18 Dec 2025

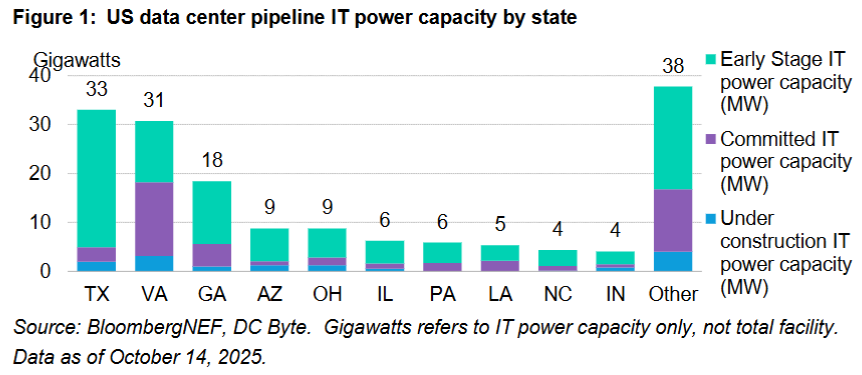

Comparing two different sources so this is not apples-to-apples but BNEF cites DCByte data to show state-by-state pipeline in GW vs. facilities. Overlap in top 10-20 states.

18 Dec 2025

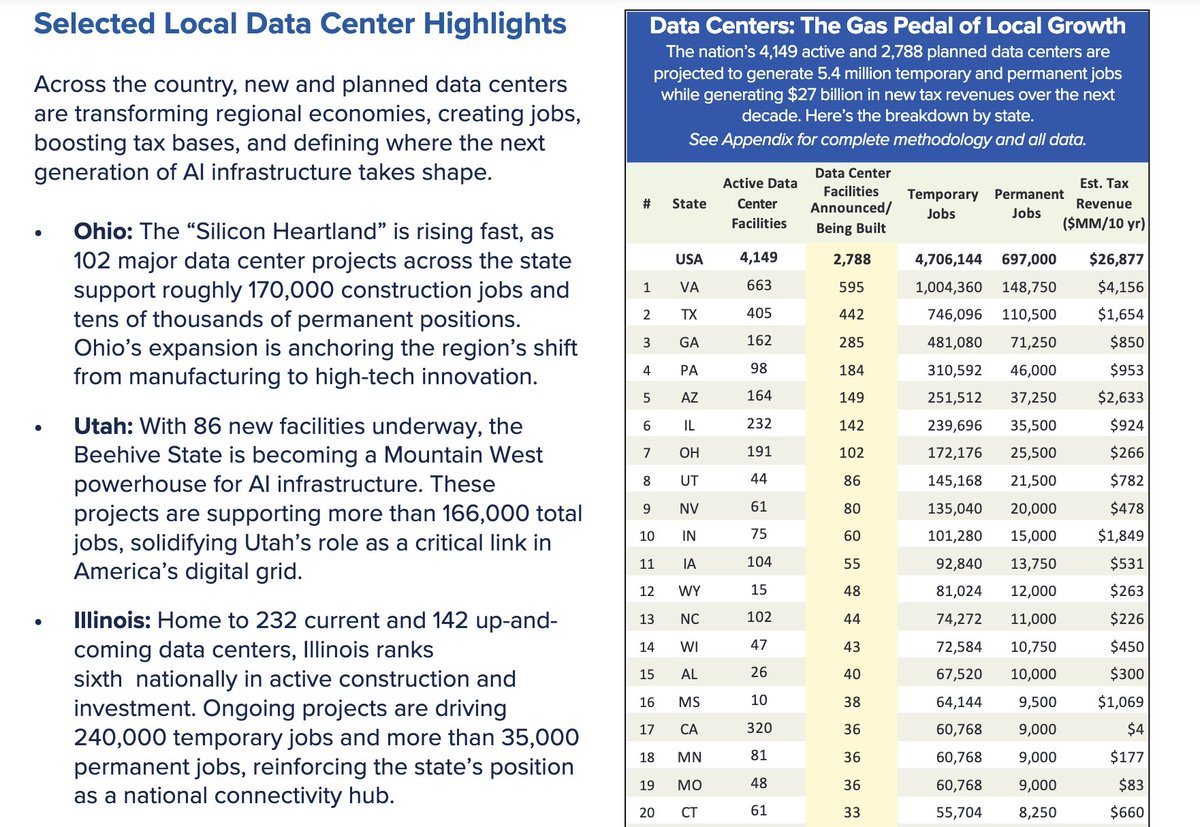

Not familiar with the company that published this report (American Edge) but they included this table in their report

