Highlights on #ESMOBreast26 from #CommunityOnc:

Her2

1. #DB11 Update: NeoAdj TDXd

2. #PHERGain: De-escalation

3. #SATEEN: Sacituzumab

HR

4. #PREcoopERA: Role of OFS

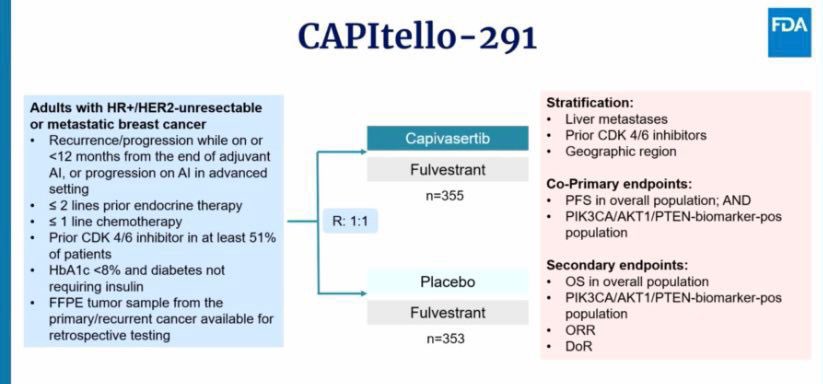

5. #CAPItello291 Update: Capivasertib

TNBC

6. #TROPIONBreast02: DatoDXd

#OncTwitter #bcsm @myESMO

1/7

3

49

115

10,524

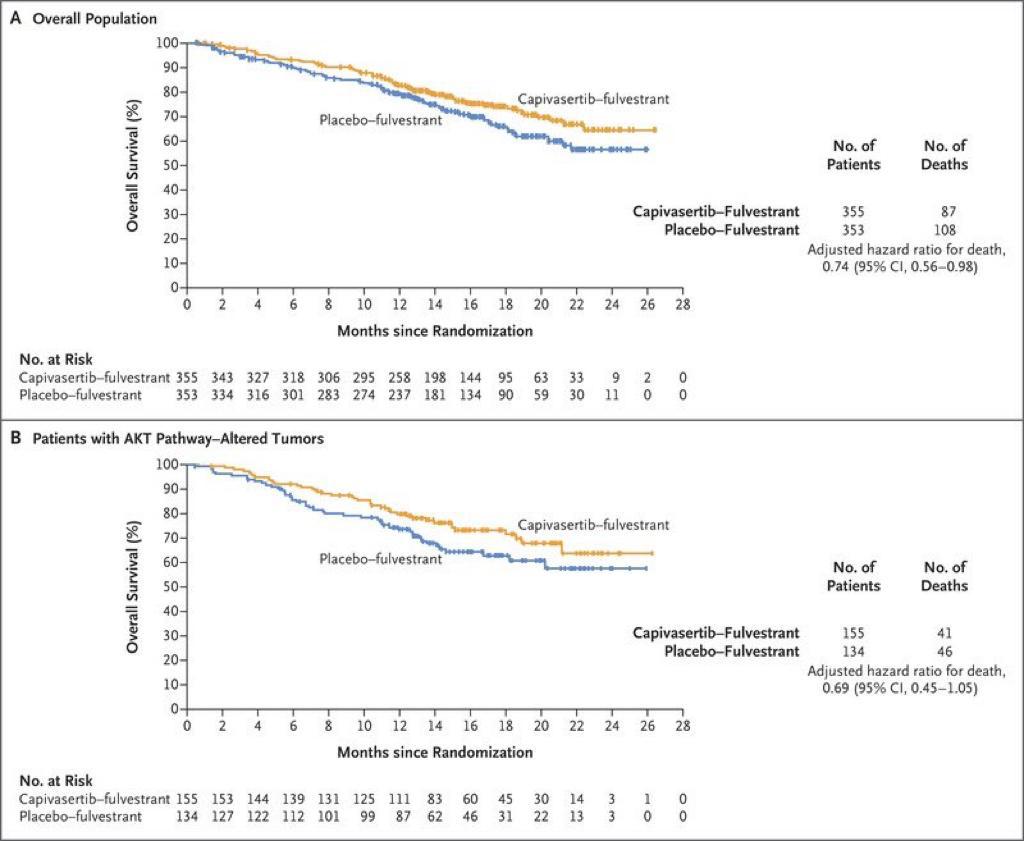

🔥 CAPItello-291 delivers a nuanced final OS story in HR /HER2− advanced breast cancer.

Final overall survival data showed that capivasertib fulvestrant did not significantly improve OS compared with placebo fulvestrant.

But the story does not end there.

In patients with PIK3CA/AKT1/PTEN-altered disease, capivasertib fulvestrant showed:

📌 Numerical OS trend, but not statistically significant

📈 Improved PFS2

⏳ Delayed time to first subsequent chemotherapy

🧬 Continued relevance of AKT pathway inhibition

✅ No new safety signals with longer follow-up

This matters because in HR /HER2− advanced breast cancer, delaying chemotherapy is still a meaningful clinical goal — especially when endocrine-based targeted therapy can extend disease control.

The key message from CAPItello-291 is not “OS positive.”

It is more precise than that:

👉 Capivasertib fulvestrant improves disease control and delays chemotherapy, even without a final OS advantage.

A good reminder that trial interpretation needs more than one endpoint.

oncodaily.com/oncolibrary/br…

@MOliveira_MD @JavierCortesMD @AstraZeneca

#CAPItello291 #Capivasertib #Fulvestrant #BreastCancer #MetastaticBreastCancer #HRPositiveBreastCancer #HER2Negative #PIK3CA #AKT1 #PTEN #ESMOBreast26 #OncoDaily #OncoDailyBreast

1

7

209

Apr 6

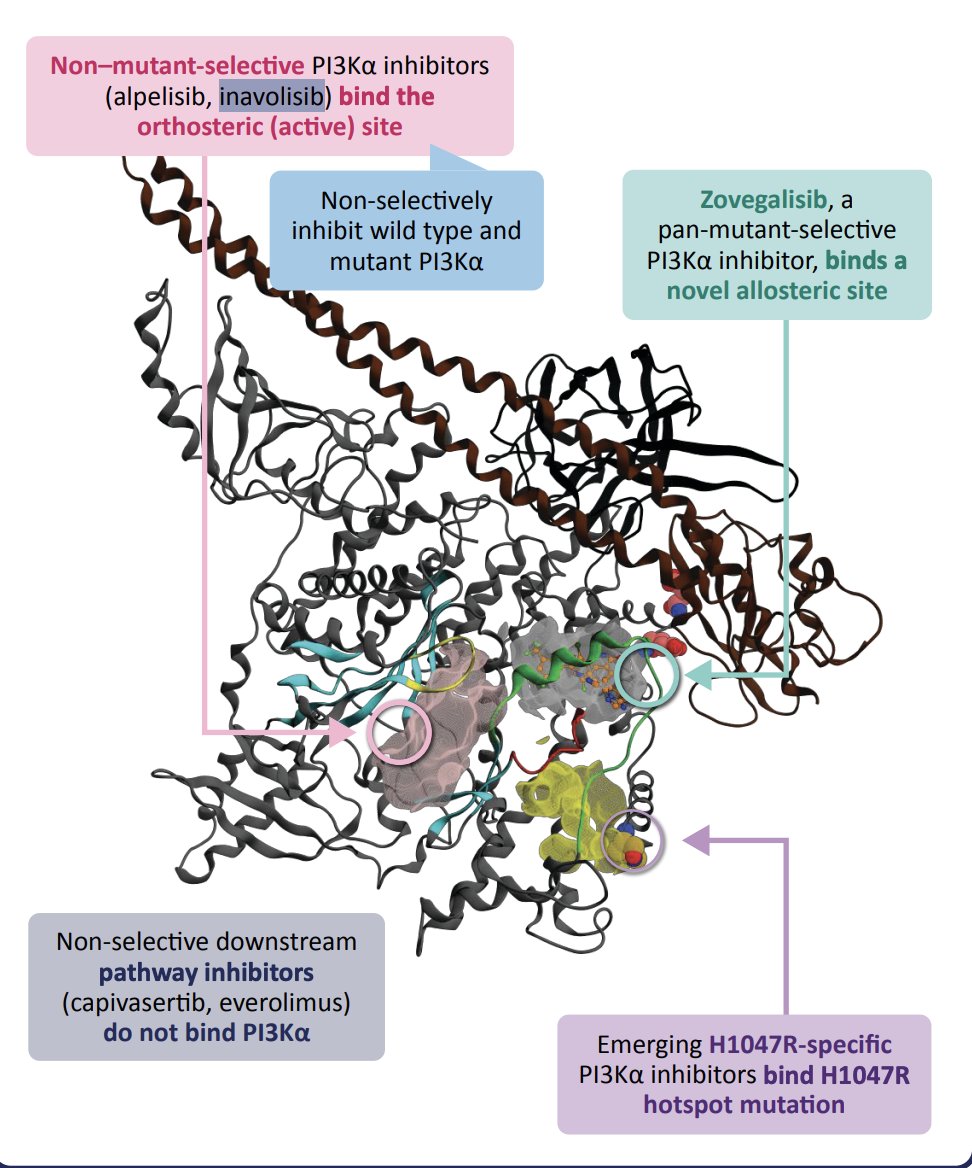

$RLAY is an interesting case study because from the time they announced their initial 2L pi3k serd PFS data in HER2-/HR breast cancer the stock went down ~60% over the next 5 months (coincident with bad macro environment) and then up ~530% over the next 12 months. As Jonathon points out, the stock steadily trended up from Apr 2025 to Mar 2026 to a current 2.2B market cap. How? Why?

