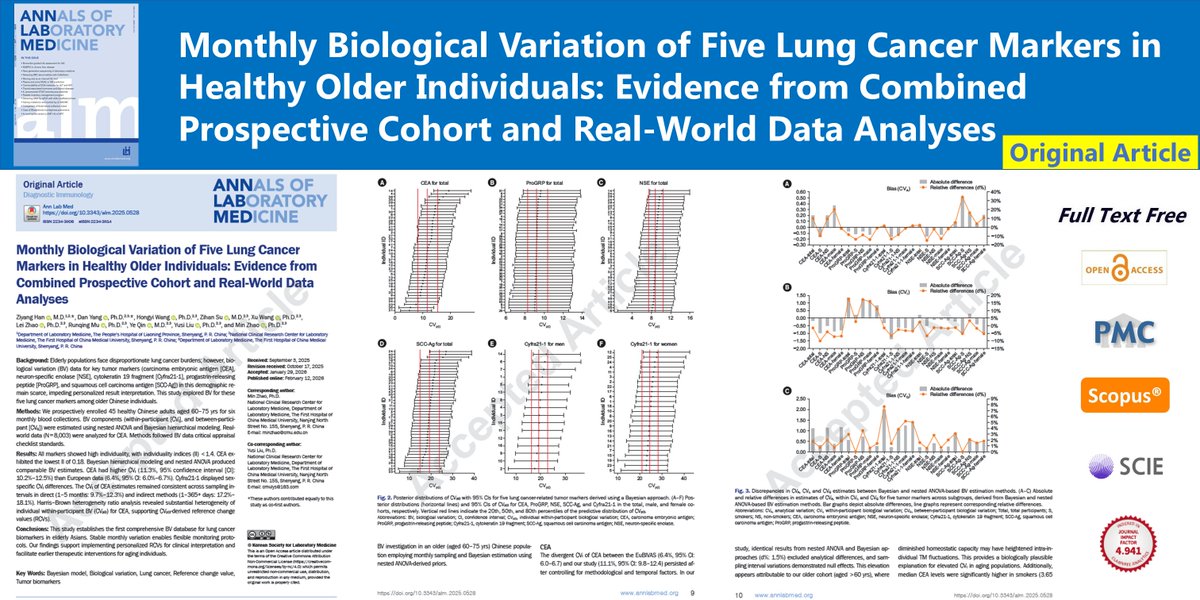

Monthly Biological Variation of Five Lung Cancer Markers in Healthy Older Individuals: Evidence from Combined Prospective Cohort and Real-World Data Analyses

