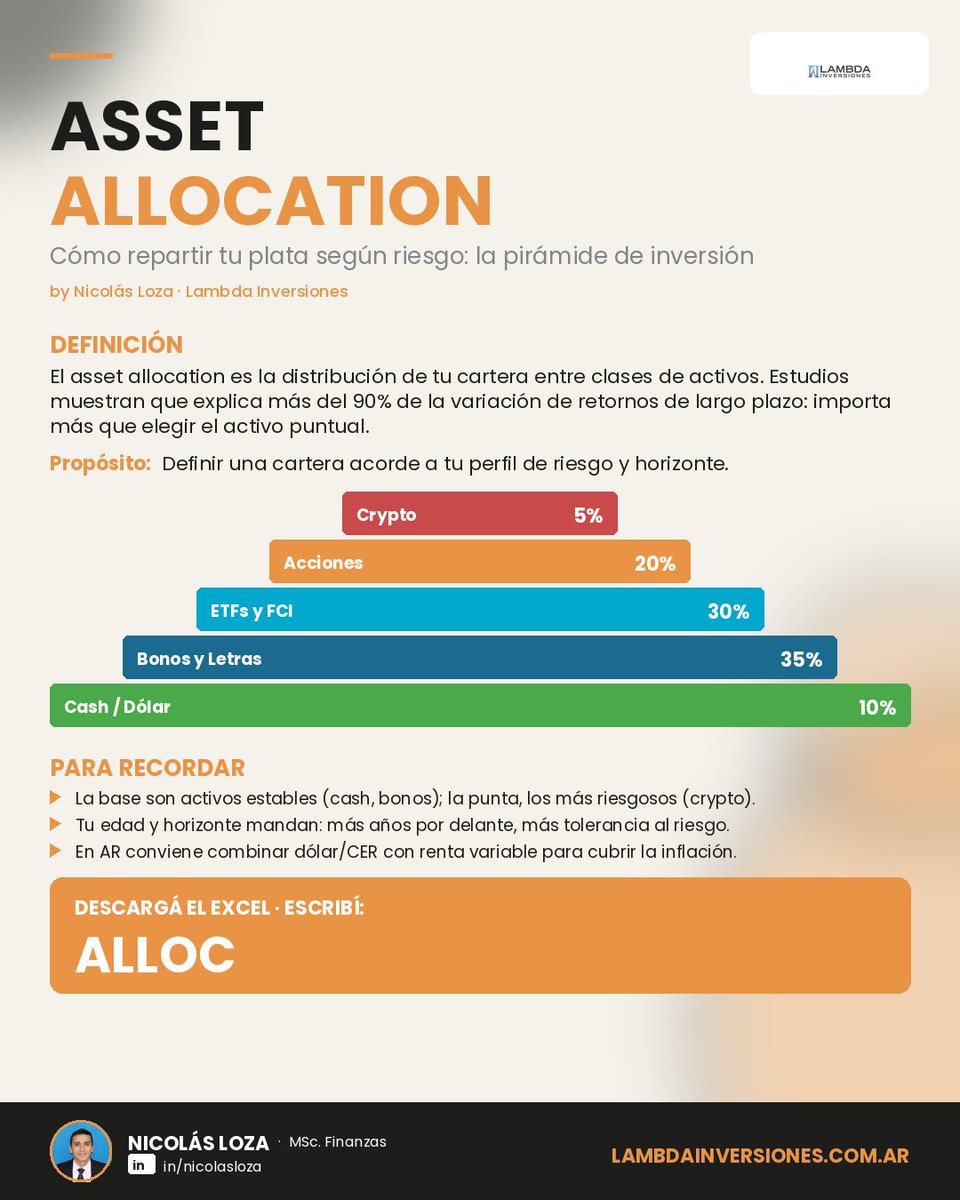

Elegir bien la acción importa menos de lo que pensás. Esto importa más.

El asset allocation es cómo repartís tu plata entre clases de activos: cash, bonos, fondos, acciones, crypto. Estudios clásicos muestran que explica más del 90% de la variación de retornos de largo plazo. O sea: pesa más cómo distribuís que qué activo puntual elegís.

Pensalo como una pirámide: base ancha de activos estables, punta angosta de los más riesgosos.

• La base son activos estables (cash, bonos)

• La punta, los más riesgosos (crypto)

• Tu edad y horizonte definen la mezcla

En Argentina conviene combinar instrumentos en dólar y ajustados por CER con algo de renta variable, para que la inflación no te licúe el capital mientras buscás crecimiento.