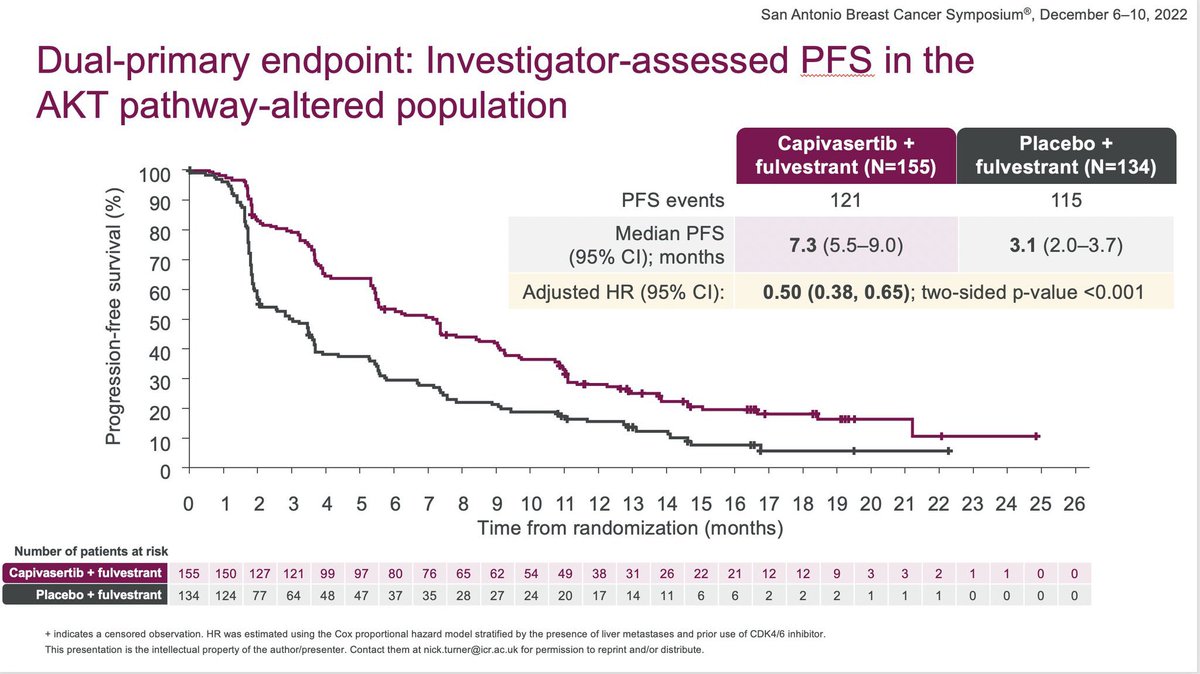

First, the PI3Ki HER2-/HR landscape has changed a but in the last few years. Invalosib (Roche), a selective PI3Kα inhibitor, recieved BTD in May 2024 and approval in October 2024 for triplet invalosib fulvestrant palbociclib in endocrine resistant HR /HER- mutant PIK3CA breast cancer. Improved median OS by 7 months from 27 to 34 compared to fulvestrant palbociclib (Jhaveri et al NEJM 2025). Capivasertib (AstraZeneca), a pan-AKT inhibitor, initially approved in late 2023 is indicated for PIK3CA/AKT1/PTEN-altered HR /HER2- breast cancers following at least 1 endocrine based therapy. In the CAPITello291 trial in this setting oround 70% of patients had prior CDK4/6 inhibitor therapy. In AKT altered tumors, overall survival was 70% at 20 months in capi-fulvestrant treated patients compared to ~60% at 20 months in fulvestrant monotherapy patients.

Positioning for zovegalisib $rlay is PIK3CA-mutant HR /HER2- breast cancer patients with prior treatment of 1-2 endocrine therapy and 1 CDK4/6 inhibitor therapy. Open label trial. Excluded if prior PIK3/AKT/mTOR pathway drug has been given. This means invalosib treated patients are ineligible. Of course, invalosib triplet is an earlier line of therapy so that narrows the pool of patients considerably for zovegalisib if approved. Has a 4 month PFS improvement relative to capi-fulvestrant comparing across trials (VERY rough, but that's what we have till the ReDISCOVER2 trial reads out)

Zovegalisib targets a different site on PI3Ka than inavolisib and is billed as a more mutant selective molecule. This comes with better tumor specificity and if so, less side effects. Relative to doublet, inavo triplet carries on an absolute basis, a 7% higher hyperglycemia grade 3 rate, 6% higher grade 3 stomatitis, 10% higher thrombocytopenia rate. Relative to fulvestrant, capi combination carries on an absolute basis, a 9% higher grade 3 diarrhea rate, 12% higher grade 3 rash, 2% grade 3 hyperglycemia rate. Absolute rates of grade 3 AEs at the phase 3 dose for zovegalisib is similar to inavo triplet and a bit better than capi-fulvestrant.

$rlay zoveg may be a more efficacious and tolerable drug than capi BUT the patient population is going to be cut considerably given $rlay can only give their drug to patients NOT given inavo triplet.

Summary of relevant corporate actions from Dec 2024 to Apr 2026:

- Reprioritized pipeline and focused on PIK3CA program after seeing interim safety and efficacy data in Q4 2024 from open-label phase 1 study.

- Jan through April of 2025, like most other small biotechs, stock got hit hard due to macro factors.

- Outlicensed FGFR2 program to Elevar, delayed initiation of fabry and nras programs (originally slated for 2025 IND but still yet to file), cut research programs and costs. More disciplined cash usage. Discipline, pare down.

- Board member stepped down and new board member appointed in June 2025. New board member experienced in oncology drug development.

- Aug 2025 start phase 3 trial. Primary completion expected in 2028.

- Brought in two other board members in Nov 2025 who were experienced in commercializing / developing biotech drugs.

- Get breakthrough designation from FDA in Feb 2026.

- Report data in Mar 2026 from open label phase 1b study at the phase 3 dose and compare efficacy/safety head to head against previous dose strategy (Dec 2024).

- Apr 2026 announced that they will present data on vascular abnormalities in May.

4

6

45

15,001

This episode of our #BreastCancerBreakthroughs series, has Drs. Harold Burstein (@DrHBurstein) and Erica Mayer (@elmayermd) discuss the #CAPItello291, #VIKTORIA1, and #STX478 trials which were presented at #SABCS25. Watch the recording here ⬇️