Here's a snapshot of the top 20 states by active data center facilities facilities announced/being built per their figures

1

3

20

4,973

15 Dec 2025

Data Centres Are Now the World’s Most Competitive Infrastructure – And Demand Has Gone Exponential @DC_Byte

#DCByte #TwitterDailyBlog #DataStorage #DataCenter #ExecutiveSearch #CapitalFlows #EnergyPolicy

dcbyte.com/news-blogs/data-c…

4

2

27

4 Nov 2025

บริษัทหลักทรัพย์ เกียรตินาคินภัทร (KKPS) เผยผลวิเคราะห์ร่วมกับ DCByte ระบุว่า ประเทศไทยกำลังก้าวสู่การเป็นศูนย์กลางดาต้าเซ็นเตอร์สำคัญของเอเชียตะวันออกเฉียงใต้ โดยมีโครงการรวมกว่า 4.5–4.6 กิกะวัตต์

.

แรงขับเคลื่อน: เกิดจากกระแสการย้ายฐานลงทุนของผู้ให้บริการขนาดใหญ่ระดับโลก (Hyperscaler) หลังสิงคโปร์เริ่มจำกัดกำลังผลิต และยะโฮร์ (มาเลเซีย) เผชิญปัญหาพลังงาน ทำให้ไทยกลายเป็น "จุดหมายถัดไป" ที่สมดุลด้านศักยภาพและความเป็นไปได้เชิงปฏิบัติ

.

จุดแข็งและความได้เปรียบของไทย

โครงสร้างพื้นฐาน: ไทยมีความ มั่นคงด้านพลังงาน และระบบโครงสร้างพื้นฐานที่แข็งแกร่งกว่า

.

กระบวนการ: มี กระบวนการอนุญาตที่ยืดหยุ่นกว่า ในภูมิภาค

.

ทำเลศักยภาพ: การลงทุนขยายไปยัง พื้นที่ EEC (ฉะเชิงเทรา–ชลบุรี–ระยอง) ซึ่งเน้นรองรับโครงการขนาดใหญ่ (100 เมกะวัตต์ขึ้นไป) สำหรับงานด้าน AI และ Cloud Computing ส่วนกรุงเทพฯ เหมาะกับศูนย์ขนาดเล็กที่เน้นความเร็วสูง

.

การลงทุน Hyperscaler โลก

ตลาดไทยกำลังเปลี่ยนจากโมเดล Colocation สู่การลงทุนโดยตรงของ Hyperscaler ซึ่งครองส่วนแบ่งความต้องการมากกว่า 80%

.

ฝั่งตะวันตก: Amazon Web Services (AWS) เริ่มก่อสร้างแล้ว, Google ซื้อที่ดินเตรียมสร้างศูนย์, Microsoft ปรับกลยุทธ์เช่าพื้นที่ระยะสั้น

.

ฝั่งจีน: ByteDance เป็นผู้ใช้รายใหญ่ที่สุด, Alibaba และ Tencent ขยายบริการผ่านพันธมิตรในไทย

KKPS ย้ำว่า การลงทุนดาต้าเซ็นเตอร์คือ โครงสร้างพื้นฐานใหม่ของเศรษฐกิจดิจิทัล ที่จะขับเคลื่อนอุตสาหกรรมเทคโนโลยี พลังงาน และอสังหาริมทรัพย์ของประเทศ

.