Comentá "ALLOC" por DM y te paso el Excel interactivo.

#Lambda #LambdaInversiones #Inversiones #AssetAllocation #MercadoDeCapitales

8

Most People Don’t Have a Wealth Problem. They Have a Capital Allocation Problem.

I’ve seen this many times across Pakistan, the UAE, the UK and other markets. Families own valuable assets — inherited land, old commercial plots, empty properties or apartments they don’t want to sell — but still struggle with cash flow. On paper, they are wealthy. In reality, the assets are not working hard enough for them.

Being asset-rich and cash-poor is not a wealth strategy. It is usually a capital allocation problem. A family may own agricultural land worth hundreds of millions, but after tenants, expenses, delays, disputes and management headaches, the real net yield may only be 2–3%. Another family may own a plot in a growing city that has appreciated a lot, but produces zero income. It just sits there because nobody can agree whether to sell, develop or hold.

I understand the emotional attachment. Some assets were bought by parents or grandparents, and selling them can feel difficult. But capital does not care about emotion. Every asset you own is producing a return, whether you measure it or not. The real question is whether that return justifies the capital tied up, the management burden and the opportunity cost.

A PKR 50 million plot producing no income has a real cost. If the same capital could earn even 6% net somewhere else, that is PKR 3 million a year in missed income. Over 10 years, that becomes a very serious number.

This is the exercise most families avoid. Take every asset you own and calculate the real net yield after costs, taxes, maintenance, vacancy, disputes and your own time. Then compare it with what the same capital could earn if it was redeployed into better income-producing assets. That gap is the cost of doing nothing.

Liquidity also matters. Illiquid assets don’t just underperform; they trap you. When real opportunities appear — a distressed sale, a market correction or a chance to buy quality assets cheaply — the family with liquid capital can act. The family stuck in low-yielding land or an empty plot cannot.

This does not mean every inherited asset should be sold. Some assets have strategic value, emotional value or development potential. But they should still be reviewed properly. Sentiment is not a strategy. Hope is not underwriting. And “we have always owned it” is not a strong investment thesis.

Most wealth does not disappear in one bad decision. It leaks slowly through poor yields, emotional attachment and years of inaction.

Sometimes the compounding you are missing is not in a new investment. It is sitting inside the assets you already own, but are not using properly.

#CapitalAllocation #WealthManagement #FamilyWealth #RealEstateInvesting #PortfolioStrategy #AssetAllocation #LongTermInvesting

46

Most investors think gold moves for one reason.

Fear.

Peter Grant, a widely followed precious metals strategist, recently shared an insight in a Reuters report that shows why that view is incomplete.

Gold rose 1.5% to $4,861/oz and headed for a fourth straight weekly gain even as hopes of a U.S.-Iran deal improved and the Strait of Hormuz stayed open. Oil fell. The dollar weakened. Rate-cut expectations returned. Gold still held strong.

That is the real lesson:

Gold is not reacting to one headline.

It is responding to a system.

And that matters for your wealth decisions.

My investing framework is simple:

1. STOP ASKING “WHAT WILL GOLD DO?”

Ask:

- What changed in inflation expectations?

- What changed in rates?

- What changed in liquidity?

- What changed in the dollar?

- What changed in portfolio risk?

Better questions create better decisions.

2. USE GOLD AS a ROLE, NOT a BET

Gold does not need to be your whole strategy.

It can serve as:

- resilience capital

- diversification

- crisis ballast

- psychological stability in volatile periods

Assets should have jobs.

3. BUILD ALLOCATION BEFORE VOLATILITY ARRIVES

Do not decide during panic.

Decide in advance:

- maximum allocation

- rebalance rules

- when to add

- when to trim

- why you own it

That turns emotion into process.

4. WEALTH is BUILT by SYSTEMS

You do not need to predict every geopolitical event.

You need a portfolio that can function across many outcomes.

That is how long-term investors win.

Not by perfect forecasts.

By repeatable decisions.