youtube.com/watch?v=clTOtLV5…

4

10

1,352

11 Dec 2025

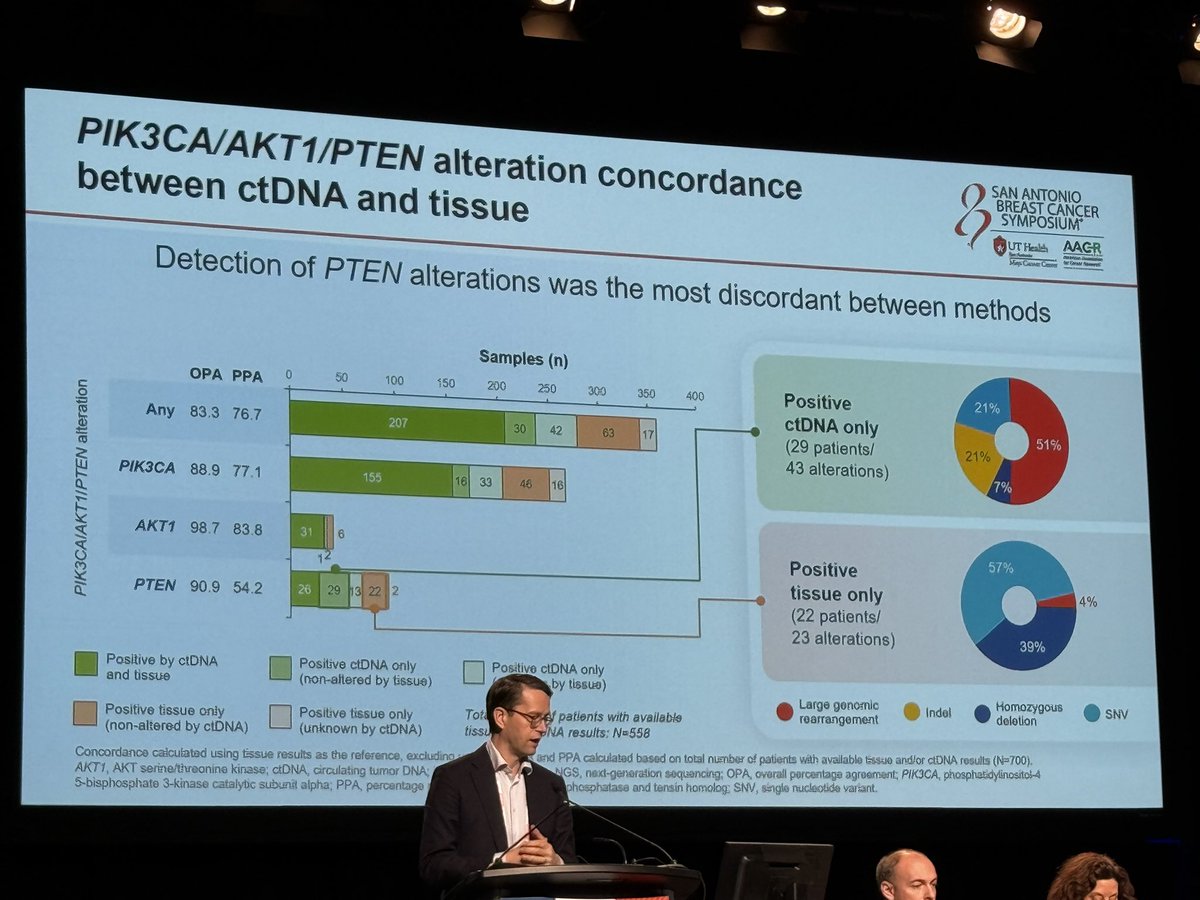

Interesting ctDNA sub-analysis from CAPItello291. Most PIK3CA/AKT/PTEN alterations are found both on tissue and ctDNA, but about 10% are found only on one of the two methods. PTEN alterations the most discordant. #SABCS25

2

16

51

4,548

28 Aug 2024

Inactivating alterations in PTEN by NGS was how capitello291 described eligibility #TumorBoardTuesday

28 Aug 2024

#TumorBoardTuesday

🙋I'm curious how they defined "PTEN altered"❓

➡️PTEN deletion/pathogenic alteration🧬

or

➡️Just loss of PTEN expression by IHC🔬

1

4

679

21 Jun 2024

Performance of single-agent fulvestrant after CDK4/6i in recent randomized trials for HR /HER2- mBC (median PFS):

- postMONARCH: 5.3 months

- PACE: 4.8 months

- PALMIRA: 3.6 months

- MAINTAIN: 2.7 months

- CAPItello291: 2.6 months

- EMERALD: 1.9 months

9

23

121

12,503

20 May 2024

🚨 The @OncoAlert COMPLETE COVERAGE of #ESMOBreast24 is COMING!

REGISTER TO GET IT: 👉 Oncoalert360.com👉 Newsletter Registration

Covering:

🎯IMPASSION132

🎯CAPITELLO291

🎯PF-07220060

🎯TROPION-BREAST01

🎯BRCA BCY

🎯NATALEE

🎯CARABELA

🎯MORPHEUS-PAN BC

🎯HER2DX

🎯IPATHER

🎯PANTHER

🎯PREFERABLE-EFFECT

🎯DESTINY BREAST 02

19 May 2024

The @OncoAlert 🚨COMPLETE COVERAGE of #ESMOBreast24🇩🇪is COMING

✉️REGISTER TO GET IT at Oncoalert360.com or oncoalert.m-pages.com/nhMpwe…

Covering:

✅IMPASSION132💊

✅CAPITELLO291

✅PF-07220060

✅TROPION-BREAST01

✅BRCA BCY🤰

✅NATALEE

✅CARABELA

✅MORPHEUS-PAN BC

✅HER2DX🧬

✅IPATHER

✅PANTHER🐈⬛

✅PREFERABLE-EFFECT🏃♀️

✅DESTINY BREAST 02

These are our picks of some of the top #BreastCancer trials presented

@matteolambe @aftimosp @E_de_Azambuja @NicoleKuderer @FAndreMD @prat_aleix @DrSGraff @jesusanampa @StoverLab @curijoey @ErikaHamilton9 @double_whammied @stage4kelly @coffeemommy @itsnot_pink @maryam_lustberg @IBCResearch @kevinpunie @raalbany @hoperugo @teamoncology @stolaney1 @LoiSher @SirohiBhawna @chemobrainfog @jamecancerdoc @JavierCortesMD @JaniceTNBCmets @paspears88 @MammaMiaMagazin @itrisabel

#OncoAlertAF

@nataliagandur @acampsmalea @MartaPerachino @heinrich_kat @BiagioRicciutMD @DenizCanGuven1

@yekeduz_emre @HHorinouchi @FadiHaddad_MD

@Dr_Ivanoncologo @Abdallah81MD @FernandoOnco

@ElisaAgostinett @dr_yakupergun @to_be_elizabeth @anmwongNZ

@VJOncology @high5md

1

1

8

2,182

19 May 2024

The @OncoAlert 🚨COMPLETE COVERAGE of #ESMOBreast24🇩🇪is COMING

✉️REGISTER TO GET IT at Oncoalert360.com or oncoalert.m-pages.com/nhMpwe…

Covering:

✅IMPASSION132💊

✅CAPITELLO291

✅PF-07220060

✅TROPION-BREAST01

✅BRCA BCY🤰

✅NATALEE

✅CARABELA

✅MORPHEUS-PAN BC

✅HER2DX🧬

✅IPATHER

✅PANTHER🐈⬛

✅PREFERABLE-EFFECT🏃♀️

✅DESTINY BREAST 02

These are our picks of some of the top #BreastCancer trials presented

@matteolambe @aftimosp @E_de_Azambuja @NicoleKuderer @FAndreMD @prat_aleix @DrSGraff @jesusanampa @StoverLab @curijoey @ErikaHamilton9 @double_whammied @stage4kelly @coffeemommy @itsnot_pink @maryam_lustberg @IBCResearch @kevinpunie @raalbany @hoperugo @teamoncology @stolaney1 @LoiSher @SirohiBhawna @chemobrainfog @jamecancerdoc @JavierCortesMD @JaniceTNBCmets @paspears88 @MammaMiaMagazin @itrisabel

#OncoAlertAF

@nataliagandur @acampsmalea @MartaPerachino @heinrich_kat @BiagioRicciutMD @DenizCanGuven1