🌷doi.org/10.3343/alm.2025.052…

Ann Lab Med. February 12, 2026. Ziyang Han

#BayesianModel #LungCancer #TumorBiomarkers

1

2

31

2 Sep 2025

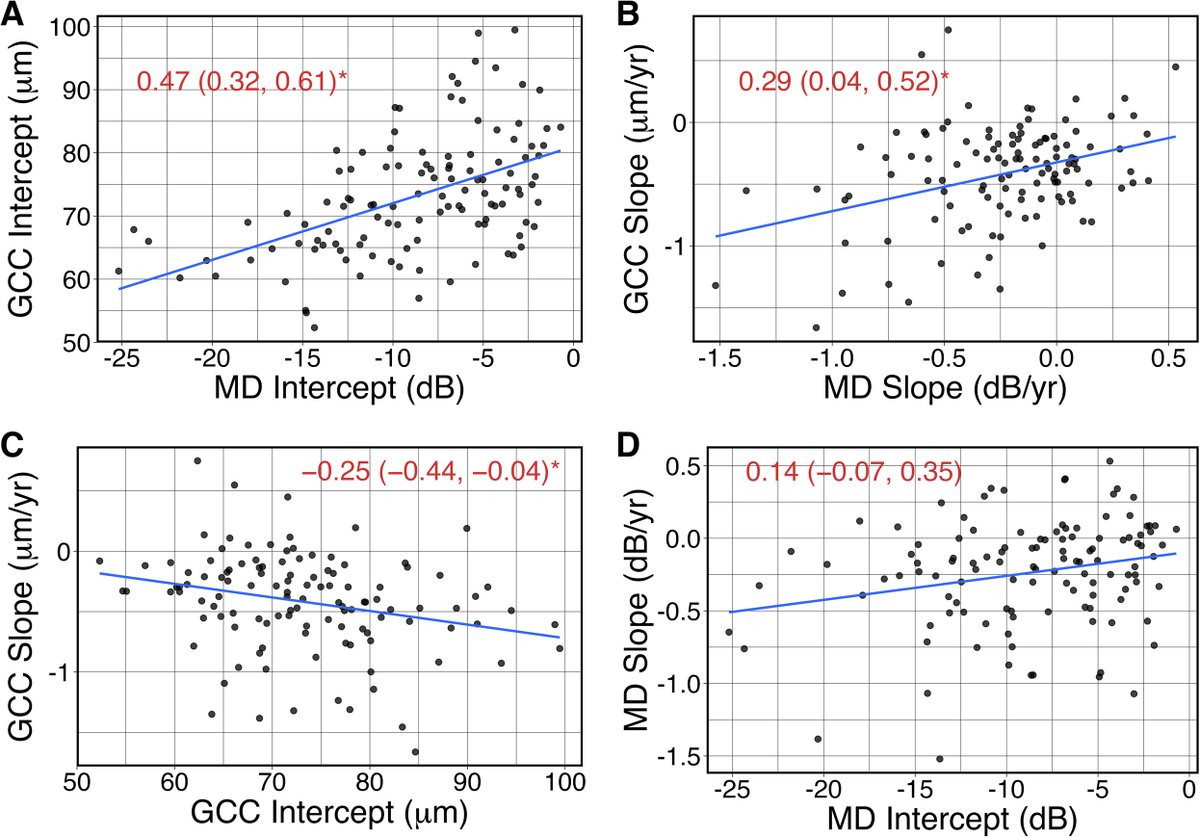

A Bayesian joint bivariate longitudinal model examines structure-function relationships in glaucoma. New paper outlines slope estimation and prediction accuracy vs. SLR, supporting better monitoring of disease progression. #glaucoma #BayesianModel

ow.ly/ZFYr50WyIqf

2

1

6

775

22 Jul 2025

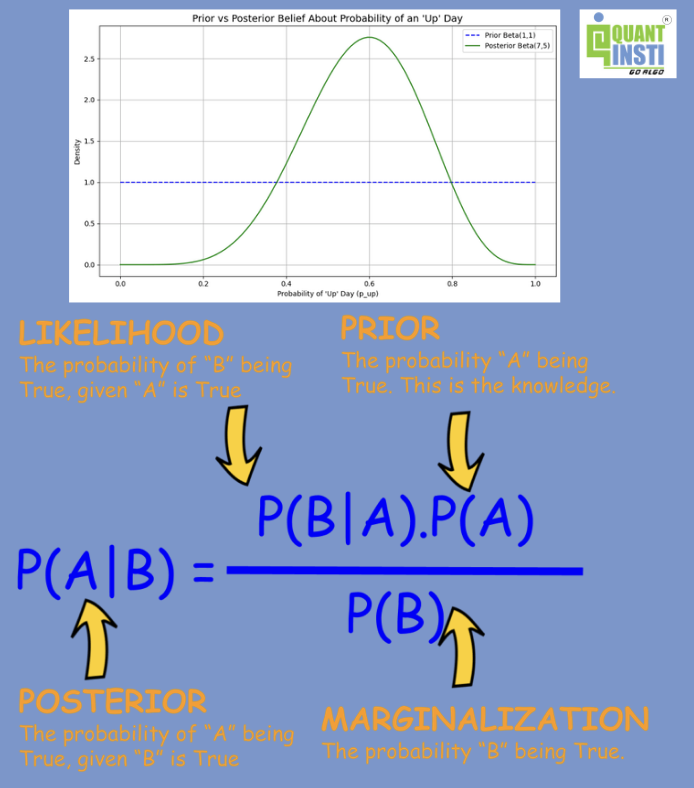

📊 Exploring Bayesian Techniques in Algorithmic Trading

Bayesian methods provide a framework in which probabilities are updated as new information becomes available, making them particularly relevant for evolving financial systems.

This project outlines how such techniques were applied to trading-related tasks involving price prediction, parameter adaptation, and risk evaluation.

