17 May 2025

🌀Most investors are still using outdated methods to build portfolios.

But pros? They're simulating 10,000 portfolios in Python. Here's how you can too. 👇

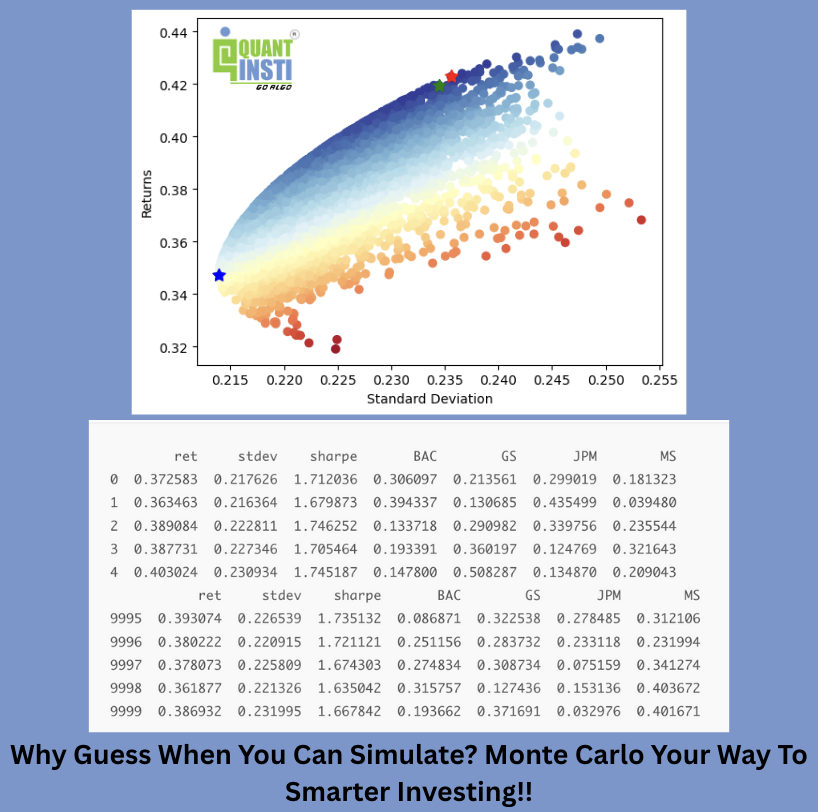

📈 Portfolio Optimization with Monte Carlo Simulation — step-by-step, with real data.

Whether you're a quant, finance student, trader, or Python enthusiast…

This post is your roadmap to smarter investing using data science and probabilistic modelling.

💡 What’s inside the blog?

🔹 What is Portfolio Optimization?

🔹 Objective-driven approaches:

— Maximize Sharpe Ratio (Tangency Portfolio)

— Minimize Portfolio Variance

— Maximize Return at a Fixed Level of Risk

🔹 Data used: Stock prices from BAC, JPM, GS, MS (2024)

🔹 Annualized return & risk calculation

🔹 10,000 Monte Carlo simulations in Python

🔹 Sharpe-optimized portfolios using real data

🔹 Beautiful visualizations to backtest results

🧠 Why it matters:

In 2025, alpha isn’t found in gut feeling—it’s in models that adapt, simulate, and evolve.

Monte Carlo helps you explore the entire opportunity set, not just a handful of guesses.

⚙️ Tools used: yFinance, NumPy, Pandas, Matplotlib — beginner-friendly, real-world results.

📊 Learn how to:

✅ Use Python for smarter investing

✅ Rebalance assets based on simulated performance

✅ Build a portfolio that’s actually built for risk-adjusted returns

📚 Full article complete code:

👉 blog.quantinsti.com/portfoli…

💬 What’s YOUR take on Monte Carlo in portfolio management?

Tried it? Struggled with it? Curious to apply it?

Let’s share insights below 🔽

#PortfolioOptimization #MonteCarloSimulation #PythonForFinance #QuantTrading #FinancialModelling #SharpeRatio #AssetAllocation #InvestmentStrategy #Backtesting #DataScienceInFinance #RiskManagement #AlgorithmicTrading #QuantResearch #QuantitativeFinance #StockMarketStrategy #PythonInvesting #TradingWithPython