@yekeduz_emre @HHorinouchi @FadiHaddad_MD

@Dr_Ivanoncologo @Abdallah81MD @FernandoOnco

@ElisaAgostinett @dr_yakupergun @to_be_elizabeth @anmwongNZ

@VJOncology @high5md

1

25

58

39,871

6 Dec 2023

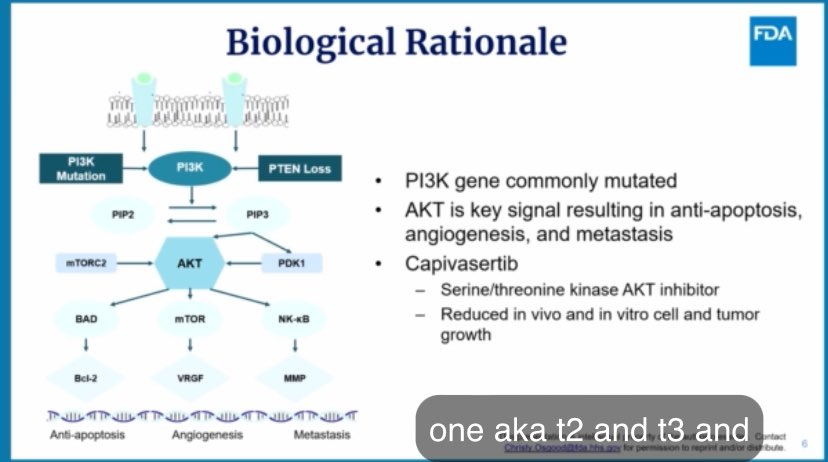

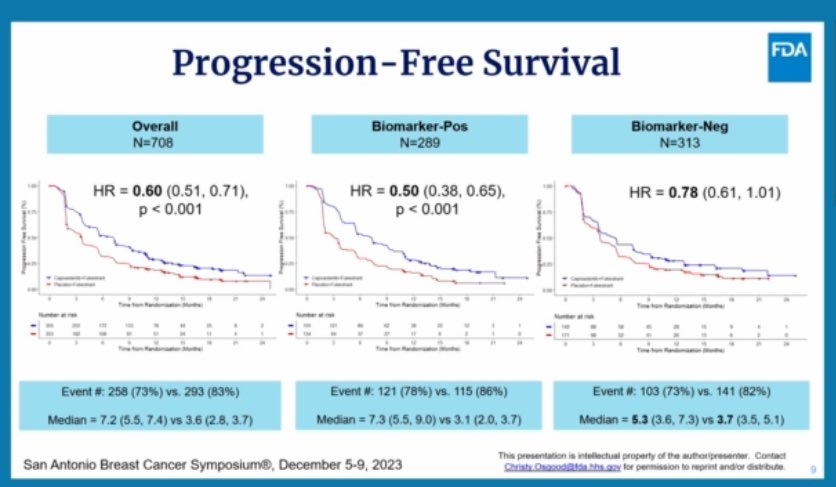

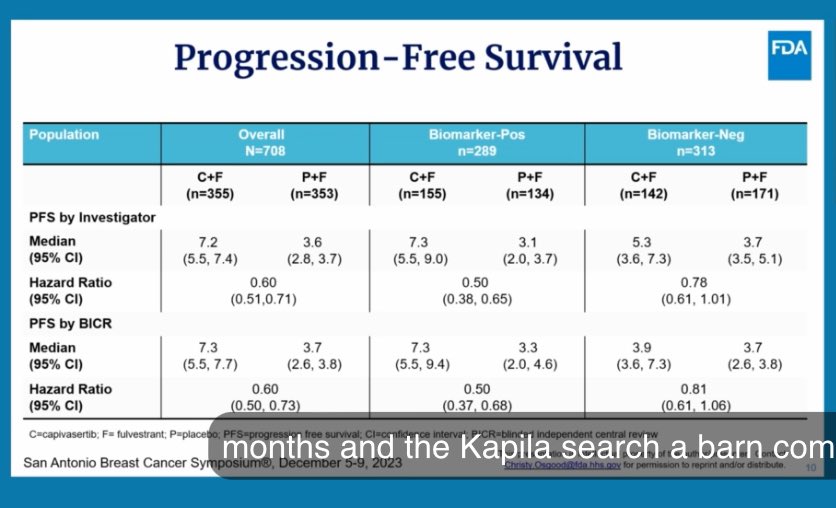

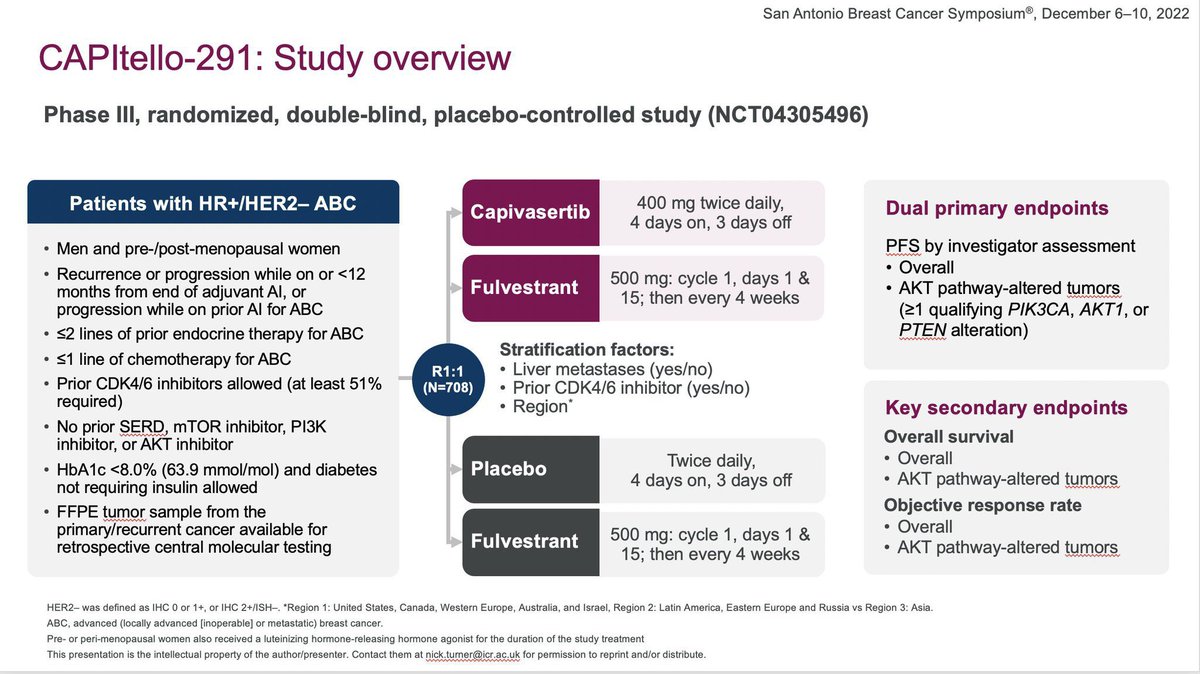

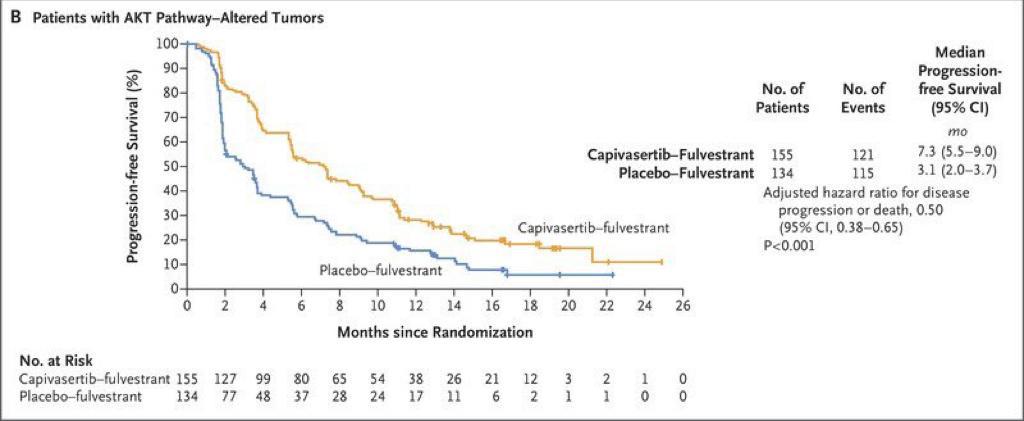

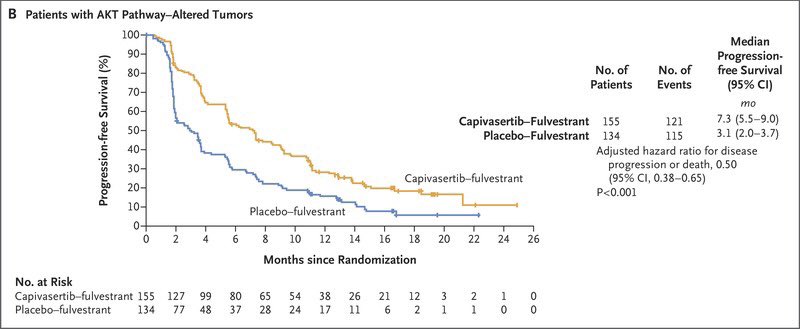

1. #Capivasertib approved on 11/16/23 w/ AKT pathway alteration based off: #CAPItello291. Capi Fulvestrant vs Fulvestrant Placebo

- ⬆️ PFS w/ capivasertib 7.2mos vs 3.6mos (HR 0.60)

- Pending OS

- 400mg BID, 4days on/3days off

x.com/stage4kelly/status/173…

#bcsm

2/6

5 Dec 2023

Finally, and only approved a couple of weeks ago, is Capivasertib (Trucap), an AKT inhibitor, approved for those with mutations in the PIK3CA-AKT-MTOR pathway or loss of PTEN. PFS was better in those with these mutations, confirmed by blinded independent review. #SABCS23

1

5

1,527

6 Dec 2023

#SABCS23 Day 1 Highlights #CommunityOnc:

@FDAOncology Review on recent approvals

1. #CAPItello291

2. #EMERALD

3. #TDxD

4. Tumor Agnostic landscape

5. Post CDK4/6i HR

@SABCSSanAntonio @VivekSubbiah @VKaklamani @JaniceTNBCmets #bcsm @DrSGraff @oreganruth

1/6

2

38

104

16,099

17 Nov 2023

بالامس وافقت #USFDA على الدواء Capivasertib لمرضى سرطان الثدي الهرموني المنتشر بالجسم Metastatic Breast Cancer Hormone Positive

جاءت الموافقه بعد النتائج لدراسه #CAPItello291 تم فيها مقارنه استخدام الدواء بالاضافه الى دواء ال fulvestrant لبحث استدامه مقاومه تطور المرض PFS