🔍 Project Highlights

• Built two deep learning models to forecast open prices of the Bank Nifty index and its top five constituents

• Used 21 months of 1-minute data and 20 years of daily data for training/testing

• Integrated techniques such as SMOTE for class imbalance and XGBoost for feature ranking

• Applied Keras callbacks (EarlyStopping, ModelCheckpoint) to address overfitting

• Focused on consensus-based signals, where both models must agree before executing trades

• Managed minute-level and daily datasets using a MySQL database

🧠 Tools and Techniques Used

TensorFlow & Keras

Scikit-learn, XGBoost, TA-Lib

SMOTE (Imbalanced-learn)

Feature engineering with RSI, MFI, ATR, Bollinger Bands, and more

Read the full guide with the entire project here: blog.quantinsti.com/introduc…

📚 For readers interested in related topics:

Quant Roles Overview: quantinsti.com/quant-roles

Quantitative Trader: quantinsti.com/articles/quan…

Quant Analyst & Researcher: quantinsti.com/articles/quan…

Quant Developer: quantinsti.com/quant-roles/q…

Risk Analyst: quantinsti.com/articles/risk…

🔗 Learn more about the EPAT programme: quantinsti.com/epat

📣 🔴 Detailed EPAT Walkthrough & AMA | Live Webinar

Join us for a dedicated session exploring the Executive Programme in Algorithmic Trading (EPAT).

Get a comprehensive overview of the 6-month journey, support offered, alumni success, and post-programme career services. The session concludes with a live Q&A.

🗓️ Thursday, July 24, 2025

🕗 8:30 AM EST | 6:30 PM IST | 9:00 PM SGT

🎤 Speaker: Rohan Mathews, Global Business Head – QuantInsti

🔗 Register: quantinsti.com/epat

#QuantInsti #EPAT #AlgorithmicTrading #QuantRoles #DeepLearning #PythonForFinance #BayesianModel #TradingSystems #FinancialData #Backtesting #QuantitativeFinance #FeatureEngineering

1

3

289

6 May 2025

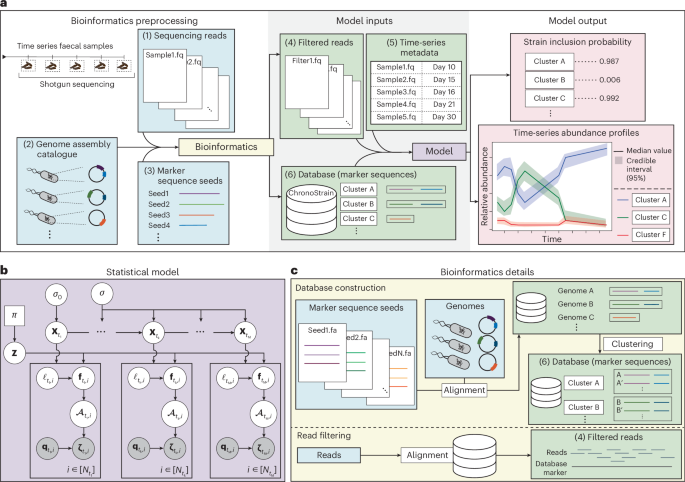

Out Now! Longitudinal profiling of low-abundance strains in microbiomes with ChronoStrain bit.ly/3RR64eE #Microbiology #Microbiome #BayesianModel

20

54

6,011

6 Jun 2024

Bayesian Approach Enhances Understanding and Prediction of Leishmania Disease - scft.link/vXIMV

Dr. Felix Pabon-Rodriguez from Indiana University School of Medicine and his team developed a Bayesian joint model to better understand and predict Leishmania disease progression.

The research, published in PLOS ONE, integrates longitudinal data and time-to-event data to explore the interactions between pathogen load, immune responses, and disease outcomes.

#BayesianModel #LeishmaniaResearch #InfectiousDisease #Biostatistics #ImmuneResponse #sciencefeatured #sciencenews

4

32,847

JM! Don't miss the opportunity to read the #originalarticle, #openaccess “Allergen #immunotherapy in #MASK-air users in real-life: Results of a #Bayesian mixed-effects model” published in the #CTA_Journal.