6

385

12 May 2025

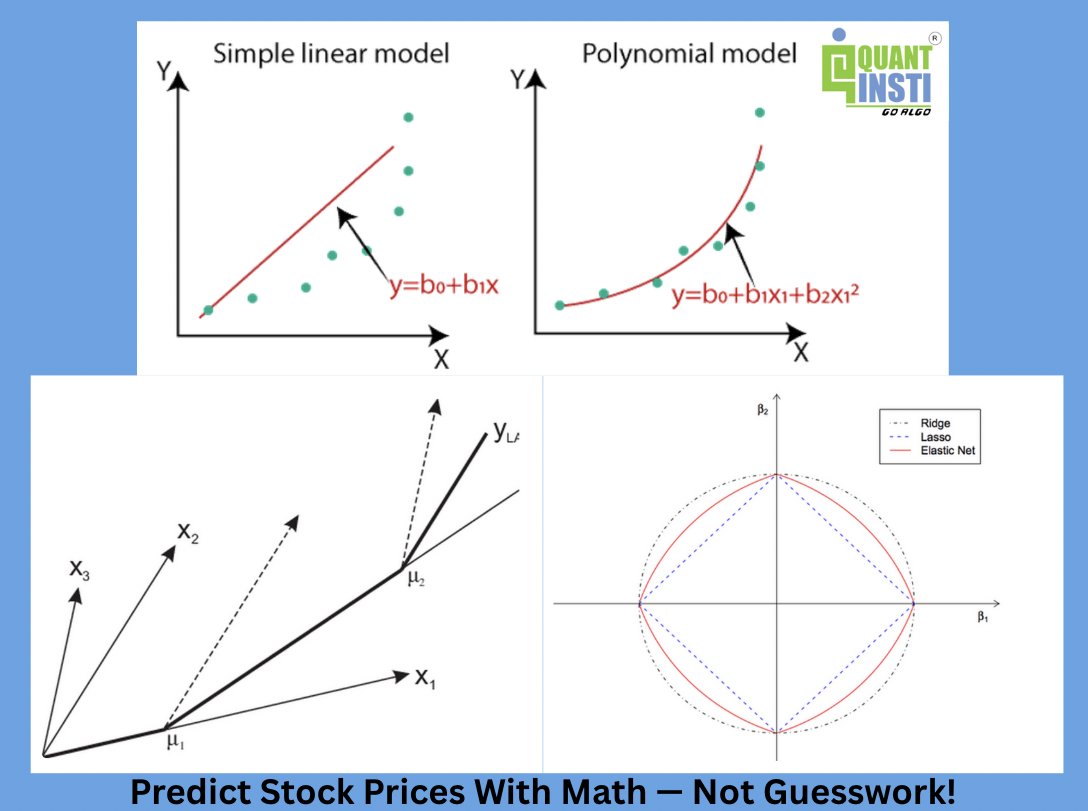

🧠 Want to predict stock prices with math — not guesswork?

Most traders stop at linear regression...

But markets aren't linear — and neither should your models be.

In our latest blog, we break down the real tools quants use to detect trends and forecast smarter.

🚀 Inside Part 1: Advanced Regression Models in Finance

📌 Go beyond basics with:

✅ Polynomial Regression – for capturing non-linear price curves

✅ Ridge Regression – to solve multicollinearity in financial data

✅ Real-world use cases in trading portfolio modeling

Whether you're a beginner or a quant-in-training, this is a must-read.

📖 Read now 👉 blog.quantinsti.com/advanced…

💬 Have you tried any of these regression techniques in your strategies? Share below 👇

🎯 Want to master algorithmic trading with confidence?

Learn how to build, test, and deploy data-driven trading strategies using Python and industry-grade tools.

🔗 quantinsti.com/epat

🚀 With the EPAT® Programme, you’ll gain expertise in:

✅ Algorithmic & quantitative trading techniques

✅ Python, machine learning & financial data analysis

✅ Live strategy execution, risk management & portfolio design

💼 Designed by top industry professionals. Trusted by traders, analysts, and quants around the globe.

If you're serious about becoming a skilled algo trader, EPAT® is your launchpad.

#MachineLearningInFinance #QuantTrading #RegressionAnalysis #PolynomialRegression #RidgeRegression #FinanceBlog #AlgoTrading #DataScienceInFinance #TradingModels #LearnQuant #AIinFinance

2

302

26 Apr 2025

🔍 What Are Autocovariance and Autocorrelation in Time Series?

If you're working with financial time series data, understanding autocovariance and autocorrelation is crucial. Let’s break them down in simple terms. 👇

📊 Covariance measures how two different variables move together.

🔁 Autocovariance does the same—but with a twist. It measures how a variable (say, stock returns) correlates with its own past values. For example, the covariance of Microsoft’s return today with its return yesterday.

🧠 Think of it like this:

Cov(X, Y) ➡️ Two variables

Cov(Xₜ, Xₜ₋ₛ) ➡️ Same variable at different time points (this is autocovariance)

📈 Autocorrelation, also called serial correlation, is the normalized version of autocovariance. It tells you how strongly today’s return is related to yesterday’s (or any lag) on a scale from -1 to 1.

🔗 Autocorrelation at lag 0 = 1 (makes sense—any series is perfectly correlated with itself at the same time).

📉 In practice:

Negative autocorrelation? Mean-reverting asset.

Positive autocorrelation? Trending asset.

✅ Why does this matter?

Autocovariance and autocorrelation are fundamental in:

📊 Time series modeling (ARMA, ARIMA, etc.)

⚙️ Quant strategy development

📉 Volatility forecasting

👉 Check out this blog on Autocorrelation and autocovariance to find out more:

blog.quantinsti.com/autocorr…

🎯 Want to master algorithmic trading with confidence?

Learn how to build, test, and deploy data-driven trading strategies using Python and industry-grade tools.

🔗 quantinsti.com/epat

🚀 With the EPAT® Programme, you’ll gain expertise in:

✅ Algorithmic & quantitative trading techniques

✅ Python, machine learning & financial data analysis

✅ Live strategy execution, risk management & portfolio design

💼 Designed by top industry professionals. Trusted by traders, analysts, and quants around the globe.

If you're serious about becoming a skilled algo trader, EPAT® is your launchpad.

#QuantFinance #TimeSeries #TradingStrategies #Autocovariance #Autocorrelation #FinanceTips #QuantAnalysis #DataScienceInFinance

3

262

13 Apr 2022

Bu sabah @sibirbil hocamı dinliyorum gözlerim kapalı (sıkıntıdan değil zevkten)

#dsfc #datascienceinfinance

1

1

22

Bravo à @Sebastien_Jehan pour le #meetup #datascienceinfinance. Super talk de Christophe et @laurentgrangeau à propos de @ProjectJupyter !

4

4