1

8

26

20,875

17 Nov 2023

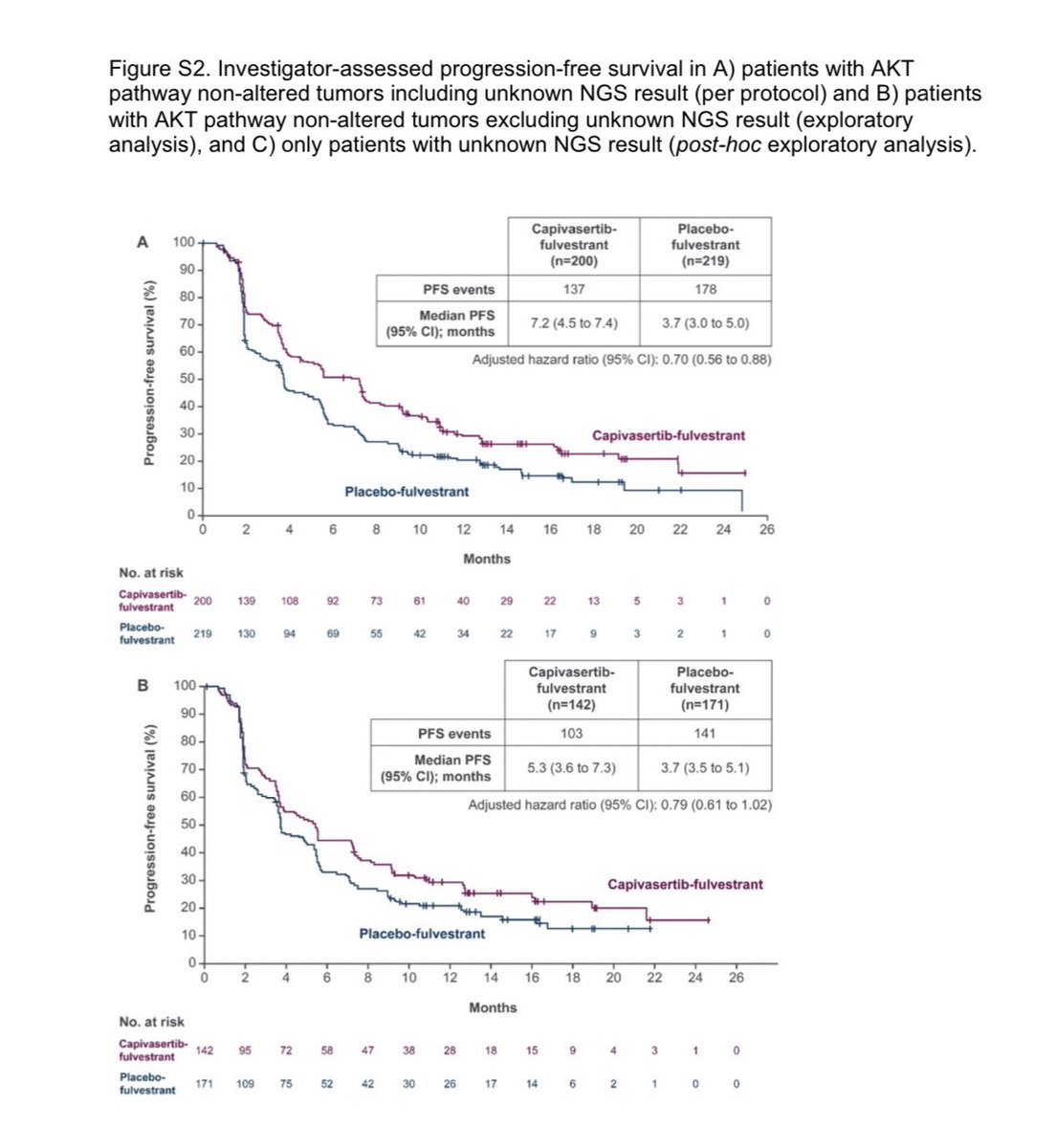

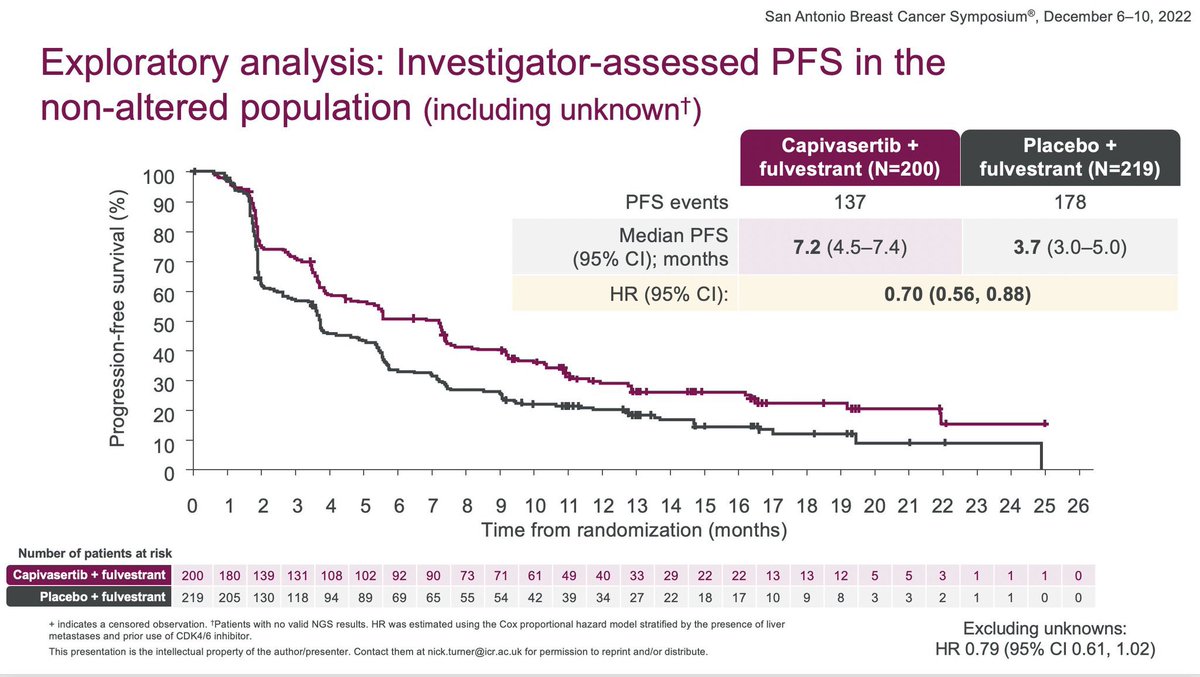

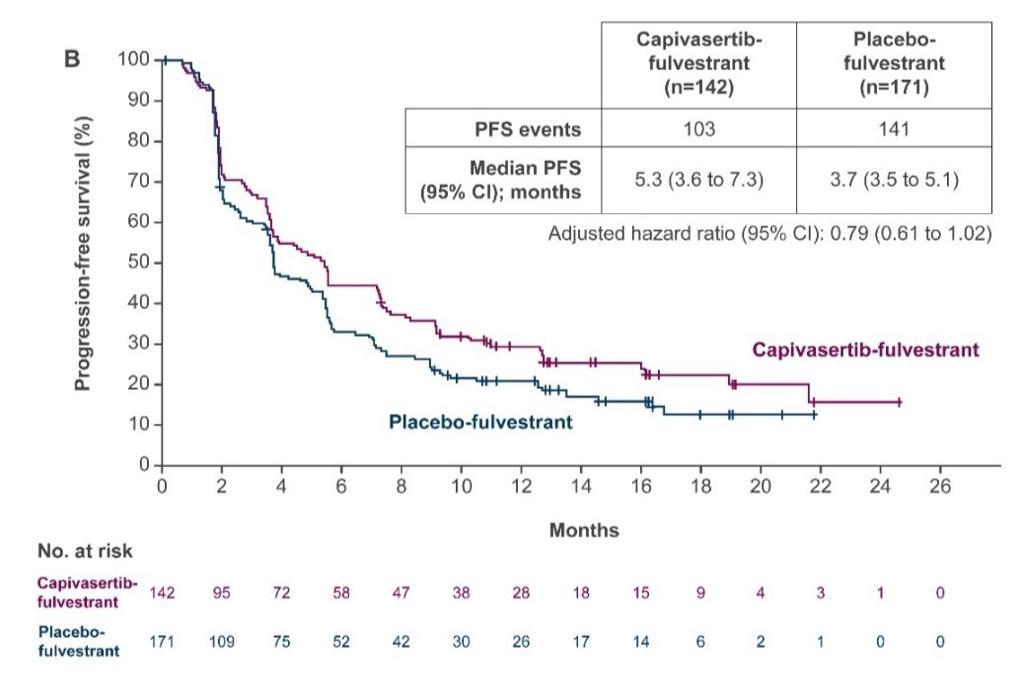

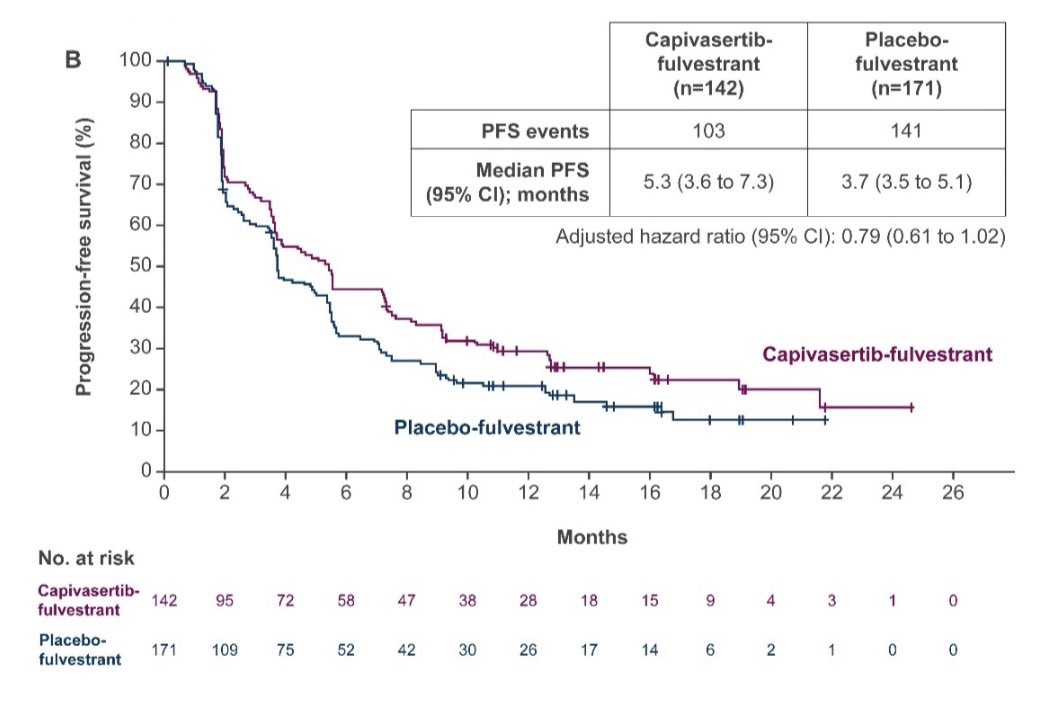

I'm confused by this, Capitello291 is Positive in the overall and in the Non-altered population with a similar trend (albeit underpowered in a small subgroup) HR 0.79 (0.61-1.02).