#ดาต้าเซ็นเตอร์

#DataCenter

#อาเซียน

#เศรษฐกิจดิจิทัล

#KKP

#EEC

#โครงสร้างพื้นฐานดิจิทัล

#โพสต์ทูเดย์

#Posttoday

1

9

13

1,453

1 Nov 2025

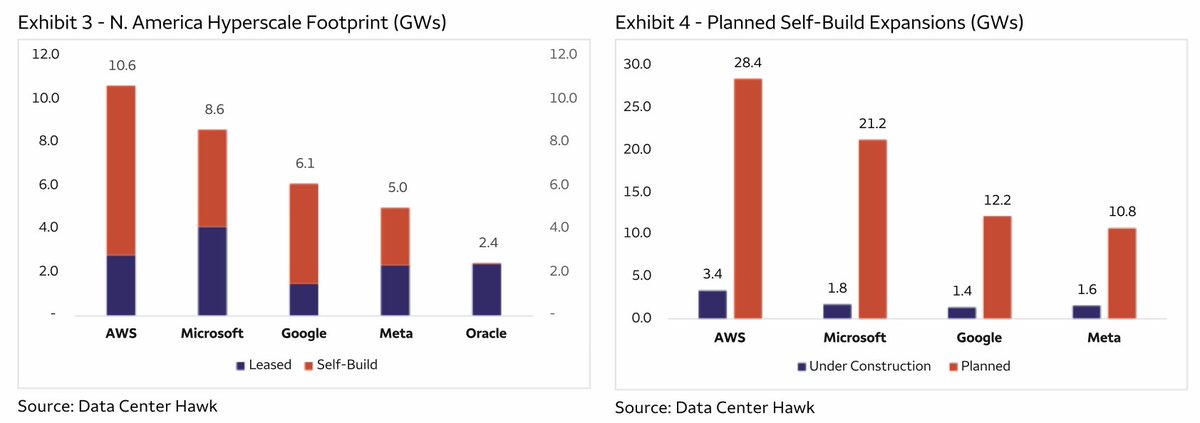

Woke up and thought let's do some quick maths & guesstimating for fun. Using rough approximations, it appears AMZN and MSFT are credibly bringing on 2 GWs/yr each over the next 1-2 years while META and GOOGL in the 1-2 GW/yr range. ORCL ambitions seem to be ~2 GWs/yr as well.

DatacenterHawk vs. DCByte (diff sources = diff methodologies) - Current Capacity:

-AMZN ~8 GW self-build vs. ~4.7 GW live

-MSFT ~4.4 GW self-build vs. ~3.3 GW live

-GOOGL~4.7 GW self-build vs. ~3.5 GW live

-META ~2.9 GW self-build vs. ~3.8 GW live

-If you include leased for DCH = AMZN-10.6 GW, MSFT-8.6 GW, GOOGL-6.1 GW, META-5.0 GW

-ORCL leases all their capacity today at ~2.5 GW

Under Construction (same two sources):

-AMZN ~3.4 GW vs. ~1.61 GW

-MSFT ~1.8 GW vs. ~1.72 GW

-GOOGL~1.4 GW vs. ~1.53 GW

-META - ~1.6 GW vs. ~2.17 GW

We know AMZN and MSFT are the largest and seem to also be the fastest. ORCL is attempting a rapid scale-up so will probably move aggressively.

-AMZN 3Q25: 3.8 GW added in the last 12 months. ≥1 GW more to be energized in Q4 CY25. Now double the power capacity they had in 2022 and on track to double again by 2027.

-MSFT 2Q 3Q25: 2 GW of new capacity over the past 12 months and will increase total AI capacity by over 80% this year and roughly double our total data-center footprint over the next two years.

-GOOGL: Joint release with Anthropic states Google Cloud will provide the AI start-up “well over a gigawatt of capacity coming online in 2026"

-META: bring online almost 1 GW of capacity this year (CY-2025) and is building a 2 GW (and potentially larger) AI data center.

>ORCL 3Q25: management said contracted power capacity will “double this calendar year and triple by the end of next fiscal year" 4.5 GW deal with OpenAI

>So if we assume AMZN has 5-11GW and plan to double next years implies ~2.5-5.5 GW/yr.

>MSFT at ~3-9GW and plan to double next two years implies 1.5-4.5 GW/yr.

>Checks out as faster to GOOGL and Meta which appear to be in the 1-2 GW/yr range based on the above data points?

>ORCL maybe bringing online ~5 GW to go from 2.5 to 7.5 GW from 2025-YE26. That is consistent with the 4.5 GW partnership with OAI but expected to be over several years. If you count that as 1yr, seems insanely fast. I'm thinking it's more likely in the ~2.5 GW/yr conversation too which is in-line with the other fastest in market scalers.

Sense check: Bain has 16 GW hyperscale self-build 13GW hyperscale co-lo as of 2024. This moves to 38 GW and 23 GW, respectively in 2027. So 22 GW self-build for hyperscalers, call it 11 GW/yr. For sake of convo let's say AMZN - 4-5 GW, MSFT - 2-3 GW, ORCL - 2 GW, GOOGL - 1-2 GW, META 1-2 GW = ~10-14 GW per year. Generally in-line.