Here 🔗 onlinelibrary.wiley.com/doi/…

#allergen #MASKair #Bayesianmodel

1

3

442

27 Oct 2023

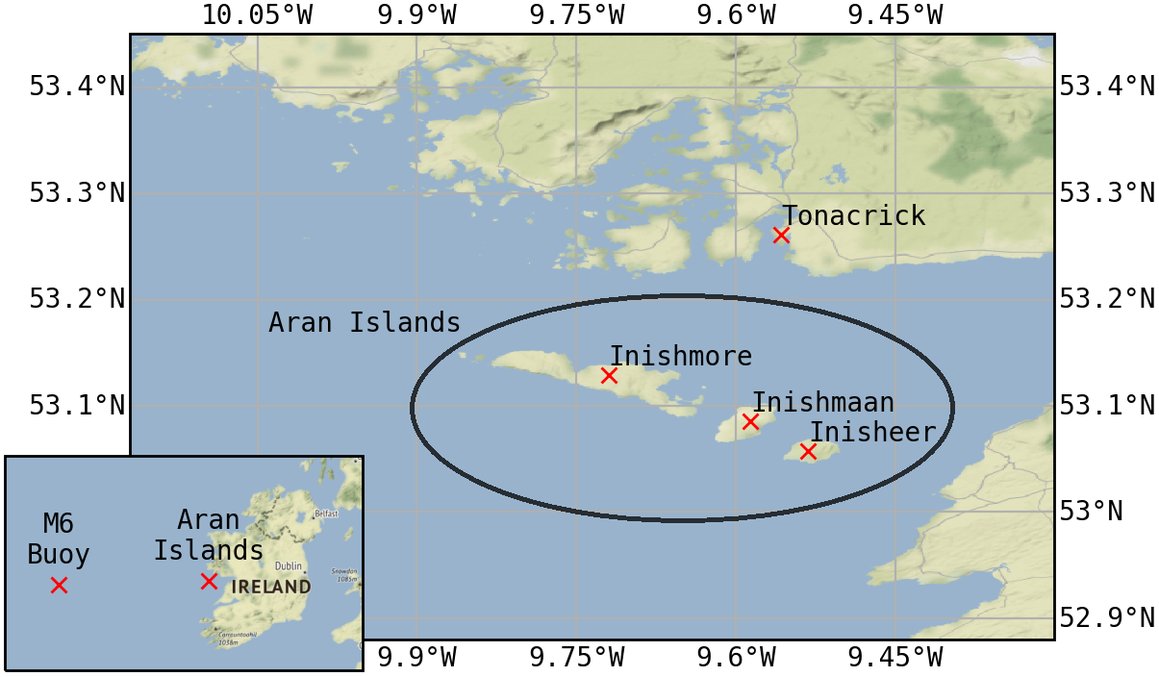

Boosting sea state forecasts for the Aran Islands! This study combines local-scale forecasts and Bayesian Model Averaging to improve accuracy by 1-8%. An accessible method for anyone reliant on precise sea state predictions, with minimal computational power needed. 🌊⚡️

Tatjana Kokina (@koksikt), Daniel Santiago Peláez-Zapata, Thomas Brendan Murphy & Frédéric Dias (@FredericDiasUCD)

@CentreBorelli

-> doi.org/10.1017/eds.2023.31

#seastateforecast #BayesianModel #waves #wavestatistics #weatherprediction #Aran

6

11

1,478

26 Apr 2023

New experiment: launching my @topmateHQ page today, where you can book a 1:1 call or ask any queries you may have.

Whether you need help with a #BayesianModel, are looking for a #StatsModeling mentor, or even wanna chat on #GoingNomad -- I'm available!

Best Bayesian wishes 🖖

1

2

451

28 Jan 2023

6. Bayesian Model

Bayesian Model Selection is a method of comparing the relative likelihoods of different hypotheses given the data and selecting the hypothesis with the highest likelihood.

@hashnode @WeMakeDevs #bayesianmodel

1

2

28

6 Jan 2023

New #research - Spatially Varying Intergenerational Changes in the Prevalence of Female Genital Mutilation/Cutting in #Nigeria: Lessons Learnt from a Recent Household #Survey - @DHSprogram

#FGM #GBV #SDG5 #Geospatial #BayesianModel #DHSdata doi.org/10.1007/s12061-022-0…

1

2

460

4 Jan 2023

Variational inference uses optimization, rather than integration, to approximate the marginal likelihood, and thereby the posterior, in a Bayesianmodel.