I would like to check the FDA review document to see why it was limited to the mutated population.

5

318

16 Nov 2023

#Capivasertib now @FDAOncology approved w/ AKT alteration based off: #CAPItello291: Capi Fulvestrant vs Fulvestrant Placebo

- ⬆️ PFS w/ capivasertib 7.2mos vs 3.6mos (HR 0.60)

- Pending OS

- 400mg BID, 4days on/3days off

- Diarrhea a big SE

#bcsm #MedTwitter #OncTwitter

2

33

88

20,004

CAPItello291 is now out in NEJM! Capivasertib–fulvestrant combo resulted in significantly longer pfs fulvestrant alone post cdk4/6i. This is going to change we practice!

1

3

505

31 May 2023

Pre-ASCO treat: #CAPItello291 is now out on NEJM! Meaningful improvement in PFS with capivasertib added to fulvestrant, particularly in Akt-path altered tumors (40%); benefit less clear in non-altered tumors. Tox: diarrhea (72%), rash (38%) & nausea (34%). nejm.org/doi/full/10.1056/NE…

2

56

165

30,566

24 May 2023

🎥 @matteolambe explains that we have more data from #ESMOBreast23 on the role of neoadjuvent therapies, that is the most promising way to implement immunotheraphy in early #Breastcancer.