#Investing #WealthBuilding #Gold #AssetAllocation #BehavioralFinance #LongTermInvesting #PortfolioManagement #MacroInvesting

31

Jun 14

Beyond Wealth | 14 มิถุนายน 2569

มหกรรมฟุตบอลโลกเริ่มเปิดฉาก ทุกทีมต่างต้องวางแผนให้สมดุล ทั้งเกมรุก เกมรับ และจังหวะการครองเกม เพราะการมีแค่กองหน้าที่เก่งอย่างเดียว อาจไม่พอให้ทีมไปถึงเป้าหมาย

“การจัดพอร์ตลงทุนก็เช่นกัน”

พอร์ตที่ดีไม่ควรมีเฉพาะสินทรัพย์ที่หวังเติบโตสูง แต่ต้องมีทั้งตัวสร้างผลตอบแทน ตัวช่วยกระจายความเสี่ยง ตัวลดความผันผวน และสินทรัพย์ป้องกันพอร์ตในวันที่ตลาดไม่เป็นใจ

ที่น่าสนใจคือ หากมองสถิติในอดีตช่วงฟุตบอลโลก ตลาดหุ้นไม่ได้มีทิศทางเดียวเสมอไป บางปีหลังจบทัวร์นาเมนต์ตลาดปรับขึ้นแรง เช่น ฟุตบอลโลกปี 1994 ที่สหรัฐฯ ตลาดบวกต่อเนื่องหลังจบงาน ขณะที่บางปี เช่น 1998, 2002 และ 2006 ตลาดกลับเผชิญแรงกดดันหลังการแข่งขัน

จากข้อมูล Bloomberg report พบว่า ผลตอบแทนค่ากลางของตลาดหุ้นในช่วงฟุตบอลโลกอยู่ที่ราว 1.0% ระหว่างการแข่งขัน และ 4.6% ในช่วง 12 เดือนหลังจบการแข่งขัน สะท้อนว่า “บอลโลกอาจสร้างสีสันให้ตลาด” แต่ไม่ได้เป็นปัจจัยชี้ขาดทิศทางการลงทุน

ดังนั้น สิ่งที่สำคัญกว่าการลุ้นจังหวะสั้น ๆ คือการมีพอร์ตที่จัดโครงสร้างดีพอสำหรับหลายสภาวะตลาด

Beyond Wealth จึงจัดทีมกองทุนในแผน 4-3-3 เพื่อให้เห็นบทบาทของแต่ละกองทุนในพอร์ตอย่างชัดเจน

กองหน้า คือกลุ่มที่เน้นสร้างโอกาสเติบโต เพิ่มศักยภาพผลตอบแทนเชิงรุกให้พอร์ต

นำโดย MEGA10AI, SCBKEQTG และ LHCOPPER

กองกลาง คือกลุ่มที่ช่วยกระจายความเสี่ยง คุมจังหวะพอร์ต และลดการพึ่งพาตลาดใดตลาดหนึ่งมากเกินไป

ประกอบด้วย K-VIETNAM, ES-EG และ ASP-NGF

กองหลัง คือกลุ่มที่เน้นลดความผันผวน เสริมความมั่นคงให้พอร์ตในช่วงตลาดแกว่ง

ได้แก่ KKP-INCOME, UGIS, KT-CSBOND และ MAUTOCALL

ส่วน ผู้รักษาประตู อย่าง SCBGOLD ทำหน้าที่เป็นสินทรัพย์ป้องกันความเสี่ยง ช่วยรับมือกับความไม่แน่นอน ทั้งจากดอกเบี้ย ค่าเงิน ภูมิรัฐศาสตร์ และความผันผวนของตลาดโลก

📌 มุมมอง Beyond Wealth

สถิติในอดีตบอกเราว่า ช่วงฟุตบอลโลกอาจไม่ได้ทำให้ตลาดหุ้นขึ้นหรือลงแบบตายตัว เพราะผลลัพธ์หลังการแข่งขันขึ้นอยู่กับปัจจัยใหญ่กว่า ทั้งวัฏจักรเศรษฐกิจ เงินเฟ้อ ดอกเบี้ย กำไรบริษัทจดทะเบียน และความเสี่ยงภูมิรัฐศาสตร์

พอร์ตที่ดีจึงไม่จำเป็นต้องบุกหนักตลอดเวลา แต่ควรเป็นพอร์ตที่ “ยืนระยะได้” ในหลายสภาวะตลาด

ช่วงตลาดเปิดเกมรุก กองหน้าต้องเป็นตัวเร่งผลตอบแทน แต่ในวันที่ตลาดผันผวน กองกลาง กองหลัง และผู้รักษาประตูจะเป็นส่วนสำคัญที่ช่วยให้พอร์ตไม่เสียสมดุล

หัวใจของการลงทุนไม่ใช่การเลือกกองทุนที่ดูเด่นเพียงตัวเดียว แต่คือการจัดบทบาทของแต่ละกองทุนให้เหมาะกับเป้าหมาย ระยะเวลาลงทุน และระดับความเสี่ยงที่รับได้