12

38

298

89,168

29 Oct 2025

'KKP' ชี้ไทยขึ้นแท่น 'Data Center Hub' แห่งอาเซียน พลังงานมั่นคง–โครงสร้างพื้นฐานหนาแน่น ดึงยักษ์เทคทั่วโลกลงทุน

บริษัทหลักทรัพย์ เกียรตินาคินภัทร จำกัด (มหาชน) (KKPS) เปิดเผย ผลการพูดคุยกับบริษัทวิจัยโครงสร้างพื้นฐานดิจิทัลระดับโลก DCByte พบว่า ประเทศไทยกำลังก้าวขึ้นเป็นหนึ่งในศูนย์กลางดาต้าเซ็นเตอร์สำคัญของเอเชียตะวันออกเฉียงใต้ จากกระแสการย้ายฐานการลงทุนของผู้ให้บริการขนาดใหญ่ (Hyperscaler) จากสิงคโปร์และยะโฮร์ ประเทศมาเลเซีย เข้ามาลงทุนในไทยเพิ่มขึ้นอย่างมีนัยสำคัญ

ปัจจุบันประเทศไทยมีโครงการดาต้าเซ็นเตอร์รวมราว 4.5–4.6 กิกะวัตต์ ขณะที่ตลาดมาเลเซียอยู่ที่ประมาณ 8–9 กิกะวัตต์ (โดยยะโฮร์เพียงแห่งเดียวคิดเป็นกว่า 5 กิกะวัตต์) ส่วนสิงคโปร์มีตลาดขนาดเล็กกว่า 2 กิกะวัตต์ ซึ่งสะท้อนว่าไทยเริ่มขึ้นมาเป็น “จุดหมายถัดไป” ของการขยายดาต้าเซ็นเตอร์ในภูมิภาค

📌 จุดแข็งของไทยเหนือประเทศเพื่อนบ้าน

• สิงคโปร์จำกัดการเพิ่มกำลังผลิตใหม่ ขณะที่ยะโฮร์เริ่มเผชิญข้อจำกัดด้านพลังงานและทรัพยากร ส่งผลให้ผู้ประกอบการระดับโลกมองหาแหล่งลงทุนใหม่ที่มีความพร้อม ซึ่งประเทศไทยโดดเด่นในหลายด้าน ได้แก่

• ความมั่นคงด้านพลังงานและระบบโครงสร้างพื้นฐานที่หนาแน่นกว่า

• กระบวนการอนุญาตที่ยืดหยุ่น

• ความหนาแน่นของประชากรต่ำกว่า ทำให้เหมาะต่อการตั้งดาต้าเซ็นเตอร์ขนาดใหญ่

ในขณะที่ประเทศอื่นในภูมิภาคยังมีข้อจำกัด เช่น ฟิลิปปินส์เผชิญความเสี่ยงจากภัยธรรมชาติ อินโดนีเซียมีต้นทุนโครงสร้างพื้นฐานสูง และเวียดนามยังมีกฎระเบียบซับซ้อน ไทยจึงถือเป็น “ตลาดที่สมดุลระหว่างศักยภาพและความเป็นไปได้เชิงปฏิบัติ” แม้ยังต้องพัฒนาในด้านมาตรฐานอุตสาหกรรม ความโปร่งใส และบุคลากรทักษะสูง

อ่าน: bangkokbiznews.com/finance/s…

#กรุงเทพธุรกิจ #กรุงเทพธุรกิจEconomic

3

3

1,378

20 Oct 2025

What sources are you using here @BenBajarin?

I've seen a lot of estimates in this realm but it's hard to track b/c:

>Different sources have different data (e.g., DCByte, SemiAnalysis, Datacenterhawk)

>So much building/leasing going on it's hard to attribute the actual sites/projects to the ultimate end user that "has the MWs" (e.g., MSFT call said they brought on 2GW of power last year but not a lot of sources have that captured)