Watch: 👉medicaldigest.org/scientific…👈

@UniGenova @SanMartino_Ge @myESMO #CAPItello291 #DESTINYBreast04 #IMpassion031

3

9

1,407

11 May 2023

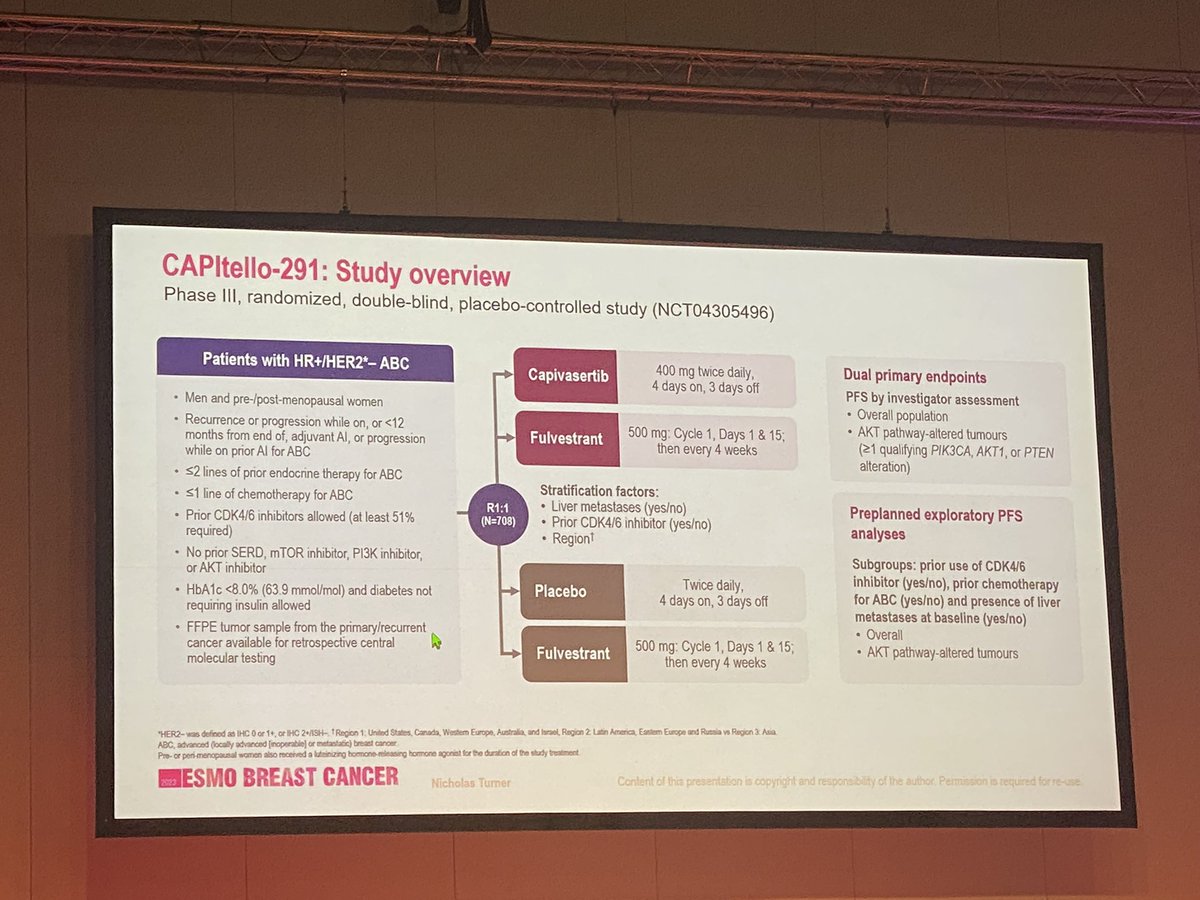

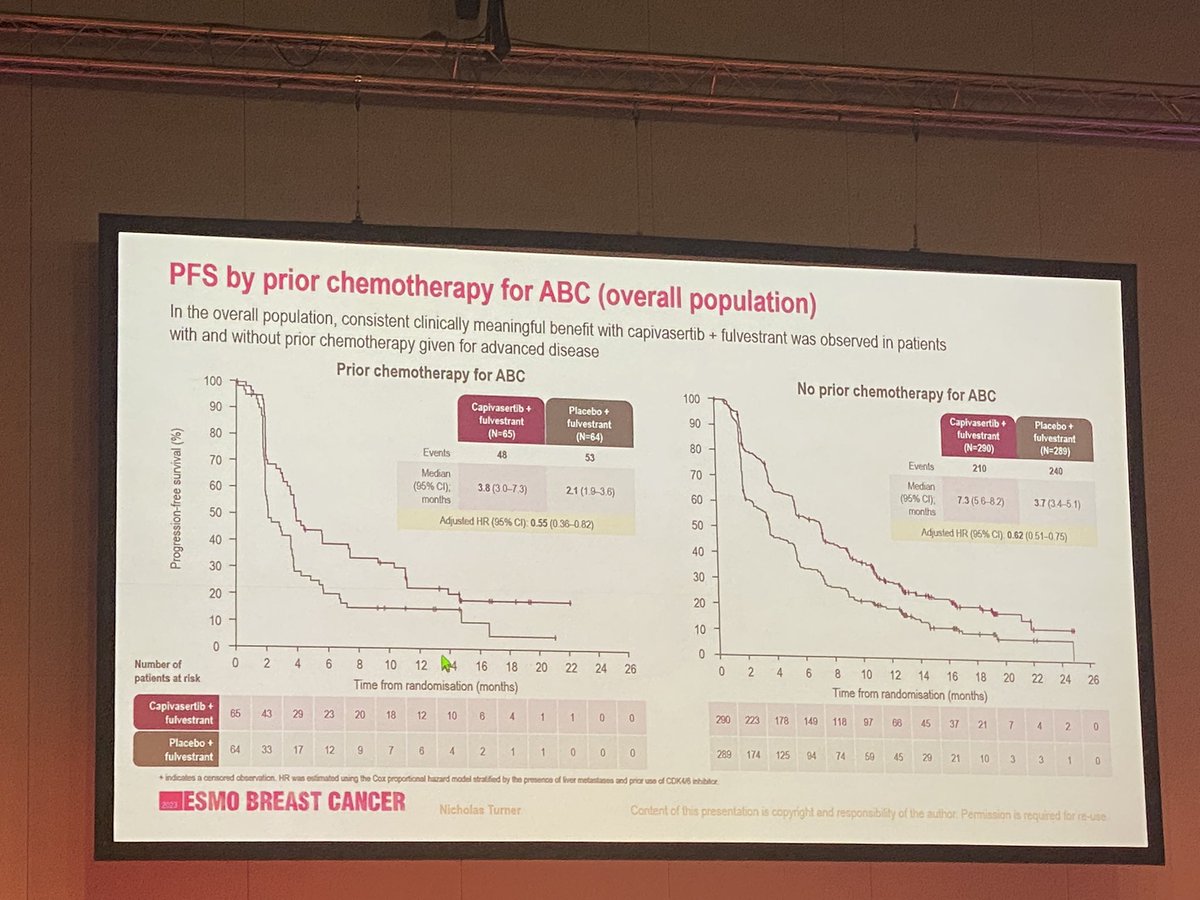

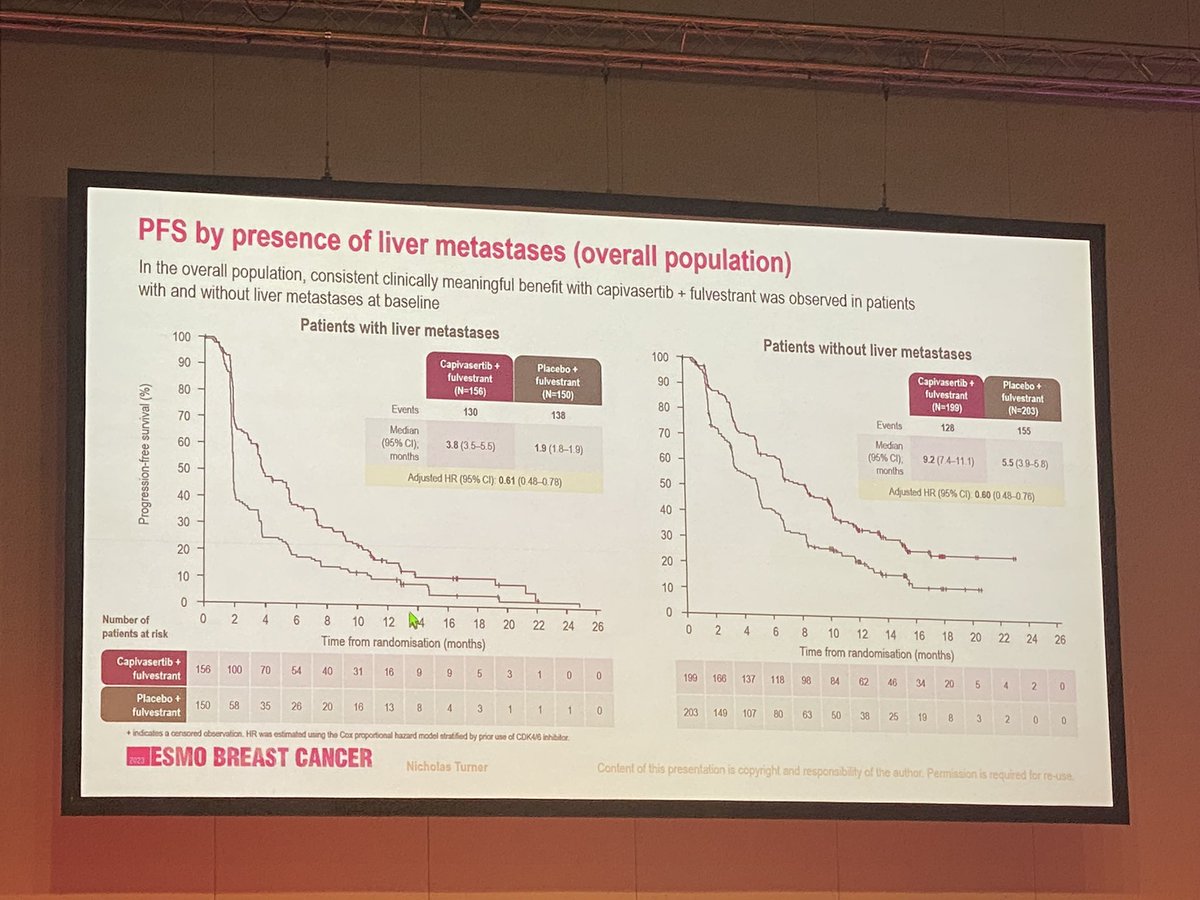

CAPItello291: Capivasertib fulvestrant improves PFS compared to fulvestrant alone in patients:

•prev tx w/CDK4/6 inhibitor

• prev tx w/ chemotherapy for mBC

•pts w/ liver mets

#ESMOBreast23

3

7

983

11 May 2023

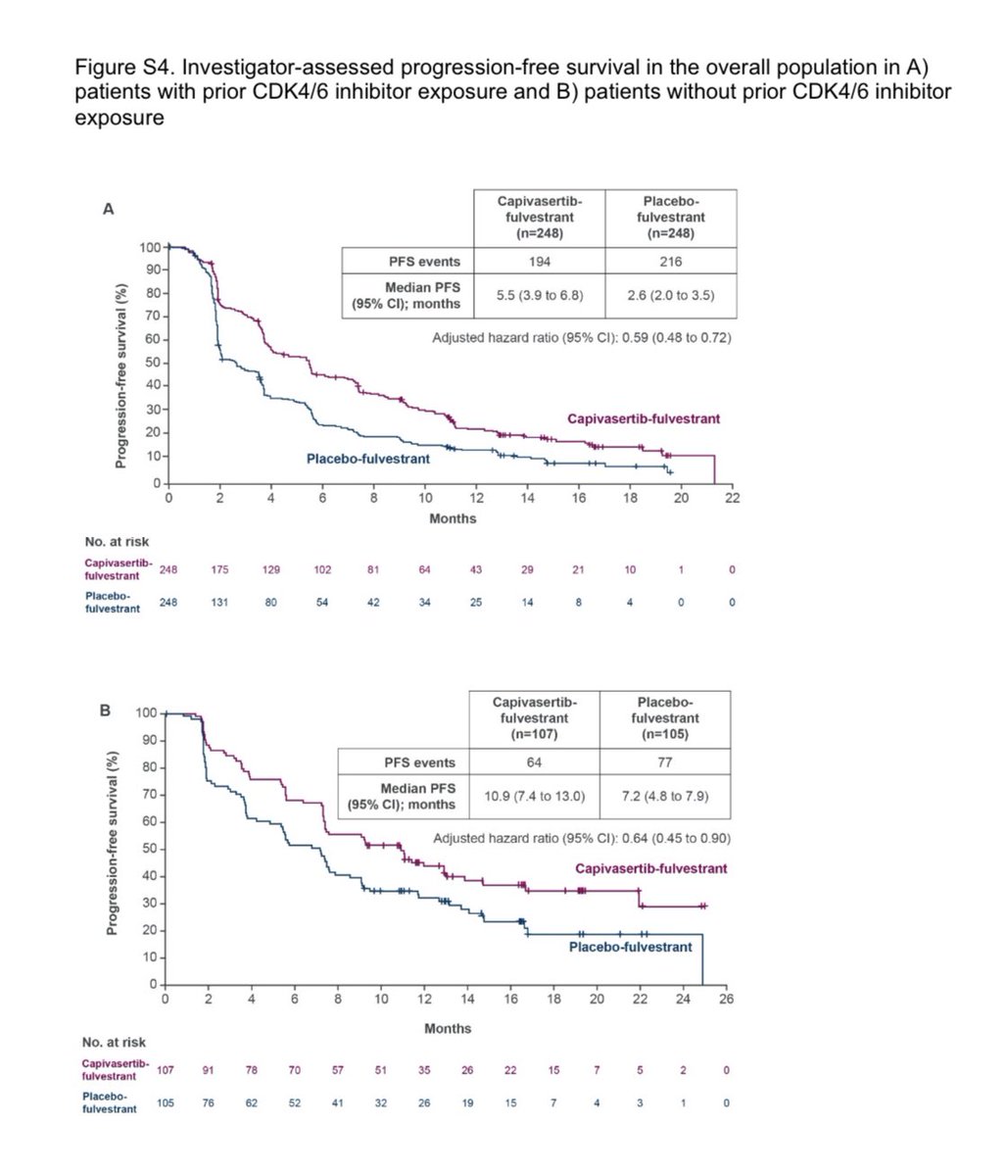

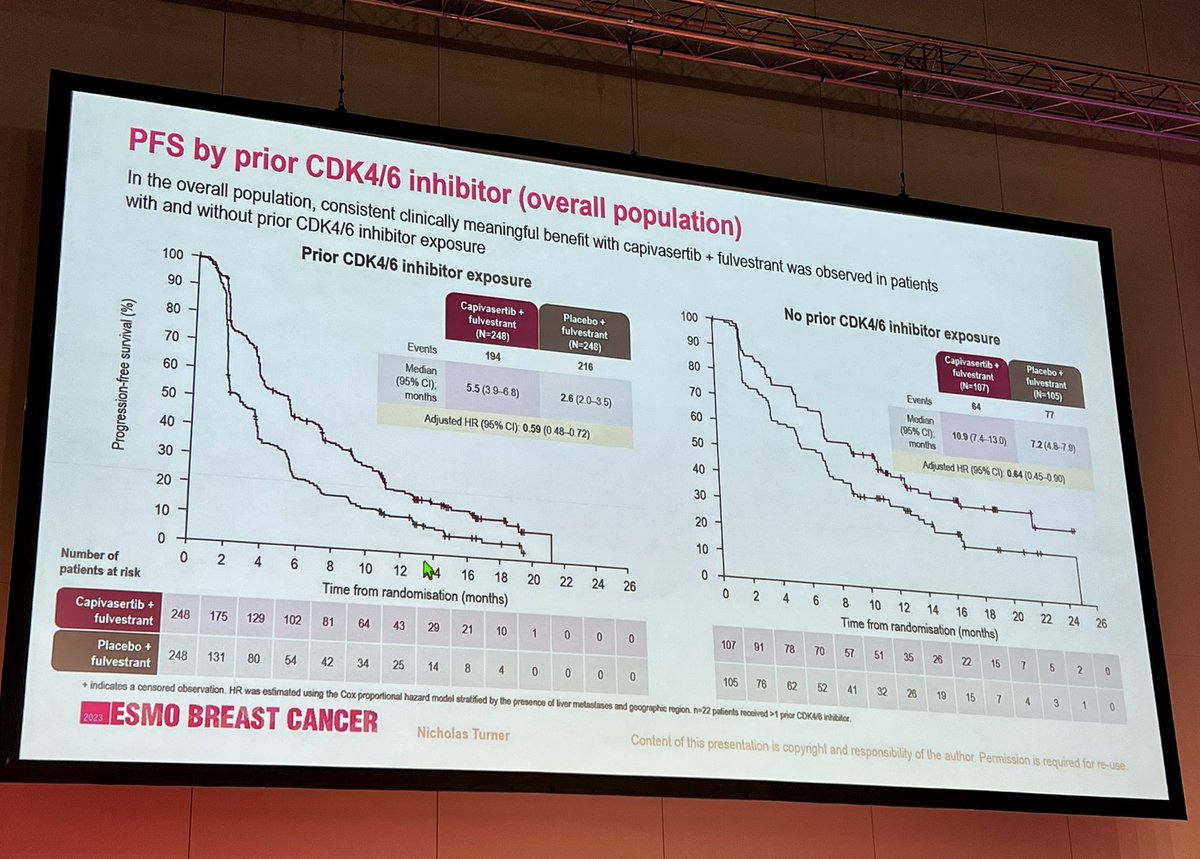

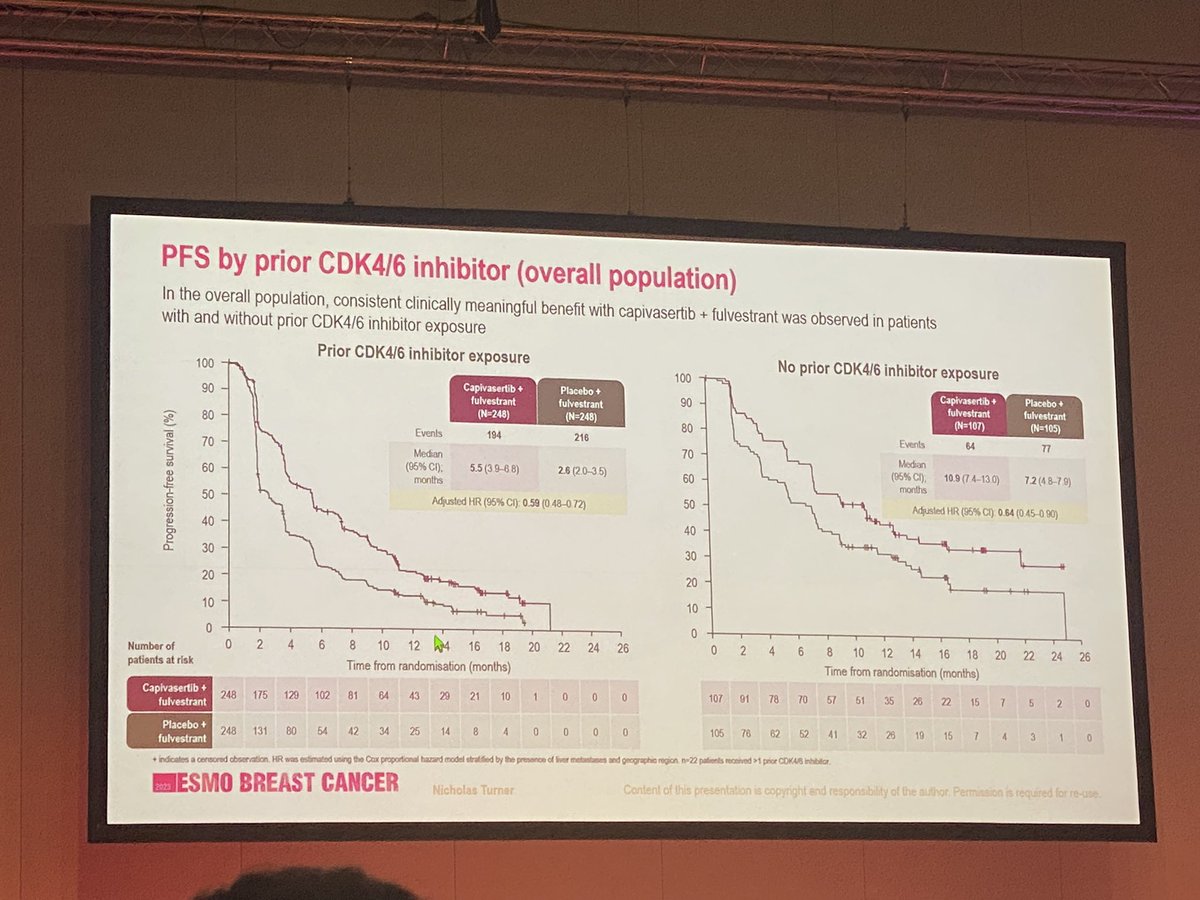

Nick Turner presents subgroup analyses from #CAPItello291. Interesting to look at outcomes in pts pretreated with CDK4/6-inhibitors: significant benefit of adding capi to fulvestrant, but smaller absolute numbers (5.5 vs 2.6 months) vs ITT. Numbers quite similar to #MAINTAIN.

1

6

28

3,552

11 May 2023

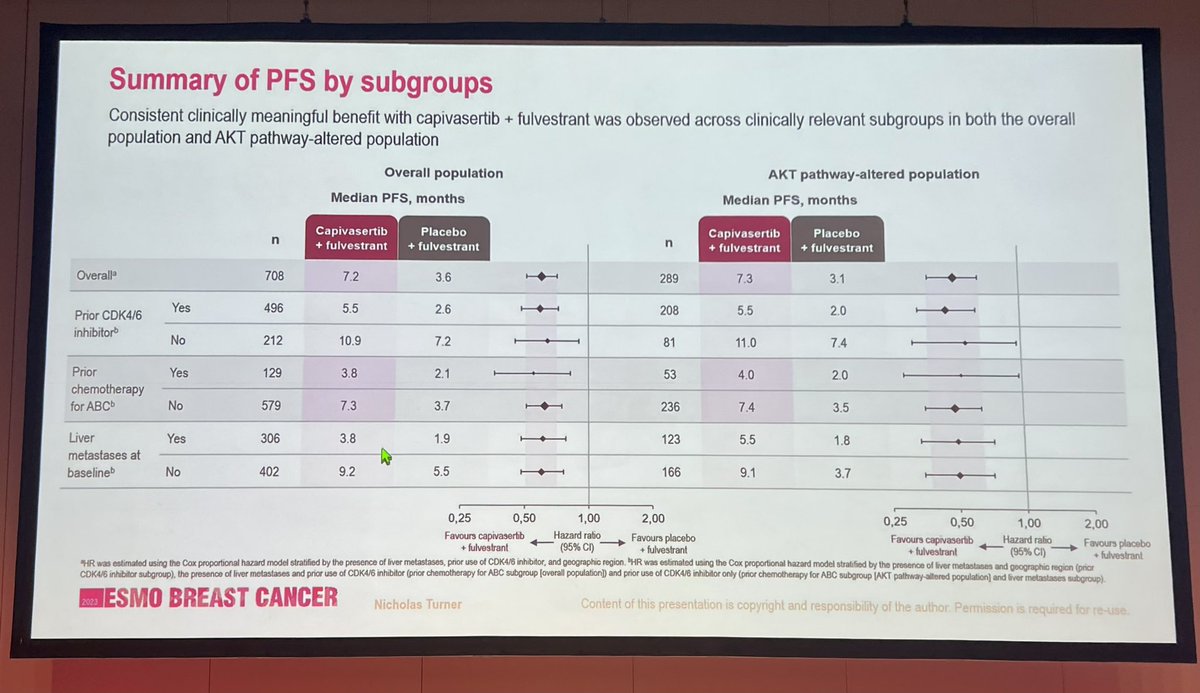

Further convincing efficacy data from the #CAPItello291 trial presented at #ESMObreast23: consistent PFS benefit across all subgroups of patients with endocrine resistant #BreastCancer receiving #capivasertib added to #fulvestrant

@myESMO @OncoAlert @ErikaHamilton9 #bcsm

12

34

2,538