เพราะสุดท้ายแล้ว ทั้งฟุตบอลและการลงทุนไม่ได้ชนะด้วยการบุกอย่างเดียว แต่ชนะด้วย “ทีมที่สมดุล” และแผนการเล่นที่เหมาะกับทุกจังหวะ

#BeyondWealth #BeyondSecurities #AssetAllocation #WorldCup2026

56

Jun 14

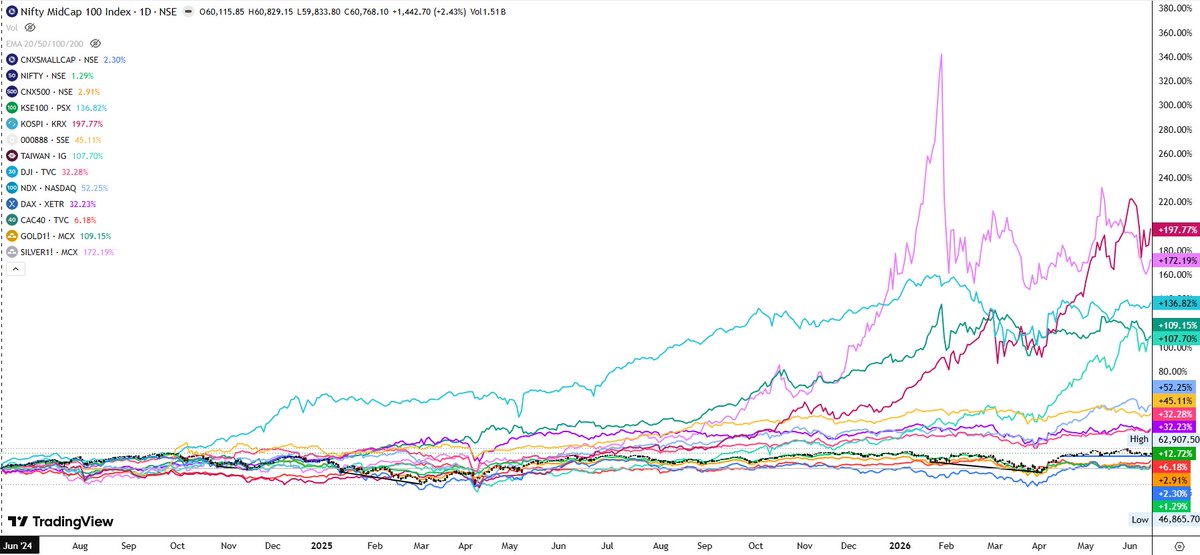

#Investing #Investment #Bullish #Nifty #Midcap #StockMarketIndia #Investing #TechnicalAnalysis #Nifty500 #Gold #Silver #Nifty50 #Investing #Commodities #AssetAllocation #MacroEconomics

🧵 Asset Class Performance: Equities Stall, While Gold & Silver Explode into a Mega Bull Run! 🪙🚀

If you are still only tracking equity returns, you are missing out on the real kings of the last 24 months. Between June 2024 and June 2026, precious metals have completely stolen the show while domestic equities remained locked in a tight consolidation.

The multi-asset leaderboard tells a fascinating macro story: 👇

1️⃣ The New Global Performance Leaderboard

🟣 KOSPI (South Korea Equity): 🚀 197.77% (Leading global tech/hardware)

🌸 SILVER (MCX): 🥈 172.19% (Outsized gains — Commodity Super-Cycle)

🟢 KSE 100 (Pakistan): 📈 136.82%

🟢 GOLD (MCX): 🥇 109.15% (Wealth protection turning into a multi-bagger)

🟢 TAIWAN (Taiwan Tech): 💻 107.70%

🔵 NASDAQ (US Tech): 🇺🇸 52.25%

🇮🇳 Indian Equities (Nifty/Nifty 500): 📊 1% to 3% (Completely flatlined).

@DAmmannaya

@drprashantmish6

@DRCHETANLALSETA

@VijayThk

@ADX_Learner

@AmitabhJha3

@TraderHarneet

@garwasanjay

@Rishikesh_ADX

@Investor_Mohit

@jitu_stock

2

2

237

Jun 13

You don’t need a crystal ball or a stock tip.

You need a clean asset allocation and a way to keep it in line.

Enrich lets you:

• Connect all your accounts in one place.

• Set goal‑based target allocations for each bucket in your life.

• Track drift and get step‑by‑step rebalance instructions when it’s time to act.

You stay in control of every trade. Flat subscription, no AUM.

#assetallocation #diyinvesting #goalbasedinvesting #taxawareinvesting #indexinvesting #longterminvesting #enrichfinance #personalfinance #investing

9