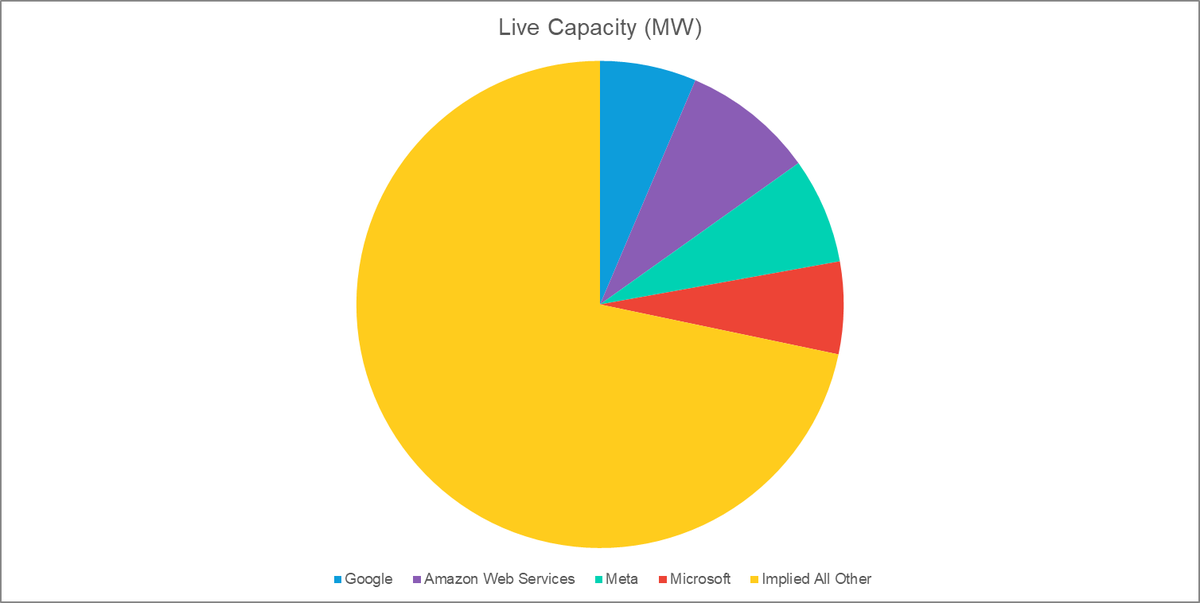

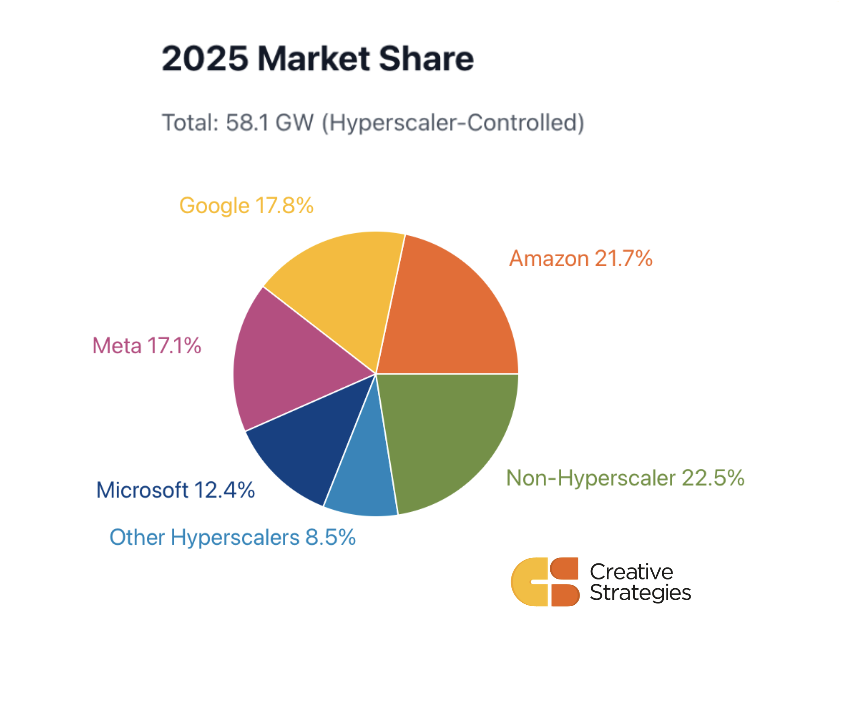

BNEF uses DCByte and has a global GW figure of ~53-54GW which is close enough for these purposes but the pie chart of hyperscalers vs. all other looks a lot different so not sure how to gauge the quality of the dataset. Few cuts included here.

3rd party estimates (that I don't have access to underlying detail) typically converge on ~50% US and hyperscalers being 50-60% of capacity so it's hard to reconcile.