📄 arxiv.org/abs/2301.01236v1

2

135

22 Sep 2022

New #research article related to our #ZeroDose work for @gavi - Conditional probability and ratio-based approaches for #mapping the coverage of multi-dose #vaccines - #Vaccination #BayesianModel #NigeriaDHS doi.org/10.1002/sim.9586

1

2

21 Sep 2022

New #research led by @Chigedson - Conditional probability and ratio-based approaches for #mapping the coverage of multi-dose #vaccines - in @WileyGlobal #StatisticsInMedicine #ZeroDose #Vaccination #BayesianModel #NigeriaDHS doi.org/10.1002/sim.9586

2

6

14 Sep 2022

New #research using our #population #opendata - The prevalence of #onchocerciasis in #Africa and #Yemen, 2000–2018: a #geospatial analysis - in @BMCMedicine led by @davidmpigott #BayesianModel bmcmedicine.biomedcentral.co…

1

3

13 Sep 2022

Research Fellow @Chigedson is @RSSAnnualConf presenting our new national #immunisation coverage methodology Background on this @WHO and @UNICEF funded #ZeroDose project:

worldpop.org/current-project…

#StatsMethods #BayesianModel

ALT Dr Chigozie Edson Utazi at the 2022 Royal Statistical Society conference

ALT Presentation title slide: Bayesian hierarchical modelling approaches for combining information from multiple data sources to produce annual estimates of national immunization coverage

1

7

My new paper is out in the ICES Journal of Mar. Sci.- @BouchardC_ et al: @ICES_ASC @OxfordJournals @OUPAcademic – tinyurl.com/5n7wcxns - #GlassEel #EuropeeanEel #recruitment #SpatialVariations #MediterraneanSea #BayesianModel @TourduValat @inrae_ecobiop @universite_uppa

3

3

The #originalarticle “#Allergenimmunotherapy in #MASK-air users in real-life: Results of a Bayesian mixed-effects model” published in the #CTA_Journal is available and #openaccess! 🔗Link: onlinelibrary.wiley.com/doi/… #allergen #bayesianmodel

3

4

6 Jun 2022

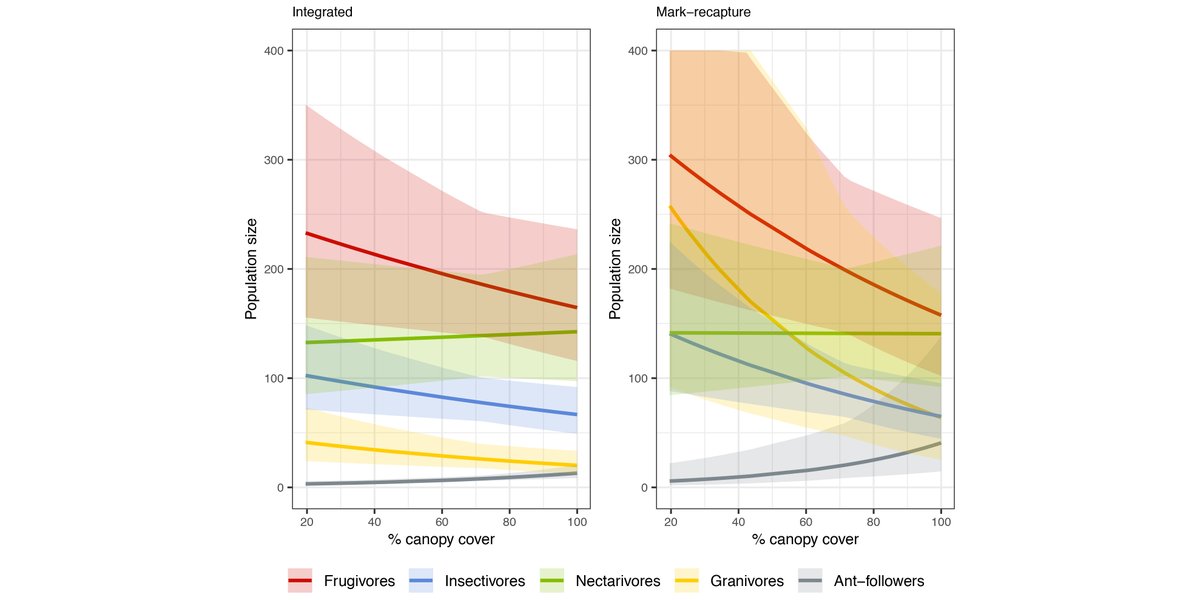

A new Statistical Report in @ESAEcology:

Integration of mark–recapture and acoustic detections for unbiased population estimation in animal communities

doi.org/10.1002/ecy.3769

With #OpenData in @figshare

@IBAHCM @__Biodiversity @CrinanJarrett

#PopulationSize

#BayesianModel

1

8

12

26 Nov 2021

scCODA is a Bayesian model for compositional single-cell data analysis. #scRNAseq #DataAnalysis #BayesianModel

nature.com/articles/s41467-0… @NatureComms

3

5

18 May 2021

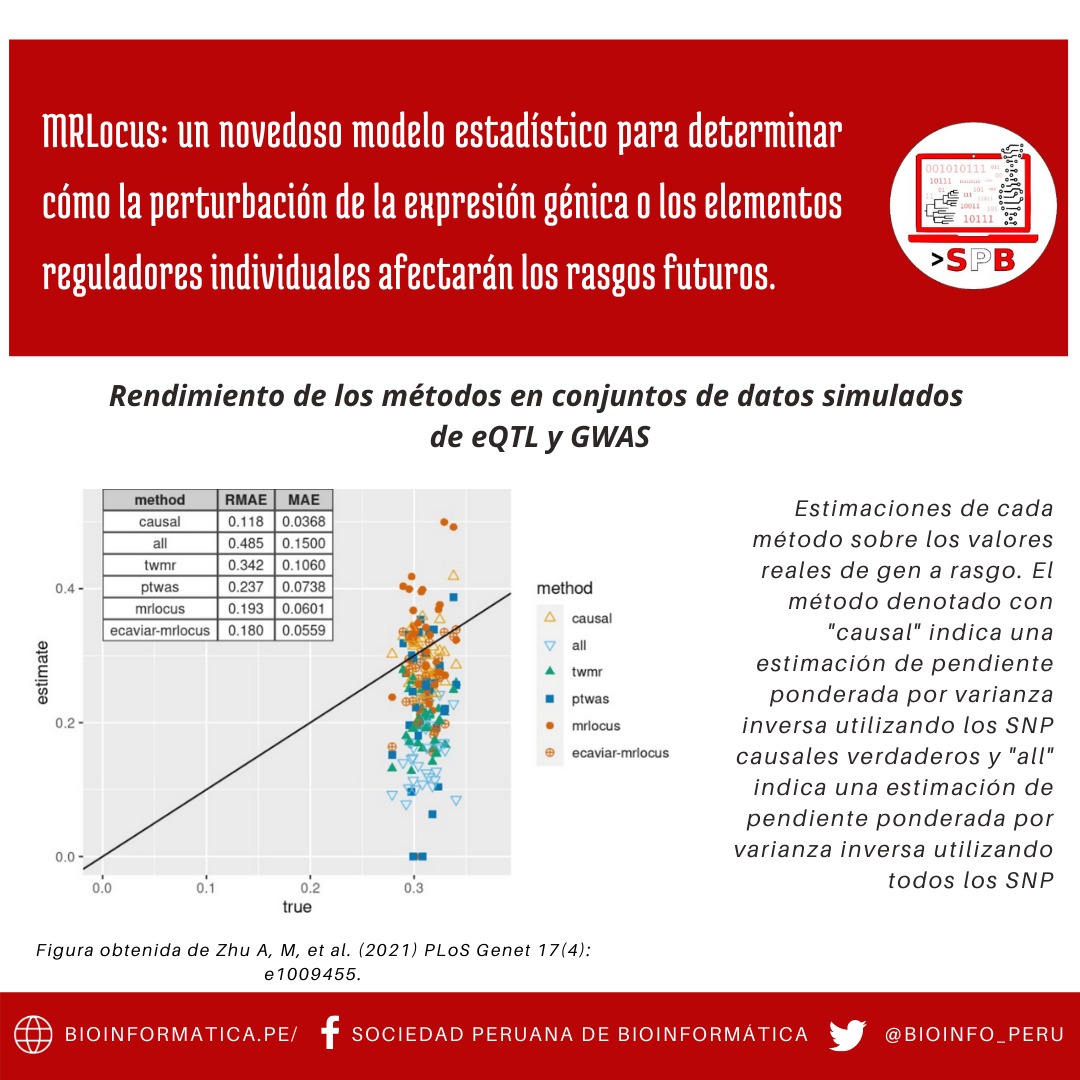

MRLocus: un novedoso modelo estadístico para determinar cómo la perturbación de la expresión génica o los elementos reguladores individuales afectarán a rasgos futuros.

#NewResearch #GeneExpression #GWAS #eQTL #RPackage #BayesianModel

(1/7)

1

5

15