20 Oct 2025

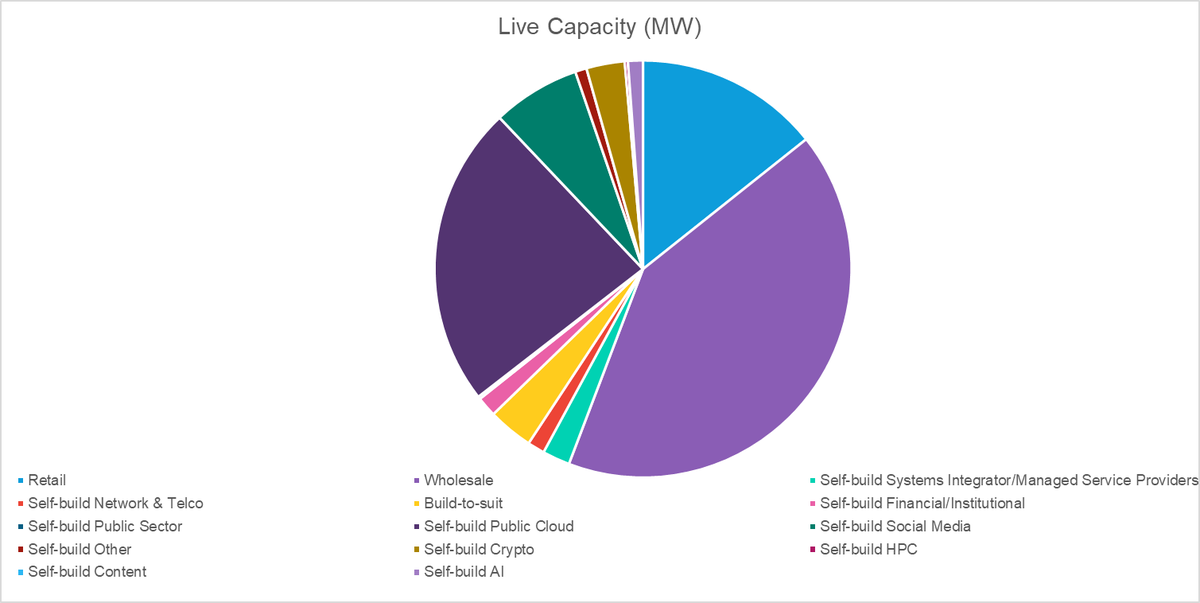

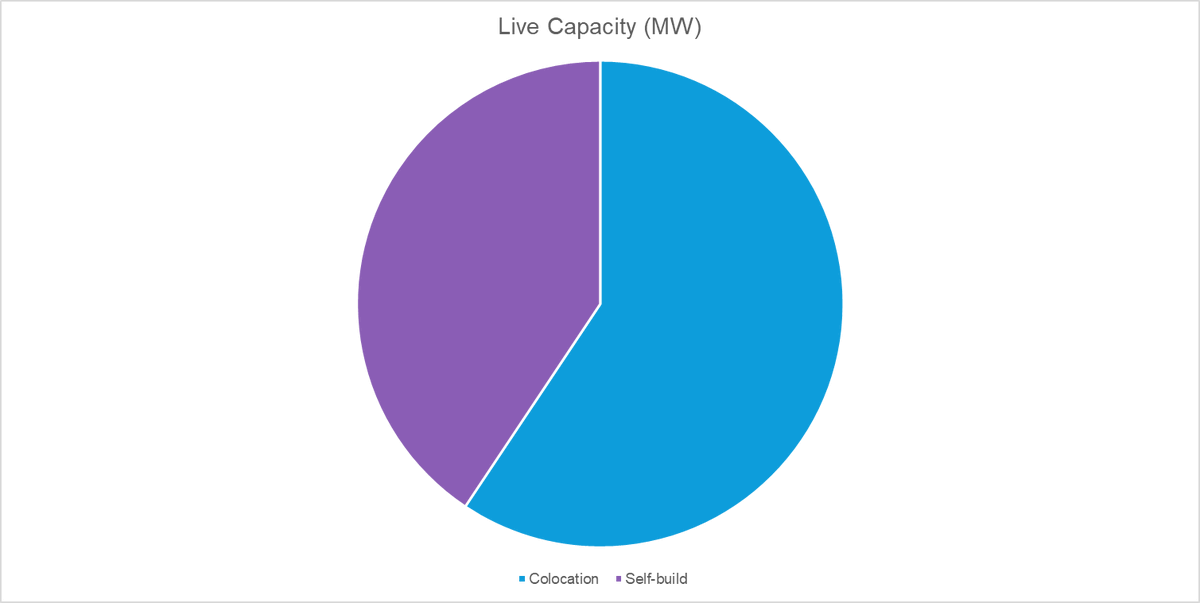

In my quest to keep tracking the GW, still a work in progress trying to seperate retail/wholesale/hyperscale, but directionally right in terms of who has the most and who needs more.

Interesting that Microsoft likely needs to be the most aggressive in securing capacity.

1

6

4,331

4 Aug 2025

Anyone know what the best source is to track granular data center capacity by company/cloud (public or paywall)?

E.g., I want to track specifically what MSFT, AMZN, META, ORCL, GOOGL, CRWV, etc. have brought online in recent years and tie it out to what they've said on calls (e.g., MSFT stood up 2GW of capacity last year alone per call) and have in the pipeline. If you have access to a dataset or want to trade notes, DMs are open.

I know popular sources include. What does the best dataset cost?

-datacenterHawk @datacenterhawk

-DCByte @DC_Byte

-SemiAnalysis @SemiAnalysis_

-BloombergNEF @BloombergNEF

If you had to point to one source that was very accurate and timely, what would people go to?

10

5

75

9,886

London Tech Trivia Time! 🧠 In 1869, which London-based telecom company launched the world's first public telegraph service? 📷 Test your knowledge! Unlock insights about London's data centre scene in our Market Spotlight report!📷 bit.ly/3rr3cLq #MarketSpotlight #DCByte

1

4

64

🔍 Meet Rupert Duckworth! The man behind our latest Market Spotlight - London! Rupert's passion for connecting with people and traveling complements his focus on the London market, the largest market in EMEA. Dive deeper into the Spotlight: bit.ly/3rCzCTj

#DCByte

1

3

25

🎉 Trivia Answer Revealed! The North African country investing in the development of the technology hub, Technopolis Rabat, is Morocco! Discover more about the growth of the digital economy in our African Market Spotlight report: bit.ly/46WmaK8 #TriviaAnswer #DCByte

2

28

Tokyo, here we come! 🇯🇵 DC Byte is thrilled to attend the Japan Cloud & Datacenter Convention 2023. Meet our onsite representatives, James and Jingwen. Drop us a message to schedule a meeting. Can't make it to Japan? Our next stop is Singapore! #Networking #DCByte

1

2

53

DC Byte Founder and CEO Ed Galvin gives his predictions on the #datacenter #markets in 2021 and beyond in today's edition of DCD News. bit.ly/2J9fbqY

#dcbyte #research #Insights

2

#DataCenter #USA announcement for today. @CoreSite opening its newest VA3 bit.ly/32s3EHS facility In Reston Virginia. The expansion will add over 660,000 sq ft of #colocation space to the existing Reston Campus, currently consisting of VA1 and VA2.

#dcbyte

3

Amazing news @digitalrealty provisioned renewable energy to support its growing #datacenter footprint in Northern #Virginia with the collaboration of @ENGIEServicesUS supplying 107,000 additional megawatt-hours of renewable solar power annually.

#dcbyte #GreenEnergy

2

4

More to announce for the #DataCenter market #Munich. @DECIX increased its presence outside Frankfurt by expanding its presence at @EdgeConneX's edge data center in Munich.

#datacenters #dcbyte

3

5

A warm welcome to our newest association member, the #Finnishdatacenterforum. With almost 100 members comprising DC operators, developers, suppliers and more, FDCF has influence well beyond the Finnish borders! bit.ly/2ml73bN.

#datacenters #dcbyte

2

A #dcbyte news update:

1. @digitalrealty announces #datacentres in Seoul & Frankfurt bit.ly/2Ks5d0W

2. @ZayoGroup agrees to acquisition bit.ly/2YIz7mL

3. @Microsoft's #datacenter in AZ to run on #renewables bit.ly/2YE79wo

1

2

An afternoon stroll for the #DCByte team in #Monaco. Come say hello at Stand 2 tomorrow once @DatacloudGlobal kicks off tomorrow morning, we’ll show you how we’re revolutionising the sector!

1

Attending @DatacloudGlobal in #Monaco this week? Head to Stand 2 to meet the #DCByte team. See you there! #DataCentres #Edge #IoT #5G

3

Heading to @DatacloudGlobal and want to learn more about #dcbyte? Look out for our stand or get in touch to arrange a meeting! #datacenters #datacloudcongress #monaco

3

3